GCC Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

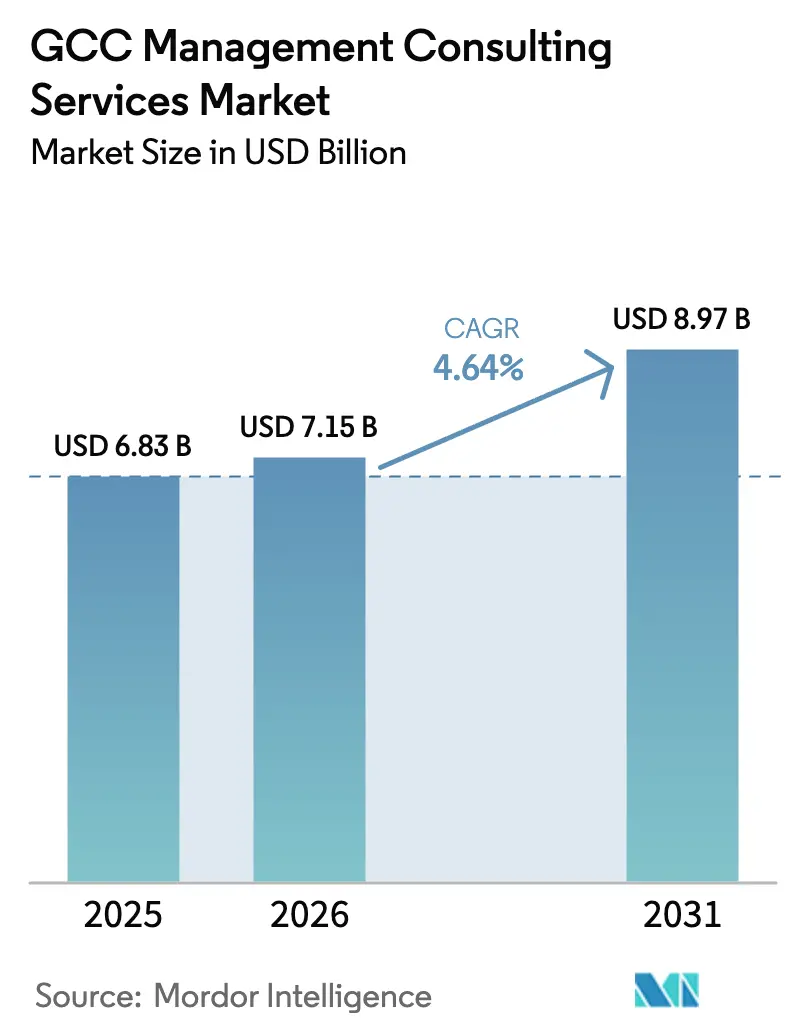

| Base Year Market Size (2025) | USD 6.83 Billion |

| Market Size (2026) | USD 7.15 Billion |

| Market Size (2031) | USD 8.97 Billion |

| Growth Rate (2026 - 2031) | 4.64% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Management Consulting Services Market Analysis by Mordor Intelligence

The GCC management consulting services market size was valued at USD 6.83 billion in 2025 and estimated to grow from USD 7.15 billion in 2026 to reach USD 8.97 billion by 2031, at a CAGR of 4.64% during the forecast period (2026-2031). Demand stays resilient because governments are channeling record public-sector budgets into transformation programs, while multinational firms outsource complex regulatory, digital, and ESG mandates to local advisers. Saudi Arabia’s Vision 2030 pipeline alone tops USD 500 billion in planned outlays. The UAE’s Digital Strategy 2025-2027 allocates AED 13 billion (USD 3.54 billion) to embed over 200 AI solutions across all government interactions. Localisation rules, mandatory ESG disclosures, and the professionalisation of family-owned conglomerates further enlarge opportunity pools for advisory firms. Meanwhile, moderate competition persists as global consultancies balance regional headquarters commitments with stricter data-sovereignty rules.

Key Report Takeaways

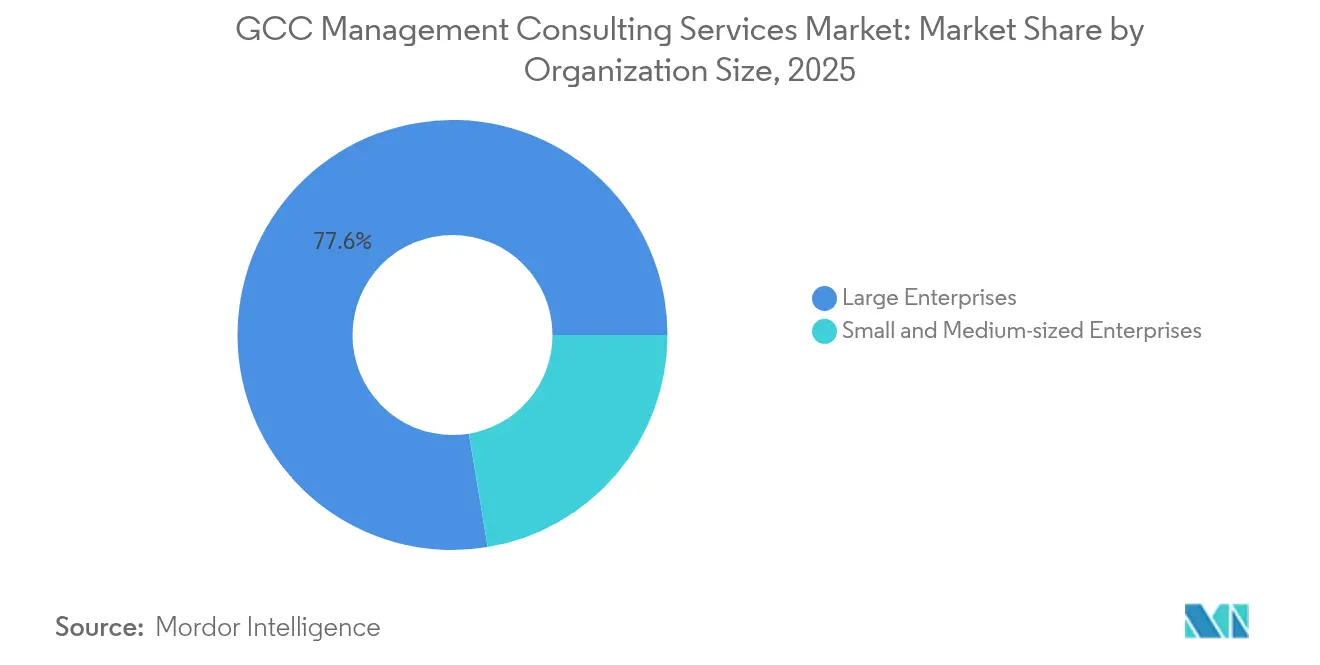

- By organization size, large enterprises captured 77.62% of the GCC management consulting services market size in 2025; small and medium enterprises are forecast to grow at 5.67% CAGR between 2026 and 2031.

- By service type, operations consulting led with 34.33% revenue share in 2025, whereas technology consulting is projected to rise at 7.48% CAGR through 2031.

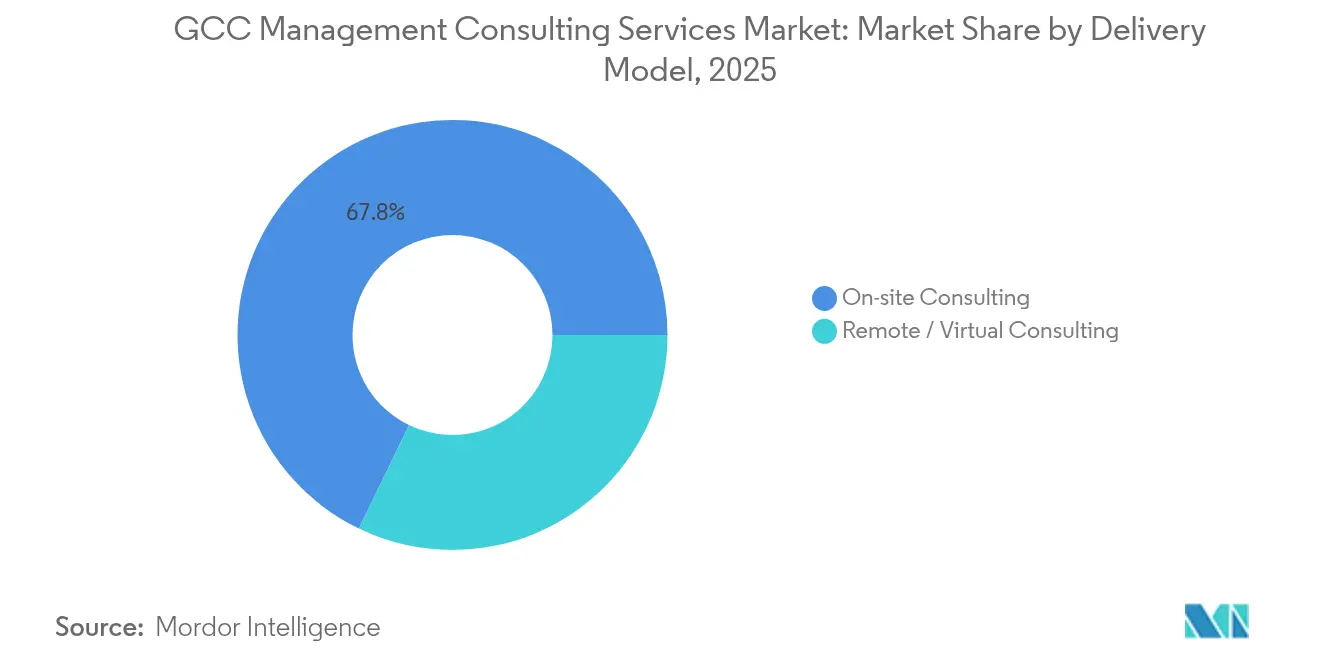

- By delivery model, on-site consulting represented 67.84% of revenues in 2025; remote and virtual delivery is anticipated to post 5.02% CAGR to 2031.

- By end-user industry, financial services accounted for 27.35% of spending in 2025, while healthcare consulting demand is forecast to accelerate at 11.12% CAGR through 2031

- By country, Saudi Arabia held 45.12% of the GCC management consulting services market share in 2025, while the UAE is expected to expand at a 6.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-backed mega-projects fuelling demand | +1.2% | Saudi Arabia, UAE, Qatar | Long term (≥ 4 years) |

| Accelerating digital transformation agendas | +0.9% | GCC-wide | Medium term (2-4 years) |

| Public-sector outsourcing of strategy and implementation | +0.7% | Saudi Arabia, UAE | Medium term (2-4 years) |

| Mandatory ESG disclosure needs | +0.5% | GCC-wide | Short term (≤ 2 years) |

| Localisation policies driving joint-venture advisory | +0.4% | Saudi Arabia, UAE | Long term (≥ 4 years) |

| Professionalisation of family-owned conglomerates | +0.3% | GCC-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government-backed Mega-projects Fuelling Demand

Roughly USD 1.1 trillion in GCC infrastructure investments keeps advisory pipelines filled well beyond 2030. Saudi Arabia’s NEOM development alone spans 26,500 sq km and demands expertise in urban planning, environmental permitting and advanced technology integration. Qatar’s Ashghal is modernising highways, drainage and smart-city assets under National Vision 2030, requiring continuous program-management guidance. [1]Public Works Authority, “Overview of Ashghal,” ashghal.gov.qaThe UAE aims to lift GDP to USD 6 trillion by 2050, driving advisory needs in industrial diversification and logistics optimisation. Oman Vision 2040 seeks 6% annual growth, supported by foreign-investment reforms that open fresh market-entry mandates.

Accelerating Digital Transformation Agendas

Abu Dhabi targets 100% sovereign-cloud adoption and full process automation across 200+ AI use cases, anchoring long-term demand for cybersecurity, cloud-migration, and AI strategy support. Saudi policies such as the Cloud First framework extend digital-infrastructure spending to private enterprises. The UAE-Google Cloud cybersecurity hub aims to avert USD 6.8 billion in cybercrime losses by 2030 and will create over 20,300 skilled jobs, stimulating advisory engagements in risk and talent planning. [2]Google Cloud Press Corner, “Empowering Cyber Defense,” googlecloudpresscorner.com Healthcare IT spending is rising at 9.2% CAGR to USD 7.9 billion by 2028 as 75% of public facilities implement EHR systems, widening technology-consulting pipelines. Oman’s USD 400 million AI program further expands specialist advisory opportunities.

Public-sector Outsourcing of Strategy and Implementation

Saudi Arabia’s Health Sector Transformation Programme is moving 290 hospitals and 2,300 primary centers toward private models, creating multi-year engagements in governance, PPP structuring, and digital health. The UAE’s Malaffi platform links 1.7 billion clinical records, illustrating continuous advisory needs throughout large-scale public-private rollouts. Qatar adopts ISSB-aligned reporting by 2026, boosting ESG compliance consulting. UNDP’s work on 17 Saudi cities shows the role external advisers play in urban-prosperity metrics. Oman’s unified public-finance system roll-out requires change management and SAP optimisation support.

Mandatory ESG Disclosure Needs

The UAE’s Climate Responsibility Law makes greenhouse-gas reporting compulsory for all entities by May 2025, sparking short-cycle projects in carbon baselining and roadmap design. Qatar’s plan to embed ISSB rules intensifies demand for double-materiality assessments. US-listed GCC corporates must satisfy the SEC’s March 2024 climate-risk rules, adding cross-border compliance complexity. Aramco’s JV with Baosteel underscores the interdependence between heavy-industry decarbonisation and advisory input on lifecycle emissions. The EU’s CSRD further widens the client base to exporters needing scope-3 emissions baselines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Restrictions on foreign consultancies | -0.8% | Saudi Arabia, UAE | Medium term (2-4 years) |

| Consultant salary inflation and talent shortages | -0.6% | GCC-wide | Short term (≤ 2 years) |

| Rise of in-house strategy teams | -0.4% | Saudi Arabia, UAE | Long term (≥ 4 years) |

| Cultural resistance among family businesses | -0.3% | GCC-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Restrictions on Foreign Consultancies

Saudi regulators barred PwC from Public Investment Fund work in March 2025, signalling stronger data-sovereignty enforcement and boosting local content requirements. The Kingdom’s regional-headquarters mandate obliges multinationals to employ at least 15 staff locally to qualify for government contracts, inflating cost bases. [3]Mayer Brown, “Updates on Saudi Arabia’s Regional Headquarters Program,” mayerbrown.com Emiratisation policies add parallel pressures, with agencies increasingly scoring bids on knowledge-transfer metrics. Together, the rules curb short-term entry of purely fly-in experts and may slow some foreign-led engagements.

Consultant Salary Inflation and Talent Shortages

AI, cybersecurity and ESG specialists remain scarce, lifting remuneration packages and narrowing project margins. Research on GCC AI-strategy implementation highlights dependency on expatriate talent, creating bottlenecks for new digital programs. Saudization prompts seasoned nationals to move into higher-paying government posts, leaving private firms scrambling for replacements. The UAE-Google Cloud center will hire 20,300 new professionals, intensifying regional competition for cyber skills. Healthcare digital projects such as Seha Virtual Hospital consume the same talent pool, compounding shortages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Organization Size: SMEs Drive Professionalization Wave

Large enterprises generated 77.62% of 2025 revenue, anchored by government-linked giants and multinationals coordinating multi-business-unit transformations. Seismic initiatives such as Aramco’s IKTVA program alone open consulting budgets exceeding USD 16 billion per year. The GCC management consulting services market size attached to these complex mandates supports high-value, multi-year retainers.

SMEs are projected to grow at 5.67% CAGR to 2031 as family-owned conglomerates formalise governance and succession structures. Mandatory sustainability reporting under the UAE Climate Law forces smaller firms to seek ESG advisory, while Saudi Vision 2030’s SME agency drives digital-upgrade vouchers that channel spend toward external consultants.

By Service Type: Technology Consulting Accelerates Digital Leadership

Operations consulting delivered the highest 34.33% share in 2025 as oil-to-chemicals majors and infrastructure owners streamlined cost bases and compliance processes. However, technology engagements are forecast to climb 7.48% CAGR, reflecting AI expenditure surges across public agencies. The GCC management consulting services market size tied to AI-native government programs now spans cloud architecture design, LLM integration and zero-trust security.

Parallel demand spikes for data-governance frameworks, telehealth platforms and cybersecurity roadmaps make technology the most contested growth frontier. Saudi Arabia’s Seha Virtual Hospital demonstrates how digital use cases translate into steady platform-maintenance retainers for consultancies.

By Delivery Model: Remote Consulting Gains Permanent Foothold

On-site delivery still controls 67.84% of 2025 spending because clients insist on in-person relationship building and secure data rooms. Mandatory local HQ rules in Saudi Arabia preserve this bias.

Virtual engagements, however, are expanding at 5.02% CAGR as sovereign-cloud coverage widens. The GCC management consulting services market share of remote projects benefits from Abu Dhabi’s TAMM platform, which confirms user acceptance of AI-enabled self-service formats. Hybrid models merge periodic on-site workshops with continuous virtual delivery, cutting travel costs while respecting cultural norms.

By End-user Industry: Healthcare Digitalization Drives Unprecedented Growth

Financial services led 2025 revenue at 27.35%, underpinned by USD 3.2 trillion in regional banking assets and aggressive fintech rollouts. Regulatory projects related to open banking, CBDCs and anti-money-laundering compliance sustain high consultancy utilisation.

Healthcare is rising fastest at 11.12% CAGR as governments push integrated EHR networks, telemedicine and precision-medicine analytics. The GCC management consulting services market size dedicated to health IT is boosted by UAE’s Malaffi and Saudi Arabia’s hospital-privatisation roadmap. Intensive advisory expertise is needed to mesh clinical protocols with AI decision-support tools, cyber standards and reimbursement models.

Geography Analysis

Saudi Arabia represented 45.12% of 2025 spending, anchored by Vision 2030’s USD 500 billion capital plan and the GCC management consulting services market size embedded in megaproject delivery. Programs such as IKTVA and the Health Sector Transformation Programme produce multi-disciplinary advisory demand across supply-chain localisation, PPP structuring and digital care. New data-classification rules heighten the premium on firms holding Saudi cloud infrastructure and deep Arabic talent pools.

The UAE is forecast to record 6.96% CAGR through 2031, the highest in the bloc, thanks to its ambition to become the world’s first AI-native government. Abu Dhabi’s AED 13 billion digital allocation guarantees a steady flow of AI, cloud and cyber mandates. Simultaneously, USD 6 trillion GDP diversification targets present strategic-planning work across clean energy, advanced manufacturing and global logistics corridors.

Qatar, Oman, Bahrain and Kuwait contribute stable mid-single-digit growth. Qatar’s Ashghal projects keep infrastructure advisers engaged while ISSB-aligned ESG rules add near-term compliance work. Oman’s Vision 2040 and 100% foreign-ownership law incentivise wave-by-wave advisory on SME incubation and venture-capital policy.

Competitive Landscape

Market concentration remains moderate as global firms still dominate high-value transformation deals but must now satisfy local hiring and data-hosting mandates. PwC’s exclusion from PIF contracts illustrates the risk of non-compliance with emerging sovereignty expectations. Firms invest in on-shore delivery centers, knowledge-transfer programs and joint ventures with national champions to retain eligibility.

Technology consulting capabilities have become the pivotal differentiator. Advisers able to marry strategy with hands-on AI engineering win contracts connected to Abu Dhabi’s sovereign-cloud rollout and Saudi Arabia’s national AI investments. Boutique GCC-based players gain share by leveraging cultural proximity, Arabic language fluency and lower fee structures.

At the same time, in-house strategy units inside sovereign wealth funds and ministries absorb portions of earlier outsourced scope, pressing advisers to shift toward specialist niches such as climate-risk modelling, quantum-compute readiness and family governance. Talent scarcity and salary inflation add cost tension, leading some firms to pilot offshore analyst hubs in India and Eastern Europe.

GCC Management Consulting Services Industry Leaders

McKinsey & Company Inc.

Accenture Middle East B.V.

PricewaterhouseCoopers (PwC) Middle East

Deloitte & Touche (M.E.) LLP

KPMG Lower Gulf Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Saudi Arabia unveiled a USD 1.5 billion expansion of AI infrastructure with Groq to strengthen national compute capacity.

- April 2025: The UAE Cyber Security Council and Google Cloud agreed to build a cybersecurity center of excellence projected to prevent USD 6.8 billion in losses by 2030.

- May 2025: Vanguard confirmed its first global capability center in Hyderabad, hiring 2,300 tech staff over four years.

- January 2025: Abu Dhabi launched the Digital Strategy 2025-2027 backed by AED 13 billion to become an AI-native government.

GCC Management Consulting Services Market Report Scope

| Large Enterprises |

| Small and Medium-sized Enterprises |

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Technology Consulting |

| Other Service Types |

| On-site Consulting |

| Remote / Virtual Consulting |

| IT and Telecommunications |

| Healthcare and Life Sciences |

| Financial Services (BFSI) |

| Manufacturing and Industrial |

| Energy and Utilities |

| Government and Public Sector |

| Real Estate and Construction |

| Retail and Consumer Goods |

| Media, Entertainment and Sports |

| Hospitality and Travel |

| Other Industries |

| Saudi Arabia |

| Qatar |

| United Arab Emirates |

| Rest of GCC |

| By Organization Size | Large Enterprises |

| Small and Medium-sized Enterprises | |

| By Service Type | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Technology Consulting | |

| Other Service Types | |

| By Delivery Model | On-site Consulting |

| Remote / Virtual Consulting | |

| By End-user Industry | IT and Telecommunications |

| Healthcare and Life Sciences | |

| Financial Services (BFSI) | |

| Manufacturing and Industrial | |

| Energy and Utilities | |

| Government and Public Sector | |

| Real Estate and Construction | |

| Retail and Consumer Goods | |

| Media, Entertainment and Sports | |

| Hospitality and Travel | |

| Other Industries | |

| By Country | Saudi Arabia |

| Qatar | |

| United Arab Emirates | |

| Rest of GCC |

Key Questions Answered in the Report

How large is the GCC management consulting services market in 2026?

The market is valued at USD 7.15 billion in 2026 and is forecast to reach USD 8.97 billion by 2031 at a 4.64% CAGR.

Which GCC country spends the most on external consulting?

Saudi Arabia accounts for 45.12% of total 2025 spending because Vision 2030 projects sustain multi-sector advisory demand.

Which segment grows fastest through 2031?

Technology consulting is expected to rise at 7.48% CAGR, driven by AI-native government programs and healthcare digitalization.

What is the main regulatory driver behind ESG advisory demand?

The UAE Climate Responsibility Law, effective May 2025, mandates greenhouse-gas reporting for every business entity.

How are localisation rules affecting foreign consultancies?

Saudi Arabia’s Regional Headquarters Program requires multinationals to maintain at least 15 local staff to win government work, raising operating costs and favouring firms with strong local footprints.

Which end-user industry shows the highest growth rate?

Healthcare consulting demand is forecast to expand at 11.12% CAGR to 2031 as hospitals privatise and digital health tools scale across the GCC.

Page last updated on: