Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 97.92 Billion |

| Market Size (2031) | USD 113.53 Billion |

| Growth Rate (2026 - 2031) | 3.01% CAGR |

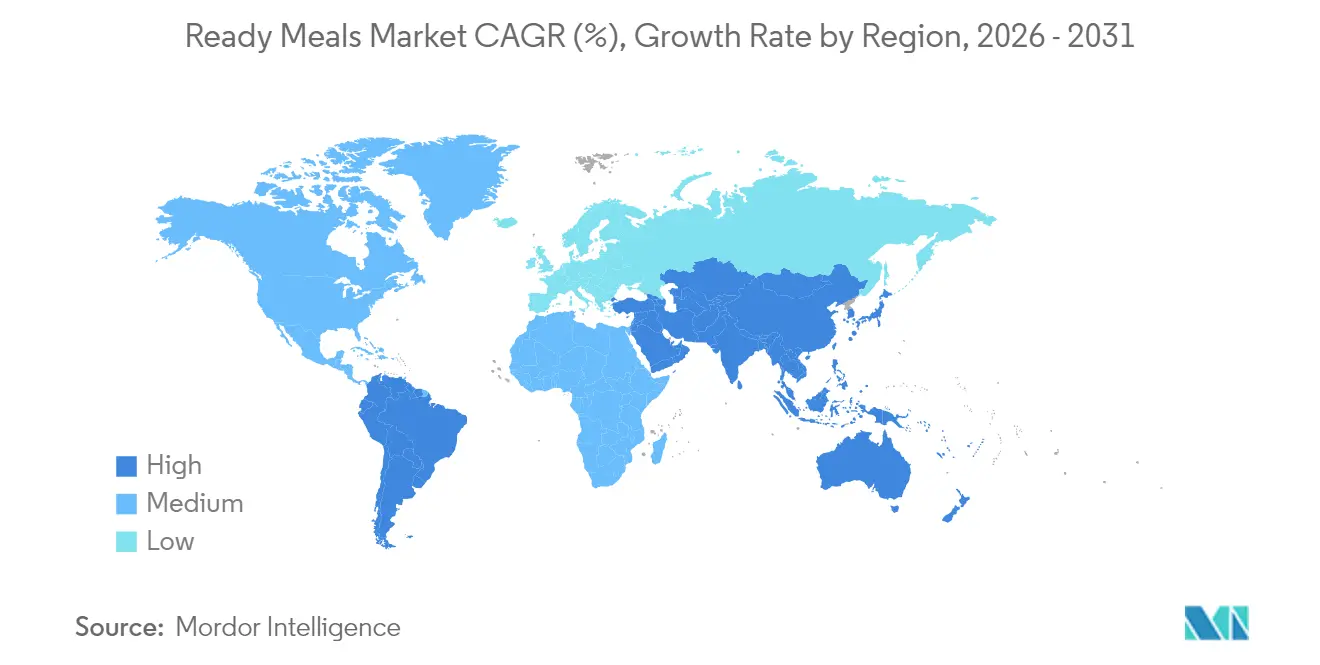

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

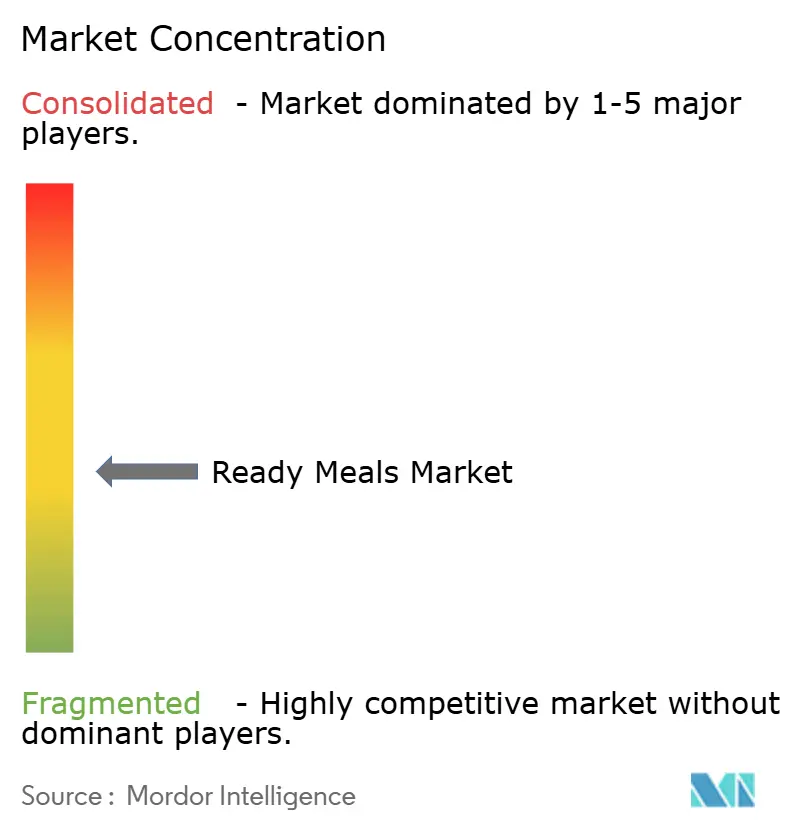

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Ready Meals Market Analysis by Mordor Intelligence

Ready meals market size in 2026 is estimated at USD 97.92 billion, growing from 2025 value of USD 95.05 billion with 2031 projections showing USD 113.53 billion, growing at 3.01% CAGR over 2026-2031. This growth reflects the market's maturity, while also demonstrating continued consumer demand for convenient meal solutions. The market's stability is supported by advances in food preservation technology, changing consumer lifestyles, and industry consolidation that has improved operational efficiency and distribution networks. In addition, technological advancements are driving market growth, particularly through preservation methods such as high-pressure processing, cold plasma treatment, and intelligent packaging systems, which extend product shelf life while preserving nutritional value. These innovations help manufacturers address the challenge of combining convenience with quality, allowing them to compete in premium market segments. The adoption of nanotechnology in packaging has resulted in systems that monitor food freshness, which reduces waste and increases consumer trust.

Key Report Takeaways

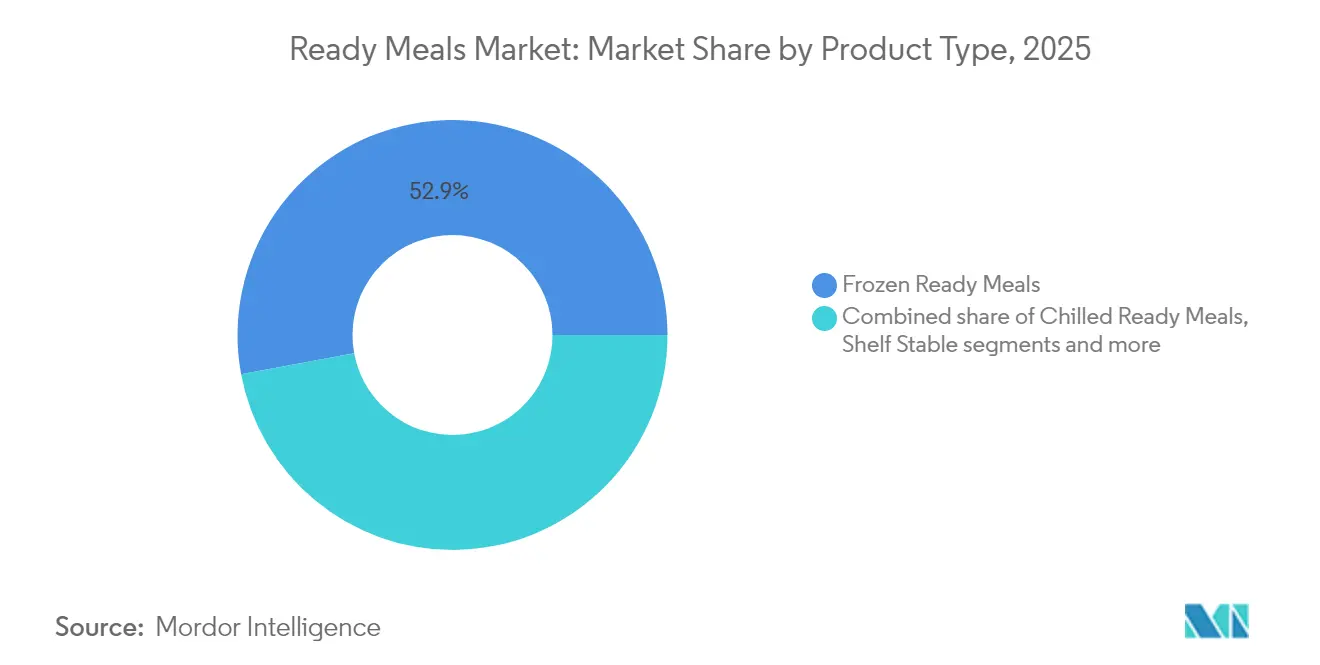

- By product type, frozen ready meals led with 52.93% of the ready meals market share in 2025 and are projected to register the fastest 3.55% CAGR to 2031.

- By ingredient, conventional formulations captured 77.85% share of the ready meals market size in 2025, whereas free-from alternatives are advancing at the highest 3.84% CAGR.

- By category, the non-vegetarian segment accounted for 60.02% of the ready meals market size in 2025, while vegetarian meals are forecast to grow at 4.15% CAGR through 2031.

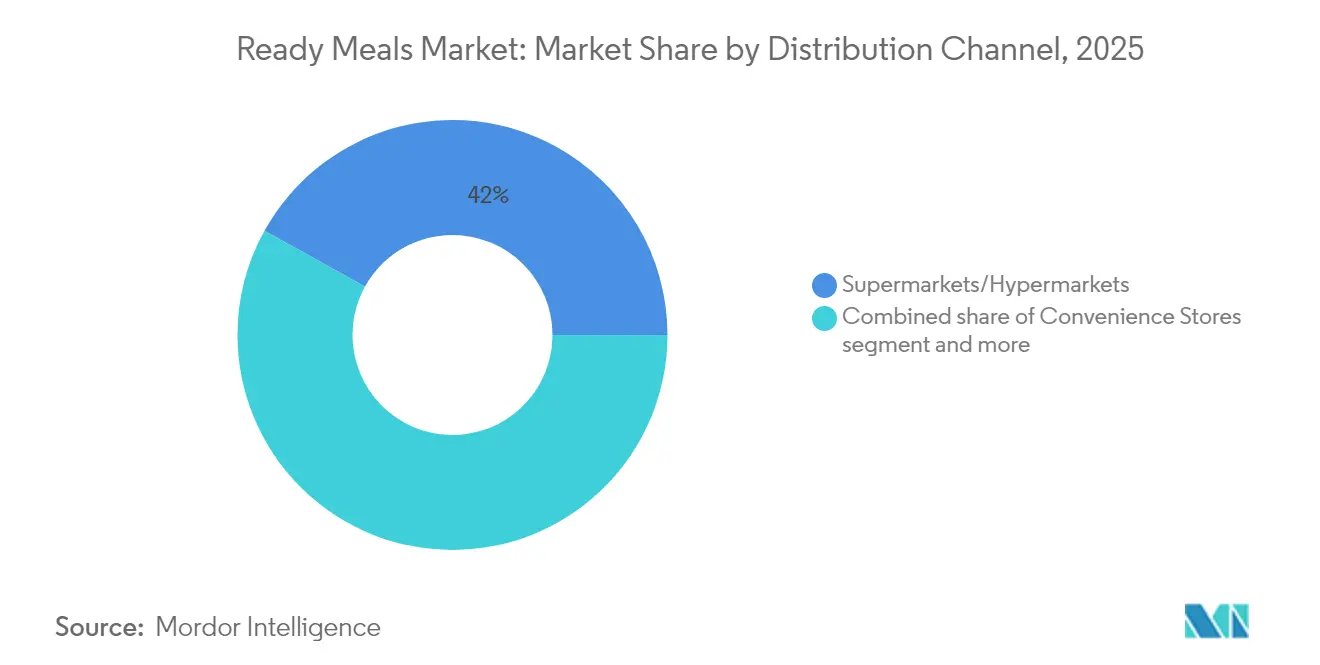

- By distribution channel, supermarkets/hypermarkets captured 41.95% of the ready meals market share in 2025; online retail is the fastest-growing channel, expanding at 4.52% CAGR.

- By geography, North America dominated with 34.10% revenue share in 2025; Asia-Pacific is poised to grow the quickest, at a 4.83% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ready Meals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological advancements in food preservation | +0.8% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Sustainability and eco-friendly packaging | +0.6% | Europe and North America leading, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Innovation in plant-based and alternative proteins | +0.7% | North America and Europe core, emerging in Asia-Pacific | Medium term (2-4 years) |

| Cultural and ethnic diversity | +0.4% | Global, with concentration in multicultural urban centers | Long term (≥ 4 years) |

| Flavor and culinary trends | +0.5% | Global, with regional variations in taste preferences | Short term (≤ 2 years) |

| Surge in demand for clean-label ready meals | +0.9% | North America and Europe leading, spreading globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Technological Advancements in Food Preservation

Technological advancements in food preservation technologies serve as a primary driver in the global ready meals market through enhanced product safety protocols, extended shelf life capabilities, and optimal nutritional value retention. The implementation of High Pressure Processing (HPP), Modified Atmosphere Packaging (MAP), and smart packaging technologies has fundamentally transformed the production and consumption patterns of ready meals. These technological implementations enable manufacturers to deliver convenient meal solutions while maintaining the quality standards comparable to traditional home-cooked preparations. The integration of these advanced preservation methodologies addresses the increasing consumer requirements for nutritionally superior, extended durability, and environmentally sustainable food alternatives. For instance, in June 2025, United Arab Emirates-based corporation Red Planet implemented advanced freeze-drying technology to introduce ready-to-eat meal products with a preservation duration of 25 years. These meal solutions maintain their organoleptic properties, nutritional composition, and food safety parameters without requiring refrigeration systems or synthetic preservation compounds, thereby addressing critical requirements in food security protocols and emergency preparedness initiatives.

Sustainability and Eco-Friendly Packaging

Environmental sustainability in packaging is driving changes in the global ready meals market, influenced by consumer awareness and government regulations. Consumers and regulators are pushing for reduced plastic usage and increased adoption of biodegradable, recyclable, and compostable materials in food packaging. Government policies, such as the United States Plastics Pact, require all plastic packaging to be reusable, recyclable, or compostable by 2025 [1]Source: U.S. Plastics Pact Inc., "U.S. Plastics Pact Roadmap to 2025", usplasticspact.org . Additionally, food manufacturers are implementing minimalist and lightweight packaging designs to reduce material usage and improve recyclability. For instance, in May 2025, Marks & Spencer (M&S) implemented a trial in the United Kingdom to replace plastic trays with paper fiber packaging for ready meals, beginning with its Fiery Chicken Tikka Masala. The company established a partnership with 2SFG and GPI to develop this recyclable packaging solution. The new tray, produced from FSC-certified renewable paper fiber, demonstrated compatibility with both oven and microwave heating, maintaining convenience while reducing environmental impact.

Innovation in Plant-Based and Alternative Proteins

The global ready meals market is transforming due to the rise in plant-based and alternative protein innovations. Consumers are increasingly seeking convenient, healthy, and sustainable food options, leading manufacturers to develop ready meals with plant-based proteins, including those derived from peas, chickpeas, rice, and potatoes. These innovations address the growing demand for meat alternatives and align with the increasing preference for flexitarian and vegan diets. Companies such as Beyond Meat and Impossible Foods have entered the ready meals segment, offering frozen plant-based bowls and international dishes. For instance, in May 2023, Beyond Meat launched plant-based frozen ready meals in the United Kingdom, featuring three varieties: Spaghetti Bolognese, Keema Curry & Pilau Rice, and Chili with Coriander Rice. Moreover, government initiatives are instrumental in advancing the adoption of plant-based ready meals across regions. Denmark's comprehensive "Action Plan for Plant-Based Foods," implemented in 2023, establishes a strategic framework to reduce the environmental impact of food consumption through the promotion of plant-based dietary choices [2]Source: Ministry of Food, Agriculture and Fisheries of Denmark, "Danish Action Plan for Plant-based Foods", fvm.dk . The initiative encompasses educational programs, including professional culinary training focused on plant-based meal preparation, to facilitate broader market acceptance and adoption.

Cultural and Ethnic Diversity

The global ready meals market is transforming significantly, driven by migration, globalization, and increasing consumer interest in culinary exploration. Demand for ethnic ready meals, including Indian curries, Mexican enchiladas, Japanese sushi kits, and Italian risottos, is expanding rapidly. Leading companies such as Kraft Heinz, Nestlé, and Conagra Brands are strategically diversifying their portfolios with single-serve and frozen ethnic meal options that combine convenience with authenticity. Regional players like MTR Foods in India and CJ CheilJedang in South Korea are leveraging local insights to develop innovative, market-specific products. Younger demographics, particularly Millennials and Gen Z, are driving this trend, influenced by social media and their openness to global flavors. Retail channels, including supermarkets and e-commerce platforms, are capitalizing on this demand by offering a wider range of international meal kits and ready-to-eat platters, catering to both impulse and planned purchases. The growing multicultural populations in regions such as North America and Western Europe are further accelerating demand for diverse product offerings. Manufacturers are responding by adhering to authentic recipes and sourcing traditional ingredients to meet consumer expectations. Regulatory and food safety standards are reinforcing trust in these products by ensuring high quality and cultural authenticity. Overall, the ready meals market is evolving, with ethnic diversity emerging as a critical growth driver and a key differentiator in the competitive landscape.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Short shelf life for premium products | -0.4% | Global, particularly affecting premium segments | Short term (≤ 2 years) |

| Strong competition from fresh and home-cooked alternatives | -0.6% | Developed markets with established fresh food supply chains | Medium term (2-4 years) |

| Taste and quality perception | -0.5% | Global, with regional variations in quality expectations | Long term (≥ 4 years) |

| Limited appeal in rural areas | -0.3% | Rural regions globally, particularly in developing markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Short Shelf Life for Premium Products

Premium ready meals face shelf life limitations that restrict market expansion and increase operational complexity for manufacturers and retailers. According to Food Standards Scotland's 2025 guidance, determining shelf life requires evaluating multiple factors, with no standard methodology available due to product variations and storage conditions [3]. Premium products with natural ingredients and minimal preservatives experience faster spoilage rates, with total volatile basic nitrogen levels indicating spoilage that must remain within legal limits during distribution. Quality control requires monitoring systems to detect microbes, including Listeria monocytogenes, Salmonella, and E. coli, which present contamination risks that increase with longer shelf life requirements. These limitations create cost pressures and restrict geographic distribution, particularly affecting small and medium-sized producers without advanced preservation technologies.

Strong Competition from Fresh and Home-Cooked Alternatives

The global ready meals market encounters substantial limitations due to competition from fresh and home-prepared alternatives. Consumers predominantly consider freshly prepared meals superior in nutritional value and adaptability, prompting their selection of home cooking over pre-prepared options. Home-prepared meals facilitate precise control over ingredient composition, serving quantities, and preparation methodologies, accommodating specific dietary requirements and health objectives. The emergence of meal preparation services and digital culinary instruction platforms has enabled consumers to execute restaurant-caliber dishes within domestic settings, consequently diminishing ready meal demand. These alternatives deliver superior freshness and traditional culinary experiences while potentially offering enhanced economic efficiency over extended periods. Educational initiatives, exemplified by the United Kingdom's "Chefs in Schools" program, implement nutritionally balanced, freshly prepared meals for students while simultaneously imparting culinary expertise and promoting beneficial dietary practices. These institutional programs generate additional market pressure by establishing a preference for home-prepared meals among the younger demographic.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Frozen Dominance Drives Market Stability

Frozen ready meals hold 52.93% market share in 2025 and are projected to grow at 3.55% CAGR through 2031, demonstrating significant market dominance. This position reflects consumer trust in frozen preservation methods that maintain nutritional value and taste while offering extended shelf life and storage benefits. Modern freezing technologies and packaging systems have effectively addressed issues like freezer burn and quality deterioration, enabling frozen meals to maintain competitive quality standards. The implementation of smart packaging enables continuous monitoring of product conditions throughout the cold chain, reducing waste and improving consumer trust.

Chilled ready meals maintain a substantial secondary market position, with advantages in perceived freshness but limitations in shelf life that restrict distribution capabilities. Shelf-stable products fulfill specific market requirements where refrigeration access is limited, particularly in developing markets and emergency food supplies. While freeze-dried ready meals show potential in outdoor recreation and long-term storage markets, their current market presence remains modest due to higher production expenses and limited consumer awareness. The frozen segment maintains its market leadership through improved preservation methods, enhanced packaging solutions, and efficient supply chain management that ensures consistent product quality during distribution.

By Ingredient: Free-From Acceleration Challenges Conventional Leadership

Conventional ingredients hold 77.85% market share in 2025, while free-from alternatives grow at 3.84% CAGR through 2031, reflecting evolving consumer dietary preferences. This trend indicates that conventional products maintain broad market appeal, while free-from alternatives gain traction among health-conscious consumers and those with dietary restrictions. Consumer acceptance of clean-label products varies across categories, with higher education levels and health-focused dietary patterns correlating with increased free-from product adoption. The free-from segment includes gluten-free, dairy-free, preservative-free, and allergen-free products that address specific dietary needs at premium price points.

Free-from product manufacturing faces challenges in maintaining taste, texture, and shelf stability without traditional ingredients, necessitating alternative preservation and flavoring methods. The conventional segment's market leadership stems from lower production costs, established supply chains, and widespread consumer acceptance. The growth in free-from products signals market premiumization and demographic shifts toward health-focused consumption, influencing product development strategies across the industry.

By Distribution Channel: Online Retail Disrupts Traditional Dominance

Traditional supermarkets/hypermarkets maintain a 41.95% market share in 2025, supported by their established infrastructure and consumer shopping patterns. The online retail segment is growing at a 4.52% CAGR through 2031, driven by digital transformation in food retail and increasing consumer demand for convenience and home delivery services. Quick commerce operations, offering delivery within 30 minutes, are transforming food distribution through dark stores in urban areas, though profitability remains a concern. The implementation of advanced transportation management systems is improving frozen food distribution through enhanced route optimization and product quality maintenance while reducing operational costs.

Convenience stores cater to specific market segments focused on immediate consumption and impulse purchases. Additional distribution channels include foodservice establishments, vending machines, and specialty retailers serving distinct consumer groups. The growth in online retail is supported by improvements in cold chain logistics, last-mile delivery solutions, and increased consumer adoption of digital food purchasing. While traditional retail maintains its strengths in product inspection, immediate availability, and consumer trust, the expansion of online channels reflects fundamental changes in shopping preferences toward convenience, product variety, and time efficiency, influencing distribution strategies across the ready meals industry.

By Category: Vegetarian Surge Challenges Non-Vegetarian Majority

Non-vegetarian ready meals command a 60.02% market share in 2025, supported by established protein preferences and supply chain infrastructure. Vegetarian ready meals demonstrate a 4.15% CAGR through 2031, reflecting increased consumer adoption of plant-based nutrition, environmental sustainability, and health-conscious eating habits. Market analysis shows ready meals rank third in consumer preference for plant-based alternatives, following finger foods and fried items, demonstrating expansion opportunities in the vegetarian segment. Besides, the COVID-19 pandemic drove higher consumption of plant-based ready meals due to increased consumer focus on health and environmental sustainability.

Consumer acceptance barriers persist, particularly regarding taste, texture, and price compared to conventional meat products. Research in Australia indicates that while younger consumers demonstrate demand for plant-based options, cultural ties to traditional meat consumption create market resistance. Conventional meat products maintain competitive advantages in established supply chains, consumer familiarity, and perceived protein content. However, the plant-based market continues to expand, driven by environmental considerations, health benefits, and product quality improvements that address taste and texture limitations.

Geography Analysis

North America commands the largest market share at 34.10% in 2025, supported by mature cold chain infrastructure, high consumer acceptance of convenience foods, and established distribution networks. The region's leadership stems from decades of investment in frozen food technology and sophisticated supply chain management systems that ensure product quality from manufacturing to consumer delivery. However, the region faces challenges from increasing health consciousness and competition from fresh alternatives, meal kits, and home cooking trends.

Asia-Pacific emerges as the fastest-growing region at 4.83% CAGR through 2031, driven by rapid urbanization, rising disposable incomes, and evolving dietary patterns in emerging economies. Advanced transportation management systems are enhancing frozen food distribution capabilities across the region, improving route optimization and product quality while reducing costs. China's inclusion of lab-grown meats and plant-based food alternatives in its five-year agricultural plan indicates a focus on sustainable food technologies to ensure food security and address climate change. However, infrastructure challenges persist in rural areas, where inadequate cold chain systems and limited transportation access constrain market penetration.

Europe maintains a significant market position with established consumer bases and regulatory frameworks that support food safety and quality standards, though growth rates remain moderate compared to emerging markets. The region leads in sustainability initiatives and clean-label product development, reflecting consumer preferences for environmental responsibility and natural ingredients. Moreover, South America, and Middle East and Africa present emerging opportunities with varying growth trajectories influenced by economic development, infrastructure capabilities, and cultural food preferences. Rural logistics challenges across these regions necessitate innovative transportation solutions to improve food accessibility and market reach.

Competitive Landscape

The ready meals market exhibits moderate fragmentation, creating competitive market conditions. Major players, including Nestlé S.A., Conagra Brands Inc., The Kraft Heinz Company, Nomad Foods Limited, and Tyson Foods Inc., operate alongside regional specialists and new market entrants. This market structure encourages companies to differentiate their products through innovation and develop specialized offerings for specific consumer segments and dietary requirements.

Technology adoption is a key competitive factor in the ready meals market. Companies implement advanced preservation methods, smart packaging systems, and automated production lines to improve product quality and operational efficiency while reducing costs. New developments include battery-free, stretchable, and autonomous smart packaging that monitors food freshness and extends shelf life, contributing to waste reduction and sustainability. Companies are also implementing reinforcement learning in robotic packaging systems to improve productivity and maintain consistent product quality despite supply variations.

Furthermore, companies are implementing strategic changes in response to evolving consumer preferences, emphasizing product transparency, sustainability initiatives, and nutritional value in their ready meals segment. Conagra introduced carbon-neutral certified frozen meals, demonstrating the implementation of environmental practices into convenience foods. Nestlé expanded its plant-based ready-to-eat meal portfolio to address market demand from health-conscious consumers seeking meat alternatives. Companies are implementing clean-label strategies and incorporating nutritional ingredients to establish competitive advantages in the ready meals market.

Ready Meals Industry Leaders

-

Nestlé S.A.

-

Conagra Brands Inc.

-

The Kraft Heinz Company

-

Nomad Foods Limited

-

Tyson Foods Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: YO! expanded its product portfolio by introducing a frozen meal range in Tesco stores, which included Chicken Katsu Bao Bun Kit, Chicken Teriyaki, Korean Style BBQ Beef, and Chicken Katsu.

- February 2025: Bonduelle introduced ready-to-eat Lunch Bowls that contained plant-based ingredients with over 10 grams of protein and no artificial preservatives.

- January 2025: SPAR Gran Canaria expanded its product portfolio by launching a 'Fresh To Go' ready meal range across its retail network. The range, developed in collaboration with Helamore, featured 40-50 meal options and was available in more than 55 SPAR Supermarkets in Gran Canaria.

Global Ready Meals Market Report Scope

Ready meals are already prepared foods that are sold in shops and required to heat before consumption. The global ready meals market is segmented by product type, distribution channel, and geography. By product type it is segmented into frozen ready meals, chilled ready meals, canned ready meals, and freeze-dried ready meals. Distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, online retailers, and other distribution channels. The study also involves the global-level analysis of the main regions such as North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. For each segment, the market sizing and forecasts have been done based on value (in USD Million).

By Product Type

| Frozen Ready Meals |

| Chilled Ready Meals |

| Shelf Stable |

| Freeze-Dried Ready Meals |

By Ingredient

| Conventional |

| Free-From |

By Category

| Vegetarian |

| Non-Vegetarian |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Frozen Ready Meals | |

| Chilled Ready Meals | ||

| Shelf Stable | ||

| Freeze-Dried Ready Meals | ||

| By Ingredient | Conventional | |

| Free-From | ||

| By Category | Vegetarian | |

| Non-Vegetarian | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the ready meals market?

The ready meals market size is USD 97.92 billion in 2026 and is projected to climb to USD 113.53 billion by 2031.

Which product segment holds the largest ready meals market share?

Frozen entrées dominate with 52.93% market share in 2025 and remain the fastest-growing at a 3.55% CAGR.

Which region is expanding the quickest in the ready meals market?

The Asia-Pacific market projects a CAGR of 4.83% through 2031, attributed to urbanization and rising disposable incomes.

How is e-commerce influencing the ready meals industry?

The online retail market is expanding at a CAGR of 4.52%, supported by dark-store logistics operations, efficient last-mile delivery networks, and increasing consumer adoption of digital purchasing channels.

Page last updated on: