GRC Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 23.32 Billion |

| Market Size (2031) | USD 39.01 Billion |

| Growth Rate (2026 - 2031) | 10.84% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GRC Software Market Analysis by Mordor Intelligence

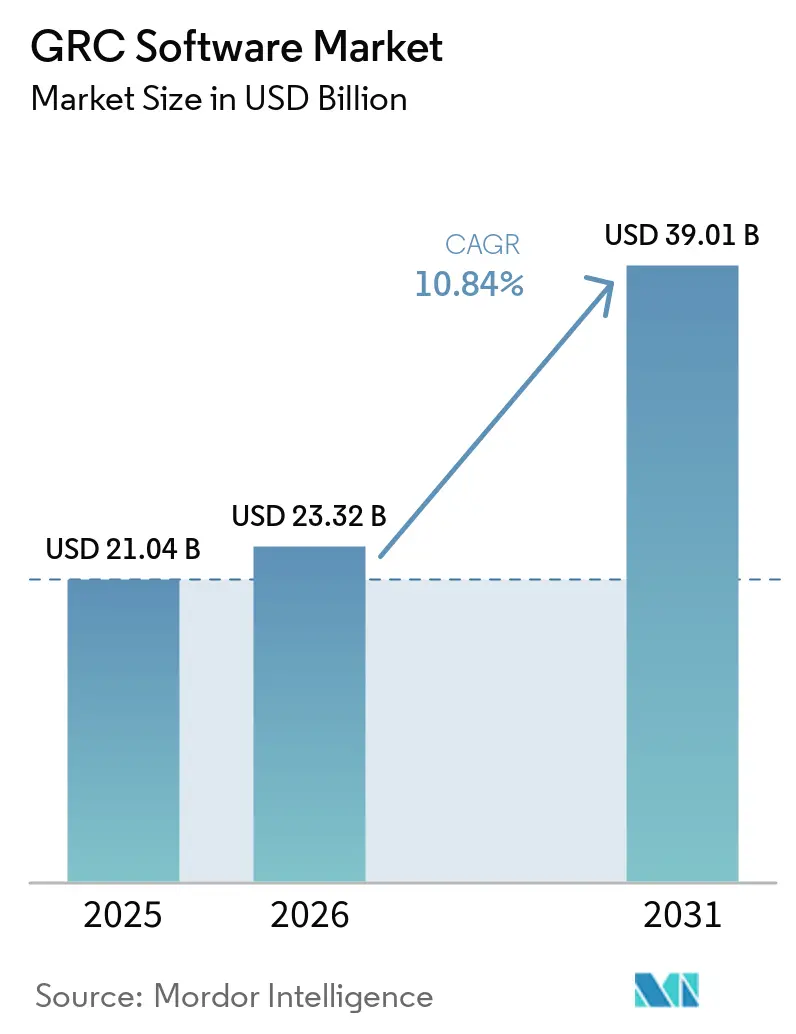

The Governance, Risk, and Compliance (GRC) Software market size was valued at USD 21.04 billion in 2025 and estimated to grow from USD 23.32 billion in 2026 to reach USD 39.01 billion by 2031, at a CAGR of 10.84% during the forecast period (2026-2031). Heightened regulatory divergence, growing cyber-attack surfaces, and board-level demand for continuous controls monitoring are steering enterprises toward unified, cloud-native platforms that integrate policy, risk, and audit workflows in real time. Software components continue to dominate, yet double-digit expansion of managed services signals a preference for expert-led implementations that offset internal skills shortages. Cloud deployment is accelerating as firms seek collaborative oversight across globally distributed operations, while AI-driven analytics are turning the Governance, Risk, and Compliance (GRC) Software market from a reactive compliance outlay into a proactive risk-intelligence investment.[1]International Federation of Accountants, “Fragmented Financial Regulation: A 780 Billion Tax on the Global Economy,” ifac.org Convergence of ESG, privacy, and operational-resilience mandates is also reshaping platform roadmaps, pushing vendors toward modular suites that embed carbon accounting, AI governance, and cyber-insurance evidence collection within a single pane of glass.

Key Report Takeaways

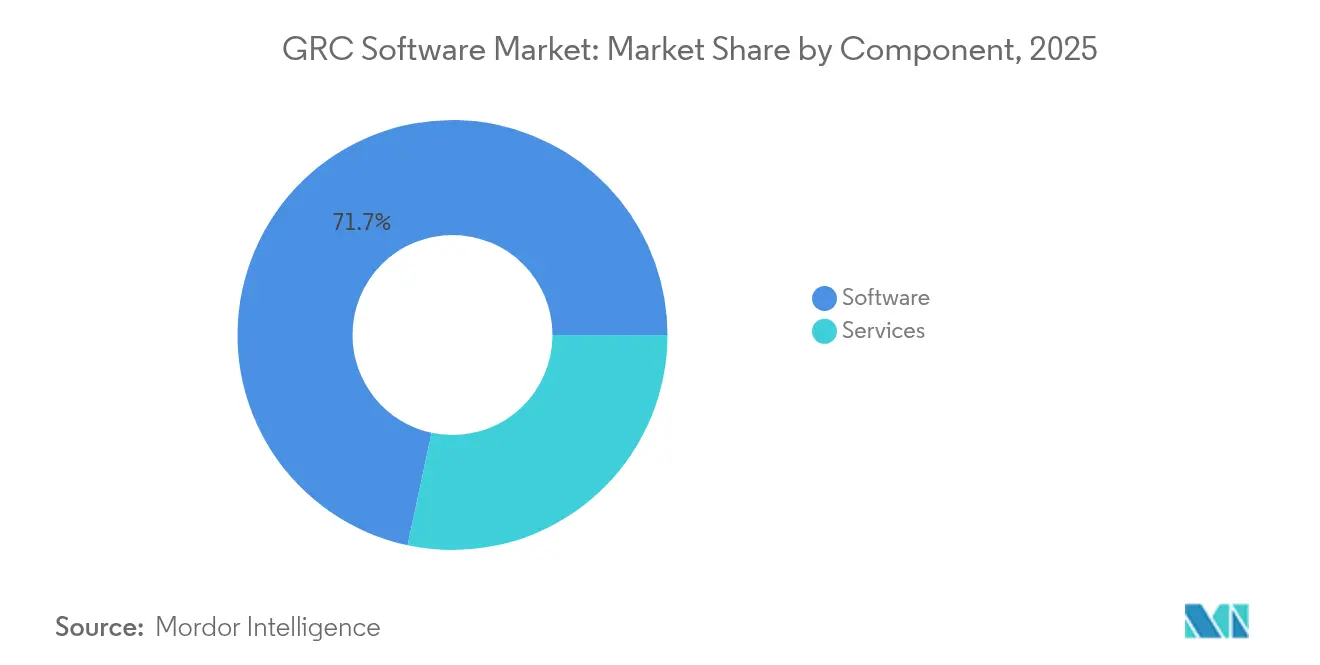

- By component, software held 71.65% of the Governance, Risk, and Compliance (GRC) Software market share in 2025, whereas services are projected to record a 12.98% CAGR through 2031.

- By deployment mode, cloud captured 62.90% of the Governance, Risk, and Compliance (GRC) Software market size in 2025 and is expected to expand at a 13.85% CAGR to 2031.

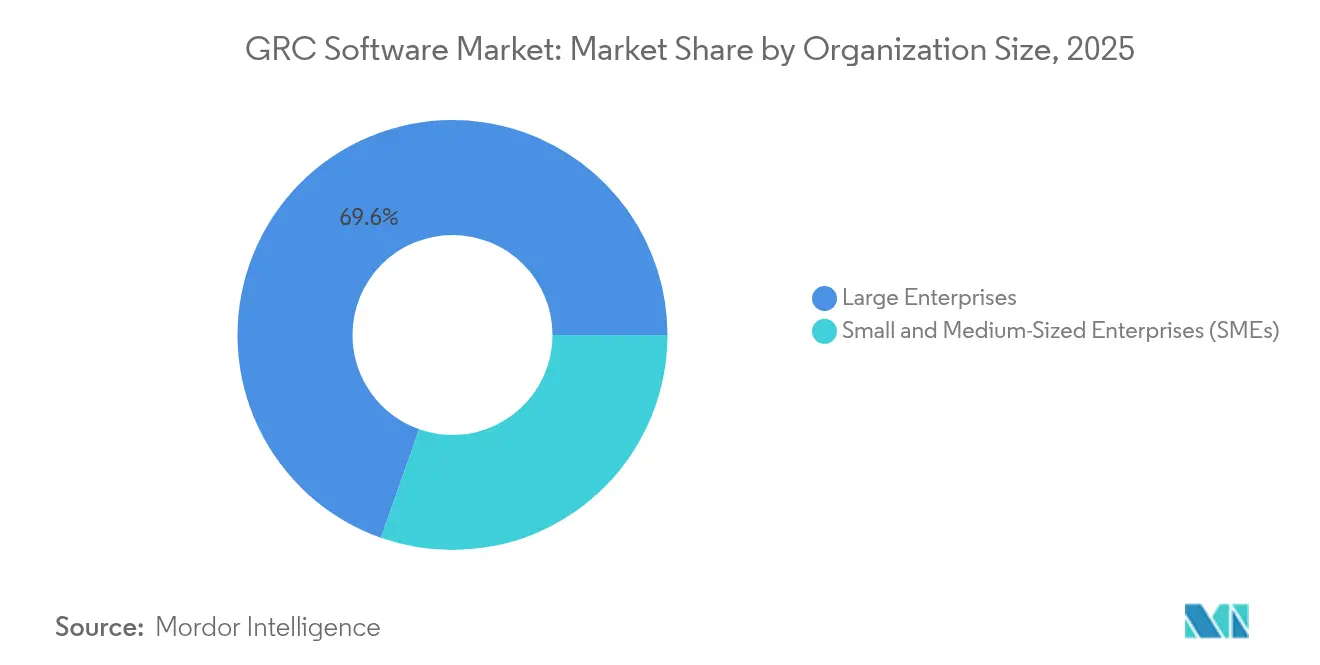

- By organization size, large enterprises controlled 69.60% of 2025 revenue, but small and medium-sized enterprises are forecast to grow at a 13.02% CAGR through 2031.

- By vertical, BFSI commanded 24.60% revenue in 2025; healthcare and life sciences are projected to post a 14.15% CAGR, the fastest across all industries.

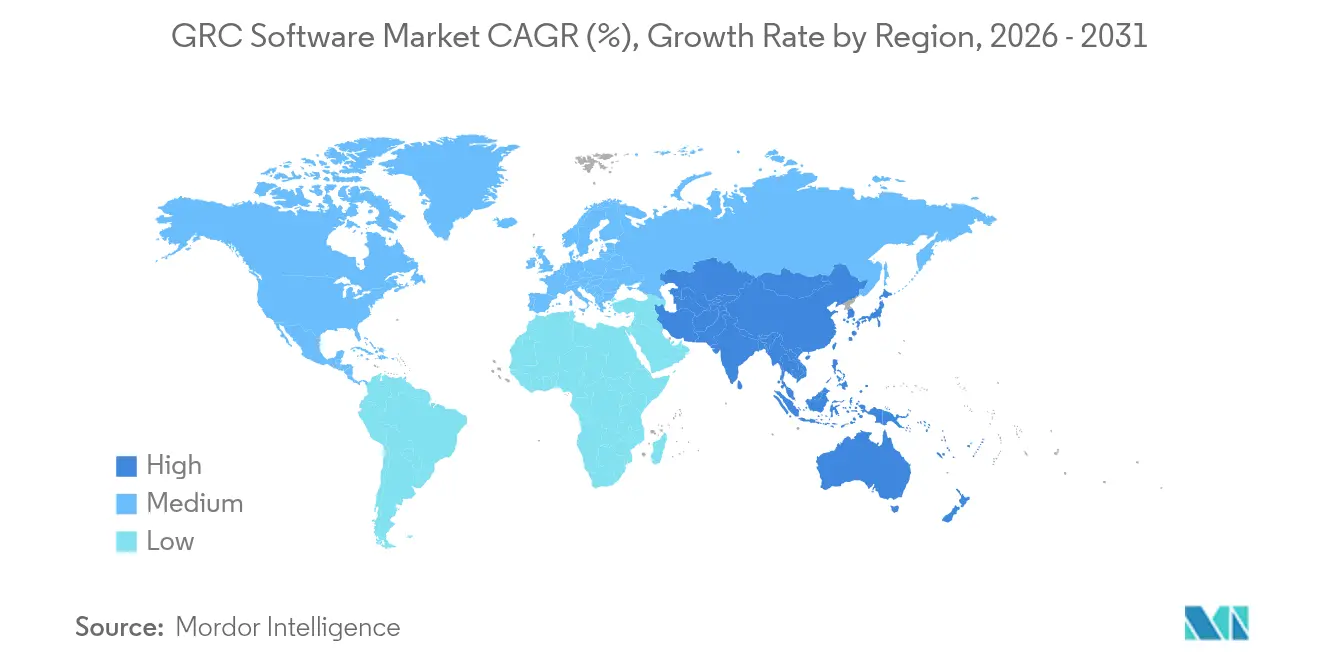

- By geography, North America commanded 39.55% revenue in 2025, yet Asia-Pacific is set to post a 15.1% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global GRC Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying global data-privacy regulations | +2.1% | Global, EU, and North America are leading | Medium term (2-4 years) |

| Proliferation of cloud-native applications | +1.8% | Global, Asia-Pacific, and North America | Short term (≤ 2 years) |

| Surge in cyber-insurance underwriting requirements | +1.5% | North America and the EU, expanding to the Asia-Pacific | Medium term (2-4 years) |

| Expansion of ESG reporting mandates | +1.4% | EU leading, North America and Asia-Pacific following | Long term (≥ 4 years) |

| AI-driven predictive analytics in risk | +1.2% | North America and the EU, spillover to the Asia-Pacific | Short term (≤ 2 years) |

| Board-level demand for continuous controls | +1.0% | Global, mature markets leading | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intensifying Global Data-Privacy Regulations

Cross-border data privacy mandates are multiplying, and stiff financial penalties are forcing multinationals to replace patchwork toolsets with end-to-end platforms that automate evidence gathering and breach notification. New regimes such as the Digital Operational Resilience Act enlarge the scope of reportable incidents and impose strict third-party oversight, prompting enterprises to consolidate data-mapping, consent management, and vendor-risk workflows inside a single Governance, Risk, and Compliance (GRC) Software market platform. The cascading nature of non-compliance—where a lapse in one jurisdiction can trigger parallel investigations elsewhere—elevates the value of real-time dashboards that surface control gaps by geography. Vendors are responding with policy libraries updated daily against more than 400 global statutes, while integrated workflow engines route remediation tasks to line-of-business owners. Platforms that deliver machine-readable audit trails are achieving faster regulator sign-offs and lowering external-audit fees, reinforcing a cycle of budget reallocation from manual spreadsheets to AI-augmented compliance hubs.

Proliferation of Cloud-Native Applications

Microservices, containers, and serverless architectures generate ephemeral resources that evade traditional audit snapshots, making continuous controls monitoring indispensable. Modern platforms now embed Kubernetes admission-controller hooks that validate policy at deploy time, streaming telemetry into risk models that recalculate heat maps every few seconds. This dynamic oversight is especially critical in Asia-Pacific, where digital-first start-ups deploy code hundreds of times per day and regulators are mandating operational-resilience disclosures. Real-time correlation of configuration drift, vulnerability posture, and compliance posture cuts mean-time-to-detect for policy violations from weeks to minutes, helping boards justify additional investment in the Governance, Risk, and Compliance (GRC) Software market. Cloud service providers are partnering with GRC vendors to publish compliance APIs that remove the need for agent installation, reducing onboarding friction for small teams. As a result, cloud-native integration has shifted evaluation criteria from checkbox support for a framework to latency, scale, and automated remediation depth.

Surge in Cyber-Insurance Underwriting Requirements

Rising claim volumes and loss ratios have forced cyber insurers to escalate pre-binding questionnaires into continuous assurance programs. Carriers now request API-level access to policy, control, and incident data housed within Governance, Risk, and Compliance (GRC) Software market deployments to price coverage dynamically.[2]CRC Group, “2025 Cyber State of the Market at a Glance,” crcgroup.com Enterprises that can furnish automated evidence of multifactor authentication, privilege governance, and patching cadence receive premium reductions and higher coverage limits, creating a financial incentive for platform adoption. The integration of actuarial engines within leading suites allows risk managers to translate technical control scores into monetary exposure, streamlining negotiations with underwriters. In North America, where coverage penetration is highest, insurers increasingly embed preferred-vendor clauses that expedite claim adjudication when evidence originates from certified solutions. This symbiotic ecosystem is converting cyber-insurance requirements from a barrier into an accelerant for market growth.

Expansion of ESG Reporting Mandates

Mandatory sustainability disclosures are widening beyond carbon to encompass biodiversity, labor practices, and board diversity, expanding the data universe Governance, Risk, and Compliance (GRC) platforms must govern. The EU Corporate Sustainability Reporting Directive obliges more than 50,000 companies to publish audited ESG statements, while Asia-Pacific exchanges roll out climate-related financial-risk guidelines. Vendors have responded by integrating carbon-accounting engines capable of ingesting utility bills, travel data, and supplier emission reports into the Governance, Risk, and Compliance (GRC) Software market framework. Automated variance analysis flags anomalies in emission trajectories, and scenario modeling aligns net-zero pathways with financial planning. Boards leverage consolidated dashboards that juxtapose ESG metrics with traditional risk indicators, enabling a holistic view of enterprise resilience. Forward-looking firms are embedding green-taxonomy rules inside procurement workflows, ensuring only suppliers with verified science-based targets enter approved vendor lists, thereby extending compliance accountability deep into the value chain.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complexity and cost of multi-jurisdictional compliance | -1.8% | Global, acute in multinational enterprises | Long term (≥ 4 years) |

| Shortage of in-house GRC domain expertise | -1.2% | Global, severe in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Regulatory uncertainty around AI governance | -0.9% | North America and the EU are leading | Short term (≤ 2 years) |

| Vendor lock-in concerns in integrated suites | -0.7% | Global, concentrated in large enterprises | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Complexity and Cost of Multi-Jurisdictional Compliance

Fragmented rulebooks add overlapping documentation duties that inflate the total cost of compliance by USD 780 billion annually. Each divergence—be it reporting thresholds, retention periods, or risk-assessment cadences—multiplies tooling, process, and staffing demands. Multinationals that lack an orchestrated Governance, Risk, and Compliance (GRC) Software market backbone juggle separate instances for anti-corruption, privacy, and operational-resilience programs, creating data silos and audit fatigue. Platform unification drives up-front licensing fees yet delivers payback through reduced external-consultant spend and fewer regulatory fines. While regional harmonization efforts such as Basel III offer partial convergence, new country-specific regimes like France’s Sapin II or Germany’s Supply-Chain Act continue to proliferate, keeping cost pressures acute over the long term.

Shortage of In-House GRC Domain Expertise

Demand for professionals who blend legal interpretation, cyber-risk quantification, and automation skills far outstrips supply, particularly in emerging markets. Organizations compensate by engaging managed-service providers, which in turn propels the services segment of the Governance, Risk, and Compliance (GRC) Software market. However, external reliance inflates operating expenditure and can weaken institutional knowledge transfer. Vendors are introducing low-code policy-builder interfaces, embedded training materials, and AI-driven control mapping in an effort to democratize platform usage. Despite these advances, the talent deficit remains a drag on adoption speed, especially for small and mid-tier firms that struggle to compete for scarce expertise.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain Momentum as Implementations Mature

Software retained a 71.65% revenue share in 2025 thanks to enterprise preference for integrated suites that consolidate risk, audit, privacy, and ESG modules. Yet services posted the fastest expected expansion at a 12.98% CAGR through 2031, underscoring a market shift toward outcome-based engagements that fuse technology enablement with subject-matter guidance. Managed service providers deploy platform accelerators, map controls to regional regulations, and operate continuous monitoring centers on behalf of clients with limited in-house staff. This hybrid delivery approach improves time-to-value for mid-sized buyers and shortens payback periods for large multinationals that must roll out across dozens of jurisdictions simultaneously. The Governance, Risk, and Compliance (GRC) Software market size for services is projected to climb steadily as vendors package advisory, configuration, and run-time operations into subscription bundles. Enhanced post-deployment analytics that benchmark control maturity across peer cohorts create cross-sell pathways for consulting arms eager to monetize insights through remediation roadmaps.

Platform suppliers are enriching software with AI-aided control mapping and natural-language policy ingestion, decreasing the manual effort requirement for baseline deployment. They also expose open APIs to facilitate ecosystem integrations with cyber range testing, e-discovery, and low-code workflow tools. This extensibility attracts partners that extend core capabilities, stimulating indirect revenue streams. Despite automation advances, complex configuration tasks—such as multi-ledger segregation of duties or fine-grained data-sovereignty partitioning—still require specialist input, ensuring that the services revenue pool remains buoyant. Over the forecast window, enterprise buyers are expected to allocate an increasing share of total program budgets to managed capabilities, reinforcing the dual-track expansion of software and services within the Governance, Risk, and Compliance (GRC) Software market.

By Deployment Mode: Cloud-First Architectures Redefine Control

Cloud deployments accounted for 62.90% of revenue in 2025 and are on course to register a 13.85% CAGR, reflecting enterprise appetite for elastic scalability and collaborative oversight. Continuous controls monitoring delivered as a service allows risk teams to interrogate real-time telemetry drawn from SaaS, infrastructure-as-a-service, and on-premises connectors without the capex burden of local hardware. This architecture underpins faster policy updates, automated compliance evidence collection, and remote audit access, qualities valued by distributed workforces. The Governance, Risk, and Compliance (GRC) Software market size for cloud solutions is forecast to outpace on-premises equivalents as integration blueprints mature and as vendors achieve compliance with stringent data-residency statutes through region-specific tenancy.

On-premises deployments will persist in segments such as defense, public safety, and critical infrastructure, where air-gapped environments remain mandatory. These buyers demand hardened appliances, internal API gateways, and offline reporting capabilities. Nonetheless, vendors are introducing containerized editions that can run either in customer data centers or sovereign clouds, blurring the deployment boundary. Migration roadmaps often begin with non-production workloads in hosted sandboxes before extending to regulated data sets once encryption, key management, and access-segregation standards are validated. Hybrid orchestration consoles provide unified dashboards spanning both modes, ensuring policy consistency and audit traceability across heterogeneous estates. Consequently, the Governance, Risk, and Compliance (GRC) Software market continues its transformation toward a “cloud when possible, on-prem where required” paradigm that balances performance, sovereignty, and cost.

By Organization Size: Democratization Fuels SME Uptake

Large enterprises retained 69.60% of 2025 spending, leveraging deep budgets to customize workflows that align with complex internal hierarchies and multi-country footprints. Yet small and medium-sized enterprises are projected to log a 13.02% CAGR as subscription-based packaging reduces entry barriers. Pre-configured control libraries and guided onboarding wizards accelerate time-to-compliance for resource-constrained teams, enabling SMEs to meet escalating customer and partner due diligence demands. The Governance, Risk, and Compliance (GRC) Software market share held by SMEs is therefore primed to expand, propelled by procurement clauses that require third-party vendors to prove a robust governance posture as a prerequisite for contract award.

Tailored pricing tiers scale seat counts, data-retention thresholds, and framework coverage to firm size, preventing feature overload. Lightweight agentless integrations connect cloud accounting, HR, and ticketing systems, offering unified risk visibility without heavy IT lift. Nonetheless, mid-market firms grapple with governance challenges that slow AI and cloud initiatives, underscoring the need for bundled advisory hours and automated policy templates. Vendors that embed contextual training videos, natural-language chatbots, and community support forums directly inside the interface enjoy higher renewal rates. As frameworks such as ISO 27001, SOC 2, and PCI DSS expand their supplier clauses, SME adoption momentum will remain a structural growth lever for the overall Governance, Risk, and Compliance (GRC) Software market.

By Vertical: Healthcare Accelerates amid BFSI Leadership

BFSI held 24.60% of 2025 revenue, anchored by stringent capital adequacy, anti-money-laundering, and operational-resilience directives that demand granular risk classification, scenario analysis, and regulatory reporting. Institutions employ advanced modeling engines to align with Basel III rules while orchestrating third-party assurance across distributed fintech ecosystems. The Governance, Risk, and Compliance (GRC) Software market size tied to BFSI is projected to grow steadily as digital banking expands customer touchpoints and regulators intensify scrutiny of cyber incident disclosure.

Healthcare and life sciences are set to register a 14.15% CAGR through 2031, the fastest across verticals, fueled by the proliferation of electronic health records, telemedicine, and decentralized clinical trials. Platforms integrate FDA 21 CFR Part 11 workflows that enforce electronic signature validation, audit logging, and training attestation, reducing inspection findings. Beyond patient privacy, the vertical faces escalating ESG and supply-chain-integrity requirements, driving uptake of modules that trace ingredient provenance and monitor greenhouse gas emissions. Vendors that offer pre-validated templates aligned to global standards reduce deployment cycles, reinforcing the sector’s momentum within the Governance, Risk, and Compliance (GRC) Software market. Other industries—manufacturing, IT and telecommunications, government, energy, and retail—exhibit stable double-digit growth trajectories as sector-specific mandates emerge around operational technology security, spectrum allocation, and ethical sourcing.

Geography Analysis

North America commanded 39.55% of 2025 revenue, underpinned by mature regulatory frameworks, deep cyber-insurance penetration, and a high incidence of shareholder litigation that drives board accountability. Federal agencies now expect near-real-time breach notification, compelling firms to adopt continuous monitoring and automated evidence management embedded in leading Governance, Risk, and Compliance (GRC) Software market platforms. Consolidation among technology and consulting providers has also accelerated regional uptake by offering bundled advisory plus SaaS subscriptions that streamline procurement cycles.

Europe maintains a structurally large user base due to pioneering legislation such as GDPR and the upcoming EU AI Act, which extends accountability to algorithmic transparency and lifecycle monitoring. Banks, insurers, and energy operators must now submit Digital Operational Resilience Act self-assessments, creating fresh demand for scenario-testing engines that model ICT failure propagation. The Governance, Risk, and Compliance (GRC) Software market share associated with European buyers is therefore reinforced by policy activism that stresses both consumer protection and systemic stability. Vendors differentiate through localized data-processing zones, multilingual policy libraries, and in-platform cross-border data transfer checks that align with Schrems II requirements.

Asia-Pacific is projected to achieve a 15.1% CAGR, the highest globally, fueled by rapid digitization, fintech innovation, and expanding carbon-trading schemes. Governments across China, Japan, Korea, and Singapore have launched sustainability disclosure standards that mirror, yet diverge from, European rules, prompting multinationals to favor configurable platforms capable of addressing multiple frameworks in parallel. Regional SMEs increasingly adopt pay-as-you-grow pricing to meet stringent supplier-qualification metrics imposed by global brands, funneling incremental volume into the Governance, Risk, and Compliance (GRC) Software market. Meanwhile, Latin America, the Middle East, and Africa are at earlier stages of adoption but display rising interest as foreign direct investors require documented governance controls before releasing capital.

Competitive Landscape

The market reflects moderate concentration, with IBM, SAP, Oracle, and ServiceNow occupying prominent positions through comprehensive suites and extensive partner ecosystems. IBM’s March 2025 expansion of watsonx.governance introduced automated evaluation metrics for AI agents, positioning the firm as an early mover in algorithmic oversight.[4]IBM, “IBM’s Answer to Governing AI Agents,” ibm.com Kroll’s December 2024 acquisition of Resolver fused contextual threat intelligence with workflow automation, illustrating a trend toward vertically integrated platforms that encompass incident response, audit, and policy management. ServiceNow’s Unified Compliance Framework integration further demonstrates strategic moves that fold external libraries into native catalogs to accelerate control mapping.

Emerging challengers leverage cloud-native stacks and aggressive pricing to court the SME segment. Their differentiation lies in frictionless onboarding, automated evidence collection, and integration with marketplaces that connect with DevSecOps pipelines. Platform roadmaps converge on ESG, third-party risk, and cyber-insurance modules, areas still underserved by legacy tools. Vendors are also embedding no-code policy builders and conversational AI assistants to mitigate talent shortages that hamper user adoption.

Partnership ecosystems continue to widen. Cloud hyperscalers provide secure enclaves and regional data-residency zones, while cybersecurity startup alliances supply continuous attack-surface scanning that feeds risk scoring engines. This federated approach enables customers to swap components without dismantling core governance workflows, alleviating vendor lock-in concerns that previously restrained investment. Over the forecast horizon, sustained double-digit growth and recurring-revenue valuations are likely to drive further consolidation, accelerating the innovation cadence across the Governance, Risk, and Compliance (GRC) Software market.

GRC Software Industry Leaders

IBM Corporation

SAP SE

MetricStream, Inc.

NAVEX Global, Inc.

ServiceNow, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: IBM enhanced watsonx governance with AI security modules to manage ISO 42001 and EU-AI-Act compliance, partnering with AllTrue.ai for usage visibility.

- March 2025: IBM introduced life-cycle governance for AI agents, adding automated context-relevance and faithfulness evaluation metrics.

- January 2025: Diligent secured “Built for NetSuite” status for Diligent Boards, linking real-time financial metrics to leadership dashboards.

- December 2024: Kroll finalized the acquisition of Resolver, merging risk-intelligence analytics with governance workflows.

Global GRC Software Market Report Scope

| Software |

| Services |

| Cloud |

| On-Premises |

| Large Enterprises |

| Small and Medium-Sized Enterprises (SMEs) |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Manufacturing |

| IT and Telecommunications |

| Government and Public Sector |

| Energy and Utilities |

| Retail and Consumer Goods |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Software | ||

| Services | |||

| By Deployment Mode | Cloud | ||

| On-Premises | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium-Sized Enterprises (SMEs) | |||

| By Vertical | Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare and Life Sciences | |||

| Manufacturing | |||

| IT and Telecommunications | |||

| Government and Public Sector | |||

| Energy and Utilities | |||

| Retail and Consumer Goods | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What CAGR is projected for the GRC Software market through 2031?

The market is forecast to grow at a 10.84% CAGR, climbing from USD 21.04 billion in 2025 to USD 39.01 billion by 2031.

Which component category is expanding fastest within current platform deployments?

Managed and advisory services are expected to post a 12.98% CAGR, reflecting enterprise demand for expert-led implementations that accelerate time-to-value.

Why are cyber-insurance requirements influencing platform adoption?

Insurers now evaluate real-time evidence originating from GRC solutions to underwrite policies, rewarding firms with mature implementations through lower premiums and higher coverage limits.

Which region is set to record the highest regional growth rate?

Asia-Pacific is projected to lead with a 15.1% CAGR, driven by rapid digitization and expanding ESG and privacy mandates across multiple jurisdictions.

How are cloud-native architectures reshaping risk management?

Containerized workloads and microservices demand continuous controls monitoring, pushing buyers toward cloud-first GRC platforms that integrate with DevSecOps pipelines for real-time compliance validation.

What vertical is likely to outpace others in growth terms?

Healthcare and life sciences should post a 14.15% CAGR as digital health records, clinical-trial modernization, and FDA electronic-signature rules intensify governance requirements.

Page last updated on: