Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

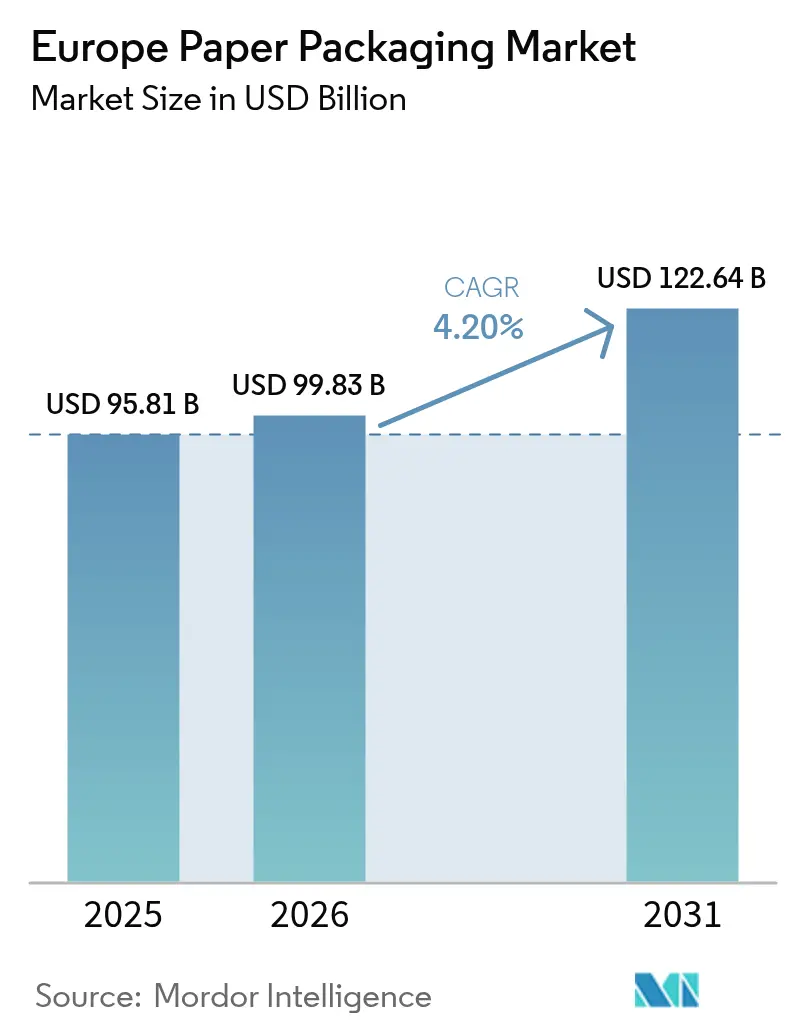

| Base Year Market Size (2025) | USD 95.81 Billion |

| Market Size (2026) | USD 99.83 Billion |

| Market Size (2031) | USD 122.64 Billion |

| Growth Rate (2026 - 2031) | 4.20% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Paper Packaging Market Analysis by Mordor Intelligence

The Europe paper packaging market size is expected to grow from USD 95.81 billion in 2025 to USD 99.83 billion in 2026 and is forecast to reach USD 122.64 billion by 2031 at 4.20% CAGR over 2026-2031. The market gains momentum from the continent’s regulatory shift toward circular economy models, widespread retailer preference for curbside-recyclable formats, and continuous technology upgrades in high-strength corrugated substrates. Fiber-based solutions increasingly displace plastic in food service, e-commerce, and meal-kit applications because they combine ease of recycling with lower carbon intensity confirmed in ISO 14040 life-cycle assessments. Upstream investments in recycled-content board capacity, especially at Nordic mills, mitigate raw-material risk while positioning suppliers for EU Carbon Border Adjustment Mechanism compliance. Heightened merger activity, including the 2024 Smurfit-WestRock combination, tightens competition and accelerates vertical integration, allowing majors to secure virgin and recycled fiber supplies, optimize freight costs, and standardize sustainable sourcing audits across pan-European customer bases. Near-term input-cost headwinds linked to energy volatility squeeze margins; nevertheless, downstream demand remains resilient because online retail penetration, quick-commerce convenience, and increasingly stringent single-use-plastic bans jointly lift packaging volumes.

Key Report Takeaways

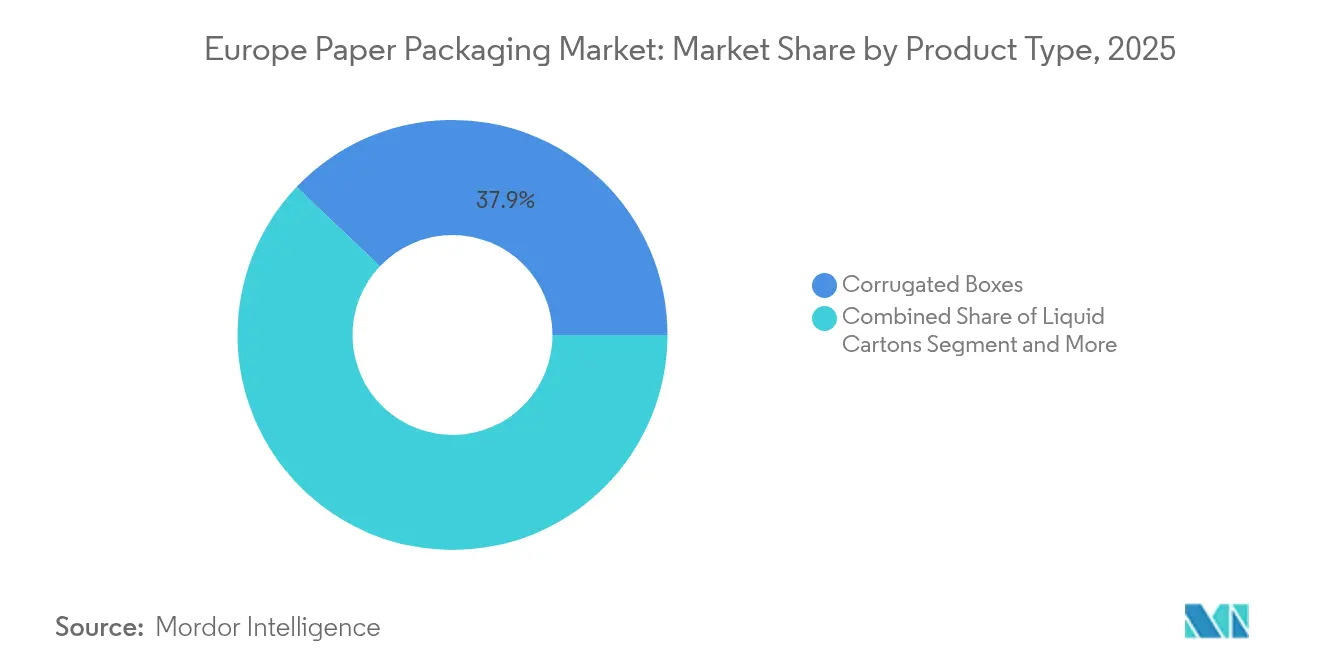

- By product category, corrugated boxes led with 37.92% revenue share in 2025; liquid cartons are forecast to expand at a 5.12% CAGR to 2031.

- By material, recycled paper captured 55.98% share of the Europe paper packaging market size in 2025 and is advancing at a 5.55% CAGR through 2031.

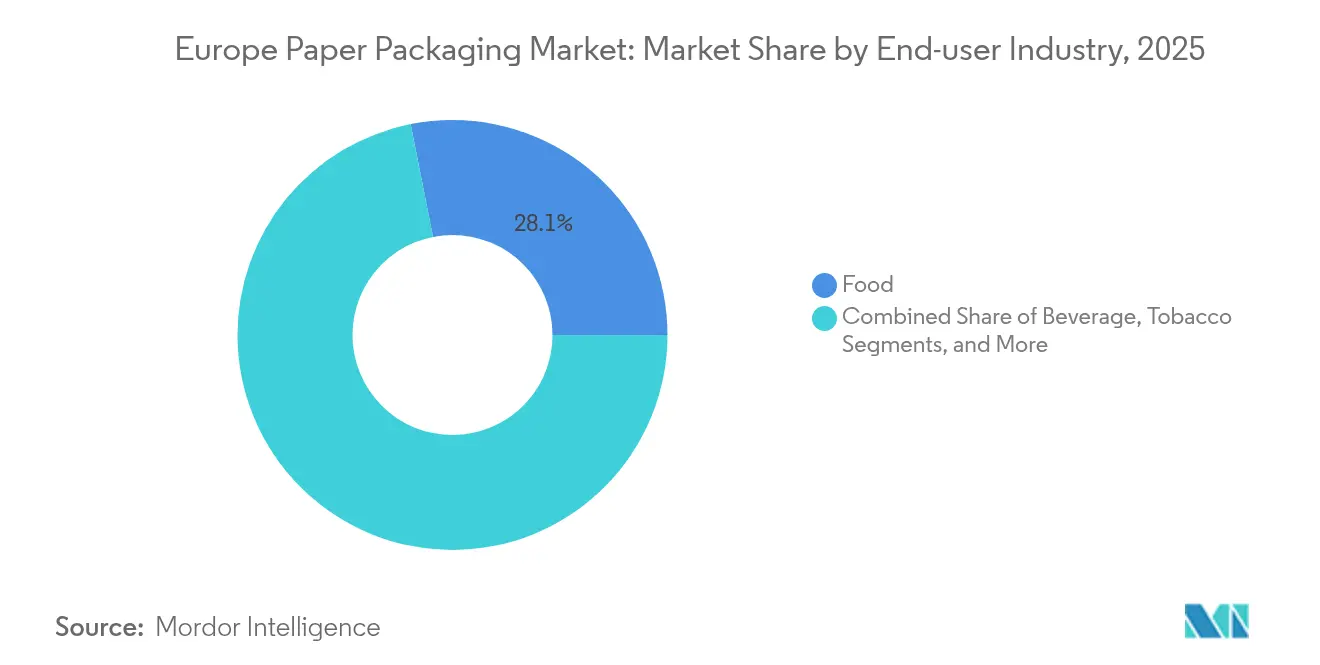

- By end-user, food applications accounted for a 28.12% share of the Europe paper packaging market size in 2025, while beverage is expected to record the highest projected CAGR at 5.21% through 2031.

- By packaging format, secondary packaging 45.94% share of the Europe paper packaging market size in 2025 and is advancing at a 4.79% CAGR through 2031.

- By geography, Germany held 21.05% of the Europe paper packaging market share in 2025; Spain is projected to grow at a 5.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Paper Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for sustainable and recyclable packaging in F&B | +1.2% | EU-wide, strongest in Germany, France, Netherlands | Medium term (2-4 years) |

| Rapid surge in e-commerce parcel volumes | +0.9% | EU-wide, concentrated in urban centers | Short term (≤ 2 years) |

| EU Single-Use Plastics Directive accelerating fiber substitution | +0.8% | EU-wide, phased implementation | Medium term (2-4 years) |

| Advancements in lightweight, high-strength corrugated technology | +0.6% | Germany, Netherlands, Nordic countries | Long term (≥ 4 years) |

| Growth of meal-kit and quick-commerce requiring right-sized packs | +0.5% | Urban markets in Germany, UK, France, Netherlands | Short term (≤ 2 years) |

| EU Carbon Border Adjustment Mechanism driving recycled mills | +0.4% | Border regions, import-dependent markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for sustainable and recyclable packaging in Food and Beverage

European food and beverage brands publicly commit to 100% recyclable packaging targets for 2030, prompting procurement scorecards that prioritize fiber over multilayer plastics. Leading grocers impose shelf-readiness criteria that reward mono-material fiber trays, as shown by Marks & Spencer’s rollout of paper-fiber ready-meal trays in May 2025. Distillers and brewers showcase flagship launches such as a 90% paper bottle for Scotch whisky, reinforcing consumer perception that paper embodies lower environmental impact. Life-cycle studies covering chocolate bar wrappers confirm lower greenhouse-gas footprints for paper against oriented polypropylene in every midpoint category. Packaging converters intensify collaboration with coating-technology suppliers to meet upcoming 25 ppb PFAS limits in August 2026, aligning product reformulations with brand owners’ public sustainability roadmaps. As ISO 14040 compliance becomes mandatory for cross-border central procurement tenders, paper solutions with verified cradle-to-gate data sets gain preferred-supplier status across multinational F&B groups.

Rapid surge in e-commerce parcel volumes

European online retail purchases maintain double-digit growth, fueling a steep rise in box counts and ancillary cushioning across fulfillment centers. Corrugated consumption in the United Kingdom increased 12.6% between 2010 and 2024 as omnichannel grocers and specialty retailers upgraded distribution networks. Amazon reports the elimination of more than 1 billion single-use plastic mailers since 2018 by converting its European operations to 100% recyclable paper pouches and board envelopes in January 2025. Automated right-size packaging equipment, such as solutions codeveloped by Mondi and CMC Packaging Automation, generates on-demand box dimensions that cut paper use up to 40% while improving truck-cubic-utilization metrics. [1]Mondi and CMC Packaging Automation, “Mondi and CMC Packaging Automation partner on e-commerce packaging solutions.” Packaging Europe, packagingeurope.com Urban grocery quick-commerce, projected to jump from EUR 25 billion in 2021 to EUR 72 billion by 2025, requires dimensionally optimized secondary packs that preserve product integrity in 10-minute delivery windows. Consequently, converters prioritize high-speed die-cutting, digital print customization, and inline quality-control sensors to meet both volume scale and branding agility demanded by e-commerce merchants.

EU Single-Use Plastics Directive accelerating fiber substitution

Directive provisions came into force gradually from 2021 and continue to tighten post-2025, outlawing a growing list of single-use plastic articles while exempting cellulose-based formats when recyclable in household streams. Producers with pan-European manufacturing footprints, such as Graphic Packaging International, rapidly engineer recyclable paperboard sushi trays to capture on-the-go food categories previously dominated by PET clamshells. France pledges a total single-use plastic phase-out by 2040, compelling retailers to accelerate substitution timetables beyond EU baselines. Italy’s targeted bans on cotton-bud sticks and cutlery provide additional impetus for fiber innovators. Extended producer-responsibility fees imposed on plastic escalate annually, narrowing cost differentials and rendering paperboard sleeves, wraps, and trays economically attractive replacements. Member-state variations in enforcement place a premium on supplier agility and regulatory affairs competencies, enabling compliant launches across diverse national regimes without duplicate tooling.

Advancements in lightweight, high-strength corrugated technology

Material scientists achieve 15-20% grammage reductions through proprietary dry-forming of long-fiber pulp, evidenced by Stora Enso’s pilot line at Fors, Sweden.[2]Stora Enso, “Stora Enso to build a new dry forming production unit at its Fors mill in Sweden.” storaenso.comNovel fluting geometries and adhesive formulations lift edge-crush and box-compression performance, allowing downgauging without risking product damage during multicycle shipping. Digital inkjet systems now print full-color graphics in one pass on micro-flute grades, supporting personalized messaging for subscription-box brands and minimizing ink inventory. Sensors embedded into corrugated walls track vibration, temperature, and humidity, vital for pharma cold-chain compliance, while remaining recyclable at scale. Platform-wide Corrugated 4.0 initiatives harness plant-wide data analytics to optimize starch application, furnace firing curves, and die-cutter speed, cutting waste and energy intensity simultaneously. These breakthroughs address EU Ecodesign objectives on material efficiency and end-of-life recyclability while delivering freight-weight reductions that lower scope 3 emissions for brand owners.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Deforestation concerns and raw-material supply volatility | -0.7% | EU-wide, particularly Nordic supply regions | Medium term (2-4 years) |

| Improving recyclability of flexible plastics narrowing advantage | -0.4% | EU-wide, flexible applications | Long term (≥ 4 years) |

| Energy-price shocks raising mill operating costs | -0.5% | EU-wide, energy-intensive Nordic mills | Short term (≤ 2 years) |

| PFAS phase-out uncertainty in barrier-coated papers | -0.3% | EU-wide, food-contact papers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Deforestation concerns and raw-material supply volatility

The EU Deforestation Regulation, effective 2025, mandates traceability back to geolocated forest plots, adding 3-5% to procurement overhead as converters implement satellite verification and blockchain ledgers. Nordic sawmill capacity interruptions, stemming from electricity-cost surges and periodic labor stoppages, and thin virgin-fiber availability, are forcing buyers to tap spot markets at premium prices. Billerud’s productivity program underscores industry-wide urgency to offset margin compression arising from pulp price spikes and raw-material scarcity. Alternative fibers such as wheat straw and miscanthus attract attention for molded-fiber food bowls, yet inconsistent fiber length and brightness curtail adoption for high-definition print packs. Geographic diversification toward Iberian and Baltic forests mitigates concentration risk but extends logistics chains, partially reversing carbon-footprint gains. Over the medium term, mills expedite closed-loop water systems and reforestation commitments to reassure stakeholders and comply with tightening due diligence audits.

Improving recyclability of flexible plastics narrowing advantage

Chemical recycling demonstration units scale up across Western Europe, converting mixed polyolefin films into food-grade naphtha feedstock, thereby eroding paper’s recyclability narrative. PepsiCo’s 50% recycled-content flexible film for snack products achieves shelf-life parity with virgin PET laminates while lowering net emissions by 30%. Capri-Sun’s mono-material polypropylene pouch integrates tethered caps to meet upcoming EU lid-attachment rules, simplifying curbside sortation and boosting recycling rates. Post-consumer recycled PET content targets of 30% by 2030, codified in the draft Packaging and Packaging Waste Regulation, spur infrastructure funding that narrows cost gaps relative to paperboard multipacks. High-melt-strength recycled HDPE research confirms mechanical properties comparable to virgin resin, expanding applicability to heavier liquid formats. [3]Giulia Bernagozzi et al., “High Melt Strength Recycled High-Density Polyethylene.” Polymers, mdpi.com As plastics enhance their circularity credentials, paper converters must double down on barrier-coating breakthroughs, print quality, and efficient fiber-use ratios to sustain competitive positioning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Corrugated Dominance Drives Innovation

Corrugated boxes held 37.92% of 2025 revenue, underscoring their status as the workhorse format across fulfillment, industrial, and grocery distribution channels. Europe's paper packaging market size for corrugated boxes is projected to compound steadily, given e-commerce parcel proliferation, customized print runs, and continuous lightweighting gains that lower freight emissions without forfeiting crush strength. Liquid cartons post the fastest 5.12% CAGR through 2031, propelled by dairy-alternative beverages, shelf-stable juice lines, and brand-led commitments to curb multilayer plastics usage.

Secondary products such as folding cartons maintain relevance for pharmaceutical blister overwraps and high-graphic personal-care packs where precise creasing and glossy varnishes create shelf appeal. Paper sacks and retail bags regain momentum as national bans phase out single-use plastic carriers, with grocers switching to kraft options featuring wet-strength additives for reuse durability. Specialty niches—tear-resistant freezer bags, shaped formed-fiber trays, and molded-pulp void-fill expand addressable volumes, yet corrugated remains the anchor that underpins converter plant utilization rates and capex justification across the region.

By Material Type: Recycled Content Mandates Reshape Supply

Recycled grades captured 55.98% share in 2025, an outcome of stringent post-consumer content targets and robust collection systems that feed domestic mills. Europe paper packaging market share for recycled liner is expected to widen as CBAM makes imports of virgin grades more expensive relative to low-carbon recycled sheet. High-quality white-top testliner gains favor in display-ready cases requiring printable surfaces, while brown testliner dominates standard shipping cartons.

Virgin-fiber substrates remain indispensable for premium cosmetics gift boxes, medical device manuals, and folding cartons demanding pristine print fidelity and superior stiffness. Composite paperboard featuring dispersion or extrusion barriers occupies a middle ground where water-vapor and fat resistance are critical, yet PFAS-phase-out risk tempers near-term expansion. Supply chains gravitate toward dual-sourcing strategies, combining Scandinavian softwood kraft with Iberian eucalyptus hardwood to balance strength and smoothness. Mills engage in circularity partnerships with retailers to backhaul OCC (old corrugated containers) from distribution centers, shortening loop time and securing feedstock purity levels imperative for food-grade recycled content.

By End-user Industry: Food Applications Lead Transformation

Food brands commanded 28.12% of demand in 2025, capitalizing on modular carton formats that accommodate SKU proliferation and ready-meal convenience trends. Europe paper packaging market size continues to expand here, supported by supermarket deli counters adopting grease-resistant kraft wraps now free of fluorochemicals ahead of the 2026 PFAS deadline. Beverage operators outpace aggregate growth at 5.21% CAGR as carton bottle concepts move from pilot to limited national rollouts for still water and spirits, tapping into consumer appetite for visibly sustainable packaging.

Pharmaceuticals gravitate toward tamper-evident folding cartons and leaflets produced in ISO 22301 certified facilities, while household-care players leverage hybrid board pouches to decrease plastic jug use for powdered detergent concentrates. E-commerce platforms standardize two-piece corrugated mailers with tear-strips and easy-return glue lines, a pattern exemplified by apparel re-ship programs in Germany and France. Meal-kit companies remain innovation hotbeds, integrating molded-pulp separators and thermal liners to secure perishables, thereby driving incremental tonnage despite leaner material footprints per serving.

By Packaging Format: Secondary Packs Drive Volume and Efficiency

Secondary formats represented 45.94% of aggregate tonnage in 2025, rising 4.79% annually as fulfillment centers demand crush-resistant, RFID-enabled shippers that navigate complex last-mile routings. Europe's paper packaging market size gains ground from brand owners’ push to consolidate multiple primary items into one protective outer, improving pick efficiency and reducing dunnage. ThermoBox solutions delivering polystyrene-like insulation, yet remaining fully kerbside-recyclable, find scope in high-value seafood and biologic pharma lanes where temperature excursions jeopardize product integrity.

Primary packs face functional headwinds, notably moisture ingress and long-shelf-life oxygen barriers, yet dispersion-coated cupstock and extrusion-laminated soup cartons slowly erode PET and HDPE bottle share. Tertiary packaging, pallet sheets, corner posts, and slip-sheets gain incremental value through sensor integration that transmits tilt and impact events, assisting logistic providers in root-cause damage analysis. Continuous right-sizing initiatives, aided by 3D-scanning software, curb corrugated usage per shipped unit, though absolute tonnage still grows with parcel counts.

Geography Analysis

Germany remained the largest national market with 21.05% share in 2025 because its export-oriented manufacturing base relies on high-performance corrugated and folding cartons to protect precision goods throughout long-haul distribution. Mills cluster along the Rhine corridor, benefitting from barge logistics that reduce freight emissions while feeding large corrugators servicing automotive and engineering clients. Mandatory reusable-takeaway packaging laws enacted in 2023 stimulate the development of fiberboard bowls compatible with dishwashing cycles, although early surveys report slow consumer uptake due to deposit-return administrative hassle.

Spain delivers the highest 5.78% CAGR to 2031 as national waste-law amendments compel supermarkets to halve plastic-wrap usage for produce aisles, opening doors for micro-flute trays and molded-pulp clamshells. The port of Valencia serves as a hub funneling citrus exports into fiber-based ventilated cartons, while domestic converter capacity grows in Catalonia to serve quick-commerce grocers in Barcelona and Madrid. Local R&D alliances, such as Graphic Packaging’s PaperSeal Shape Tray pilot line, demonstrate a nimble response to evolving EU regulations and retailer requirements.

France and the United Kingdom jointly represent nearly one-quarter of regional demand, driven by dense retail landscapes, advanced recovery infrastructure, and active brand commitments to plastic reduction. Post-Brexit customs paperwork complexity nudges U.K. e-tailers toward local corrugated sources to avoid continental lead-time uncertainty. Italy and the Netherlands act as innovation nodes: Lombardy hosts pharmaceutical-grade carton specialists compliant with GMP Annex 11, whereas Dutch firms pioneer closed-loop beverage-carton recycling anchored by Tetra Pak’s 20,000 tonne non-fiber component facility in Ittervoort. Emerging Eastern European markets contribute incremental volume as EU accession financing modernizes collection systems and aligns packaging legislation with Western standards.

Regulatory Landscape

The European Commission is tightening packaging rules through Regulation (EU) 2025/40 (Packaging and Packaging Waste Regulation, PPWR). The regulation entered into force on 11 February 2025 and applies from 12 August 2026. A core compliance anchor is the PPWR requirement that packaging placed on the EU market must be recyclable from 12 August 2026, shifting design and material decisions toward formats that meet harmonized EU criteria rather than fragmented national transpositions under Directive 94/62/EC.

In June 2026, the European Commission issued a guidance notice (C/2026/3084) with clarifications and FAQs to support more uniform implementation by Member States and economic operators. PPWR also sets up follow-on delegated and implementing acts that define methodologies and conformity assessment details, creating a compliance workstream for paper packaging suppliers around recyclability assessment, labelling expectations, and documentation readiness ahead of the August 2026 applicability date.

Value Chain Analysis

The value chain starts with sustainable forestry and recovered-paper collection (OCC and mixed paper), followed by pulping, containerboard and cartonboard production, and then downstream converting into corrugated boxes, folding cartons, bags and sacks, and liquid-carton substrates. European packaging-grade output is closely linked to recycling loops, with packaging grades accounting for a majority share (about 63%) of total production and serving as key uses of paper for recycling. This reinforces the importance of collection quality, sorting, and bale availability for recycled liner and board.

Midstream, energy-intensive mills and integrated players manage exposure to power and fuel costs through efficiency and fuel-switching programs, while large groups use vertical integration to secure fiber and optimize logistics. Downstream, converters and brand owners increasingly require auditable sustainability and footprint data, and industry coordination on common LCA approaches shows up through collaborations involving CEPI, FEFCO, and Smurfit WestRock to standardize carbon footprint reporting. The regulatory pull from PPWR (Regulation (EU) 2025/40, applicable from 12 August 2026) also adds documentation and design-for-recycling requirements that propagate upstream into fiber sourcing traceability, mill quality systems, and converter specifications for food, beverage, and e-commerce packs.

Competitive Landscape

Europe paper packaging market exhibits moderate concentration, with the top five integrated groups- Smurfit WestRock, Mondi, Stora Enso, DS Smith, and Mayr-Melnhof- controlling an estimated 65-70% of regional containerboard and cartonboard capacity. The July 2024 Smurfit-WestRock merger created an entity generating USD 34 billion annual revenue, delivering raw-material optionality between European kraftliner and North American semichemical fluting grades. Competitors respond via bolt-on acquisitions: Mondi acquired Schumacher Packaging in April 2025, gaining specialty corrugated plants in Germany and Poland plus a foothold in molded-fiber inserts.

Technology investment becomes a key battleground. Stora Enso’s Oulu mill board line introduces AI-driven quality control that detects pinholes in real-time, cutting off-spec output and safeguarding food-contact compliance. DS Smith scales digital printing across 200 corrugators, offering brand owners late-stage artwork changes suited to seasonal promotions. Vertical integration patterns intensify; converters sign multi-year contracts with forest owners to lock in FSC-certified fiber, shielding themselves from deforestation regulation disruptions.

Strategic partnerships target e-commerce automation and pharmaceutical packaging. Mondi works with CMC Packaging Automation to embed fan-fold kraft paper into high-velocity pack stations that create on-demand right-sized boxes. Mayr-Melnhof deepens co-development with biotech firms needing tamper-evident micro-perforations and covert security inks. Smaller regional players carve out niches in luxury rigid boxes and fruit-ventilated trays but face margin pressure due to rising pulp and energy inputs.

Europe Paper Packaging Industry Leaders

Mondi Group

Hamburger Containerboard GmbH (Prinzhorn Group)

Smurfit Westrock

Metsa Board Oyj

International Paper Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

One clear whitespace is compliance-ready, paper-based food-contact packaging that fits tightening chemical and recyclability expectations under Regulation (EU) 2025/40, which applies from 12 August 2026 and raises design-for-recycling requirements across materials. This is supporting demand for fluorine-free functional barriers and simpler pack constructions in ready-meals, bakery, and on-the-go categories, where paperboard trays, wraps, and coated papers compete directly with plastic formats. Retailer actions such as Marks & Spencer rolling out paper-fiber ready-meal trays (May 2025) provide a concrete demand signal from end customers.

Another opportunity involves scaling recycled-content board and containerboard supply alongside higher-performance lightweight corrugated for e-commerce and quick-commerce. In these channels, right-sized packaging and print personalization are procurement priorities. The direction is supported by capacity and capability moves in the region, including Stora Enso starting production on its consumer board line at Oulu (May 2025), and the shift by large shippers toward paper-based mailers and pouches, including Amazon reaching 100% recyclable packaging across European fulfillment (January 2025). With PPWR harmonizing market access rules, suppliers that combine regional recycled-fiber sourcing with validated recyclability documentation and LCA-ready data sets are better positioned for pan-European tenders in food, beverage, and retail distribution.

Recent Industry Developments

- July 2026: Smurfit WestRock partnered with Coca-Cola on specialized packaging tied to World Cup-related demand peaks. The collaboration highlights how large beverage and CPG accounts are using event-driven volume spikes to test faster design-to-shelf cycles and scalable paper-based promotional packaging across Europe.

- March 2026: Metsa Board introduced MetsaBoard Pro FBB Go and paired it with a fast-track sheet delivery service for European customers. The effort targets shorter lead times for brand packaging and helps converters and brand owners accelerate pack redesigns and specification changes ahead of PPWR-driven requirements.

- December 2024: Graphic Packaging International introduced a paperboard sushi-pack range positioned to comply with EU Single-Use Plastics Directive-related recyclability criteria. The launch supports fiber substitution in on-the-go food formats that have been dominated by plastic clamshells, strengthening paperboard trays as a mainstream alternative in retail convenience.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers paper-based packaging sold and used across Europe, where fiber materials are converted into packaging formats for protecting, transporting, and presenting goods in supply chains.

Scope exclusions: We exclude plastic-dominant packs, packaging machinery, and printing services that are billed as standalone work.

Segmentation Overview

- By Product Type

- Folding Cartons

- Corrugated Boxes

- Paper Bags and Sacks

- Liquid Cartons

- Other Paper Packaging

- By Material Type

- Virgin Fiber Paper

- Recycled Paper

- Composite Paperboard

- By End-user Industry

- Food

- Beverage

- Healthcare and Pharmaceutical

- Personal Care and Household

- E-commerce and Retail

- Tobacco

- Other End-user Industries

- By Packaging Format

- Primary Packaging

- Secondary Packaging

- Tertiary Packaging

- By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market guardrails and build initial assumptions that could later be tested against market signals. We relied on public and official references, including Eurostat manufacturing and trade series, European Commission policy updates and packaging waste reporting (including EPR related guidance), and national statistics offices for country level production indicators.

To avoid basing the model on a single data stream, we added checks from CEPI publications on paper and board, customs and trade releases, peer-reviewed journals on packaging materials, and selected patent databases that indicate activity around barrier papers and recyclability. Company annual reports, investor presentations, and reputable business press were also reviewed to understand capacity additions, mill conversions, and regional demand themes. Paid subscriptions for company financials and news intelligence were used only to speed up cross-checks on revenue exposure and event timelines. These examples are not exhaustive, and other public sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was carried out through expert interviews and structured surveys with packaging converters, paper and board producers, distributors, and large end users that buy high volumes for food, beverage, e-commerce, and healthcare. These discussions were used to confirm what gets counted as paper packaging in practice, to sanity-check price movements, and to validate demand shifts across major European country clusters.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 13% | |

| Mid tier: 51% | Functional/Unit leaders: 38% | |

| Smaller Players: 22% | Managers: 49% |

Market-Sizing & Forecasting

Sizing started with a top-down reconstruction where packaging demand is built from end-use output and trade signals across Europe, then filtered into paper packaging using penetration and substitution assumptions. To keep the totals realistic, we corroborated the result with selective bottom-up approximations, including sampled converter revenue exposure, spot checks on country volumes, and price-per-ton to volume relationships that were validated during interviews.

Key inputs used in the model included paper and board production trends, packaging-grade import and export movement, recycled fiber availability signals, average selling price progression for major paper packaging formats, and end-use demand indicators tied to food and beverage, retail, and e-commerce. Because pricing can swing with energy costs and recovered paper input costs, forecast assumptions were checked against how contracts are typically reset, then applied consistently by country group. For forecasting, scenario analysis was used so different outcomes for regulation timing, recycled-content supply, and substitution away from plastic could be reflected without overstating volatility. Where bottom-up information was missing for smaller countries, gaps were filled using proxy intensity factors based on output and consumption patterns, followed by interview-led reasonableness checks.

Data Validation & Update Cycle

Before finalizing, outputs were triangulated across independent signals, including production and trade direction, price movement logic, and end-use demand narratives shared by respondents. Variances were flagged when country totals moved away from known manufacturing activity patterns, and then the assumptions were revisited until the drivers matched what the market could realistically absorb.

A multi-step internal review was followed, and re-contacts were triggered when large gaps appeared in key variables such as pricing, recovered paper availability, or major capacity changes. Reports are refreshed annually, with interim updates added when material events occur. Before delivery, the numbers receive a fresh pass so clients get the most current view available at that time.

Mordor Intelligence's Europe Paper Packaging Market Size Versus Other Published Estimates

Published market sizes for Europe paper packaging can vary because each publisher uses a different mix of products, end users, and timing for the base year. Even when geography overlaps, the way paperboard is treated versus broader paper products, and whether packaging-adjacent revenues are counted, can shift the final number.

The main gap comes from scope choices around what counts as packaging, where Mordor Intelligence counts paper packaging across defined formats and end uses, while leaving out wider paper and paperboard activity that is not sold as packaging to end customers.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 95.81 B (2025) | |

| Industry Publisher A | USD 57.96 B (2025) | Uses a narrower packaging definition that appears to undercount several paper packaging formats and channels across Europe, which can compress the market total even when the growth rate looks similar. |

| Consulting Publisher B | USD 54.46 B (2024) | Uses an earlier base year and a tighter segment lens focused on select grades and end uses, which can omit parts of paper packaging demand tied to retail and distribution-heavy applications. |

Looking across the three figures, the spread is mostly explained by how the packaging scope is drawn and how the base year is selected. By keeping the included formats and end-use demand pool explicit, and then checking price and volume logic with market participants, the estimate stays traceable to clear inputs and repeatable steps.

Key Questions Answered in the Report

What is the forecast value of Europe paper packaging by 2031?

It is expected to reach USD 122.64 billion, reflecting a 4.20% CAGR over 2026-31.

Which product leads demand in European fiber packaging?

Corrugated boxes hold 37.92% share due to their versatility in e-commerce, industrial, and grocery channels.

Why is Spain the fastest-growing European country in this sector?

Aggressive plastic-reduction mandates, rapid e-commerce adoption, and local innovations like PaperSeal trays push Spanish demand at a 5.78% CAGR.

How are EU regulations shaping barrier-coated paper development?

A 25 ppb PFAS limit effective 2026 forces converters to commercialize fluorine-free water and grease barriers for ready-meal and bakery formats.

What strategic move reshaped the competitive landscape in 2024?

The Smurfit-WestRock merger created a USD 34 billion revenue leader, accelerating vertical integration and global reach.

Which material segment benefits most from the Carbon Border Adjustment Mechanism?

Recycled linerboard, because localized production avoids CBAM carbon charges on imported virgin grades while meeting content mandates.

Page last updated on: