Market Overview

| Study Period | 2021 - 2031 |

|---|---|

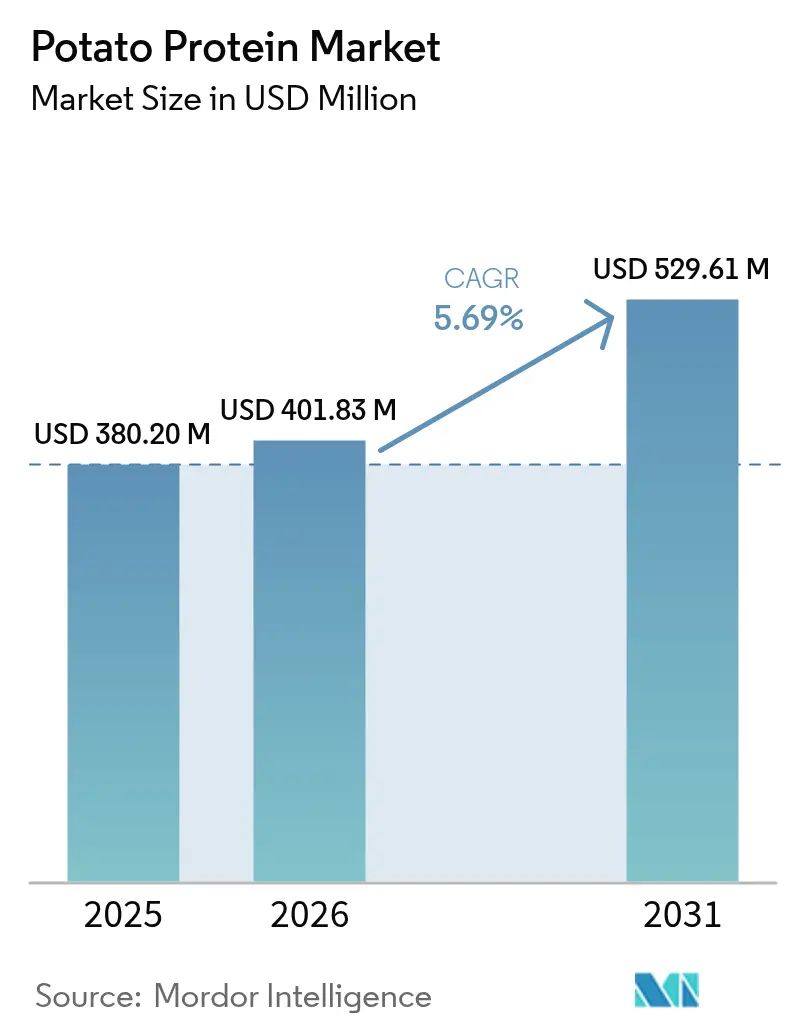

| Market Size (2026) | USD 401.83 Million |

| Market Size (2031) | USD 529.61 Million |

| Growth Rate (2026 - 2031) | 5.69% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Potato Protein Market Analysis by Mordor Intelligence

The potato protein market size is expected to grow from USD 380.20 million in 2025 to USD 401.83 million in 2026 and is forecast to reach USD 529.61 million by 2031 at 5.69% CAGR over 2026-2031. The market growth is driven by increasing adoption of plant-based diets, demand for clean-label ingredients, and efficient processing methods that utilize potato-starch by-products. Food manufacturers use potato protein in various applications, including meat alternatives, dairy substitutes, baked goods, beverages, and sports nutrition products, contributing to higher selling prices and expanded end-use applications. Recent procurement data indicates that small and medium-sized brands are increasing their bulk purchases, demonstrating a wider distribution of product development activities. This diversification of customer base helps suppliers maintain stable revenue streams during economic fluctuations.

Key Report Takeaways

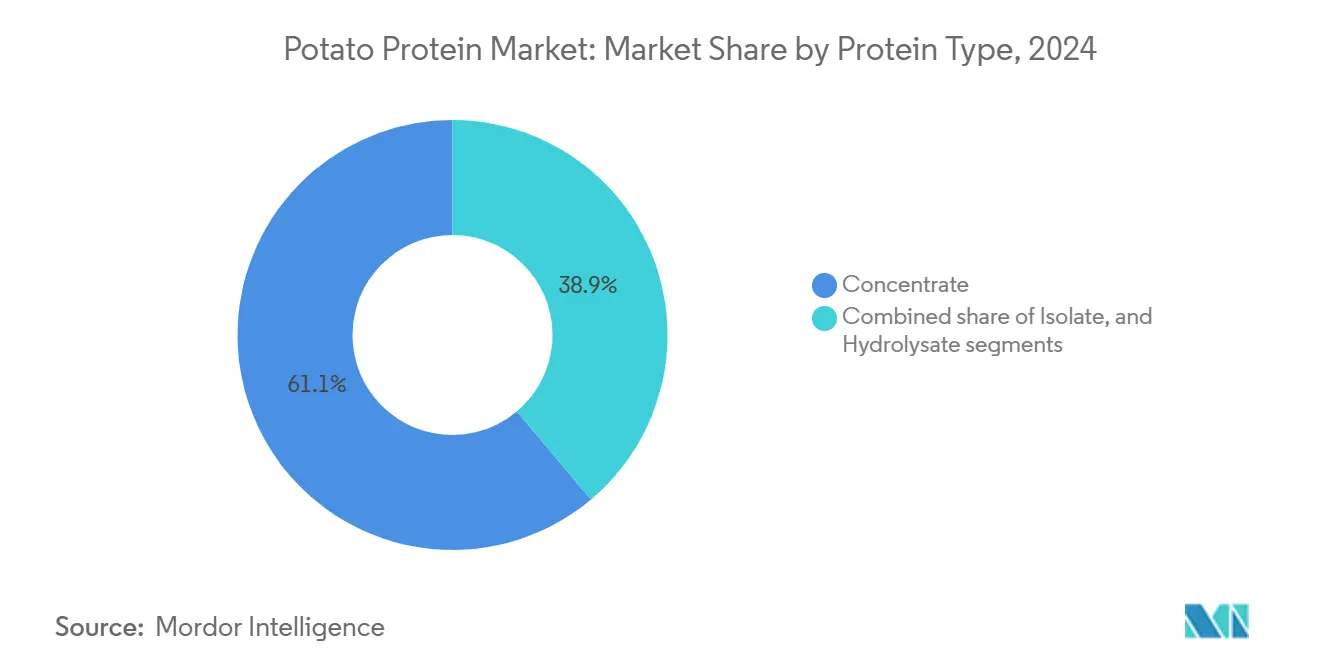

- By protein type, concentrates led with 60.62% of the potato protein market share in 2025, isolates are projected to expand at an 8.42% CAGR through 2031.

- By nature, conventional held 87.74% share of the market in 2025, and organic is poised for a 9.96% CAGR to 2031.

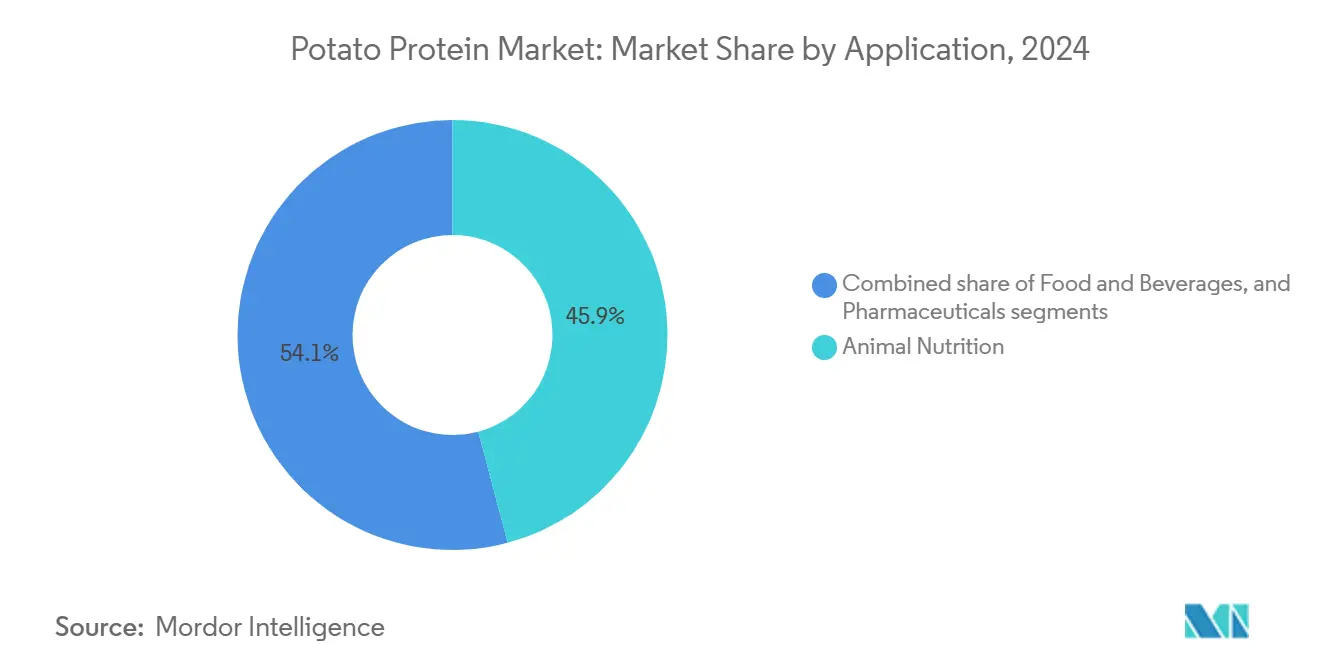

- By application, animal nutrition dominated the market with a maximum share of 45.32% in 2025, whereas pharmaceuticals are the fastest growing with a CAGR of 8.76% in 2031.

- By distribution channel, B2B held 89.58% share of the market in 2025, and B2C is poised for a 7.12% CAGR to 2031.

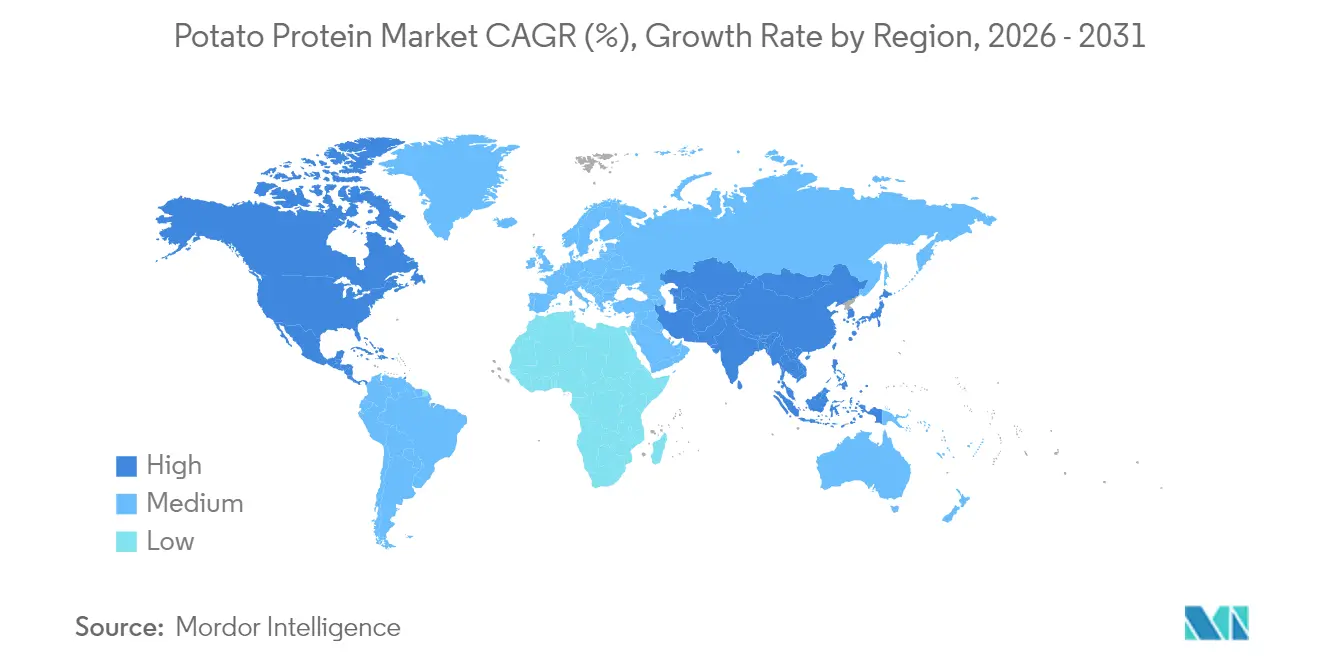

- By geography, Europe dominated the market with 44.86% in 2025, and Asia-Pacific remains the fastest-growing region with a CAGR of 8.05% in 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Potato Protein Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing consumer preference for vegan products | +2.1% | Global, with concentration in Europe and North America | Medium term (3-4 years) |

| Surging demand for non-allergenic gluten-free ingredients | +1.5% | North America and Europe | Medium term (3–4 years) |

| Expansion of aquafeed production and animal feed industries | +1.2% | Asia-Pacific and Europe | Short term (≤ 2 years) |

| Growing demand for sustainable and clean label ingredients | +2.0% | Europe, North America, expanding in Asia-Pacific | Medium term (3–4 years) |

| Increasing application in plant-based meat products | +2.2% | Global, with rapid uptake in Asia–Pacific | Short to Medium term (≤ 4 years) |

| Rising use in snacks and ready to eat products | +1.8% | Global, with highest impact in North America and Europe | Medium term (3-4 years) |

| Source: Mordor Intelligence | |||

Increasing Consumer Preference for Vegan Products

The growth of flexitarianism is transforming the potato protein market by generating significant demand for plant-based proteins. The rise in veganism has increased consumer awareness regarding the environmental and ethical implications of food choices. In response, food manufacturers are developing alternative protein sources to meet the expanding demand for plant-based products. In January 2023, approximately 707,000 people participated in Veganuary, a global campaign by a British non-profit organization that encourages participants to adopt a vegan diet during January. The 2023 participation represents a fourfold increase from 2018 levels [1]Source: Veganuary, "The Official Veganuary 2023 Participant Survey", veganuary.com. This significant application versatility increase demonstrates the growing consumer interest in plant-based diets and sustainable food choices.

Potato protein offers manufacturers a neutral flavor profile and functional properties, making it an ideal choice for meat alternative products. Its complete amino acid profile and high digestibility rating (PDCAAS score of 0.99) establish it as an effective ingredient for companies seeking differentiation in the plant-based market. Consumer preferences are shifting from meat-mimicking products toward natural plant-based alternatives that highlight authentic flavors and textures, expanding potato protein applications beyond traditional meat substitutes. This application's versatility has positioned potato protein as a valuable ingredient in the evolving plant-based food industry.

Surging Demand for Non-Allergenic Gluten-Free Ingredients

Potato protein's allergen-free profile is emerging as a key market differentiator amid the global increase in food allergies and intolerances. Consumer demand for potato protein has grown as they seek transparent, minimally processed food products without common allergens such as gluten and lactose. In 2022, the Food and Beverage Journal reported that 68% of consumers preferred clean-label products with simplified ingredient lists containing recognizable, natural components. Potato protein contains no gluten, lactose, or common allergens, making it suitable for manufacturers targeting the free-from market segment. This characteristic is essential in formulations for specialized diets and sensitive consumer groups, including children and individuals with multiple food sensitivities.

Several countries show high rates of lactose intolerance, influencing global dietary trends and ingredient preferences. According to World Population Review, South Korea, Yemen, Ghana, and Malawi report 100% lactose intolerance among their populations, while the Solomon Islands show a 99% intolerance rate as of 2025 [2]Source: World Population Review, "Lactose Intolerance Around the World", worldpopulationreview.com. This widespread lactose intolerance drives the food and beverage industry's demand for non-allergenic, gluten-free ingredients. Potato protein's functional versatility enables it to replace allergenic ingredients in various applications while maintaining desired textural and nutritional properties, creating opportunities for innovation in categories previously challenging for allergen-sensitive consumers.

Expansion of Aquafeed Production and Animal Feed Industries

The animal nutrition sector, which currently holds 46% of the potato protein market in 2024, is experiencing significant transformation driven by sustainability concerns and the search for alternative protein sources. Potato protein's high digestibility and complete amino acid profile make it an effective replacement for resource-intensive protein sources in animal feed formulations. The Food and Agriculture Organization of the United Nations (FAO) reported that global aquaculture production reached 130.9 million tons in 2022/23, contributing to total fisheries and aquaculture production of 223.2 million tons. This represented a 4% increase from 2020. The growth in aquaculture has increased demand in the aquafeed and animal feed industries, which require sustainable, plant-based protein alternatives. Potato protein has become a valuable ingredient for aquafeed formulations due to its high digestibility, amino acid profile, and low allergenicity.

Advancements in extraction technology have improved the cost-effectiveness of potato protein for feed applications, expanding its use across different animal species and life stages. For instance, in November 2024, IQI Trusted Petfood Ingredients partnered with Royal Avebe to launch ProtaSTAR®, a potato-based protein for the pet food industry. The product contains 80% protein content and a complete amino acid profile, enabling the production of nutritionally balanced vegetarian pet foods. This launch addresses the increasing demand for plant-based proteins, particularly in vegan and grain-free formulations.

Rising Use in Snacks and Ready to Eat Products

This growth trajectory in the snack market is driving increased demand for potato protein, which manufacturers increasingly prefer as an ingredient due to its functional properties and allergen-free characteristics. The protein enrichment trend now extends beyond traditional protein products into mainstream snack categories. Potato protein's exceptional functionality in snacks comes from its superior gelation, emulsification, and foaming properties, which enhance texture and stability in processed foods. Research demonstrates that potato protein isolate (PPI) forms stable gels at pH 3 and pH 7 at temperatures between 45-50°C, making it particularly valuable for snack products requiring specific textural attributes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Presence of low protein content | -1.7% | Global | Long term (≥ 5 years) |

| High production costs | -1.9% | Global; higher impact in developing regions | Medium term (3–4 years) |

| Limited consumer awareness | -1.0% | Asia-Pacific, South America | Short term (≤ 2 years) |

| Functional limitations in some applications | -0.8% | Global, pronounced in high-acid RTD beverages | Short to Medium term (≤ 3 years) |

| Source: Mordor Intelligence | |||

Presence of Low Protein Content

The inherently low protein content in raw potatoes (typically 2-2.5%) presents a significant challenge for the potato protein industry, creating multiple technical and economic challenges across the value chain. This percentage is significantly lower compared to other plant protein sources such as soybeans (35-40%) and peas (20-25%). The fundamental limitation creates a cascading effect of technical and economic challenges throughout the production process.

The extraction process compounds this challenge, with yields typically achieving only 30-40% recovery of the available protein content. This low recovery rate affects the industry's ability to compete on price with other plant proteins, particularly in price-sensitive markets like animal feed. In these markets, potato protein must demonstrate superior functional or nutritional benefits to justify its premium pricing and overcome competitive disadvantages.

In response to these challenges, biotechnology companies are developing innovative solutions. In 2024, ReaGenics introduced cell culture techniques that can increase potato protein content to 31%, with the potential to reach 40%. Additionally, PoLoPo's molecular farming technology aims to produce protein-rich potato tubers by the end of 2024, targeting the USD 26.6 billion egg protein market. However, the industry continues to face yield inefficiencies that affect its ability to compete with naturally protein-rich alternatives like pea and soy, requiring ongoing technological advancements to improve extraction efficiency and protein content.

High Production Costs

The complex extraction processes required to isolate potato protein from industrial potato starch production byproducts significantly impact its market competitiveness. The potato protein market faces significant growth constraints due to its high production costs compared to alternative plant-based proteins like soy, wheat, and pea. The protein extraction process requires complex separation and purification techniques, including thermal coagulation, ultrafiltration, and drying. These processes are energy-intensive and technologically demanding, resulting in higher operational and capital expenditure for manufacturers. Current industrial methods rely on energy-intensive processes like ion exchange and expanded bed adsorption, contributing to higher production costs compared to other plant proteins.

The inherently low protein content in potatoes (below 2%) necessitates processing large volumes of raw material to produce small quantities of protein. This inefficiency increases costs across the supply chain, from raw material procurement to transportation, storage, and waste management of unused potato components. The production of high-quality potato protein, particularly for food-grade and pet nutrition applications, requires rigorous quality control measures. These include maintaining low glycoalkaloid content and consistent amino acid profiles, which further increase processing complexity and production costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Protein Type: Potato Protein Concentrate Lead While Isolates Show Rapid Growth

The potato protein market, by protein type, is dominated by concentrates, which is the largest segment, holding a 61.13% market share in 2024. This dominance is attributed to their cost-effectiveness and versatility across multiple applications, particularly in animal feed, where price sensitivity is high. Potato protein concentrates maintain their market leadership through extensive use in animal feed applications, specifically in aquafeed and livestock nutrition, offering high digestibility and balanced amino acid profiles. The simplified and economical production process of concentrates enables their use in high-volume applications. These concentrates provide functional properties, including binding, emulsification, and foaming capabilities, making them suitable for processed food and pet food formulations.

Isolates represent the fastest-growing segment with an 8.71% CAGR (2025-2030), driven by their superior functional properties and higher protein content (≥90%), which justifies their premium pricing in specialized applications. Recent advancements in extraction technology have enhanced the efficiency of isolate production. For instance, in August 2024, ReaGenics has developed cell culture techniques that can increase potato protein content to 31%, which may significantly impact the isolate segment's growth.

Hydrolysates comprise the smallest segment but hold technological significance by offering enhanced digestibility and bioavailability for specialized nutrition applications. Their characteristics, including improved solubility and reduced allergenicity, make them valuable for pharmaceutical and sports nutrition products. The segment's expansion is supported by research on bioactive peptides from potato proteins, which show potential in applications such as anti-hyperuricemia treatments. These developments are broadening hydrolysates' applications in functional food and nutraceutical markets.

Note: Segment shares of all individual segments will be available upon report purchase

By Nature: Organic Premium Drives Growth

The conventional segment held a dominant 88.25% share of the potato protein market, being the largest segment in 2024, supported by established supply chains and cost-effective large-scale production capabilities. The organic segment is the fastest growing and is projected to grow at 10.37% CAGR during 2025-2030, exceeding the market's overall growth rate. This expansion reflects increasing consumer preference for sustainable and clean-label products. The USDA's Organic Situation Report indicates robust market conditions in the United States, with organic retail sales reaching USD 63.8 billion in 2023 [3]Source: U.S. Department of Agriculture, "Organic Situation Report, 2025 Edition", www.ers.usda.gov.

Government and industry initiatives are advancing sustainable agriculture and plant-based ingredient production through organic farming investments, infrastructure development, and food processing technology improvements. These efforts increase the supply of quality potato raw materials while meeting the growing demand for clean-label, allergen-free protein ingredients. A significant example is the Commonwealth of Pennsylvania's USD 3 million investment in Folkland Foods, an organic potato company in Erie County, through the Redevelopment Assistance Capital Program (RACP) in 2024. This funding supports manufacturing plant construction, freezer warehouse development, and potato storage facility establishment, generating up to 50 jobs and encouraging sustainable farming practices among local agricultural communities.

Organizations such as PURIS are responding to market demands by processing non-GMO seeds in certified-organic North American facilities, demonstrating their commitment to sustainable sourcing practices. The combination of environmental awareness and health considerations is creating substantial growth opportunities for organic potato protein, particularly in sports nutrition and premium pet food segments, where consumers prioritize ingredient quality and origin over price considerations.

By Application: Animal Feed Dominates Potato Protein Market as Pharmaceuticals Applications Expand

Animal nutrition dominates the potato protein market, being the largest category with a 45.87% share in 2024, primarily due to potato protein's excellent digestibility and complete amino acid profile. In addition, the functional properties of potato protein, specifically its emulsification and binding capabilities, enhance feed pellet quality and stability, resulting in improved feed efficiency. The livestock industry's increasing requirement for sustainable and allergen-free protein sources indicates an expanding market for potato protein in animal nutrition.

Additionally, the pharmaceuticals segment reflects this trend, with an expected 9.04% CAGR from 2025 to 2030, being the fastest-growing application segment. The pharmaceutical industry's demand for potato protein continues to grow, driven by its hypoallergenic properties, high digestibility, and amino acid composition. These characteristics enable its use in medical nutrition applications, specifically in enteral nutrition products for patients with dietary restrictions. Research and development initiatives are examining its applications in protein-based pharmaceuticals, which expands their market potential in the pharmaceutical industry. their

Note: Segment shares of all individual segments will be available upon report purchase

By Distribution Channel: B2B Dominates the Market

The B2B channel serves as the primary distribution pathway for potato protein, dominating the market with a share of 90.06% in 2024, facilitating bulk transactions between manufacturers and industrial users in food processing, animal feed, and pharmaceutical sectors. This channel operates through established relationships and efficient logistics systems that support large-volume movements. The B2B distribution dominance aligns with the market structure, where potato protein functions primarily as an industrial ingredient rather than a retail product. Companies like Cargill utilize their extensive B2B networks to distribute plant proteins, including potato-based variants, to food manufacturers incorporating protein enrichment in various products and applications.

The B2C channel, while currently smaller in scale, represents the fastest-growing segment with a projected CAGR of 7.44% through 2030, driven by increasing consumer awareness of specialized plant proteins. This segment primarily caters to niche markets, including sports nutrition and specialty diets, where consumers value potato protein's hypoallergenic properties and complete amino acid profile. The introduction of consumer-ready products, such as protein powders and bars containing potato protein, is gradually expanding this channel's market presence and significance.

Geography Analysis

Europe holds a dominant 44.86% share of the potato protein market in 2025, supported by its extensive potato processing infrastructure and extraction technologies. The region's market strength stems from established companies like Royal Avebe, Roquette Frères, and Emsland Group, which operate vertically integrated facilities from potato cultivation to protein extraction. The European Food Safety Authority's (EFSA) updated guidance for novel food applications, effective February 2025, simplifies the approval process for innovative protein products. This regulatory framework, combined with increasing consumer demand for plant-based alternatives, creates a conducive environment for continued market expansion and development.

Asia-Pacific exhibits the highest growth rate at 8.05% CAGR (2026-2031), attributed to food processing industrialization and growing consumer interest in protein-enriched products. The region's development is supported by strategic production investments, as demonstrated by the joint venture between Tummers Food Processing Solutions and Kiron Food Processing Technologies in India to improve potato processing infrastructure. China and Japan are the primary market drivers, while South Korea shows increased adoption in sports nutrition applications. The growth of animal feed and aquaculture sectors across Asia-Pacific generates additional demand for potato protein, particularly in developing economies where meat and fish consumption increases with rising disposable incomes.

North America maintains a substantial potato protein market share, driven by strong demand for plant-based proteins and gluten-free ingredients. The United States leads regional consumption, supported by growing consumer preference for alternative proteins. The USDA's USD 300 million organic transition initiative from 2022 indirectly benefits the organic potato protein segment by increasing organic potato supply. The region's food innovation capabilities and robust consumer purchasing power support continued growth, especially in premium applications like sports nutrition and specialized dietary products.

Competitive Landscape

The potato protein market exhibits a moderately consolidated structure, with a few major companies controlling global production and innovation. These companies focus on advanced extraction technologies, strategic partnerships, and product diversification to maintain their market positions. Royal Avebe, Roquette Frères, and Emsland Group lead the market through their technical capabilities and robust distribution networks, further strengthening their positions through strategic partnerships.

The market landscape is transforming as biotechnology companies introduce innovative protein production methods. Companies such as ReaGenics and PoLoPo are developing new technologies that address the fundamental challenge of low protein content in conventional potatoes, potentially reshaping the market dynamics.

Moreover, Avebe manufactures potato protein products, including PerfectaSOL, which enhances texture, elasticity, and moisture retention in plant-based formulations. The ingredient is utilized in cookies, muffins, and veggie-based baked goods. Its clean-label profile and allergen-free properties address consumer requirements for natural food alternatives.

Potato Protein Industry Leaders

-

Avebe

-

Omega Protein Corporation

-

Tereos Group

-

Roquette Frères

-

Agrana Beteiligungs-AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: PoLoPo has finalized the design of its first pilot-scale facility to process genetically modified potatoes into functional protein powders for the food industry.

- November 2024: IQI Trusted Petfood Ingredients has formed an exclusive partnership with Royal Avebe to introduce ProtaSTAR, a potato-based protein ingredient for the pet food industry. ProtaSTAR contains 80% protein and provides a complete amino acid profile, serving as an alternative to animal proteins such as beef and chicken. The ingredient undergoes a refinement and purification process that improves its nutritional value and digestibility.

- August 2024: ReaGenics, an Israeli biotech startup, has developed potato biomass with 31% protein content using plant cell culture technology, compared to 2% in conventional potatoes. The company cultivates specific potato varieties in bioreactors under optimized conditions and aims to increase the protein concentration to 40% without genetic modification. The protein demonstrates high digestibility with a Protein Digestibility-Corrected Amino Acid Score (PDCAAS) of 0.99 and exhibits functional properties including solubility, emulsification, and gelling capabilities for food applications.

- July 2024: Israeli biotechnology company PoLoPo implemented protein-producing potato cultivation through genetic modification. The modified potatoes generate functional proteins, including ovalbumin and patatin, in their tubers through molecular farming processes. The company established large-scale manufacturing plans, with a production target of 300 tons in 2022.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global potato protein market as the total annual sales value of food-grade and feed-grade protein concentrates and isolates extracted from industrial potato processing side-streams. Functional hydrolysates, raw potatoes, starch, and fiber fractions fall outside this scope.

Scope exclusion: pharmaceutical-grade hydrolyzed peptides are not covered.

Segmentation Overview

-

By Protein Type

- Potato Protein Concentrate

- Potato Protein Isolate

- Potato Protein Hydrolysate

-

By Nature

- Conventional

- Organic

-

By Application

-

Food and Beverages

- Bakery and Confectionery

- Meat Analogues

- Dairy Alternatives

- Sports Nutrition and Bars

- Others

-

Animal Nutrition

- Livestock Feed

- Pet Food

- Aquafeed

- Pharmaceuticals

-

Food and Beverages

-

By Distribution Channel

- B2B

- B2C

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- France

- United Kingdom

- Spain

- Netherlands

- Italy

- Sweden

- Poland

- Belgium

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Indonesia

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Chile

- Colombia

- Peru

- Rest of South America

-

Middle East and Africa

- United Arab Emirates

- South Africa

- Nigeria

- Saudi Arabia

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed ingredient processors, specialty feed formulators, sports-nutrition brand managers, and equipment suppliers across Europe, North America, and Asia. Discussions clarified typical protein recovery rates, prevailing contract prices, and regional regulatory hurdles, letting us verify secondary assumptions and close data gaps.

Desk Research

We began with trade and crop data from bodies such as the FAO, Eurostat, and the USDA, which reveal potato cultivation volumes and by-product yields. Import-export flows from UN Comtrade, production economics from Potatoes USA, and patent activity accessed via Questel helped us size available raw material pools and gauge extraction technology adoption. Company 10-Ks and investor decks supplied capacity, pricing, and expansion signals, while news archives on Dow Jones Factiva tracked plant openings and M&A moves. The sources listed are illustrative; many others informed the evidence base.

Market-Sizing & Forecasting

A top-down model converts regional potato harvest tonnage into available protein output through stage-wise yield factors, which are then adjusted by utilization rates in food and feed applications. Select bottom-up checks, sampled plant capacities multiplied by average selling prices, provide a sanity cross-check before totals are finalized. Key variables include: industrial potato processing share, protein extraction efficiency, average selling price by grade, uptake in plant-based meat launches, and aquafeed production growth. Forecasts employ multivariate regression that links these drivers to demand, complemented by scenario analysis vetted through our interview panel. When supplier roll-ups are patchy, interpolation uses three-year moving averages anchored to verified trade data.

Data Validation & Update Cycle

Outputs face layer-by-layer peer review, variance checks against alternative protein benchmarks, and anomaly flags triggered by quarterly earnings calls. Our models refresh every twelve months, with interim revisions after material events. A final analyst audit occurs just before report delivery.

Credibility Anchor: Why Mordor's Potato Protein Baseline Stands Up

Published estimates differ because firms choose dissimilar scopes, years, and pricing assumptions.

Our disciplined inclusion of both food and feed grades, latest-year currency conversion, and balanced scenario set positions our figure as a dependable midpoint for strategic planning.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 380.2 million (2025) | Mordor Intelligence | - |

| USD 105 million (2022) | Global Consultancy A | Excludes animal nutrition channels; older base year |

| USD 230.2 million (2024) | Industry Journal B | Counts concentrates only and applies regional ASP averages without inflation parity |

These comparisons show that scope breadth, refresh cadence, and price reference choices drive sizeable swings. According to Mordor analysts, our integrated approach delivers a transparent, reproducible baseline clients can trust.

Key Questions Answered in the Report

What is the expected potato protein market size by 2031?

The potato protein market is forecast to reach USD 529.61 million by 2031.

Which region currently has the largest potato protein market share?

Europe leads with 44.86% share, driven by its integrated starch-processing ecosystem

Why are potato protein isolates growing faster than concentrates?

Isolates offer ≥ 90% protein and improved solubility, enabling premium claims in beverages and sports nutrition and therefore showing an 8.42% CAGR.

How does potato protein support sustainable aquafeed?

Its high digestibility and balanced amino-acid profile enable partial replacement of fish meal, lowering environmental impact while maintaining growth performance.

Page last updated on: