GPU Architecture And Compute IP Licensing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

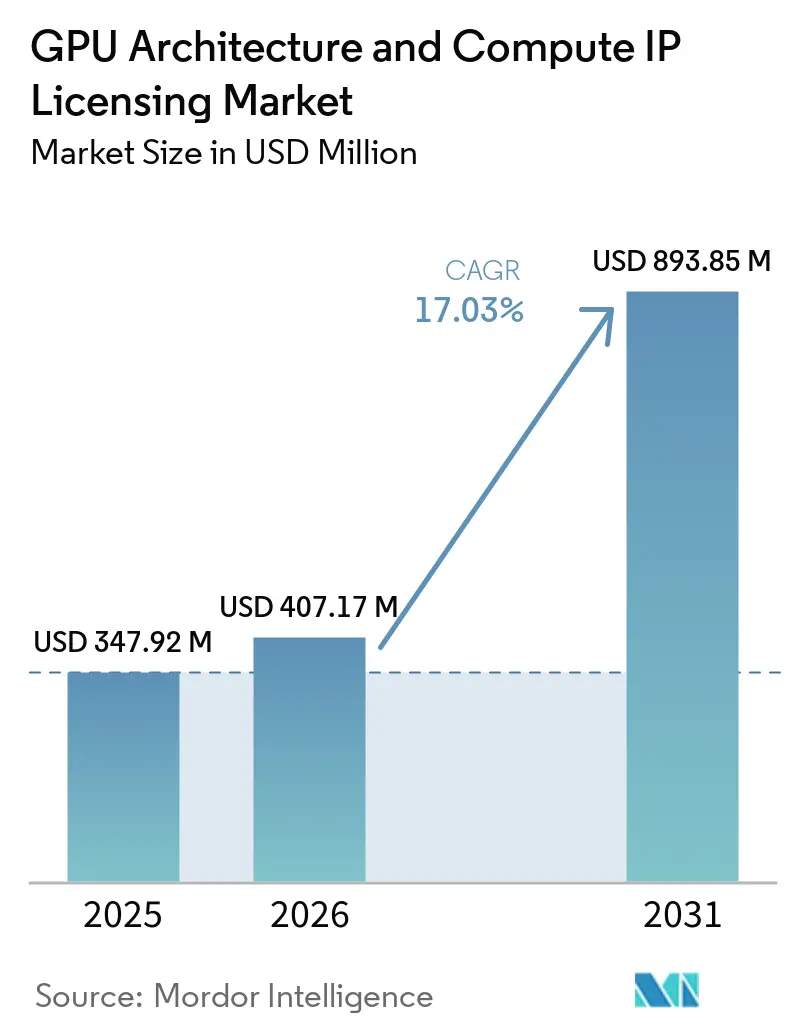

| Market Size (2026) | USD 407.17 Million |

| Market Size (2031) | USD 893.85 Million |

| Growth Rate (2026 - 2031) | 17.03% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GPU Architecture And Compute IP Licensing Market Analysis by Mordor Intelligence

The Graphics Processing Unit (GPU) Architecture and Compute Intellectual Property (IP) Licensing Market size is expected to increase from USD 347.92 million in 2025 to USD 407.17 million in 2026 and reach USD 893.85 million by 2031, growing at a CAGR of 17.03% over 2026-2031. Growing demand for workload-specific accelerators, escalating non-recurring engineering costs at leading-edge nodes, and persistent export-control uncertainty are prompting hyperscalers and fabless firms to license tensor-core and instruction-set IP rather than buy finished silicon. Vertical integration by cloud providers is shrinking the available market for discrete GPUs, pressuring incumbents to open their core designs to external partners. Open-source ISAs such as RISC-V are lowering switching costs and encouraging sovereign programs to pursue in-house architectures, while chiplet and advanced-packaging trends are increasing the value of cache-coherent interconnect IP blocks. Meanwhile, software-toolchain maturity remains a key differentiator, with vendors that bundle compilers and model-optimization libraries enjoying faster design-win velocity.

Key Report Takeaways

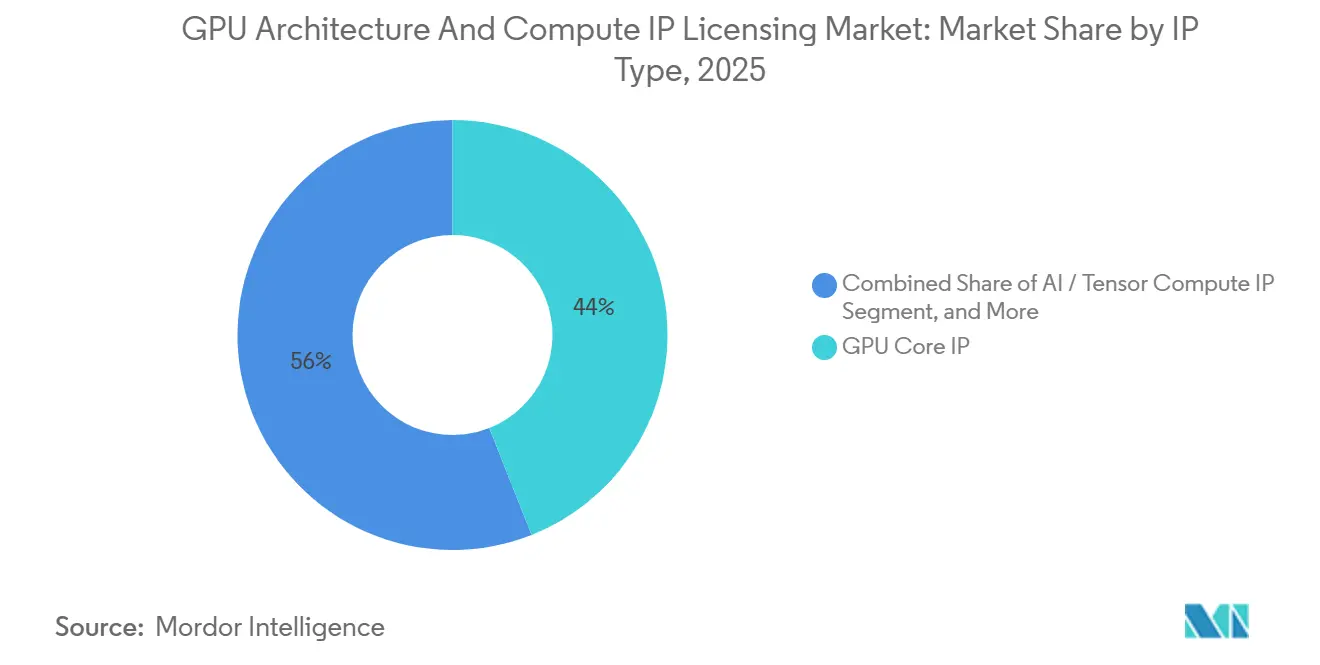

- By IP type, GPU core IP led with 44% of the GPU architecture and compute IP licensing market share in 2025, whereas AI and tensor compute IP is expected to advance at a 21.90% CAGR through 2031.

- By licensing model, perpetual license plus royalty agreements accounted for 52% of revenue in the GPU architecture and compute IP licensing market in 2025, while subscription and access-based licensing is projected to expand at an 18.80% CAGR to 2031.

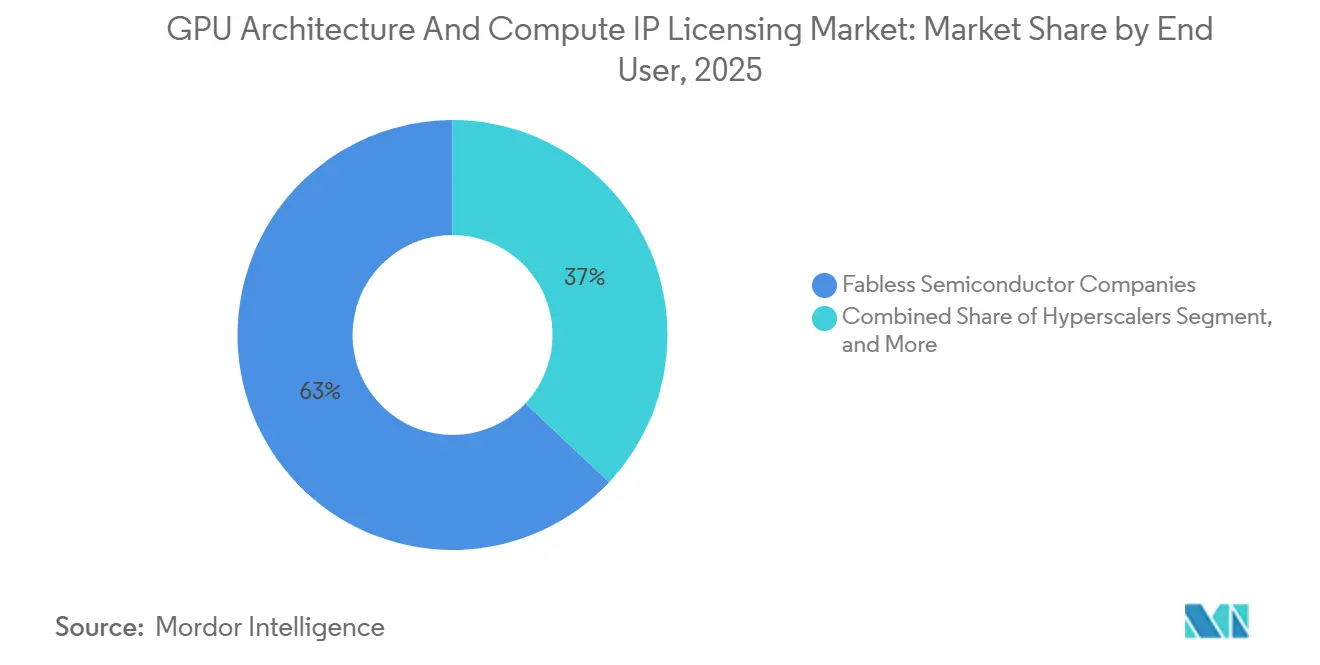

- By end user, fabless semiconductor companies captured 63% of revenue of the GPU architecture and compute IP licensing market in 2025, yet hyperscalers represent the fastest-growing customer group at a 22.40% CAGR through 2031.

- By geography, Asia-Pacific dominated with a 46% share of the GPU architecture and compute IP licensing market size in 2025, whereas North America is forecast to post the highest regional CAGR at 19.20% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global GPU Architecture And Compute IP Licensing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive AI Workload Growth In Data Centers | +5.20% | Global, concentration in North America and Asia-Pacific | Medium term (2–4 years) |

| Proliferation Of Edge AI Devices | +3.80% | Global, led by Asia-Pacific smartphone and IoT markets | Short term (≤ 2 years) |

| Rising GPU Adoption In Automotive ADAS | +2.10% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Mainstreaming Of Ray Tracing In Consumer Graphics | +1.90% | Global, early adoption in North America and Europe | Medium term (2–4 years) |

| Sovereign Semiconductor Strategies Driving In-House IP | +2.70% | Asia-Pacific, Europe, North America | Long term (≥ 4 years) |

| Open-Source ISA Momentum Catalyzing Custom GPUs | +1.40% | Global, leadership in Europe and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive AI Workload Growth In Data Centers

Hyperscale cloud providers are licensing tensor-core IP to build application-specific accelerators that trim energy cost per inference and avoid the margin stack of discrete GPUs. AWS Trainium2 instances, rolled out in March 2025, deliver 30% better performance per watt than H100 clusters, cutting the operator’s annual GPU purchase bill by USD 1.2 billion.[1]AWS, “Introducing Amazon EC2 Trn2 Instances Powered by AWS Trainium2,” amazon.comGoogle’s TPU v6e, co-developed with Broadcom, achieves one-third the energy cost of comparable GPU farms.[2]Google, “Announcing TPU v6e: Our Most Cost-Efficient AI Accelerator,” cloud.google.com The USD 20 billion Nvidia-Groq agreement proved that even inference-focused start-ups now seek IP access to preserve roadmap flexibility. This licensing preference accelerates revenue because perpetual-plus-royalty or subscription models let hyperscalers iterate every 18 months without renegotiating supply contracts. Resulting demand growth drives a positive 5.2% contribution to the overall CAGR forecast.

Proliferation Of Edge AI Devices

Smartphones, consumer IoT nodes, and smart-home appliances require on-device generative models that satisfy privacy mandates and sub-100 millisecond latency budgets. Qualcomm’s Snapdragon 8 Elite integrates AI tensor slices capable of 45 TOPS for real-time video segmentation.[3]Qualcomm, “Snapdragon 8 Elite Mobile Platform,” qualcomm.com MediaTek’s Dimensity 9400 combines Arm Mali-G925 GPU IP with a 16-core NPU to locally run 7-billion-parameter models.[4]MediaTek, “Dimensity 9400 Flagship 5G Chipset,” mediatek.comArm reported a 34% royalty jump in fiscal 2025 on shipments of 1.8 billion Mali- and Immortalis-equipped SoCs. Automotive demand adds further momentum as Imagination’s IMG CXT wins Level 3 ADAS sockets. The breadth of design wins underpins a 3.8% uplift to forecast CAGR.

Rising GPU Adoption In Automotive ADAS

Level 2+ to Level 4 autonomy pipelines must fuse lidar, radar, and camera feeds at 60 Hz or higher, pushing automakers toward licensed GPU and vision-processing IP. Ceva’s NeuPro-M inside Nextchip’s NX6000 delivers 50 TOPS while meeting automotive-grade reliability. Imagination’s XS and DXS families integrate ray-tracing for virtual-mirror rendering and have secured 2027 model-year design wins. WeRide licensed AMD RDNA IP to hit a 120 Hz path-planning loop within a 150-watt envelope. Software-defined-vehicle strategies mean OEMs value IP ownership that supports over-the-air updates for a decade, translating into a 2.1% positive CAGR contribution.

Mainstreaming Of Ray Tracing In Consumer Graphics

Ray tracing has moved from desktops to smartphones and handheld consoles. NVIDIA’s RTX 5090 introduced ReSTIR PT, cutting per-frame ray counts by 40% without visual compromise. Arm’s Immortalis-G925 enables variable-rate ray tracing in smartphones at 60 fps within 5 watts. Game-engine mandates force fabless companies to license ray-intersection IP rather than absorb an 18-month in-house development cycle. The requirement to refresh GPU IP annually sustains licensing demand, adding 1.9% to CAGR expectations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-Front NRE Costs For Advanced Nodes | -2.80% | Global, acute in Asia-Pacific and Europe | Medium term (2–4 years) |

| Export Controls On High-Performance Compute IP | -3.10% | Asia-Pacific (China), spillover to Middle East and Africa | Short term (≤ 2 years) |

| Fragmentation Of Software Toolchains | -1.60% | Global | Medium term (2–4 years) |

| Escalating Patent Litigation Risk | -1.20% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Up-Front NRE Costs For Advanced Nodes

Mask sets for 3 nm and 2 nm processes now exceed USD 30 million, and first-silicon outlays can reach USD 80 million, pricing many mid-tier fabless firms out of leading-edge designs. CoWoS packaging adds USD 1,500 per die, up from USD 900 in 2023. Samsung’s 3 nm gate-all-around node is 15% cheaper but yielded six-month delays in early tape-outs. As a workaround, smaller licensees migrate to mature 7 nm nodes or adopt chiplets, sacrificing power efficiency. The spending barrier removes 2.8% from the projected CAGR.

Export Controls On High-Performance Compute IP

U.S. Bureau of Industry and Security rules cap licensing of GPU IP above 300 TOPS and 600 GB/s bandwidth to entities in China and 21 other jurisdictions. Chinese vendors Biren and Moore Threads lost access to Arm and Synopsys IP after the Entity List designation in March 2025. The proposed Remote Access Security Act could extend limitations to cloud instances, forcing licensors to embed monitoring circuits that lengthen design cycles by up to 18 months. These restrictions shave 3.1% from forecast growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By IP Type: Tensor Cores Reshape Licensing Mix

GPU core IP held 44% revenue share in 2025, a position built on Arm Mali and Imagination PowerVR franchises that ship in more than 2 billion devices annually. AI and tensor compute IP is expanding at a 21.90% CAGR as hyperscalers prioritize INT8 and sparsity engines over rasterization, redirecting spend toward specialized matrix blocks. The Nvidia-Groq arrangement illustrates how licensees increasingly value Blackwell-generation tensor cores and NVLink fabrics for export-compliant inference chips. Compute ISA IP, primarily RISC-V vector extensions, captured 18% share, buoyed by sovereign programs in Europe and India that seek royalty-free instruction sets. On-chip interconnect IP reached 14% share as chiplet adoption demands sub-100-nanosecond latency meshes.

Hyperscalers also favor sparse-tensor accelerators that boost operations per watt, as seen in Google’s TPU v6e, which integrates custom sparsity logic yielding 2.4× dense-matrix throughput. Meta’s MTIA v2 licensed only memory-controller and interconnect blocks while designing proprietary inference units. SiFive’s Intelligence X390 NPU blends RISC-V vectors with a 128-lane matrix engine, offering licensees a royalty-free path to 50 TOPS at 5 watts. As a result, AI-centric IP is positioned to overtake classic GPU shader cores before 2031.

By Licensing Model: Subscription Gains As Fabless Players Seek Flexibility

Perpetual license plus royalty agreements generated 52% of revenue in 2025 because high-volume customers amortize fees across millions of units. Arm’s Flexible Access program added 340 new subscribers in fiscal 2025, charging USD 75,000-200,000 per year for full portfolio entry. Imagination’s tiered subscription service, launched in June 2025, trims first-tape-out schedules by nine months for start-ups. Royalty-only deals, now 19% of revenue, appeal to venture-backed firms and grew after Synopsys extended DesignWare GPU subsystems to royalty-only terms.

Subscription licensing aligns with agile development because teams can shelve underperforming prototypes without incurring unit royalties. Nevertheless, hyperscalers still prefer perpetual ownership to avoid cumulative fee inflation, explaining the coexistence of both models. Over the forecast period, the GPU architecture and compute IP licensing market size for subscription contracts is likely to double, whereas perpetual deals will retain dollar leadership.

By End User: Hyperscalers Redefine Demand Patterns

Fabless semiconductor companies dominated with 63% revenue share in 2025, led by smartphone and automotive chip suppliers that embed GPU IP to differentiate their systems-on-chip. However, hyperscalers are growing fastest at 22.40% CAGR through 2031 as Amazon, Google, and Meta internalize accelerator design. AWS disclosed that Trainium2 and Inferentia3 now handle 40% of training and 65% of inference workloads, saving USD 1.2 billion in annual GPU capital outlays. Google’s multi-year arrangement with Broadcom covers not just tensor cores but also optical interconnect IP for pod-scale deployments.

Integrated device manufacturers accounted for 18% of revenue in 2025. Intel licensed Arm Mali IP for its automotive roadmap, while AMD paired in-house compute dies with Synopsys HBM3E controllers in MI325X accelerators. Samsung’s 3 nm GAA process attracted IDM clients seeking chiplet integration, although yield challenges delayed schedules. The bifurcation underscores how hyperscalers’ willingness to absorb eight-figure NRE outlays is reshaping vendor business models.

Geography Analysis

Asia-Pacific held 46% of the GPU architecture and compute IP licensing market share in 2025, anchored by Taiwan’s TSMC, which fabricates more than 70% of licensed GPU designs worldwide. China earmarked CNY 45 billion (USD 6.3 billion) for domestic GPU development despite export-control headwinds. India’s Design Linked Incentive reimburses up to 50% of IP fees, drawing Imagination, SiFive, and Cadence into local partnerships. Japan committed JPY 200 billion (USD 1.3 billion) to RISC-V GPU IP via the Rapidus consortium. Although Biren and Moore Threads lost access to Arm and Synopsys IP, both pivoted to Alibaba’s royalty-free Xuantie C930 cores.

North America is projected to expand at a 19.20% CAGR through 2031, fueled by CHIPS Act incentives and hyperscaler vertical integration. AWS, Google, and Meta invested more than USD 8 billion in custom-silicon IP during 2025, and TSMC’s Arizona fab will produce Trainium2 and TPU v6e volumes from Q1 2026. The October 2024 U.S. export-control update inadvertently accelerated domestic licensing, as providers now must tailor ASICs for regional compliance.

Europe captured 12% share in 2025, with automotive ADAS and sovereign compute driving demand. The European Processor Initiative licensed SiFive RISC-V vectors for its Rhea2 exascale processor. Germany budgeted EUR 500 million (USD 565 million) to subsidize GPU IP in the auto supply chain. Rest-of-World regions, including South America, Middle East, and Africa, together represented 6% share, hindered by weaker IP-protection enforcement and limited fab capacity.

Competitive Landscape

The Graphics Processing Unit (GPU) Architecture and Compute Intellectual Property (IP) Licensing market is moderately concentrated, with Arm, Imagination Technologies, and Nvidia collectively holding approximately 55% of the revenue share in 2025. Arm’s lawsuit against Qualcomm in December 2025 over Nuvia-derived Oryon cores highlights stricter enforcement of architectural license terms. Horizontal IP vendors, such as Synopsys and Cadence, are expanding their DesignWare and Tensilica portfolios to address the growing demand for chiplet interconnect and vision-DSP solutions. These expansions aim to capture emerging opportunities in the market. Meanwhile, vertical integrators like Nvidia, AMD, and Intel are selectively licensing proprietary blocks. For instance, Nvidia has opened Blackwell tensor cores to partners, AMD has licensed ROCm toolchains to facilitate migration, and Intel plans to license Xe2 GPUs starting in 2026.

Disruptors are actively addressing software gaps in the market, creating new opportunities for competition. Tenstorrent’s Metalium stack has achieved CUDA-level performance on RISC-V tensors, securing four hyperscale design wins. Similarly, Esperanto has licensed its ET-Maxion AI cores to undisclosed cloud customers, while SiFive’s X390 has gained traction with three automotive tier-1 deals. These advancements demonstrate the growing capabilities of emerging players in the market. Despite these developments, incumbents maintain a competitive edge through their extensive patent portfolios. For example, Arm holds over 6,000 patents related to GPU and interconnect technologies, and Nvidia’s NVLink IP remains critical for clusters exceeding 10,000 devices.

However, the rising adoption of RISC-V and increased sovereign funding could exert downward pressure on royalties and potentially lead to mid-tier vendor consolidation over the next five years. These trends are expected to reshape the competitive landscape, creating both challenges and opportunities for market participants. New entrants may find opportunities to gain market share, while established players will need to adapt to maintain their dominance. The evolving dynamics could also encourage innovation and collaboration among stakeholders. As the market progresses, companies must remain agile to navigate these changes and leverage emerging trends effectively.

GPU Architecture And Compute IP Licensing Industry Leaders

Arm Ltd.

Imagination Technologies Ltd.

Nvidia Corporation

Advanced Micro Devices, Inc.

Intel Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Arm unveiled the Mali-G930 GPU IP family with variable-rate shading and neural-network super-sampling, targeting 2027 flagship smartphones.

- March 2026: Synopsys and Samsung Foundry began co-optimizing DesignWare GPU and HBM4 IP for Samsung’s 2 nm process, aiming for Q4 2026 silicon.

- February 2026: Nvidia licensed Blackwell GPU and NVLink IP to MediaTek for automotive SoCs in a USD 1.5 billion, five-year deal.

- January 2026: Tenstorrent raised USD 500 million in Series D funding, citing RISC-V IP design wins at four hyperscalers and two automotive OEMs.

Global GPU Architecture And Compute IP Licensing Market Report Scope

The Graphics Processing Unit (GPU) Architecture and Compute Intellectual Property (IP) Licensing Market is Segmented by IP Type (GPU Core IP, AI/Tensor Compute IP, Compute ISA/Architecture IP, On-Chip Compute Interconnect IP), Licensing Model (Perpetual License + Royalty, Subscription/Access-Based Licensing, Royalty-Only Models), End User (Fabless Semiconductor Companies, Integrated Device Manufacturers, Hyperscalers), and Geography (North America, Europe, Asia-Pacific, Rest of World). Market Forecasts are Provided in Terms of Value (USD).

| GPU Core IP |

| AI / Tensor Compute IP |

| Compute ISA / Architecture IP |

| On-Chip Compute Interconnect IP |

| Perpetual License + Royalty |

| Subscription / Access-Based Licensing |

| Royalty-Only Models |

| Fabless Semiconductor Companies |

| Integrated Device Manufacturers (IDMs) |

| Hyperscalers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By IP Type | GPU Core IP | |

| AI / Tensor Compute IP | ||

| Compute ISA / Architecture IP | ||

| On-Chip Compute Interconnect IP | ||

| By Licensing Model | Perpetual License + Royalty | |

| Subscription / Access-Based Licensing | ||

| Royalty-Only Models | ||

| By End User | Fabless Semiconductor Companies | |

| Integrated Device Manufacturers (IDMs) | ||

| Hyperscalers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Key Questions Answered in the Report

What is the 2026 value of the GPU architecture and compute IP licensing market?

The GPU architecture and compute IP licensing market size is estimated at USD 407.17 million in 2026, according to Mordor Intelligence.

Which IP category is growing fastest through 2031?

AI and tensor compute IP leads growth with a projected 21.90% CAGR to 2031, driven by hyperscaler demand for workload-specific tensor engines.

Why are hyperscalers shifting from discrete GPUs to licensed IP?

Licensing enables custom silicon that lowers energy cost per inference, avoids export-control bottlenecks, and shortens refresh cycles, improving total cost of ownership.

How do advanced-node NRE costs affect smaller fabless firms?

Mask-set and first-silicon expenses above USD 30 million at 3 nm and 2 nm nodes often force mid-tier firms to remain on 7 nm or adopt chiplet strategies to contain budgets.

What role does RISC-V play in this market?

RISC-V's royalty-free ISA and modular extension model attract sovereign and cost-sensitive programs, fostering custom GPU cores that challenge proprietary architectures.

Which region is expected to post the highest CAGR through 2031?

North America is forecast to grow at 19.20% CAGR, fueled by CHIPS Act incentives and hyperscaler investments in domestically fabricated custom accelerators.

Page last updated on: