Market Overview

| Study Period | 2021 - 2031 |

|---|---|

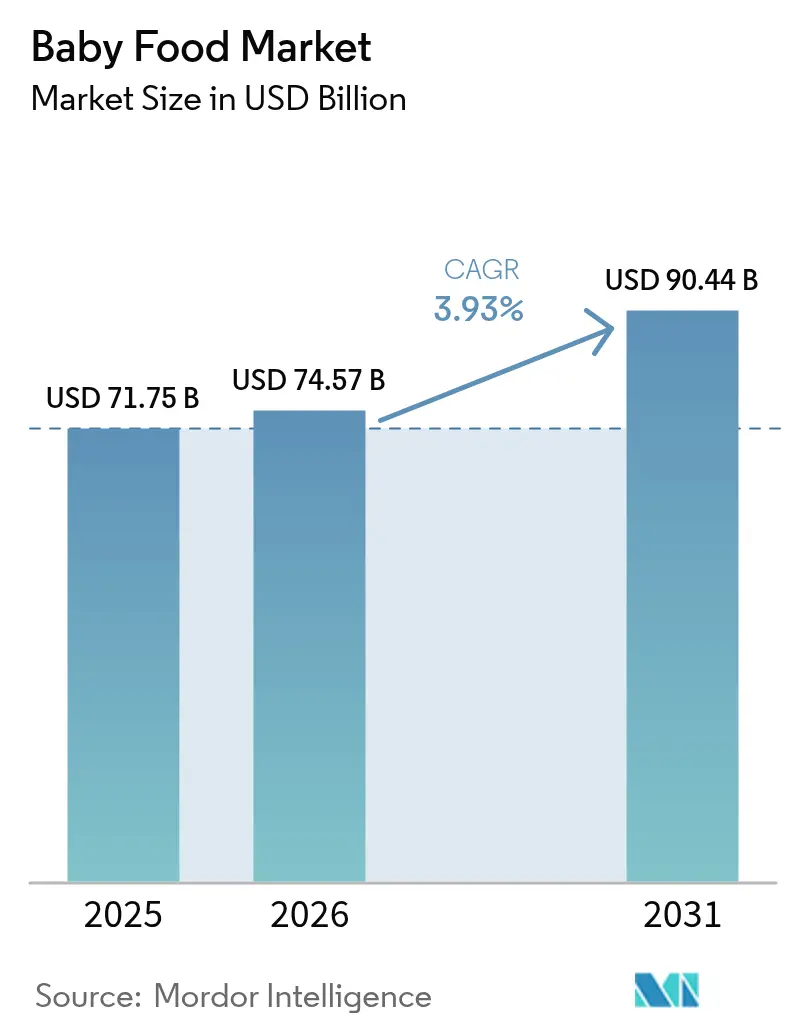

| Market Size (2026) | USD 74.57 Billion |

| Market Size (2031) | USD 90.44 Billion |

| Growth Rate (2026 - 2031) | 3.93% CAGR |

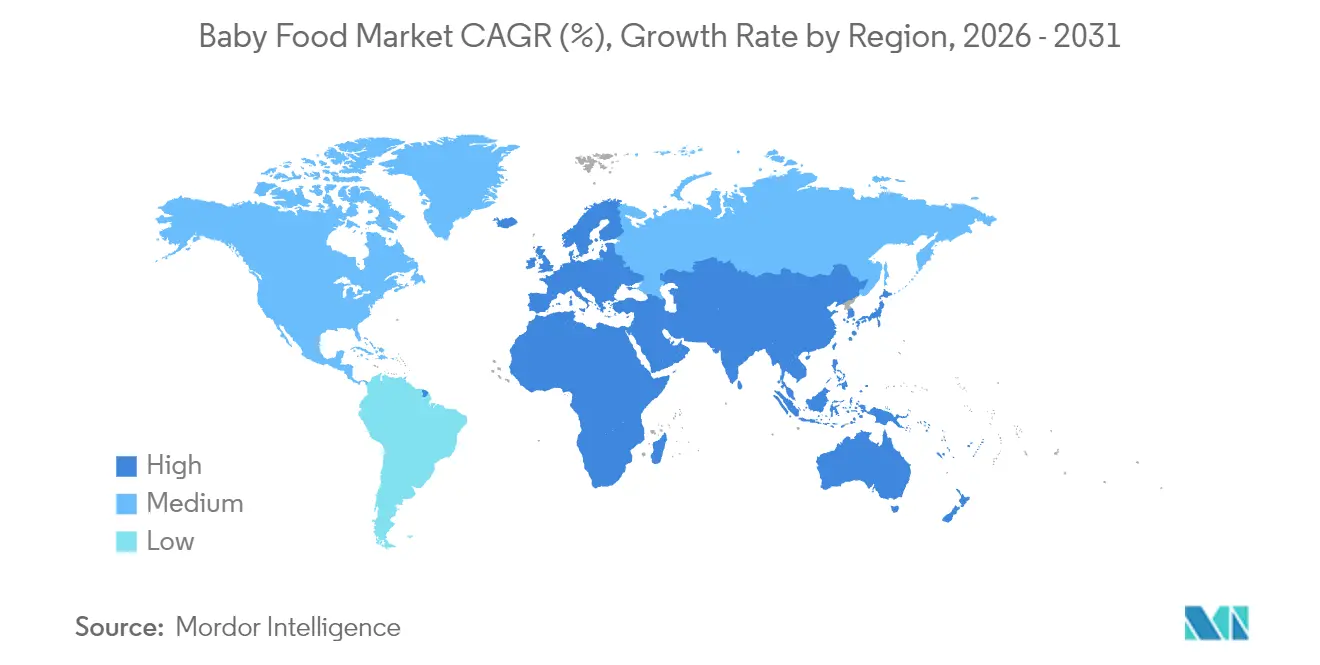

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

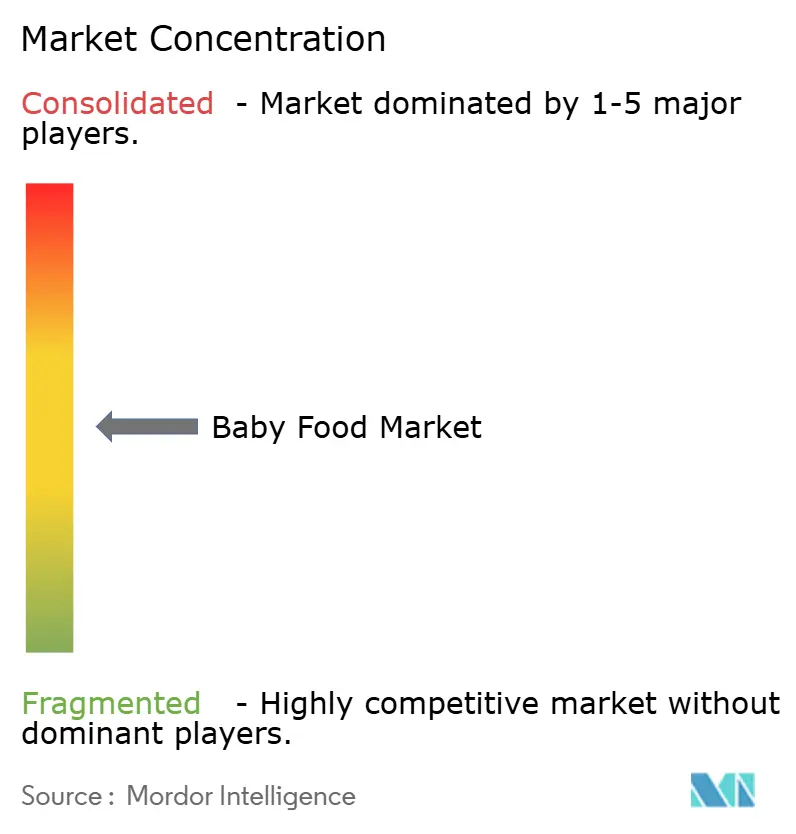

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Baby Food Market Analysis by Mordor Intelligence

Baby food market size in 2026 is estimated at USD 74.57 billion, growing from 2025 value of USD 71.75 billion with 2031 projections showing USD 90.44 billion, growing at 3.93% CAGR over 2026-2031. This growth is driven by a combination of factors: increasing participation of women in the workforce, a shift towards premium nutrition, and swift innovations in ingredients. The Asia-Pacific region, bolstered by its large infant population and a burgeoning middle class, takes the lead on the global stage. Meanwhile, North America and Europe are banking on premiumization strategies to fuel their revenue growth. Competition intensifies among both global and regional brands, spurred by tech-driven product innovations, most notably human-milk-oligosaccharide (HMO) fortification and novel digital engagement strategies. However, the momentum is tempered by stricter safety regulations and declining birth rates in developed nations.

Key Report Takeaways

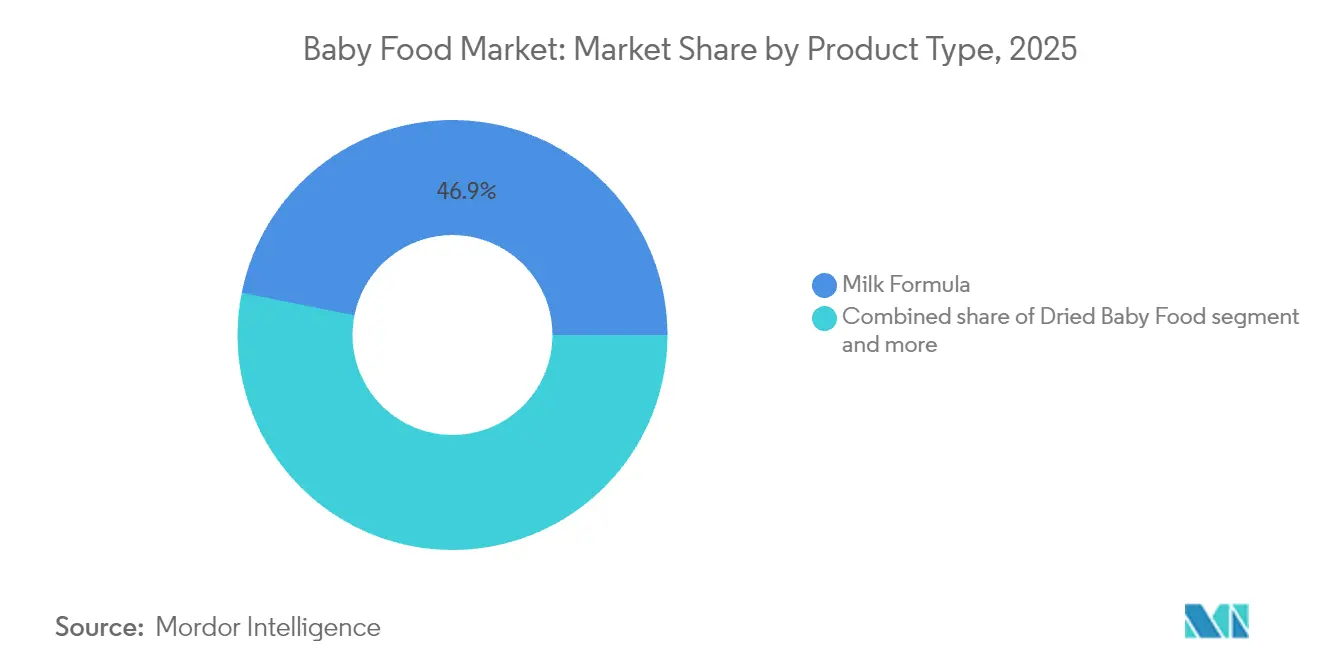

- By product type, milk formula captured 46.85% of the baby food market share in 2025, while prepared baby food is forecast to expand at a 6.17% CAGR to 2031.

- By category, conventional offerings held 64.05% revenue share in 2025; organic products are poised for a 7.36% CAGR through 2031.

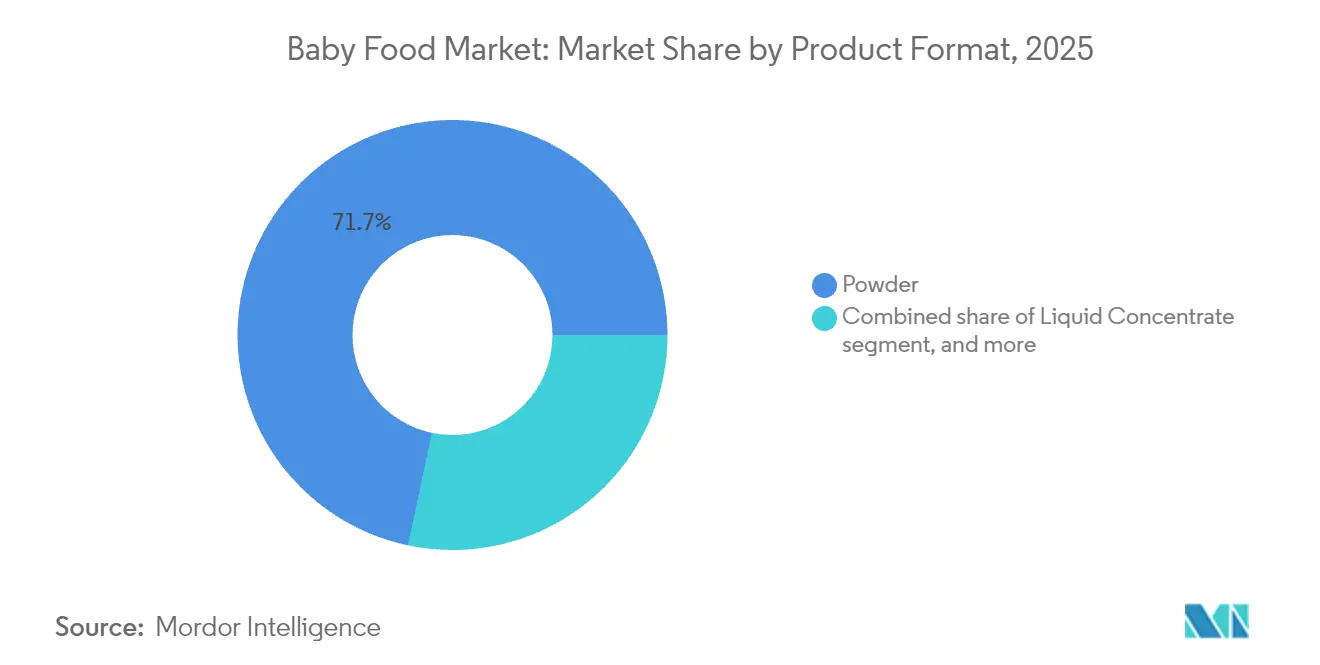

- By product format, powder accounted for 71.68% of the baby food market size in 2025, and ready-to-feed leads growth at a 5.75% CAGR.

- By age group, infants aged 0–6 months represented 45.25% of 2025 revenue, and the 24–36 months cohort is advancing at a 6.35% CAGR.

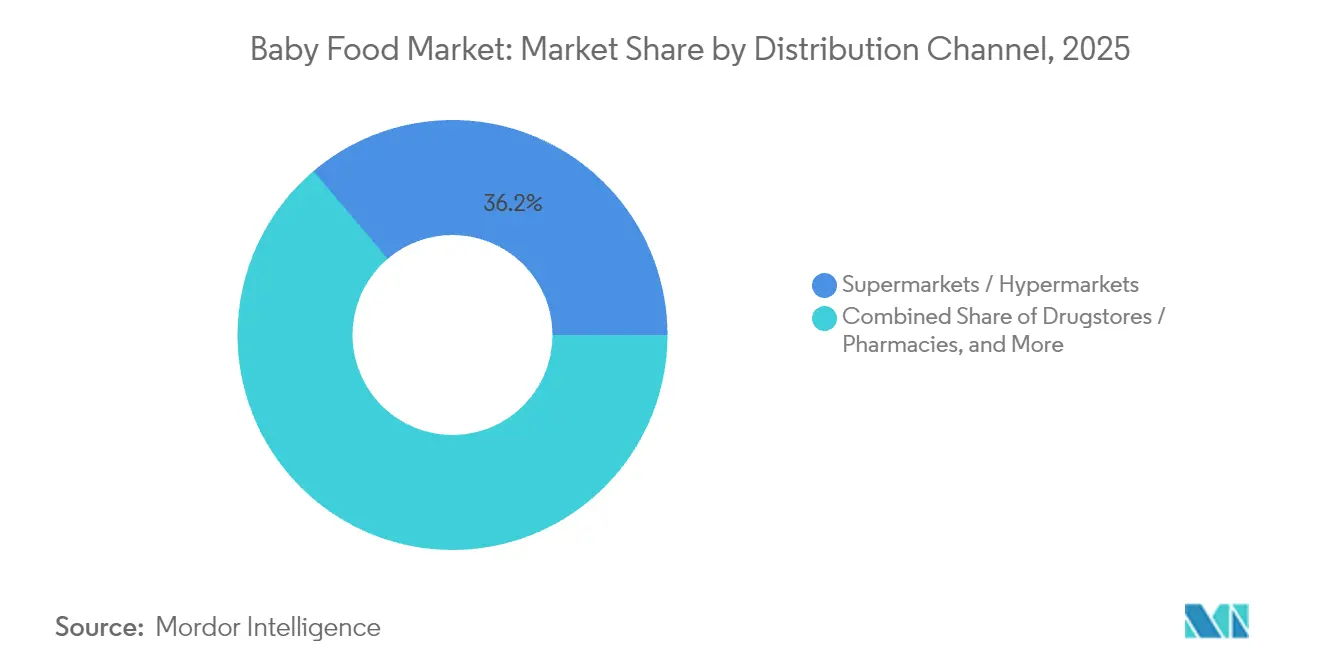

- By distribution channel, supermarkets and hypermarkets led with 36.20% revenue share in 2025, whereas online retail stores shows a 6.58% CAGR to 2031.

- By geography, the Asia-Pacific accounted for 44.40% in 2025, and is expected to grow at a 6.82% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Baby Food Market*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising female workforce participation | +1.2% | Global, with strongest impact in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Premiumisation in upper-middle-income households | +0.8% | North America, Europe, urban Asia-Pacific centers | Long term (≥ 4 years) |

| Commercialisation of human-milk-oligosaccharide (HMO) fortification | +0.6% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Plant-based and hybrid formulas | +0.5% | North America, Europe, with spillover to urban Asia-Pacific | Medium term (2-4 years) |

| Functional nutrition and immunity support | +0.4% | Global, with premium positioning in developed markets | Long term (≥ 4 years) |

| Ready-to-eat and portable formats | +0.3% | Global, strongest in urban centers and working-parent demographics | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising female workforce participation

As more mothers join the workforce, infant feeding patterns are shifting. Working mothers are turning to formula and ready-made baby foods to keep up with feeding schedules. In the U.S., labor force participation rates for mothers with children under three have rebounded to post-pandemic levels. Meanwhile, in India, female workforce participation hit 37% in 2022-23, marking a notable demographic shift, according to the Bureau of Labor Statistics. This trend is especially evident in urban areas, where dual-income households are increasingly common, driving a consistent demand for convenient feeding solutions. In markets with limited maternity leave policies, the link between maternal employment and formula use is particularly strong. Here, the need for supplemental feeding options arises from an earlier return to work. Furthermore, government initiatives, such as extended childcare benefits and workplace lactation support, are shaping regional demand patterns. These efforts are steering preferences towards premium and convenient baby food options.

Premiumisation in upper-middle-income households

Upper-middle-income households are increasingly opting for premium baby food products. Organic and functional nutrition segments now command a price premium of 30-50% over their conventional counterparts. This trend towards premiumization underscores a shift in parental priorities, emphasizing ingredient transparency, nutritional value, and brand trust. This is especially pronounced among millennial and Gen Z parents, who often prioritize quality over cost. In developed markets, where disposable income growth outstrips inflation, there's a notable willingness to invest in what are perceived as superior nutrition options. Organic baby food sales are surging, outpacing conventional products, as parents come to equate organic certification with enhanced safety and nutrition. This shift is paving the way for smaller, specialized brands to seize market share, leveraging targeted positioning and direct-to-consumer distribution strategies.

Commercialisation of human-milk-oligosaccharide (HMO) fortification

In a significant advancement for infant nutrition, the commercialization of HMO fortification is gaining momentum, with numerous companies obtaining regulatory nods for innovative HMO ingredients in 2024 and 2025. Arla, in collaboration with DSM-Firmenich, has fast-tracked the introduction of 2'-FL and LNnT oligosaccharides. Meanwhile, Kyowa Hakko Bio and Inbiose have broadened the range of HMO variants available to formula producers, as recognized by the FDA[1]Source: U.S. Food and Drug Administration, “Food Additive Petitions,” fda.gov. Backed by clinical evidence highlighting the advantages of HMO for immune development and gut health, premium formula brands are increasingly adopting HMO fortification, often at a notable price premium. However, the intricate nature of this technology poses challenges for smaller manufacturers, hinting at a potential market consolidation favoring established players with robust research and development and regulatory know-how. Looking ahead, 2025 is poised to witness a surge in FDA approvals for more HMO variants, paving the way for diverse formulations and a heightened competitive edge.

Plant-based and hybrid formulas

Companies like Else Nutrition and Danone are leading the charge in the evolving landscape of plant-based infant formulas. Else Nutrition has recently secured regulatory approvals for its pea protein-based formulations, while Danone is making strides by investing in hybrid technologies that blend plant and animal proteins. These plant-based formulas are not just a trend; they're addressing key consumer concerns, from environmental sustainability and allergen avoidance to ethical considerations in dairy production, as highlighted by the FDA. The FDA is also playing a pivotal role in shaping the future of these formulas, offering clearer guidance on nutritional equivalency and safety testing protocols. However, the segment faces challenges: higher production costs and the need for consumer education. Parents, understandably, seek assurances that these plant-based alternatives meet their infants' nutritional needs. As a response, hybrid formulations, which merge plant and animal proteins, are gaining traction, striking a balance between sustainability and familiar nutrition.

Restraints Impact Analysis of Baby Food Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Breast-feeding promotion and stringent marketing codes | -0.7% | Global, with strongest enforcement in Europe and WHO member states | Long term (≥ 4 years) |

| Declining birth rates in developed economies | -0.5% | Europe, North America, developed Asia-Pacific markets | Long term (≥ 4 years) |

| Stringent regulations and product safety concerns | -0.4% | Global, with tightest standards in United States and European Union | Medium term (2-4 years) |

| Reformulation costs from looming global sugar-reduction mandates | -0.3% | Global, with earliest implementation in Europe and select emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Breast-feeding promotion and stringent marketing codes

As WHO marketing codes tighten and national campaigns bolster breastfeeding, formula marketing faces mounting challenges. According to the WHO, its Member States are pushing for broader digital marketing regulations, especially targeting social media and influencers, key platforms for millennial parents[2]Source: World Health Organization, “Infant and Young Child Feeding,” who.int. Globally, the regulatory landscape is becoming more stringent, with advanced enforcement mechanisms and harsher penalties for violations. Strategies that engage healthcare professionals are under heightened scrutiny, curbing the traditional relationship-building tactics once favored by formula companies for market entry. In response, these companies are shifting towards educational content and indirect marketing, a move that's driving up customer acquisition costs and dampening conversion rates.

Declining birth rates in developed economies

Key developed markets are grappling with alarmingly low fertility rates: Germany stands at 1.35, the UK at 1.49, and projections from the OECD indicate a continued decline through 2030[3]Source: Organisation for Economic Co-operation and Development, “Fertility Rates,” oecd.org. This demographic trend imposes structural volume constraints that premiumization can't remedy, pushing companies to seek geographic diversification in emerging markets with higher fertility rates. The US Congressional Budget Office forecasts a slight dip in fertility rates from 1.62 to 1.60 births per woman by 2030. Meanwhile, New Zealand's rate has already settled at 1.52 births per woman, underscoring widespread demographic challenges in developed nations. China's baby food market, reeling from declining birth rates, saw a contraction of USD 4.8 billion, highlighting the swift impact of demographic changes on market dynamics. In response, companies are branching out into related areas, such as toddler nutrition and adult nutritional products, to counterbalance the waning demand for infant formula.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Baby Food Market Segment Analysis

By Product Type:

Formula Dominance Faces Convenience ChallengeIn 2025, milk formula commands a dominant 46.85% market share, solidifying its role as the go-to substitute for working mothers and a primary choice in supplemental feeding. Meanwhile, prepared baby food is on a rapid ascent, projected to grow at a 6.17% CAGR through 2031. This surge underscores a notable shift towards convenience, catering to the fast-paced lifestyles of today's parents. Innovations in packaging and technologies extending shelf life are propelling ready-to-feed baby food, allowing parents to opt for on-the-go consumption without any prep. Dried baby food remains in steady demand, especially in emerging markets with limited refrigeration, thanks to its cost-effectiveness and storage benefits.

As infants typically transition from a milk-centric diet to complementary foods around the 6-month mark, the product type segmentation mirrors these changing feeding patterns. Recent launches highlight a wave of innovation: Amara rolled out organic smoothie melts, while Sprout Foods debuted plant-based protein purees in January 2025. Additionally, other categories are gaining momentum. Products like Inspired Start's 8-allergen system, designed for allergen introduction, and specialized therapeutic formulas are resonating with health-conscious parents keen on proactive nutrition. This shift towards functional nutrition underscores a broader trend: prepared foods are increasingly seen as tools for delivering specific health benefits, moving beyond mere sustenance.

By Category:

Organic Surge Challenges Conventional LeadershipIn 2025, conventional baby food products command a dominant 64.05% market share, leveraging established distribution networks, competitive pricing, and widespread acceptance across various economic segments. Meanwhile, the organic segment, though smaller, is surging ahead with a robust 7.36% CAGR, underscoring a shift in consumer preferences towards cleaner and safer nutrition. This pronounced growth in the organic sector indicates a pivotal change in parental priorities, with organic offerings gaining traction as a hallmark for premium brand differentiation and an avenue for capturing greater market share.

Organic certification not only sets high standards but also acts as a gatekeeper, creating barriers to entry and allowing for substantial price premiums. Typically, organic products command a price that's 30-50% higher than their conventional counterparts. The organic sector's growth is bolstered by a more accessible supply of organic ingredients and a maturing supply chain, which have alleviated some of the cost challenges that once hindered organic adoption. In Spain, companies like Smileat are centering their entire business models around a 100% organic ethos. At the same time, established brands are broadening their organic product lines, eager to seize the burgeoning opportunities. Globally, as regulatory frameworks for organic agriculture and certification processes move towards standardization, they pave the way for organic-centric brands to expand internationally.

By Product Format:

Powder Dominance Meets Ready-to-Feed MomentumIn 2025, the powder format commands a dominant 71.68% market share, thanks to its cost-effectiveness, extended shelf life, and efficient storage. These advantages resonate with both manufacturers and consumers. This format is especially favored in price-sensitive markets and bulk purchases, where the convenience of reconstitution is a plus. Meanwhile, the ready-to-feed format is on a growth spree, boasting a 5.75% CAGR. This surge is largely attributed to urban lifestyles and the preferences of working parents who seek immediate consumption without the hassle of preparation.

Liquid concentrate finds itself in a balanced spot, offering some convenience benefits while still being more cost-effective than ready-to-feed options. The segmentation of formats underscores a broader consumer dilemma: balancing convenience, cost, and storage. Each format caters to unique use cases and consumer demographics. However, packaging innovations are challenging these traditional boundaries. Companies are rolling out hybrid solutions, such as concentrated pouches and single-serve powder packets, merging convenience with cost-effectiveness. A case in point is Sprout Foods, which, in 2025, unveiled clear pouches, showcasing how packaging can set a brand apart in a crowded market.

By Age Group:

Early Infancy Dominates While Toddler Segment AcceleratesIn 2025, the 0-6 months age group commands a dominant 45.25% market share, underscoring the pivotal role of early infant nutrition and the heightened feeding demands of this stage. This segment's lead is consistent with exclusive feeding practices, which typically transition to complementary foods around the 6-month mark. Meanwhile, the 24-36 months segment is witnessing the swiftest growth, boasting a 6.35% CAGR, signaling a burgeoning interest in toddler nutrition as firms broaden their offerings beyond conventional infant products.

Distinct nutritional profiles, textures, and packaging formats tailored to developmental stages naturally segment the market. The 6-12 months and 12-24 months brackets serve as pivotal transition phases, marked by increasing feeding complexities and a notable expansion in product variety. Recent innovations highlight this age-specific focus: Hiya's launch of Kids Daily Greens targets children aged 2, and several firms are rolling out graduated texture progressions. This segmentation underscores a heightened awareness of the rapidly evolving nutritional needs and feeding skills in early childhood, paving the way for specialized product innovations.

By Distribution Channel:

Traditional Retail Leads While E-commerce SurgesIn 2025, supermarkets and hypermarkets command a dominant 36.20% market share, capitalizing on their extensive reach, competitive pricing, and the allure of one-stop shopping, especially for busy parents. Meanwhile, online retail is surging ahead with a robust 6.58% CAGR, underscoring the swift digital embrace by millennial parents and the undeniable perks of subscription-based deliveries. This trend is especially evident in urban areas, where parents, pressed for time, increasingly favor doorstep deliveries and the ease of automated reordering.

Drugstores and pharmacies carve out a notable market presence, skillfully using endorsements from healthcare professionals. They position baby food not merely as commodities but as health-centric purchases. Convenience stores cater to urgent needs and last-minute buys. Other distribution avenues encompass specialty baby stores and direct-to-consumer platforms. This evolution in channels mirrors the overarching trend of retail digitization. For instance, Indian company Rorosaur is pioneering direct-to-consumer models, sidestepping traditional retail markups. The e-commerce boom is bolstered by advancements in cold-chain logistics and the rising adoption of subscription models, ensuring steady revenue for manufacturers.

Geography Analysis

APAC Baby Food Market

In 2025, the Asia-Pacific region commands a dominant 44.40% market share and boasts the highest growth rate at 6.82% CAGR through 2031. This growth is fueled by demographic advantages and a burgeoning middle class with increasing purchasing power. While China's market remains pivotal despite declining birth rates, India and Indonesia are on an upswing, driven by rising disposable incomes and urbanization. The Bureau of Labor Statistics highlights that as female workforce participation rates rise, reaching 37% in India for the 2022-23 period, demand for convenient feeding solutions increases. Rapidly evolving regulatory frameworks are seeing China's FSMP registration system greenlight 206 products, and India's FSSAI aligning sugar content norms with global health standards. The competitive arena heats up as local entities, such as Feihe International and Yili Group, vie for dominance against global giants.

North America Baby Food Market

North America stands as a mature market, leaning into premiumization and organic product adoption over sheer volume growth. With fertility rates projected by the US Congressional Budget Office to decline from 1.62 to 1.60 births per woman by 2030, according to OECD data, the region faces structural volume constraints. Yet, buoyed by high disposable incomes and a health-centric consumer base, there's a pronounced tilt towards premium product positioning, unlocking margin expansion avenues. The FDA's January 2025 tightening of infant formula safety regulations reshapes the competitive landscape, with compliance costs likely benefiting larger manufacturers boasting established quality systems. North American firms, leading in HMO fortification and plant-based formulations, are setting the pace in global product development.

Europe Baby Food Market

Europe grapples with moderate growth, hampered by some of the globe's lowest fertility rates, Germany at 1.35 and the UK at 1.49, as per OECD. Yet, the region shines in organic product leadership and stringent quality standards, securing a premium global stance. Companies like Smileat champion 100% organic models, and regulatory frameworks bolstering sustainable agriculture offer a leg up to eco-conscious brands. Europe's focus on sustainability and clean-label products is reshaping global product trends, with its standards often becoming international benchmarks. However, navigating the complexities of Brexit-related trade shifts and diverse national regulations within the EU demands adept regulatory navigation skills for market access strategies.

Regulatory Landscape

Infant and young-child nutrition is governed by stringent product composition, manufacturing, and marketing controls, with the United States and European Union setting many global compliance baselines. In the United States, the FDA regulates infant formula under 21 CFR Part 106 and Part 107, including a requirement for manufacturers to submit a new infant formula notification at least 90 days before introducing it into interstate commerce (21 CFR 106.120). The FDA has also expanded its regulatory toolkit through guidance updates, including May 2026 guidance documents on evaluation of infant formula response, which reinforce expectations around quality systems and incident readiness.

In Europe, baby food for infants and young children is governed under the EU framework for foods for specific groups, including Regulation (EU) No 609/2013 and related delegated acts that define compositional and labeling requirements. Commission Delegated Regulation (EU) 2026/743 amended protein-related requirements for infant and follow-on formula manufactured from protein hydrolysates, raising the bar for documentation and technical substantiation for specialty protein sources. In China, the State Administration for Market Regulation (SAMR) maintains a registration-led approach for infant formula, and amendments to the Administrative Measures for Product Formula Registration of Formula Milk Powder for Infants and Young Children (Order 80), effective December 1, 2025, broadened the framework to include liquid infant formula, extending dossier and approval expectations beyond powder formats.

Competitive Landscape

In the baby food market, established multinationals like Nestlé, Danone, and Abbott wield significant advantages through their expansive global distribution and robust research and development. However, these giants are increasingly challenged by nimble startups, which are rolling out unique formulations and adopting direct-to-consumer strategies. A notable trend is the push towards premiumization, with firms pouring resources into organic certifications, HMO fortifications, and positioning in functional nutrition, all to command higher prices and safeguard their market presence.

Regulatory shifts are reshaping the competitive landscape. For instance, the FDA's tightening safety protocol set for January 2025 may benefit larger manufacturers with their established compliance systems, while posing challenges for smaller entities. Moreover, technology is emerging as a pivotal differentiator, with firms harnessing digital marketing, subscription services, and tailored nutrition platforms to forge closer ties with consumers. There are untapped opportunities in areas like plant-based products, allergen-introduction items, and regional flavor preferences that global players might miss.

Disruptors such as Else Nutrition, championing pea protein formulas, and Begin Health, focusing on probiotics, are redefining traditional approaches and carving out fresh market niches. The industry's innovation trajectory underscores a deepening understanding of nutritional science. For instance, companies like Arla and DSM-Firmenich are pioneering HMO commercialization, opening doors to new differentiations recognized by the FDA. Furthermore, heightened patent activity around innovative ingredients and processing methods signals a fierce competitive landscape, as firms vie for an edge through exclusive formulations.

Baby Food Industry Leaders

Nestlé SA

Danone SA

Reckitt Benckiser Group PLC

Abbott Laboratories

Feihe International Inc.

- *Disclaimer: Major Players sorted in no particular order

Baby Food Market Companies Covered in this Report

- Nestlé SA

- Danone SA

- Reckitt Benckiser

- Abbott Laboratories

- Feihe International

- Royal FrieslandCampina

- Junlebao Dairy

- Ausnutria Dairy

- Yili Group

- HiPP GmbH

- Perrigo Company

- Bellamy's Organic

- Hero Group

- Arla Foods

- Bubs Australia

- Beingmate Co.

- Bobbie Baby Inc.

- Hain Celestial Group

- Kendal Nutricare

- Meiji Company

Market Opportunities and Future Outlook

Compliance-led reformulation and transparency programs are creating room for brands that can industrialize testing and disclosure while keeping premium positioning. In the United States, state-level heavy metal requirements have shifted from voluntary actions into mandated routines, including Virginia's Baby Food Protection Act (HB 1844) taking effect in January 2026, with monthly testing and public disclosure for baby food sold in the state. This patchwork also increases opportunities for ISO 17025-accredited testing partnerships, QR-code or web-based disclosure workflows, and ingredient-sourcing strategies aligned with FDA efforts such as Closer to Zero, particularly for prepared baby food where contamination scrutiny and parent trust can influence purchase decisions.

Investment and partnering activity also shows where manufacturers are placing bets across supply chains, capacity, and differentiated nutrition. Nestle's July 2026 Thai government approval for a 23 billion baht smart factory and distribution center points to continued modernization of production and logistics nodes in Asia, while the June 2026 Nestle and Helaina partnership to integrate bioactive protein technology into global infant nutrition highlights a route to premium differentiation beyond conventional fortification. On capacity and specialization, Danone's May 2026 expansion plans for an Advanced Medical Nutrition facility at Macroom, Ireland, and Mead Johnson's Zeeland, Michigan expansion approvals in 2026 indicate that manufacturers are adding or upgrading regulated production footprints that can support tighter quality requirements and a wider set of product formats, including ready-to-feed and medical or specialized nutrition adjacencies.

Recent Industry Developments in Baby Food Market

- July 2026: Nestle received Thai government approval for a 23 billion baht investment in a smart factory and distribution center. The project strengthens regional manufacturing and distribution capability in a high-growth geography and supports tighter quality control and responsiveness across infant nutrition supply chains.

- January 2025: The US Food and Drug Administration released final guidance on action levels for lead in processed foods intended for babies and young children. The guidance accelerated industry alignment around testing, supplier qualification, and reformulation priorities, particularly for prepared baby food where contaminant management is central to brand trust.

- August 2024: Abbott expanded its Pure Bliss line of infant formulas to include European-made and organic products, including an organic liquid formula positioned for US retail. The move broadened premium and convenience-oriented offerings and increased competitive pressure in ready-to-feed and organic-led segments.

Baby Food Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the baby food market covers packaged foods and beverages made specifically for infants and toddlers, and sold through retail and pharmacy channels. The scope includes prepared meals, purees, cereals, snacks, and infant formula. Values are tracked in USD across major regions.

Scope exclusions: This sizing does not count breastfeeding services, vitamins or medicines sold as supplements, and feeding accessories such as bottles, nipples, and warmers.

Segments Covered in This Report

- By Product Type

- Milk Formula

- Ready to Feed Baby Food

- Dried Baby Food

- Other Product Type

- By Category

- Organic

- Conventional

- By Product Format

- Powder

- Liquid Concentrate

- Ready-to-Feed

- By Age Group

- 0–6 Months

- 6–12 Months

- 12–24 Months

- 24–36 Months

- By Distribution Channel

- Supermarkets/Hypermarkets

- Drugstores/Pharmacies

- Convenience Stores

- Online Retail Stores

- Other Distribution Channel

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

- Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the initial demand and supply picture and to keep assumptions grounded in publicly visible signals. We typically start with population and birth indicators by country, then connect them to infant and toddler food consumption patterns and retail channel shifts.

For baby food, useful public references include UN demographic datasets, World Bank indicators, USDA and other national agriculture and food statistics portals, and WHO and UNICEF nutrition publications. We also use customs trade statistics portals to track import and export movements for relevant food categories. In parallel, we review company annual reports, investor presentations, trusted press coverage, and product and regulation updates from food safety authorities. Select paid subscriptions are used only to speed up company financial checks, patent screening, and shipment or trade lookups where available. These desk sources are not exhaustive, and many other references were also used for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test the desk assumptions, especially on pricing, channel margins, and category mix changes (for example, the split between formula, cereals, purees, and snacks). We spoke with a mix of manufacturers, ingredient and packaging participants, distributors and retailers, and domain experts across APAC, EMEA, and the Americas to reflect on-ground realities beyond published averages.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 15% | APAC: 53% |

| Mid tier: 55% | Functional/Unit leaders: 29% | EMEA: 29% |

| Smaller Players: 15% | Managers: 56% | Americas: 18% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where births, infant and toddler population bands, and age-appropriate feeding adoption are translated into a consumption pool. That pool is then converted to value using observed price tiers by category and channel. The model is corroborated with selective bottom-up approximations, such as roll-ups of sampled supplier revenues and channel checks on shelf pricing. For a few high-visibility categories, volume is multiplied by average selling price, which helps us adjust for gaps.

Key inputs that shape the numbers include live births and cohort size (0 to 6 months through 24 to 36 months), urbanization and working-parent share as a proxy for convenience demand, mix shift between milk formula and ready-to-eat formats, organic versus conventional penetration, and pricing progression by pack type and retail channel. When country data is thin, we use proxy markets with similar income and feeding patterns, then normalize the results back to observable trade and retail signals.

For forecasting, scenario analysis is used so the outlook can reflect different birth-rate paths, premiumization speed, and the tightness of safety or labeling regulation. These scenarios are reviewed with experts, and a base case is selected when the assumed volume and price movements align with what is being seen in the market.

Data Validation & Update Cycle

Outputs are checked through triangulation against independent signals, including demographic totals, import and export movements for relevant baby food categories, and retailer channel expansion patterns. Variance checks are run at country and regional levels, and any sharp jumps are reviewed to confirm they come from a real driver such as price inflation, mix shift, or a channel change.

Before sign-off, the work goes through multi-step analyst review so assumptions, calculations, and conversions remain consistent across segments and geographies. When meaningful mismatches show up, we re-contact interviewees or schedule follow-up calls to identify the driver. Reports are refreshed annually, with interim updates when major events occur, followed by a final pre-delivery pass so clients receive the latest view.

Mordor Intelligence's Baby Food Market Sizing Compared With Other Published Estimates

Published baby food market values often differ because each study chooses its own product list, age coverage, and pricing point in the value chain, and those choices can move the total by several billions. Differences also show up when a publisher uses a different base year or converts currencies using different timing and inflation treatment.

Some external totals expand the basket by counting adjacent toddler beverages and a wider snack definition, and they may apply faster price-growth assumptions across all categories. In the Mordor Intelligence build, baby food is counted as packaged infant and toddler foods sold through defined retail and pharmacy channels. The value build is constrained by age-cohort demand signals and channel-level price checks, so the total does not drift beyond what consumption and trade patterns support.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 74.57 B (2026) | |

| Global Consultancy A | USD 74.33 B (2024) | Uses a different base year and may include a wider set of baby and toddler snack and beverage items. As a result, its value pool is anchored to an earlier pricing mix and a broader basket. |

| Industry Publisher B | USD 85.80 B (2025) | Applies a higher implied value per child by leaning into premiumization and formula weight. Its category mapping can pull in more snack and drink spend under baby food than a strict age and channel-defined build. |

The spread in the table is mainly explained by year choice and what gets counted in the basket, followed by how price and mix are projected. By keeping the steps tied to visible cohort, category, and channel inputs, the estimate stays traceable and repeatable when assumptions are updated.

Key Questions Answered in the Report

How big is the baby food market in 2026 and how fast is it growing?

The market stands at USD 74.57 billion in 2026 and is on track for a 3.93% CAGR through 2031.

Which product segment generates the most revenue?

Milk formula leads with 46.85% baby food market share in 2025, reflecting its role as the primary breast-milk substitute.

Which region will contribute most to future growth?

Asia Pacific combines a 44.40% revenue share with the highest 6.82% CAGR, thanks to large infant populations and rising incomes.

What are the main growth drivers for manufacturers?

Rising female workforce participation, premiumization, HMO fortification, and growing acceptance of plant-based formulas underpin demand.

How is e-commerce influencing distribution?

Online retail is expanding at a 6.58% CAGR as subscription delivery models and improved cold-chain logistics gain parent trust.

Page last updated on: