Governance, Risk And Compliance (GRC) Platforms Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

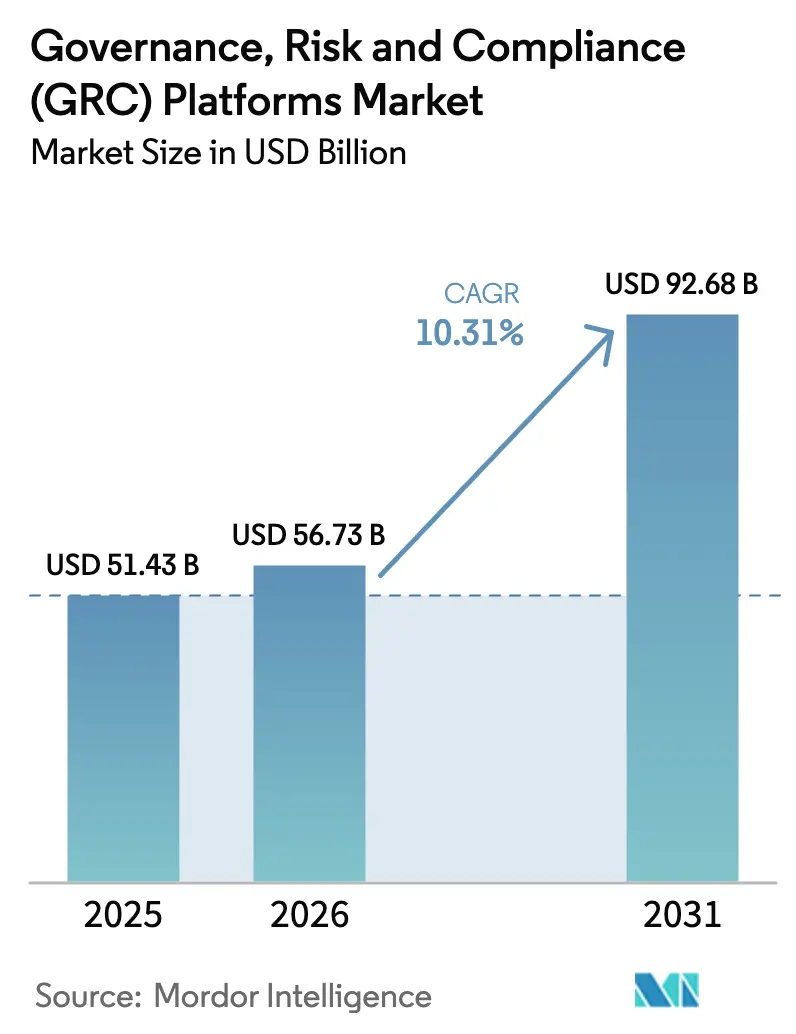

| Market Size (2026) | USD 56.73 Billion |

| Market Size (2031) | USD 92.68 Billion |

| Growth Rate (2026 - 2031) | 10.31% CAGR |

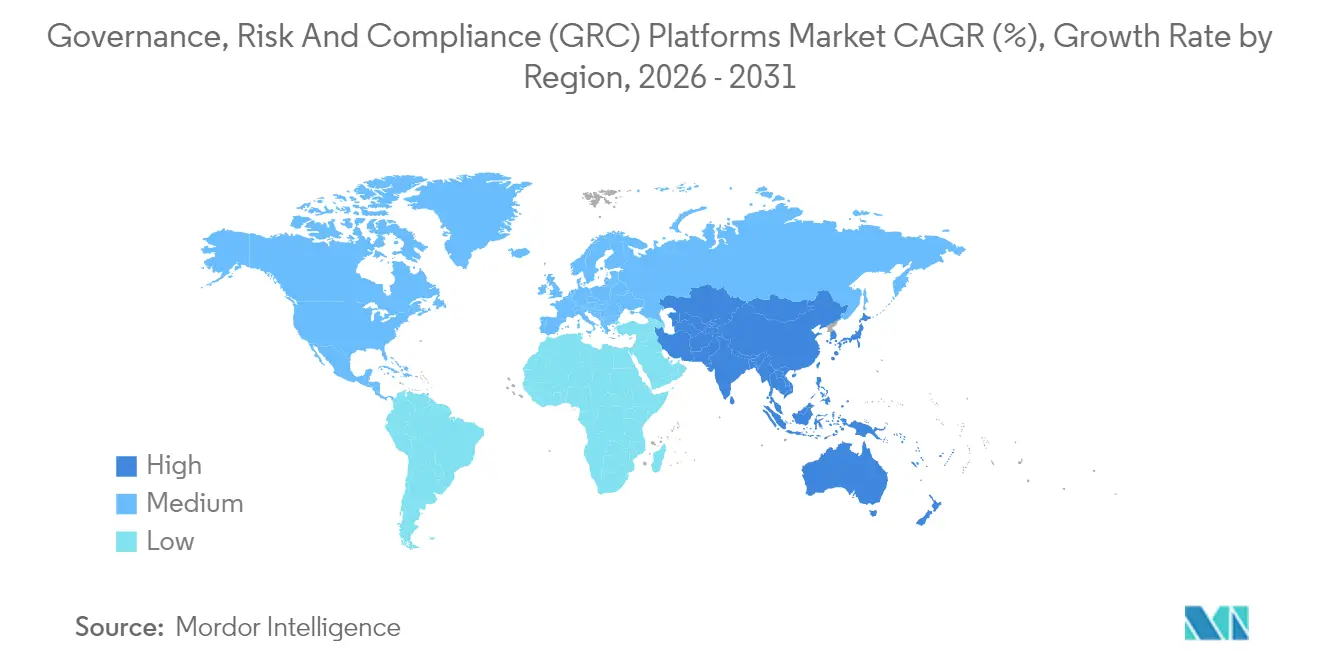

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

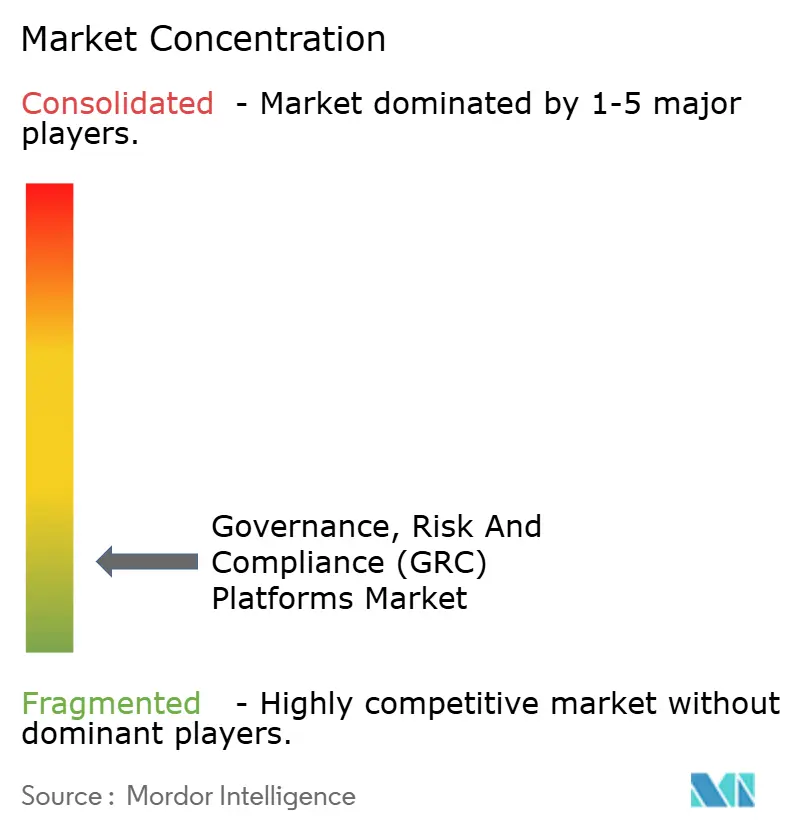

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Governance, Risk And Compliance (GRC) Platforms Market Analysis by Mordor Intelligence

The GRC platforms market size is expected to grow from USD 51.43 billion in 2025 to USD 56.73 billion in 2026 and is forecast to reach USD 92.68 billion by 2031 at 10.31% CAGR over 2026-2031. Intensifying regulatory complexity, mandatory ESG disclosures, and heightened cybersecurity reporting duties are recasting compliance platforms as strategic assets rather than cost centers. Predictive analytics powered by AI now enable proactive risk mitigation that reduces audit cycle times and speeds board decisions. Cloud deployment dominates as organizations decentralize workforces and seek scalable architectures that lower the total cost of ownership by up to 35%. Private-equity-backed consolidation, led by USD 3 billion-plus and GBP 1.05 billion deals, is accelerating platform integration to meet demand for unified governance ecosystems. North America leads current spending, while Asia-Pacific’s 15.1% CAGR signals outsized future growth as digitization and regulatory modernization converge.

Key Report Takeaways

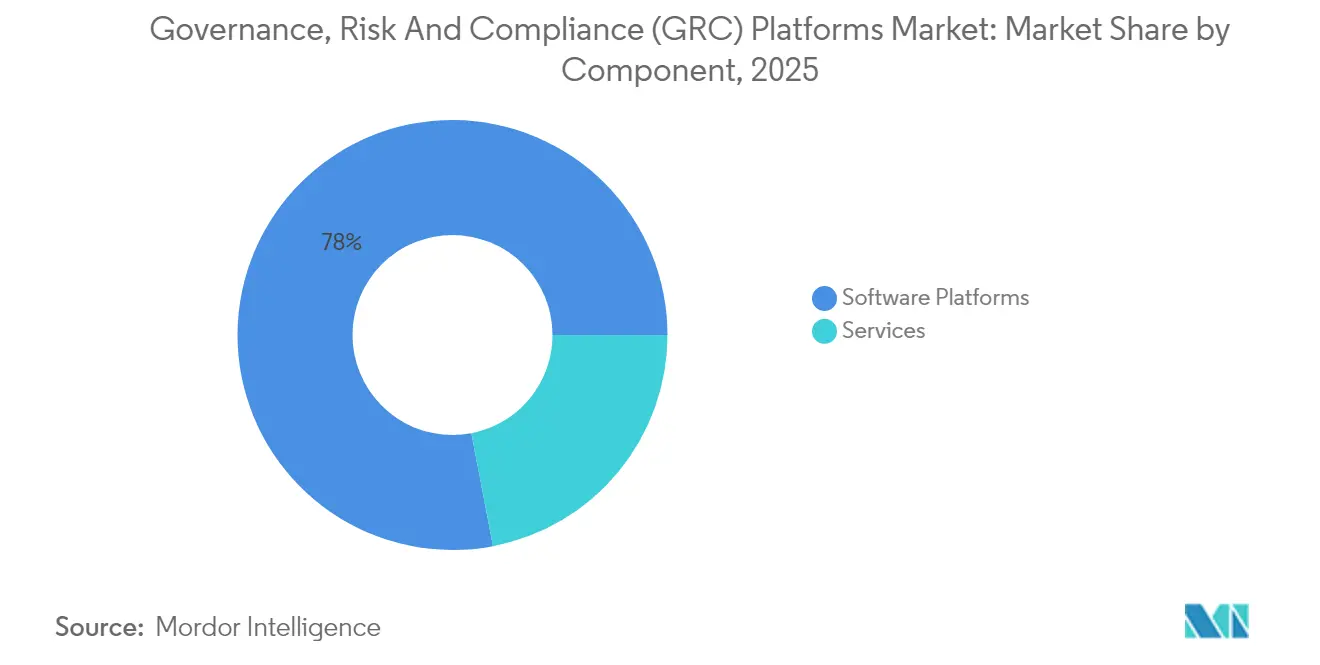

- By component, software platforms held 78.02% of the GRC platforms market share in 2025, while services recorded the fastest 12.74% CAGR through 2031.

- By deployment mode, cloud solutions captured 66.88% share of the GRC platforms market size in 2025 and are poised for a 14.16% CAGR through 2031.

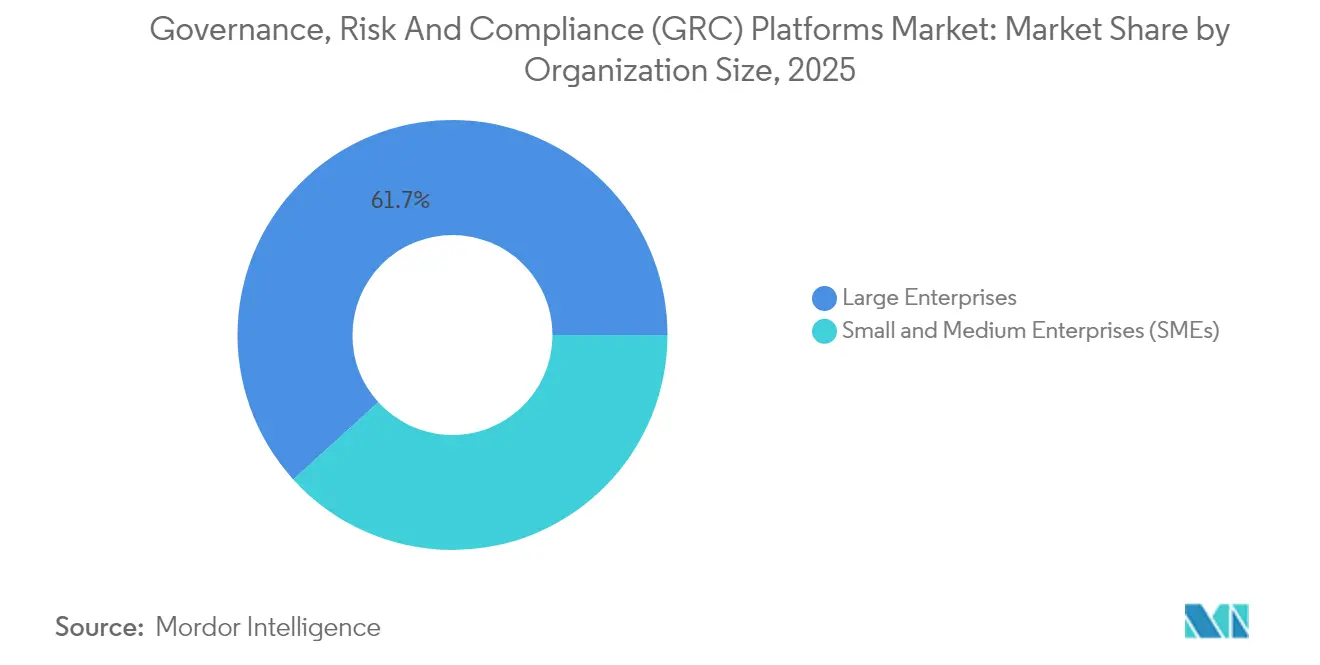

- By organization size, large enterprises accounted for a 61.72% share of the GRC platforms market in 2025, whereas small and medium enterprises exhibit a 14.89% CAGR to 2031.

- By industry vertical, BFSI led with 24.88% revenue share in 2025; healthcare and life sciences are projected to expand at a 15.58% CAGR through 2031.

- By geography, North America led with 40.85% revenue share in 2025; Asia-Pacific is projected to expand at a 14.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Governance, Risk And Compliance (GRC) Platforms Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating volume and complexity of global regulations | +2.8% | Global, with concentrated impact in North America and the EU | Medium term (2-4 years) |

| Rapid adoption of cloud-based GRC suites | +2.1% | Global, led by North America, is expanding in the Asia-Pacific | Short term (≤ 2 years) |

| Integration of cybersecurity and data privacy mandates | +1.9% | North America and the EU are primary, Asia-Pacific is emerging | Medium term (2-4 years) |

| Board-level demand for integrated ESG–GRC reporting | +1.6% | Global, with the EU leading, North America following | Long term (≥ 4 years) |

| AI-driven predictive risk analytics uptake | +1.4% | North America and EU core, selective Asia-Pacific adoption | Medium term (2-4 years) |

| Insurance-premium incentives for demonstrable governance | +0.7% | North America primary, expanding to the EU and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating volume and complexity of global regulations

Financial institutions grappled with more than 1,200 separate rules and 250 regulatory updates each day in 2024, turning compliance into a nonstop exercise.[1]Shaun Hunt, “Integrated Governance, Risk Management and Compliance,” Tech Mahindra, insights.techmahindra.com The SEC’s 2024 cybersecurity-incident disclosure rules obligate public companies to report material breaches within four business days. Europe’s Corporate Sustainability Reporting Directive and California’s climate laws broaden mandatory emissions reporting. Manual processes cannot keep pace, so enterprises deploy automated GRC workflows that trim audit labor by double-digit percentages. Vendors embed rule libraries that update in real time, shielding enterprises from penalty exposure. The resulting investment reinforces the GRC platforms market as foundational infrastructure for global operations.

Rapid adoption of cloud-based GRC suites

Cloud architecture secured 67.3% of 2024 deployments as enterprises prioritized anywhere-access controls during pandemic-era workplace shifts. Subscription revenues of USD 10.6 billion in 2024 demonstrated a hunger for scalable compliance capabilities. Cloud platforms integrate AI engines that scan millions of control points daily, issuing alerts within seconds. Mid-market companies achieve 30-35% cost savings versus on-premises installations. Continuous software upgrades minimize versioning risk and speed time-to-value. The trend will intensify as data residency rules evolve, prompting vendors to open additional regional cloud zones to satisfy localization mandates.

Integration of cybersecurity and data-privacy mandates

Cybersecurity moved from server rooms to boardrooms after the SEC formalized breach-reporting deadlines. Insurers now grant premium discounts to firms that document controls through integrated GRC dashboards. Apple’s partnership with Cisco illustrates how technology stacks combine with insurance incentives to reward secure operational behavior. GRC platforms link vulnerability metrics with regulatory control frameworks, creating network effects where stronger security improves compliance posture. Enterprises consequently embed cyber risk scoring into enterprise-wide risk registers, supporting strategic capital allocation.

Board-level demand for integrated ESG–GRC reporting

Mandatory climate-risk disclosures adopted in March 2024 signal that sustainability metrics now carry the same gravitas as financial statements.[2]Securities and Exchange Commission, “SEC Adopts Rules to Enhance and Standardize Climate-Related Disclosures for Investors,” sec.gov Boards ask for single dashboards that reconcile emissions data, supply-chain labor metrics, and governance controls. An EY 2025 survey found companies with mature governance frameworks were twice as likely to meet climate targets. Investor appetite amplifies pressure, with 85% of fund managers incorporating ESG factors into valuations. Integrated ESG–GRC suites streamline external assurance, accelerating report cycles and enhancing market perception.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High implementation and legacy-integration costs | -1.8% | Global, more pronounced in mature markets with legacy systems | Short term (≤ 2 years) |

| Shortage of skilled GRC professionals | -1.2% | Global, acute in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Platform lock-in concerns amid vendor consolidation | -0.9% | North America and the EU are primary, emerging in the Asia-Pacific | Medium term (2-4 years) |

| AI-algorithm transparency scrutiny is delaying deals | -0.6% | EU leading, North America following, limited Asia-Pacific impact | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High implementation and legacy-integration costs

Enterprises often under-scope data migration, process redesign, and staff training needs, causing budgets to overrun by 40-60%. On-premise environments add hardware refresh obligations that undermine ROI. Complex legacy systems require interface layers that prolong deployment timelines. Yet post-implementation studies show 327% three-year ROI where integration succeeds. Vendors now package rapid-start templates and managed services to reduce risk, but upfront capital outlays remain a near-term brake.

Shortage of skilled GRC professionals

The pace of regulatory change outstripped workforce development, leaving gaps in AI model governance and multi-jurisdiction rule mapping. Asia-Pacific faces a particularly tight talent supply, prompting MetricStream to appoint a dedicated regional managing director in Singapore to bolster service delivery. Organizations respond by outsourcing operations or funding internal academies, yet elevated wage inflation and high turnover temper market momentum. Platforms embed low-code configuration to ease administration, but deep domain expertise remains irreplaceable for sustained success.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platform dominance reinforced by managed-service momentum

Software platforms captured 78.02% of 2025 demand, anchoring the GRC platforms market foundation with unified workflows that replace point solutions. Services, however, display a 12.74% CAGR through 2031 as enterprises seek implementation, integration, and continuous monitoring assistance. Many organizations reallocate audit budgets to managed services that fine-tune AI models and maintain regulatory libraries. In 2025, ServiceNow’s subscription line reached USD 3.005 billion, underscoring customer preference for broad platforms that centralize risk control. Specialist consultants co-deliver platform rollouts, reflecting the reality that technology alone cannot guarantee compliance effectiveness. Joint offerings such as AuditBoard-Protiviti accelerators underscore the synergy between software and advisory talent.

The services surge signals a long-term shift where continuous compliance operations are partly outsourced. Vendors extend managed offerings that monitor control health, deliver quarterly rule updates, and provide board-ready reports, freeing internal teams for strategic tasks. As AI capabilities deepen, enterprises pay for data-science expertise to validate model transparency and guard against bias. The dual-track growth of platforms and services anchors a durable revenue mix that sustains the GRC platforms market over the forecast horizon.

By Deployment Mode: Cloud migration underpins modern compliance

Cloud solutions held a 66.88% share in 2025 and will outpace on-premises at a 14.16% CAGR. Multi-tenant architectures cut maintenance overhead, deliver instant feature updates, and support globally dispersed teams that now constitute the norm. The GRC platforms market size for cloud deployments is projected to expand steadily as organizations retire legacy data centers in favor of SaaS contracts tied to usage metrics. Continuous monitoring functions running in cloud environments analyze telemetry at scale, surfacing anomalies before auditors arrive.

On-premises installations persist for entities with strict data localization or air-gapped security policies, notably in defense and critical infrastructure. Yet even these organizations pilot hybrid models that push non-sensitive modules to the cloud. Vendors answer sovereignty concerns with regional data farms and encryption controls that satisfy European GDPR and similar statutes. Over time, declining hardware budgets and rising board expectations for real-time oversight will tilt procurement decisively to cloud, reinforcing the architecture’s position at the heart of the GRC platforms market.

By Organization Size: SME adoption democratizes enterprise-grade governance

Large enterprises commanded a 61.72% share in 2025, driven by intricate regulatory obligations and deep budgets. Small and medium enterprises, however, are forecast to post a 14.89% CAGR, turning the GRC platforms market into a more evenly distributed arena. Cloud subscription pricing, pre-configured industry templates, and low-code customization shrink barriers for firms that once relied on spreadsheets. SMEs gain competitive credibility in supply-chain audits by demonstrating automated control frameworks, unlocking contracts with multinationals.

For large enterprises, attention pivots to optimization. They leverage AI to correlate controls against key performance indicators, reducing duplicative testing and cutting annual audit efforts by double-digit percentages. Vendors release tiered offerings: foundational packages for SMEs, advanced analytics for global conglomerates. The resulting product ladder maintains profitability while ensuring addressable-market expansion, underpinning future GRC platforms market growth.

By Industry Vertical: Financial services steady, healthcare surges

Financial services retained leadership with 24.88% revenue, reflecting sophisticated risk cultures and persistent regulatory scrutiny. Nevertheless, sector growth moderates as banks migrate from initial deployments to incremental enhancements. Healthcare and life sciences demonstrate a leading 15.58% CAGR as patient-data privacy, clinical-trial integrity, and supply-chain transparency drive platform uptake. In many regions, hospital groups must map data flows in real time to comply with cross-border transfer rules, making integrated GRC suites indispensable.

Manufacturing, energy, and government also accelerate adoption as ESG, cyber-resilience, and anti-corruption laws expand. Vendors increasingly tailor taxonomies and control libraries to each sector, recognizing that risk terminology differs sharply between a refinery and a retail bank. Vertical specialization, combined with modular design, positions platforms to capture the diverse demand patterns that characterize the evolving GRC platforms market.

Geography Analysis

North America retained a 40.85% share in 2025, propelled by sophisticated regulatory frameworks and deep enterprise IT budgets. The SEC’s cybersecurity incident rules and climate-reporting mandates galvanized investments, encouraging firms to transition manual logs into living control matrices. Private-equity interest remained high, evidenced by USD 3 billion-plus and multibillion-dollar takeovers that underscore faith in subscription revenue durability.

Asia-Pacific recorded the fastest 14.63% CAGR. Nations including Australia and Singapore tightened anti-bribery statutes while broadening data-protection enforcement, prompting companies to embed compliance automation from the outset. Digital-first business models across e-commerce and fintech amplify risk exposures, and local regulators increasingly require demonstrable governance to secure foreign investment. Vendors respond with multilingual interfaces and region-specific rule sets hosted in local cloud zones. MetricStream’s new Singapore hub underscores the vendor's commitment to sustaining customer success in diverse legal landscapes.

Europe sits at the nexus of sustainability and data privacy policy leadership. The Corporate Sustainability Reporting Directive and anticipated Corporate Sustainability Due Diligence Directive extend mandatory disclosures, compelling enterprises to harmonize environmental metrics with financial reports. Ideagen’s GBP 1.05 billion acquisition marks strategic capital allocation toward platforms capable of spanning multiple European jurisdictions. Data-sovereignty strictures prompt in-region hosting and algorithmic explainability, adding complexity but also heightening demand for centralized GRC orchestration.

Middle East and Africa and South America remain emerging yet promising markets as governments introduce cybersecurity and anti-money-laundering statutes aligned with global standards. Multinationals operating in these regions deploy GRC suites to ensure group-wide control consistency, indirectly fostering domestic adoption. The interplay of regional regulatory evolution and global supply-chain integration signals that the GRC platforms market will globalize further, rewarding vendors that localize swiftly while retaining platform coherence.

Competitive Landscape

The market remains moderately fragmented despite accelerating consolidation. Hg’s USD 3 billion-plus acquisition of AuditBoard, Goldman Sachs-Blackstone’s investment in NAVEX, and Hg’s GBP 1.05 billion Ideagen deal highlight investor conviction in recurring compliance spending. Scale economies from these transactions fund AI development, international sales teams, and vertical solution packages.

Technology differentiation centers on artificial intelligence. MetricStream’s AiSPIRE uses large-language-model inference to recommend controls, while AuditBoard’s risk analytics claim 20 million manual hours saved across its customer base. Vendors embed explainability dashboards that trace model outputs to underlying data sources, addressing emerging regulatory scrutiny over algorithmic transparency.

Strategic moves increasingly reflect ecosystem partnerships. ServiceNow integrates with cloud-security posture management tools to furnish single-pane visibility across IT, risk, and compliance, bolstering its USD 10.6 billion subscription stream. AuditBoard and Protiviti released connectors that merge ERP data with audit workflows, shortening fieldwork cycles. LogicGate emphasized mid-market reach through low-code configurability and posted record growth in 2025.

White-space opportunities lie in SME segments and converging ESG-cyber-risk domains. Vendors that blend modular architecture, vertical libraries, and embedded AI stand to command premium valuations. Customer decisions hinge on measurable ROI, proven security credentials, and the ability to future-proof against shifting regulations, reinforcing competitive dynamics that reward continual innovation.

Governance, Risk And Compliance (GRC) Platforms Industry Leaders

Diligent Corporation

NAVEX Global, Inc.

MetricStream, Inc.

Archer Integrated Risk Management

ServiceNow, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Goldman Sachs Alternatives and Blackstone acquired a majority stake in NAVEX to accelerate platform expansion.

- July 2025: Hg completed the GBP 1.05 billion (USD 1.33 billion) takeover of Ideagen, earmarking funds for product and M&A investment.

- June 2025: Scytale acquired AudITech, adding SOX ITGC automation to its compliance suite.

- February 2025: AuditBoard appeared in G2’s 2025 Best Software Awards, underscoring customer satisfaction.

Global Governance, Risk And Compliance (GRC) Platforms Market Report Scope

| Software Platforms |

| Services |

| On-Premise |

| Cloud |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Banking, Financial Services and Insurance (BFSI) |

| Information Technology and Telecom |

| Healthcare and Life Sciences |

| Manufacturing |

| Government and Public Sector |

| Energy and Utilities |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Software Platforms | ||

| Services | |||

| By Deployment Mode | On-Premise | ||

| Cloud | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By Industry Vertical | Banking, Financial Services and Insurance (BFSI) | ||

| Information Technology and Telecom | |||

| Healthcare and Life Sciences | |||

| Manufacturing | |||

| Government and Public Sector | |||

| Energy and Utilities | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Southeast Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the GRC platforms market in 2026?

The market stands at USD 56.73 billion in 2026 and is expected to reach USD 92.68 billion by 2031.

Which region expands fastest for governance, risk, and compliance platforms?

Asia-Pacific posts the highest 14.63% CAGR through 2031 due to rapid regulatory modernization and digitization.

Which deployment model leads current adoption?

Cloud deployment secured 66.88% of 2025 demand and continues to outpace on-premises solutions.

What industry vertical will grow quickest to 2031?

Healthcare and life sciences lead with a forecast 15.58% CAGR driven by data privacy and clinical governance mandates.

Why are services growing faster than core software?

Organizations need implementation expertise, managed monitoring, and AI model tuning, driving a 12.74% CAGR in services.

What factor most restrains near-term growth?

High implementation and legacy-system integration costs, which can add 40-60% to project budgets, remain the chief constraint.

Page last updated on: