Vitamin And Mineral Premixes Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 8.04 Billion |

| Market Size (2030) | USD 11.02 Billion |

| Growth Rate (2025 - 2030) | 6.51% CAGR |

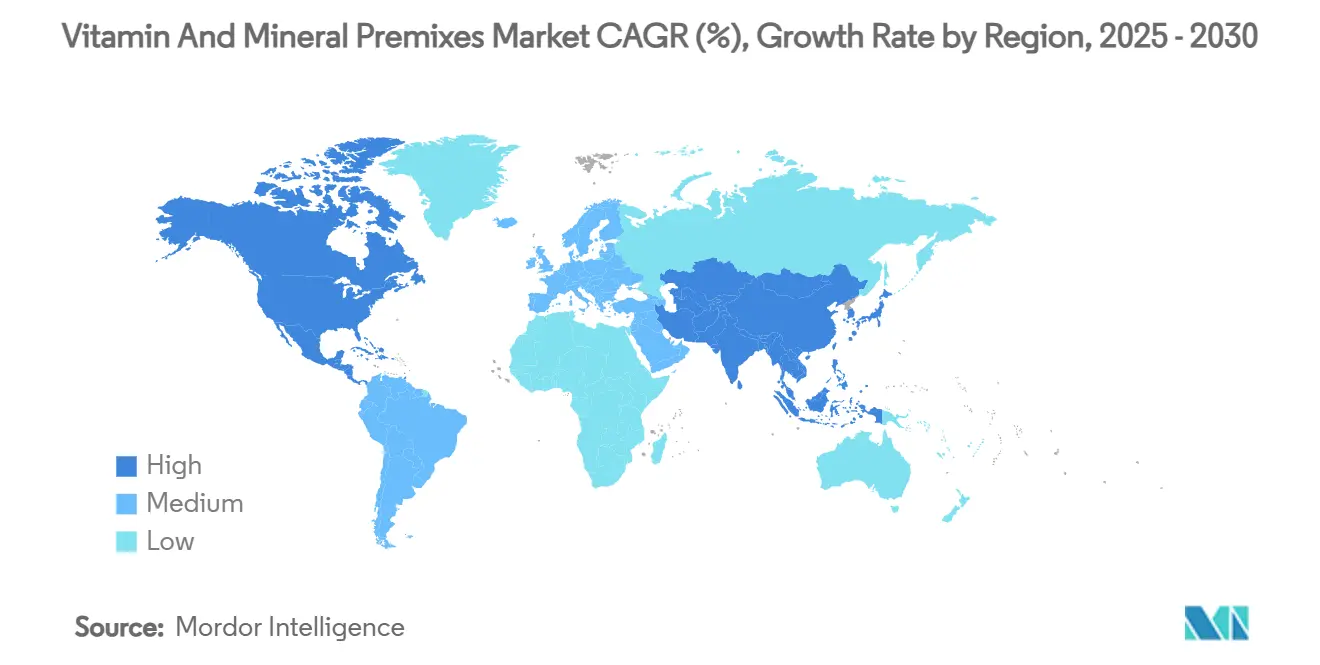

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

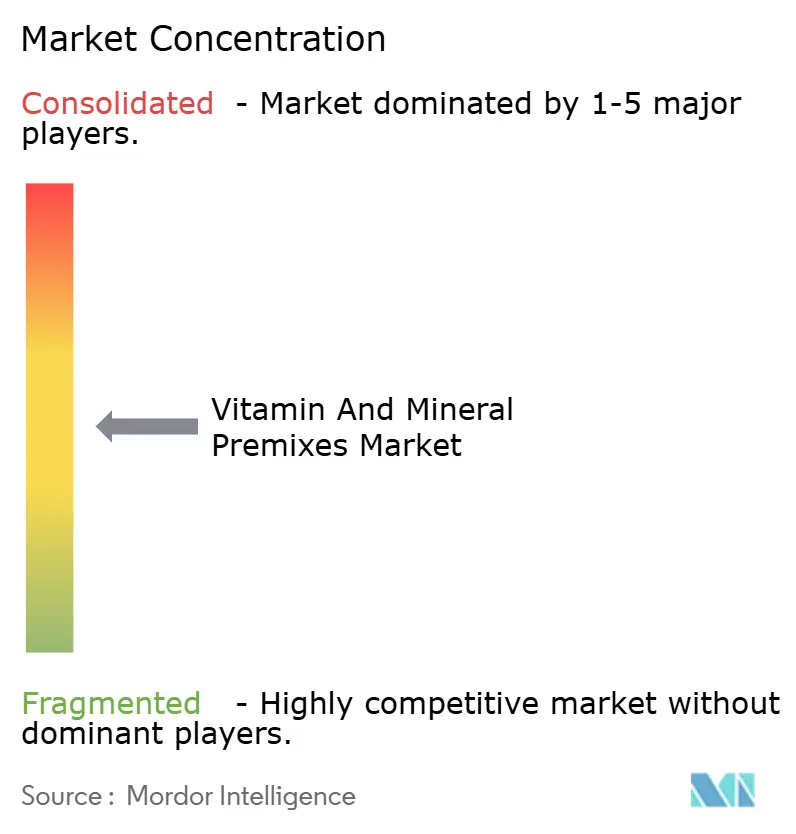

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Vitamin And Mineral Premixes Market Analysis by Mordor Intelligence

The Vitamin And Mineral Premixes Market size is estimated at USD 8.04 billion in 2025, and is expected to reach USD 11.02 billion by 2030, at a CAGR of 6.51% during the forecast period (2025-2030). This growth trajectory reflects the market's evolution from a commodity-driven sector to a strategic enabler of global nutrition security, particularly as governments worldwide implement mandatory fortification programs to address micronutrient deficiencies affecting over 5 billion people globally[1]Source: World Health Organization, "Micronutrients Database", platform.who.int. Asia-Pacific dominates the market, driven by rapid industrialization of animal agriculture and expanding food fortification programs across China, India, and Southeast Asia. Government nutrition policies covering more than 80 countries, coupled with breakthroughs in bioavailability technology, reinforce steady volume growth. Supply-chain shocks—such as the 2024 BASF vitamin A and E outage—underscore the importance of diversification strategies that favor regionally integrated production bases. The sector’s shift from single nutrients to synergistic blends accelerates consolidation, while the organic sub-segment captures a growing premium customer base in early-life and personalized applications.

Key Report Takeaways

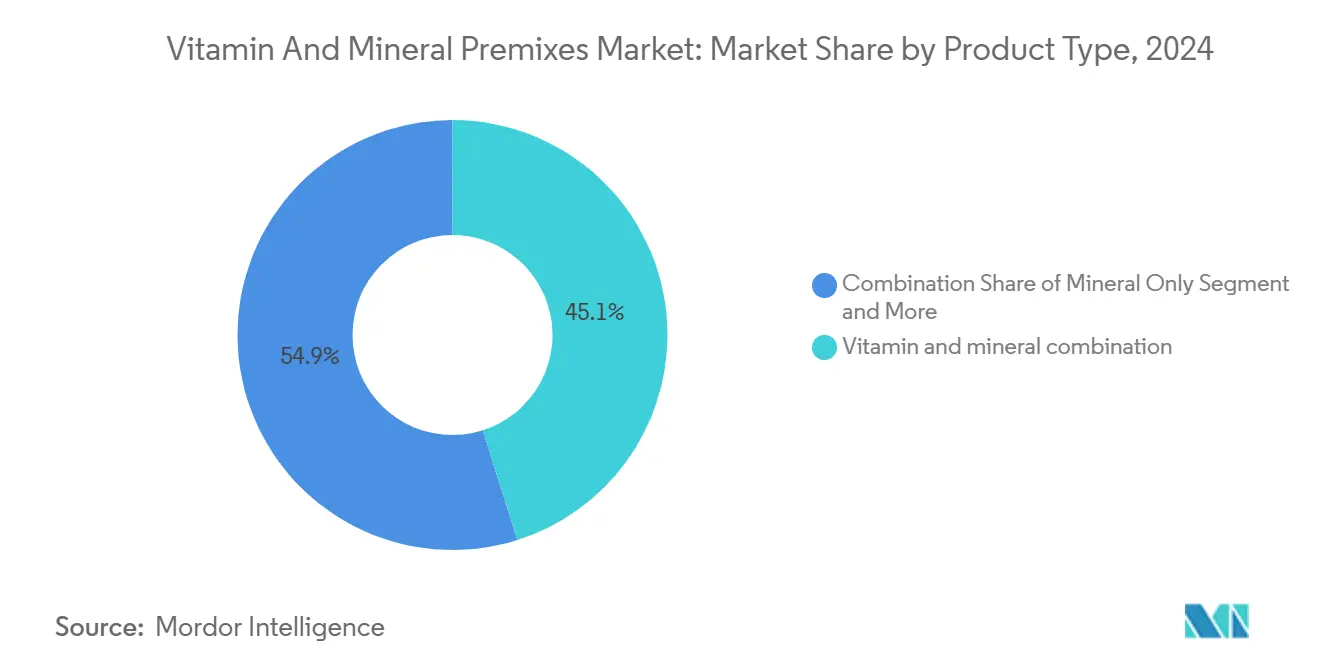

- By product type, vitamin and mineral combinations accounted for 45.11% of the vitamin and mineral premix market share in 2024 and will expand at 7.23% CAGR through 2030.

- By form, powder forms held 75.21% revenue share in 2024, whereas liquid formats are set to post the fastest 7.17% CAGR to 2030.

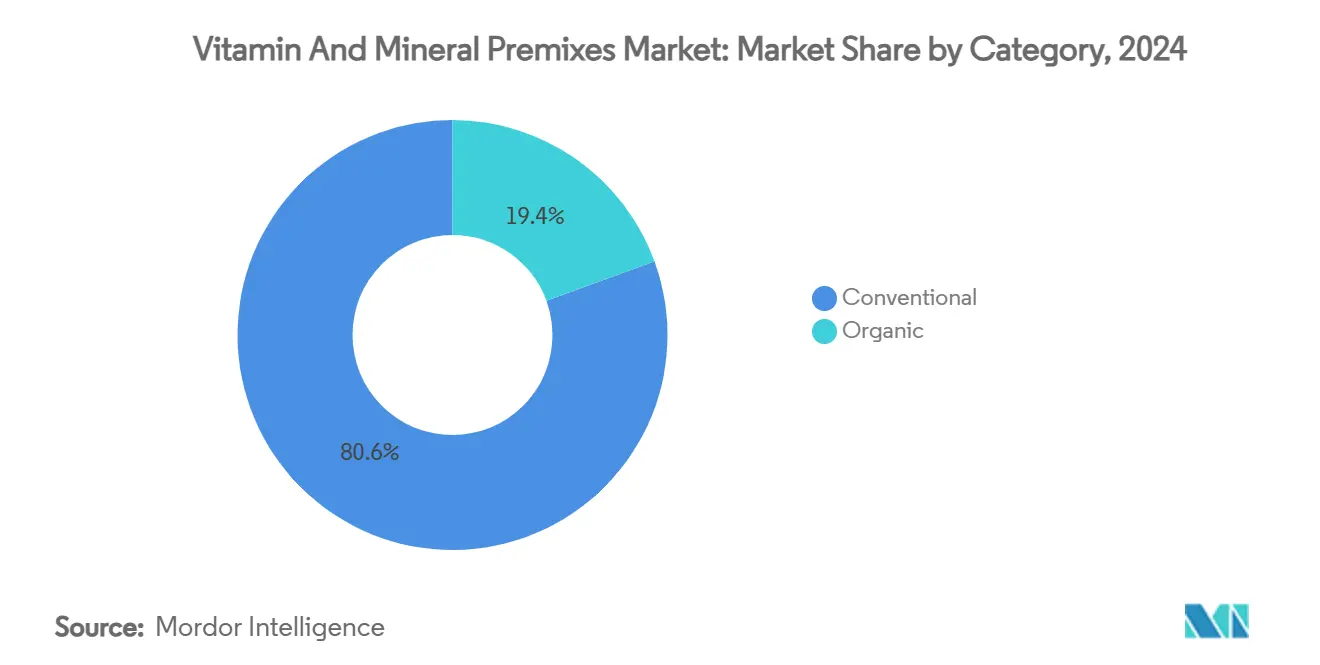

- By category, conventional premixes led with 80.57% share in 2024; organic variants are projected to grow at an 8.32% CAGR through 2030.

- By application, animal food and feed commanded 41.26% share in 2024, while infant nutrition will be the fastest-advancing application at 7.07% CAGR by 2030.

- By geography, Asia-Pacific dominated with 41.24% share in 2024 and is forecast to sustain the quickest 6.78% CAGR to 2030.

Market Trends and Insights

Drivers Impact Analysis of Vitamin And Mineral Premixes Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Animal Nutrition Segment | +1.8% | Global, with Asia-Pacific and Latin America leading | Medium term (2-4 years) |

| Growth of Fortified Foods and Beverages | +1.5% | Global, strongest in LMIC regions | Long term (≥ 4 years) |

| Clean Label and Natural Ingredient Movement | +1.2% | North America & European Union primarily | Short term (≤ 2 years) |

| Government and Public Health Fortification Programs | +1.0% | Global, with Sub-Saharan Africa and South Asia priority | Long term (≥ 4 years) |

| Advancements in Formulation Technology | +0.8% | Global, R&D centers in developed markets | Medium term (2-4 years) |

| Micronutrient Deficiency Prevalence | +0.7% | Global, highest impact in LMIC regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Animal Nutrition Segment

The animal nutrition segment's expansion reflects structural shifts in global protein consumption patterns and regulatory mandates for livestock health optimization. Animal feed applications represent 41.26% of the premix market, with growth accelerating through intensive farming practices that demand precise nutritional supplementation to maximize feed conversion ratios and minimize environmental impact. The segment benefits from technological innovations such as Dispersible Liquid Concentrates that enhance fat-soluble vitamin bioavailability by up to 30% compared to traditional dry formulations. Regulatory frameworks increasingly mandate trace mineral supplementation to prevent deficiency-related diseases, with the EU's upcoming deforestation regulation creating additional compliance requirements that favor standardized premix solutions. The segment's growth trajectory aligns with rising global meat consumption, particularly in Asia-Pacific markets where per capita protein intake continues expanding. Recent capacity expansions, including dsm-firmenich's 100,000-ton annual facility in Brazil in October 2024, demonstrate industry confidence in sustained demand growth.

Growth of Fortified Foods and Beverages

Mandatory fortification programs represent the most significant long-term driver for premix demand, with 93 countries implementing wheat flour fortification legislation and the World Food Programme distributing over 1.4 million metric tons of fortified foods annually [2]Source: World Food Programme, "Food Fortification", wfp.org. The economic rationale for fortification remains compelling, with every USD 1 invested yielding USD 27 in economic returns through improved health and productivity outcomes [3]Source: OECD (Organization for Economic Co-operation and Development), "Regulatory governance of large-scale food fortification", oecd.org. Large-scale food fortification programs can reduce zinc deficiency prevalence by up to 50% globally, with 82 low- and middle-income countries having mandatory standards, though only 33 currently include zinc. The Global Alliance for Improved Nutrition's USD 300 million investment since 2002 has reached 1.3 billion people with fortified foods, demonstrating the scalability of premix-enabled interventions. Innovation in fortification technology, including dsm-firmenich's new dry vitamin A formulation with over 90% retention after six months, addresses stability challenges that have historically limited fortification effectiveness.

Clean Label and Natural Ingredient Movement

Consumer demand for transparency and natural ingredients is reshaping premix formulations, with clean label claims driving premium pricing and market differentiation opportunities. The movement extends beyond simple ingredient lists to encompass sustainability credentials, with dsm-firmenich's EcoVadis Platinum certification exemplifying industry responses to environmental scrutiny. Organic premix segments command 8.32% CAGR growth compared to 6.51% for the overall market, reflecting willingness to pay premiums for certified natural ingredients. Technological innovations enable clean label compliance without compromising functionality, including leguminous protein encapsulation systems that replace synthetic carriers while improving bioavailability. The trend creates competitive advantages for companies investing in natural extraction and processing technologies, though regulatory complexity increases as clean label definitions vary across jurisdictions. Personalized nutrition trends further amplify clean label importance, with custom premix solutions allowing brands to target specific consumer segments while maintaining ingredient transparency.

Government and Public Health Fortification Programs

Regulatory mandates for fortification create sustained demand growth independent of economic cycles, with government programs targeting micronutrient deficiencies that affect 30.7% of women aged 15-49 globally according to the World Health Organization. The WHO's Vitamin and Mineral Nutrition Information System provides surveillance infrastructure that enables evidence-based fortification policies, with 40 indicators across 17 micronutrients guiding intervention strategies. India's large-scale fortification initiatives demonstrate program scalability, with government integration of fortified staples into social safety net programs reaching vulnerable populations. The Philippines' January 2025 guidelines for vitamin and mineral classification in dietary supplements illustrate ongoing regulatory evolution that creates new market opportunities while requiring compliance investments. Fortification programs increasingly emphasize biofortification and conventional fortification integration, with research demonstrating synergistic effects when combined with breastfeeding initiatives.

Restraints Impact Analysis of Vitamin And Mineral Premixes Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Allergen and Cross-Contamination Risks | -0.9% | Global, stricter in European Union and North America | Short term (≤ 2 years) |

| Ingredient Sourcing Challenges | -1.2% | Global, acute in supply-dependent regions | Medium term (2-4 years) |

| High R&D (Research and Development) Costs | -0.7% | Developed markets primarily | Long term (≥ 4 years) |

| Complex Regulatory Landscape | -0.8% | Global, varying by jurisdiction | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Allergen and Cross-Contamination Risks

Manufacturing complexities in premix production create significant contamination risks that require substantial quality control investments and can trigger costly product recalls. The French study on chemical risks in premix manufacturing identified over 3,000 workers potentially exposed to hazardous additives, with average inhalable dust exposure at 7.45 mg/m³. Vitamin A stability challenges during pet food manufacturing demonstrate broader industry issues, with losses of 26% during pre-conditioning and 8% during extrusion stages requiring overfortification strategies that increase costs. The Association of American Feed Control Officials' updated model regulations for pet food introduce new labeling requirements that increase compliance complexity while addressing allergen concerns. Cross-contamination risks are particularly acute in facilities processing multiple product types, requiring dedicated production lines and extensive cleaning protocols that reduce operational efficiency and increase capital requirements.

Ingredient Sourcing Challenges

Supply chain concentration creates systemic vulnerabilities, with 75% of nutritional ingredients sourced from China amid rising geopolitical tensions and environmental regulations that increase production costs. The American Feed Industry Association's call for domestic vitamin production investment reflects strategic concerns about supply security, particularly as trade tensions escalate. Recent supply disruptions, including the BASF fire that affected vitamin A and E production, demonstrate how single-point failures can create market-wide shortages and price volatility. Tariff implications add cost pressures, with proposed 25% tariffs on Canadian and Mexican goods and 10% on Chinese products potentially increasing raw material costs significantly. Alternative sourcing strategies require substantial lead times and quality validation, with countries like India, Brazil, and parts of Africa emerging as potential alternatives despite infrastructure and regulatory challenges.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Vitamin And Mineral Premixes Market Segment Analysis

By Product Type:

Combinations Drive Comprehensive NutritionVitamin and mineral combinations command 45.11% market share in 2024 and lead growth with 7.23% CAGR through 2030, reflecting industry consolidation toward comprehensive nutritional solutions that simplify manufacturing and regulatory compliance. The preference for combination products stems from synergistic nutrient interactions and cost efficiencies in premix production, with manufacturers able to achieve better economies of scale through standardized formulations . Single vitamin products face margin pressure as commodity pricing dynamics intensify, while mineral-only formulations serve specialized applications in aquaculture and ruminant nutrition where targeted supplementation addresses specific deficiency patterns.

Innovation in combination formulations focuses on bioavailability enhancement and stability optimization, with dsm-firmenich's ROVIMIX product line demonstrating superior performance through advanced coating technologies that minimize nutrient degradation during storage and processing. The segment benefits from regulatory preferences for standardized premix compositions that reduce quality control complexity and enable consistent nutritional outcomes across diverse manufacturing environments. Emerging applications in personalized nutrition create opportunities for customized combination products, though regulatory frameworks lag behind technological capabilities in most jurisdictions.

By Form:

Powder Dominance Challenged by Liquid InnovationPowder formulations maintain 75.21% market share in 2024, leveraging cost advantages and handling convenience that align with established manufacturing infrastructure across feed mills and food processors. However, liquid formulations achieve 7.17% CAGR growth through 2030, driven by superior bioavailability and processing advantages in specific applications. Dispersible Liquid Concentrates represent the most significant innovation in liquid formulations, offering enhanced stability for fat-soluble vitamins while enabling uniform distribution in liquid feeding systems.

Microencapsulation technologies bridge the gap between powder and liquid advantages, with companies like Lubrizol developing LIPOFER microcapsules that improve iron delivery while addressing taste and gastric irritation concerns. Advanced formulation techniques, including liposome production for vitamin C delivery, achieve over 80% encapsulation efficiency while enabling controlled release in gastrointestinal environments. The form selection increasingly depends on end-application requirements, with aquaculture and pet food sectors driving liquid adoption while traditional livestock applications maintain powder preferences due to cost considerations and existing infrastructure investments.

By Category:

Organic Growth Outpaces Conventional BaseConventional premixes dominate with 80.57% market share in 2024, reflecting established supply chains and cost advantages that align with price-sensitive applications in animal nutrition and basic food fortification. However, organic premixes achieve 8.32% CAGR growth through 2030, commanding premium pricing that justifies higher production costs and certification requirement. The organic segment benefits from clean label trends and consumer willingness to pay premiums for certified natural ingredients, particularly in infant nutrition and dietary supplement applications where quality perceptions drive purchasing decisions.

Regulatory complexity in organic certification creates barriers to entry while protecting established players with comprehensive certification portfolios. The segment requires dedicated supply chains and processing facilities to maintain organic integrity, with cross-contamination risks necessitating substantial quality control investments[4]Source: Canadian Food Inspection Agency, "Hazard Identification", umass.edu. Innovation opportunities exist in organic-compliant extraction and processing technologies, with leguminous protein encapsulation systems offering sustainable alternatives to synthetic carriers while maintaining functional performance. The category's growth trajectory aligns with broader sustainability trends, though scalability challenges limit market penetration in price-sensitive segments.

By Application:

Animal Feed Leadership Meets Infant Nutrition InnovationAnimal food and feed applications command 41.26% market share in 2024, leveraging established distribution networks and regulatory frameworks that facilitate large-volume transactions with predictable demand patterns. The segment benefits from intensive farming practices that require precise nutritional supplementation to optimize feed conversion ratios and minimize environmental impact. Food and beverage fortification represents the second-largest application, driven by mandatory fortification programs that create sustained demand independent of economic cycles.

Infant nutrition emerges as the fastest-growing application with 7.07% CAGR through 2030, reflecting innovation in clean-label formulations and enhanced bioavailability technologies that address the critical nutritional needs of the first 1,000 days of life. The segment commands premium pricing due to stringent quality requirements and regulatory oversight, with manufacturers investing in specialized facilities and quality systems to serve this demanding market. Other applications, including pharmaceuticals and cosmetics, benefit from crossover technologies developed for primary segments, though regulatory complexity limits growth potential in these specialized markets.

Geography Analysis

APAC Vitamin And Mineral Premixes Market

Asia-Pacific dominates the vitamin and mineral premix market with 41.24% share in 2024 and leads regional growth at 6.78% CAGR through 2030, driven by rapid industrialization of animal agriculture and expanding food fortification programs across China, India, and Southeast Asia. China's regulatory framework requires comprehensive registration processes for feed additives, with the General Administration of Customs and Ministry of Agriculture and Rural Affairs overseeing import licensing that creates barriers to entry while protecting domestic producers. India's large-scale fortification initiatives demonstrate the region's commitment to addressing micronutrient deficiencies, with government integration of fortified staples into social safety net programs creating sustained demand growth.

North America and Europe Vitamin And Mineral Premixes Market

North America and Europe represent mature markets with established regulatory frameworks and premium pricing structures that favor innovation and quality differentiation over volume growth. The FDA's new Animal Food Ingredient Consultation process, following the expiration of the AAFCO memorandum of understanding, creates regulatory uncertainty while potentially extending ingredient approval timelines from current 3-5 years. European markets benefit from stringent quality standards that create competitive advantages for established players while limiting low-cost competition, though Brexit-related regulatory divergence adds complexity for multinational operations.

LATAM and MEA Vitamin And Mineral Premixes Market

Latin America and Middle East & Africa emerge as high-growth regions driven by expanding livestock sectors and government fortification mandates that address widespread micronutrient deficiencies. Brazil's animal nutrition market growth of 2.6% annually attracts significant investment, with ADM's new Paraná facility increasing production capacity by 40% to serve regional demand. Sub-Saharan Africa faces the highest burden of micronutrient deficiencies globally, with Central Sub-Saharan Africa showing the most severe vitamin A and iodine deficiency rates, creating substantial opportunities for fortification programs supported by international development organizations.

Competitive Landscape

The vitamin and mineral premix market exhibits moderate concentration, reflecting a competitive landscape where established multinationals compete alongside specialized regional players and emerging technology-focused companies. Some of the prominent players include Archer Daniels Midland (ADM), Prinova Group LLC, Corbion, SternVitamin GmbH & Co. KG, and DSM-Firmenich, among others. Market leaders leverage vertical integration strategies that span raw material production through finished premix manufacturing, with dsm-firmenich's separation of its Animal Nutrition & Health business exemplifying strategic focus on core competencies while reducing exposure to vitamin price volatility.

The competitive intensity increases as supply chain disruptions create opportunities for agile players to gain market share through superior service levels and supply reliability. Technology differentiation emerges as a key competitive factor, with companies investing in advanced formulation technologies including microencapsulation, nanotechnology, and bioavailability enhancement systems that command premium pricing. Patent portfolios provide competitive moats, as demonstrated by dsm-firmenich's favorable judgment in patent infringement cases regarding 25-hydroxyvitamin D3 feed applications.

Strategic acquisitions reshape competitive dynamics, with Nutreco's completion of the Micronutrients acquisition and Barentz's planned acquisition of China's Fengli Group demonstrating consolidation trends that enhance geographic reach and technical capabilities. Opportunities exist in specialized applications including personalized nutrition, organic formulations, and emerging markets where regulatory frameworks favor innovative approaches over established commodity strategies.

Vitamin And Mineral Premixes Industry Leaders

-

Archer Daniels Midland (ADM)

-

Prinova Group LLC

-

Corbion

-

SternVitamin GmbH & Co. KG

-

DSM-Firmenich

- *Disclaimer: Major Players sorted in no particular order

Vitamin And Mineral Premixes Market Companies Covered in this Report

- DSM-Firmenich

- Prinova Group LLC

- Archer Daniels Midland (ADM)

- Corbion NV

- SternVitamin GmbH & Co. KG

- Glanbia Nutritionals

- Cargill Inc

- Camlin Fine Sciences Limited (Vitafor)

- Vitablend Nederland B.V.

- Farbest Brands

- Hexagon Nutrition

- VDS Premix

- Adisseo

- Watson Inc.

- AdvaCare Pharma

- Biovin Ingredients

- INCOLTEC

- Biovencer Group of Companies

- Trouw Nutrition

- NATURAL, s.r.o.

Recent Industry Developments in Vitamin And Mineral Premixes Market

- September 2024: DSM-Firmenich inaugurated a new animal nutrition and health premix and additives manufacturing plant in Sadat City, Egypt. This facility marked the company's 50th production site worldwide. The opening of the new plant in Sadat City allowed the company to meet the rising demand for feed premixes, in terms of quantity, quality and reliability, in Egypt and in export markets.

- March 2023: The Danish premix company Vilomix (owned by Danish Agro, Agravis and Vestjyllands Andel) closed an agreement to acquire 75% of the Brazilian premix and minerals company Vitamix Nutrição Animal, which owned factories in Brazil and Paraguay. The company had a premix and mineral plant in Naranjal, Paraguay. The acquisition created synergies between Vitamix and Vilomix, and together they had great potential in the sales of feed additives and customized premix solutions.

Global Vitamin And Mineral Premixes Market Report Scope

Segmentation Overview

| Vitamin only |

| Mineral only |

| Vitamin and mineral combination |

| Powder |

| Liquid |

| Organic |

| Conventional |

| Animal Food and Feed |

| Food and Beverage Fortification |

| Infant Nutrition |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Vitamin only | |

| Mineral only | ||

| Vitamin and mineral combination | ||

| By Form | Powder | |

| Liquid | ||

| By Category | Organic | |

| Conventional | ||

| By Application | Animal Food and Feed | |

| Food and Beverage Fortification | ||

| Infant Nutrition | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the vitamin and mineral premix market in 2025 and what growth is expected by 2030?

The vitamin and mineral premix market size is USD 8.04 billion in 2025 and will reach USD 11.02 billion by 2030, demonstrating a 6.51% CAGR.

Which region currently leads demand for vitamin and mineral premixes?

Asia-Pacific holds 41.24% of global demand, driven by mandatory food fortification and expanding animal agriculture.

Which application generates the highest revenue?

Animal food and feed remain the largest application, accounting for 41.26% of 2024 revenue.

Which product type is gaining the most traction?

Vitamin and mineral combination premixes dominate with 45.11% share and are projected to grow at 7.23% CAGR.

Page last updated on: