Greek Yogurt Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

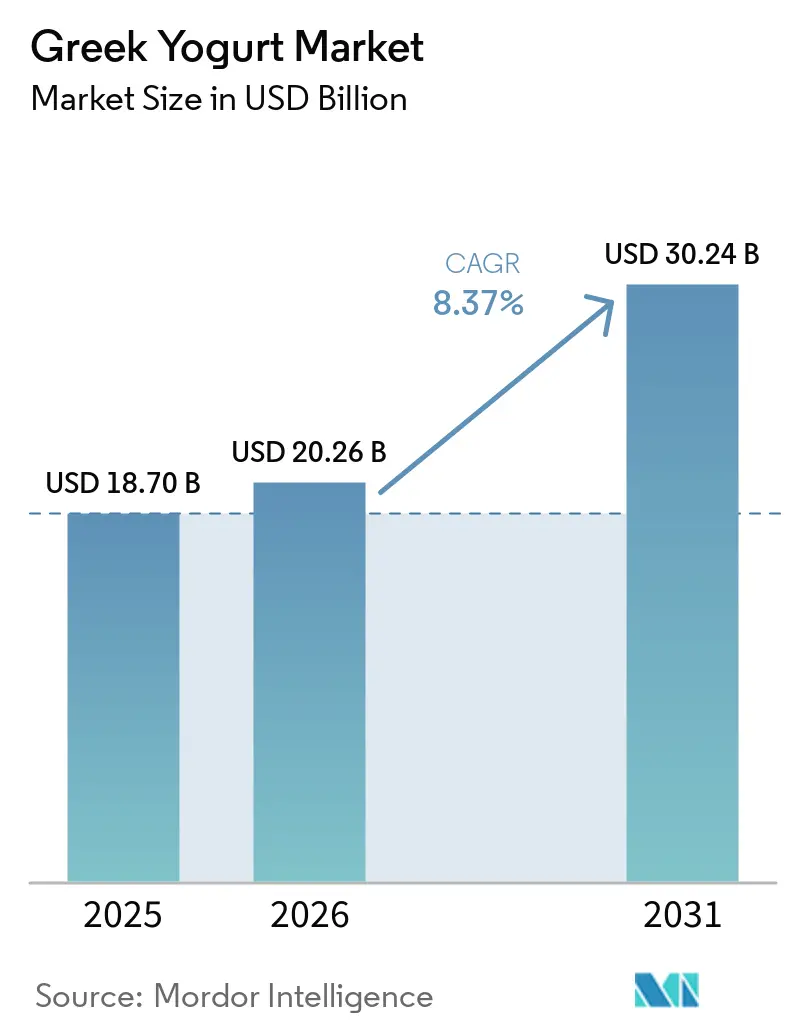

| Market Size (2026) | USD 20.26 Billion |

| Market Size (2031) | USD 30.24 Billion |

| Growth Rate (2026 - 2031) | 8.37% CAGR |

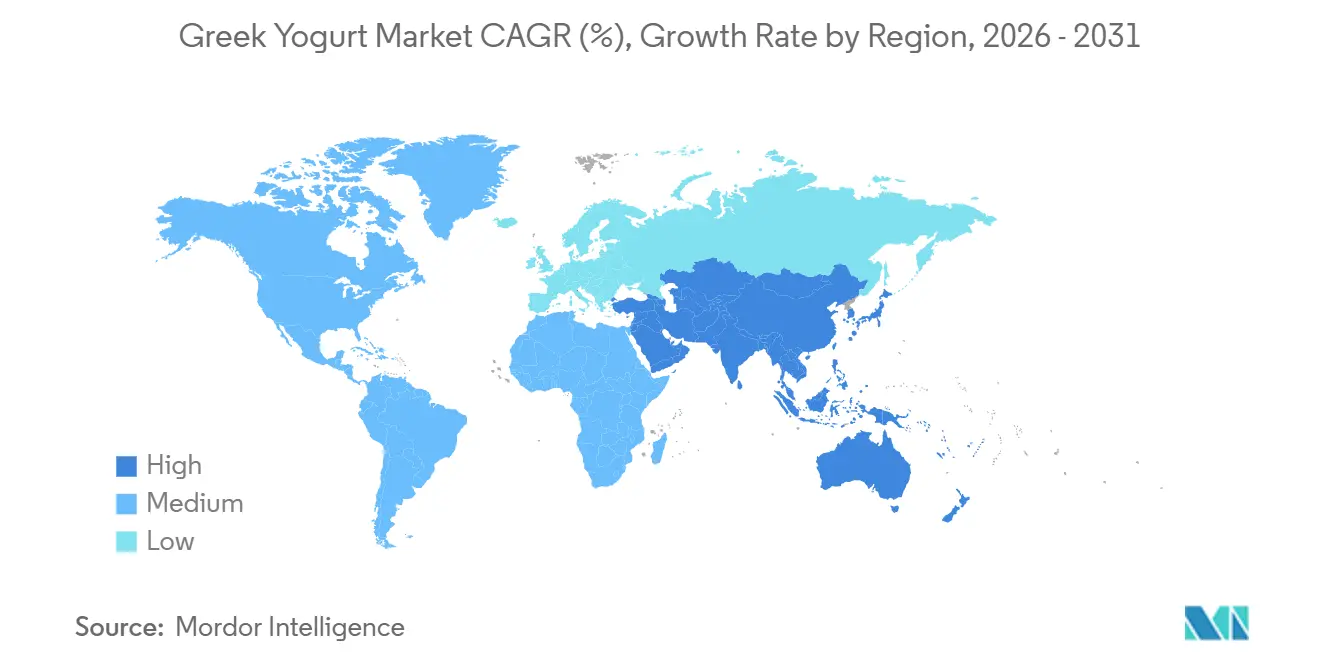

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Greek Yogurt Market Analysis by Mordor Intelligence

The Greek yogurt market size is projected to grow from USD 18.70 billion in 2025 to USD 20.26 billion in 2026, reaching USD 30.24 billion by 2031, with a CAGR of 8.37% during the forecast period (2026-2031). Regulatory support, such as the U.S. Food and Drug Administration’s qualified health claim linking regular yogurt consumption to a reduced risk of type 2 diabetes, has repositioned the category as a form of preventive nutrition rather than merely an occasional snack [1]Source: U.S. Food and Drug Administration, “Qualified Health Claim: Yogurt and Type 2 Diabetes,” fda.gov. Consumers are increasingly shifting toward protein-rich foods, and Greek yogurt, offering 15-20 grams of protein per serving at an affordable price point, is driving upgrades from traditional yogurt and even protein bars. The Asia-Pacific region is expected to lead growth, driven by urbanization in countries such as China, India, and Indonesia, where per capita dairy consumption remains significantly lower than in Western markets. Processors are investing in advanced technologies such as anaerobic digestion and ultrafiltration to capitalize on whey protein isolates. However, the capital-intensive nature of these technologies benefits large-scale players while creating entry barriers for regional competitors. Additionally, plant-based Greek-style alternatives are gaining momentum in the market.

Key Report Takeaways

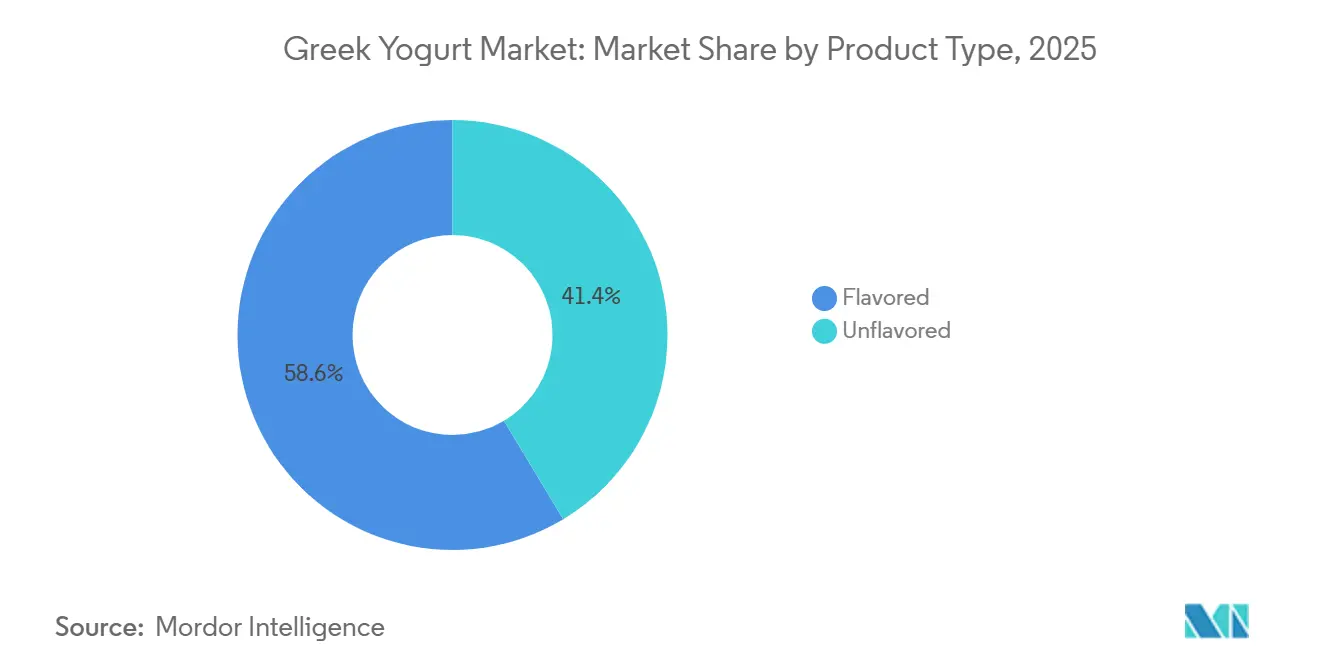

- By product type, flavored offerings led with 58.61% of 2025 revenue, while unflavored offerings are forecast to post the highest growth at a 9.83% CAGR for 2026-2031.

- By fat content, full-fat formats accounted for 43.03% of the 2025 market, yet non-fat formats are set to outpace all other tiers with a 10.34% CAGR over 2026-2031.

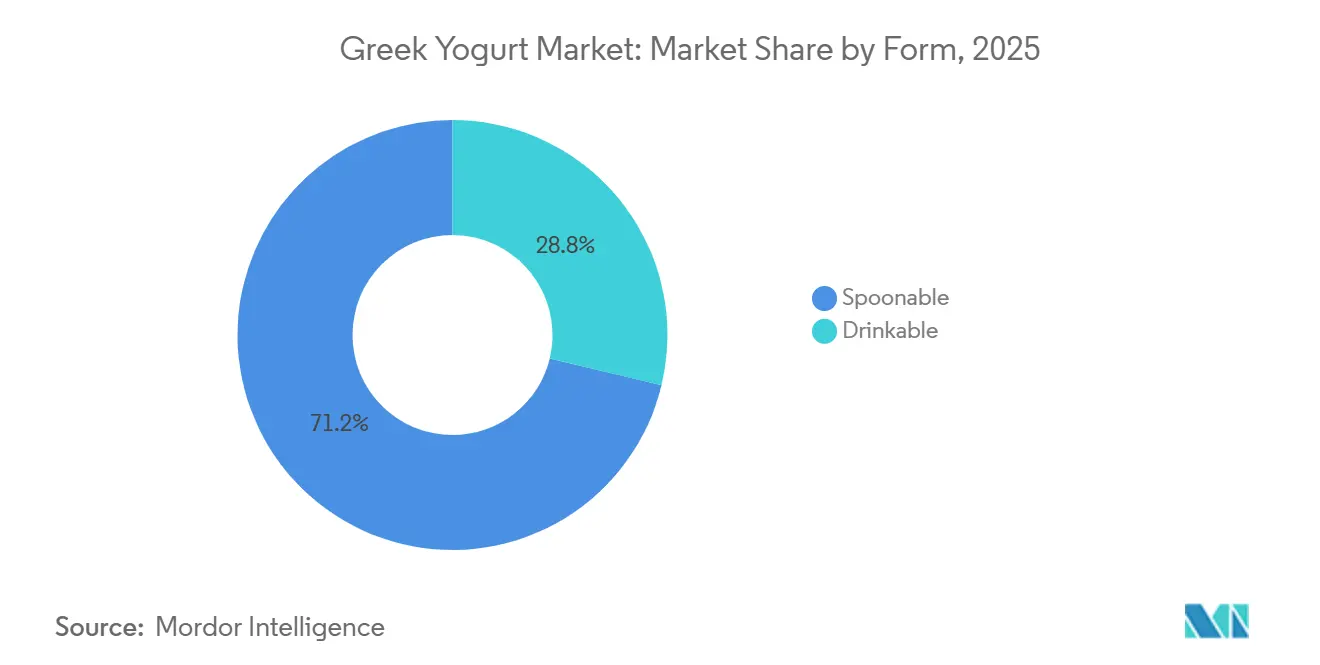

- By form, spoonable Greek yogurt accounted for 71.24% of global demand in 2025; drinkable lines are projected to expand fastest at 10.12% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets accounted for 43.65% of 2025 volume, whereas online retail shows the strongest upside, with an 11.05% CAGR forecast for 2026-2031.

- By geography, North America captured 37.52% of the market share in 2025, yet Asia-Pacific is forecast to be the fastest-growing region at a 9.68% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Greek Yogurt Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in demand for high-protein functional foods | +2.1% | Global, with peak adoption in North America, Western Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Growing consumer focus on gut health and immunity advantages | +1.8% | Global, strongest in North America and Europe; emerging in Asia-Pacific urban centers | Medium term (2-4 years) |

| Expansion of low-fat and flavored product lines in supermarkets | +1.3% | NorthAmerica and Europe; selective penetration in Asia-Pacific and South America | Short term (≤ 2 years) |

| Expansion of e-commerce platforms and enhanced distribution networks | +1.5% | Global, with highest growth in Asia-Pacific, North America, and select European markets | Short term (≤ 2 years) |

| Influence of regional dietary preferences and growing popularity of the Mediterranean diet | +0.9% | Europe (especially Mediterranean basin), North America, and emerging in Middle East | Long term (≥ 4 years) |

| Rising popularity of organic and clean-label Greek yogurt | +1.2% | North America and Western Europe; nascent in Asia-Pacific and South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in demand for high-protein functional foods

The surge in demand for high-protein functional foods has significantly driven the growth of the Greek yogurt market. Consumers increasingly view protein as a critical component of daily nutrition, with Greek yogurt emerging as a convenient and accessible source. Each serving typically contains 15-20 grams of complete protein, making it a preferred choice for muscle preservation and overall health. The FDA’s qualified health claim from March 2024 further elevated yogurt's status, positioning it as a preventive nutrition product rather than a dessert. In response, brands like Chobani introduced high-protein variants with up to 30 grams of protein per serving, achieving double-digit sales growth in 2025. Additionally, the rising adoption of GLP-1 medications has created a new consumer segment that prioritizes portion-controlled, protein-rich options. This trend has led to basket substitution, where consumers replace protein bars and shakes with chilled dairy cups, enabling premium pricing without compromising volume. As a result, Greek yogurt has firmly positioned itself within the broader functional foods category, aligning with evolving consumer preferences for health-focused, high-protein products.

Growing consumer focus on gut health and immunity advantages

Live cultures, once considered a niche for digestive health, are now a staple of daily immunity routines. Currently, 97.8% of U.S. yogurt UPCs (Universal Product Codes) feature at least one functional claim, reflecting this shift in consumer priorities [2]Source: U.S. Department of Agriculture Economic Research Service, "A Case Study of Claims on Milk and Yogurt," ers.usda.gov. Scientific studies have linked specific Lactobacillus strains to improved gut barrier integrity, encouraging brands to invest in strain-specific clinical trials to substantiate new health claims. Organic Greek yogurt lines are growing as consumers increasingly associate the USDA organic seal with clean fermentation practices and the absence of antibiotic residues. Retailers are leveraging this trend by emphasizing probiotic benefits through shelf-talkers, effectively elevating yogurt from a commodity to a functional food. This growing focus on gut health and immunity continues to drive the Greek yogurt market, fostering the development of daily consumption habits among health-conscious consumers.

Expansion of low-fat and flavored product lines in supermarkets

Supermarkets are increasingly expanding their Greek yogurt offerings, driven by the rising demand for low-fat and flavored product lines. Low-fat Greek yogurt is experiencing robust growth as health-conscious consumers prioritize protein-rich, low-calorie options. Flavored variants, including dessert-inspired options like key lime crumble and fruit-based staples such as strawberry and vanilla, continue to attract a diverse consumer base, particularly younger demographics like Gen Z. Retailers are leveraging these trends by dedicating more shelf space to Greek yogurt, creating a premium tier that supports higher price points. Additionally, private-label brands are capitalizing on this momentum by offering competitively priced alternatives that align with clean-label preferences. These developments reinforce supermarkets as the dominant channel for Greek yogurt discovery and sales, even as e-commerce gains traction.

Influence of regional dietary preferences and growing popularity of the Mediterranean diet

The growing popularity of the Mediterranean diet, endorsed by the World Health Organization for its heart health benefits, has significantly boosted demand for Greek yogurt as a key dietary component. While Southern European markets maintain strong traditional consumption, North American and Asia-Pacific regions are increasingly adopting Greek yogurt due to its association with longevity and wellness. Regional preferences, however, continue to shape product offerings. For instance, Latin American consumers favor sweeter, fruit-infused options, while Middle Eastern consumers prefer date-flavored variants. To cater to these diverse tastes, brands are localizing their formulations while preserving the signature thick and creamy texture of Greek yogurt. This alignment with regional dietary preferences and the Mediterranean diet's health halo effect ensures sustained demand and positions Greek yogurt as a culturally adaptable and resilient product in the global market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuations in milk prices increase the already high input cost structure | -1.4% | Global, with acute pressure in North America, Europe, and export-dependent regions | Short term (≤ 2 years) |

| Strict food safety and labeling regulations | -0.8% | Global, with stringent enforcement in North America and Europe; emerging in Asia-Pacific | Medium term (2-4 years) |

| Rising competition from both dairy-based and plant-based alternatives | -1.1% | Global, with highest intensity in North America and Europe; growing in Asia-Pacific | Medium term (2-4 years) |

| Environmental concerns regarding acid-whey disposal lead to stricter regulations | -0.9% | North America and Europe; emerging regulatory focus in Asia-Pacific and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fluctuations in milk prices increase the already high input cost structure

Milk accounts for up to 70% of production costs for Greek yogurt, and its price volatility significantly increases the already high input cost structure. Greek yogurt production requires approximately three times as much milk as traditional yogurt, amplifying its cost sensitivity. Large-scale producers mitigate this risk through long-term contracts with dairy suppliers, ensuring price stability and consistent supply. In contrast, smaller brands reliant on spot markets face greater margin pressures due to fluctuating milk prices. Additionally, farmers in regions such as Illinois are experiencing negative margins, driven by rising feed and operational costs, which could constrain the raw milk supply during peak demand periods. These rising input costs often lead to higher retail prices, potentially dampening volume growth in price-sensitive segments of the Greek yogurt market. Furthermore, the increasing focus on sustainable dairy farming practices may add to production costs, further influencing market dynamics.

Strict food safety and labeling regulations

Strict food safety and labeling regulations significantly impact the Greek yogurt market, creating challenges for manufacturers to ensure compliance across regions. The FDA's updated yogurt standard of identity in 2024 introduced new requirements, including the allowance of vitamin D3 fortification up to 178 IU per 100 g in 2025, necessitating adjustments in production processes, audits, and packaging [3]Source: Federal Register, “Food Additives Permitted for Direct Addition to Food for Human Consumption,” federalregister.gov. Similarly, Europe enforces stringent guidelines under Regulation 1169/2011, requiring exporters to navigate dual compliance frameworks. Additionally, any probiotic health claims must be substantiated by clinical evidence, which extends the time-to-market for functional product innovations. Smaller processors, in particular, face difficulties managing regulatory complexities, as limited resources increase the risk of non-compliance and potential recalls. These regulatory hurdles elevate fixed costs and slow down the pace of innovation, posing a significant restraint on the growth of the Greek yogurt market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Flavored Dominance Meets Unflavored-Variant Upswing

Flavored Greek yogurt commanded 58.61% of the market in 2025, driven by consumer preference for fruit-forward profiles and dessert-inspired variants. However, the segment faces challenges due to increasing consumer scrutiny of added sugars and artificial sweeteners, prompting reformulations with natural alternatives such as stevia, monk fruit, and allulose. Manufacturers are also innovating with indulgent dessert-inspired flavors like key lime crumble, chocolate cheesecake, and salted caramel to maintain consumer interest and drive incremental sales rather than cannibalizing existing products. Foodservice operators are also leveraging flavored Greek yogurt in smoothies, parfaits, and breakfast bowls, further expanding its application and market reach.

Unflavored Greek yogurt is expanding at a 9.83% CAGR through 2031, marking the fastest growth rate within this segmentation. Unflavored variants cater to purists seeking minimal ingredients and clean-label products while serving as versatile culinary inputs in savory dishes, baking, and meal replacements. This segment benefits from its adaptability, as consumers increasingly use unflavored Greek yogurt as a base for homemade dips, salad dressings, and marinades. The rise of health-conscious eating has further boosted demand, with unflavored Greek yogurt being perceived as a high-protein, low-sugar option suitable for various dietary preferences, including keto and low-carb diets. Additionally, its growing use in plant-based and hybrid recipes, where it is paired with alternative proteins or grains, underscores its versatility.

By Fat Content: Non-Fat Surges as Weight-Management Cohort Expands

Full-fat formats held 43.03% of 2025 sales, reflecting heritage taste preferences and indulgent texture. Full-fat Greek yogurt continues to appeal to consumers seeking rich, creamy options that align with traditional recipes and premium indulgence. The segment benefits from increasing consumer awareness of the potential health benefits of dairy fats, such as improved satiety and nutrient absorption. Additionally, full-fat variants are gaining traction in Mediterranean and European markets, where they are often associated with authenticity and superior taste.

Non-fat Greek yogurt is projected to grow at a robust 10.34% CAGR through 2031, driven by its appeal to health-focused consumers who prioritize high protein content and low calorie intake. Non-fat Greek yogurt is particularly popular among fitness enthusiasts and individuals following weight management programs, including those using GLP-1 medications. Manufacturers are leveraging advancements in food technology to enhance the texture and flavor of non-fat variants, incorporating fat-mimicking fibers and inulin to replicate the creaminess of full-fat options. Low-fat Greek yogurt remains a significant segment, catering to mainstream shoppers seeking a balanced option between indulgence and health. Low-fat Greek yogurt is often fortified with probiotics and other functional ingredients, enhancing its appeal as a health-focused product.

By Form: Drinkables Blur the Dairy-Beverage Line

Spoonable Greek yogurt commanded 71.24% of the market in 2025, anchored by its versatility across breakfast bowls, snacks, and culinary applications. Its dominance reflects an established presence in traditional consumption occasions, with manufacturers defending this segment through texture innovation, mix-ins, and premium packaging. For instance, Chobani's Flip line, which combines Greek yogurt with granola, chocolate, and other toppings in a dual-chamber cup, has sustained strong sales by transforming yogurt into an interactive snacking experience. The segment also sees increasing demand for single-serve packaging, catering to on-the-go consumers and reinforcing its position as a staple in the yogurt market.

Meanwhile, drinkable formats are expanding at a 10.12% CAGR through 2031, driven by the growing demand for on-the-go consumption and the convergence of yogurt with functional beverages. Drinkable Greek yogurt appeals to commuters, fitness enthusiasts, and meal-skippers who prioritize convenience and single-hand consumption. Manufacturers are innovating in packaging, protein content, and flavor profiles to differentiate from traditional drinkable yogurts. For example, Oikos launched a PRO drinkable variant in Canada in 2025 with 18 to 24 grams of protein, positioning it as a post-workout recovery drink and competing with protein shakes. However, drinkable formats face challenges maintaining probiotic viability and maintaining a thick texture throughout shelf life.

By Distribution Channel: Online Retail Surges as DTC Models Gain Traction

Supermarkets and hypermarkets accounted for 43.65% of Greek yogurt distribution in 2025, leveraging their role as discovery channels for new flavors and their ability to offer competitive pricing through private-label alternatives. These outlets remain the primary choice for consumers due to their extensive product variety, frequent promotional campaigns, and the convenience of one-stop shopping. Supermarkets and hypermarkets are defending their share by expanding refrigerated sections, introducing exclusive SKUs, and leveraging loyalty programs to drive repeat purchases. Additionally, they are increasingly collaborating with Greek yogurt brands to offer in-store sampling events and targeted discounts, boosting consumer engagement and trial rates.

Online retail is expanding at a 11.05% CAGR through 2031, the fastest rate among all distribution channels, driven by increased yogurt purchases via platforms such as DoorDash. E-commerce enables direct-to-consumer models that bypass traditional retail slotting fees, allowing brands to test limited-edition flavors, personalized bundles, and subscription programs. Online platforms also facilitate geographic expansion into underserved markets where cold-chain infrastructure limits physical retail presence, and they provide rich consumer data that informs product development and marketing. Brands are developing ambient-stable or frozen Greek yogurt variants for e-commerce fulfillment. Convenience stores remain critical for impulse purchases and on-the-go consumption, particularly for single-serve drinkable formats. Other distribution channels, including specialty stores, health food retailers, and foodservice, serve niche segments seeking organic, artisanal, or bulk-format Greek yogurt.

Geography Analysis

North America led the Greek yogurt market with a 37.52% revenue share in 2025 and is expected to register mid-single-digit growth, with a roughly 4.7% CAGR through 2031, as protein branding revitalizes a maturing category. The FDA’s diabetes-risk claim, along with surging GLP-1 prescriptions, is driving renewed demand, while capacity expansions by Danone and Chobani ensure a consistent supply. Mexico shows significant potential within the region as low- and no-sugar product penetration rises, signaling a growing preference for healthier cultured dairy options.

Asia-Pacific is projected to be the fastest-growing region, with a 9.68% CAGR through 2031, driven by urbanization in China, India, and Indonesia, where per-capita dairy consumption remains significantly lower than Western norms.Japan's aging population and focus on functional foods create demand for probiotic-rich Greek yogurt, while Australia's established dairy industry and health-conscious consumers position it as a regional leader. However, Asia-Pacific faces structural challenges such as lactose intolerance prevalence in many countries, cold-chain infrastructure in underdeveloped rural areas, and price sensitivity. Manufacturers are responding with lactose-free formulations, smaller pack sizes, and localized flavors such as mango, lychee, and matcha to align with regional taste preferences.

Europe, anchored by traditional consumption in Greece, Italy, and Spain, benefits from endorsements of the Mediterranean diet that sustain everyday use. Premium brands in the region are differentiating themselves through organic and pasture-raised claims. Meanwhile, Latin America and the Middle East and Africa, though starting from smaller bases, are expected to outpace the global average growth rate as urban middle classes increase their protein and probiotic intake. Manufacturers are targeting these emerging markets for greenfield plant investments to avoid tariffs and reduce freight costs, a strategy that is expected to expand the geographic footprint of the Greek yogurt market over the next decade.

Competitive Landscape

The Greek yogurt market remains moderately concentrated, anchored by global leaders yet punctuated by agile challengers leveraging authenticity, technology, and sustainability to carve profitable niches. Danone has intensified capital deployment, adding USD 110 million to its Minster, Ohio site to support Oikos and Activia pipelines, while allocating USD 4 million to expand Fort Worth, Texas, for Danimals and YoCrunch lines. These actions aim to defend shelf dominance in a maturing North American arena. Chobani secured a USD 650 million investment in late 2025 at a USD 20 billion valuation, with a two-pronged strategy to increase throughput and capture cross-category collaboration.

Regional specialists are seizing emerging opportunities that major players have overlooked. Nounós Creamery introduced A2 Greek Yogurt made with 100% A2/A2 milk and Non-GMO Project verification, positioning digestibility and regenerative sourcing as competitive advantages against mass-market formulations. Forager Project’s cashew-based Greek-style line delivers 10 g of plant protein, testing flexitarian demand and pressuring dairy incumbents to communicate their environmental credentials. Private-label programs at Kroger, Walmart, and Aldi replicate leading textures at a discount, compressing branded margins and driving premiumization through novel mix-ins, limited-edition desserts, and clinically validated probiotic strains.

Technology, regulation, and sustainability are redefining competitive levers. Arla Foods’ Nutrilac protein system enables co-packers to achieve Greek-style viscosity with existing fermentation lines, reducing capex for late entrants. Scale players are investing in anaerobic digestion and ultrafiltration to monetize acid-whey by-products, converting an environmental liability into high-margin whey protein isolates for sports nutrition channels. The FDA’s amended yogurt standard of identity and its 2025 vitamin D3 fortification limit create new on-pack claims and reformulation opportunities that favor R&D-rich operators.

Greek Yogurt Industry Leaders

-

Chobani Global Holdings, LLC

-

Danone S.A.

-

Fage International S.A.

-

General Mills Inc.

-

Lactalis Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Danone North America announced a USD 4 million expansion of its Fort Worth, Texas yogurt plant, adding 3,495 square feet and remodeling 1,843 square feet to accommodate new production equipment for Danimals, Activia, and YoCrunch brands, addressing capacity constraints driven by high-protein yogurt demand.

- June 2025: Lactalis USA completed the acquisition of General Mills' U.S. yogurt business for approximately USD 1.2 billion, consolidating Yoplait, Go-Gurt, Oui, Mountain High, and: ratio brands under a new Midwest Yogurt division based in Minneapolis, along with approximately 1,000 employees and two manufacturing facilities in Murfreesboro, Tennessee, and Reed City, Michigan.

- May 2025: Nounós Creamery launched the nation's first A2 Greek Yogurt line, made from 100% A2/A2 milk and Non-GMO Project verified, in four flavors (Plain, Vanilla Bean, Coconut Mango, Mixed Berry) at select retailers, positioning the brand as easier to digest due to the absence of A1 beta-casein and aligned with regenerative farming practices.

- May 2025: Clover Sonoma reintroduced Greek yogurt with the launch of Pasture Raised Organic Greek Nonfat Plain Yogurt, featuring 22 grams of protein per serving and made from pasture-raised organic milk, available in 32-ounce containers at a SRP of USD 9.99 at independent and natural grocers, Safeway, and Sprouts.

Global Greek Yogurt Market Report Scope

The Greek yogurt market is segmented by product type, fat content, form, distribution channel, and geography. Based on product type, the market is segmented into flavored and unflavored. By fat content, the market is segmented into full-fat, low-fat, and non-fat. By form, the market is segmented into spoonable and drinkable. By distribution channels, the market has been segmented into hypermarkets/supermarkets, convenience stores, online retail stores, and other distribution channels. By geography, the market has been segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done based on value (USD) and volume (Tons).

| Flavored |

| Unflavored |

| Full-Fat |

| Low-Fat |

| Non-Fat |

| Spoonable |

| Drinkable |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Flavored | |

| Unflavored | ||

| By Fat Content | Full-Fat | |

| Low-Fat | ||

| Non-Fat | ||

| By Form | Spoonable | |

| Drinkable | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the Greek yogurt market be by 2031?

The Greek yogurt market is set to reach USD 30.24 billion by 2031, expanding from USD 20.26 billion in 2026 at an 8.37% CAGR.

Which region is growing fastest for Greek yogurt?

Asia-Pacific shows the highest upside, projected at a 9.68% CAGR through 2031, led by China, India and Indonesia.

What product type is expected to grow quickest?

Unflavored Greek yogurt leads with a 9.83% CAGR through 2031.

Why is non-fat Greek yogurt gaining share?

GLP-1 weight-management users prioritize high-protein, low-calorie foods, driving non-fat SKUs at a 10.34% CAGR.

Which sales channel will post the strongest growth?

Online retail is expected to rise at a 11.05% CAGR as direct-to-consumer bundles and grocery apps normalize chilled delivery.

Page last updated on: