Gravure Printing Machines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.46 Billion |

| Market Size (2031) | USD 3.67 Billion |

| Growth Rate (2026 - 2031) | 1.17% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia-Pacific |

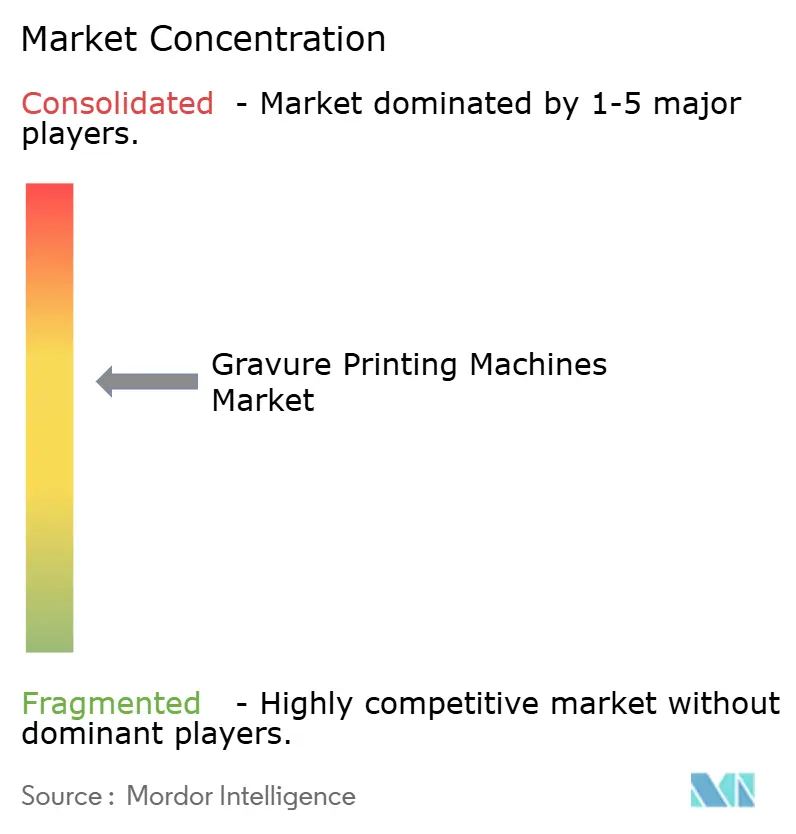

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gravure Printing Machines Market Analysis by Mordor Intelligence

The gravure printing machines market size is expected to increase from USD 3.42 billion in 2025 to USD 3.46 billion in 2026 and reach USD 3.67 billion by 2031, growing at a CAGR of 1.17% over 2026-2031. Demand is strongest where converters need consistent ink lay-down on downgauged, post-consumer-recycled flexible films, and where stringent brand and regulatory requirements still favor cylinder-based micro-engraving. Automated high-speed presses, energy-efficient solvent recovery systems, and trivalent chrome plating are lowering operating costs, helping the gravure printing machines market defend its premium graphics niche against encroachment from flexographic and digital technologies. Asian suppliers are seizing mid-tier opportunities by offering presses that pair servo drives with competitive pricing, while European incumbents differentiate through Industry 4.0 connectivity and Pantone-certified extended-gamut workflows. Finally, anti-counterfeiting features, serialization mandates, and Europe's sustainability targets continue to anchor gravure’s relevance in premium packaging and security printing applications.

Key Report Takeaways

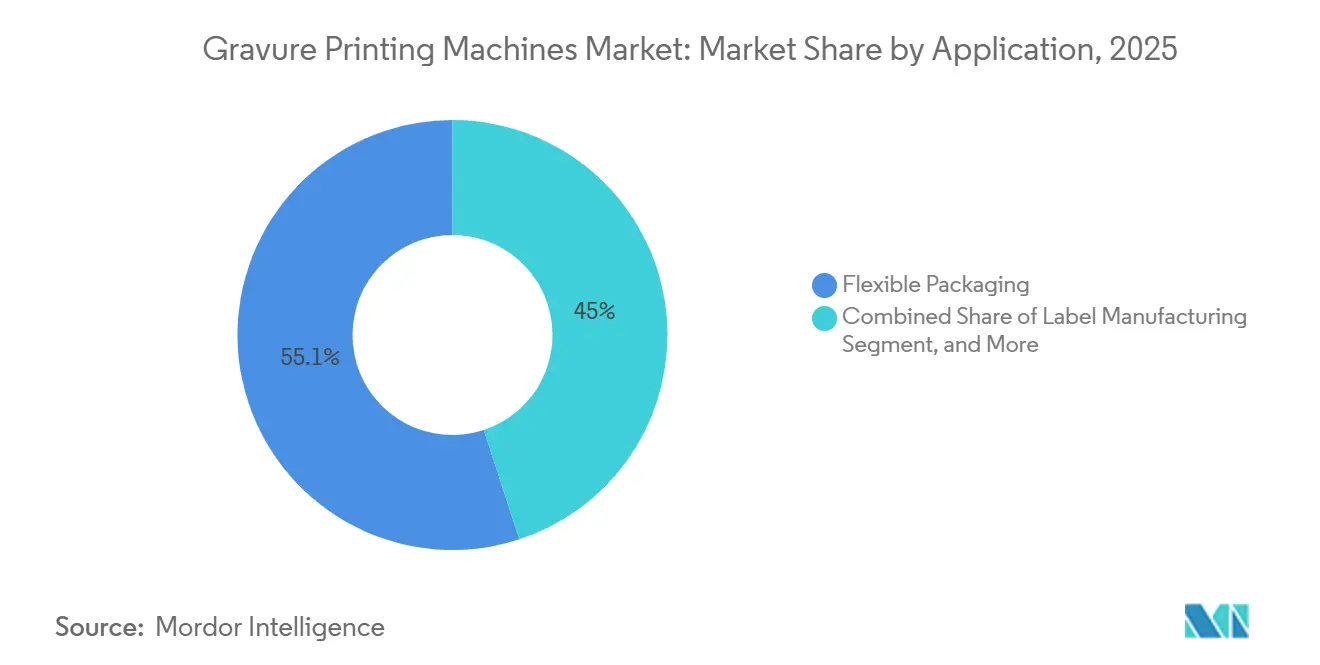

- By application, flexible packaging led with 55.05% share of the gravure printing machines market in 2025, whereas industrial and security printing is advancing at an 1.65% CAGR to 2031.

- By substrate type, plastic films retained 60.23% share of the Gravure printing machines market in 2025, whereas metallic foils are on track for a 1.77% CAGR as premium spirits and cosmetics shift toward extended-gamut metallic effects.

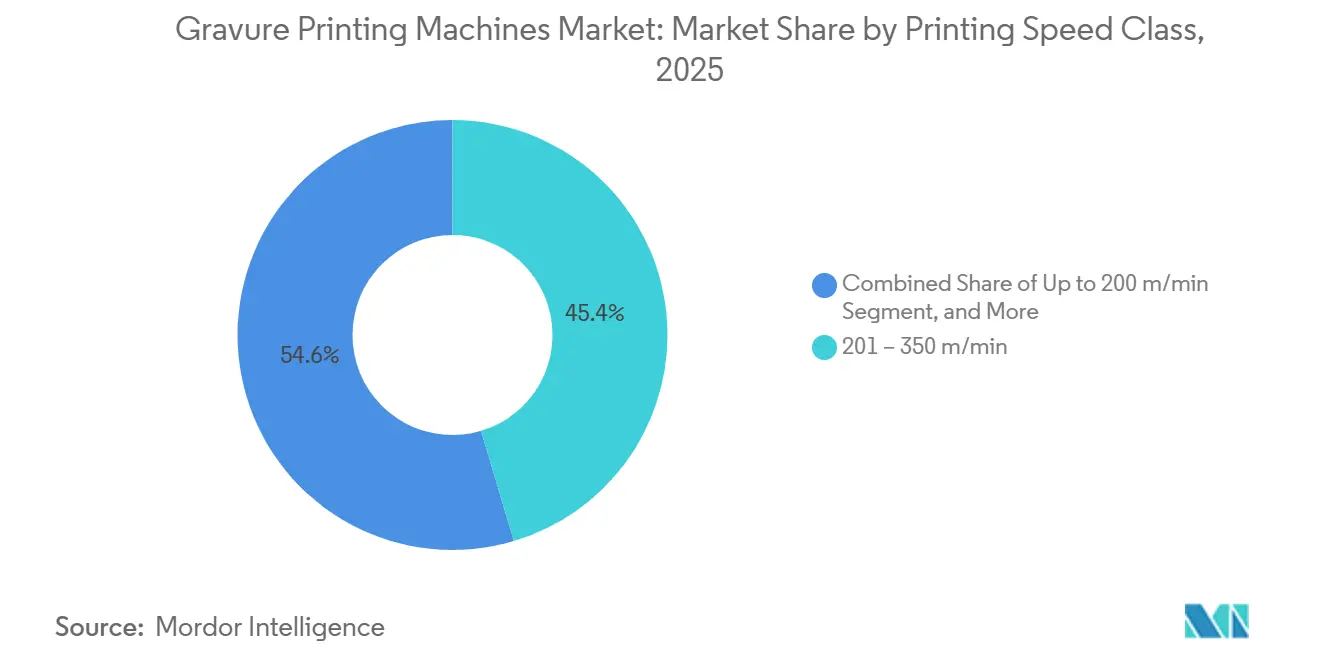

- By printing speed class, presses rated 201-350 m/min captured 45.38% share of the gravure printing machines market in 2025, but models above 350 m/min will expand at 1.19% CAGR, reflecting converters’ push for lower unit costs on long runs.

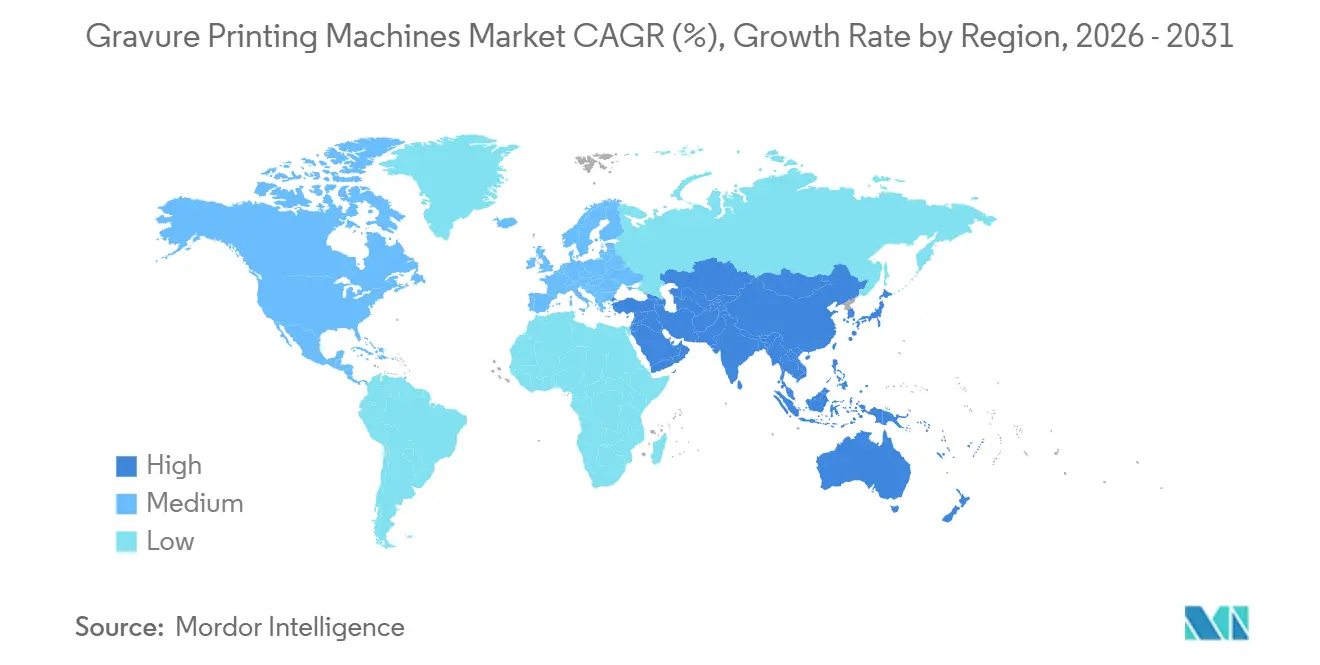

- By geography, Asia-Pacific accounted for 42.16% of the gravure printing machines market in 2025, while the Middle East recorded the fastest trajectory with a 1.97% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Gravure Printing Machines Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for High-Quality Flexible Packaging in E-Commerce | +0.2% | Global, concentrated in urban corridors across North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Technological Advancements in High-Speed and Automated Gravure Presses | +0.2% | Europe and Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Adoption of Eco-Friendly Inks and Solvent Recovery Systems Driven by Regulations | +0.1% | Europe and North America, spillover to export-oriented Asia-Pacific converters | Medium term (2-4 years) |

| Expansion of Packaging Capacity in Emerging Asian Economies | +0.1% | China, India, Southeast Asia, with spillover to the Middle East and Africa | Long term (≥ 4 years) |

| Integration of Digital Gravure Modules for Short-Run Personalization | +0.1% | North America and Europe, early uptake in premium segments | Medium term (2-4 years) |

| Growth in Anti-Counterfeiting Security Features Requiring Gravure Micro-Engraving | +0.1% | Global, emphasis on pharmaceutical and luxury supply chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for High-Quality Flexible Packaging in E-Commerce

Online retail continues to reshape packaging specifications, pushing converters toward gravure presses that deliver high-opacity graphics on downgauged films durable enough for automated fulfillment centers. Mid-width lines between 1,050 mm and 1,250 mm equipped with cart-mounted cylinder trolleys now change jobs in under 10 minutes, letting plants handle limited-edition batches of 10,000-20,000 linear meters without sacrificing color density. A new class of shaftless presses introduced in 2026 further elevates throughput to 500 m/min while maintaining tension on ultra-thin mono-material webs, a key requirement for meeting EU post-consumer-recycled content mandates. Brand owners in Asia-Pacific and North America prefer these lines because they combine premium shelf appeal with compliance to migration limits on food-contact films, ensuring product integrity throughout multi-modal distribution networks.

Technological Advancements in High-Speed and Automated Gravure Presses

Manufacturers have embedded servo drives, inline spectrophotometry, and cloud-based recipe libraries to eliminate the skilled-operator bottleneck that historically limited gravure to long runs. One flagship system measures optical density 9,500 times per second, holds ink viscosity within a 4 °C window, and completes makeready in under eight minutes, reducing ink waste by half. In China, newly launched lines integrate HD video inspection and independent deck motors to hit 500 m/min with ±10 µm register accuracy, a specification once reserved for European flagships. These automation gains push the economic crossover where gravure beats flexo down to roughly 5,000 m², opening profitable space in medium runs and allowing the gravure printing machines market to penetrate segments traditionally served by flexography.[1]SHAANXI BEIREN PRINTING MACHINERY CO LTD, “Company News,” beireninternational.com

Adoption of Eco-Friendly Inks and Solvent Recovery Systems Driven by Regulations

The EU Industrial Emissions Directive and the planned phase-out of hexavalent chromium have accelerated investment in trivalent chrome plating, laser-engraved cylinders, and closed-loop solvent capture. A recently commercialized ink-supply module delivers 80% energy savings in the dryer and VOC emissions below 20 mg/m³, exceeding upcoming regional thresholds. Cylinder engravers switching to laser etching report 44% less copper and 50% less chrome use, trimming raw-material bills and hazardous-waste fees. Converters in North America and Europe are early adopters because their brand customers mandate full chain-of-custody reporting on carbon, solvent, and heavy-metal footprints, further reinforcing gravure’s strategic pivot toward sustainable production.

Expansion of Packaging Capacity in Emerging Asian Economies

Rising incomes and reshoring trends are spurring greenfield investments in gravure facilities across China, India, Vietnam, and Indonesia. One leading Chinese supplier now claims 70% home-market share and has exported more than 350 presses to 35 countries, proving that localized service and competitive pricing can win outside its domestic base. Indian multinationals are licensing European engineering to produce high-speed lines domestically, slashing import duties and shortening lead times from 30 weeks to 14 weeks. These moves underpin the growth of the gravure printing machines market in Asia-Pacific and drive vibrant aftermarket demand for laser-engraved cylinders, sleeve handling, and on-press viscosity control systems.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Capital Investment and Long Payback Period | -0.3% | Global, strongest for small and medium converters in emerging markets | Long term (≥ 4 years) |

| Intensifying Competition from Digital and Flexographic Printing for Short Runs | -0.3% | North America and Europe, spillover to the Asia-Pacific | Medium term (2-4 years) |

| Volatility in Copper and Chromium Prices Affecting Cylinder Costs | -0.1% | Global, with the greatest impact in the Asia-Pacific and the Middle East | Short term (≤ 2 years) |

| Skilled Operator Shortage Leading to Production Bottlenecks | -0.2% | Global, most severe in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Investment and Long Payback Period

Eight- to ten-color gravure lines with solvent recovery and color automation cost USD 3-5 million, while cylinder inventories can add another USD 500,000 for a mid-size SKU portfolio. Converters in emerging markets often struggle to secure that financing, especially when order volumes are volatile or denominated in weak local currencies. Even with automation that lowers the cost crossover to 5,000 m², payback can exceed seven years without sustained 70-80% uptime. Refurbished presses and lower-cost Chinese models partially offset capex, but they also entail higher utility bills and longer makereadies, reinforcing the dilemma for small plants seeking to enter the premium flexible packaging.[2]Labels & Labeling, “Bobst Closes Gravure Color Loop,” labelsandlabeling.com

Intensifying Competition from Digital and Flexographic Printing for Short Runs

Central-impression flexo presses with extended-gamut ink sets match gravure’s color fidelity while completing job changes in minutes instead of hours. Digital inkjet devices eliminate cylinders and enable profitable runs below 1,000 linear meters, a sweet spot that gravure cannot reach without a hybrid module. Brand owners now favor mixed-technology fleets such as gravure for metallic effects and heavy ink laydown, flexo for midsize lots, and digital for microruns or variable data. As a result, gravure press suppliers must either adopt hybrid architectures or double down on automation and special-effect capabilities to defend addressable volume, especially in North America and Europe.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Flexible Packaging Commands the Bulk of Investment

Flexible packaging accounted for 55.05% of the gravure printing machines market in 2025, and gravure’s high-opacity graphics on downgauged films remain indispensable for brand differentiation on crowded e-commerce shelves. Converters running lines between 1,050 mm and 1,250 mm have proven they can execute limited-edition drops profitably, trimming makeready from 45 minutes to under 10. The gravure printing machines market for flexible packaging continues to benefit from sustainability mandates that drive mono-material film adoption, as gravure’s controlled ink lay-down maintains intact barrier properties.[3]Innovia Films, “High-Barrier BOPP Films for Flexible Packaging,” innoviafilms.com

Industrial and security printing is projected to expand at a 1.65% CAGR through 2031, outpacing all other uses. Pharmaceutical serialization laws and luxury goods’ anti-counterfeiting requirements demand micro-engraved cylinders capable of sub-10 µm line widths, a feat beyond the capabilities of flexographic or digital methods. Converters serving these sectors invest in inline inspection cameras and closed-loop register control, ensuring production at 300 m/min without compromising code legibility. Publication gravure, by contrast, slipped below 8% of 2025 volume as magazines migrate to web offset, confirming a long-term secular decline.

By Substrate Type: Metallic Foils Graduate From Niche to Growth Engine

Plastic films held 60.23% of the 2025 volume, but rising preferences for gold, silver, and bronze finishes in premium spirits and cosmetics are propelling metallic foils at a 1.77% CAGR. Extended-gamut workflows now replicate metallics without spot cylinders, slashing solvent use and setup time. The gravure printing machines market share for foils is therefore climbing as converters realize they can deliver luxury effects while meeting EU recycling criteria.

Meanwhile, paper and paperboard maintain a steady share of approximately 22% of the market, primarily driven by their use in tobacco packaging and gift wrap applications. These applications continue to favor gravure printing for its ability to deliver a thick ink layer and a tactile, glossy finish that enhances the visual appeal of the final product. On the other hand, specialty laminates, which account for about 5% of total volume, are predominantly used in automotive and furniture décor films. In these segments, the demand for high-quality wood-grain fidelity ensures that gravure printing remains a preferred choice, even with relatively small production runs.

By Printing Speed Class: Productivity Race Above 350 m/min

Presses running 201-350 m/min captured 45.38% of 2025 installs because they balance energy use, web tension, and maintenance complexity. Yet converters chasing lower cost per unit on long runs are migrating toward platforms above 350 m/min, lifting that speed class at a 1.19% CAGR. A 500 m/min shaftless line introduced in 2026 exemplifies this, as its trolley-based cylinder exchange completes changeovers in 8 minutes, enabling 20-hour daily utilization and faster ROI.

Presses operating below 200 m/min continue to serve niche applications such as décor and security work, where intricate pattern repeats and frequent color changes take precedence over higher speeds. These presses are particularly valued in scenarios where precision and customization are critical. To address evolving market demands, vendors are strategically positioning mid-speed models with energy-saving features. This approach not only enhances the sustainability of these presses but also ensures their competitiveness against ultra-high-speed flagship models. Additionally, these mid-speed presses help maintain converters' operational efficiency and uptime, especially in developing regions where cost-effectiveness and reliability remain key priorities.

Geography Analysis

Asia-Pacific accounted for 42.16% of the gravure printing machines market revenue in 2025. Chinese manufacturers dominate domestic demand and increasingly win orders abroad through competitive pricing, localized parts networks, and faster commissioning cycles. India’s packaging majors are ramping up domestic press build under technology-transfer licenses, shrinking lead times to 14 weeks, and cutting duty exposure. Southeast Asian nations, Vietnam, Thailand, and Indonesia, benefit from multinationals’ China-plus-one strategies, driving greenfield installations of 200-350 m/min lines tuned for aseptic pouches and retort applications.[4]Fuji Kikai Kogyo Co Ltd, “Rotogravure and Metal Decorating Machines,” fujikikai.co.jp

The Middle East is the fastest-growing region, with a 1.97% CAGR through 2031, as Gulf Cooperation Council states diversify into value-added packaging. However, many plants are swapping mid-run gravure work for central-impression flexo, seeking faster turnarounds for goods bound to regional supermarkets. Europe commands about 28% of value, but aging assets must now meet VOC caps and chrome-free mandates, creating retrofit demand for solvent capture and trivalent plating. North America holds a notable share, where consolidation among flexible-packaging converters fuels interest in hybrid gravure-digital architectures compliant with serialization laws.

South America contributes a notable share of revenue, led by Brazilian converters upgrading to Chinese mid-speed lines as currency volatility discourages European imports. Argentina prolongs equipment life through retrofits rather than new buys, dampening volume growth. Africa, at about 5%, remains fragmented; South Africa and Egypt anchor most installs, while the rest of the continent awaits retail formalization and logistics upgrades that justify branded printed packs.

Competitive Landscape

The market is moderately concentrated, with European leaders Bobst, Windmöller and Hölscher, and Uteco each holding mid-teens market share, but facing pressure from Chinese challengers such as Shaanxi Beiren, Weifang Donghang, and Jiangyin Lida. The latter group captures mid-tier volume by offering 30-40% price discounts and local service crews. Bobst counters with Industry 4.0-ready lines that halve operator count and have earned Pantone certification for extended-gamut workflows. Windmöller and Hölscher leverages solvent-recovery alliances to deliver 80% energy savings, turning environmental compliance into a sales differentiator.

Koenig and Bauer firmly establishes itself as a leader in the security-printing niche, showcasing a significant order backlog of EUR 1,032.8 million (USD 1,165 million) in Q1 2025. This growth is primarily attributed to strong demand from banknote and pharmaceutical contracts, which continue to drive the company's performance. Meanwhile, hybrid printing platforms are becoming a critical area of competition within the industry. Uteco’s innovative gravure-inkjet combination technology efficiently directs solid fills to cylinders while assigning variable data to inkjet heads. This approach significantly reduces the cost per impression, particularly for mixed SKUs, making it a cost-effective solution for diverse printing requirements.[5]Uteco Converting SpA, “OnyxOmnia Hybrid Press Platform,” uteco.com

Chinese entrants now offer 500 m/min presses at prices below USD 2 million, creating significant competitive pressure on established players. This competition has compelled incumbents to accelerate the integration of advanced features, such as energy-saving technologies and automated cylinder handling, secured, to maintain their premium pricing strategies. Despite losing bids for new press installations, European suppliers have secured consistent aftermarket revenue streams by providing retrofitting solutions. These include upgrades for trivalent chrome plating, energy-efficient ovens, and viscosity control systems, which ensure long-term customer retention and recurring income.

Gravure Printing Machines Industry Leaders

Bobst Group SA

Windmöller & Hölscher KG

Uteco Converting S.p.A.

Shaanxi Beiren Printing Machinery Co., Ltd.

Comexi Group Industries SAU

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Windmöller and Hölscher showcased gravure capability on post-consumer-recycled and mono-material polyethylene webs to meet forthcoming EU recycled-content mandates.

- March 2026: ContiTech, a division of Continental, has rolled out a new gravure printing machine tailored for the furniture and building components industries.

- February 2026: UFlex launched the Ceruflex 500 shaftless high-speed press, built under an exclusive license with an Italian technology partner, for the Indian and export markets.

- April 2025: Koenig and Bauer formed Kyana, a Google-Cloud-enabled design and workflow platform, integrating digital services with its gravure hardware portfolio.

Global Gravure Printing Machines Market Report Scope

The Gravure Printing Machines Market refers to the global industry that manufactures, distributes, and sells gravure printing equipment for high-speed, high-volume printing applications across the packaging, publishing, decorative, and industrial sectors. Gravure printing machines use engraved cylinders to transfer ink onto various substrates, enabling consistent image quality, precise color reproduction, and efficient long-run production. These machines are widely utilized for printing on flexible packaging materials, labels, paper products, metallic foils, and specialty substrates where durability, print clarity, and production efficiency are critical.

The Gravure Printing Machines Market Report is Segmented by Application (Flexible Packaging, Label Manufacturing, Publication and Commercial Printing, Decorative Printing, and Industrial and Security Printing), Substrate Type (Plastic Films, Paper and Paperboard, Metallic Foils, and Other Substrate Types), Printing Speed Class (Up to 200 m/min, 201-350 m/min, and More than 350 m/min), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Flexible Packaging |

| Label Manufacturing |

| Publication and Commercial Printing |

| Decorative Printing |

| Industrial and Security Printing |

| Plastic Films |

| Paper and Paperboard |

| Metallic Foils |

| Others (Textiles, Laminates) |

| Up to 200 m/min |

| 201-350 m/min |

| More than 350 m/min |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Application | Flexible Packaging | |

| Label Manufacturing | ||

| Publication and Commercial Printing | ||

| Decorative Printing | ||

| Industrial and Security Printing | ||

| By Substrate Type | Plastic Films | |

| Paper and Paperboard | ||

| Metallic Foils | ||

| Others (Textiles, Laminates) | ||

| By Printing Speed Class | Up to 200 m/min | |

| 201-350 m/min | ||

| More than 350 m/min | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast gravure printing machines market size?

The gravure printing machines market size is projected to rise from USD 3.46 billion in 2026 to USD 3.67 billion by 2031 at a 1.17% CAGR, according to Mordor Intelligence.

Which application segment is growing fastest in gravure printing?

Industrial and security printing leads growth at a 1.65% CAGR because pharmaceutical and luxury-goods brands require micro-engraved security elements.

Why are metallic foils gaining share in gravure printing?

Luxury spirits and cosmetics brands now replicate gold, silver, and bronze tones through extended-gamut workflows, driving metallic foil usage at a 1.77% CAGR.

How are regulations influencing gravure press design?

EU VOC and chrome-free mandates are pushing converters toward trivalent plating, closed-loop solvent capture, and energy-efficient dryers, prompting press manufacturers to embed these features natively.

Which substrate type holds the highest share in the gravure printing machines market?

Plastic films held the leading market share of 60.23% in 2025, supported by their extensive use in flexible packaging applications requiring high-quality and durable print performance.

Page last updated on: