Rapid Liquid Printing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

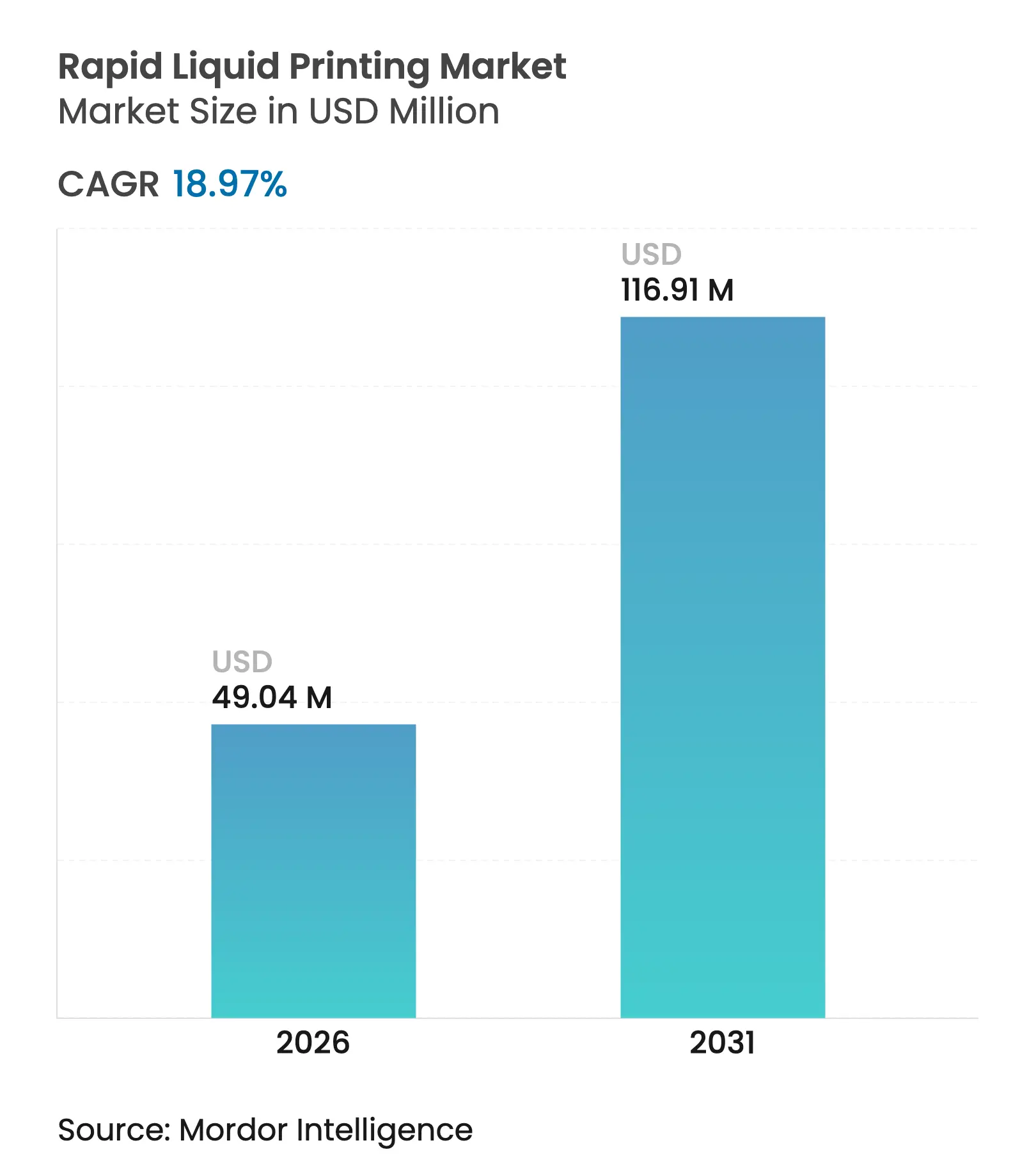

| Market Size (2026) | USD 49.04 Million |

| Market Size (2031) | USD 116.91 Million |

| Growth Rate (2026 - 2031) | 18.97 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Rapid Liquid Printing Market Analysis by Mordor Intelligence

The rapid liquid printing market size in 2026 is estimated at USD 49.04 million, growing from 2025 value of USD 41.22 million with 2031 projections showing USD 116.91 million, growing at 18.97% CAGR over 2026-2031. The technology prints objects inside a thermoreversible gel, bypassing the layer-by-layer constraint and enabling complex channels, overhangs, and meter-scale parts in a single uninterrupted pass. Early adoption in automotive and healthcare illustrates how ultra-fast cycle times and geometry freedom compress both product development and production lead times. Printers remain the primary revenue engine as OEMs retrofit lines for short-run interior panels and surgical devices, yet AI-driven software is emerging as the critical enabler for quality control, yield, and gel-flow efficiency. The expanding palette of industrial silicones, elastomers, and liquid metals moves the technology beyond prototyping toward durable, end-use components that rival injection-molded equivalents. Venture funding, led by major automakers and aerospace primes, underscores confidence that rapid liquid printing will unlock profitable mass-customization in high-value sectors.

Key Report Takeaways

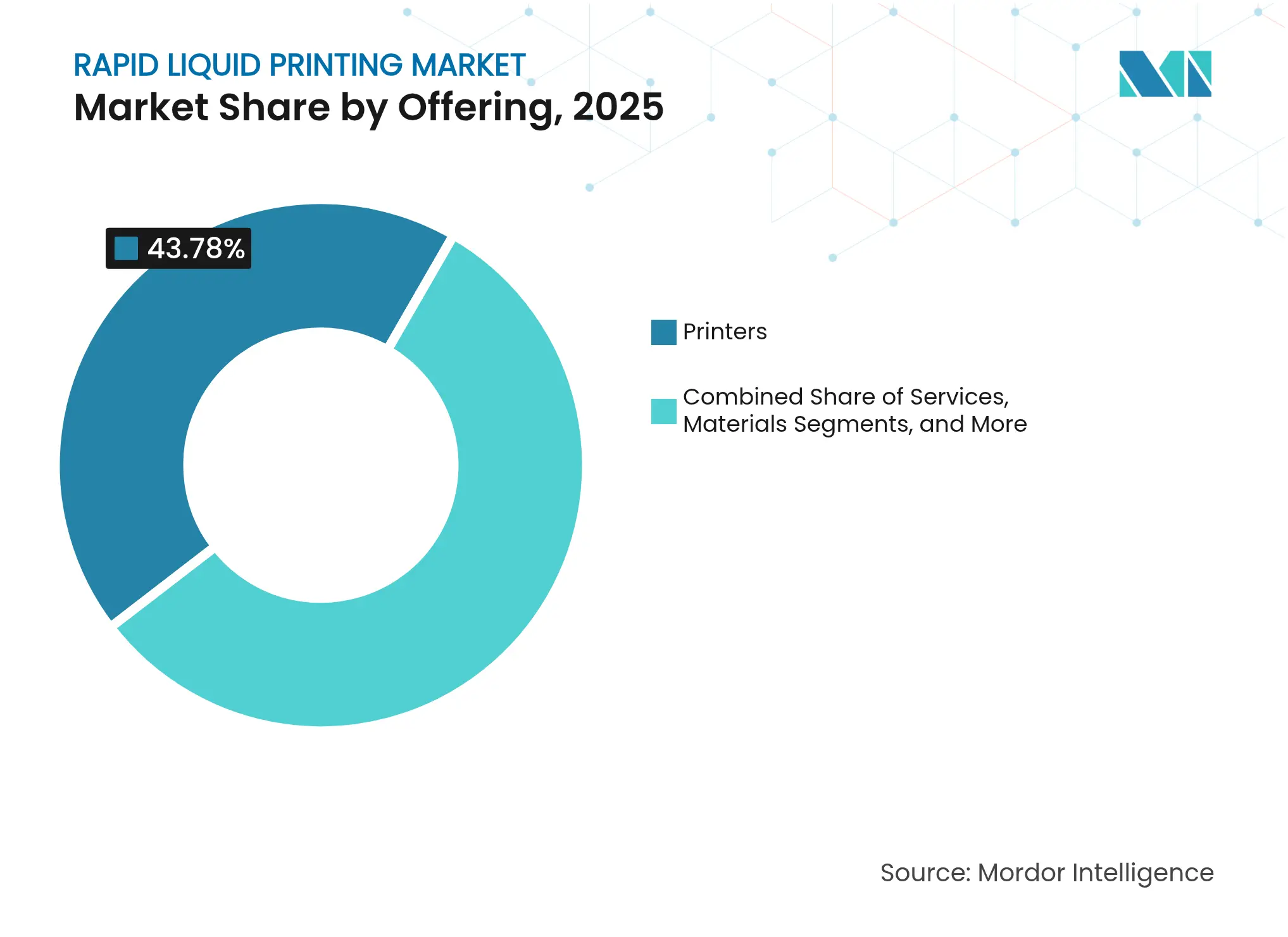

- By offering, printers held 43.78% of rapid liquid printing market share in 2025, while software is forecast to climb at 22.18% CAGR to 2031.

- By application, prototyping led with 47.85% revenue share in 2025; functional part manufacturing is advancing at a 22.61% CAGR through 2031.

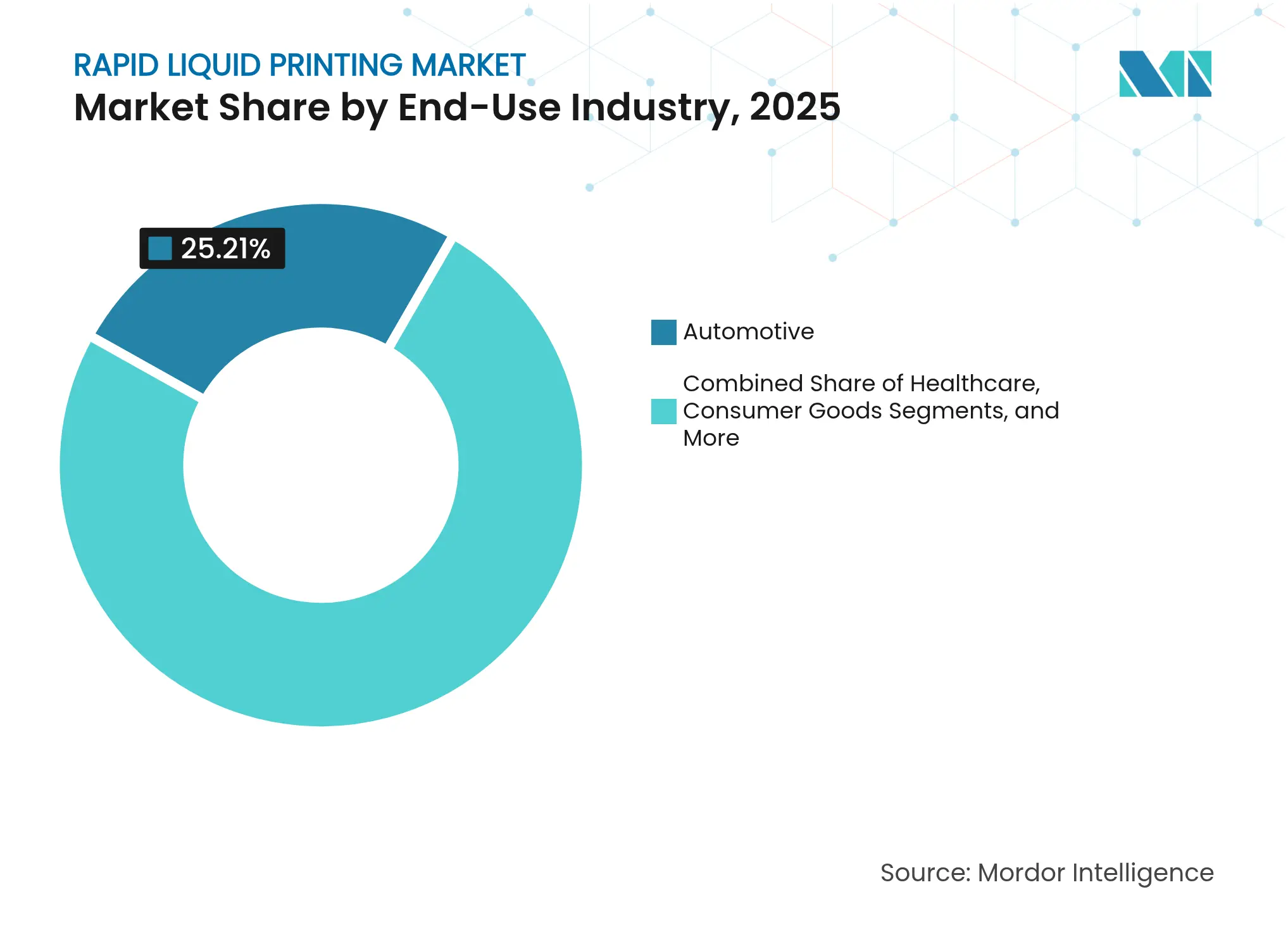

- By end-use industry, automotive captured 25.21% of rapid liquid printing market size in 2025; healthcare records the fastest 21.55% CAGR to 2031.

- By material type, photopolymer resins accounted for 57.92% share of the rapid liquid printing market in 2025, whereas metals and alloys expand at 22.47% CAGR through 2031.

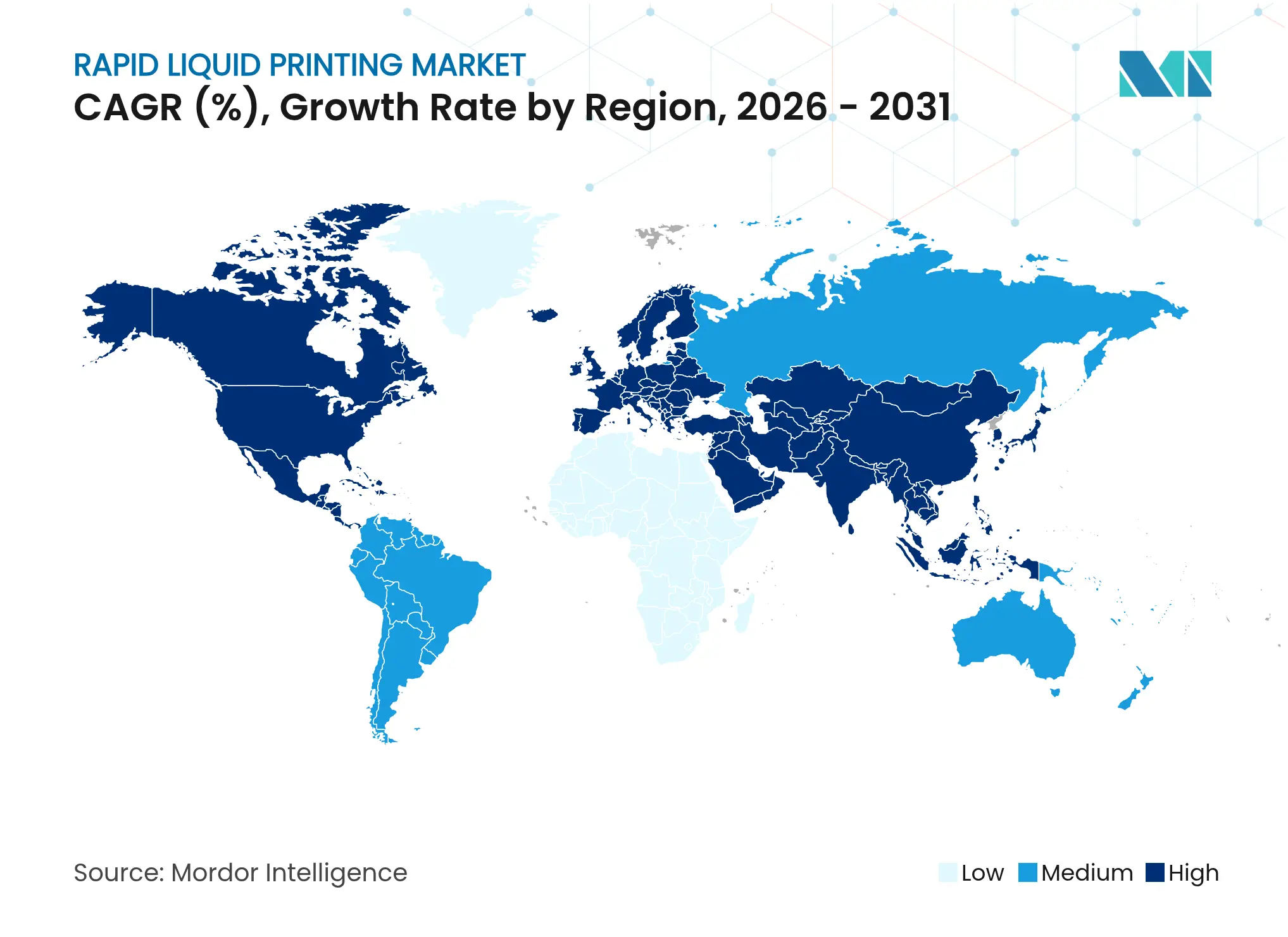

- By geography, North America dominated with 34.12% share in 2025; Asia-Pacific is the fastest-growing region at 22.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Rapid Liquid Printing Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Ultra-fast production cycles for large-format parts Ultra-fast production cycles for large-format parts | +4.2% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:+4.2% |

Geographic Relevance

:Global, with concentration in North America & Europe |

Impact Timeline

:Medium term (2-4 years) |

Industrial-grade elastomers and silicones broaden use-cases Industrial-grade elastomers and silicones broaden use-cases | +3.8% | North America & APAC core, spill-over to Europe | Long term (≥ 4 years) | |||

Surge in custom automotive interiors and lightweight parts Surge in custom automotive interiors and lightweight parts | +3.5% | Global, early gains in North America, Germany, Japan | Medium term (2-4 years) | |||

Expanding medical adoption for patient-specific devices Expanding medical adoption for patient-specific devices | +3.1% | North America & Europe, emerging in APAC | Long term (≥ 4 years) | |||

AI-enabled real-time tool-path optimization AI-enabled real-time tool-path optimization | +2.4% | Global, with early adoption in North America | Short term (≤ 2 years) | |||

ESG-driven shift to solvent-free gel matrices ESG-driven shift to solvent-free gel matrices | +2.1% | Europe & North America, expanding to APAC | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Ultra-fast production cycles for large-format parts

Printing inside a gel bath removes the sequential layer build, enabling prints that are 10–100 times faster than fused-filament or photopolymer methods for components exceeding 1 m in any axis. Washington State University showed that AI path-planning cuts another 35% from cycle time while holding ±0.1 mm accuracy. Multiple objects can share the same gel volume, pushing throughput high enough for limited-series dashboards, spoiler skins, or prosthetic sockets. BMW’s pilot line reduced interior trim lead time from weeks to hours by eliminating tooling and curing stages. Capacity gains translate directly into lower per-unit cost for low-to-mid volumes, a sweet spot traditional molding cannot reach.

Industrial-grade elastomers and silicones broaden use-cases

Silicone and high-durometer TPU keep their thermal stability and chemical resistance after gel-suspension printing, opening pathways for under-hood gaskets, flexible connectors, and acoustic dampers. Sika Automotive shortened acoustic baffle development from 4–8 weeks to 2–5 days by printing proprietary elastomers that self-support within the gel and cure without warping. Covestro’s conductive TPU films demonstrate integration of heating elements directly into sunroof shades, merging multiple parts into a single print.[1]Covestro, “Concept Car Sunroof Shade,” solutions.covestro.comThe ability to program material gradients inside a single elastomer piece widens adoption in footwear and wearable devices where comfort zones vary across the geometry.

Surge in custom automotive interiors and lightweight parts

General Motors installed more than 130 printed components in the Cadillac Celestiq, including its largest metal steering-wheel core, proving the feasibility of additive production in luxury series. 9T Labs achieved a 67% weight cut in brackets using continuous carbon-fiber infill while trimming lifetime CO₂ by 47%. Rapid liquid printing brings similar design latitude to elastomeric and metal parts that require deep undercuts or lattice reinforcement, allowing automakers to hit weight and personalization targets without delaying launch schedules.

Expanding medical adoption for patient-specific devices

The technology supports variable-density structures and porous scaffolds conducive to osseointegration. 3D-printed orthoses are projected to double from USD 289.49 million in 2023 to USD 587.19 million by 2030, pointing to strong demand for bespoke medical hardware. Abbott uses additive processes to accelerate diagnostic device iterations while retaining FDA design-history files. Surgical guides tailored to each patient reduce theater time and improve alignment outcomes, validating premium pricing for hospitals.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High capital expenditure for printers

High capital expenditure for printers

| −2.8% | Global, acute in emerging economies | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

−2.8%

|

Geographic Relevance

:

Global, acute in emerging economies

|

Impact Timeline

:

Medium term (2-4 years)

|

Limited catalogue of standardized materials

Limited catalogue of standardized materials

| −2.3% | Global, especially in regulated sectors | Long term (≥ 4 years) | |||

Health risks from aerosolized gel micro-drops

Health risks from aerosolized gel micro-drops

| −1.9% | Europe, North America | Short term (≤ 2 years) | |||

IP leakage from unsecured file sharing

IP leakage from unsecured file sharing

| −1.4% | Defense, aerospace value chains | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

High capital expenditure for proprietary printers

Industrial rapid liquid printing systems range from USD 20,000 to more than USD 1 million, a hurdle for small manufacturers whose ROI relies on sporadic custom jobs.[2]Unionfab, “How Much Does It Cost to 3D Print Something (2024)?,” unionfab.com Recent tariffs lifted prices of China-sourced hardware by up to 145% and lengthened delivery cycles, lowering the tech’s appeal for cost-sensitive buyers. Service bureaus are emerging as a bridge, offering print capacity on demand so users can evaluate the process without heavy capex.

Limited catalogue of standardized printable materials

Few chemistries are certified under aerospace, automotive, or medical standards, so engineers struggle to qualify parts that must last decades or withstand corrosive fluids. Specialized metal powders cost USD 300–1,000 per kg, and each new alloy demands fresh print-parameter discovery and fatigue testing. Purdue University’s 900 MPa aluminum variant shows progress, but data sets remain thin for long-term creep or crack growth. Standard bodies are drafting methods tailored to gel suspension, yet until they finalize protocols, adoption in safety-critical parts will proceed cautiously.

Segment Analysis

By Offering: Software ignites digital transformation

Printers anchored 43.78% of rapid liquid printing market share in 2025 as OEMs installed large-volume cells for automotive consoles and orthopedic shells. The segment benefits from recurring consumable sales and service contracts that lock users into proprietary gel formulas. Software, however, posts the quickest 22.18% CAGR through 2031. Multi-objective Bayesian solvers adapt tool paths in real time, shrinking scrap by 30% and elevating surface accuracy, thereby justifying premium licenses.

Service providers represent a rising slice as integrators help calibrate print parameters for elastomer blends and metallic suspensions. Materials growth remains tied to supplier capacity and geopolitics, with photopolymer resins widely available while custom TPU and liquid metal blends carry longer lead times. Integration of cloud MES platforms is also advancing, linking printer data to enterprise resource planning, and further embedding software into the production stack. These developments ensure the rapid liquid printing market continues shifting from hardware-centric to software-orchestrated ecosystems. The rapid liquid printing industry therefore pivots toward data-driven value capture rather than unit sales of machines.

Note: Segment shares of all individual segments available upon report purchase

By Application: Functional manufacturing gathers speed

Prototyping held 47.85% of revenue in 2025, yet functional manufacturing accelerates at 22.61% CAGR, signaling confidence in repeatable quality and isotropic properties. Automakers use rapid liquid printing to eliminate soft tools for runs under 5,000 units, slashing program launch costs. Medical OEMs rely on the process for porous implants that match patient CT scans, reducing revision surgeries and postoperative stays.

Tooling applications gain traction as conformal cooling channels decrease injection-mold cycle times by up to 30%, offsetting the higher metal powder price. Decorative consumer goods such as footwear midsoles and fashion accessories validate the process at scale through brands seeking individualized aesthetics. The rapid liquid printing market thus transitions from a design-verification instrument to a short-run production resource, expanding its revenue pool beyond engineering departments. The rapid liquid printing industry enjoys wider executive-level sponsorship as business cases shift from cost-avoidance to revenue generation.

By End-Use Industry: Healthcare accelerates adoption

Automotive captured 25.21% of rapid liquid printing market size in 2025, reflecting both prototyping and rising content in premium electric vehicles. Custom interiors, vent bezels, and lightweight support brackets illustrate where subtractive machining fails to meet cost targets. Healthcare, posting 21.55% CAGR, is expected to eclipse automotive spending before 2031 as regulations codify digital workflows for patient-matched devices.

Hospitals favor in-house print labs that produce surgical guides within 24 hours of scan, bypassing external suppliers and inventory costs. Consumer goods makers exploit multi-material capability for ergonomic wearables that morph with body movement, while aerospace primes explore gel-printed titanium for weight-critical ducts. Altogether, sector diversity cushions cyclicality and underpins steady revenue expansion for the rapid liquid printing market.

Note: Segment shares of all individual segments available upon report purchase

By Material Type: Metals drive innovation

Photopolymer resins dominate with 57.92% share due to low viscosity, minimal odor, and established cure profiles. They underpin most prototypes and visual models. Metals and alloys, growing at 22.47% CAGR, unlock value for lightweight structural parts where density and yield strength are critical. MIT’s liquid-metal advances enable continuous extrusion of aluminum and copper inside the gel, removing oxidation issues that plague powder-bed fusion.

Elastomers and silicones benefit from inherent compliance, supporting seals and vibration isolators in harsh settings. Composite gels that blend chopped carbon fibers or conductive fillers broaden electromagnetic shielding and thermal-management possibilities. Efficient recycling of the carrier gel further aligns the segment with ESG mandates, reinforcing uptake across regulated markets. Consequently, material innovation propels both volume and margin expansion in the rapid liquid printing market.

Geography Analysis

North America led with 34.12% share in 2025, fueled by Detroit’s integration of more than 130 printed parts into Cadillac Celestiq production and by GE Aerospace’s USD 1 billion commitment to additive engine components. Universities such as MIT and Purdue supply talent and material breakthroughs, while the FDA’s clarified guidance on patient-matched devices accelerates hospital adoption. Canada and Mexico supplement regional momentum through cross-border automotive supply chains and defense offsets that specify domestic additive content.

Asia-Pacific records the fastest 22.66% CAGR, propelled by China’s industrial policy and Japan’s magnesium-alloy milestone, set for commercialization by 2029. Chinese print-head makers such as Bambu Lab posted CNY 1.5 billion (USD 210 million) in 2024 sales, validating local demand for consumer and industrial printers. India’s EV supply chain begins to swap machined aluminum for printed brackets, shortening model cycles in a fiercely competitive domestic market. In Australia, mining firms test gel-printed elastomer seals that withstand abrasive slurries, targeting reduced downtime on remote sites.

Europe maintains steady expansion underpinned by stringent waste-reduction mandates and premium auto brands. BMW’s additive center in Germany proves out lattice-reinforced mounts that trim curb weight without sacrificing crash integrity. France and Italy focus on luxury goods and aerospace interiors, where customization commands pricing power. Regulatory alignment on REACH and MDR shapes supplier roadmaps and reinforces traceability features in print-monitoring software, bolstering the rapid liquid printing market’s credibility among risk-averse buyers.

Competitive Landscape

Market Concentration

The rapid liquid printing market remains consolidated. Heritage players such as Stratasys and 3D Systems leverage installed bases and service networks, yet pure-play innovators capitalize on gel-suspension know-how. Rapid Liquid Print, backed by USD 7 million Series A funds from BMW i Ventures, aims to scale to automotive takt times by pairing proprietary gels with open-architecture robots.

Strategic intent centers on vertical integration. Hardware firms bundle AI path-planning suites and proprietary resin cartridges to lock in recurring revenue. Service bureaus differentiate via certifications such as AS9100 and ISO 13485, giving regulated industries a turnkey route when capital budgets tighten. Patent activity clusters around gel chemistry, anti-settling agents, and sensorized nozzles that auto-correct deposition drift, creating defensive moats.

Mergers are expected as legacy CNC and laser-cladding vendors seek entry points into high-growth additive niches. Partnerships between printer OEMs and material suppliers accelerate validation cycles, with Purdue-developed alloys licensed to powder vendors for niche aerospace contracts. Competitive intensity therefore shifts from pure hardware throughput to holistic platform performance, encompassing software, materials, and after-sales ecosystems.

Rapid Liquid Printing Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: GE Aerospace committed USD 1 billion to expand US additive manufacturing facilities focused on rapid liquid printing for engine components.

- January 2025: SpaceX debuted Raptor 3 featuring gel-printed cooling channels for mission-critical performance.

- November 2024: Makino and Fraunhofer ILT integrated EHLA3D into a five-axis CNC platform, reaching 30 m/min deposition speeds.

- November 2024: Nike launched the Air Max 1000 with Zellerfeld, showcasing consumer-grade customization via rapid liquid printing.

Table of Contents for Rapid Liquid Printing Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Ultra-fast production cycles for large-format parts

- 4.2.2Industrial-grade elastomers and silicones broaden use-cases

- 4.2.3Surge in custom automotive interiors and lightweight parts

- 4.2.4Expanding medical adoption for patient-specific devices

- 4.2.5AI-enabled real-time tool-path optimisation (under-the-radar)

- 4.2.6ESG-driven shift to solvent-free gel matrices (under-the-radar)

- 4.3Market Restraints

- 4.3.1High capital expenditure for proprietary printers

- 4.3.2Limited catalogue of standardised printable materials

- 4.3.3Health risks from aerosolised gel micro-droplets (under-the-radar)

- 4.3.4IP leakage via unsecured design file sharing (under-the-radar)

- 4.4Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter's Five Forces Analysis

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

- 4.8Recycling and Sustainability Analysis

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1By Offering

- 5.1.1Printers

- 5.1.2Services

- 5.1.3Materials

- 5.1.4Software

- 5.2By Application

- 5.2.1Prototyping

- 5.2.2Functional Part / End-Use Manufacturing

- 5.2.3Tooling

- 5.3By End-Use Industry

- 5.3.1Healthcare

- 5.3.2Consumer Goods

- 5.3.3Automotive

- 5.3.4Fashion and Accessories

- 5.3.5Electronics

- 5.3.6Other End-Use Industries

- 5.4By Material Type

- 5.4.1Elastomers and Silicones

- 5.4.2Photopolymer Resins

- 5.4.3Composite Gels

- 5.4.4Metals and Alloys (liquid metal variants)

- 5.4.5Bio-inks / Hydrogels

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Russia

- 5.5.2.7Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2India

- 5.5.3.3Japan

- 5.5.3.4South Korea

- 5.5.3.5Australia and New Zealand

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1Middle East

- 5.5.4.1.1United Arab Emirates

- 5.5.4.1.2Saudi Arabia

- 5.5.4.1.3Turkey

- 5.5.4.1.4Rest of Middle East

- 5.5.4.2Africa

- 5.5.4.2.1South Africa

- 5.5.4.2.2Nigeria

- 5.5.4.2.3Egypt

- 5.5.4.2.4Rest of Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1Stratasys Ltd.

- 6.4.23D Systems Corporation

- 6.4.3Rapid Liquid Print

- 6.4.4Dassault Systèmes SE

- 6.4.5Materialise NV

- 6.4.6Autodesk Inc.

- 6.4.7ExOne Operating LLC

- 6.4.8Steelcase Inc.

- 6.4.9GE Additive

- 6.4.10HP Inc.

- 6.4.11EOS GmbH

- 6.4.12Proto Labs Inc.

- 6.4.13Desktop Metal Inc.

- 6.4.14Carbon Inc.

- 6.4.15Formlabs Inc.

- 6.4.16Markforged Inc.

- 6.4.17SLM Solutions

- 6.4.18XJet Ltd.

- 6.4.19voxeljet AG

- 6.4.20EnvisionTEC GmbH

- 6.5Heat Map Analysis

- 6.6Competitor Analysis – Emerging vs. Established Players

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1White-space and Unmet-need Assessment

Global Rapid Liquid Printing Market Report Scope

The rapid liquid printing market is segmented by offering (Printers, Services, Materials and Software), by application (Prototyping, Functional Part/End-Use Manufacturing and Tooling), and by end-use industry (Healthcare, Consumer Goods, Automotive, Fashion & Accessories, Electronics and Other End-Use Industries) and by geography (North America, Europe, Asia Pacific, South America and Middle East and Africa). The market sizing and forecasts are provided in terms of value (USD) for all the above segments.