Online Grocery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

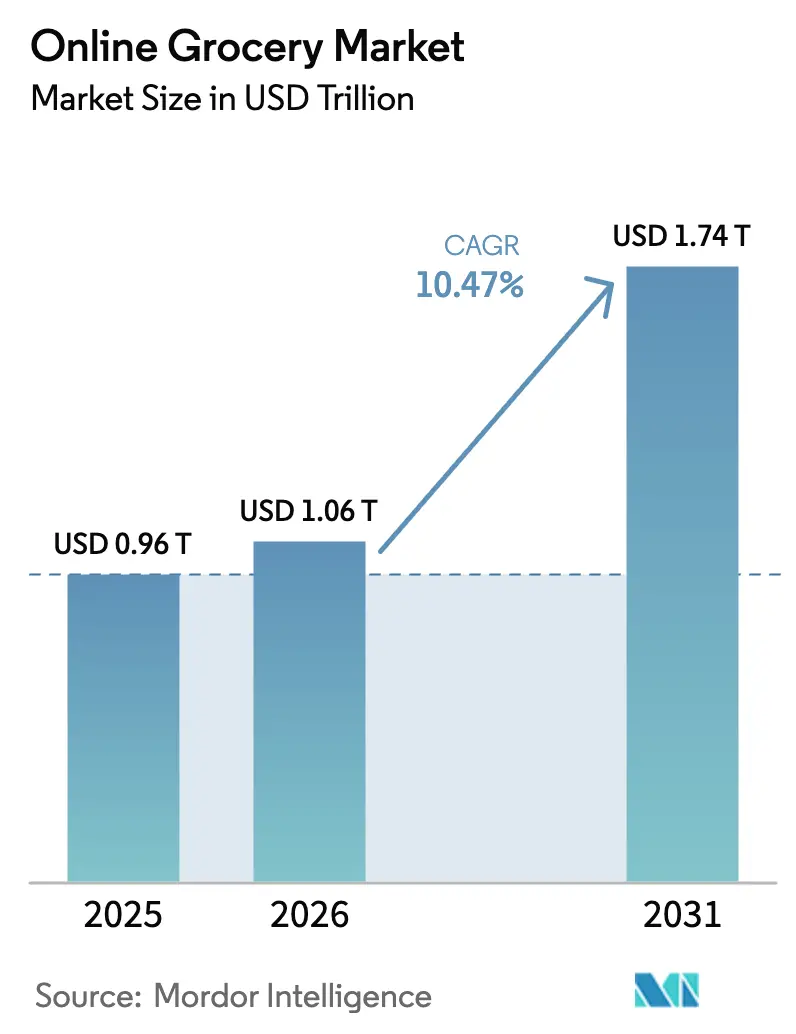

| Market Size (2026) | USD 1.06 Trillion |

| Market Size (2031) | USD 1.74 Trillion |

| Growth Rate (2026 - 2031) | 10.47% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Online Grocery Market Analysis by Mordor Intelligence

The online grocery market size in 2026 is estimated at USD 1.06 trillion, growing from the 2025 value of USD 0.96 trillion, with 2031 projections showing USD 1.74 trillion, growing at 10.47% CAGR over 2026-2031. This growth underscores a significant shift in consumer behavior, leaning towards digital-first and convenience-centric shopping. Key drivers of this expansion include the swift rise of dark stores and micro-fulfillment centers, AI-driven inventory and picking systems, and a growing preference for same-day delivery. Additionally, subscription-based loyalty programs and the expansion of private labels via proprietary apps are fortifying ties between retailers and customers. Major platforms like Amazon Fresh, Walmart Grocery, and BigBasket showcase the power of automation, proximity-based fulfillment, and technological integration in revolutionizing grocery retail. Urbanization is intensifying the demand for quicker, more adaptable delivery options. With consumers placing a premium on speed, variety, and convenience, online grocery shopping is solidifying its status as a central tenet of contemporary retail strategy, rather than merely an adjunct channel.

Key Report Takeaways

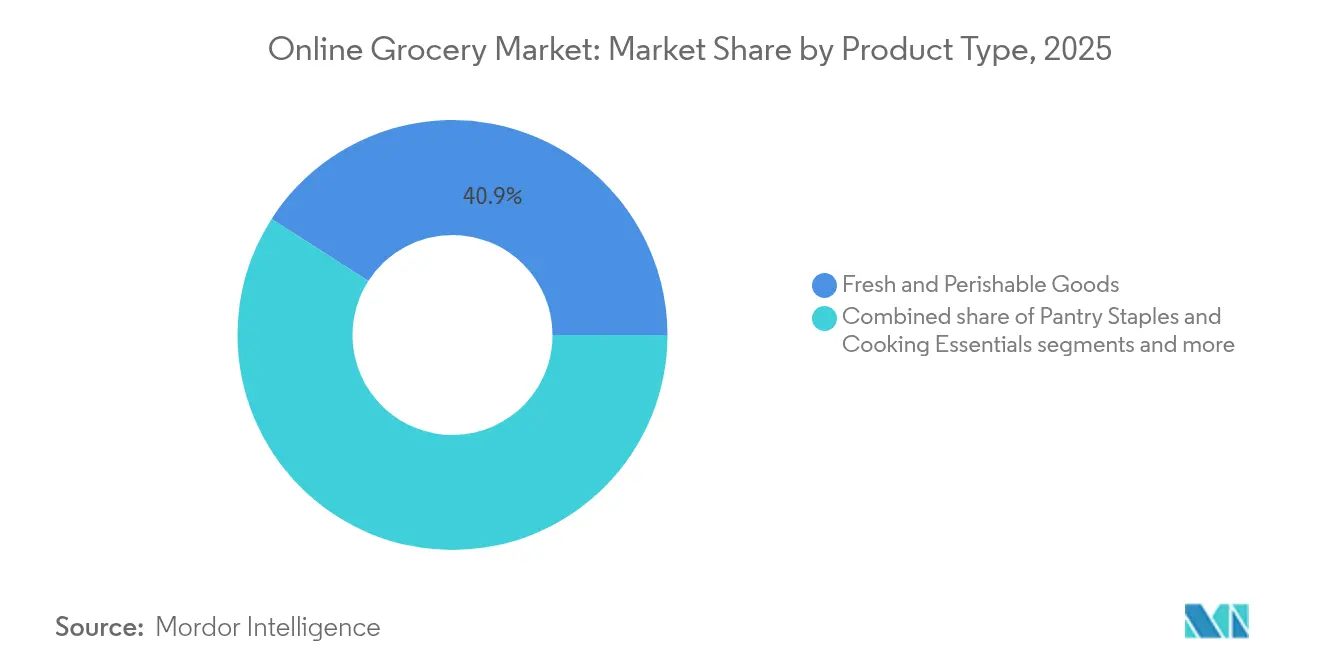

- By product category, fresh and perishable goods held 40.92% of the online grocery market share in 2025, whereas packaged foods are projected to register a 18.85% CAGR through 2031.

- By delivery model, same-day services commanded 51.78% of the online grocery market size in 2025, and instant delivery is set to grow at 17.92% CAGR to 2031.

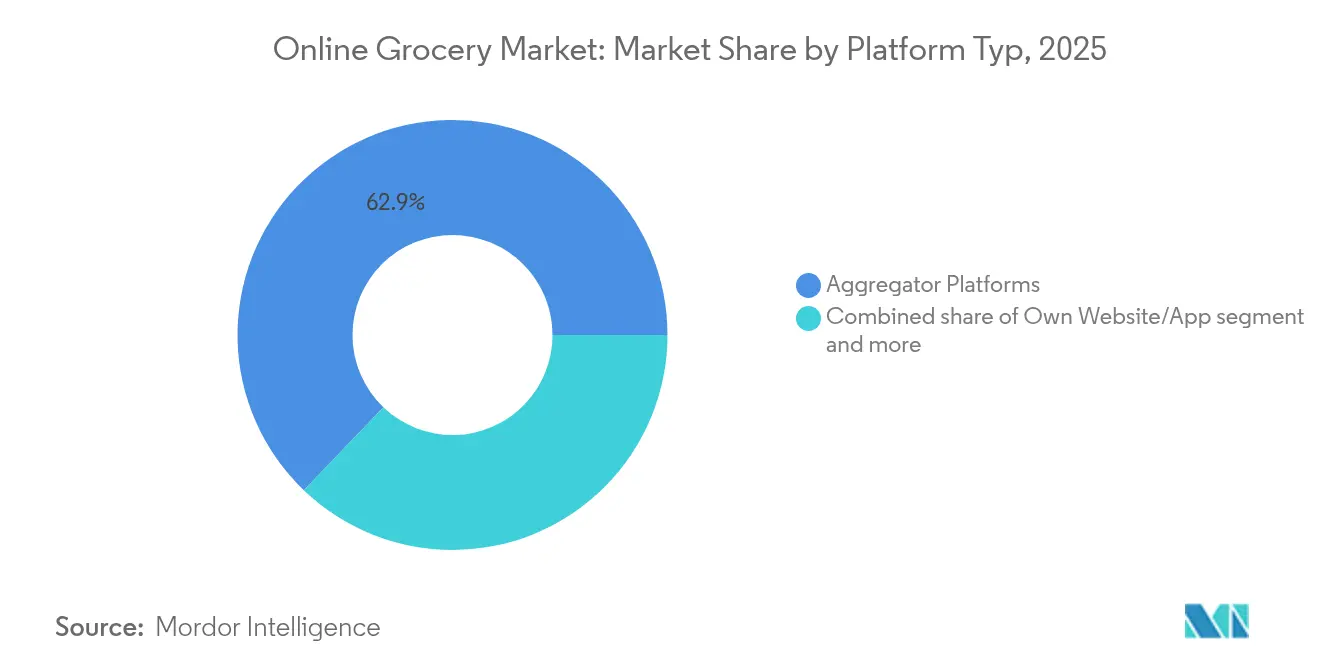

- By platform type, aggregator sites controlled 62.85% of 2025 spend, while retailer-owned sites and apps are forecast to expand at 17.45% CAGR by 2031.

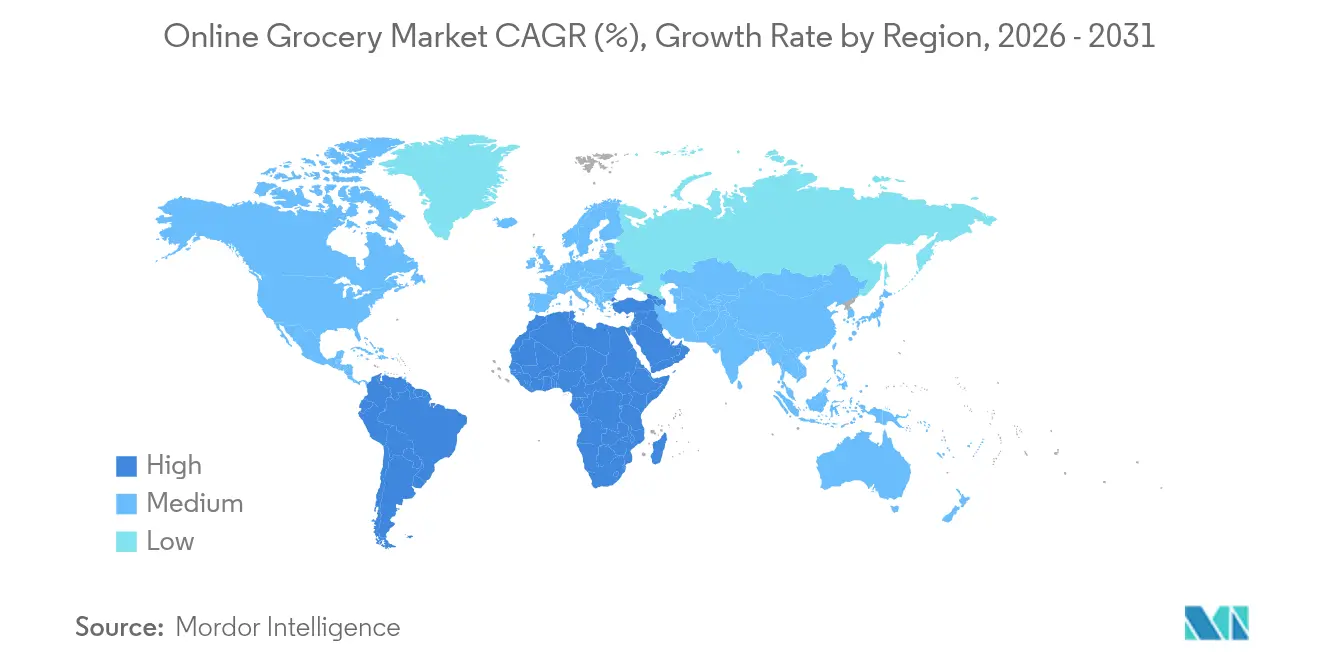

- By geography, North America led with 35.98% revenue share in 2025, and Asia-Pacific is on track for 20.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Online Grocery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Convenience driven by urban lifestyles | +2.8% | Global metro areas | Medium term (2-4 years) |

| Customer loyalty through subscriptions | +1.9% | North America, Europe, emerging Asia-Pacific | Long term (≥ 4 years) |

| Faster delivery through dark store expansion | +2.1% | North America-led global roll-out | Short term (≤ 2 years) |

| Personalized and contactless tech integration | +1.7% | Developed markets, selective Asia-Pacific | Medium term (2-4 years) |

| Mobile-optimized shopping and digital payments | +1.5% | Asia-Pacific leadership, global spread | Short term (≤ 2 years) |

| Demand for sustainable and eco-friendly packaging | +1.1% | Europe, North America, widening reach | Long term (≥ 4 years |

| Source: Mordor Intelligence | |||

Convenience Driven by Urban Lifestyles

Urbanization is accelerating, and with the rise of dual-income households, grocery shopping behaviors are evolving worldwide. In urbanized nations such as Japan (92%), Argentina (90%), the Netherlands (89%), and the U.S. (83%), city dwellers are increasingly turning to convenient solutions for their daily essentials [1]Source: World Population Review (2024)"Most Urbanized Countries 2024," worldpopulationreview.com. In cities like Mumbai and New York, consumers schedule deliveries to align with their routines, avoiding long queues and crowded aisles. Platforms like BigBasket (Tata Group) and Instacart (in collaboration with various U.S. retailers) are revolutionizing the shopping experience with features like flexible delivery windows, saved shopping lists, and auto-reordering. Retail giants such as Amazon (Amazon Fresh), Walmart (Great Value, Sam’s Choice), and Kroger (Simple Truth) are enhancing the journey through personalized product curation, AI-driven recommendations, and micro-fulfillment centers. Concurrently, FMCG behemoths like Nestlé, Unilever, and PepsiCo are capitalizing on these platforms, optimizing product visibility, bundling strategies, and ensuring delivery readiness for the digital-savvy consumer.

Customer Loyalty Through Subscriptions

Online grocery subscription models are reshaping the landscape of FMCG sales, catering to a consumer base that increasingly values convenience, consistency, and personalization. For consumers, these subscriptions streamline routine purchases like milk, cereals, or snacks by automating the reordering process. This not only minimizes effort but also fosters habitual brand loyalty. Take Kroger’s Boost and Albertsons’ Schedule & Save, for instance. They enable consumers to effortlessly subscribe to regular deliveries from major brands like Nestlé, Unilever, and PepsiCo, ensuring their pantries are consistently stocked without the hassle of repeated decision-making. Beyond just free delivery, these subscription models offer added perks, exclusive discounts, priority delivery slots, and even fuel rewards. Such incentives not only bolster consumer loyalty to the platform but also to the brands prominently featured in their subscriptions. In emerging markets, platforms like Blinkit and Zepto are capitalizing on this trend. Urban Indian consumers are increasingly leveraging subscription and instant delivery features, especially for impulse buys and high-turnover items like snacks and beverages.

Faster Delivery Through Dark Store Expansion

Dark stores, tailored exclusively for online grocery orders, are reshaping the landscape of delivery speed and reliability in busy urban locales. Unlike traditional supermarkets, these centers prioritize rapid picking, packing, and dispatching, resulting in heightened efficiency, fewer stockouts, and superior inventory management. U.S.-based GoPuff and India's BigBasket have broadened their dark store networks, responding to urban demands, particularly during peak times like festivals or lockdowns. Retail behemoths, such as Walmart, have rolled out dark stores in cities like Dallas and Bentonville. By doing so, they've adeptly separated in-store experiences from logistics, amplifying both operational speed and customer satisfaction. Nestled within a 2–3 mile radius of densely populated areas, these facilities promise delivery windows of 30 minutes or less, propelling the quick commerce surge. For FMCG brands, dark stores ensure better shelf availability and faster product turnover, especially benefiting high-demand items like snacks, dairy, and beverages. As consumer appetite for immediacy grows, dark stores have transitioned from simple logistical tools to pivotal players in the race for speed, consistency, and accuracy in the modern grocery retail arena.

Mobile-Optimized Shopping and Digital Payments

Smartphones and affordable internet access have made mobile-first shopping a key player in the online grocery scene. Shoppers are turning to mobile apps for their grocery needs, drawn by the convenience, real-time personalization, and smooth integration with secure payment systems like UPI, Google Pay, Paytm, and credit cards. In India, retailers like Blinkit (formerly Grofers) and Reliance Smart have crafted user-friendly mobile platforms. These platforms boast features such as instant product searches, tailored promotions, order tracking, and one-tap payments, making the shopping experience more efficient. The Press Information Bureau (2024) reports that in FY 2023–24, India saw over 13,462 crore digital payment transactions, with UPI making up 44% of retail payments [2]Source: Press Information Bureau, “Digital Payments in India: Performance 2023-24,” pib.gov.in. At the same time, as internet access broadens, so does the reach of mobile grocery services. World Population Review (2024) highlights that internet penetration is at 66% in India, 77.5% in China, and exceeds 90% in the United States and the United Kingdom [3]Source: World Population Review (2024)"Internet Penetration by Country," worldpopulationreview.com. Mobile grocery platforms, with features like push notifications, auto-replenishment, and personalized reminders, not only simplify the shopping process but also foster frequent and engaged interactions with FMCG brands.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High delivery fees and surcharges | -1.8% | Global, price-sensitive regions | Short term (≤ 2 years) |

| Persistent preference for in-store shopping | -2.1% | Rural areas, traditional markets | Long term (≥ 4 years) |

| Concerns over freshness and quality | -1.4% | Universal, perishables-centric baskets | Medium term (2-4 years) |

| Operational complexities in fulfillment | -1.2% | Emerging markets, dispersed geographies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Delivery Fees and Surcharges Impact Affordability

As economic conditions tighten, price-sensitive consumers are increasingly wary of delivery fees, hindering the adoption of online grocery shopping. Retailers grapple with the challenge of balancing soaring operational costs against consumers' demand for budget-friendly services. Take Amazon Fresh, for example: it recently upped its free delivery threshold from USD 35 to a hefty USD 150. This move drew ire from loyal users, many of whom felt it created an unwelcome barrier. Across the pond in the United Kingdom, Tesco's decision to raise its minimum order value from EUR 40 to EUR 50 underscores a broader industry trend. Retailers are not just aiming to boost average order sizes but also to enhance the economics of each order. With rising delivery expectations, online grocery platforms face the daunting task of balancing affordability with operational efficiency.

Preference for In-Store Shopping

Even as online grocery platforms expand, many consumers still favor the traditional in-store shopping experience. This is especially true for fresh items like fruits, vegetables, and meats, where touch, smell, and visual inspection are crucial. Older adults and rural shoppers often hesitate to embrace digital platforms, citing either limited digital literacy or skepticism about the quality of items chosen by others. In-store shopping allows consumers to compare products, discover new ones, and participate in promotions activities some find more intuitive than navigating online. Retailers have rolled out features like high-resolution images, freshness guarantees, and hassle-free returns, yet these can't fully replicate the tactile, social, and exploratory aspects of in-person shopping. This enduring preference for brick-and-mortar grocery shopping poses a significant challenge to the growth of online grocery platforms, especially in regions with deep-rooted supermarket cultures and established shopping habits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Fresh Goods Drive Volume, Packaged Foods Accelerate Growth

In 2025, fresh and perishable goods dominate the online grocery landscape, commanding a 40.92% market share. This trend underscores a growing consumer trust in the integrity of cold chains and the promptness of deliveries. FMCG players, especially in the dairy, produce, and protein sectors, are seizing this opportunity, tapping into direct-to-consumer channels that were previously the domain of offline retail. Brands such as Amul, Mother Dairy, and Nestlé are broadening their horizons, forging alliances with e-grocery platforms. Meanwhile, meat and seafood entities like Licious and ITC Master Chef are making strides with dark-store models and refrigerated logistics, emphasizing hygiene, quality, and convenience to scale their online presence in the perishable FMCG segment.

While fresh goods lead in market share, packaged and convenience foods are on a rapid ascent, boasting a projected CAGR of 18.85% through 2031. This surge is advantageous for brands like PepsiCo, ITC, and Mondelez, as their ready-to-eat snacks, cereals, and meal kits enjoy frequent online basket placements. Digital platforms empower FMCG companies to roll out tailored promotions, combo deals, and auto-reorder features, amplifying both purchase frequency and order size. Premium segments, notably baby care, are witnessing a surge in online traction.

By Delivery Model: Same-Day Dominance Challenged by Instant Expansion

As of 2025, same-day delivery dominates the online grocery market, holding a 51.78% share. This model strikes an optimal balance between speed and cost, making it the go-to choice for industry giants like Unilever, Nestlé, and PepsiCo. These companies, known for their diverse range of daily-use FMCG products, have partnered with platforms like BigBasket and Amazon Fresh. This collaboration ensures swift access to essentials, from packaged foods and dairy to beverages and personal care items. Such a strategy not only promotes frequent purchases but also guarantees consistent visibility on digital shelves.

Meanwhile, instant delivery is surging ahead, boasting a robust CAGR of 17.92% projected through 2031. Major players like ITC, Amul, Coca-Cola, and Dabur are harnessing the power of quick commerce platforms, including Blinkit, Zepto, and Swiggy Instamart. These platforms cater to urban consumers' cravings for groceries delivered in a mere 10 to 30 minutes. By capitalizing on impulse and convenience-driven buying habits, these platforms enable companies to amplify sales of popular items like juices, frozen foods, snacks, and health supplements. As a result, instant delivery is solidifying its role as a pivotal channel for enhancing order frequency and reinforcing brand recall in bustling urban landscapes.

By Platform Type: Aggregators Lead While Proprietary Channels Gain Ground

In 2025, aggregator platforms command a significant 62.85% share of the online grocery market, streamlining access to multiple retailers for consumers. This approach not only boosts visibility and sales volume for FMCG companies but also aids brands like Dabur, ITC, and Nestlé in tapping into a broader audience, driven by the allure of convenience. Aggregators such as Blinkit, Instamart, and BigBasket enhance the shopping experience for consumers, facilitating easy comparisons and swift checkout elements that spur both impulse and habitual purchases.

Meanwhile, proprietary websites and apps are witnessing the fastest growth, with a projected CAGR of 17.45% through 2031. Retail giants like Walmart and Kroger are channeling investments into these direct platforms, sidestepping aggregator fees and securing customer data control. This strategic pivot fosters deeper collaborations between FMCG companies and retail partners, paving the way for tailored promotions, strategic bundling, and meticulous inventory planning. While consumers still gravitate towards aggregator platforms for their convenience and diverse offerings, proprietary channels present enhanced profit margins and superior brand positioning for both retailers and FMCG entities.

Geography Analysis

In 2025, North America commands a dominant 35.98% share of the online grocery market, underscoring its status as the industry's most developed region. This supremacy is attributed to North America's sophisticated e-commerce framework, the widespread embrace of digital payments, and a pronounced urban demand. Major FMCG players have adeptly harnessed platforms like Amazon Fresh, Walmart, and Kroger, crafting robust omnichannel strategies to cater to the needs of time-sensitive consumers. The region's urban centers, with their heightened emphasis on convenience and speed, have bolstered consistent sales of packaged foods, personal care products, and household necessities, facilitated through both same-day and scheduled delivery services.

Meanwhile, the Asia-Pacific region is witnessing the most rapid expansion, boasting a CAGR of 20.95% projected through 2031. Swift urbanization, a mobile-centric consumer base, and the rise of instant retail services fuel this surge. Countries such as India, Indonesia, and Vietnam are experiencing heightened FMCG engagement, with platforms like Blinkit, BigBasket, and GrabMart,JD.com, Alibaba’s Freshippo, and Pinduoduo These platforms not only facilitate the sale of cooking essentials and health beverages but also leverage algorithmic recommendations and expedited reordering, much to the advantage of FMCG brands.

Europe's steady growth is driven by regulatory support for sustainable deliveries and digital transparency. Major players like Nestlé and Danone are aligning with local sustainability and packaging standards while partnering with platforms such as Ocado and Carrefour Online. South America's digital landscape is evolving due to smartphone adoption and the dominance of platforms like Mercado Libre, enabling FMCG brands to enhance digital distribution in beverages and dry groceries. In the Middle East and Africa, rising urban density and mobile payments are helping companies like Unilever and PepsiCo establish digital platforms and collaborate with local e-retailers.

Mordor Intelligence provides coverage of the online grocery market across other key regional markets, including Asia, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to Canada incorporating local coverage and market participation, as required.

Competitive Landscape

The online grocery market is moderately consolidated, and FMCG companies vie for a larger slice of consumer spending through digital channels. With a growing number of consumers opting for online orders, brands are feeling the heat to stand out on the digital shelf, be it through pricing, packaging, or savvy promotions. Meanwhile, online delivery giants like Amazon Fresh, BigBasket, and Swiggy Instamart leverage data-driven algorithms to dictate product placements, often swaying which brands dominate search results and snag promotional spots.

This competition has escalated as these delivery platforms, doubling as distribution partners, also champion their private labels, directly challenging national FMCG brands. For example, Amazon and Reliance, for instance, aggressively promote their in-house offerings in food staples and household categories, putting them in direct contention with industry stalwarts like Unilever, ITC, and Nestlé for coveted digital shelf space. In response, FMCG brands are rolling out exclusive SKUs, bundle deals, and platform-specific launches, underscoring that today's competition is as much about digital finesse as it is about product quality.

FMCG companies are also zeroing in on delivery performance and consumer experience, forging alliances with partners that promise swift fulfillment, appealing product presentation, and reliable service. Brand loyalty is increasingly tethered to the reliability of delivery and online representation. This makes collaborations with platforms that prioritize automation, cold chain logistics, and user-friendly apps paramount.

Online Grocery Industry Leaders

-

Nestlé S.A.

-

Unilever PLC

-

The Kraft Heinz Company

-

General Mills, Inc.

-

PepsiCo, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: C&S Wholesale Grocers acquired SpartanNash for USD 1.77 billion, creating a network of nearly 60 distribution centers that serves about 10,000 independent stores

- June 2025: Walmart opened dedicated dark stores in Dallas, Texas and Bentonville, Arkansas to accelerate e-commerce order fulfillment

- January 2025: Wegmans partnered with Uber Eats to widen delivery reach and leverage shared rider fleets

- July 2024: Walmart announced five automated fresh-food distribution centers across five U.S. states to boost perishables capacity

Global Online Grocery Market Report Scope

| Fresh and Perishable Goods | Fresh Produce |

| Dairy Products | |

| Meat, Poultry and Seafood | |

| Bakery | |

| Pantry Staples and Cooking Essentials | Cereals, Grains, Pulses |

| Cooking Oils | |

| Spices and Condiments | |

| Packaged and Convenience Foods | Ready-to-Eat (RTE) and Ready-to-Cook (RTC) Foods |

| Snacks | |

| Meat, Poultry and Seafood | |

| Confectionery | |

| Other Packaged Foods | |

| Beverages | |

| Personal Care Products | |

| Household Cleaning Products | |

| Baby Care Products | |

| Others |

| Instant Delivery |

| Same-Day Delivery |

| Scheduled Delivery |

| Other Models |

| Own Website/App |

| Aggregator Platforms |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Category | Fresh and Perishable Goods | Fresh Produce |

| Dairy Products | ||

| Meat, Poultry and Seafood | ||

| Bakery | ||

| Pantry Staples and Cooking Essentials | Cereals, Grains, Pulses | |

| Cooking Oils | ||

| Spices and Condiments | ||

| Packaged and Convenience Foods | Ready-to-Eat (RTE) and Ready-to-Cook (RTC) Foods | |

| Snacks | ||

| Meat, Poultry and Seafood | ||

| Confectionery | ||

| Other Packaged Foods | ||

| Beverages | ||

| Personal Care Products | ||

| Household Cleaning Products | ||

| Baby Care Products | ||

| Others | ||

| By Delivery Model | Instant Delivery | |

| Same-Day Delivery | ||

| Scheduled Delivery | ||

| Other Models | ||

| By Platform Type | Own Website/App | |

| Aggregator Platforms | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the online grocery market?

The online grocery market size is valued at USD 1.06 trillion in 2026 and is forecast to reach USD 1.74 trillion by 2031.

Which product category leads digital grocery sales today?

Fresh and perishable goods account for 40.92% of online grocery market share, reflecting strong consumer trust in cold-chain reliability.

How fast is instant delivery growing?

Instant delivery services in the online grocery market are projected to post 17.92% CAGR between 2026 and 2031, outpacing other delivery models.

Which region will see the fastest online grocery growth?

Asia-Pacific is set to expand at 20.95% CAGR through 2031, driven by mobile-first consumer behavior and dense urban ecosystems.

Page last updated on: