Paper-Based Blister And Foil-Free Blister Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

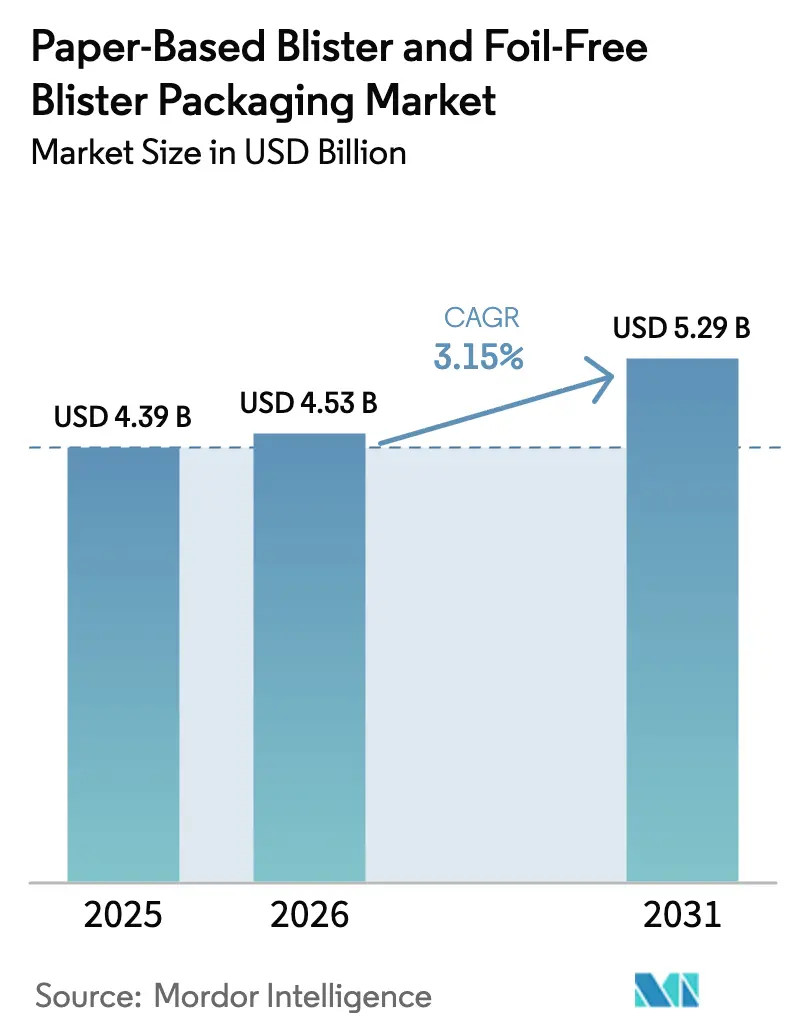

| Market Size (2026) | USD 4.53 Billion |

| Market Size (2031) | USD 5.29 Billion |

| Growth Rate (2026 - 2031) | 3.15% CAGR |

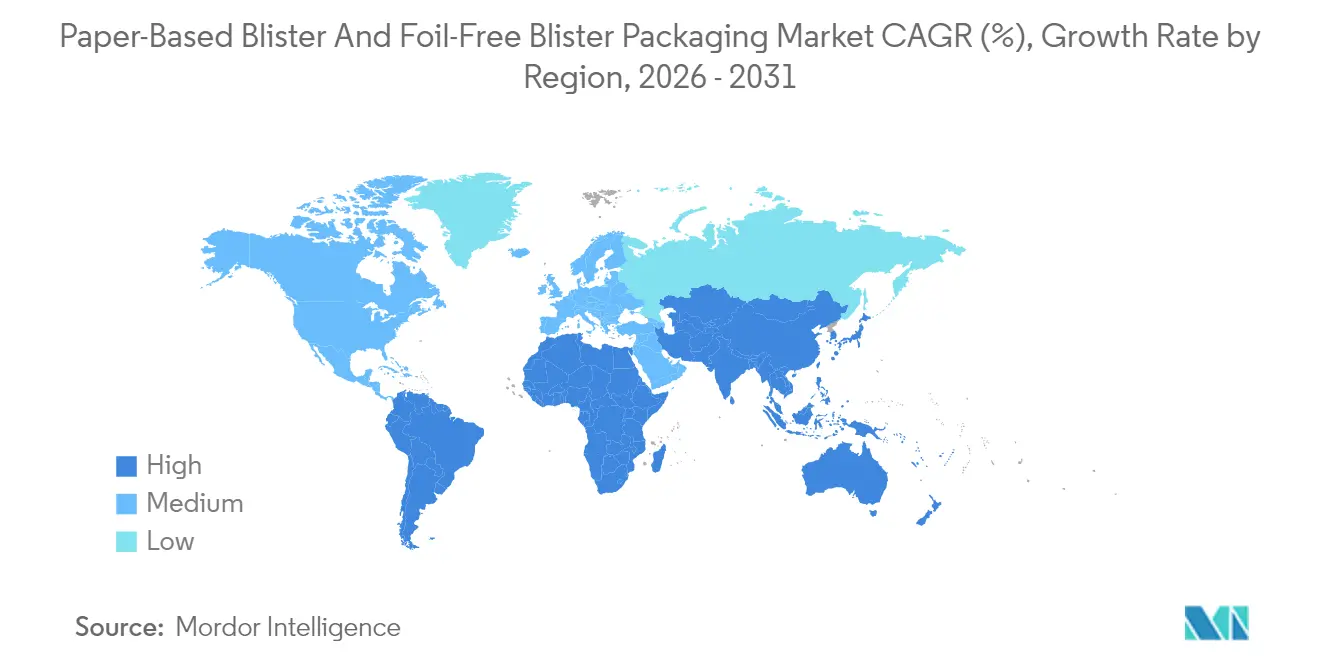

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Paper-Based Blister And Foil-Free Blister Packaging Market Analysis by Mordor Intelligence

Paper-based blister and foil-free blister packaging market size in 2026 is estimated at USD 4.53 billion, growing from 2025 value of USD 4.39 billion with 2031 projections showing USD 5.29 billion, growing at 3.15% CAGR over 2026-2031. Demand gains stem from rapid regulatory alignment around recyclability, corporate decarbonization targets that favor fiber substrates, and cost parity achieved by thermo-formable barrier papers. Steady investments in nanocellulose coatings, coupled with proven unit-dose stability data, are shifting the competitive balance away from PVC-aluminum systems toward fiber-based alternatives. The Asia-Pacific region retains volume leadership, while South America registers the fastest growth, driven by expanded extended producer responsibility frameworks and rising generic pharmaceutical output. Competitive strategies focus on vertical integration, which secures pulp supply and proprietary barrier formulations, thereby enabling price resilience amid fluctuating fiber costs.

Key Report Takeaways

- By material type, Solid Bleached Sulphate paperboard captured 37.68% of the Paper-Based Blister and Foil-Free Blister Packaging Market share in 2025.

- By form, Paper-Based Blister and Foil-Free Blister Packaging Market size for pre-die-cut sheets is projected to grow at 5.08% CAGR between 2026–2031.

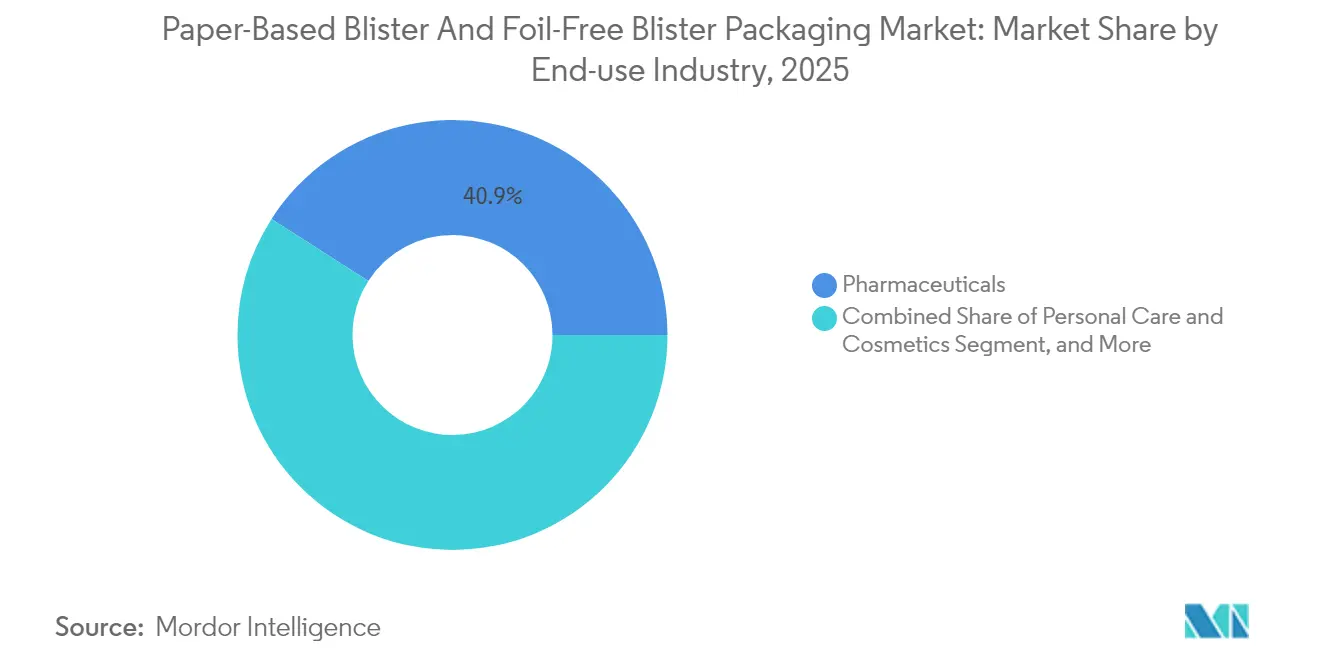

- By end-use industry, pharmaceuticals captured 40.92% of the Paper-Based Blister and Foil-Free Blister Packaging Market share in 2025.

- By geography, Paper-Based Blister and Foil-Free Blister Packaging Market size in South America is projected to grow at 6.31% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Paper-Based Blister And Foil-Free Blister Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising single-use-plastic bans and EPR regulations | +0.8% | Global, led by European Union and California | Medium term (2-4 years) |

| Brand owners’ net-zero commitments | +0.6% | North America and European Union, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Cost parity from scaling of thermo-formable barrier papers | +0.9% | Global, production centered in Northern Europe | Short term (≤ 2 years) |

| Retailer “paper shelf-ready” mandates | +0.4% | North America and Western Europe | Medium term (2-4 years) |

| Pharmaceutical unit-dose shift toward curb-side-recyclable packs | +0.7% | Asia-Pacific core, spill-over to Middle East and Africa and South America | Medium term (2-4 years) |

| Consumer perception premium for paper aesthetics | +0.3% | Global, strongest in premium consumer segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Single-Use-Plastic Bans and Extended Producer Responsibility Regulations

Thirty-five nations now enforce extended producer responsibility fees that escalate the total system cost of plastic-heavy formats, while the European Union’s Packaging and Packaging Waste Regulation mandates 65% recycled content by 2030 and universal recyclability by 2035. California’s SB 54 imposes a 25% reduction target for plastic by 2032, reshaping the cost structures for over-the-counter medicines. Pharmaceutical firms are accelerating their transitions to fiber blisters, which integrate seamlessly with paper recovery streams and avoid costly multi-material separation. Accelerated timelines compress innovation cycles, favoring suppliers with turnkey barrier-coated papers that already meet moisture and oxygen specifications. Parallel PFAS restrictions eliminate incumbent fluoropolymer coatings, further tipping adoption toward water-based solutions compatible with paper substrates.

Brand Owners’ Net-Zero Commitments Accelerating Fiber Adoption

More than USD 43 trillion in enterprise value is now tied to explicit net-zero roadmaps that include packaging decarbonization milestones. Unilever has pledged a 50% reduction in virgin plastic by 2030, while Walmart’s Project Gigaton reports a cumulative 1 billion-ton supply-chain emission reduction, with packaging optimization contributing nearly one-quarter of the total.[1]Walmart, “2024 Environmental, Social and Governance Report,” corporate.walmart.com These targets embed fiber packaging preferences into procurement scorecards, amplifying supplier competition on lifecycle metrics rather than unit cost alone. Executive remuneration linked to ESG outcomes sustains investment even during macroeconomic downturns, ensuring that capacity expansions for barrier-coated paperboard receive priority capital allocation.

Cost Parity from Scaling of Thermo-Formable Barrier Papers

Since 2024, EUR 2.3 billion (USD 2.5 billion) in European mill upgrades has delivered the learning-curve gains that align the cost per 1,000 dose cavities of barrier paper with PVC-aluminum packs. Stora Enso’s Performa Nova platform secures 18-month stability for solid doses while eliminating the need for foil. Mondi’s BarrierPack Recyclable now achieves sub-0.1 cc/m²/day oxygen ingress at a 15% lower cradle-to-grave cost once landfill fees and producer levies are factored. These breakthroughs dismantle the historic cost barrier, empowering procurement managers to adopt fiber solutions without compromising margins.

Pharmaceutical Unit-Dose Format Shift Toward Curb-Side-Recyclable Packs

Japan’s Pharmaceutical and Medical Device Agency guidance accepted paper blisters for stability-tested formulations in 2025, removing a regulatory hurdle for regional generic producers. China’s tightened import restrictions on contaminated plastics encourage domestic manufacturers to adopt paper-based packaging that is compatible with municipal recycling infrastructure. Competitive differentiation intensifies as brands position fiber packaging as a quality cue that reflects environmental stewardship, supporting modest price premiums even in cost-sensitive markets. Municipal waste systems that already capture mixed paper achieve higher recovery yields than those sorting multilayer plastics, reinforcing the economic logic of fiber formats.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Moisture-barrier limitations in tropical distribution chains | -0.5% | Southeast Asia, Sub-Saharan Africa, Central America | Medium term (2-4 years) |

| Line-speed penalties (15-25% slower vs PVC-al) | -0.4% | Global, especially large-scale pharmaceutical lines | Short term (≤ 2 years) |

| Capital-intensive retrofits of legacy thermoforms | -0.3% | North America and Europe have mature facilities | Long term (≥ 4 years) |

| Supply risk of specialty barrier coatings | -0.2% | Global, coating suppliers concentrated in Northern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Moisture-Barrier Limitations in Tropical Distribution Chains

Coated paper blisters exhibit water-vapor transmission rates three to five times higher than those of aluminum foil, leading to stability failures in humidity levels above 75%. Field audits in Southeast Asia reported 12% higher API degradation for hygroscopic tablets shipped in fiber packs versus conventional blisters. Seasonal monsoon cycles and non-climate-controlled warehouses further widen the performance gap. Workarounds such as desiccant inserts and modified atmospheres add USD 0.03-0.08 per unit, eroding cost parity. Until water-based nanocellulose coatings deliver foil-class vapor resistance at scale, pharmaceutical adoption in equatorial markets will track slowly.

Line-Speed Penalties Slow High-Volume Production

Thermoforming fiber substrates necessitate prolonged heating and cooling cycles, cutting throughput by 15-25% on existing rotary lines. Output losses compress margins for generic drug makers competing on pennies per pack. Equipment vendors now market induction heating platens and servo-controlled forming dies that help reclaim part of the speed gap; however, capital outlays approach USD 2 million per line, and yield payback horizons are near two years. Management teams therefore stagger retrofits, tempering global conversion rates during the current forecast window.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: SBS Dominance Faces Nanocellulose Disruption

Solid Bleached Sulphate board retained 37.68% of the paper-based and foil-free blister packaging market share in 2025, due to its entrenched converter familiarity and compatibility with FDA-approved aqueous barrier dispersions. The segment accounts for the largest share of the paper-based and foil-free blister packaging market size, as integrated pulp-to-pack players secure quality and price stability through captive forests and in-house coating assets. Moderate density and caliper uniformity ensure low scrap rates on high-speed forming lines, which is particularly beneficial for pharmaceutical applications that require narrow dimensional tolerances.

Micro-fibrillated cellulose sheets promise to disrupt the incumbent base, as their oxygen and moisture performance now rivals that of aluminum at a significantly lower basis weight. UPM’s FibDex delivers foil-level oxygen ingress while remaining fully repulpable. The material commands premium pricing but finds ready uptake for biologics and high-value specialty therapeutics, where packaging costs are less than 1% of the finished-product value. Blending microfibrils into SBS fiber additionally enhances internal bond strength, allowing for shallower draw ratios and reduced forming energy. Over the forecast period, blended structures will erode SBS's share; however, SBS will continue to anchor mainstream volume in regulated drug channels until the nanocellulose supply broadens and costs normalize.

By Form: Pre-Die-Cut Innovation Drives Premium Positioning

Roll stock accounted for a 63.10% share of the paper-based blister and foil-free blister packaging market in 2025, as pharmaceutical plants rely on continuous web processing to minimize downtime and labor. Existing slit-and-rewind infrastructure allows quick swap-in of coated fiber webs without major tooling, preserving capex budgets while advancing sustainability objectives. Pre-die-cut sheets, growing at a 5.08% CAGR, increasingly target direct-to-consumer nutraceuticals and limited-edition prescription kits that emphasize user experience.

Complex cavity geometries, tactile embossing, and integrated tamper indicators elevate brand value while supporting accessible opening features for seniors. Sheet formats also suit regional co-packers that lack in-house slitting lines, making them a gateway for emerging brands to adopt fiber blisters without deep technical expertise. As e-commerce market share rises, visually disruptive packs shipped in sheets reinforce social media unboxing appeal, sustaining premium price points.

By End-use Industry: Nutraceuticals Outpace Traditional Pharmaceuticals

The pharmaceutical channel held a 40.92% share of the paper-based blister and foil-free blister packaging market in 2025, driven by harmonized serialization mandates and stringent child-resistance requirements. Large multinational drug makers deploy paper blisters primarily in over-the-counter lines to balance environmental commitments against validated stability profiles. Generics rely on fiber packs as a low-cost differentiator, layering curb-side recyclability claims onto therapeutic equivalents priced at parity.

Nutraceutical brands, posting a 4.05% CAGR, leverage flexible claims regimes to accelerate novel package launches without multi-year stability dossiers. Consumers accept 15-25% premiums for supplements positioned as wellness and sustainability, which lifts gross margins and funds rapid design iterations. Direct-to-consumer subscription models intensify pack visibility at every delivery cycle, amplifying the marketing value of aesthetically pleasing fiber blisters. The segment will therefore absorb a disproportionate share of forthcoming nanocellulose capacity, cementing its role as a proving ground for barrier innovations before pharmaceutical roll-out.

Geography Analysis

The Asia-Pacific region generated 34.57% of the paper-based and foil-free blister packaging market in 2025, driven by China and India’s combined 45% share of global pharmaceutical output. Harmonized ASEAN stability guidelines streamline paper blister approvals, shortening go-to-market timelines. Japan’s high-precision forming machinery and South Korea’s electronics packaging expertise spill over into pharmaceutical tooling improvements, further entrenching the regional manufacturing ecosystem. Government circular-economy strategies reward local content by granting tax rebates on domestically sourced fiber substrates, thereby enhancing regional competitiveness.

South America, expanding at an 6.31% CAGR, benefits from Brazil’s USD 1.2 billion annual EPR levy and credit system, which cuts compliance charges by up to 35% for fully recyclable packs. Argentina’s generic drug exporters rely on paper blisters to meet European recyclability specifications, opening new route-to-market channels. [2]Ministry of Health Argentina, “Pharmaceutical Export Strategy 2025-2030,” argentina.gob.ar Chile’s mining-driven consumer affluence boosts demand for premium wellness supplements, resulting in higher adoption of specialty fiber formats. Abundant forestry resources and advancing pulp capacity position the region as a future export hub for barrier-coated roll-stock.

Europe and North America remain mature, with adoption driven by replacement cycles of legacy PVC-al lines rather than greenfield volumes. The European Union’s consistent regulatory timeline assures investors, while established converter relationships in the United States enable seamless substrate qualification. Middle East and Africa lie in early adoption phases, constrained by hot-humid climates and limited recycling infrastructure. Nevertheless, donor-funded upgrade programs in public health supply chains could trigger pilot deployments, especially for malaria and HIV therapies where international NGOs procure large volumes.

Competitive Landscape

Industry concentration is moderate. The top five converters together hold an estimated 48% of the global paper-based and foil-free blister packaging market, reflecting ongoing merger activity, but leaving a meaningful share for regional specialists. International Paper’s USD 8.6 billion purchase of DS Smith in 2025 created a vertically integrated pulp-to-blister giant with added European reach. Smurfit WestRock’s merger yielded a USD 21.4 billion revenue platform that pairs corrugated leadership with specialty barrier coating R&D.

Amcor and Huhtamäki pursue cooperative agreements with pharmaceutical brands, securing multi-year offtake contracts that underwrite capex for next-generation coating lines. Patent filings for fiber blister technologies increased by 23% in 2024, driven by the use of water-based dispersion chemistries and high-cycle forming dies. Competitors differentiate on moisture barrier, line speed, and lifecycle carbon metrics.[3]World Intellectual Property Organization, “Patent Landscape Report: Sustainable Packaging,” wipo.int

Nanocellulose coating start-ups leverage venture funding to accelerate the translation from lab to plant, creating acquisition targets for incumbents seeking a technological edge. Supply chain risk remains concentrated in Nordic coating resin suppliers, though diversification initiatives in North America are underway. Market entry barriers revolve around regulatory dossier preparation and stability testing, favoring incumbents with established quality systems and global pharma customer audits.

Paper-Based Blister And Foil-Free Blister Packaging Industry Leaders

Huhtamäki Oyj

Amcor plc

Smurfit WestRock plc

Sonoco Products Company

Stora Enso Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: International Paper completed its USD 8.6 billion acquisition of DS Smith, forming the largest sustainable packaging supplier focused on barrier-coated paperboard for pharmaceutical applications.

- September 2025: Amcor launched the AmSky Blister System, the first FDA-approved fully recyclable paper-based pack offering 24-month stability for moisture-sensitive drugs.

- Aug 2025: Stora Enso invested EUR 150 million (USD 162 million) to expand Performa Nova capacity by 200,000 tons annually at the Oulu mill.

- July 2025: Smurfit WestRock unveiled a USD 300 million program to co-develop next-generation fiber blisters with pharmaceutical partners, targeting cost parity with PVC-aluminum.

- June 2025: Huhtamäki introduced blueloop Paper, a PFAS-free, water-based barrier that achieves sub-0.1 cc/m²/day oxygen ingress, enabling extended shelf life.

Global Paper-Based Blister And Foil-Free Blister Packaging Market Report Scope

| Solid Bleached Sulphate (SBS) Paperboard |

| Molded Fiber |

| Hybrid Barrier-Coated Kraft |

| Micro-Fibrillated Cellulose Sheets |

| Others Material Type |

| Roll-Stock |

| Pre-Die-Cut Sheet |

| Pharmaceuticals |

| Nutraceuticals |

| Food |

| Consumer Electronics |

| Personal Care and Cosmetics |

| Other End-use Industry |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Material Type | Solid Bleached Sulphate (SBS) Paperboard | ||

| Molded Fiber | |||

| Hybrid Barrier-Coated Kraft | |||

| Micro-Fibrillated Cellulose Sheets | |||

| Others Material Type | |||

| By Form | Roll-Stock | ||

| Pre-Die-Cut Sheet | |||

| By End-use Industry | Pharmaceuticals | ||

| Nutraceuticals | |||

| Food | |||

| Consumer Electronics | |||

| Personal Care and Cosmetics | |||

| Other End-use Industry | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the paper-based blister and foil-free blister packaging market?

The market is valued at USD 4.53 billion in 2026, with a forecast to reach USD 5.29 billion by 2031.

How rapidly is this packaging format expanding globally?

The paper-based blister and foil-free blister packaging market is projected to expand at a 3.15% CAGR from 2026 to 2031.

Which region leads to the adoption of paper blisters for pharmaceuticals?

The Asia-Pacific region holds the largest share of 34.57%, primarily due to the manufacturing dominance of China and India, as well as supportive regulatory alignment.

What segment shows the highest growth rate within this packaging space?

Nutraceutical applications are projected to register the fastest growth rate of 4.05% as consumers accept higher prices for environmentally responsible packaging.

Which material technology is disrupting traditional SBS boards?

Micro-Fibrillated Cellulose Sheets, offering foil-grade barrier performance at lower weights, are forecast to grow at a 4.21% CAGR.

What major restraint could slow adoption in tropical markets?

Moisture-barrier limitations that lead to higher API degradation rates remain a key hurdle in hot-humid distribution chains.

Page last updated on: