Soybean Oil Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 43.87 Billion |

| Market Size (2031) | USD 57.66 Billion |

| Growth Rate (2026 - 2031) | 5.62% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Soybean Oil Market Analysis by Mordor Intelligence

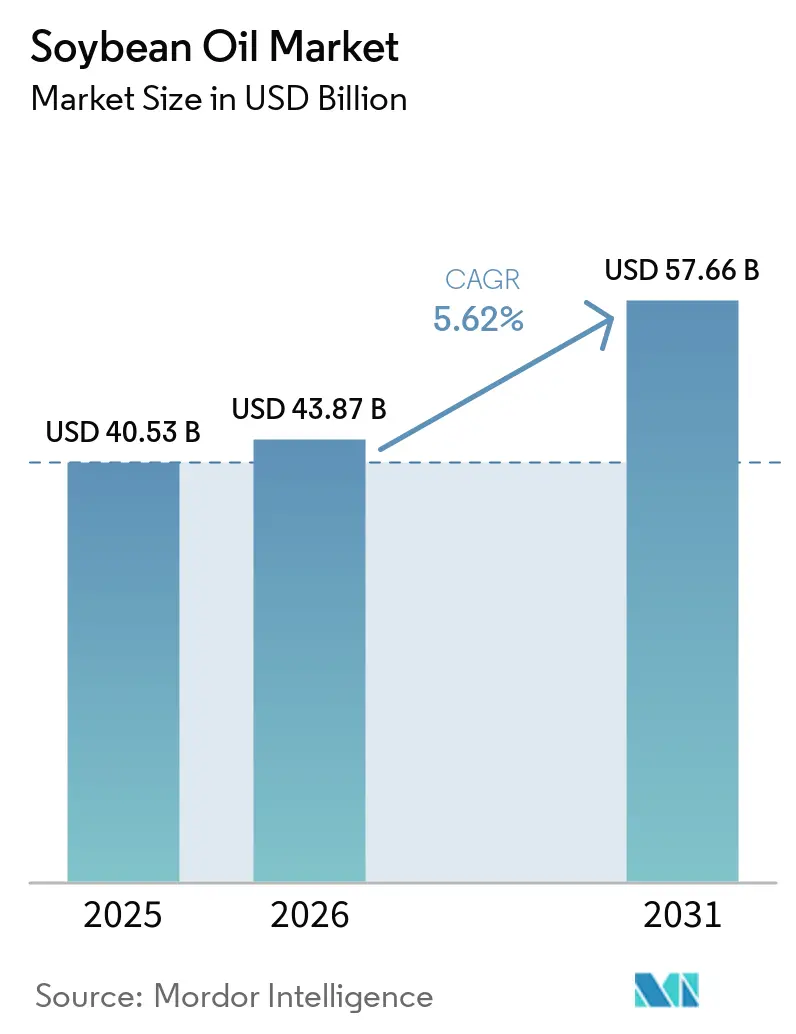

The soybean oil market size was valued at USD 40.53 billion in 2025 and estimated to grow from USD 43.87 billion in 2026 to reach USD 57.66 billion by 2031, at a CAGR of 5.62% during the forecast period (2026-2031). Rising demand from renewable diesel refineries, plant-based food manufacturers, and industrial oleochemical producers is widening end-use diversity, while the new EU Deforestation Regulation is pushing retailers and processors to secure traceable, certified supply chains. Additional crushing capacity in Brazil and Argentina is balancing slower North American expansion, keeping global production on an upward trajectory. Technological gains such as high-oleic cultivars and enzyme-assisted extraction are lowering processing costs and extending product shelf life. Renewable energy mandates across the United States, Canada, Brazil, and the European Union guarantee a structural demand floor for biofuel feedstock, buffering the soybean oil market against cyclical swings in food consumption.

Key Report Takeaways

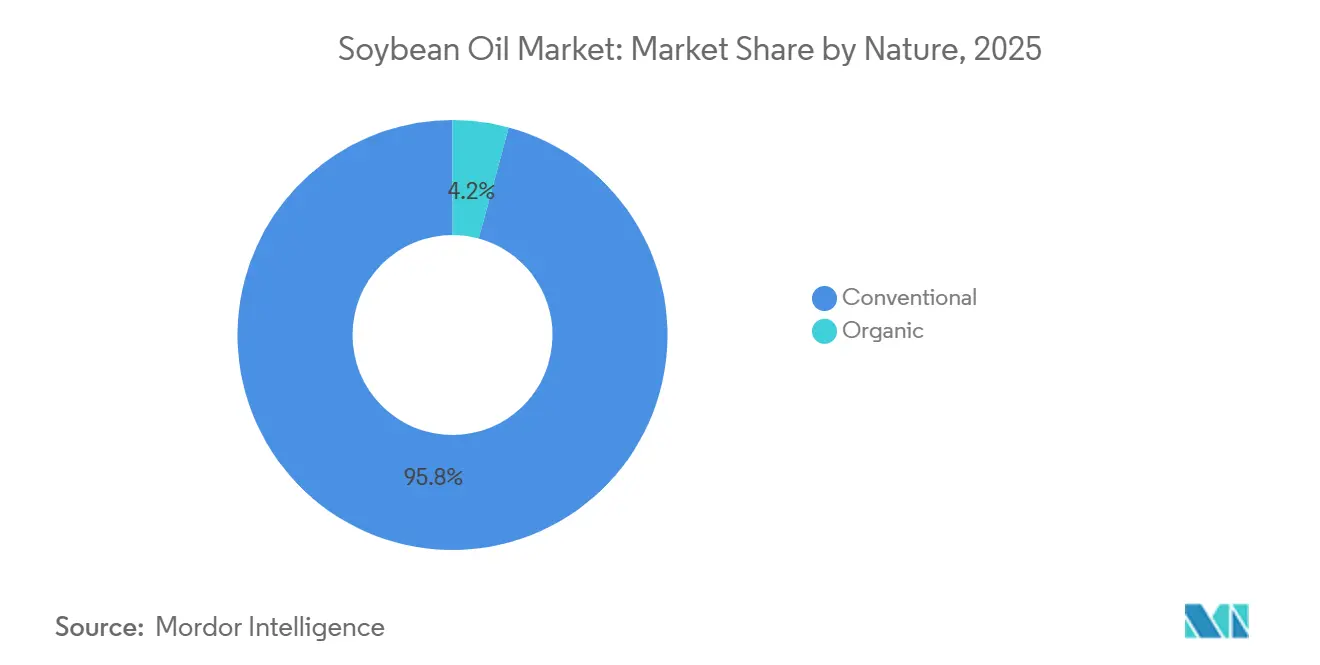

- By nature, conventional soybean oil led with 95.78% of the soybean oil market share in 2025, while organic variants are advancing at a 7.46% CAGR through 2031.

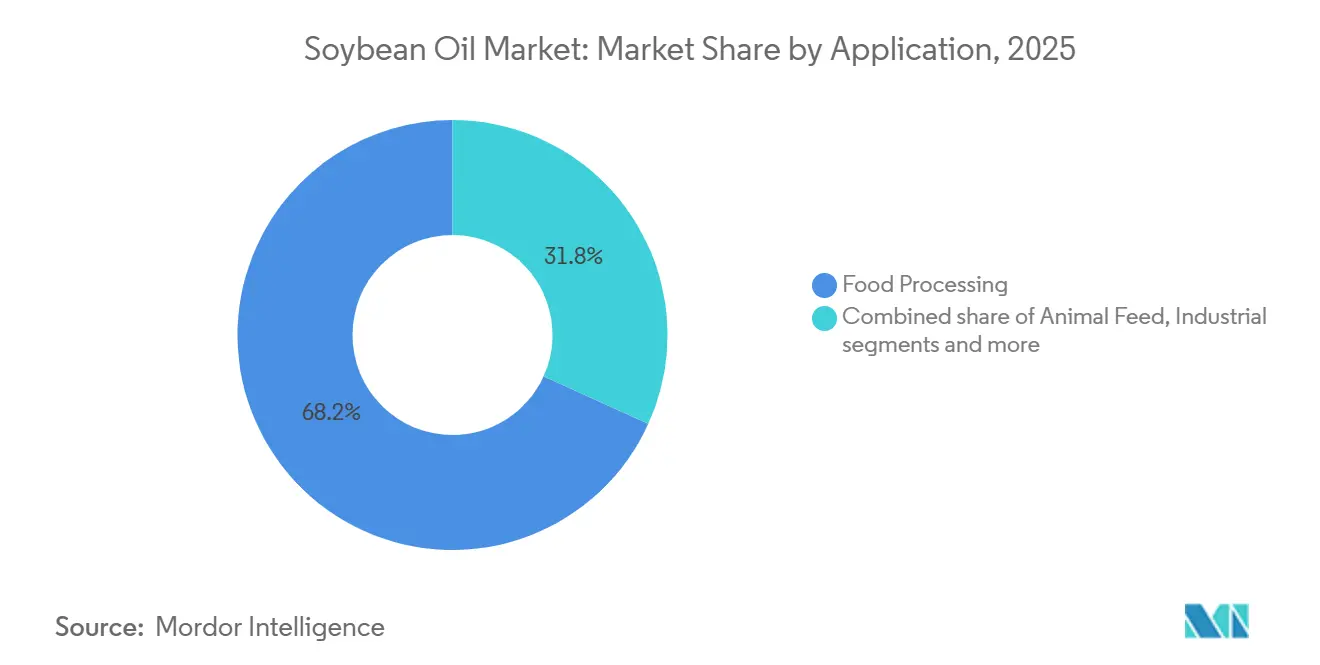

- By end user, food processing accounted for 68.23% of the soybean oil market in 2025, whereas industrial applications are projected to register the fastest expansion at a 5.82% CAGR between 2026 and 2031.

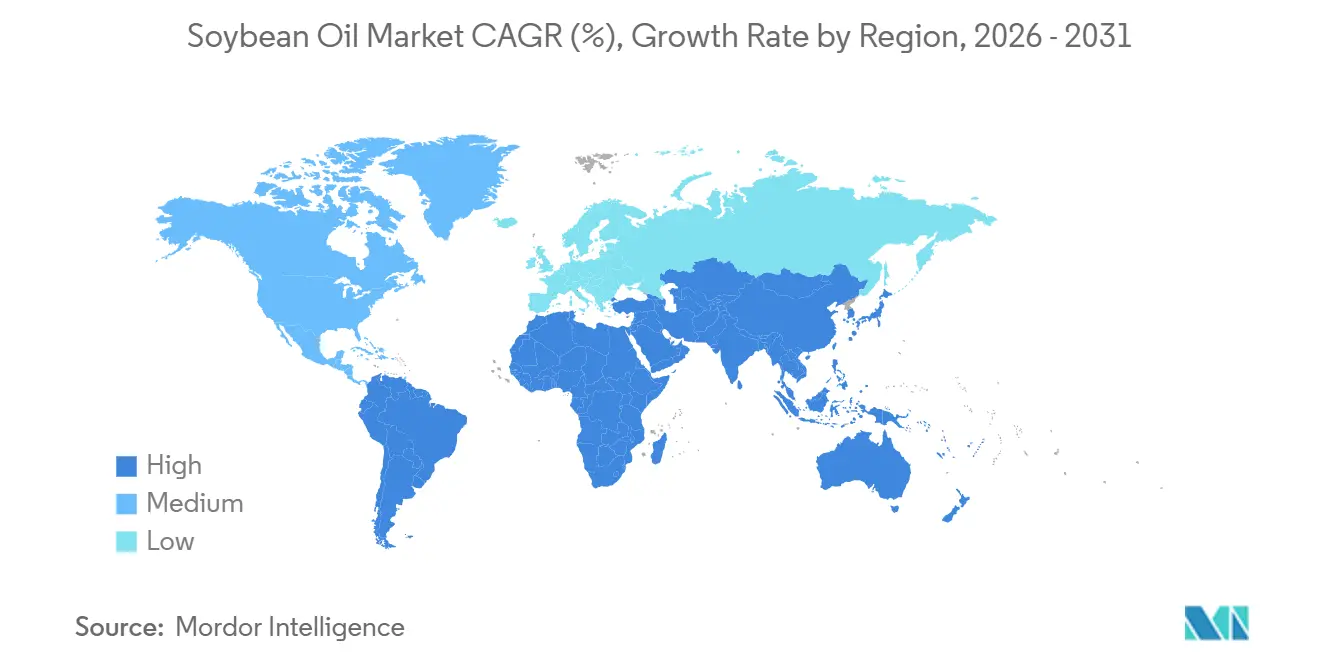

- By geography, Asia-Pacific commanded 42.77% of the 2025 global volume, yet the Middle East and Africa region is poised to post the highest regional CAGR of 6.69% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Soybean Oil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing global consumption of processed and convenience foods | +1.2% | Asia-Pacific, North America | Medium term (2-4 years) |

| Increasing protein demand supporting soybean crushing activities | +1.5% | China, India, Southeast Asia | Long term (≥ 4 years) |

| Technological advancements in soybean cultivation and processing | +0.8% | North, South America | Medium term (2-4 years) |

| Expansion of plant-based and vegan food markets | +0.9% | North America, Europe | Short term (≤ 2 years) |

| Growth in industrial applications | +1.0% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Government policies promoting renewable energy supporting soybean oil demand | +1.3% | North America, Europe, Brazil | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Global Consumption of Processed and Convenience Foods

Urbanization and dual-income households are accelerating demand for shelf-stable packaged foods that rely on refined soybean oil for texture, mouthfeel, and extended shelf life. The Food and Agriculture Organization documented that global per-capita consumption of vegetable oils rose from 24.1 kilograms in 2020 to 26.3 kilograms in 2025, with soybean oil accounting for 28% of the incremental volume as bakery manufacturers reformulated products to eliminate partially hydrogenated fats following trans-fat bans in over 50 countries[1]Source: Food and Agriculture Organization, “Oilcrops Market Summary,” FAO.org. Snack food producers in India and Indonesia are shifting from palm olein to soybean oil blends to meet consumer preferences for "heart-healthy" labeling, even though clinical evidence for differential cardiovascular outcomes remains contested. Foodservice chains in North America increased soybean oil purchases by 11% in 2025 as quick-service restaurants adopted high-oleic varieties that withstand 30% more frying cycles than commodity grades, reducing oil replacement frequency and waste disposal costs, according to the USDA Economic Research Service. Compliance with Codex Alimentarius standards for edible fats ensures that refined soybean oil meets international trade requirements, facilitating cross-border shipments to Middle Eastern and African markets where domestic oilseed production lags consumption growth.

Increasing Protein Demand Supporting Soybean Crushing Activities

Rising livestock and aquaculture production in Asia generates sustained demand for soybean meal, the primary co-product of oil extraction, creating an economic incentive for crushers to maximize throughput even when oil margins compress. China imported 100 million metric tons of soybeans in 2025, with 78% destined for domestic crushing to supply hog and poultry feed, thereby producing 18 million metric tons of soybean oil as a byproduct that either displaces palm oil imports or flows into biodiesel blending, according to China Customs. India's National Centre for Cold Chain Development projected that poultry meat consumption will grow at 6.8% annually through 2030, necessitating an additional 4 million metric tons of soybean meal and yielding 800,000 metric tons of oil that will pressure domestic prices unless export channels expand. The protein-oil value chain linkage means that soybean oil supply is partially inelastic to oil-specific demand signals; crushers prioritize meal margins, and oil becomes a residual output whose price must clear the market. This dynamic explains why soybean oil prices in Brazil traded at a 15% discount to Chicago Board of Trade futures during the first quarter of 2025, as record crush runs to meet Chinese meal demand flooded domestic oil inventories.

Technological Advancements in Soybean Cultivation and Processing

Precision agriculture tools, variable-rate seeding, satellite-guided nutrient application, and predictive disease modeling lifted average U.S. soybean yields from 50.2 bushels per acre in 2020 to 52.8 bushels in 2025, increasing oil output per hectare without expanding planted area, according to the USDA National Agricultural Statistics Service[2]Source: United States Department of Agriculture, “Crop Production Statistics,” USDA.gov. Breeders commercialized high-oleic soybean varieties that contain 75% oleic acid versus 23% in conventional beans, extending frying oil life by 50% and enabling premium pricing in foodservice channels; Corteva Agriscience reported that Plenish high-oleic soybean acreage in the United States reached 1.2 million acres in 2025, triple the 2023 level. Solvent extraction efficiency improvements, counter-current washing, membrane filtration for hexane recovery, and enzyme-assisted aqueous extraction pilots reduced processing energy consumption by 12% between 2020 and 2025, lowering the carbon intensity of soybean oil and enhancing eligibility for renewable fuel incentives, according to the Journal of the American Oil Chemists' Society. Adoption of near-infrared spectroscopy for real-time oil content measurement during crushing enables processors to optimize press settings and maximize oil yield, a capability that smaller regional plants are integrating to compete with multinational-scale advantages.

Expansion of Plant-Based and Vegan Food Markets

Meat and dairy analog manufacturers are formulating products with soybean oil to deliver fatty mouthfeel and emulsification properties, creating a niche demand segment that tolerates higher prices than commodity frying applications. Unilever disclosed in its 2025 sustainability report that plant-based burger patties and dairy-free spreads consumed 45,000 metric tons of soybean oil globally, a 34% increase from 2024, as the company reformulated recipes to replace coconut oil and reduce saturated fat content. Retail sales of plant-based foods in Europe grew 18% in 2025, with soybean oil serving as a cost-effective alternative to sunflower and rapeseed oils that faced supply disruptions from the Black Sea region, according to the European Plant-Based Foods Association. Certification under ProTerra or the Round Table on Responsible Soy provides traceability assurances that appeal to brands targeting environmentally conscious consumers, though the premium for certified oil, approximately USD 50 per metric ton above conventional grades, limits adoption to premium product lines. The segment's growth trajectory depends on whether plant-based food penetration can exceed 5% of total protein consumption in major markets, a threshold that would require soybean oil volumes to double from current specialty application levels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying competition from alternative vegetable oils | -1.1% | Asia-Pacific, Europe | Medium term (2-4 years) |

| Volatility in soybean prices and supply | -0.9% | Global; import-dependent economies | Short term (≤ 2 years) |

| High production costs impact profit margins | -0.7% | North America, Europe | Medium term (2-4 years) |

| Limited availability of arable land restricts production | -0.5% | South & North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying Competition from Alternative Vegetable Oils

Palm oil, canola, and sunflower oil producers are expanding output and undercutting soybean oil pricing in key applications, eroding market share in price-sensitive segments such as foodservice frying and industrial lubricants. Indonesia and Malaysia increased combined palm oil production in 2025, with refined palm olein trading at a USD 120 per metric ton discount to soybean oil in Rotterdam spot markets during the second half of 2025. Canola crush capacity in Canada expanded by 1.2 million metric tons in 2024-2025 as Richardson International and Viterra commissioned new facilities in Saskatchewan, positioning canola oil to capture incremental demand from renewable diesel refiners who value its lower saturated fat content and superior cold-weather performance. Sunflower oil exports from Russia and Ukraine rebounded to 6.8 million metric tons in the 2024/2025 marketing year following the renewal of the Black Sea Grain Initiative, restoring supply to European and Middle Eastern buyers who had temporarily substituted with soybean oil during the 2022-2023 disruption, according to the USDA Foreign Agricultural Service. The substitution threat is most acute in markets with weak consumer preferences for specific oil types, where procurement decisions hinge on delivered cost per unit of functionality rather than on origin or sustainability attributes.

Volatility in Soybean Prices and Supply

Weather-driven yield variability, geopolitical trade tensions, and speculative commodity flows generate price swings that compress processor margins and deter long-term supply contracts, undermining investment in crush capacity and refining infrastructure. Chicago Board of Trade soybean oil futures traded in a USD 450 per metric ton range during 2025, oscillating between USD 980 and USD 1,430 as drought in Argentina, tariff threats between the United States and China, and shifts in renewable diesel feedstock preferences whipsawed market sentiment. Brazil's 2024/2025 soybean harvest fell 6% short of initial forecasts due to La Niña-induced rainfall deficits in Mato Grosso and Rio Grande do Sul, tightening global stocks-to-use ratios to 26.4%, the lowest level since 2020/2021, and triggering a 19% price spike in March 2025. Processors operating on thin crush margins, typically USD 30-50 per metric ton, face working capital strain when soybean costs surge faster than oil and meal prices adjust, forcing some regional plants to idle capacity during periods of negative crush spreads. The volatility discourages food manufacturers from committing to fixed-price soybean oil contracts beyond 6-month horizons, fragmenting the market and preventing the price discovery efficiency that would support stable investment returns.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Nature: Organic Certification Drives Niche Premiums

Conventional soybean oil accounted for 95.78% of the market in 2025, reflecting its cost advantage and broad acceptance across foodservice, industrial, and retail channels, while organic soybean oil is expanding at a 7.46% CAGR through 2031 as European retailers and North American natural food brands mandate certified deforestation-free and non-GMO sourcing. Organic acreage in the United States reached 210,000 acres in 2025, up from 175,000 acres in 2023, yet still represents less than 0.3% of total soybean plantings, constraining supply and sustaining price premiums of USD 400-600 per metric ton above conventional grades, according to the USDA National Organic Program. The European Union's organic food market grew 12% in 2025, with soybean oil used in certified organic spreads, dressings, and infant formula commanding shelf prices 30-50% above conventional equivalents, a margin that incentivizes processors to segregate organic crush runs despite the logistical complexity, according to the European Commission's Organic Farming. Conventional oil benefits from economies of scale in crushing, refining, and distribution, allowing multinational processors to deliver consistent quality at competitive pricing to mass-market customers who prioritize functionality over sustainability attributes.

Organic certification under USDA National Organic Program, EU Organic Regulation, or equivalent standards requires third-party verification of non-GMO seed, synthetic pesticide-free cultivation, and segregated handling throughout the supply chain, adding USD 80-120 per metric ton in compliance and audit costs that smaller processors struggle to absorb. ProTerra and Round Table on Responsible Soy certifications offer intermediate sustainability assurances, non-deforestation sourcing, fair labor practices, reduced agrochemical use, without the full organic premium, creating a tiered market where buyers select the certification level aligned with their brand positioning and willingness to pay. Wilmar International reported in its 2025 sustainability update that 18% of its soybean oil volumes carried third-party sustainability certification, up from 11% in 2023, as European customers responded to the EU Deforestation Regulation that prohibits imports linked to forest conversion after December 2020 Wilmar Sustainability Report 2025. The organic segment's 7.46% CAGR will likely moderate if conventional high-oleic varieties achieve functional parity in frying and baking applications, reducing the performance justification for organic premiums.

By End User: Industrial Gains Outpace Food Processing

Food processing commanded 68.23% share in 2025, anchored by bakery, confectionery, and spreads applications where soybean oil delivers neutral flavor, stable emulsification, and compliance with trans-fat elimination mandates, yet industrial applications are growing at 5.82% CAGR through 2031 as renewable diesel refiners, oleochemical producers, and bioplastic manufacturers diversify feedstock portfolios. Margarine and butter-substitute manufacturers preferred soybean oil's low saturated fat content and its ability to crystallize into plastic textures, as partially hydrogenated alternatives were phased out. Bakery and confectionery is driven by cake mixes, cookies, and pastry fillings that require oils with minimal flavor interference and oxidative stability during shelf storage. Foodservice with quick-service restaurants and institutional kitchens adopting high-oleic soybean oil to extend frying cycles and reduce oil disposal frequency, a shift accelerated by waste management cost inflation in urban markets.

Retail sales of bottled soybean oil grew modestly in 2025, constrained by consumer preference for olive, avocado, and coconut oils in developed markets, while animal feed applications, primarily soybean oil added to poultry and swine rations for energy density, a share that fluctuates with feed ingredient prices and livestock herd sizes. Industrial applications, encompassing biodiesel, renewable diesel, oleochemicals, and technical uses, and are projected to grow in share by 2031 as renewable fuel mandates tighten and petrochemical substitution accelerates. Archer Daniels Midland disclosed in its 2025 10-K filing that renewable diesel feedstock sales grew 31% year-over-year, now representing 14% of its North American soybean oil volumes, as refiners blended soybean oil with used cooking oil and tallow to optimize carbon intensity scores under California's Low Carbon Fuel Standard. The "Others" category, including cosmetics, pharmaceuticals, and specialty lubricants, a niche segment where soybean oil's hypoallergenic properties and biodegradability justify premium pricing but face competition from specialty oils like jojoba and argan.

Geography Analysis

Asia-Pacific held 42.77% market share in 2025, propelled by China's 18.5 million metric ton annual soybean crushing capacity and India's 6.2% annual growth in per-capita edible oil consumption, yet the region's heavy reliance on imported soybeans, China sourced 85% of its beans from Brazil and the United States, exposes crushers to freight cost volatility and geopolitical trade risks. China's State Administration for Market Regulation tightened quality standards for refined soybean oil in January 2025, mandating maximum peroxide values of 5 milliequivalents per kilogram and banning certain antioxidant additives, forcing domestic refiners to upgrade deodorization and filtration equipment at an estimated industry-wide cost of USD 340 million, according to the China State Administration for Market Regulation. India's soybean oil imports reached 3.8 million metric tons in the 2024/2025 marketing year, supplementing domestic production of 1.2 million metric tons, as government policies oscillated between increasing import tariffs to protect farmers and reducing them to contain food inflation, according to the Government of India, Ministry of Commerce[3]Source: Government of India Ministry of Commerce, “Trade Data,” commerce.gov.in . Southeast Asian nations, including Indonesia, Vietnam, and Thailand, are expanding domestic crushing capacity to reduce dependence on refined oil imports, with Vietnam commissioning 2 new facilities totaling 1.5 million metric tons annual capacity in 2024-2025, as stated by the Vietnam Ministry of Agriculture and Rural Development. Japan and South Korea, mature markets with stable consumption, are shifting procurement toward certified sustainable soybean oil to align with corporate ESG commitments, creating differentiated demand that commands USD 30-50 per metric ton premiums.

North America and South America collectively supplied signifciant share of global soybean oil exports in 2025, with the United States exporting 1.4 million metric tons, primarily to Mexico, Central America, and the Caribbean, while Brazil and Argentina shipped 2.8 million metric tons to China, India, and the European Union. Brazil's soybean oil production reached 10.2 million metric tons in 2025, with 65% consumed domestically for biodiesel blending under the B14 mandate that requires 14% biodiesel content in diesel fuel, a policy that absorbed incremental crush output and supported domestic oil prices, according to the Brazilian National Agency of Petroleum, Natural Gas and Biofuels[4]Source: Brazilian Institute of Geography and Statistics, “Agricultural Statistics,” ibge.gov.br. Argentina's export tax structure, 33% on soybeans versus 31% on soybean oil, incentivizes domestic crushing, resulting in 5.1 million metric tons of oil production in 2025, of which 4.3 million metric tons were exported, making Argentina the world's largest soybean oil exporter despite ranking third in soybean production, according to the Buenos Aires Grain Exchange. The United States diverted an increasing share of soybean oil to renewable diesel production, with domestic biofuel consumption rising to 5.2 million metric tons in 2025 from 3.8 million metric tons in 2023, tightening exportable supplies and elevating domestic prices relative to South American origins, as mentioned by USDA Economic Research Service.

The European Union's Deforestation Regulation, effective December 2024, requires importers to demonstrate through geolocation data that soybeans were not grown on land deforested after December 2020, a compliance burden that favored suppliers with established traceability systems and disadvantaged smaller Brazilian exporters lacking satellite monitoring capabilities. Middle East and Africa is expanding at 6.69% CAGR through 2031, driven by population growth averaging 2.3% annually, rising incomes that shift diets toward processed foods, and government food security initiatives that subsidize edible oil imports to stabilize retail prices. Egypt imported 680,000 metric tons of soybean oil in 2025, funded partially through World Bank food security loans, while Saudi Arabia and the United Arab Emirates are investing in domestic crushing facilities to process imported soybeans and reduce dependence on refined oil shipments. Nigeria's soybean oil consumption grew 14% in 2025 as local processors expanded capacity to serve the West African market, though infrastructure constraints, inadequate port facilities, unreliable electricity, and limited cold storage, continue to elevate logistics costs and favor imported refined oil over domestic crushing in coastal regions.

Competitive Landscape

The soybean oil market exhibits moderate concentration, indicating that the top 5 players, Bunge, Cargill, Wilmar, ADM, and Richardson, control a significant portion of global crushing capacity yet compete against a fragmented base of regional cooperatives, state-owned enterprises, and independent processors who leverage local sourcing advantages and government support. Strategic patterns emphasize vertical integration, with leading firms securing soybean supply through farmer contracts and origination networks, operating crush plants proximate to production regions to minimize freight costs, and investing in downstream refining and specialty oil production to capture value-added margins. Bunge's January 2025 announcement of a USD 200 million expansion at its Morrinhos facility in Brazil exemplifies the capacity race in South America, where proximity to the world's largest soybean production region and favorable export logistics to Asia and Europe justify capital deployment despite cyclical crush margin volatility.

Cargill's renewable diesel feedstock sales, which grew 28% in 2025 to represent 12% of North American soybean oil volumes, illustrate how incumbents are pivoting toward industrial applications that offer more stable margins and long-term offtake contracts compared to volatile food commodity markets. White-space opportunities include certified organic and high-oleic soybean oil for premium food applications, enzymatic and aqueous extraction technologies that reduce hexane use and improve sustainability profiles, and direct-to-consumer retail brands that bypass traditional distribution channels. Emerging disruptors such as regional cooperatives in Brazil, Granol S/A expanded its crushing capacity by 15% in 2024 to serve domestic biodiesel blenders, are leveraging farmer loyalty and local market knowledge to compete against multinational scale.

Technology-focused entrants are piloting membrane filtration and supercritical CO2 extraction to produce pharmaceutical-grade soybean oil that commands 3-5 times the price of refined commodity grades. The Round Table on Responsible Soy certified 4.2 million metric tons of soybean production in 2025, up from 3.1 million metric tons in 2023, creating a traceable supply pool that processors can market to European and North American buyers under sustainability premiums, though the certification's 2-3% adoption rate limits its near-term market impact. Patent filings in 2024-2025 concentrated on enzyme-assisted oil extraction processes that increase yield by 2-4 percentage points and reduce energy consumption, with ADM, Bunge, and Wilmar collectively holding 18 active patents in this domain, signaling a technology arms race to lower processing costs and differentiate on environmental footprint.

Soybean Oil Industry Leaders

Bungee Limited

Cargill Incorporated

Wilmar International Ltd

Archer-Daniels-Midland Company,

Richardson International Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Scoular has launched a new canola and soybean oilseed crush facility in Goodland, Kansas. Designed to process 11 million bushels of oilseeds annually, the facility enhances market opportunities for local soybean farmers while increasing the region's processing capacity.

- July 2024: Louis Dreyfus announced the relaunch of its edible oil brand, ‘Vibhor,’ marking a significant step in its expansion of the product portfolio. The revamped product line included a variety of oils such as soybean, palmolein, cottonseed, and mustard oils, alongside premium vanaspati.

- March 2024: Nabil Group introduced new soybean oil brand, Foodella, during a formal launch event held at Padma Hall of the Grand Riverview Hotel in Rajshahi. The event marked a significant milestone for the company as it expands its product portfolio in the edible oil market.

Global Soybean Oil Market Report Scope

Soybean oil is a vegetable oil extracted from soybean seeds. The soybean oil market is segmented by nature, application, and geography. By nature, it is segmented into organic and conventional. By application, the market is segmented into the food processing, foodservice, animal feed, industrial, and other applications. Food processing is further segmented into spreads, bakery and confectionery, and other food processing applications. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, the Middle-East, and Africa. The market value is provided in USD million, and the volume is provided in liters.

| Conventional |

| Organic |

| Food Processing | Spreads |

| Bakery and Confectionery | |

| Other | |

| Foodservice | |

| Retail | |

| Animal Feed | |

| Industrial | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Norway | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| Vietnam | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Nature | Conventional | |

| Organic | ||

| By End User | Food Processing | Spreads |

| Bakery and Confectionery | ||

| Other | ||

| Foodservice | ||

| Retail | ||

| Animal Feed | ||

| Industrial | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Norway | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| Vietnam | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the soybean oil market in 2026?

It is estimated at USD 43.87 billion, on track to reach USD 57.66 billion by 2031.

What is driving soybean oil demand in renewable fuels?

National mandates such as the U.S. Renewable Fuel Standard and California’s Low Carbon Fuel Standard channel soybean oil into biodiesel and renewable diesel, providing a stable industrial demand base.

Which region consumes the most soybean oil?

Asia-Pacific leads with 42.77% of 2025 global volume, thanks to China’s massive crushing sector and India’s rising edible-oil intake.

Why is organic soybean oil growing faster?

Retailers in Europe and North America are tightening sustainability standards, and certified organic or deforestation-free supply earns price premiums that attract processors.

How are technology advances affecting production costs?

High-oleic genetics, enzyme-assisted extraction, and membrane filtration raise oil yields and cut energy use, lowering unit costs and carbon intensity.

Page last updated on: