Vitamin K2 Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

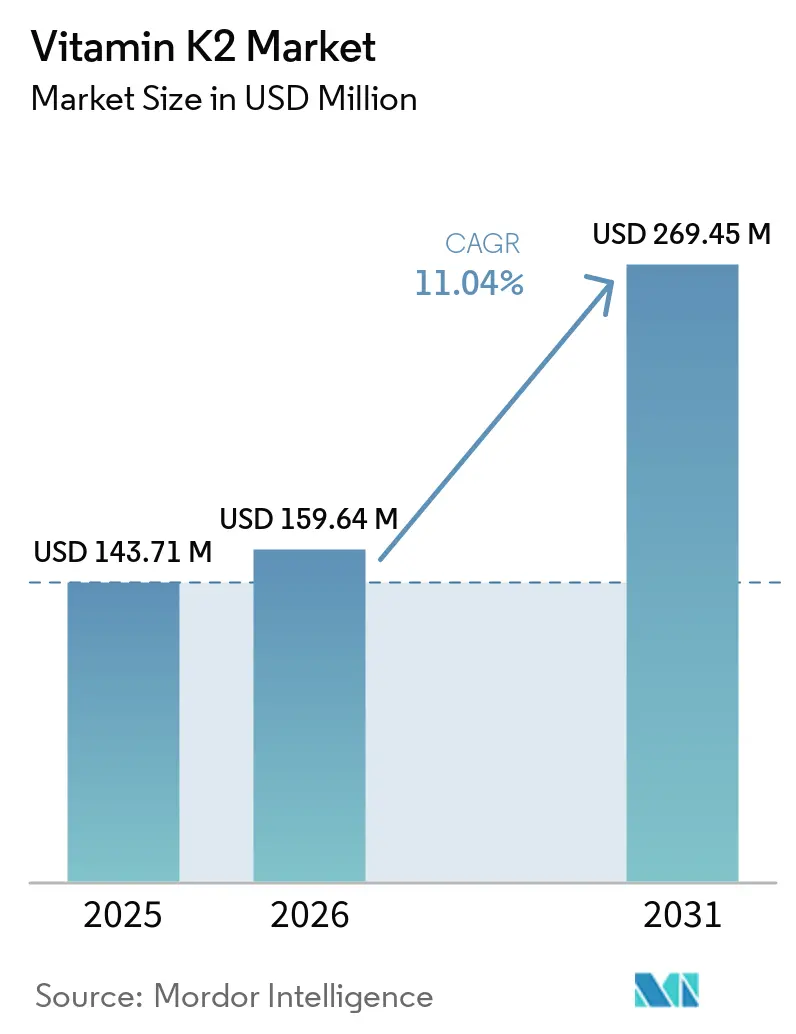

| Market Size (2026) | USD 159.64 Million |

| Market Size (2031) | USD 269.45 Million |

| Growth Rate (2026 - 2031) | 11.04% CAGR |

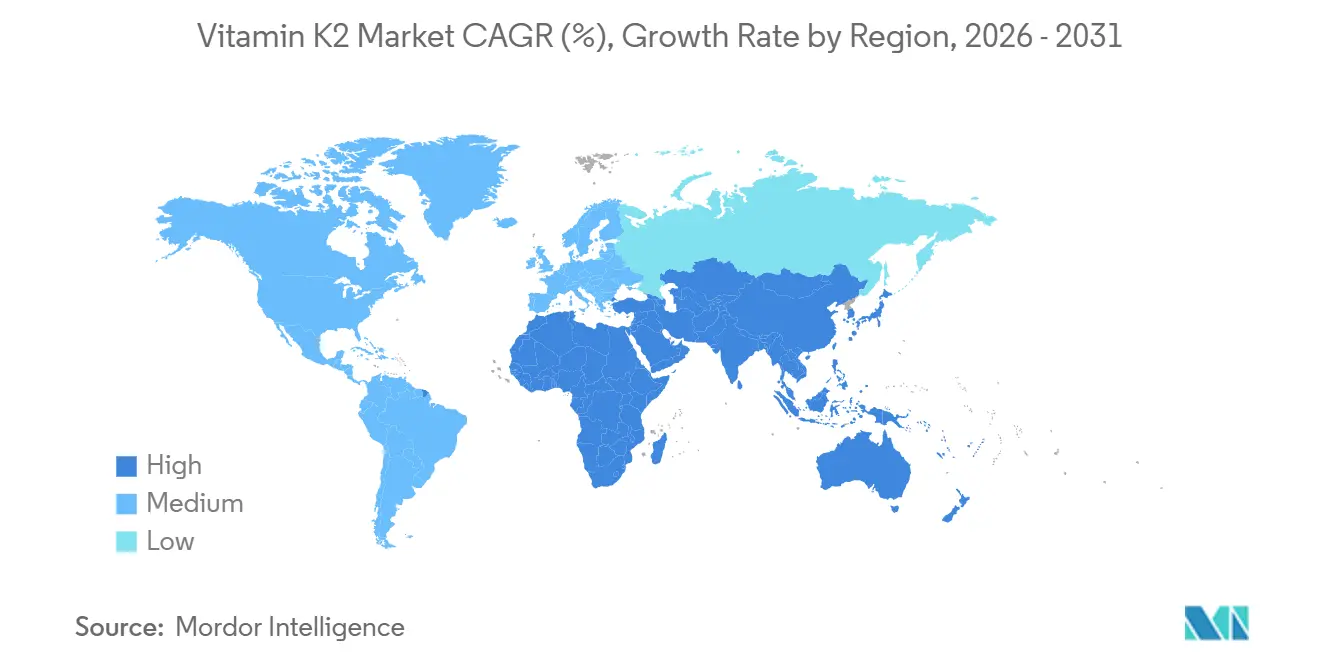

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vitamin K2 Market Analysis by Mordor Intelligence

The vitamin k2 market size is expected to grow from USD 143.71 million in 2025 to USD 159.64 million in 2026 and is forecast to reach USD 269.45 million by 2031 at 11.04% CAGR over 2026-2031. Clinical evidence highlighting benefits for cardiovascular and bone health, along with greater ingredient availability and improved product stability, drives the shift of preventive nutrition from a niche segment to mainstream acceptance. Quality plays a pivotal role in the market. Third-party audits reveal that only 29% of tested supplements meet their label claims, creating opportunities for manufacturers that prioritize quality. The MK-7 form dominates the market in finished products due to its prolonged plasma half-life. Innovations in micro- and nano-encapsulation technologies enable product development in previously challenging formats, such as beverages, gummies, and dairy. North America leads the market, supported by established regulatory frameworks and high consumer awareness. Meanwhile, the Asia-Pacific region experiences rapid growth, driven by rising disposable incomes and government-backed initiatives promoting healthy aging.

Key Report Takeaways

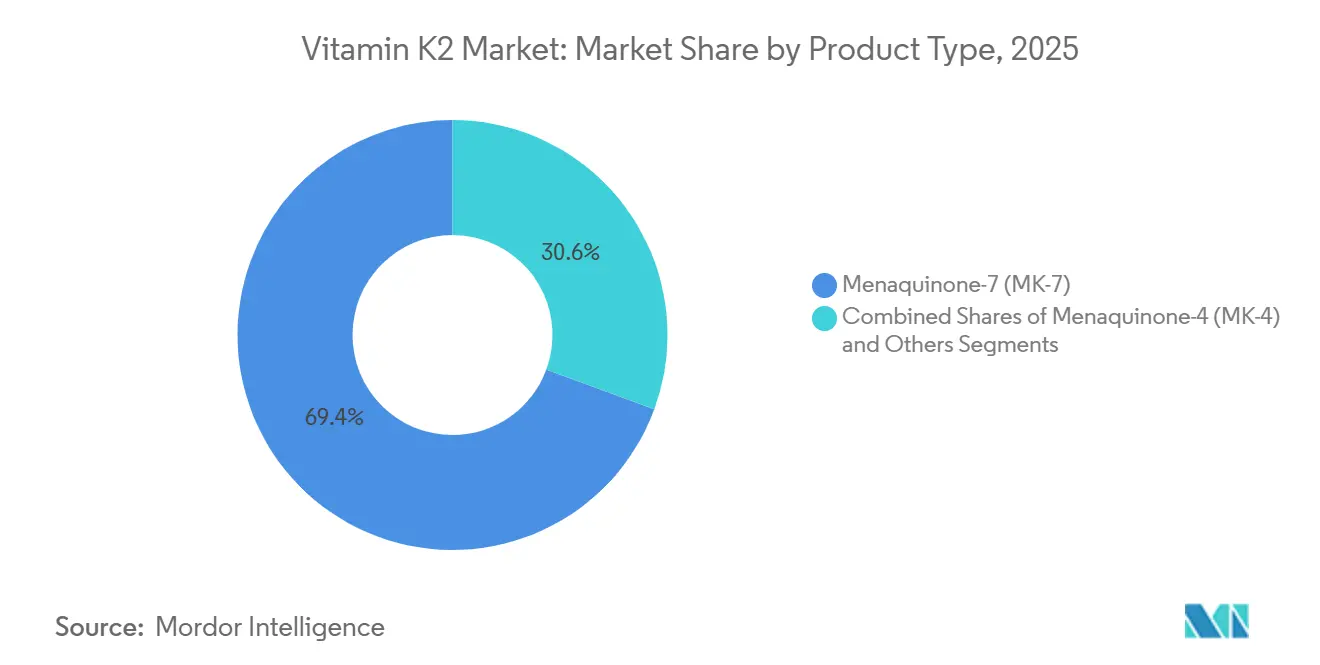

- By product type, menaquinone-7 captured 69.38% of the vitamin K2 market share in 2025 and is advancing at a 12.06% CAGR through 2031.

- By source, natural ingredients held 67.28% of 2025 revenue, while synthetic is expanding at 12.96% as pharmaceutical buyers prize batch consistency.

- By form, powders commanded 54.71% of 2025 demand; oil-based systems are the fastest-growing format at 12.92% CAGR to 2031.

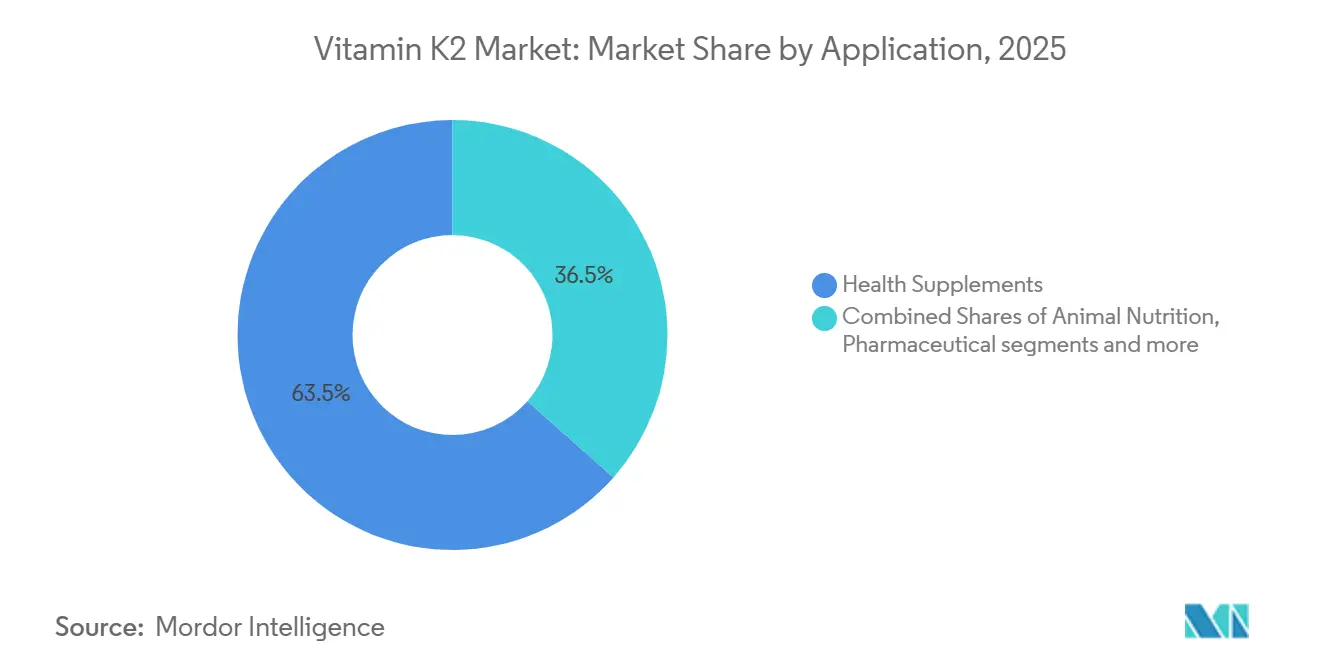

- By application, health supplements led with 63.48% revenue in 2025, whereas functional food and beverage fortification is set to grow at 13.08% through 2031.

- By region, North America retained 35.25% of 2025 value, while Asia-Pacific is projected to deliver the quickest expansion at 12.27% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Vitamin K2 Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer awareness of bone and cardiovascular health benefits | +2.5% | Global, with early concentration in North America and Western Europe | Medium term (2-4 years) |

| Increasing prevalence of osteoporosis and cardiovascular diseases | +2.0% | Global, acute in aging populations across North America, Europe, and East Asia | Long term (≥ 4 years) |

| Growing aging population driving preventive healthcare demand | +1.8% | Global, most pronounced in Japan, Germany, Italy, and emerging in China | Long term (≥ 4 years) |

| Expansion of dietary supplements and nutraceutical consumption | +1.5% | Global, led by North America and Asia-Pacific urban centers | Medium term (2-4 years) |

| Surging demand for functional foods and fortified products | +1.3% | North America, Europe, with spillover to Asia-Pacific middle class | Short term (≤ 2 years) |

| Accelerating focus on women's health and calcium metabolism support | +1.2% | Global, particularly North America and Europe targeting postmenopausal demographics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising consumer awareness of bone and cardiovascular health benefits

Rising consumer awareness regarding bone and cardiovascular health is significantly supporting the growth trajectory of the vitamin K2 market. Increasing public health campaigns and clinical evidence highlighting the role of vitamin K2 in calcium regulation, bone mineralization, and prevention of arterial calcification are influencing purchasing behavior across key demographics. According to World Heart Federation, the European Union introduced Council Conclusions in 2024 to strengthen cardiovascular health strategies for its population of approximately 440 million, reflecting heightened institutional focus on cardiovascular disease (CVD) as the leading cause of mortality globally[1]Source: World Heart Federation, “European Union takes action for the cardiovascular health of its 440 million people”, world-heart-federation.org. Within the EU, CVD affects over 60 million individuals and results in more than 1.7 million deaths annually, underscoring the scale of the health burden. This growing awareness, coupled with increasing emphasis on preventive healthcare, is encouraging consumers to adopt nutritional supplements that support heart and bone health. Additionally, aging populations and rising incidences of osteoporosis and cardiovascular conditions are further reinforcing demand. The shift toward proactive health management and functional nutrition is particularly evident in developed regions such as Europe.

Growing aging population driving preventive healthcare demand

The rapid expansion of the aging population is playing a crucial role in shaping demand for preventive healthcare solutions, thereby supporting the growth of the vitamin K2 market. Older adults are more susceptible to conditions such as osteoporosis, arterial calcification, and cardiovascular diseases, which has increased the focus on early intervention through nutrition and supplementation. According to World Health Organization, population ageing is accelerating significantly, with one in six people expected to be over the age of 60 by 2030, and the global elderly population projected to reach 2.1 billion by 2050[2]Source: World Health Organization, “Ageing and Health”, who.int. This demographic shift is prompting greater awareness around maintaining bone density and cardiovascular health in later life. Vitamin K2, known for its role in directing calcium to bones while preventing its accumulation in arteries, is increasingly being incorporated into daily health regimens. Furthermore, healthcare systems are encouraging preventive approaches to reduce long-term treatment costs associated with chronic diseases. The growing inclination toward healthy ageing and longevity is also driving demand for functional supplements among middle-aged and elderly consumers

Expansion of dietary supplements and nutraceutical consumption

The expanding consumption of dietary supplements and nutraceuticals is substantially contributing to the growth of the vitamin K2 market. Increasing health consciousness, coupled with a shift toward preventive healthcare, has led consumers to actively incorporate supplements into their daily routines for long-term wellness. Vitamin K2 is gaining prominence within this space due to its scientifically supported benefits in bone health and cardiovascular function. The rising popularity of functional nutrition, particularly among urban and aging populations, is further accelerating demand for targeted micronutrients. Additionally, the proliferation of e-commerce platforms and direct-to-consumer brands has improved accessibility and product awareness across global markets. Manufacturers are also innovating with combination formulations, such as vitamin D3 and K2 blends, to enhance efficacy and appeal. Regulatory support and growing clinical validation are strengthening consumer confidence in nutraceutical products.

Surging demand for functional foods and fortified products

The increasing demand for functional foods and fortified products is playing a significant role in accelerating the adoption of vitamin K2 across global markets. Consumers are actively seeking food and beverage options that offer added health benefits beyond basic nutrition, particularly those supporting bone strength and cardiovascular health. Vitamin K2 is being increasingly incorporated into dairy products, plant-based alternatives, nutritional beverages, and fortified snacks to enhance their functional value. This trend is strongly driven by busy lifestyles, where consumers prefer convenient, health-enhancing food solutions over traditional supplementation alone. Food manufacturers are responding by developing innovative fortified products that align with clean-label and wellness-oriented preferences. Additionally, growing awareness of micronutrient deficiencies is encouraging the inclusion of vitamins such as K2 in everyday food consumption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited consumer awareness compared to mainstream vitamins | -0.8% | Global, most acute in emerging markets and rural areas | Short term (≤ 2 years) |

| Regulatory inconsistencies across regions | -0.6% | Global, particularly fragmented in Asia-Pacific and South America | Medium term (2-4 years) |

| Price volatility of raw materials | -0.5% | Global, affecting fermentation feedstock costs | Short term (≤ 2 years) |

| Limited standardization in dosage and health claims | -0.4% | Global, hindering clinical validation and formulary inclusion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited consumer awareness compared to mainstream vitamins

Limited consumer awareness compared to mainstream vitamins continues to restrict the widespread adoption of vitamin K2 across global markets. While vitamins such as Vitamin D and Vitamin C are widely recognized and routinely consumed, vitamin K2 remains relatively underrepresented in consumer knowledge and marketing visibility. Many individuals are still unfamiliar with its specific role in calcium regulation, bone mineralization, and cardiovascular health, which limits its inclusion in daily supplementation routines. This knowledge gap is further compounded by limited promotional efforts and fewer large-scale public health campaigns focused on vitamin K2. Additionally, healthcare professionals may prioritize more established nutrients, reducing recommendations for K2 unless in specific clinical contexts. The lack of clear differentiation between Vitamin K1 and K2 also contributes to confusion among consumers. As a result, demand growth is somewhat constrained despite increasing scientific evidence supporting its benefits.

Regulatory inconsistencies across regions

Regulatory inconsistencies across regions continue to pose a significant challenge to the growth and standardization of the vitamin K2 market. Variations in classification, approval processes, and permissible health claims create complexities for manufacturers operating across multiple geographies. In 2024, the European Food Safety Authority reaffirmed that no tolerable upper intake level has been established for vitamin K, reflecting a relatively permissive regulatory stance in Europe[3]Source: European Food Safety Authority, “Regulations”, efsa.europa.eu. This contrasts with Japan, where high-dose MK-4 is regulated under pharmaceutical frameworks, imposing stricter controls on formulation and distribution. Similarly, China maintains an evolving nutraceutical registration system that requires domestic clinical trials for novel ingredients, adding time and cost burdens for market entry. These divergent regulatory approaches complicate product development, labeling, and cross-border commercialization strategies. Companies must invest in region-specific compliance, which can limit scalability and delay product launches. Furthermore, inconsistent guidelines may create uncertainty among consumers and healthcare professionals regarding safety and efficacy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: MK-7 Dominance Driven by Pharmacokinetic Superiority

Menaquinone-7 (MK-7) held a 69.38% share of the market in 2025, with projections indicating a robust growth rate of 12.06% CAGR extending through 2030. MK-7's market supremacy was largely attributed to its superior bioavailability and prolonged half-life when juxtaposed with other vitamin K2 variants. Unlike Menaquinone-4 (MK-4), which boasted a mere 1-2 hour half-life, MK-7's active presence in the body spanned up to 72 hours. This extended duration facilitated more effective activation of vitamin K-dependent proteins, which played a critical role in various physiological processes, including bone health and cardiovascular function.

Ongoing clinical research underscored MK-7's prowess in cardiovascular applications, with findings showcasing significant enhancements in arterial flexibility and a decrease in coronary artery calcification. These benefits were particularly relevant in addressing age-related cardiovascular issues, making MK-7 a key ingredient in products targeting aging populations. Meanwhile, in the pharmaceutical realm, Menaquinone-4 (MK-4) retained its prominence, especially in Japan. Here, MK-4 garnered regulatory nods for osteoporosis treatment, prescribed at a daily dose of 45 mg. This approval highlighted MK-4's therapeutic potential in bone health management, particularly in clinical settings. However, due to MK-4's abbreviated half-life, its penetration into the consumer supplement arena remained limited.

By Source: Natural Preference Meets Synthetic Scalability

Natural ingredients dominated the Vitamin K2 market in 2025, accounting for 67.28% of total revenue, driven by strong consumer preference for naturally derived compounds in supplements and functional products. These ingredients are favored for their perceived health benefits, safety profile, and alignment with clean-label and wellness trends. Natural Vitamin K2 is widely incorporated in dietary supplements, fortified foods, and beverages, supporting bone and cardiovascular health. Manufacturers also emphasize traceability, sustainable sourcing, and minimal processing to meet consumer expectations and regulatory standards. The segment benefits from strong brand recognition, established supply chains, and extensive clinical research supporting efficacy.

In contrast, the synthetic Vitamin K2 segment is projected to be the fastest-growing source, expanding at a CAGR of 12.96% over the forecast period. Synthetic formulations are particularly valued by pharmaceutical buyers and large-scale supplement manufacturers for their batch-to-batch consistency, stability, and predictable potency. This reliability makes synthetic Vitamin K2 ideal for precise dosing in therapeutic applications and mass production. Technological advancements in synthesis processes and quality control are further enhancing the segment’s appeal. Additionally, synthetic sources can be produced at scale more efficiently, reducing supply chain constraints and mitigating fluctuations in natural raw material availability.

By Form: Powder Stability Meets Oil Innovation

Powdered Vitamin K2 held the largest share of the market in 2025, accounting for 54.71% of total demand, owing to its versatility, stability, and ease of integration across dietary supplements, fortified foods, and beverages. The powder format allows manufacturers to create capsules, tablets, protein blends, and dry mixes with precise dosing and extended shelf life. Consumers favor powders for their convenience, neutral taste, and compatibility with a variety of consumption methods. Additionally, established supply chains and widespread availability in both retail and e-commerce channels support strong market penetration. Innovation in flavored powders, combination formulations, and functional blends has further reinforced its leading position.

In contrast, oil-based Vitamin K2 systems are projected to be the fastest-growing segment, with a CAGR of 12.92% through 2031. Oil-based formulations are valued for their enhanced bioavailability, allowing improved absorption and effectiveness, which appeals to both consumers and healthcare professionals. These systems are increasingly used in softgel capsules, liquid supplements, and functional oils, offering convenience and precision in dosing. Rising awareness of the importance of bioavailability in nutraceuticals is driving the adoption of oil-based formats. Manufacturers are also innovating with combination products, flavor masking, and premium delivery systems to expand their offerings.

By Application: Supplements Lead, Functional Foods Accelerate

Health supplements dominated the Vitamin K2 market in 2025, accounting for 63.48% of total revenue, driven by widespread consumer demand for targeted bone, cardiovascular, and overall wellness support. These supplements are widely available in capsules, tablets, powders, and softgel formats, offering convenience, precise dosing, and long shelf life. Consumers increasingly rely on health supplements to address nutrient deficiencies and support preventive healthcare, particularly in aging populations and health-conscious adults. The segment benefits from strong brand presence, extensive retail distribution, and online availability, making it easily accessible across regions. Additionally, clinical research and scientific validation of Vitamin K2’s role in bone and heart health have reinforced consumer confidence in supplement-based solutions.

In contrast, functional food and beverage fortification is projected to be the fastest-growing application, expanding at a CAGR of 13.08% through 2031. Increasing consumer interest in convenient, on-the-go nutrition and fortified products is driving the adoption of Vitamin K2 in functional foods, beverages, and dairy products. Manufacturers are incorporating Vitamin K2 into protein bars, fortified drinks, yogurts, and ready-to-consume formulations to meet demand for daily nutrient intake without relying solely on capsules or tablets. The trend is particularly pronounced among younger, urban populations seeking health benefits through everyday foods and beverages.

Geography Analysis

North America held the largest share of the Vitamin K2 market in 2025, accounting for 35.25% of total revenue, driven by strong consumer awareness of bone and cardiovascular health, as well as established supplement consumption habits. The region benefits from high disposable income, well-developed retail and e-commerce channels, and a robust presence of leading global brands. Health-conscious consumers increasingly seek clinically validated supplements, and Vitamin K2 is widely incorporated into capsules, softgels, powders, and combination formulations with vitamins D and calcium. Extensive marketing, scientific research, and regulatory support for nutraceuticals have further strengthened the region’s market position. Additionally, aging populations in the U.S. and Canada are driving sustained demand for joint, bone, and heart health supplements.

In contrast, Asia-Pacific is expected to be the fastest-growing region, with a projected CAGR of 12.27% through 2031. Rising disposable incomes, urbanization, and growing health awareness are fueling demand for Vitamin K2 supplements and fortified foods in countries such as China, Japan, South Korea, and India. Younger populations are increasingly seeking preventive healthcare solutions and functional foods, boosting the popularity of collagen, vitamins, and mineral-fortified products. Expansion of modern retail, online platforms, and innovative product launches are improving accessibility across urban and semi-urban markets.

Other regions, including Europe, South America, and the Middle East and Africa, are also contributing to market growth, albeit at a more moderate pace. Europe demonstrates steady demand due to high consumer awareness of health and wellness supplements, as well as regulatory support for nutraceutical products. South America is gradually expanding, with countries such as Brazil and Argentina seeing increased adoption of functional foods and supplements. The Middle East & Africa market is emerging, driven by rising disposable income, urbanization, and growing interest in preventive healthcare.

Competitive Landscape

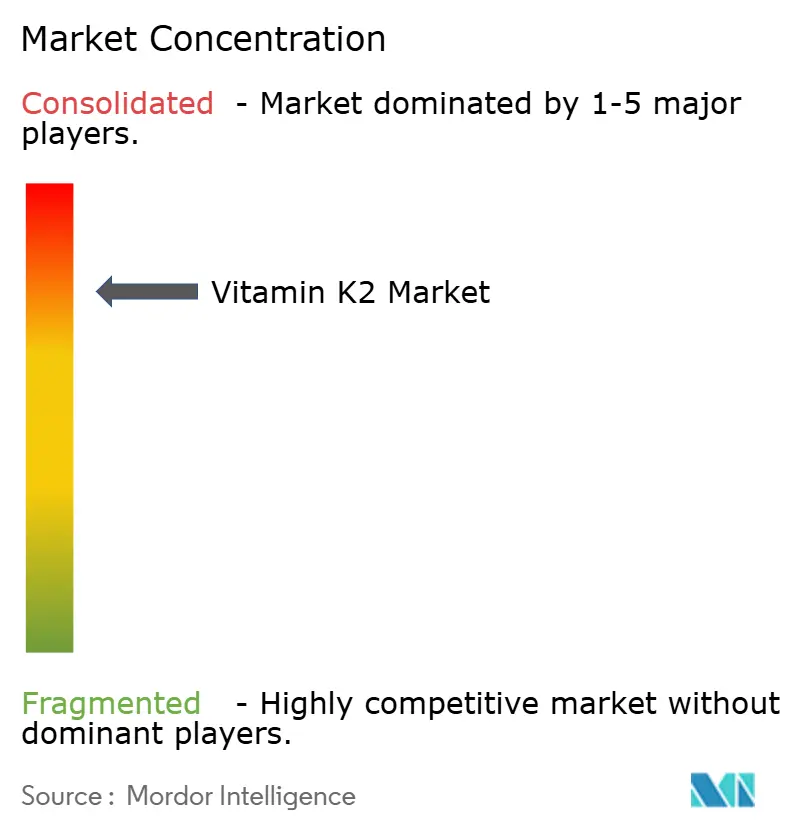

The vitamin K2 market is highly concentrated, with established companies maintaining strong positions through investments in manufacturing, research, and regulatory compliance. These companies have built their market presence through years of dedicated focus on specialized fermentation technologies, comprehensive clinical validation processes, and adherence to complex regulatory frameworks. Their financial capabilities and established infrastructure create significant barriers for new market entrants.

Major players in the vitamin K2 market actively pursue strategies focused on vertical integration and technological innovation. By managing both manufacturing processes and application development across the supply chain, they ensure consistent quality control and drive innovation. These companies have implemented advanced stabilization techniques, such as microencapsulation and nano-encapsulation, to enhance the functionality and value of their products. This approach has allowed them to expand their offerings into high-growth segments, including functional foods and animal nutrition, meeting the evolving demands of these markets.

The market offers significant opportunities in developing regions where consumer awareness about vitamin K2 remains low and in emerging applications like cognitive health and athletic performance. Ongoing clinical research continues to validate new use cases for vitamin K2 supplementation, further supporting these opportunities. Industry leaders, including Gnosis by Lesaffre and NattoPharma, actively strengthen their market positions by leveraging patent-protected processes and maintaining consistent investments in research. These efforts are particularly crucial as they face growing competition from synthetic alternatives entering the market.

Vitamin K2 Industry Leaders

Gnosis by Lesaffre

Balchem Corp.

BASF SE

DSM-Firmenich AG

Kyowa Hakko U.S.A., Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: AstaReal AB launched a new vegan Vitamin D3+K2 dietary supplement under its “by Astaxin” range, strengthening its presence in the plant-based nutraceutical segment. The supplement combines lichen-derived vitamin D3, a sustainable alternative to animal-based lanolin, with clinically supported MenaQ7 vitamin K2 to support bone health, muscle function, and immune performance.

- February 2026: Gnosis by Lesaffre launched MenaQ7 Olive Oil, a vitamin K2 formulation, specifically designed for functional beverages, gummies, and salad dressings. By leveraging olive oil as a carrier, the product enhanced bioavailability and enabled the fortification of everyday foods, expanding beyond traditional supplement formats.

- July 2025: Gnosis by Lesaffre's MenaQ7, a clinically validated vitamin K2 (MK-7) ingredient derived from plant-based precision fermentation, demonstrates effectiveness in supporting bone and heart health.

- February 2025: FC Bayern Women have entered into a new partnership with Balchem The partnership is set to run for several years and will focus specifically on the patented vitamin K2 brand K2VITAL.

Global Vitamin K2 Market Report Scope

Vitamin K2 refers to a group of fat-soluble vitamins known as menaquinones that play a critical role in calcium metabolism and overall bone and cardiovascular health. The vitamin k2 market is segmented by product type, source, form, application and geography. By product type, the market is segmented into menaquinone-7, menaquinone-4, and others. By source, the market is segmented into natural and synthetic. By form, the market is segmented into powder and oil. Based on application, the market is segmented into functional food and beverage, health supplements, animal nutrition, pharmaceutical and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. For each segment, the market sizing and forecasting have been done in value terms (USD million).

| Menaquinone-7 (MK-7) |

| Menaquinone-4 (MK-4) |

| Others |

| Natural |

| Synthetic |

| Powder |

| Oil |

| Functional Food and Beverage |

| Health Supplements |

| Animal Nutrition |

| Pharmaceutical |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Product Type | Menaquinone-7 (MK-7) | |

| Menaquinone-4 (MK-4) | ||

| Others | ||

| By Source | Natural | |

| Synthetic | ||

| By Form | Powder | |

| Oil | ||

| By Application | Functional Food and Beverage | |

| Health Supplements | ||

| Animal Nutrition | ||

| Pharmaceutical | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the vitamin K2 market by 2031?

It is forecast to reach USD 269.45 million by 2031, reflecting an 11.04% CAGR from 2026.

Which product type leads current sales?

Menaquinone-7 dominates, holding 69.38% of 2025 revenue and growing at 12.06% through 2031.

Why is Asia-Pacific the fastest-growing region?

Post-2024 regulatory reforms in China, expanding capacity among certified fermenters and rising aging populations drive a 12.27% CAGR to 2031.

Which delivery format is gaining share fastest?

Oil-based MK-7 suspensions are advancing at 12.92% CAGR due to superior bioavailability and versatility in gummies and beverages.

How has regulation improved market prospects in the U.S.?

The FDA’s GRAS GRN 887 and CRN’s 375 µg safety ceiling eliminate uncertainty, enabling brands to launch higher-dose MK-7 products quickly.

Page last updated on: