Grain-Free Pet Food Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

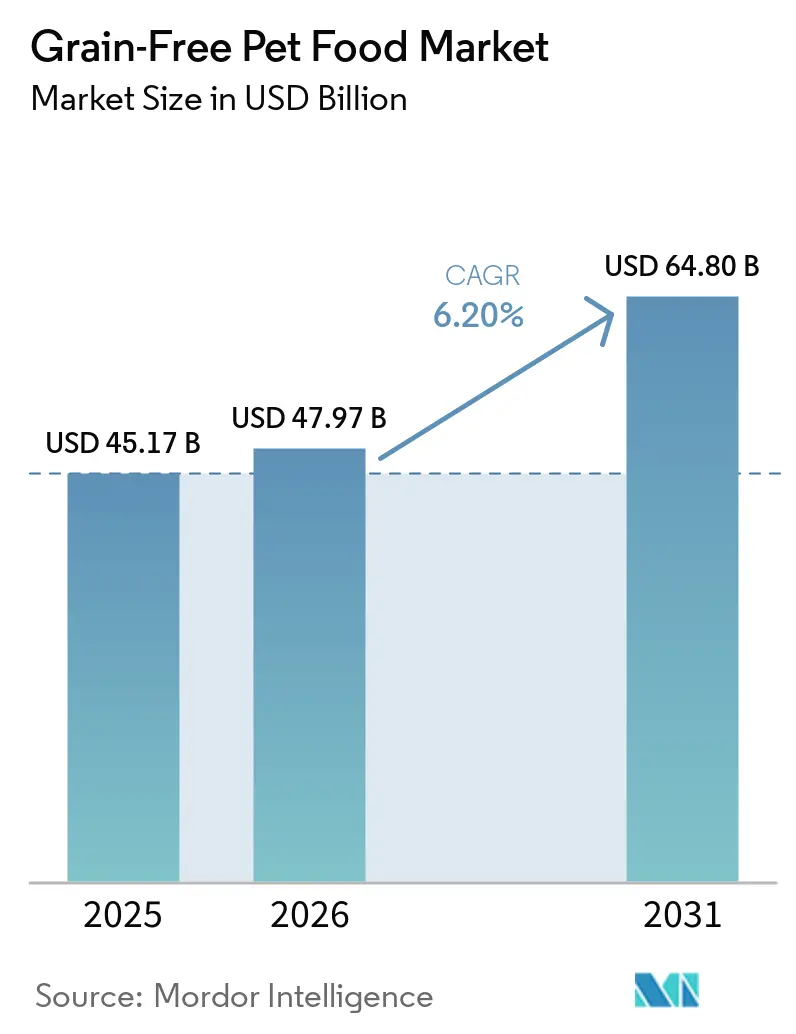

| Market Size (2026) | USD 47.97 Billion |

| Market Size (2031) | USD 64.80 Billion |

| Growth Rate (2026 - 2031) | 6.20% CAGR |

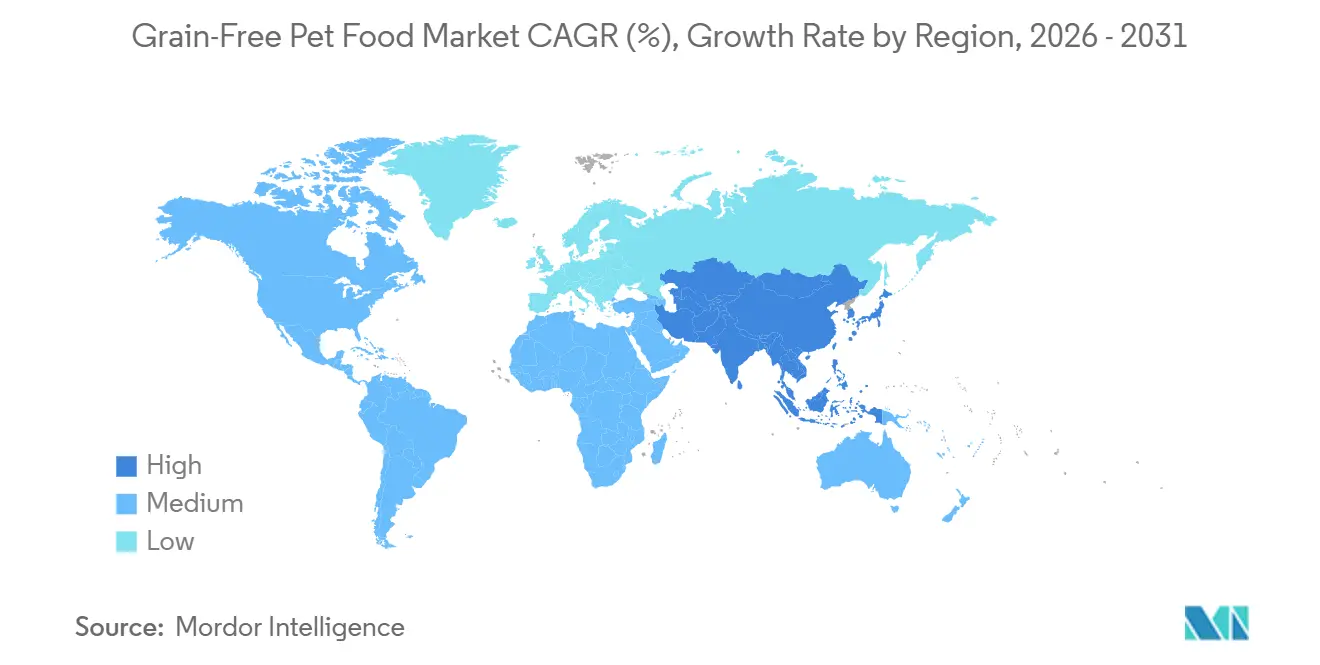

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Grain-Free Pet Food Market Analysis by Mordor Intelligence

The grain-free pet food market is projected to grow from USD 45.17 billion in 2025 and USD 47.97 billion in 2026 to USD 64.80 billion by 2031, registering a CAGR of 6.2% between 2026 and 2031. The market is being shaped by strong premiumization, increased adoption of functional ingredients, and heightened veterinary scrutiny. Leading manufacturers are investing in research to develop taurine-fortified, novel-protein recipes aimed at addressing concerns related to dilated cardiomyopathy while maintaining the clean-label appeal that drives category growth. The expansion of direct-to-consumer subscription services is enhancing first-party data collection and reducing distribution challenges, particularly in the United States and China. Additionally, the market is benefiting from the rising popularity of fresh, freeze-dried, and gently cooked formats, which bypass starch-free extrusion limitations and create opportunities for new entrants adept at managing cold-chain logistics. Declining costs of insect and single-cell proteins are also alleviating margin pressures, making sustainable alternatives a viable option for producing price-competitive, high-protein diets.

Key Report Takeaways

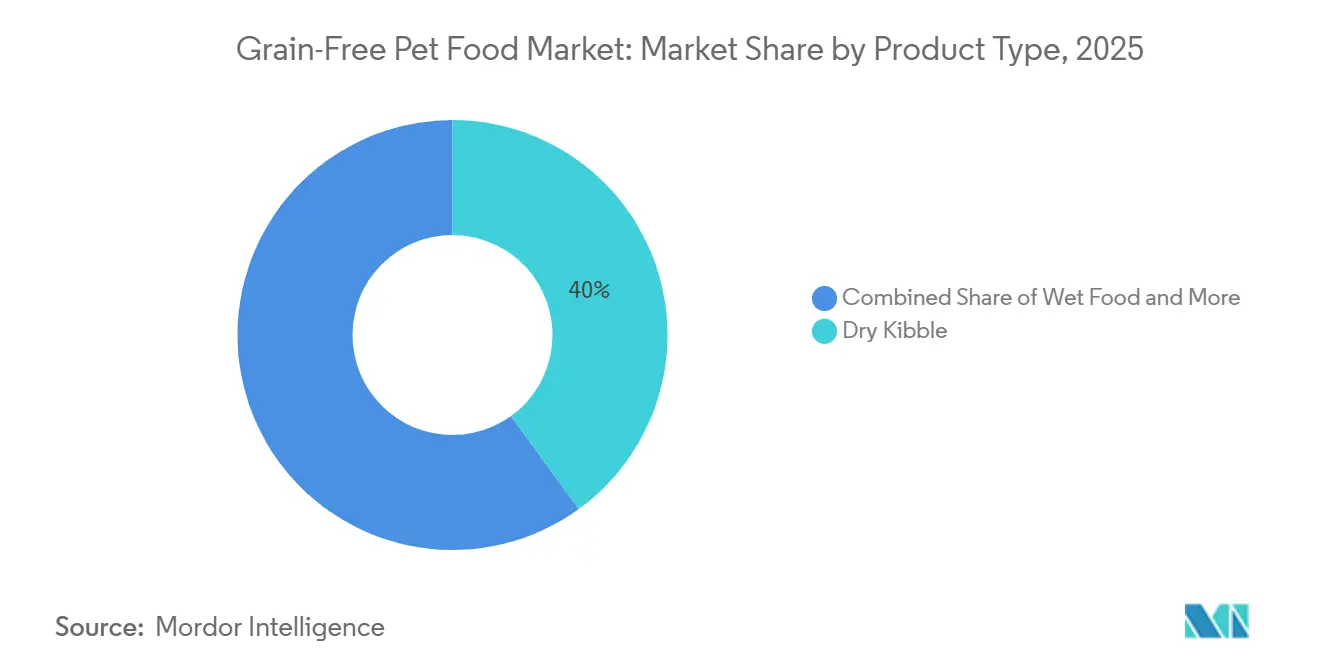

- By product type, dry kibble accounted for the largest 40% of the grain-free pet food market share in 2025, whereas freeze-dried and raw formats are projected to grow at the fastest 11.4% CAGR from 2026 to 2031.

- By pet type, dogs captured the largest 55% of the grain-free pet food market size in 2025, while cats are anticipated to grow at the fastest 9.5% CAGR from 2026 to 2031.

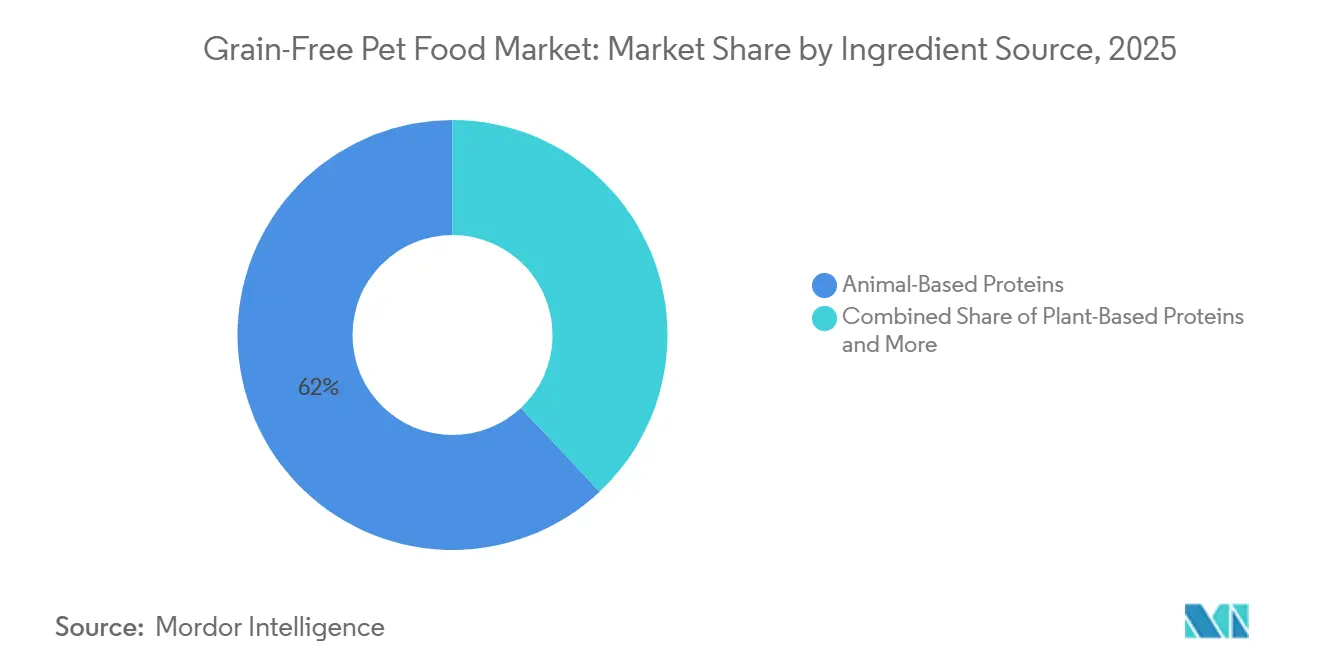

- By ingredient source, animal-based proteins held the largest 62% of the grain-free pet food market share in 2025, whereas insect and alternative proteins are projected to expand at the fastest 12.8% CAGR from 2026 to 2031.

- By geography, North America commanded the largest 42% of the grain-free pet food market share in 2025, while the Asia-Pacific market is projected to grow at the fastest 8.7% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Grain-Free Pet Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pet humanization fueling premium nutrition spend | +1.2% | Global with strongest uptake in North America, Western Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Increasing diagnosis of grain allergies/intolerances | +0.8% | North America and Europe, emerging in Australia and New Zealand | Short term (≤2 years) |

| Rapid expansion of online direct-to-consumer channels | +0.9% | Global, led by North America and China e-commerce ecosystems | Short term (≤2 years) |

| Premiumization toward high-protein clean-label diets | +1.1% | North America, Europe, Japan, and South Korea | Medium term (2-4 years) |

| Veterinary therapeutic adoption of grain-free formulas | +0.7% | North America and Europe, spillover to Middle East veterinary clinics | Long term (≥4 years) |

| Cost declines from insect and single-cell proteins | +0.6% | Europe regulatory-approval lead, Asia-Pacific production hubs, gradual North America entry | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Pet Humanization Fueling Premium Nutrition Spend

Households increasingly treat companion animals as family members, steering purchasing toward premium, grain-free recipes aligned with human clean-eating values. Millennials and Generation Z prioritize traceable supply chains and ethical sourcing, rewarding brands that demonstrate transparency through certifications and sustainability initiatives. According to the American Pet Products Association (APPA), total United States pet industry expenditure increased from USD 152 billion in 2024 to USD 158 billion in 2025, reflecting rising premiumization [1]Source: American Pet Products Association (APPA), “Industry Trends & Stats,” americanpetproducts.org . Smaller family sizes and delayed parenthood further channel discretionary income into pets, while demand for limited-ingredient and single-protein diets continues to grow, reinforcing the grain-free segment’s expansion.

Increasing Diagnosis of Grain Allergies/Intolerances

Advancements in diagnostic methods are enhancing the detection of food-related intolerances in pets, driving demand for grain-free diets. The Merck Sharp & Dohme Corp. (MSD) Veterinary Manual states that food allergies in animals are primarily identified through elimination diet trials, which involve removing and reintroducing specific ingredients to pinpoint triggers. This approach often promotes the use of simplified, limited-ingredient diets, including grain-free options, to isolate potential sensitivities. As veterinarians increasingly utilize dietary trials for diagnosis, pet owners are turning to grain-free pet food as an effective solution for managing suspected intolerances, thereby contributing to the growth of the grain-free pet food market.

Rapid Expansion of Online Direct-to-Consumer Channels

E-commerce adoption is transforming the grain-free pet food market by enabling brands to directly engage with consumers through subscription models and personalized nutrition options. According to Pet Food Processing, 52% of Millennials and 48% of Generation Z pet owners purchased pet products online in 2024, demonstrating strong digital purchasing trends among these key demographics [2]Source: United States Food and Drug Administration (FDA), “Questions & Answers: FDA’s Work on Potential Causes of Non-Hereditary DCM in Dogs,” fda.gov . This shift allows grain-free pet food brands to overcome traditional retail limitations, improve customer engagement, and utilize data-driven insights to enhance retention. Consequently, online platforms are emerging as an essential growth channel for premium and specialized pet food products.

Premiumization Toward High-Protein Clean-Label Diets

Consumer demand for high-protein and clean-label nutrition is driving premiumization in the grain-free pet food market. According to a 2025 study published by the Pet Food Industry, dog owners are more willing to pay premium prices for pet food featuring health-related claims, highlighting a growing preference for natural and functional pet nutrition products [3]Source: Pet Food Industry, “Study: Dog Owners Willing to Pay More for Food Labeled With Health Claims,” Petfoodindustry.com. This trend reflects the rising demand for grain-free diets made with high-protein ingredients, minimal additives, and transparent ingredient labeling. In response, manufacturers are focusing on ingredient quality, protein sourcing, and clean-label positioning to enhance premium brand value. However, fluctuations in protein input costs continue to impact product pricing and consistency.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| United States Food and Drug Administration (FDA) scrutiny over dilated cardiomyopathy link | −0.9% | North America primary, spillover to veterinary communities worldwide | Medium term (2-4 years) |

| Higher raw-material and production costs | −0.8% | Global, with acute pressure in North America and Europe | Short term (≤2 years) |

| Intense competitive price pressure | −0.5% | North America and Europe mass-market channels, rising in Asia-Pacific e-commerce | Short term (≤2 years) |

| Limited availability of starch-free extrusion capacity | −0.4% | North America and Europe manufacturing hubs, gradual expansion in Asia-Pacific | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

United States Food and Drug Administration (FDA) Scrutiny Over Dilated Cardiomyopathy Link

Regulatory scrutiny continues to impact the grain-free pet food market due to ongoing concerns regarding canine heart health. As of 2024, the United States Food and Drug Administration (FDA) is still investigating reports of non-hereditary Dilated Cardiomyopathy (DCM) associated with both grain-free and grain-inclusive diets. This uncertainty has led to increased caution among veterinarians and pet owners, particularly for dog breeds considered at higher risk. Consequently, consumers are more likely to seek professional advice before selecting grain-free products, while manufacturers are modifying formulations and marketing strategies. These factors collectively reduce consumer confidence and hinder the wider adoption of grain-free pet food.

Higher Raw-Material and Production Costs

Rising raw material and production costs continue to constrain the grain-free pet food market, particularly for protein-rich formulations. Data from the Unites States Bureau of Labor Statistics (BLS), accessed via the Federal Reserve Bank of St. Louis, indicates that the Producer Price Index for dog and cat food manufacturing rose from 300.9 in December 2025 to 304.0 in March 2026, highlighting ongoing cost inflation. Grain-free products, which depend heavily on high-quality animal proteins and specialty ingredients, are particularly vulnerable to these cost increases. Consequently, manufacturers face margin compression and are forced to either raise prices or modify formulations, which may reduce affordability and hinder adoption among price-sensitive consumers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fresh Formats Challenge Dry Dominance

Dry kibble accounted for the largest 40% of the grain-free pet food market share in 2025, driven by factors such as convenience, affordability, and extended shelf life. Its widespread retail availability and familiarity among consumers continue to support its dominance, particularly in cost-sensitive regions. However, shifting consumer preferences toward minimally processed nutrition are gradually increasing demand for premium formats. Wet food is gaining popularity, especially among aging pets and cats that require hydration support, while treats and snacks benefit from impulse purchasing behavior. Emerging formats, including air-dried and gently cooked products, are gaining niche acceptance in developed markets.

Freeze-dried and raw formats are projected to grow at the fastest 11.4% CAGR from 2026 to 2031, driven by rising demand for high-protein and minimally processed diets. These formats align with trends in pet humanization and advancements in cold-chain logistics. Manufacturers are expanding production capacities and introducing hybrid offerings that combine fresh and freeze-dried components. However, regulatory requirements related to food safety and pathogen control are increasing compliance costs, particularly for smaller manufacturers. Regional adoption varies significantly, with developed markets leading due to superior infrastructure, while developing regions remain dominated by dry formats due to cost constraints.

By Pet Type: Feline Adoption Picks Up Pace

Dogs accounted for the largest 55% share of the grain-free pet food market in 2025, driven by higher caloric needs and a wider range of available products. Established consumption patterns and strong brand presence among dog owners have contributed to this dominance. Product innovation in this segment focuses on breed-specific and life-stage formulations, addressing nutritional needs such as joint health and digestion. Veterinary endorsements and premiumization trends further bolster demand. Although developed regions show signs of market saturation, demand remains steady due to stable pet ownership rates and shifting dietary preferences.

Cats are projected to grow at the fastest CAGR of 9.5% from 2026 to 2031, supported by rising adoption rates and specific dietary needs. Feline nutrition prioritizes high-protein, moisture-rich diets, making grain-free options particularly appealing. Urbanization and smaller living spaces are driving increased cat ownership, particularly in Asia-Pacific markets. Wet food and specialized formulations are gaining popularity due to their hydration benefits and palatability. Additionally, the segment faces fewer health-related controversies compared to canine diets, fostering stronger growth in grain-free product adoption.

By Ingredient Source: Alternative Proteins Gain Momentum

Animal-based proteins held the largest 62% of the grain-free pet food market share in 2025, supported by superior digestibility and strong consumer preference for recognizable ingredients such as chicken and fish. These proteins improve palatability and align with clean-label trends. Manufacturers focus on transparency and high-quality sourcing to support premium pricing. Despite cost challenges, demand remains steady due to the perceived nutritional advantages. Blended formulations, incorporating multiple protein sources, are increasingly utilized to balance costs and nutritional benefits while maintaining consumer appeal.

Insect and alternative proteins are projected to expand at the fastest 12.8% CAGR from 2026 to 2031, driven by sustainability concerns and advancements in production technologies. These proteins offer a lower environmental impact and enhanced scalability compared to traditional sources. Regulatory approvals and consumer acceptance are gradually improving, particularly in Europe. Companies are investing in fermentation-based and insect-derived proteins to reduce dependence on conventional inputs. While adoption remains limited in certain regions, increasing awareness of sustainability benefits is projected to drive long-term growth in the use of alternative proteins.

Geography Analysis

North America commanded the largest 42% of the grain-free pet food market share in 2025, supported by high pet ownership rates and strong consumer spending on premium pet nutrition. The region benefits from a well-developed retail infrastructure, including specialty stores and e-commerce platforms, which enhance product accessibility. Growing consumer awareness of ingredient quality and pet health continues to fuel demand for grain-free formulations. Innovation in premium formats, such as freeze-dried and fresh pet food, is particularly notable, supported by established cold-chain logistics and strong veterinary engagement.

Asia-Pacific is projected to grow at the fastest 8.7% CAGR from 2026 to 2031, driven by rising pet ownership and increasing disposable incomes. Urbanization and evolving lifestyles are contributing to greater demand for premium pet food products. Digital commerce plays a significant role in market expansion, enabling brands to reach a broader consumer base. Countries such as China, Japan, and South Korea are leading in adoption, while emerging economies are gradually entering the premium segment. Consumer education and affordability remain critical factors influencing adoption rates across the region.

Europe maintains a balance between market size and growth through stringent labeling regulations, sustainability initiatives, and strong consumer demand for premium pet nutrition products. Germany, France, the United Kingdom, Italy, and Spain remain the largest regional consumption centers for grain-free pet food products. In October 2025, Farmina invested BRL 45 million (USD 7.7 million) to expand its distribution capacity in Brazil, enhancing international logistics and export capabilities to support broader pet food supply chains. The Middle East continues to generate demand for premium products, driven by affluent consumers seeking sustainable and specialized pet diets, while Africa represents an emerging market supported by urbanization and gradually increasing pet ownership trends.

Competitive Landscape

The grain-free pet food market is moderately fragmented, with key players such as Nestlé Purina PetCare Company, Mars, Incorporated, Blue Buffalo Company, Ltd. (General Mills, Inc.), Hill's Pet Nutrition, Inc., and The J. M. Smucker Company emphasizing product innovation and premiumization strategies. These large multinational companies utilize extensive distribution networks and strong brand recognition to maintain a competitive edge. Vertical integration in sourcing and manufacturing supports cost control and ensures quality. Additionally, companies are increasingly investing in research and development to introduce functional ingredients and specialized formulations. Partnering with veterinary professionals and retailers strengthens their position, especially in premium segments.

Mid-sized and emerging players are gaining momentum through direct-to-consumer models and digital marketing initiatives. Subscription-based services and personalized nutrition offerings are enabling these companies to establish strong customer relationships. Innovation in alternative proteins and sustainable sourcing is emerging as a significant differentiator. Smaller brands are targeting niche segments, such as raw and freeze-dried products, to compete with established players. The intensifying competition is driving ongoing product development and pricing strategies aimed at attracting health-conscious consumers seeking premium grain-free options.

Market consolidation is driven by growing strategic investments and acquisitions among key players. For instance, General Mills, Inc. acquired Edgard and Cooper in April 2024 to expand its premium pet food portfolio in Europe, bolstering its position in the natural and grain-free segments. This acquisition aligns with a broader industry trend of major companies investing in high-growth, premium pet nutrition brands. These strategic expansions allow companies to advance product innovation, strengthen their regional presence, and address the increasing demand for specialized diets, such as grain-free formulations.

Grain-Free Pet Food Industry Leaders

Nestlé Purina PetCare Company

Mars, Incorporated

Blue Buffalo Company, Ltd. (General Mills, Inc.)

Hill's Pet Nutrition, Inc.

The J. M. Smucker Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Mars, Incorporated, through its ORIJEN brand, introduced FRESHPREY, a fresh pet food line offering protein-rich, grain-free recipes made with fresh or raw animal ingredients. This launch signifies the company's entry into the fresh pet food market.

- February 2026: Agrolimen S.A. acquired Ollie, a direct-to-consumer, human-grade pet food brand, to enhance its position in the United States premium pet food market and expand its expertise in personalized nutrition and cold-chain distribution.

- October 2025: General Mills, Inc., through its Blue Buffalo Company, Ltd., introduced the Love Made Fresh line nationwide, entering the fresh pet food segment with premium, minimally processed recipes. This initiative strengthens its position in the high-growth, grain-free, and clean-label pet nutrition categories.

Global Grain-Free Pet Food Market Report Scope

Grain-free pet food refers to formulations that exclude grains such as wheat, corn, and rice, substituting them with alternative ingredients. It is designed to address perceived or diagnosed food sensitivities and aligns with premium, high-protein, and clean-label pet nutrition trends. The grain-free pet food market report is segmented by product type (dry kibble, wet food, treats and snacks, freeze-dried and raw formats, and other products), by pet type (dogs, cats, and other pets), by ingredient source (animal-based proteins, plant-based proteins, insect and alternative proteins, and mixed-ingredient formulations), and by geography (North America, Europe, Asia-Pacific, South America, Middle East, and Africa). The market forecasts are provided in terms of value (USD).

| Dry Kibble |

| Wet Food |

| Treats and Snacks |

| Freeze-Dried and Raw Formats |

| Others |

| Dogs |

| Cats |

| Others |

| Animal-Based Proteins |

| Plant-Based Proteins |

| Insect and Alternative Proteins |

| Mixed-Ingredient Formulations |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | Dry Kibble | |

| Wet Food | ||

| Treats and Snacks | ||

| Freeze-Dried and Raw Formats | ||

| Others | ||

| By Pet Type | Dogs | |

| Cats | ||

| Others | ||

| By Ingredient Source | Animal-Based Proteins | |

| Plant-Based Proteins | ||

| Insect and Alternative Proteins | ||

| Mixed-Ingredient Formulations | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the grain-free pet food market in 2031?

The grain-free pet food market size is forecast to hit USD 64.8 billion by 2031.

Which product format is growing fastest in grain-free diets?

Freeze-dried and raw formats recipes lead growth with the fastest 11.4% CAGR from 2026 to 2031.

Why are insect and single-cell proteins important in grain-free formulations?

Cost declines and sustainability credentials allow insect and single-cell proteins to reach near-parity with conventional meats, enabling high-protein grain-free recipes without sharp price increases.

Which region is projected to grow most rapidly?

Asia-Pacific is forecast to register the fastest 8.7% CAGR from 2026 to 2031.

Page last updated on: