Gravure Printing Services Market Size and Share

Market Overview

| Study Period | 2024 - 2030 |

|---|---|

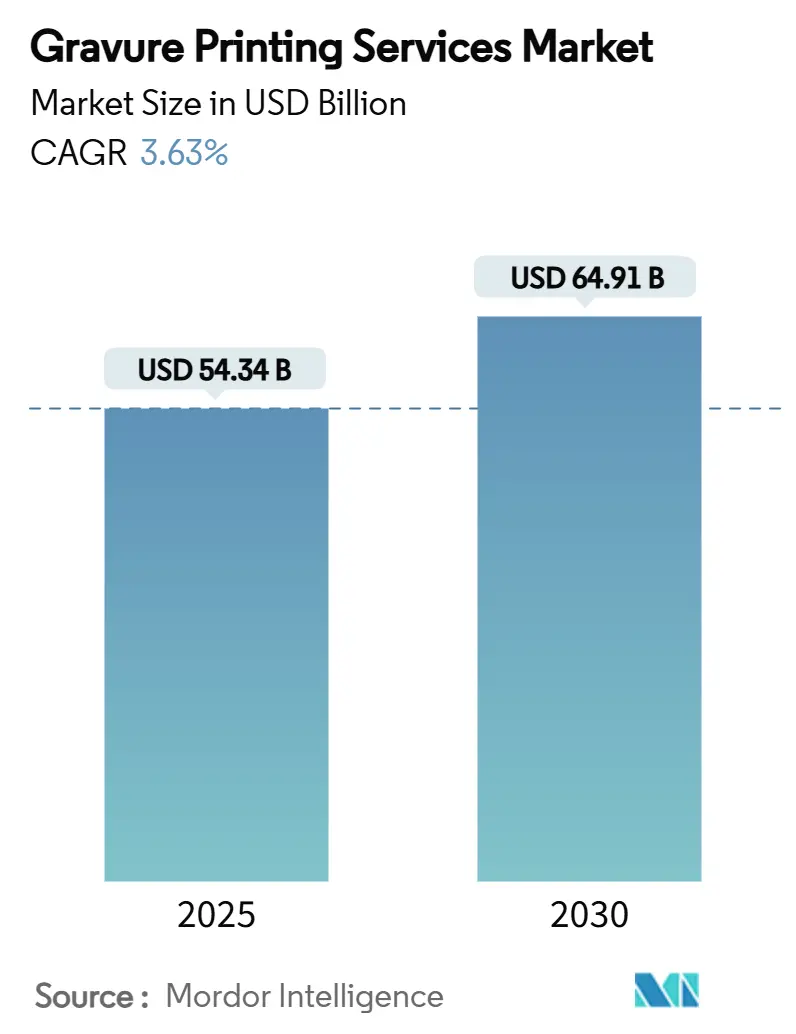

| Market Size (2025) | USD 54.34 Billion |

| Market Size (2030) | USD 64.91 Billion |

| Growth Rate (2025 - 2030) | 3.63% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gravure Printing Services Market Analysis by Mordor Intelligence

The global gravure printing services market size stands at USD 54.34 billion in 2025 and is forecast to reach USD 64.91 billion by 2030, translating into a 3.63% CAGR and reflecting steady but disciplined expansion across all major end-use segments. Rising demand for flexible packaging, accelerating adoption of mono-material substrates, and the proliferation of smart-packaging features continue to underpin revenue growth despite intensifying competition from flexographic and digital processes. Leading converters are amplifying capital spending on high-speed presses and fully digital pre-press workflows to compress job changeover times, while brand owners across premium food, beverage, and personal-care categories increasingly reward the continuous-tone image quality unique to gravure printing. Regulatory pressure to remove toluene and MEK solvents, combined with tariff uncertainty on North American imports, is forcing value-chain participants to re-engineer supply chains and retool plants, yet these same constraints are catalysing upgraded cylinder engravings, energy-efficient drying systems, and data-driven process control.[1]DNP Group, “DNP’s Mono-material Packaging,” global.dnp

Key Report Takeaways

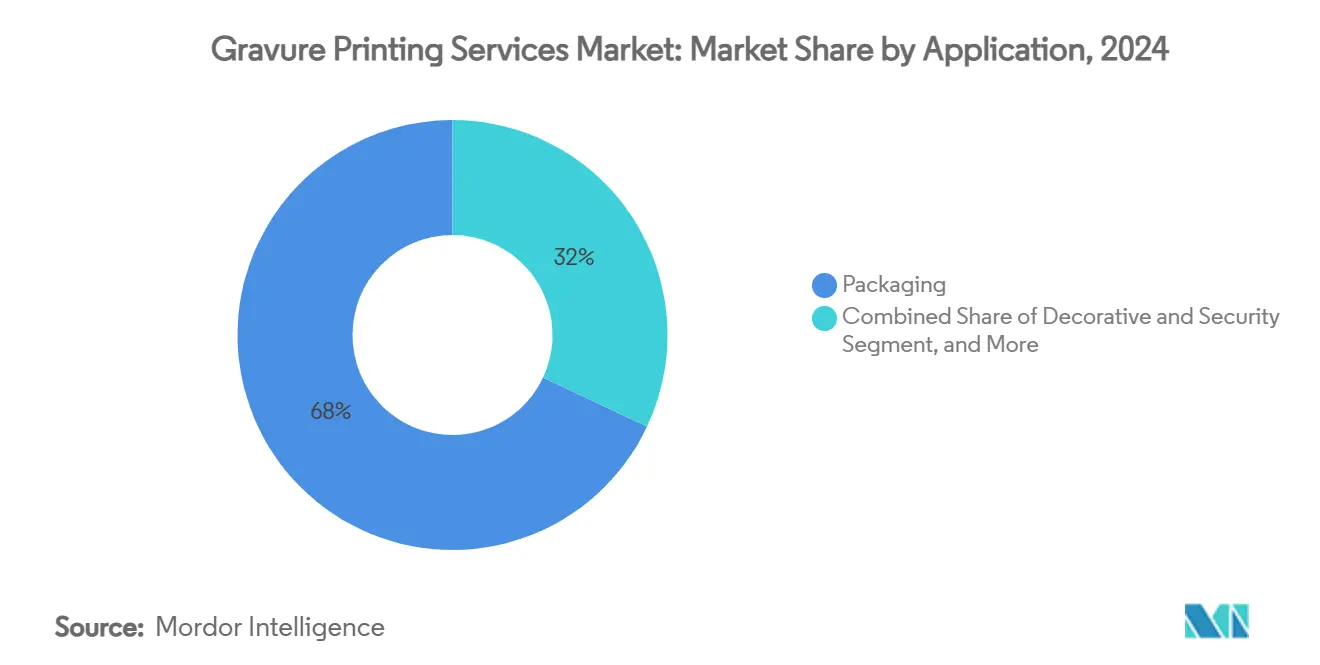

- By application, packaging led with a 68% gravure printing services market share in 2024 while functional and printed electronics is projected to grow at a 7.55% CAGR through 2030.

- By substrate, plastic film accounted for 54% of the gravure printing services market size in 2024, and the segment is advancing at a 7.80% CAGR to 2030.

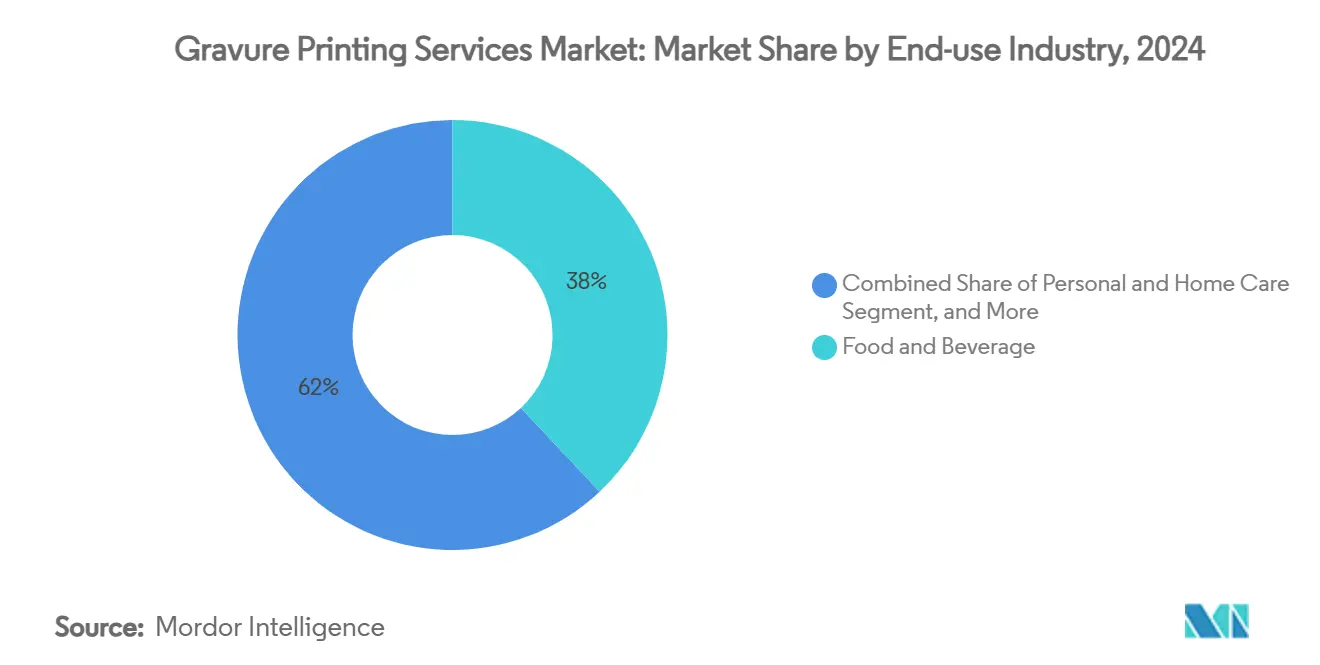

- By end-use industry, food and beverage captured 38% share of the gravure printing services market in 2024, whereas pharmaceuticals represent the fastest trajectory at 8.90% CAGR.

- By service type, printing operations held 47% revenue share in 2024, with pre-press and cylinder engraving expanding at a 7.10% CAGR over the same period.

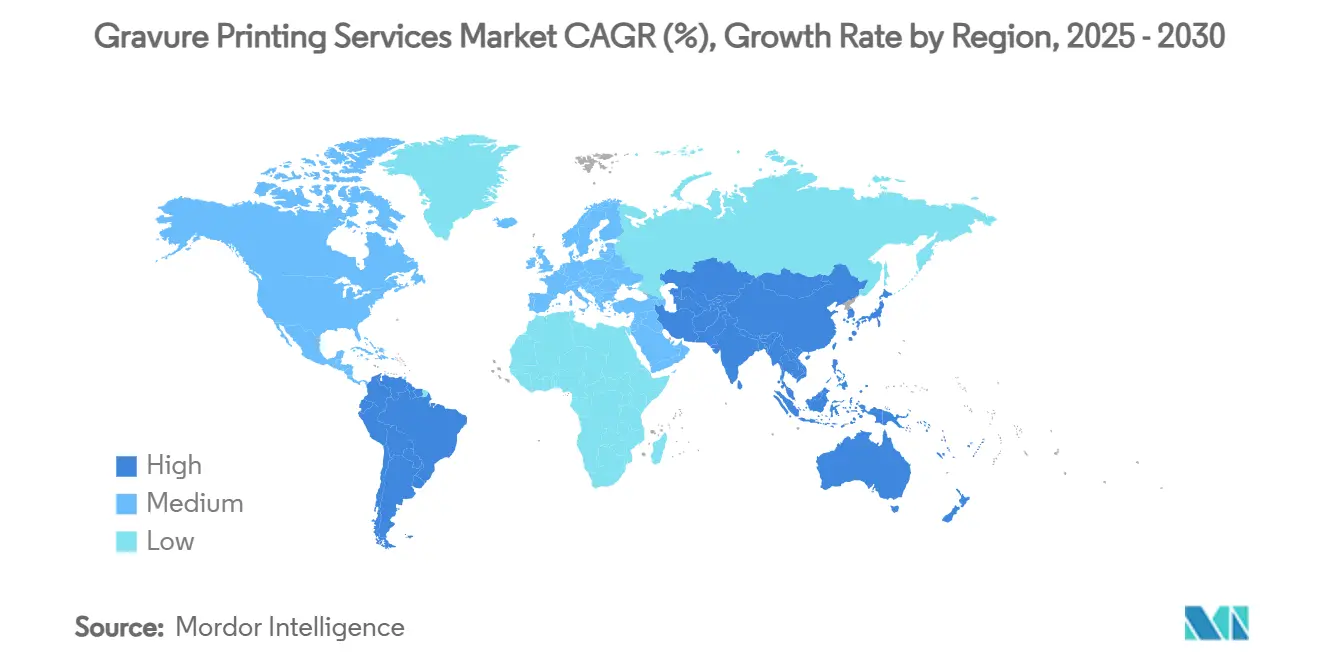

- By region, Asia-Pacific commanded 41.22% of the gravure printing services market in 2024; South America is forecast to record the highest regional growth at 7.50% CAGR to 2030.

Global Gravure Printing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward mono-material flexibles | 0.80% | Global, with early adoption in EU and North America | Medium term (2-4 years) |

| Growth of short-run SKUs in emerging Asia | 0.60% | APAC core, spill-over to MEA | Short term (≤ 2 years) |

| Brand-owner demand for photo-real graphics | 0.50% | Global, premium segments in developed markets | Medium term (2-4 years) |

| Rapid scale-up of printed electronics | 0.40% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Cylinder-as-a-Service subscription models | 0.30% | Europe and North America initially | Medium term (2-4 years) |

| EU re-industrialisation incentives | 0.20% | European Union member states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift toward mono-material flexibles

Gravure printers are repositioning their value proposition around polyethylene and polypropylene mono-material structures that comply with the European Union’s Extended Producer Responsibility rules effective in 2025. Siegwerk’s CIRKIT GreaseBar coatings preserve barrier performance on such simplified laminates while maintaining gravure’s hallmark image fidelity. Commercial uptake is strongest in Europe where recyclability scores directly influence eco-modulated fees, and early adopters are winning premium contracts that offset the costs of cylinder refurbishment and low-VOC ink qualification. With Toppan’s GL BARRIER film receiving top recyclability ratings, material suppliers and converters are jointly specifying gravure as the preferred print process for photo-real graphics on mono-material pouches. Over the next three years, mono-material adoption is forecast to lift cylinder volumes, stimulate higher-margin coating sales, and improve customer retention for service providers equipped to deliver turnkey compliance solutions.[2]Siegwerk, “Pet Food Packaging,” siegwerk.com

Growth of short-run SKUs

Consumer segmentation in India, Vietnam, and the Philippines is multiplying SKU counts and shrinking average order quantities, pushing the gravure printing services market toward agile job management. Amcor’s USD 20 million acquisition of Phoenix Flexibles secures local capacity for frequent, smaller-batch orders in India, exemplifying how multinationals are rebalancing their footprint toward high-growth APAC metros. Gravure’s historic drawback—high makeready costs—is being neutralized by faster laser-engraved cylinders that cut changeover times by up to 40%, and by modular data-driven presses that hold ±15 μm registration on repeat runs. Regional converters adopting hybrid press lines—such as Uteco’s OnyxOMNIA rated at 400 m/min—can now address unpredictable order schedules without conceding ground to flexography. This pivot is expected to reshape ordering patterns across Southeast Asia, creating fresh revenue for cylinder-as-a-service providers and digital pre-press bureaus.[3]Esko, “Esko Partners with BOBST on smartGRAVURE,” esko.com

Brand-owner demand for photo-real graphics

Luxury food, beverage, and cosmetics brands are willing to pay premiums of 12–15% for fully saturated, continuous-tone imagery that only gravure presently achieves at scale. The Esko-BOBST smartGRAVURE workflow halves colour-matching time while delivering 94.6% Delta-E accuracy, a metric that directly translates into lower waste and tighter on-shelf brand consistency. Hell Gravure Systems’ HelioKlischograph K500 further accelerates market response by engraving cylinders at 24 kHz, enabling same-shift deployment on urgent promotions. Demand for high-definition, tactile varnish effects within a single pass is rising in premium pet food, coffee, and impulse confectionery packaging, reinforcing gravure’s relevance in a landscape crowded with digital and flexo alternatives.

Rapid scale-up of printed electronics

Driven by IoT adoption, gravure printing now supports transparent conductive films exceeding 95% light transmittance at line resistances of 32 Ω mm-1, suitable for touch sensors and flexible displays. Kodak Alaris leverages long-format gravure for battery electrodes and solar back-sheets where uniform coating thickness is critical. Pilot lines in Germany and the United States are scaling from 0.5 m to 1.4 m web widths, broadening the addressable market to include RFID antennas and smart-label circuits. The expansion reinforces gravure’s unique position at the intersection of high-precision material deposition and industrial-speed roll-to-roll manufacturing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Toluene & MEK solvent phase-out | -0.70% | Global, with strictest enforcement in EU and North America | Short term (≤ 2 years) |

| Shrinking publication volumes | -0.50% | Global, most pronounced in developed markets | Medium term (2-4 years) |

| Flexo & digital price competition | -0.40% | Global, particularly in short-run applications | Medium term (2-4 years) |

| Skilled-operator shortages | -0.30% | Developed markets, emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Toluene and MEK solvent phase-out

Regulators are tightening volatile organic compound thresholds, compelling printers to swap legacy solvent-based formulations for water-based or UV-curable chemistries. France’s mineral-oil ban and the U.S. EPA’s 8% monthly HAP ceiling for publication gravure are the strictest directives currently in force. Compliance requires retrofitting ovens, reclaim systems, and explosion-proof ventilation—capital outlays that erode price competitiveness against flexography. Early adopters in Scandinavia have reported energy-use reductions of 22% yet note a 4-6% cure-speed penalty that limits web velocity, underscoring the transitional frictions that weigh on gravure’s near-term topline.

Shrinking publication volumes

Magazine and catalogue runs have fallen double digits since 2020 as advertisers pivot to digital channels, stripping gravure of the long runs that historically subsidized cylinder amortization. European presses formerly dedicated to Sunday inserts are being idled or converted to flexible-packaging work, incurring retraining costs and layout re-engineering. Although niche illustration books and high-end fashion titles still value gravure’s continuous-tone imagery, the secular decline squeezes capacity utilization rates and accelerates consolidation among publication specialists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Packaging Dominance Drives Innovation

Packaging reached a 68% gravure printing services market share in 2024 and remains the backbone of revenue generation, particularly across food, beverage, and pet-food pouches that demand high colour lay-down and robust migration compliance. Brand diversification into local flavours and seasonal limited editions translates into more changeovers per press, prompting converters to invest in automated sleeve loading, closed-loop viscosity control, and augmented-reality maintenance guides. Functional and printed electronics, although less than 5% of 2024 revenue, is pacing the field with a 7.55% CAGR to 2030. The gravure printing services market size for this segment is projected to more than double within the forecast horizon as costs per square meter of printed antenna fall and smart-label mandates proliferate in supply-chain monitoring and cold-chain integrity. Publication work continues its structural retreat, yet opportunistic print-on-demand catalogue runs still exploit gravure’s ability to maintain 1.2 g/m² ink lay-down uniformity across 96-page signatures.

Packaging’s premium tier is increasingly specified around photo-real graphics and micro-embossed brand seals, both of which favour gravure over flexography. Uteco’s hybrid presses allow sequential gravure and water-based flexo application in a single pass, thereby marrying halftone vibrancy with tactile spot varnish for luxury confectionery wraps. Meanwhile, the functional printing ecosystem is developing standardized design rules for line spacing, ink rheology, and substrate topography, enabling brand owners to tender printed electronics volumes at scale. Printed capacitor films for cosmetic facemask warming sachets and tamper-evident vape-pod labels exemplify early commercial wins that demonstrate gravure’s advantage in uniform ink-thickness control and low-resistance line formation.

By Substrate: Plastic Film Leadership Amid Sustainability Pressures

Plastic films accounted for 54% of the gravure printing services market size in 2024, buoyed by advancements in barrier coatings, antimicrobial varnishes, and downgauged multilayer structures that cut polymer consumption by up to 18%. Clear-on-clear polypropylene laminates with oxygen-scavenger coatings are gaining share in snacks and coffee applications, as they deliver extended shelf life while supporting in-pack nitrogen flushing. Paper, once the mainstay of mid-tier chocolate wrappers, is ceding volume but preserving niche growth in luxury spirits cartons where tactile coatings and raised metallic effects elevate shelf presence. Aluminium foil retains a defensible footprint in blister packs and premium meat paté lids, where gravure’s pinhole-free ink transfer ensures barrier integrity.

Circular-economy mandates are accelerating collaboration between substrate chemists and cylinder engravers. Grounded Packaging’s bio-based vacuum pouches incorporate up to 70% plant material without compromising web flatness, proving compatible with standard gravure dryers at 130 °C setpoints. Avery Dennison’s Global MDO film achieves >60% clarity gain while trimming fossil-fuel use and water consumption by 22%, allowing brand owners to shrink label gauge without sacrificing on-shelf aesthetics. For gravure printers, the substrate shift necessitates recalibrated doctor-blade angles and redesigned ink feed circuits to manage lower surface energy values.

By End-use Industry: Food and Beverage Leads Pharmaceutical Surge

Food and beverage captured 38% of gravure printing services market revenue in 2024 as pet-food pouches, stand-up snack bags, and specialty coffee liners all demand high-definition images and potent aroma and moisture barriers. Fully recyclable mono-material snack films are now commercialized with drop-in printing at 120 line/cm screen counts, and photo-chromic inks are being trailed for brand engagement campaigns in carbonated beverages. Pharmaceuticals, though representing a smaller base, is forecast to register an 8.90% CAGR to 2030 on the back of anti-counterfeit mandates, unit-dose expansion, and high-opacity white coverage for serialisation areas. The gravure printing services market share of pharmaceutical applications is thus expected to climb measurably, rewarding converters capable of meeting ISO 15378 GMP guidelines.

Personal and home care blends premiumization and functional labelling, requiring metallic varnish on shampoo sachets and micro-text security scripts for razor-blade cartons. While tobacco volumes face legislative constraint, flavoured cigarillo sleeves retain investment in gravure cylinders that can reproduce holographic tip designs unattainable by digital print at required speeds. Industrial and other markets, including printable sensor films for automotive interiors, are forecast to pivot toward gravure as safety standards call for consistent line width and resistance values over large surface areas.

By Service Type: Pre-press Innovation Accelerates Growth

Printing operations maintained a 47% market share in 2024, reflecting gravure’s historic dependence on high-volume runs where cylinder cost amortization is favourable. However, pre-press and cylinder engraving is the service tier posting the fastest 7.10% CAGR through 2030 as laser engraving resolution now reaches 5,080 dpi and integrated inspection heads correct cell geometry in situ. The gravure printing services market size attached to these preparatory workflows is swelling as converters outsource cylinder management to subscription programs that bundle storage, clean-down, and revision engraving within a monthly fee. Hell Gravure’s K500 platform, paired with AI-enhanced cell-depth algorithms, slashes lead times from 48 hours to 10 hours for image-ready cylinders, enabling converters to meet the surging micro-batch demand of brand portfolios.

Finishing and lamination continues to advance as mono-material barriers rely on solvent-free adhesive systems applied in tandem with inline gravure stations. Dual-cure cold-seal varnishes are capturing confectionery and ice-cream pack work that historically defaulted to off-line coaters, trimming supply-chain touches and speeding product launch cycles. This shift magnifies the strategic relevance of full-service gravure providers that can offer cradle-to-gate expertise spanning design, cylinder production, printing, and lamination under one roof.

Geography Analysis

Asia-Pacific retained a dominant 41.22% gravure printing services market share in 2024, anchored by China’s scale, India’s consumption growth, and Southeast Asia’s energetic contract-packing sector. Chinese converters are increasing dwell times on tobacco and snack lines to comply with updated GB 9685 additive standards, fuelling capex on new inline viscosity control to offset slower web speeds. Indian packaging groups, supported by Production-Linked Incentive schemes, are adding ten-colour gravure presses to service the rapid proliferation of regional SKUs in savoury snacks and personal-care sachets. Vietnam and Indonesia, benefiting from tariff shifts, are attracting European brand owners eager to localize sourcing amid North American trade frictions.

Europe, while a mature consumer base, is reinforcing its gravure footprint through technology leadership and stringent sustainability mandates. German and Italian engineering clusters are rolling out retrofit kits that reclaim solvent flash for closed-loop feed, lowering VOC emissions by 35% and ensuring compliance with EU chemical strategy targets. EU re-industrialization grants covering up to 20% of capex on low-energy presses are accelerating replacement cycles, contributing to incremental volume diversification toward mono-material laminates produced on gravure lines. National brands in France and the Netherlands are specifying Toppan’s GL BARRIER film in cheese and deli wraps for recyclability scores, thereby funnelling higher-margin jobs into European gravure halls.

South America is charting a 7.50% CAGR, the highest regional pace, with Brazil’s agricultural boom fuelling packaging demand for coffee, sugar, and meat exports. Local players like Fotograv are scaling platemaking output by 25% YoY to service both flexographic and gravure clients, signalling a rising tide of demand for high-resolution cylinders. Argentina’s peso stabilization program is unlocking investment in press retrofits that align with export packaging standards for whole-muscle beef and dairy powders.

North America encounters headwinds from tariff levies-25% on Canadian and Mexican flexible imports and 10% on Chinese cylinders-forcing OEMs to reconsider sourcing lanes and triggering onshoring investments in the United States Midwest. Converters are hedging cost risk by dual-qualifying component suppliers and exploring cylinder-as-a-service contracts to cap capex exposure. The Middle East and Africa remains an early-stage growth story, constrained by political instability in key markets yet buoyed by rising demand for printed electronics in smart irrigation sensors.[4]Fotograv, “Clicheria Fotograv,” fotograv.com.br

Competitive Landscape

The gravure printing services market is moderately fragmented with dozens of regional champions yet no single entity controlling more than 7% global revenue. TOPPAN Holdings’ USD 1.8 billion purchase of Sonoco’s Thermoformed and Flexible Packaging unit represents an inflection point toward strategic consolidation, knitting together advanced cylinder know-how with an extensive converter footprint. Esko, BOBST, and Hell Gravure Systems are forging technology alliances around closed-loop colour and cell-pattern standardization, creating embedded ecosystems that lock in consumable sales and protect aftermarket revenues. Iba AG’s machine-learning dashboards deliver 90% waste reduction on pilot lines, showcasing how data analytics now defines competitive edges in an industry once measured purely on visual craftsmanship.

Regional converters are pursuing cylinder-as-a-service to lower entry barriers for mid-tier brands, effectively shifting the business model from asset sales to recurring service fees. Emerging disruptors are experimenting with nanosecond pulse-laser engraving that claims 15-fold longer cylinder life, posing potential margin compression for traditional engravers. Patent filings concentrate on water-based nano-pigment inks and bio-resin adhesive chemistries, evidence that sustainability-linked innovation is the primary R and D battleground for the next cycle.

Gravure Printing Services Industry Leaders

Amcor plc

Dai Nippon Printing Co., Ltd.

Huhtamaki Oyj (Flexible Packaging)

Constantia Flexibles Group GmbH

American Packaging Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Amcor and Berry Global announced an all-stock merger creating a global leader in consumer and healthcare packaging with anticipated USD 650 million in annual synergies.

- January 2025: Amcor acquired Phoenix Flexibles, a flexible-packaging plant in India generating roughly USD 20 million in annual revenue, expanding its sustainable product lineup for food, homecare, and personal-care applications.

- January 2025: Heidelberger Druckmaschinen AG began its 175th anniversary year with a strategy targeting EUR 300 million in new sales by 2029, concentrating on packaging and digital presses.

- January 2025: Esko partnered with BOBST to introduce the smartGRAVURE system, slicing colour-matching time by more than 50% and downtime by 70% through digital workflow integration.

Global Gravure Printing Services Market Report Scope

| Packaging |

| Publication |

| Decorative and Security |

| Functional and Printed Electronics |

| Plastic Film |

| Paper |

| Aluminium Foil |

| Food and Beverage |

| Personal and Home Care |

| Pharmaceuticals |

| Tobacco |

| Industrial and Others |

| Pre-press and Cylinder Engraving |

| Printing (Press Operation) |

| Finishing and Lamination |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Packaging | |

| Publication | ||

| Decorative and Security | ||

| Functional and Printed Electronics | ||

| By Substrate | Plastic Film | |

| Paper | ||

| Aluminium Foil | ||

| By End-use Industry | Food and Beverage | |

| Personal and Home Care | ||

| Pharmaceuticals | ||

| Tobacco | ||

| Industrial and Others | ||

| By Service Type | Pre-press and Cylinder Engraving | |

| Printing (Press Operation) | ||

| Finishing and Lamination | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the gravure printing services market?

The industry is valued at USD 54.34 billion in 2025, with projections indicating USD 64.91 billion by 2030.

Which segment is expanding fastest within the gravure printing services market?

Functional and printed electronics is growing at 7.55% CAGR, propelled by RFID, sensor, and transparent conductive film demand.

Why is Asia-Pacific the largest regional market for gravure printing?

The region combines expansive consumer-goods output, cost-competitive manufacturing, and rising local brand launches, giving it 41.22% global share.

How are environmental regulations shaping gravure printing?

Toluene and MEK solvent restrictions compel migration to water-based and UV inks, driving capital upgrades and influencing process choices, especially in Europe and North America.

What technological innovations are improving gravure efficiency?

Digitalized pre-press such as Esko-BOBST smartGRAVURE halves color-matching time, while laser engraving reaches 24 kHz, drastically reducing cylinder lead times.

How are printed electronics influencing future growth?

Gravure’s capability to deposit low-viscosity functional inks at industrial speeds positions it to capitalize on smart packaging and IoT hardware integration across multiple industries.

Page last updated on: