Glassine Paper Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

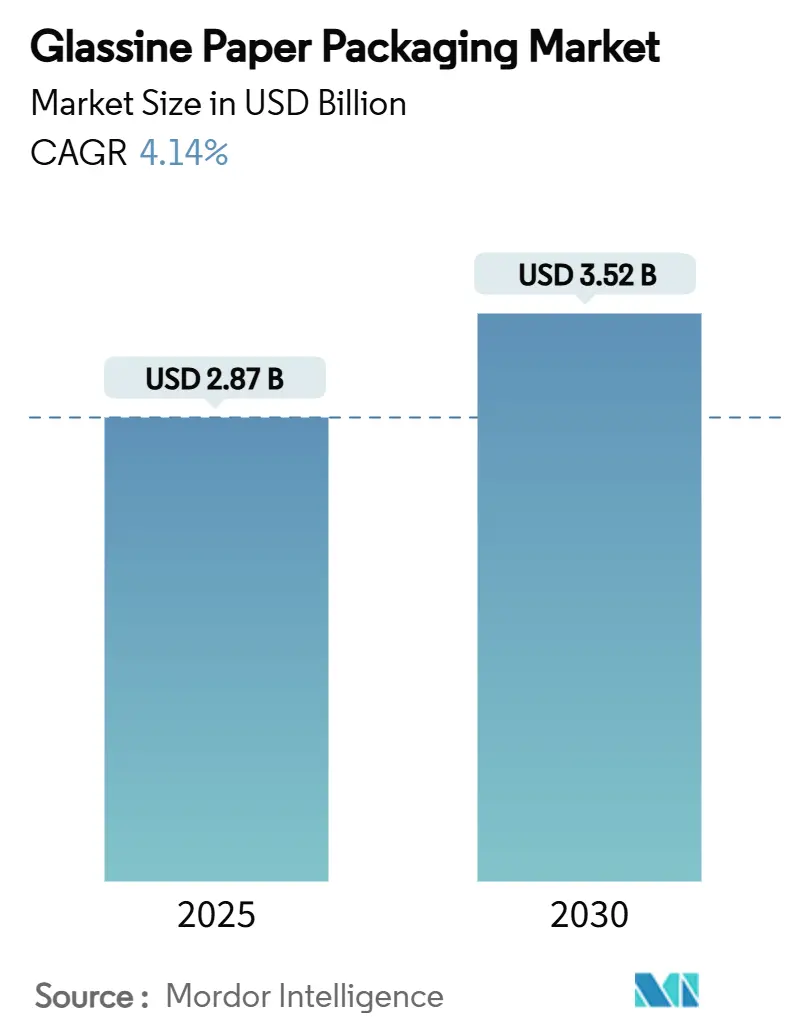

| Market Size (2025) | USD 2.87 Billion |

| Market Size (2030) | USD 3.52 Billion |

| Growth Rate (2025 - 2030) | 4.14% CAGR |

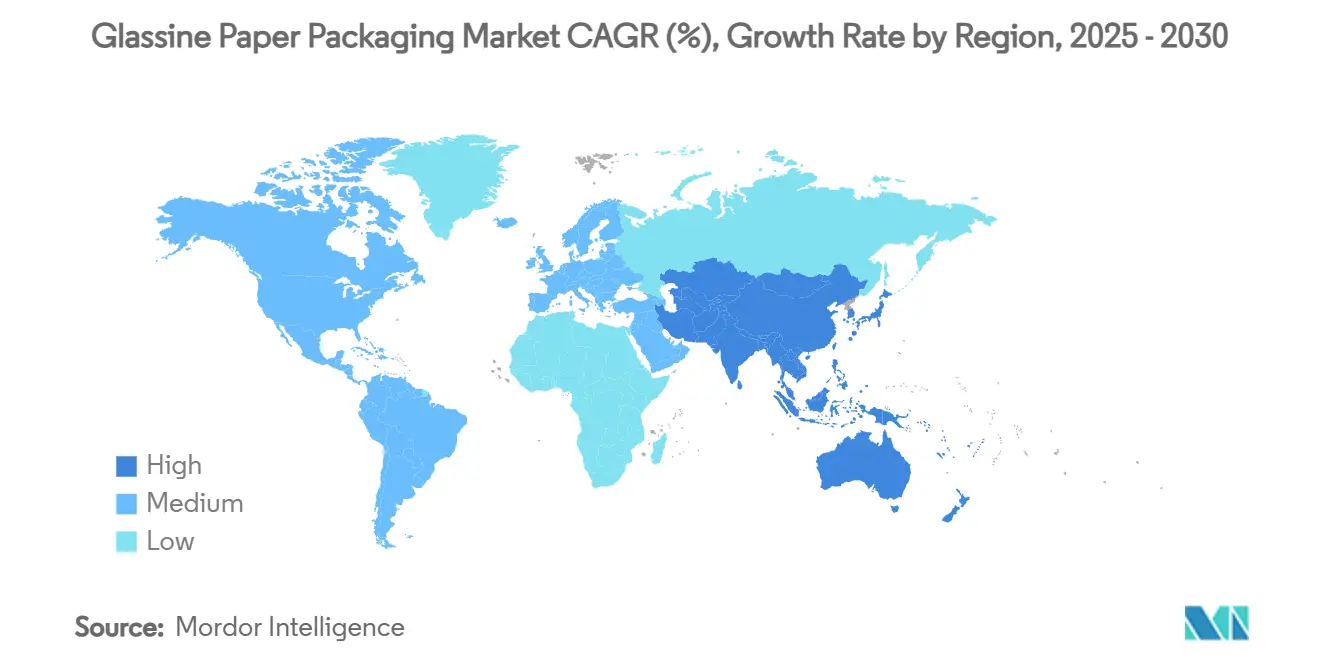

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

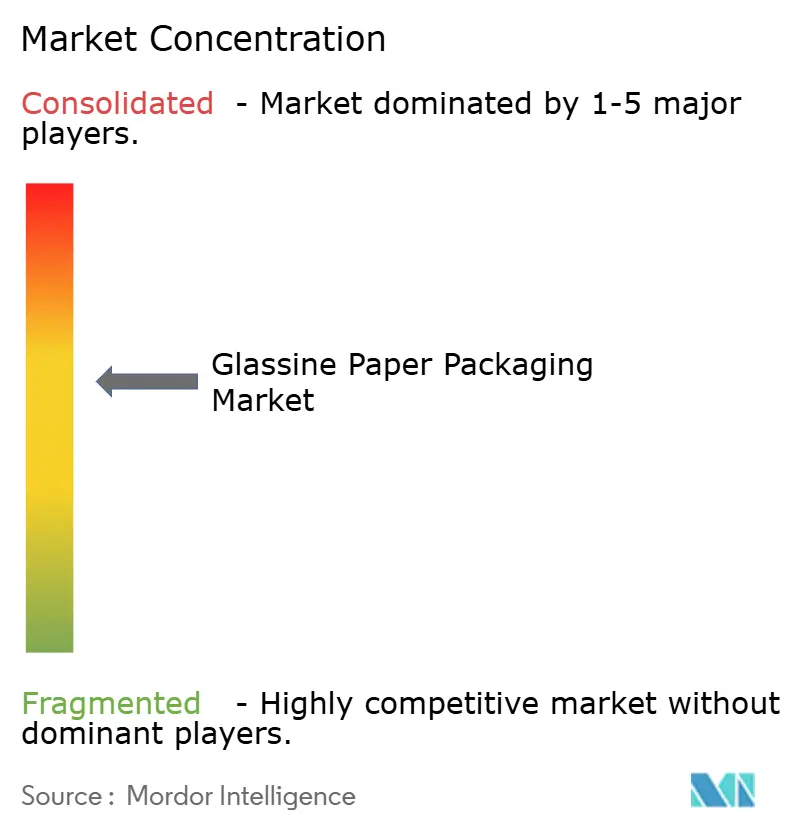

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Glassine Paper Packaging Market Analysis by Mordor Intelligence

The glassine paper packaging market size reached USD 2.87 billion in 2025 and is projected to climb to USD 3.52 billion by 2030, marking a 4.14% CAGR over the forecast period. Multiple tailwinds converge to shape this trajectory: legally binding recyclability targets in the European Union, the phased elimination of per- and polyfluoroalkyl substances (PFAS) in food-contact formats in the United States, and brand owners’ public sustainability pledges. Intensifying regulatory scrutiny elevates glassine paper from a niche substrate to a mainstream option because it meets curb-side recyclability thresholds without additional chemical treatments. Rising e-commerce volumes also increase demand for tamper-evident, grease-resistant wraps that maintain product integrity during last-mile delivery. Investments in super-calender finishing capacity by leading producers indicate confidence in premium applications despite near-term pulp supply constraints.

Key Report Takeaways

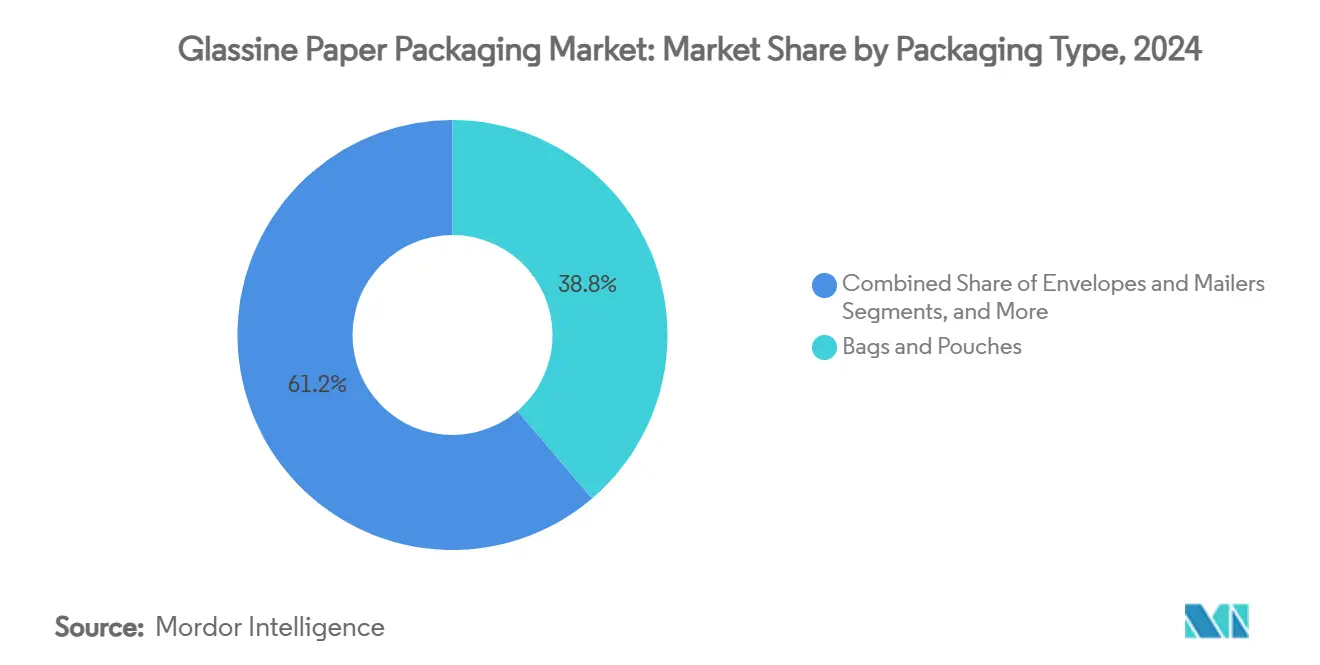

- By packaging type, bags and pouches captured a 38.76% share of the glassine paper packaging market size in 2024.

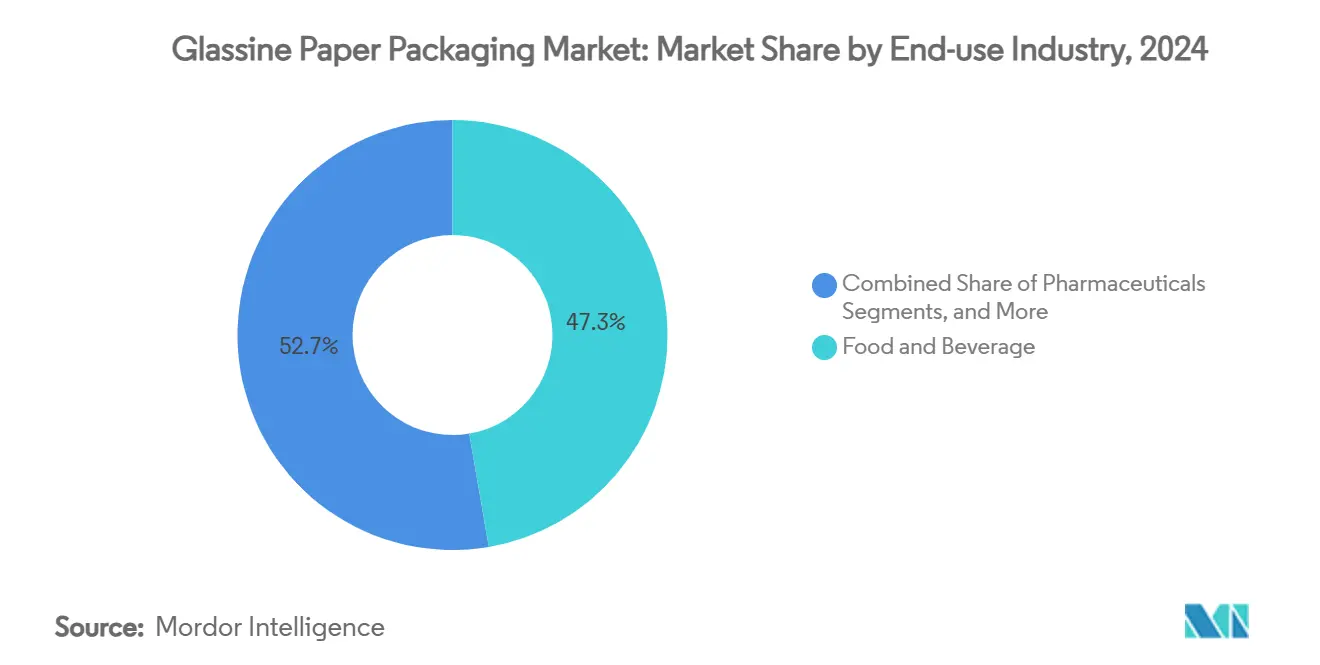

- By end-use industry, the glassine paper packaging market size for the pharmaceuticals segment is projected to grow at a 6.04% CAGR between 2025-2030.

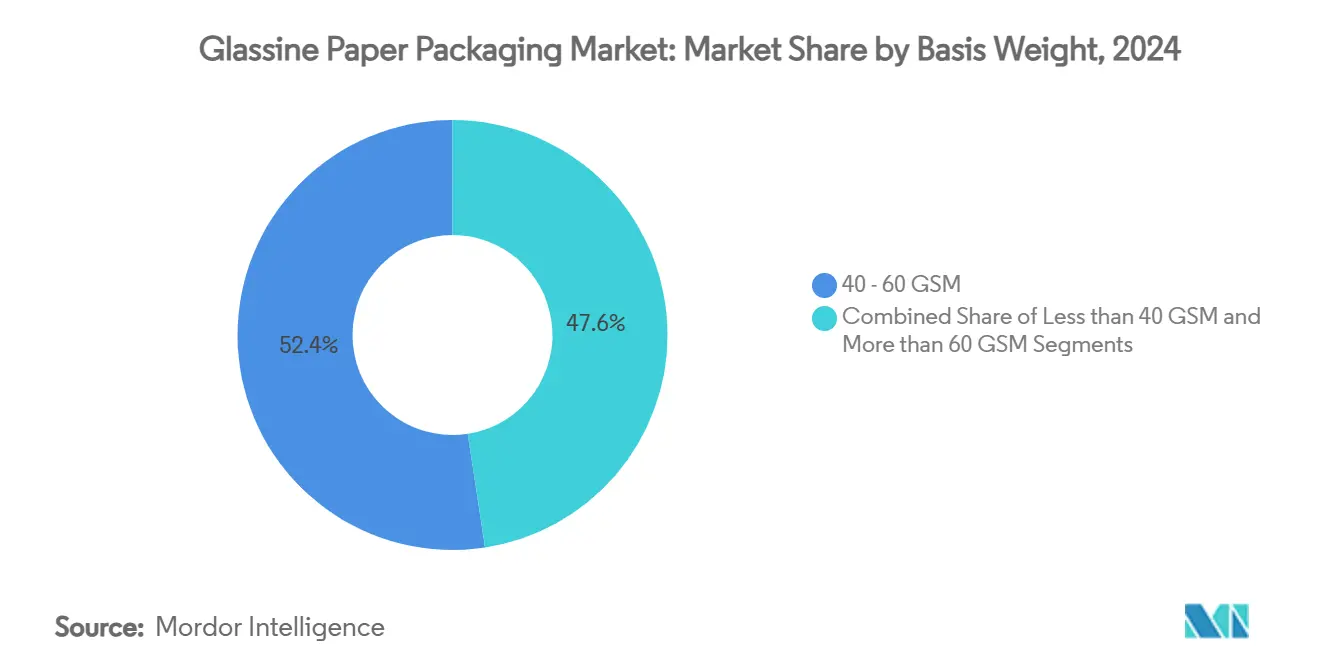

- By basis weight, the 40-60 GSM segment captured a 52.42% share of the glassine paper packaging market size in 2024.

- By geography, the glassine paper packaging market size for the Asia-Pacific region is projected to grow at a 7.16% CAGR between 2025-2030.

Global Glassine Paper Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for recyclable and compostable packaging | +1.2% | Global, with EU and North America leading | Medium term (2-4 years) |

| Stringent global and regional plastic-reduction mandates | +0.9% | EU, North America, select APAC markets | Short term (≤ 2 years) |

| Booming e-commerce and food-delivery ecosystems | +0.7% | Global, concentrated in urban centers | Medium term (2-4 years) |

| Expansion of pharmaceutical unit-dose formats | +0.5% | North America, EU, Japan | Long term (≥ 4 years) |

| Shift to silicone-free release liners | +0.3% | Global, technology-driven markets | Long term (≥ 4 years) |

| Premium translucent packs for luxury cosmetics | +0.2% | EU, North America, select APAC luxury markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Recyclable and Compostable Packaging

Legislators increasingly anchor recycling goals in binding law, turning recyclability from a marketing attribute into a market-entry ticket. The Packaging and Packaging Waste Regulation 2025/40 requires every consumer pack placed in the EU to be fully recyclable by 2030. Glassine, produced from highly refined cellulose fibers, meets curb-side collection criteria without multilayer separation. Academic work shows that boric-acid cross-linked polyvinyl-alcohol coatings lift oxygen and moisture barriers while retaining up to 82% marine biodegradation, confirming that end-of-life performance can coexist with high functionality. Brand owners view compostability as insurance against future landfill fees, encouraging specification shifts toward paper substrates

Stringent Global and Regional Plastic-Reduction Mandates

Governments now deploy trade restrictions and direct substance bans to curb single-use plastics. The U.S. FDA’s March 2025 revocation of 35 PFAS food-contact notifications removed widely used grease-proofing treatments overnight. In parallel, China’s GB 43352-2023 standard for courier parcels limits heavy metals in paper-based mailers. These converging rules accelerate material substitution toward PFAS-free glassine that already complies with heavy-metal thresholds, narrowing qualification timelines for new suppliers.

Booming E-commerce and Food-Delivery Ecosystems

Direct-to-consumer channels require packages that withstand long transit routes and multiple touchpoints. Grease-resistant wraps keep takeaway meals visually appealing, directly influencing repeat-ordering behavior. Pharmaceutical e-pharmacies add demand for tamper-evident pouches with low water-vapor transmission. The glassine paper packaging market gains as retailers seek formats compatible with automatic packing lines yet thin enough to minimize volumetric shipping costs. Producers therefore invest in high-speed precision slitting and heat-seal coating lines to meet fulfillment center cycle-time benchmarks.

Expansion of Pharmaceutical Unit-Dose Formats

Unit-dose blisters support medication adherence and reduce contamination risk. The FDA’s Essential Drug Delivery Outputs draft guidance highlights packaging integrity as a prerequisite for drug efficacy.[1]Human Foods Program, “FDA Determines Authorization for 35 Food Contact Notifications Related to PFAS Are No Longer Effective,” U.S. Food and Drug Administration, fda.gov Glassine’s heat-sealable surfaces and resistance to sterilization chemicals make it a reliable backing material for tablet and transdermal systems. Manufacturers with validated clean-room facilities and DMF filings enjoy entry barriers that defend premium margins.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher cost versus conventional polymer films | -0.8% | Global, price-sensitive applications | Short term (≤ 2 years) |

| Limited intrinsic moisture barrier | -0.6% | Global, humid climate regions | Medium term (2-4 years) |

| 2026-27 hardwood-pulp supply squeeze | -0.4% | North America, Northern Europe | Medium term (2-4 years) |

| Carbon-pricing exposure of finishing lines | -0.3% | EU, carbon-tax jurisdictions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher Cost Versus Conventional Polymer Films

Super-calendering glassine requires energy-intensive drying and polishing, raising unit costs relative to oriented polypropylene. Carbon pricing in Europe will inflate production overheads after 2026, according to producer disclosures. While premium applications can absorb price differentials, commodity snack wraps remain vulnerable to polymer substitution unless offset by recyclability fees on plastics.

Limited Intrinsic Moisture Barrier Requiring Extra Coating

Uncoated glassine absorbs moisture, which can warp delicate structures in humid climates. Barrier lacquers add process steps and supplier dependencies, slightly diluting lifecycle-assessment advantages. Research in interface engineering shows a 50.7% improvement in water-vapor resistance for paper-based systems, but commercial scale-up remains nascent.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Wraps and Rolls Drive Innovation Momentum

The wraps and rolls segment contributed 5.83% CAGR to the overall glassine paper packaging market between 2025 and 2030, while bags and pouches maintained 38.76% revenue leadership in 2024. In the wraps category, thinner calibers and continuous-feed geometries optimize material yield, aligning with e-commerce automation needs. Producers increasingly offer pre-creased formats that conform tightly to irregular objects, lowering damage rates during parcel sorting.

R&D investment focuses on heat-seal lacquers that activate at lower temperatures, reducing energy draw on flow-wrapper lines. Release-liner variants pursue silicone-free chemistries to meet recycling targets without complicating downstream paper recovery. The segment benefits from in-line digital printing, enabling short-run graphics for seasonal promotions. These factors collectively position wraps and rolls as the engine of new application development inside the glassine paper packaging market.

By End-use Industry: Pharmaceuticals Accelerate Growth

Food and beverages retained 47.31% of 2024 revenue, yet pharmaceuticals advance the glassine paper packaging market size at a 6.04% CAGR through 2030. Unit-dose formats respond to hospital demand for single-patient administration, while heat-sealable envelopes meet OTC blister-pack backing needs. FDA regulations under 21 CFR 176 permit sodium-nitrate-urea as a plasticizer up to 15 % by weight in dry-food glassine, illustrating regulatory familiarity that eases life-science adoption.

Hand-made confectioners in Europe also shift to glassine for grease-resistant wraps that showcase product texture. Cosmetics brands elevate unboxing rituals by specifying translucent sleeves that reveal product silhouettes, blending sensory appeal with recyclability. This duality of premium function and compliance accelerates penetration across varied industries.

By Basis Weight: Lighter Papers Capture Innovation

The less than 40 GSM class registers the fastest advance, adding 5.42% CAGR, yet 40-60 GSM papers still hold 52.42% of glassine paper packaging market share in 2024. Process optimization through moisture-controlled blank forming allows thinner sheets to retain shape during 3D cold-molding at tool surface temperatures around 100 °C.

Converters view basis-weight reduction as the most direct path to emissions abatement because each gram removed lowers freight fuel burn. Advanced pigments now boost opacity, allowing lighter grades to mask contents without heavier calipers. Premium >60 GSM products remain essential where tear resistance overrides cost.

Geography Analysis

North America generated 31.48% of 2024 revenue, anchored by the United States’ mature pharmaceutical and fast-food sectors. Brand-owner commitments to phase out PFAS accelerate specification changes, while Amazon’s updated vendor guidelines privilege recyclable substrates. Canada’s carbon tax steers retailers toward paper-based mailers, widening demand for ultra-light release liners. Mexico’s near-shoring boom raises requirements for grease-resistant wraps in cross-border snack exports.

Asia-Pacific leads growth at 7.16% CAGR, propelled by China’s express-delivery volumes and India’s rapid food-service expansion. China’s GB 43352-2023 courier standard sets heavy-metal thresholds that established mill laboratories can verify, awarding incumbency advantage to multinational producers. India’s FSSAI rulebook obliges food packs to use food-grade paper, catalyzing adoption among street-food aggregators.[2]Siegwerk Regulatory Affairs, “Regulations in Asia,” Siegwerk, ink-safety-portal.siegwerk.com Japan’s aging population spurs demand for unit-dose pharmaceuticals, benefiting specialty glassine backings.

Europe grows steadily under the Packaging and Packaging Waste Regulation 2025/40 umbrella. Germany pioneers curb-side collection systems where mill-tested recyclability claims enjoy consumer trust. France’s ban on plastic fruit-and-vegetable wraps channels produce packers toward thin glassine windows that maintain breathability. Luxury-goods clusters in Italy favor dyed translucent sleeves for fragrance samplers, reinforcing regional premium positioning.

Competitive Landscape

The market remains moderately fragmented; the top five suppliers control roughly 45% of global revenue, affording room for niche innovators. Mondi, UPM-Kymmene, and Sappi sustain leadership through pulp integration, shielding gross margins during wood-fiber price spikes. Mondi has earmarked EUR 1.2 billion (USD 1.29 billion) for organic growth, with 80% of funds deployed by late 2024 into flexible-packaging assets.[3]Investor Relations Team, “Interim Mondi Group Half-Year Results Announcement 2024,” Mondi Group, mondigroup.com

Stora Enso’s new 750,000-tonne consumer-board line at Oulu widens its renewable-packaging footprint and offers co-production flexibility for glassine precursors. Amcor secured a European patent for its AmFiber Performance Paper, embedding barrier layers that outperform standard greaseproof while remaining recyclable. Specialty coaters, meanwhile, target silicone-free release liners, partnering with electronics OEMs to co-design low-peel slip sheets.

Mergers and acquisitions activity intensifies as players seek scale and coating know-how. International Paper’s conditional acquisition of DS Smith signals a strategic interest in European specialty papers. Smaller converters differentiate via FSC-certified supply chains and carbon-neutral mill programs, attracting luxury-brand procurement teams. Overall rivalry centers on technological innovation, sustainability credentials and regional capacity proximity.

Glassine Paper Packaging Industry Leaders

Ahlstrom-Munksjö Oyj

Delfortgroup AG

Mondi plc

UPM-Kymmene Corporation

Sappi Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: China implemented GB 43352-2023, the first mandatory express-packaging standard covering heavy metals and designated substances.

- May 2024: KAIST and Yonsei University unveiled a boric-acid cross-linked PVA coating achieving up to 82% marine biodegradation while boosting barrier performance.

- March 2024: The FDA ruled that 35 PFAS food-contact notifications were no longer effective, accelerating the transition to alternative barriers.

- February 2024: Mondi reported EUR 7,330 million (USD 7,932 million) revenue for 2023 and confirmed a EUR 1.2 billion (USD 1.29 billion) organic growth investment program.

Global Glassine Paper Packaging Market Report Scope

| Bags and Pouches |

| Envelopes and Mailers |

| Wraps and Rolls |

| Other Packaging Types (Labels, Release Liners) |

| Food and Beverage |

| Pharmaceuticals |

| Cosmetics and Personal Care |

| Industrial and Manufacturing |

| E-commerce and Logistics |

| Other End-use Industries (FMCG, Gift Wrapping) |

| Less than 40 GSM |

| 40 - 60 GSM |

| More than 60 GSM |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Packaging Type | Bags and Pouches | ||

| Envelopes and Mailers | |||

| Wraps and Rolls | |||

| Other Packaging Types (Labels, Release Liners) | |||

| By End-use Industry | Food and Beverage | ||

| Pharmaceuticals | |||

| Cosmetics and Personal Care | |||

| Industrial and Manufacturing | |||

| E-commerce and Logistics | |||

| Other End-use Industries (FMCG, Gift Wrapping) | |||

| By Basis Weight | Less than 40 GSM | ||

| 40 - 60 GSM | |||

| More than 60 GSM | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the glassine paper packaging market by 2030?

The market is forecast to reach USD 3.52 billion by 2030 on the back of a 4.14% CAGR.

Which region is expanding fastest in glassine paper packaging?

Asia-Pacific leads growth with a 7.16% CAGR, driven by e-commerce scaling and new regulatory standards.

Why are pharmaceuticals adopting glassine paper?

Unit-dose formats need moisture-resistant, heat-sealable backings that comply with stringent FDA rules, and glassine meets these criteria.

How do regulatory bans on PFAS affect substrate choice?

The FDA’s PFAS phase-out removes legacy grease-proof coatings, shifting demand toward inherently PFAS-free glassine.

What technological advance helps recycle release liners?

A dissolvable interlayer developed at Western Michigan University enables silicone-free glassine liners to re-enter standard paper streams.

Page last updated on: