Dehydrated Pet Food Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 5.5 Billion |

| Market Size (2031) | USD 9.30 Billion |

| Growth Rate (2026 - 2031) | 11.08% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

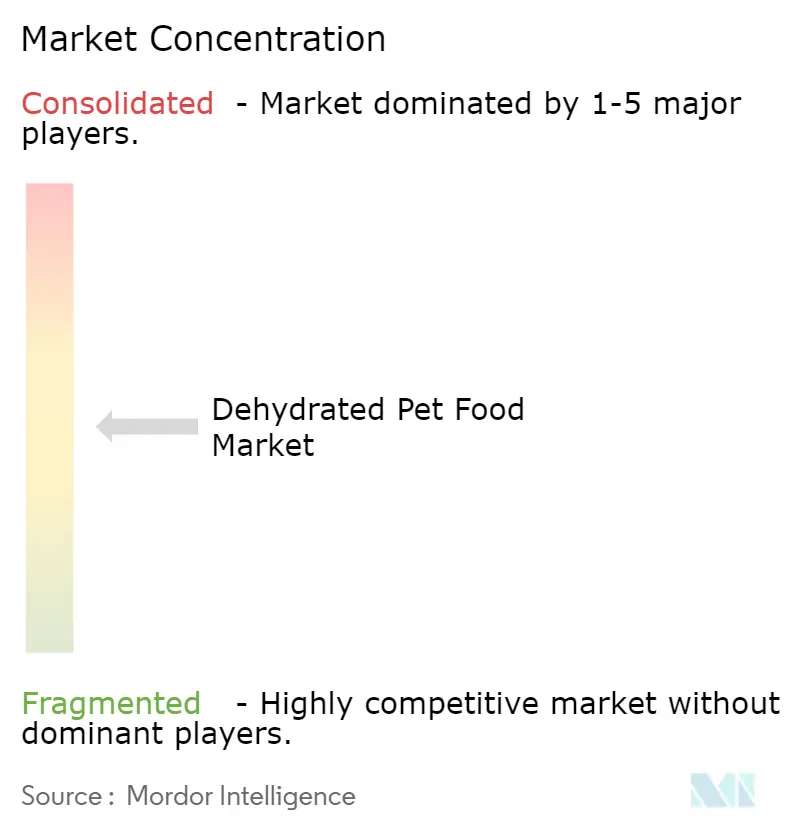

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dehydrated Pet Food Market Analysis by Mordor Intelligence

The dehydrated pet food market size is projected to grow from USD 4.90 billion in 2025 to USD 5.50 billion in 2026 and is projected to reach USD 9.30 billion by 2031, registering a CAGR of 11.08% during 2026-2031. Factors such as rising disposable income, the humanization of pets, and increased e-commerce accessibility are driving demand for minimally processed pet food formats that retain nutrient density while offering shelf stability and convenience. Freeze-dried products currently dominate revenue, but air-dried alternatives are growing faster owing to dual-stage drying processes that reduce costs and eliminate the need for cold-chain logistics. Additionally, veterinary clinics are increasingly prescribing dehydrated therapeutic diets through direct-to-consumer (DTC) platforms, fostering repeat purchases and enhancing clinical trust. Established kibble manufacturers face growing competition from DTC brands that emphasize human-grade certifications, clean-label ingredients, and pathogen-control measures to appeal to safety-conscious consumers.

Key Report Takeaways

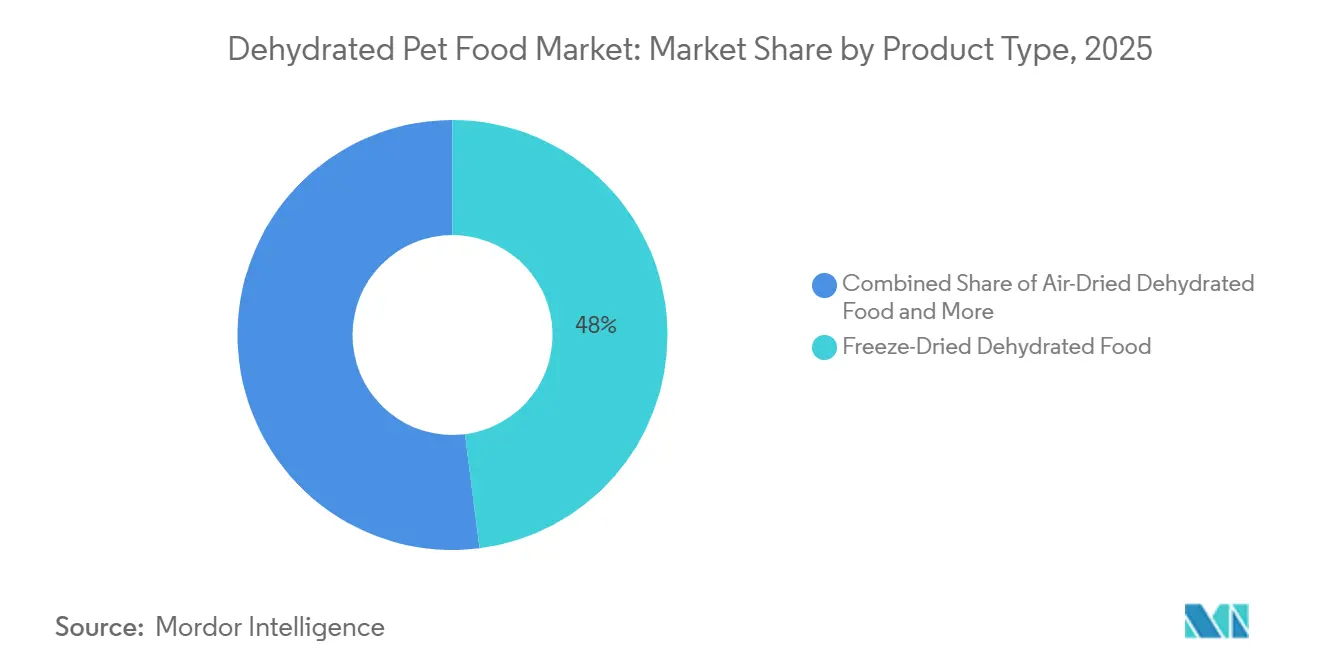

- By product type, freeze-dried dehydrated food led with the largest 48% of the dehydrated pet food market share in 2025, and the dehydrated pet food market size for the air-dried segment is projected to grow at the fastest 18.8% CAGR from 2026 to 2031.

- By pet type, the dog segment held the largest 63% of the dehydrated pet food market share in 2025, while the dehydrated pet food market size for the cats segment is projected to grow at the fastest 13.4% CAGR from 2026 to 2031.

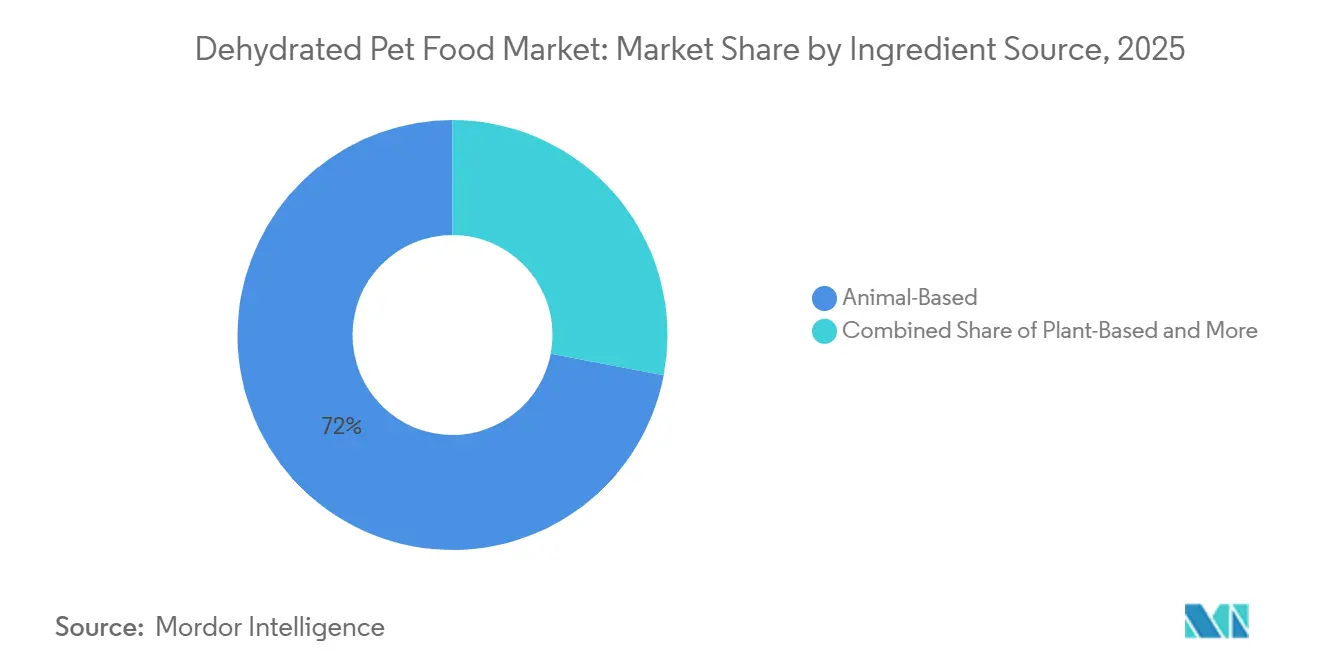

- By ingredient source, animal-based recipes captured the largest 72% of the dehydrated pet food market share in 2025, and insect-based formulas are projected to grow at the fastest 20.3% CAGR from 2026 to 2031.

- By distribution channel, pet specialty stores accounted for the largest 37% of pet food market share in 2025, and online retailers are expanding at the fastest 19.1% CAGR from 2026 to 2031.

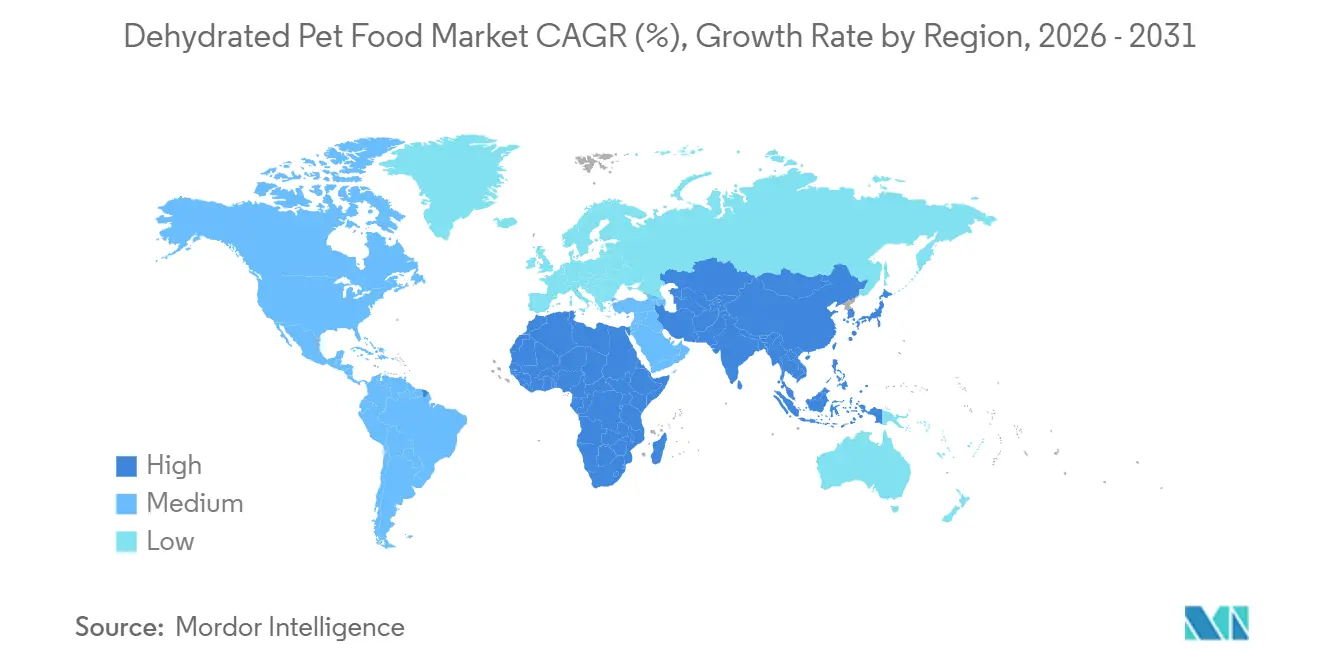

- By geography, North America commanded the largest 42% of the pet food market share in 2025, whereas Asia-Pacific market is forecast to grow at the fastest 15% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dehydrated Pet Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization of pet diets | +3.2% | Global with Emphasis in North America and Western Europe | Medium Term (2–4 Years) |

| Humanization of pets in mature economies | +2.8% | North America, Western Europe, Japan, and South Korea | Long Term (≥ 4 Years) |

| Growth of e-commerce pet-food retail | +2.5% | Global Led by Asia-Pacific and North America | Short Term (≤ 2 Years) |

| Veterinary endorsement of minimally processed nutrition | +1.9% | North America, Europe, Australia, and New Zealand | Medium Term (2–4 Years) |

| Insect-protein dehydration breakthroughs | +1.6% | Europe and North America with Early Uptake in Asia-Pacific | Long Term (≥ 4 Years) |

| Government disaster-relief stockpiling of light-weight pet rations | +0.9% | North America, Japan, and Australia | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

Premiumization of Pet Diets

Pet owners are increasingly treating their pets as family members, driving demand for premium, human-grade, minimally processed pet nutrition. According to the American Pet Products Association (APPA), premium pet food purchases rebounded in 2024, with 41% of dog owners and 38% of cat owners opting for higher-quality diets. This reflects a significant shift toward wellness-focused feeding [1]Source: American Pet Products Association (APPA), Research Insights on Premium & Functional Pet Foods, americanpetproducts.org. Dehydrated pet food aligns with this trend by providing clean-label, nutrient-dense formulations that emphasize health and ingredient transparency. Positioned between kibble and raw diets, these products appeal to consumers seeking convenient yet premium nutrition options, solidifying their role as a key beneficiary of the ongoing premiumization trend.

Humanization of Pets in Mature Economies

The growing trend of humanizing companion animals continues to drive the demand for premium, health-oriented pet nutrition. According to the American Pet Products Association (APPA) 2024–2025 National Pet Owners Survey, 94 million United States households owned a pet in 2024, highlighting the strong emotional bond and integration of pets into family life [2]Source: Insurance Information Institute (III), Facts + Statistics: Pet Ownership and Insurance (based on APPA National Pet Owners Survey), iii.org. This trend is prompting pet owners to prioritize high-quality, minimally processed, and human-grade diets. Dehydrated pet food meets these preferences by offering clean-label, nutrient-rich formulations, enabling brands to position their products as convenient, wholesome, and premium options that align with evolving consumer expectations and drive market growth.

Growth of E-Commerce Pet-Food Retail

The growth of e-commerce is reshaping pet food purchasing patterns, driven by factors such as convenience, subscription services, and personalized recommendations. According to the American Pet Products Association (APPA), 51% of pet product buyers made purchases online in 2025, compared to 47% who shopped in-store, underscoring the increasing prominence of digital channels. This transition has boosted demand for products optimized for online distribution. Dehydrated pet food aligns well with this trend due to its lightweight and shelf-stable properties, which lower shipping costs and improve delivery efficiency. Consequently, brands are using online platforms to expand their reach and boost profit margins, fueling market growth.

Insect-Protein Dehydration Breakthroughs

Advancements in insect-based protein offer a sustainable, nutritionally efficient alternative to traditional animal proteins. Ingredients like black soldier fly larvae offer high-quality amino acid profiles comparable to those of conventional meat sources while using significantly fewer natural resources. Dehydration technology preserves the nutritional integrity of functional compounds while enhancing shelf life and storage efficiency. These attributes position insect-based dehydrated formulations as a viable, hypoallergenic option, fostering innovation and meeting the growing consumer demand for sustainable, environmentally responsible pet nutrition solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price differential versus conventional kibble | -2.1% | Global with significant presence in South America and the Middle East | Short Term (≤ 2 Years) |

| Limited shelf life after opening | -1.3% | Global with Heightened Effect in Humid Tropical Climates | Medium Term (2–4 Years) |

| Supply volatility of single-species novel proteins | -1.0% | North America and Europe | Medium Term (2–4 Years) |

| Regulatory ambiguity on dehydrated raw pathogen standards | -0.8% | Global with Fragmented Rules Across Regions | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

High Price Differential Versus Conventional Kibble

Dehydrated pet food faces adoption challenges primarily because of its higher price compared to traditional kibble. The reliance on energy-intensive processes such as freeze-drying, extended production cycles, and the use of premium-quality protein ingredients substantially increases production costs. This leads to higher retail prices, making these products less affordable for cost-conscious consumers, especially in emerging, price-sensitive markets. During times of economic uncertainty or inflation, pet owners often opt for more economical feeding alternatives, which reduces demand for premium formats. As a result, the cost barrier remains a significant obstacle to wider market penetration, hindering overall growth.

Limited Shelf Life After Opening

Dehydrated pet food faces challenges maintaining quality after opening due to exposure to environmental factors such as air, heat, and humidity. According to the United States Food and Drug Administration (FDA), moisture and elevated temperatures can accelerate nutrient degradation and spoilage in pet food, impacting its quality and safety. Proper storage is essential. However, consumer practices often differ, particularly in humid climates where moisture absorption is more pronounced. Consequently, inconsistent storage conditions can reduce product usability, increase waste, and adversely affect the consumer experience.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Air-Dried Momentum Broadens Format Choice

Freeze-dried dehydrated food accounted for the largest 48% of market share in 2025, reflecting strong consumer trust, extended shelf stability, and premium positioning supported by nutrient retention and established retail presence. These products benefit from early market entry and wide availability across specialty channels, reinforcing their dominance among pet owners seeking minimally processed nutrition. Their convenience and perceived health benefits continue to drive adoption, particularly in developed markets where premium pet food consumption is well established and supported by higher disposable income and awareness of ingredient quality.

Air-dried dehydrated food is projected to grow at the fastest 18.8% CAGR from 2026 to 2031, supported by cost efficiency improvements and comparable nutritional value to freeze-dried alternatives. These products offer a balance between affordability and quality, making them attractive to consumers seeking premium options at relatively lower prices. Advances in drying technologies are improving production efficiency and product consistency, while maintaining high protein content and shelf stability. Increasing availability across online and specialty retail channels is further supporting adoption, particularly among new consumers transitioning from conventional pet food formats.

By Pet Type: Feline-Focused Nutrition Accelerates

Dogs segment accounted for the largest 63% of the market share in 2025, driven by higher consumption levels and the growing trend of premiumization among dog owners. Larger portion sizes and established feeding habits have contributed to increased product demand, while owners are placing greater emphasis on high-protein, minimally processed diets. The availability of a wide range of products tailored to breed size, age, and health conditions further strengthens this segment's dominance. Additionally, higher spending on dog nutrition compared to other companion animals continues to reinforce its market leadership.

Cats segment is projected to grow at the fastest 13.4% CAGR from 2026 to 2031, driven by increasing urban pet ownership and greater awareness of feline-specific dietary requirements. Cats require high-protein, low-carbohydrate diets, which has boosted demand for nutrient-dense formulations. The rise in apartment living and smaller household sizes has contributed to increased cat adoption, particularly in the Asia-Pacific and Europe. Manufacturers are expanding feline-focused product lines with functional ingredients and tailored formulations, supporting sustained growth and diversification within this segment.

By Ingredient Source: Insects Enter the Mainstream

Animal-based recipes accounted for 72% of the market share in 2025, driven by their strong nutritional profile and alignment with carnivorous dietary requirements. High protein content, amino acid availability, and preference for traditional meat-based diets continue to support dominance. Established supply chains and consumer familiarity further reinforce adoption. Premium positioning of animal-based formulations also supports higher pricing and brand differentiation, particularly in developed markets where demand for high-quality pet nutrition remains strong.

The insect-based formulas market size is projected to grow at the fastest 20.3% CAGR from 2026 to 2031, supported by sustainability advantages and increasing acceptance of alternative protein sources. These ingredients require fewer natural resources and offer comparable nutritional value, making them attractive for environmentally conscious consumers. Advancements in processing and regulatory approvals are improving market accessibility. Growing awareness of sustainability and ethical sourcing is further encouraging adoption, positioning insect-based formulations as an emerging growth segment within the broader market.

By Distribution Channel: Digital Convenience Rewrites Share

Pet specialty stores held the largest market share of 37% in 2025, driven by personalized services, product education, and in-store recommendations. These stores play a significant role in promoting premium products, as trained staff assist consumers in understanding ingredient benefits and feeding practices. Sampling and demonstrations further strengthen customer engagement and trust. Strong partnerships with premium brands and curated product selections underscore their importance in advancing the adoption of specialized pet food formats.

Online retailers are projected to grow at the fastest CAGR of 19.1% from 2026 to 2031, fueled by convenience, subscription models, and personalized recommendations. Digital platforms provide consumers with access to a wide range of products and enable easy comparison of options. Subscription-based purchasing ensures a steady supply of products and fosters brand loyalty. The integration of data analytics supports targeted marketing and product customization, enhancing the overall customer experience. The expansion of e-commerce infrastructure and the increasing adoption of digital continue to drive robust growth in this channel.

Geography Analysis

North America accounted for the largest 42% of the dehydrated pet food market share, driven by high pet ownership, robust consumer spending, and the widespread adoption of premium nutrition products. The region benefits from established retail networks and advanced supply chains that ensure consistent product availability. Additionally, growing consumer awareness of ingredient quality and minimally processed diets supports demand. The presence of major manufacturers and a strong distribution infrastructure further solidifies North America's leading position in the global market.

The Asia-Pacific region is projected to grow at the fastest 15% CAGR from 2026 to 2031, driven by rising pet ownership, urbanization, and higher disposable incomes. The expanding middle-class population and evolving lifestyles are driving higher spending on pet care and nutrition. Growth in e-commerce platforms is enhancing accessibility and product awareness, particularly in emerging markets. Furthermore, regulatory initiatives to improve food safety and quality standards are contributing to market growth. These factors collectively establish Asia-Pacific as a significant growth driver in the global market.

South America is experiencing changing adoption patterns influenced by growing pet ownership and increasing demand for commercial pet food, although affordability continues to be a challenge in several markets. According to the United States Department of Agriculture (USDA) Foreign Agricultural Service, South America imported USD 162.0 million worth of dog and cat food in 2024, an 11% increase compared to the previous year [3]Source: United States Department of Agriculture (USDA), Foreign Agricultural Service, Expanding the Dog and Cat Food Market in South America and the Caribbean, fas.usda.gov. This growth highlights the strengthening demand for packaged and premium pet nutrition products. It reflects improving economic conditions and a shift in consumer preferences toward higher-quality pet food, driving the gradual adoption of minimally processed and premium formats across the region.

Competitive Landscape

The industry structure is moderately fragmented, with the top five companies, The Honest Kitchen, Inc., Stella and Chewy’s, LLC, Primal Pet Foods, Inc. (Pure Treats Inc.), Nature’s Variety, Inc., and Ziwi Limited, anchoring the premium segment. These companies focus on specialized portfolios of freeze-dried and air-dried products, supported by strong brand positioning. Their strategies emphasize minimally processed and high-protein formulations and transparent sourcing to maintain competitive differentiation. Additionally, regional specialists such as K9 Natural Limited (Natural Pet Food Group) and Grandma Lucy’s, LLC strengthen the premium niche, while companies including Open Farm Inc. and Carnivore Meat Company, LLC improve product accessibility through diversified offerings and expanded retail presence.

Digital-first and emerging brands, including Steve’s Real Food, LLC, Sundays for Dogs, Inc., Kiwi Kitchens Limited, and Real Dog Box, Inc., are reshaping the competitive landscape. These companies leverage direct-to-consumer strategies, subscription models, and personalized nutrition approaches. Their focus on clean-label ingredients, veterinarian-backed formulations, and traceability helps build consumer trust and supports premium pricing. The New Zealand Natural Pet Food Co. Limited capitalizes on export-oriented production and high-quality sourcing standards to compete globally. Meanwhile, Sojos (BrightPet Nutrition Group, LLC) strengthens its market position with dehydrated meal formats and established distribution networks.

Competitive advantage in the market increasingly hinges on product innovation, ingredient sourcing, and processing capabilities. Companies investing in advanced dehydration technologies, sustainable protein sources, and improved shelf stability are better positioned to meet evolving consumer demands. Omnichannel strategies that integrate online platforms with specialty retail outlets are enhancing market reach and customer engagement. Firms that prioritize innovation in functional nutrition and maintain transparency in sourcing and production processes are likely to strengthen their market positioning. Conversely, companies relying on conventional formats face growing challenges in a premium-driven and innovation-focused competitive environment.

Dehydrated Pet Food Industry Leaders

The Honest Kitchen, Inc.

Stella & Chewy’s, LLC

Primal Pet Foods, Inc. (Pure Treats Inc.)

Nature’s Variety, Inc.

Ziwi Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Pure Treats Inc. has announced the acquisition of Primal Pet Foods from Kinderhook Industries. This acquisition expands Pure Treats Inc.'s presence in the premium raw and freeze-dried pet food market while adding manufacturing facilities in Texas and Colorado to enhance production capacity and support global distribution efforts.

- October 2025: The Honest Kitchen, Inc. unveiled Wholemade, a refreshed version of its dehydrated dog food line. This update includes new life-stage-specific recipes (puppy and senior) and updated packaging, further expanding its minimally processed, human-grade dehydrated pet food portfolio.

- September 2025: K9 Natural Limited (Natural Pet Food Group) established a strategic retail partnership with Pet Valu, Canada's largest specialty pet retailer, to facilitate the nationwide distribution of its freeze-dried, canned, and supplement product portfolio across Canada.

Global Dehydrated Pet Food Market Report Scope

Dehydrated pet food is pet food made by removing moisture from raw ingredients using low-heat or air-drying methods, which preserves nutrients and extends shelf life. It includes various sub-segments such as dehydrated dog food, dehydrated cat food, and dehydrated food for other pets. The dehydrated pet food market report is segmented by product type (freeze-dried dehydrated food, air-dried dehydrated food, and other dehydrated formats), by pet type (dog, cat, and other companion animals), by ingredient source (animal-based, plant-based, and insect-based), by distribution channel (supermarkets and hypermarkets, pet specialty stores, veterinary clinics, online retailers, and other channels), and by geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in terms of value (USD).

| Freeze-Dried Dehydrated Food |

| Air-Dried Dehydrated Food |

| Other Dehydrated Formats |

| Dog |

| Cat |

| Other Companion Animals |

| Animal-Based |

| Plant-Based |

| Insect-Based |

| Supermarkets and Hypermarkets |

| Pet Specialty Stores |

| Veterinary Clinics |

| Online Retailers |

| Other Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | Nigeria |

| South Africa | |

| Rest of Africa |

| By Product Type | Freeze-Dried Dehydrated Food | |

| Air-Dried Dehydrated Food | ||

| Other Dehydrated Formats | ||

| By Pet Type | Dog | |

| Cat | ||

| Other Companion Animals | ||

| By Ingredient Source | Animal-Based | |

| Plant-Based | ||

| Insect-Based | ||

| By Distribution Channel | Supermarkets and Hypermarkets | |

| Pet Specialty Stores | ||

| Veterinary Clinics | ||

| Online Retailers | ||

| Other Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | Nigeria | |

| South Africa | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the dehydrated pet food market by 2031?

The dehydrated pet food market size is forecast to reach USD 9.3 billion by 2031.

Which product format is projected to grow the fastest through 2031?

Air-dried dehydrated food will post the fastest 18.8% CAGR from 2026 to 2031.

How quickly will online retail sales expand?

Online channels are projected to grow at the fastest 19.1% CAGR from 2026 to 2031 as subscription models and direct-to-consumer brands reshape purchasing habits.

Why are veterinarians recommending dehydrated diets?

Minimally processed dehydration preserves enzymes and nutrient bioavailability, supporting therapeutic uses for allergies and digestive issues.

Page last updated on: