Gourmet Food Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 523.47 Billion |

| Market Size (2030) | USD 702.11 Billion |

| Growth Rate (2025 - 2030) | 6.05% CAGR |

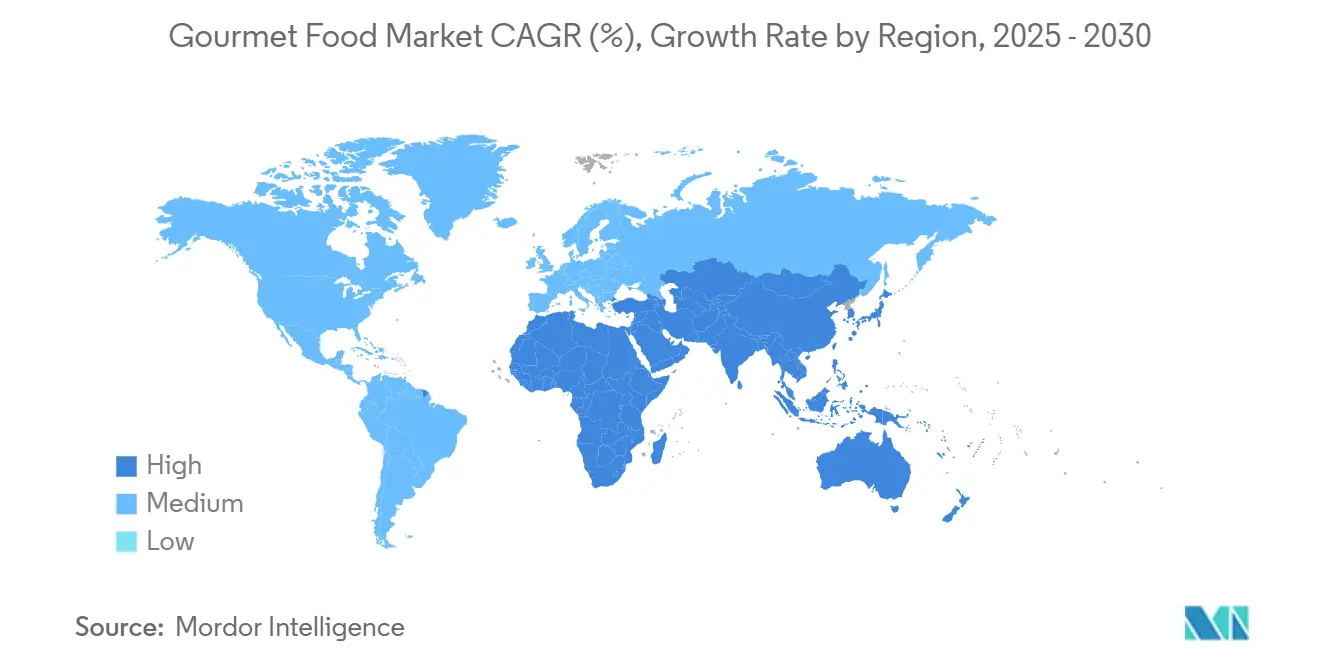

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

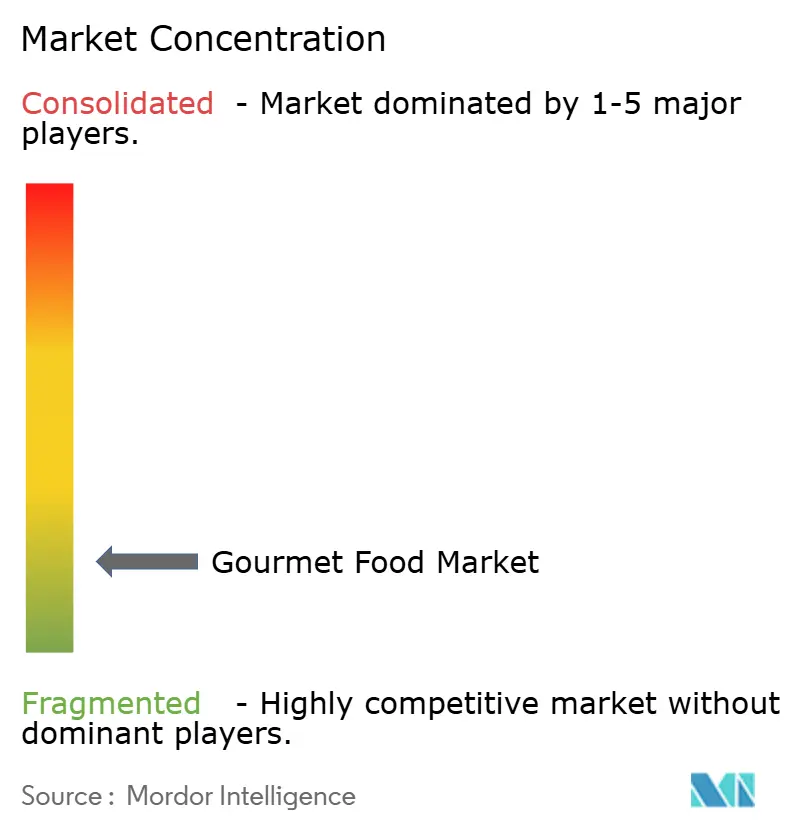

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Gourmet Food Market Analysis by Mordor Intelligence

In 2025, the gourmet food market size is estimated to be valued at USD 523.47 billion and is anticipated to grow significantly, reaching USD 702.11 billion by 2030. This growth represents a strong CAGR of 6.05%. The shift in consumer preferences from mass-produced foods to premium, high-quality gourmet offerings is driven by rising disposable incomes and increasingly aspirational lifestyles. Digital transformation in the supply chain, particularly through the adoption of blockchain technology, enhances transparency and strengthens the storytelling around product provenance, thereby fostering greater consumer trust. Additionally, the rising adoption of at-home meal kits is making gourmet food more accessible to a broader audience. Meanwhile, culinary media continues to influence consumer preferences, encouraging exploration of diverse tastes and fueling the category's expansion. Europe remains the most mature market for gourmet food, maintaining its established position. However, the Asia-Pacific region is emerging as the fastest-growing market, propelled by rapid urbanization, increasing e-commerce penetration, and the expansion of the middle-class population.

Key Report Takeaways

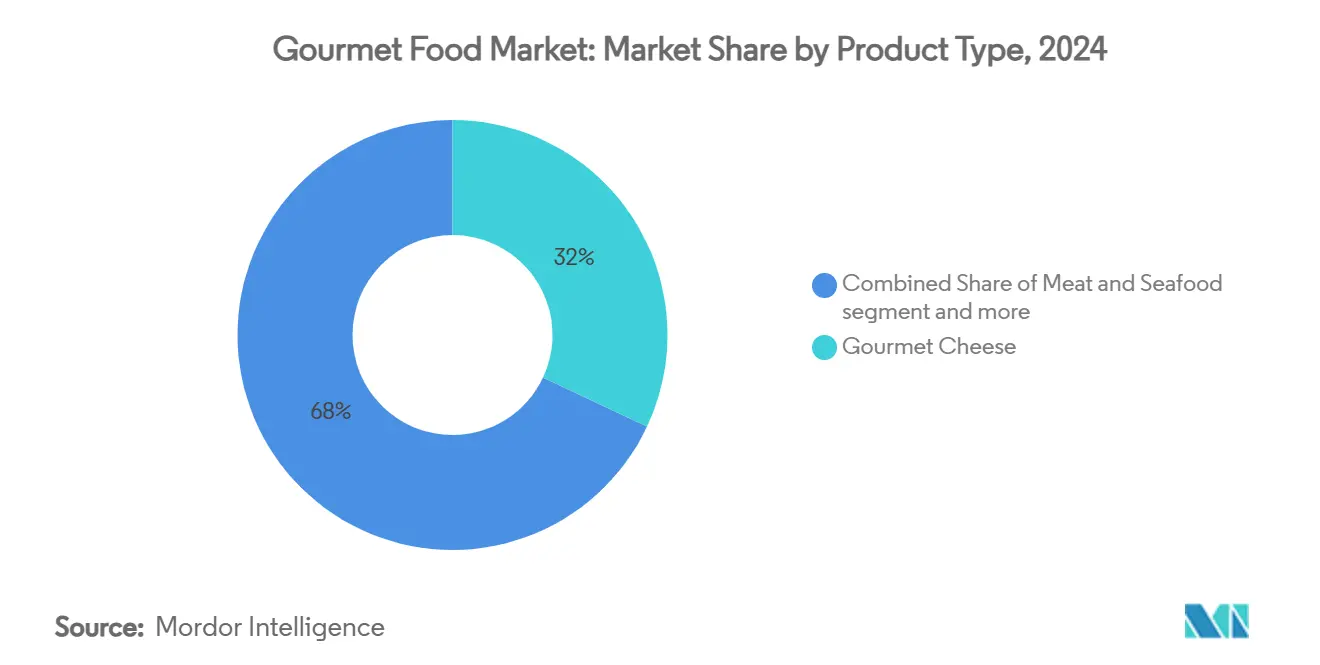

- By product type, Gourmet Cheese claimed a leading 32.03% share of the gourmet food market in 2024, while Gourmet Ready Meals secured 8.24%, with projections extending to 2030.

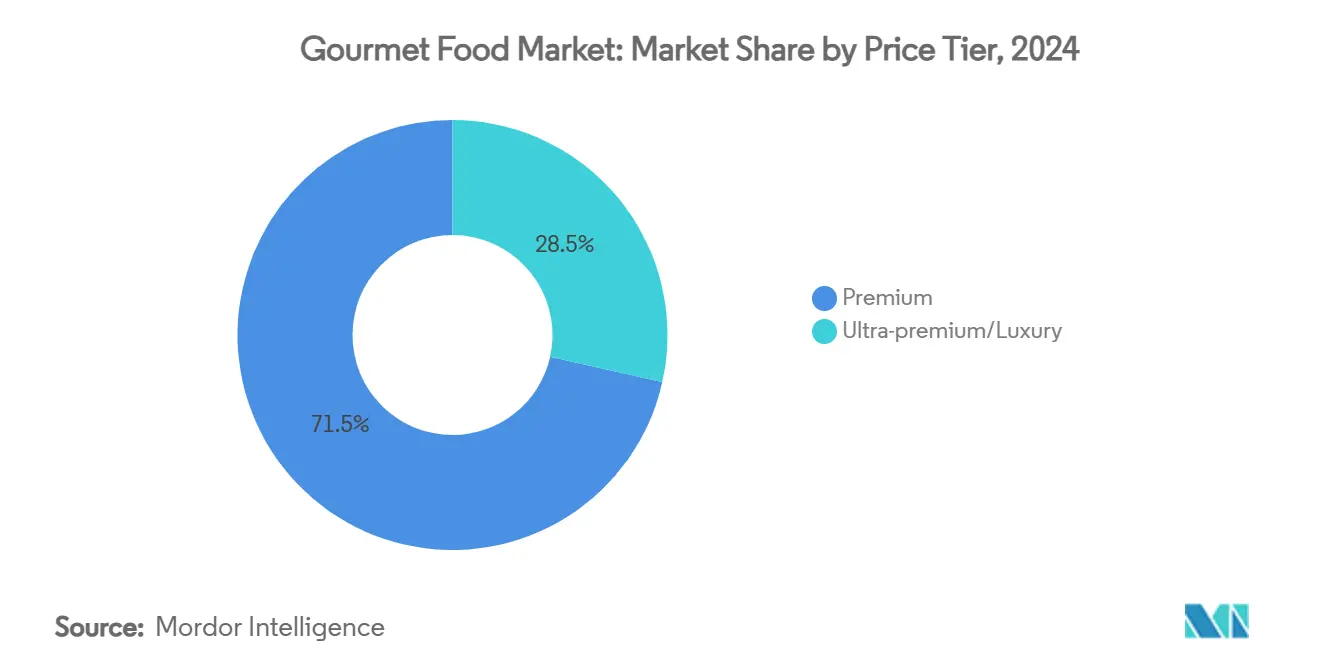

- By price tier, the Premium segment dominated the gourmet food market with a 71.54% share, while the Ultra Premium segment is set to experience the highest CAGR of 7.24% through 2030.

- By category, Conventional products commanded a 62.45% share of the gourmet food market in 2024, whereas Free From products were projected to hold 5.62% through 2030.

- By distribution channel, Supermarkets and Hypermarkets dominated distribution channels with a 55.13% market share, while Online Retail is projected to grow at a CAGR of 9.23% through 2030.

- By geography, Europe held a 29.41% market share in 2024, and the Asia-Pacific region is projected to achieve the highest growth rate at 7.91% through 2030.

Global Gourmet Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable incomes and premiumisation of diets | +1.2% | Global with strongest effect in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Expansion of gourmet-focused retail channels worldwide | +0.8% | North America and Europe core, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Increasing influence of culinary tourism and media | +0.6% | Global, premium markets lead | Short term (≤ 2 years) |

| Rapid growth of online specialty food marketplaces | +1.4% | North America and Europe, accelerating in Asia-Pacific | Medium term (2-4 years) |

| Hyper-niche provenance storytelling (blockchain-backed) | +0.4% | Premium markets globally, early adoption in EU | Long term (≥ 4 years) |

| At-home meal-kit formats for gourmet cooking | +0.7% | North America and Europe, urban centers worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Incomes and Premiumization of Diets

Despite headline inflation squeezing everyday spending, households are increasingly dedicating larger portions of their budgets to delicacies that emphasize craftsmanship and authenticity. The Gulf Cooperation Council (GCC) stands as a testament to this trend, with rising per-capita incomes leading to heightened spending on premium snacks and confectioneries, as highlighted by the United States Department of Agriculture[1]United States Department of Agriculture," Opportunities for U.S. Snacks & Sweets in the GCC Region", www.fas.usda.gov. Similarly, in Brazil, consumers are channeling 17% of their disposable income towards food, favoring upscale options even amidst broader economic challenges. For younger demographics, premium food has evolved into a form of social currency, fostering deeper brand loyalty, especially towards those that share their origin stories and artisanal crafting methods. Grocery studies from Latin America reveal a duality: while consumers are value-conscious, there's a pronounced aspiration for premium offerings. This suggests the trend's resilience, contingent on stable employment. And while spending on discretionary foods is typically more elastic than on staples, consistent wage growth and a trend towards urban professionalization are paving the way for an even greater embrace of gourmet offerings.

Expansion of Gourmet-Focused Retail Channels Worldwide

Mainstream grocers are increasingly dedicating premium aisles to cater to high-end consumers, while specialty retailers are strategically expanding their presence in affluent neighborhoods to capture a larger share of the premium market. For instance, Eataly's move into suburban areas is broadening access to Italian artisanal goods, specifically targeting higher-income shoppers. Similarly, Target has achieved significant success, generating over USD 24 billion in grocery revenue by strengthening its omnichannel engagement strategies, which have enhanced customer convenience and loyalty. Retailers are capitalizing on the higher profit margins offered by upscale product assortments, driving them to compete for the natural and gourmet market share traditionally dominated by independent retailers. The geographic clustering of stores around urban centers such as Atlanta and Richmond highlights a deliberate, data-driven approach to site selection, ensuring proximity to key consumer bases. To sustain long-term growth, retailers must effectively balance immersive merchandising experiences with robust inventory management practices, which are critical for maintaining product freshness and minimizing shrinkage on high-value items.

Increasing Influence of Culinary Tourism and Media

Food-centric travel and digital storytelling are transforming once-exclusive ingredients into accessible culinary experiences. Marriott International's Travel Trends 2024 report reveals that the Asia-Pacific region accounts for 37.8% of global culinary tourism spending, underscoring the region's rich local flavors and traditional techniques. The popularity of streaming cooking shows and social media platforms has inspired viewers to become experimental home cooks, often recreating restaurant-quality dishes in their kitchens. This shift has driven increased demand for unique ingredients such as single-origin spices, heritage grains, and cheeses from specific micro-regions. Celebrity chefs play a pivotal role as cultural ambassadors, bridging the gap between unfamiliar cuisines and global audiences. While a consistent flow of engaging content is necessary to sustain interest, the cycle of inspiration and subsequent purchasing remains particularly influential among millennials and Generation Z, who are eager to explore diverse culinary experiences.

Rapid Growth of Online Specialty Food Marketplaces

Online grocery shopping has surged since the pandemic. Specialty platforms have outperformed traditional ones, giving small producers a national stage and a chance to engage directly with consumers. Premium baskets, with their higher average order values, offset delivery fees, making them appealing to shoppers. Moreover, algorithms spotlight niche SKUs, ensuring unique products, often missed in brick-and-mortar stores, get their due attention. These platforms also allow for real-time checks on product origins, boosting consumer trust in authenticity. Yet, the triumph of online grocery models hinges on robust cold-chain logistics and customers' readiness to pay for convenience. These elements, however, differ widely by region, shaping the market landscape. Consequently, regions with better infrastructure and more disposable income are rapidly embracing and innovating in online grocery services. In contrast, emerging areas grapple with scaling challenges. To maintain momentum, online grocers need to bolster logistics and offer tailored customer experiences, fostering loyalty and bridging regional gaps.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price sensitivity in emerging economies | -0.9% | Asia-Pacific, Latin America, Middle East and Africa | Medium term (2-4 years) |

| Supply-chain fragility for exotic raw ingredients | -0.7% | Global, acute in premium segments | Short term (≤ 2 years) |

| Carbon-footprint labeling dampening certain categories | -0.5% | Europe and North America, expanding worldwide | Long term (≥ 4 years) |

| Stringent sodium- and fat-reduction regulations on artisanal cheese | -0.3% | Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Price Sensitivity in Emerging Economies

As currency devaluation and inflation continue to constrain discretionary budgets, shoppers are increasingly driven to seek promotions or shift toward private-label alternatives. According to the U.S. Department of Agriculture, Brazil's GDP is projected to grow by 3.4% in 2024[2]United States Department of Agriculture, " Grain and Feed Annual 2025", www.fas.usda.gov. However, the agricultural sector is expected to contract due to adverse weather conditions, which will negatively impact both production and imports. The report highlights economic challenges, such as rising commodity prices and escalating production costs, which are closely tied to the dynamics of premium imports. While affluent urban consumers remain a viable target market, achieving a broader consumer upgrade depends heavily on local production that circumvents import tariffs. As a result, brands must develop tiered pricing strategies that encourage consumer trials while maintaining the perception of luxury. This situation underscores a complex paradox: significant growth potential exists, but affordability remains fragile. To navigate this, businesses must focus on detailed market segmentation and implement cost-effective supply chain strategies to ensure sustainable success.

Supply-Chain Fragility for Exotic Raw Ingredients

Gourmet producers, reliant on specific terroirs and seasonal crops, find themselves increasingly vulnerable to supply chain disruptions. Global challenges, notably climate change and geopolitical tensions, have exacerbated ingredient shortages and market volatility. Take the European Union's 2023 update to the Novel Foods Regulation: it has streamlined approval processes for alternative and sustainable ingredients[3]European Union,"COMMISSION IMPLEMENTING REGULATION (EU) 2023/65", eur-lex.europa.eu. This shift allows gourmet producers to seamlessly integrate innovative substitutes—like plant-based dairy or cell-cultured proteins—without compromising compliance or consumer trust. Climate change-induced volatility in cocoa supply has led giants like Mondelez International to pivot towards solutions like cell-cultured cocoa. Such innovations not only promise a steady supply but also shield against price swings. Yet, small-scale artisans grapple with heightened challenges, constrained by limited and less diversified sourcing networks. While strategies like multi-origin procurement and controlled-environment agriculture bolster resilience and mitigate risks, they also risk muddying the authenticity narratives central to the allure of premium brands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cheese Strength Sets the Benchmark

In 2024, gourmet cheese captured a significant 32.03% of the gourmet food market, cementing its status as a category leader. While cheeses with European protected designations predominantly steer this segment, the rising demand in Japan and South Korea signals an expanding Asian embrace of these specialized dairy offerings. Simultaneously, the growth of plant-based dairy alternatives is spurring flavor innovations, broadening consumption opportunities. This robust performance in gourmet cheese, alongside the steady success of other established categories—like chocolate, cured meats, spices, and seafood—benefits from ethical sourcing claims and culinary tourism. Such dynamics offer suppliers a diverse portfolio, helping them navigate commodity risks and enhance cross-selling. Major players in these leading categories are investing in techniques like cave-aging, microflora research, and single-farm traceability, bolstering their pricing power and ensuring product integrity.

On another front, gourmet ready meals are set for a notable surge, projected to grow at a robust 8.24% CAGR through 2030. This momentum caters to busy urban families seeking restaurant-quality meals in the comfort of their homes. Innovations in this realm are blending global flavors with controlled portion sizes, promoting a rich culinary exploration. Diverging from traditional cheese producers, companies in the ready-meal sector are focusing their research and development on recyclable packaging and sous-vide techniques to ensure quality. This strategy not only enhances shelf appeal but also aligns with waste-reduction goals. Across all gourmet food segments, the unified aim is to transform everyday meals into premium experiences.

By Category: Conventional Dominance Sustains Scale

In 2024, conventional gourmet items seized the spotlight, accounting for 62.45% of the market's total turnover. This underscores a pivotal notion: one can relish elevated taste experiences without adhering to dietary restrictions. These gourmet offerings, spanning from high-quality non-GM oils to heritage grain flours and artisanal condiments, boast a superior sensory appeal, all while steering clear of special-diet claims. Established brands in this arena, bolstered by well-honed supply chains and a keen understanding of regulations, find it easier to introduce line extensions. Yet, as consumer expectations shift, particularly among younger audiences, companies are pivoting. They're enhancing transparency, unveiling origin maps and carbon footprint data, a move that's fortifying trust and brand loyalty in the conventional gourmet realm.

On the flip side, 'free-from' alternatives, which hold a 37.5% market share, are emerging as the segment with the most momentum, boasting an impressive 5.62% CAGR. This surge is largely attributed to a growing consumer inclination towards lactose-free, gluten-free, and vegan choices. Moreover, the allure of functional benefits—like gut health and allergen avoidance—provides a solid justification for their premium pricing. However, 'free-from' specialists grapple with hurdles: the high costs of ingredient sourcing and the rigorous contaminant testing, both of which strain profit margins. Yet, in the face of these challenges, innovative solutions are surfacing. Strategies such as shared research centers and cross-production facilities are being adopted, aiming to unify quality standards and optimize operations. A notable trend is the emergence of brands that deftly navigate both the conventional and 'free-from' domains, allowing them to tap into mainstream volumes while also seizing niche growth prospects.

By Price Tier: Premium Tier Anchors Value Creation

In 2024, premium products dominated the gourmet food market, accounting for 71.5% of total revenue. This segment strikes a balance, offering luxury items that, while aspirational, remain accessible to mass-affluent consumers. These consumers gravitate towards brands that weave authentic craft narratives into fair pricing, enabling them to enhance their dining experiences without overspending. Even in economic downturns, staples like flavored olive oils and origin-specific coffees hold their ground, offering a modest yet significant upgrade to home dining. Companies in this space employ tiered pricing strategies, nudging consumers towards higher-value purchases, which not only cultivates brand loyalty but also stabilizes revenue streams.

While ultra-premium products represent a smaller slice of the pie, they are the market's fastest-growing segment, boasting a 7.24% CAGR. This surge is fueled by a concentration of wealth and age-old gifting traditions. Buyers in the ultra-premium realm, often high-net-worth individuals, chase exclusivity. They are drawn to limited editions, numbered batches, and bespoke tasting experiences that spotlight rarity and craftsmanship. Even if ultra-premium volumes dip during economic slumps, their robust margins act as a buffer, safeguarding overall profitability. On the supply side, strategies diverge: premium lines emphasize lean, quality-first manufacturing, while ultra-premium offerings lean into artisanal, scarcity-driven production. This approach not only underscores their distinct value propositions but also caters to the diverse tiers of consumers in the gourmet landscape.

By Distribution Channel: Physical Retail Retains Reach, Digital Scales Discovery

In 2024, supermarkets and hypermarkets maintained their dominance in the gourmet food market, contributing 55.1% of the total turnover. This success stems from their strategic initiatives, such as the introduction of gourmet corners and hosting in-store tasting events, which actively encourage consumers to explore and sample premium products. These formats leverage the trust that shoppers already place in these retailers and the convenience of immediate product availability, making them particularly attractive to older demographics. By offering carefully curated gourmet selections within familiar retail settings, supermarkets and hypermarkets effectively bridge the gap between routine grocery shopping and the allure of premium gourmet experiences, creating a unique value proposition for consumers.

Conversely, online retail has established itself as the fastest-growing channel in the gourmet food market, achieving a robust annual growth rate of 9.23%. This growth is driven by the increasing accessibility of niche product discovery and the ability to penetrate rural areas, where specialty stores are often scarce. Online platforms, including subscription boxes and direct-to-consumer storefronts, empower smaller producers to bypass traditional distribution channels. This approach not only helps protect their profit margins but also enables them to gather critical first-party consumer data, which can be used to refine offerings and target audiences more effectively. Additionally, the integration of advanced omnichannel strategies—such as synchronized inventory management, click-and-collect services, and AI-powered personalization—has significantly enhanced the overall shopping experience. These innovations improve convenience for consumers, encourage larger basket sizes through tailored product recommendations, and drive cross-category sales, further solidifying online retail as a key growth driver in the gourmet food market.

Geography Analysis

Europe, with its rich culinary heritage and high per-capita incomes, held a 29.41% market share in 2024, nearly one-third of global gourmet food revenues. The continent's strict geographic-indication rules not only bolster the authenticity of its offerings, like protected-designation cheeses and fine pastries, but also cement their premium market positioning. While the European Commission's carbon-footprint labeling initiative introduces complexities, it simultaneously presents opportunities for environmentally conscious leaders. Despite an aging demographic tempering volume growth, Europe's sophisticated retail channels, robust inbound tourism, and dynamic cross-border e-commerce continue to drive stable growth.

Asia-Pacific is on a rapid ascent, boasting a 7.91% CAGR forecasted through 2030. Urban middle classes in nations like China, India, Indonesia, and Vietnam are increasingly embracing global flavors, a trend amplified by the omnipresence of smartphones and digital payment systems. While Japanese and South Korean consumers are leading in cheese consumption, Chinese households are now hosting Western-style wine-and-cheese gatherings. Given the region's vastness, local production hubs, like Hokkaido's premium dairy and Indonesia's single-estate cocoa are poised to play pivotal roles in meeting demand and navigating import tariffs. Yet, brands eyeing success in ASEAN markets must prioritize taste localization, adjusting spice levels, portion sizes, and halal certifications to resonate with local preferences.

North America finds itself in a unique position, balancing Europe's established maturity with Asia's rapid growth. Here, consumers, influenced by diverse cultures, are eager to explore new taste profiles. The U.S. stands at the forefront of retail innovation, with independent specialty shops banding together for cooperative purchasing, a strategy to counter national chains' price undercutting. Meanwhile, Canada's gourmet segment, buoyed by provincial agricultural promotion programs, shows a pronounced preference for organic and locally sourced products. Despite challenges like supply disruptions and labor shortages, the momentum of direct-to-consumer sales is counterbalancing constraints faced by brick-and-mortar stores. Furthermore, ongoing regulatory talks about sodium and added-sugar caps could significantly influence formulation strategies, especially in artisanal cheese and confectionery sectors.

Competitive Landscape

The gourmet food market showcases a landscape where nimble innovation often trumps sheer scale. While industry giants like Mars, Mondelez, and Nestlé harness global distribution and acquisition strategies, specialty independents carve out their niche through a focus on provenance and limited-batch releases. Mars’ USD 35.9 billion acquisition of Kellanova not only bolsters its confectionery dominance but also signals a strategic pivot towards premium snacking. Meanwhile, Mondelez’s foray into cell-cultured cocoa technology underscores its commitment to sustainability, ensuring both input security and taste authenticity.

Artisanal players are setting themselves apart with certification credentials. For instance, Valrhona’s B-Corporation status underscores its dedication to ethical sourcing and environmental responsibility. Partnership models are on the rise, and Eataly’s expansion into suburban areas underscores the potency of experiential retail in shaping gastronomic landscapes. Embracing technology, from blockchain lot codes to AI flavor predictions, enhances traceability and accelerates product development, offering a competitive edge that eclipses mere commodity price battles.

Investment trends reveal a robust merger and acquisition interest in dessert, cheese, and health-conscious segments. European private-equity firms are increasingly acquiring boutique chocolatiers, banking on growth driven by exports. Concurrently, co-manufacturing deals are paving the way for start-ups eyeing ultra-premium markets. While retailer own-brand products are gaining traction, they serve to complement rather than overshadow established brands, with premium private labels enhancing store prestige. In the end, the market rewards those who blend authentic craftsmanship with scalable operations and deep consumer insights.

Gourmet Food Industry Leaders

-

Nestlé S.A.

-

Mondelez International, Inc.

-

Arla Foods amba

-

The Kraft Heinz Company

-

Jasper Hill Farm

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: PepsiCo, with a USD 1.95 billion deal, has made a significant move by acquiring the functional soda brand Poppi, marking its foray into the realm of health-focused beverages, emphasizing prebiotics and reduced sugar content.

- November 2024: Solely, an innovative brand, has introduced a range of minimalist snacks crafted by repurposing surplus fruits. The company focuses on transforming single ingredients, such as bananas, into distinctive products like banana fusilli pasta, showcasing their commitment to sustainability and creativity in food innovation.

- October 2024: Cometeer, a premium coffee manufacturer, has introduced its Stellar Series, a new product line that highlights unique and high-quality coffee offerings. As part of this launch, the company partnered with Black & White Roasters to release a limited-edition white honey geisha coffee, showcasing their commitment to innovation and excellence in the coffee industry.

- March 2024: Tru Fru, a brand owned by Mars Inc, has expanded its market presence by collaborating with Tesco in the United Kingdom. As part of this partnership, the brand has launched new flavors of its chocolate-covered fruit snacks, including the innovative Frozen White and Dark Chocolate Covered Raspberries, aiming to cater to the growing demand for premium snack options.

Global Gourmet Food Market Report Scope

| Gourmet Cheese |

| Gourmet Chocolate and Confectionery |

| Gourmet Meat and Seafood |

| Gourmet Sauces and Condiments |

| Gourmet Snacks |

| Gourmet Oils and Vinegars |

| Gourmet Ready Meals |

| Free From Products |

| Conventional Products |

| Premium |

| Ultra-premium/Luxury |

| On-Trade | |

| Off-Trade | Supermarkets and Hypermarkets |

| Specialty Stores | |

| Online Retail/E-commerce | |

| Other Off-Trade Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type | Gourmet Cheese | |

| Gourmet Chocolate and Confectionery | ||

| Gourmet Meat and Seafood | ||

| Gourmet Sauces and Condiments | ||

| Gourmet Snacks | ||

| Gourmet Oils and Vinegars | ||

| Gourmet Ready Meals | ||

| By Cateogory | Free From Products | |

| Conventional Products | ||

| By Price Tier | Premium | |

| Ultra-premium/Luxury | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets and Hypermarkets | |

| Specialty Stores | ||

| Online Retail/E-commerce | ||

| Other Off-Trade Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current gourmet food market size?

The gourmet food market size stands at USD 523.47 billion in 2025 and is projected to surpass USD 702.11 billion by 2030.

Which product segment leads the gourmet food market?

Gourmet cheese leads, accounting for 32.0% of 2024 revenue and continuing to set quality benchmarks across the category.

How fast is online retail growing within the gourmet food market?

Online retail is forecast to grow at 9.23% CAGR through 2030 as consumers embrace convenience and niche discovery.

Which region shows the highest growth potential?

Asia-Pacific is expected to post a 7.91% CAGR between 2025 and 2030, driven by urbanization and expanding middle-class demand for premium experiences.

Page last updated on: