Waxed Paper Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

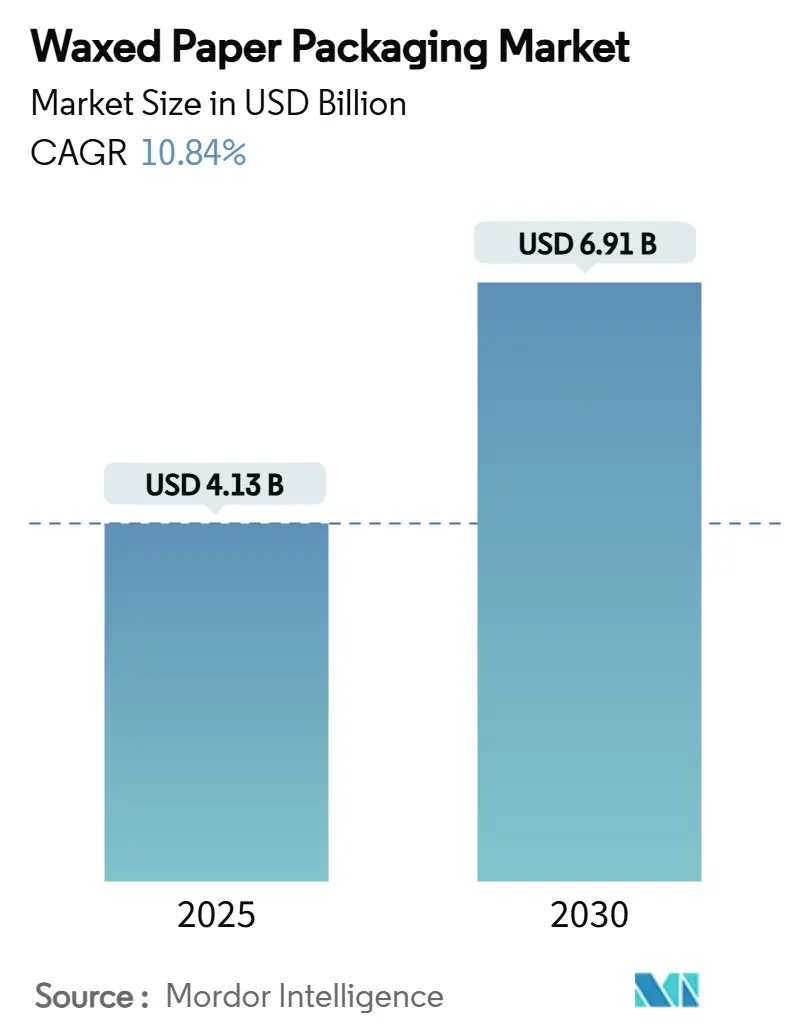

| Market Size (2025) | USD 4.13 Billion |

| Market Size (2030) | USD 6.91 Billion |

| Growth Rate (2025 - 2030) | 10.84% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Waxed Paper Packaging Market Analysis by Mordor Intelligence

The global waxed paper packaging market reached USD 4.13 billion in 2025 and is forecast to attain USD 6.91 billion by 2030, translating into a firm 10.84% CAGR over the period. Demand accelerates as regulators ban PFAS-coated substrates, prompting food brands and quick-service restaurants to switch toward wax barriers that comply with U.S. FDA and forthcoming EU limits.[1]U.S. Food and Drug Administration, “PFAS Used in Grease-Proofing Agents for Food Packaging No Longer Being Sold in the U.S.,” fda.gov Product innovation blends wax with thin polymer or bio-wax layers to raise grease and moisture resistance while keeping costs below petroleum coatings. North American adoption remains strong on the back of state-level restrictions, whereas Asia-Pacific growth reflects new food-contact standards in China and Japan that favor certified natural coatings. Consolidation among converters, highlighted by Novolex’s USD 6.7 billion takeover of Pactiv Evergreen, brings scale advantages in formulation R&D and global distribution.

Key Report Takeaways

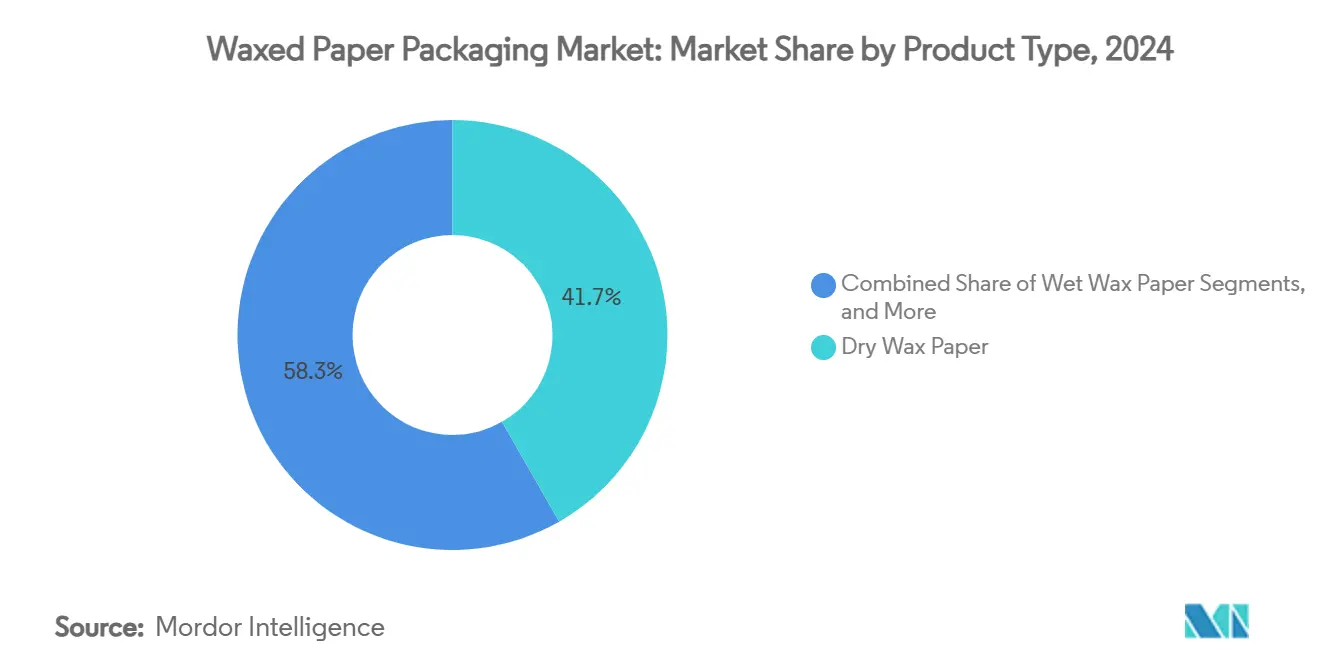

- By product type, dry wax paper captured a 41.74% of the waxed paper packaging market share in 2024.

- By coating material, the waxed paper packaging market size for the soy-based wax segment is projected to grow at a 12.13% CAGR between 2025-2030.

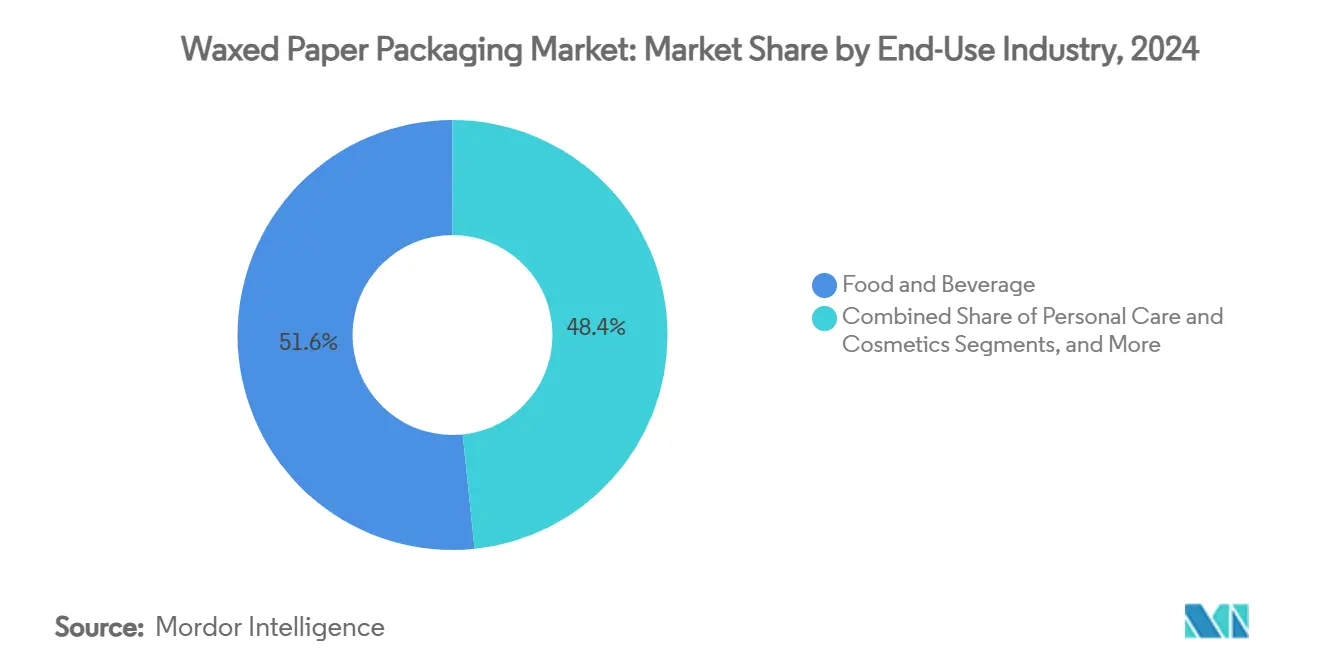

- By end-use industry, food and beverage applications captured 51.63% of the waxed paper packaging market share in 2024.

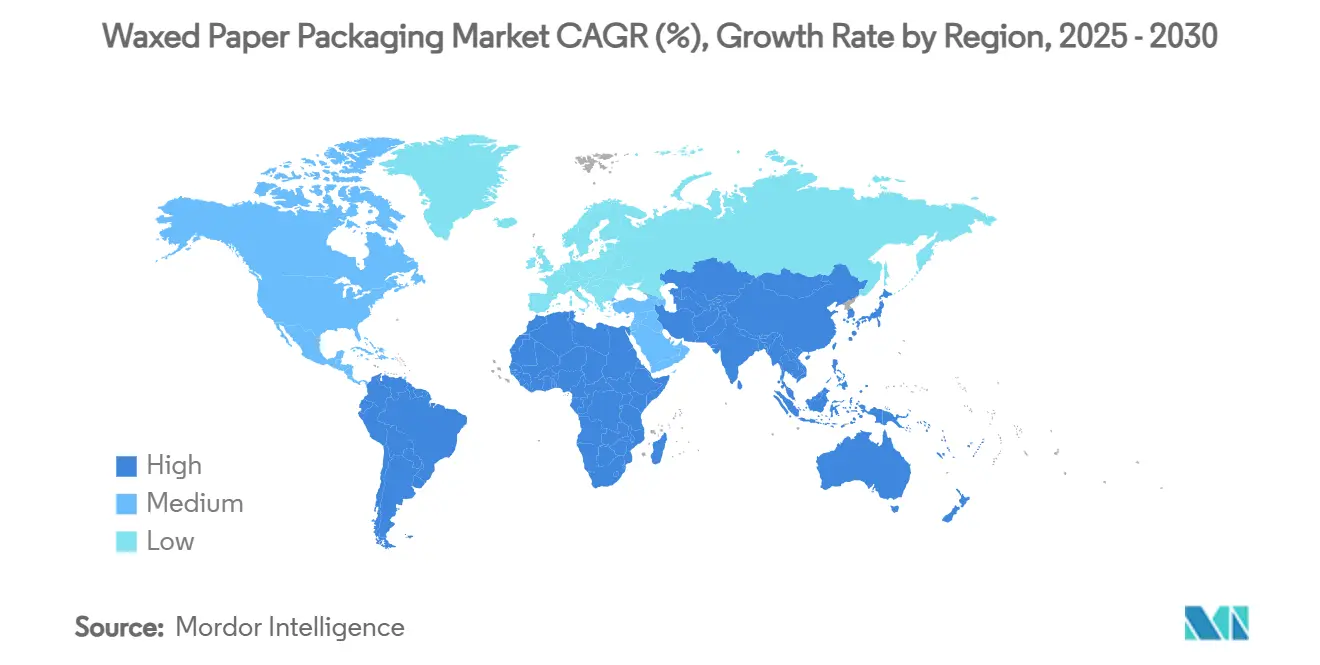

- By geography, the waxed paper packaging market size for the Asia-Pacific region is projected to grow at a 11.84% CAGR between 2025-2030.

Global Waxed Paper Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in QSR takeaway and delivery volumes | +2.8% | Global (early gains in North America, Asia-Pacific) | Medium term (2-4 years) |

| Regulatory push for PFAS-free packaging | +3.1% | North America and EU, spill-over to Asia-Pacific | Short term (≤2 years) |

| Cost competitiveness vs. polymer coatings | +1.9% | Global | Long term (≥4 years) |

| Adoption as cold-chain humidity buffer | +1.4% | Asia-Pacific core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Compostable soy/carnauba wax in gifting | +1.2% | North America and EU | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Surge in QSR Takeaway and Delivery Volumes

Global quick-service chains process millions of delivery orders daily, with Restaurant Brands International reporting more than USD 40 billion in 2024 system-wide sales across 30,000 outlets.[2]U.S. Securities and Exchange Commission, “Restaurant Brands International 2023 Form 10-K,” sec.gov Delivery formats lengthen transit time, so operators specify dual-coated wax paper that combines grease resistance with heat retention. Volume growth also encourages standardized sheet and pouch sizes, giving converters economies of scale. Sustainability claims further tilt specifications away from plastic liners toward FSC-certified paper plus food-grade wax. As multi-market QSR brands harmonize procurement, qualified suppliers enjoy rapid share gains in the waxed paper packaging market.

Regulatory Push for PFAS-Free Packaging

The U.S. FDA confirmed 35 food-contact notifications for PFAS grease-proofing agents are no longer effective, immediately barring new production. In the EU, the Packaging and Packaging Waste Regulation caps individual PFAS at 25 ppb starting August 2026, creating an urgent switch across bakery wraps, deli sheets, and takeaway clamshells. Early adopters lock in supply contracts to avoid compliance bottlenecks, giving incumbents with PFAS-free wax recipes an edge. Documentation and traceability requirements also favor vertically integrated converters with in-house coating and converting.

Cost Competitiveness vs. Polymer Coatings

Petroleum-derived polymer prices remain volatile amid refinery rationalizations and geopolitical uncertainty, whereas bio-wax feedstocks such as soy and rice bran track agricultural cycles and display steadier price curves. Wax impregnation runs on lower heat profiles than extrusion laminations, cutting energy cost up to 80% in controlled trials. In markets without curbside recycling for mixed laminates, landfill or incineration fees add further cost to polymer-heavy packs, reinforcing the economic case for waxed alternatives.

Adoption as Cold-Chain Humidity Buffer

Academic work shows carnauba-wax-coated papers achieve water-vapor transmission rates below 0.5 barrer under refrigerated humidity, outperforming uncoated kraft by an order of magnitude. Asian exporters of mangoes, lychees, and salad greens adopt the format to mitigate surface condensation during multi-day freight. Cold-storage logistics providers report spoilage reduction after shifting to breathable wax wrap layers around pallets of produce, contributing incremental demand to the waxed paper packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from biopolymer films | -1.8% | Global | Medium term (2-4 years) |

| Volatile paraffin wax supply | -1.3% | Global | Short term (≤2 years) |

| Limited recyclability infrastructure | -0.9% | Global (developing markets) | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Competition from Biopolymer Films

R&D advances in PBAT and PLA composites deliver oxygen-barrier metrics rivaling EVOH while retaining compostability, positioning bio-films as technical substitutes for wax wraps. Although current production volumes represent only 0.2% of the plastics pool, announced capacity expansions could narrow the price gap by 2028. Brand owners attracted by transparent film aesthetics may divert orders, applying pricing pressure on commodity wax grades.

Volatile Paraffin Wax Supply

The Russo-Ukrainian conflict and Middle-East shipping disruptions have tightened global paraffin supply, leading to double-digit quarterly price swings. Converters hedge through multi-wax blending and greater use of soy or rice bran derivatives, but sudden spikes still compress margins. Synthetic alternatives from China partially offset shortages yet require qualification testing, slowing the shift.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Composite Innovation Drives Market Evolution

Dry wax paper captured 41.74% of the waxed paper packaging market share in 2024, benefiting from entrenched use in burger wraps and industrial parts interleaving where moderate barrier suffices. End-users value its low basis weight and competitive pricing. Composite grades, which laminate a micro-thin polymer or bio-wax over the paper core, are scaling up fastest at an 11.97% CAGR. They answer higher grease, aroma, and puncture resistance needs of hot sandwiches, bakery trays, and frozen entrées without breaching PFAS guidelines. Wet-wax and waxed kraft formats keep niche roles in produce and recyclable applications, respectively, but ongoing R&D in hybrid coatings is poised to blur segment boundaries.

Composite materials also open new design territory such as printable glossy faces and colored barrier stripes, supporting brand aesthetics. Continuous-streak coating heads now enable grammage control within ±2%, driving material savings that boost converter profitability. Collectively, these factors reinforce composite paper’s contribution to the waxed paper packaging market size while ensuring dry wax paper retains relevance through sheer volume leadership.

By Coating Material: Bio-Based Alternatives Gain Momentum

Paraffin accounted for 46.31% of the waxed paper packaging market size in 2024, a dominance rooted in reliable supply chains stemming from petro-refinery by-products. Yet soy-based wax climbs fastest with a 12.13% CAGR, aided by renewable carbon content above 90% and farm-origin branding that resonates with consumer goods companies. Carnauba occupies premium slots where high gloss and hardness matter, including cosmetics wraps and luxury confection sleeves. Beeswax and rice-bran derivatives fill health-food and allergen-sensitive niches.

Paraffin price swings and carbon disclosure mandates hasten material diversification. Automated dosing systems allow converters to switch wax blends on the same line, facilitating incremental substitution strategies without capital overhauls. Consequently, bio-waxes move from lab trials to multi-ton runs, solidifying their foothold in the waxed paper packaging market.

By End-Use Industry: Personal Care Emerges as Growth Driver

Food and beverage retained 51.63% of total revenue in 2024 as QSR chains and bakeries standardize PFAS-free wraps and liners. Nonetheless, personal care and cosmetics is slated to outpace all others at 11.71% CAGR. Brands favor waxed tissue for facial blotters, soap wraps, and premium gift sets where tactile feel and natural-origin claims enhance shelf differentiation. Industrial sectors deploy waxed interleavers to shield metal parts from flash rust, whereas agriculture leverages breathable wax layers to cut produce desiccation.

E-commerce adds tailwinds as direct-to-consumer beauty startups prefer plastic-free inner wrap to bolster sustainability messaging. That pivot unlocks fresh demand streams and widens application breadth, thereby reinforcing the waxed paper packaging market’s resilience to cyclical swings in any single vertical.

Geography Analysis

North America commanded 33.89% of global sales in 2024 due to the immediate impact of FDA PFAS rulings and high QSR penetration. Capital spending by Georgia-Pacific—USD 425 million on a Tennessee disposable-tableware facility—is increasing domestic wax-coating capacity. Brand procurement teams also prize local supply to sidestep trans-Pacific freight disruptions.

Asia-Pacific is forecast to generate the sharpest 11.84% CAGR to 2030. China’s first mandatory express-packaging standard, GB 43352-2023, raises barrier performance thresholds and limits heavy-metal residues, steering courier firms toward certified wax papers. Japan’s positive-list system for food-contact resins, effective June 2025, encourages substitution with plant-wax coatings that require simpler regulatory dossiers. Rapid urbanization and growth of third-party delivery apps magnify downstream demand, positioning the region as a pivotal growth engine for the waxed paper packaging market.

Europe shows steady momentum under the EU’s 2026 PFAS ceiling of 25 ppb, coupled with Germany’s reusable-packaging mandate that spurs chains to trial wax-coated fiber trays for eat-in and takeaway. Extended Producer Responsibility rules in the UK further incentivize recyclable and compostable substrates, reinforcing regional preference for natural wax coatings.

Competitive Landscape

Market concentration is moderate, with strategic mergers and acquisitions shaping supplier hierarchies. Novolex’s USD 6.7 billion merger with Pactiv Evergreen created a portfolio of more than 250 brands and 39,000 SKUs, underpinning integrated design-to-delivery solutions that appeal to multinational foodservice accounts.[3]Novolex, “Novolex Completes Combination with Pactiv Evergreen,” pactivevergreen.com Georgia-Pacific’s USD 2 billion multi-site upgrade adds barrier-coating and forming assets aligned to PFAS-free specifications, closing logistics gaps and lowering order lead times.

Competitive differentiation hinges on coating chemistry, lifecycle credentials, and quality management. Producers tout cradle-to-gate carbon audits and secure FDA letters of no objection to qualify for sensitive food-contact categories. R&D labs accelerate pilot-scale trials of soy-rice-bran wax blends, targeting equivalent oil-resistance with 20% lower coating weight. Converters also adopt digital presses for short-run graphics, enabling promotional customizations without disrupting mass volumes—a service valued by QSR franchisees.

Supply-side risk management drives vertical integration into wax refining and paper mills, safeguarding feedstock during paraffin market turbulence. Simultaneously, nimble regional players carve out niche beachheads in gift, floral, and organic produce wraps, leveraging proximity and service flexibility. This dual-track dynamic sustains healthy rivalry and spurs technological upgrades across the waxed paper packaging market.

Waxed Paper Packaging Industry Leaders

Novolex

Georgia-Pacific LLC

Oji Holdings Corporation

Bomarko Inc.

Packaging Products (Coatings) Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Novolex finalized the USD 6.7 billion acquisition of Pactiv Evergreen, establishing one of the world’s largest food-service packaging groups.

- December 2024: Georgia-Pacific detailed more than USD 2 billion in 2023 U.S. facility investments, including a USD 425 million disposable-tableware site in Jackson, Tennessee.

- June 2024: China began enforcing express-packaging standard GB 43352-2023, introducing strict paper-substance limits that favor compliant wax coats.

- May 2024: Clariant launched Licocare RBW Vita rice-bran wax with 98% renewable-carbon content as a carnauba alternative.

Global Waxed Paper Packaging Market Report Scope

| Dry Wax Paper |

| Wet Wax Paper |

| Waxed Kraft Paper |

| Wax-Poly Composite Paper |

| Others |

| Paraffin Wax |

| Beeswax |

| Soy-based Wax |

| Carnauba Wax |

| Others |

| Food and Beverage |

| Personal Care and Cosmetics |

| Industrial and Automotive |

| Agriculture and Floriculture |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Dry Wax Paper | ||

| Wet Wax Paper | |||

| Waxed Kraft Paper | |||

| Wax-Poly Composite Paper | |||

| Others | |||

| By Coating Material | Paraffin Wax | ||

| Beeswax | |||

| Soy-based Wax | |||

| Carnauba Wax | |||

| Others | |||

| By End-Use Industry | Food and Beverage | ||

| Personal Care and Cosmetics | |||

| Industrial and Automotive | |||

| Agriculture and Floriculture | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the value of the waxed paper packaging market in 2025?

The market is worth USD 4.13 billion in 2025.

How fast will the waxed paper packaging market grow through 2030?

It is forecast to expand at a 10.84% CAGR, reaching USD 6.91 billion by 2030.

Which product type currently holds the largest market share?

Dry wax paper leads with 41.74% share as of 2024.

What is driving the shift toward wax-based food wraps and liners?

Global bans on PFAS-coated substrates, particularly the U.S. FDA’s phase-out, are pushing brands to adopt compliant waxed paper alternatives.

Which region is expected to post the fastest growth?

Asia-Pacific is projected to record the highest regional CAGR at 11.84% through 2030.

Page last updated on: