Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

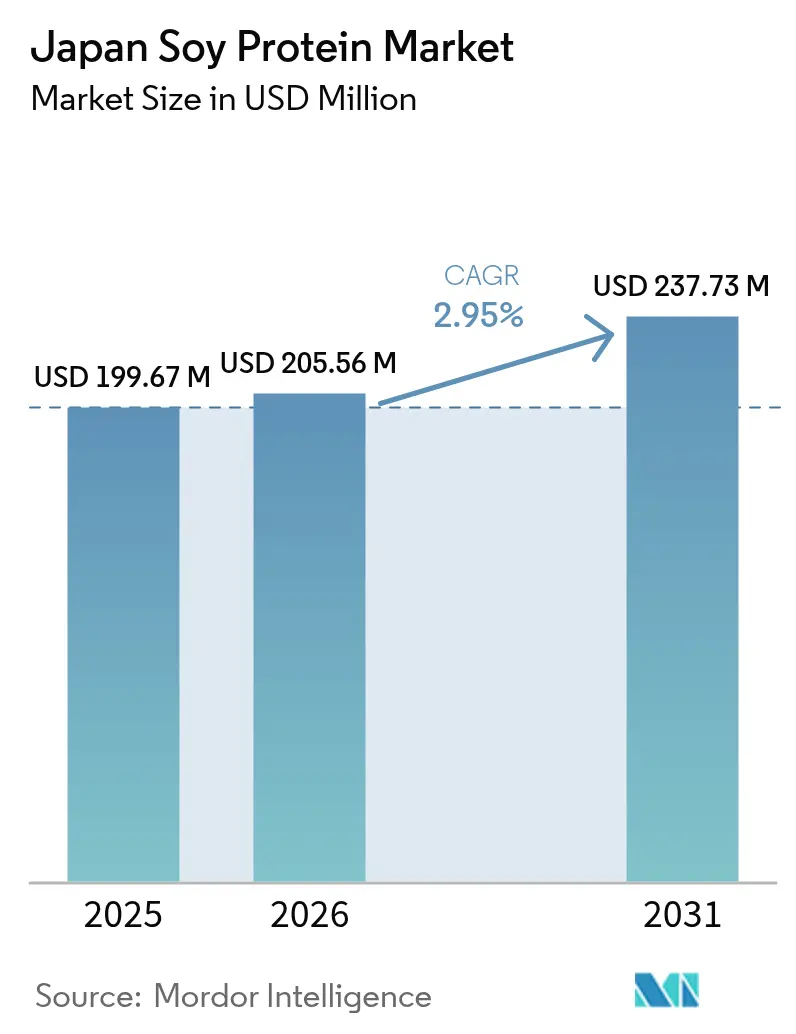

| Base Year Market Size (2025) | USD 199.67 Million |

| Market Size (2026) | USD 205.56 Million |

| Market Size (2031) | USD 237.73 Million |

| Growth Rate (2026 - 2031) | 2.95% CAGR |

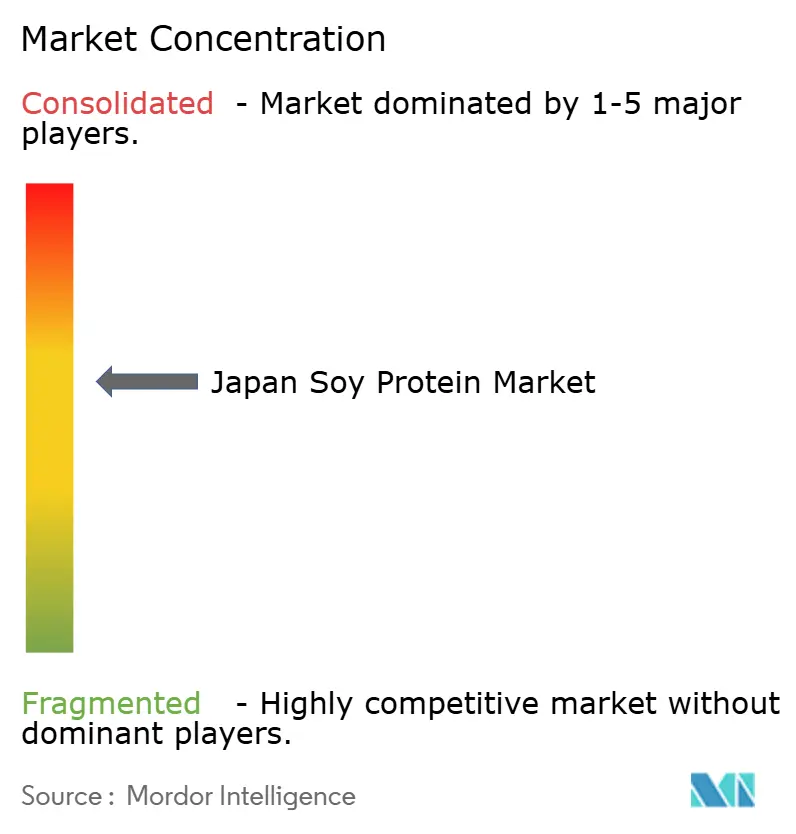

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Soy Protein Market Analysis by Mordor Intelligence

Japan soy protein market size in 2026 is estimated at USD 205.56 million, growing from 2025 value of USD 199.67 million with 2031 projections showing USD 237.73 million, growing at 2.95% CAGR over 2026-2031. The market growth is driven by Japan's aging demographic, rising health consciousness among consumers, and government initiatives to improve food self-sufficiency. Market expansion is constrained by dependence on soybean imports and increasing competition from alternative plant proteins. The demand for cost-effective, digestible, high-quality protein has increased the adoption of soy protein isolates in meat alternatives, beverages, and clinical nutrition products. The market demonstrates higher uptake of enzymatically hydrolyzed soy proteins, specifically in addressing nutritional requirements of elderly populations affected by sarcopenia. Companies are investing in research and development to enhance flavor masking, texture improvement, and allergen reduction to meet local preferences.

Key Report Takeaways

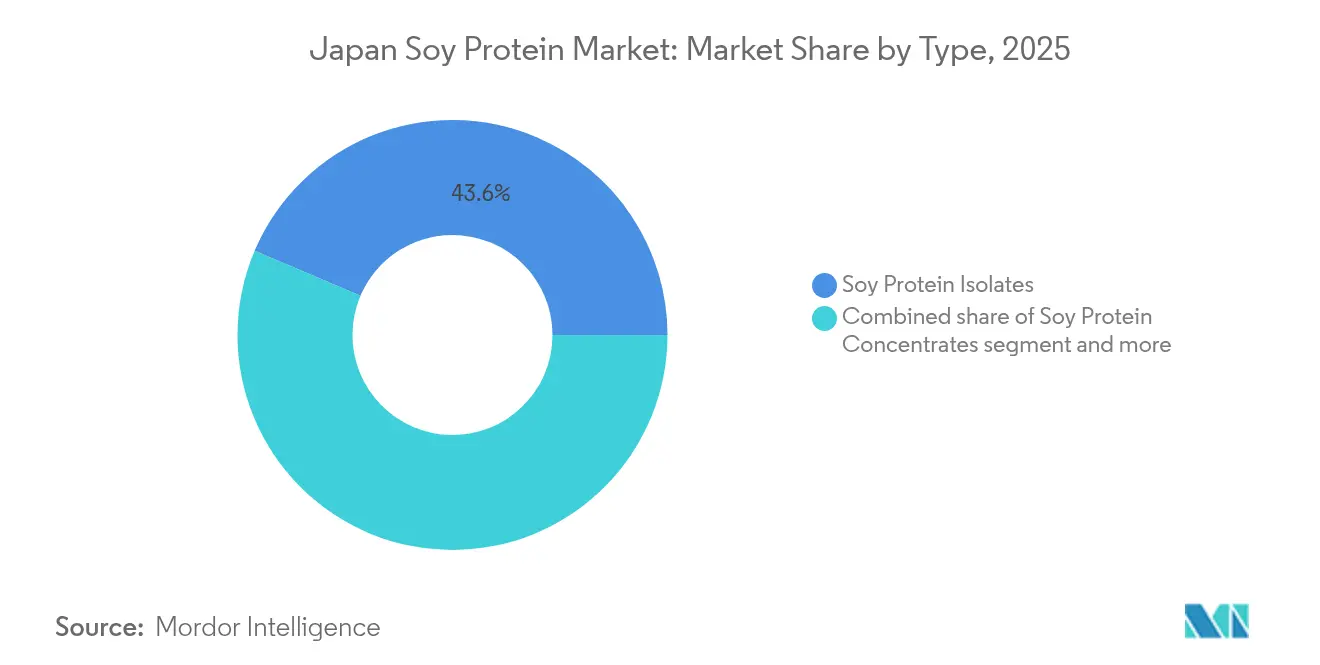

- By type, soy protein isolates led with 43.60% Japan soy protein market share in 2025, and hydrolysed soy protein records the fastest growth at a 3.42% CAGR for 2026-2031.

- By nature, the conventional segment dominated with a 90.85% share in 2025, whereas organic soy protein is projected to expand at a 4.92% CAGR to 2031.

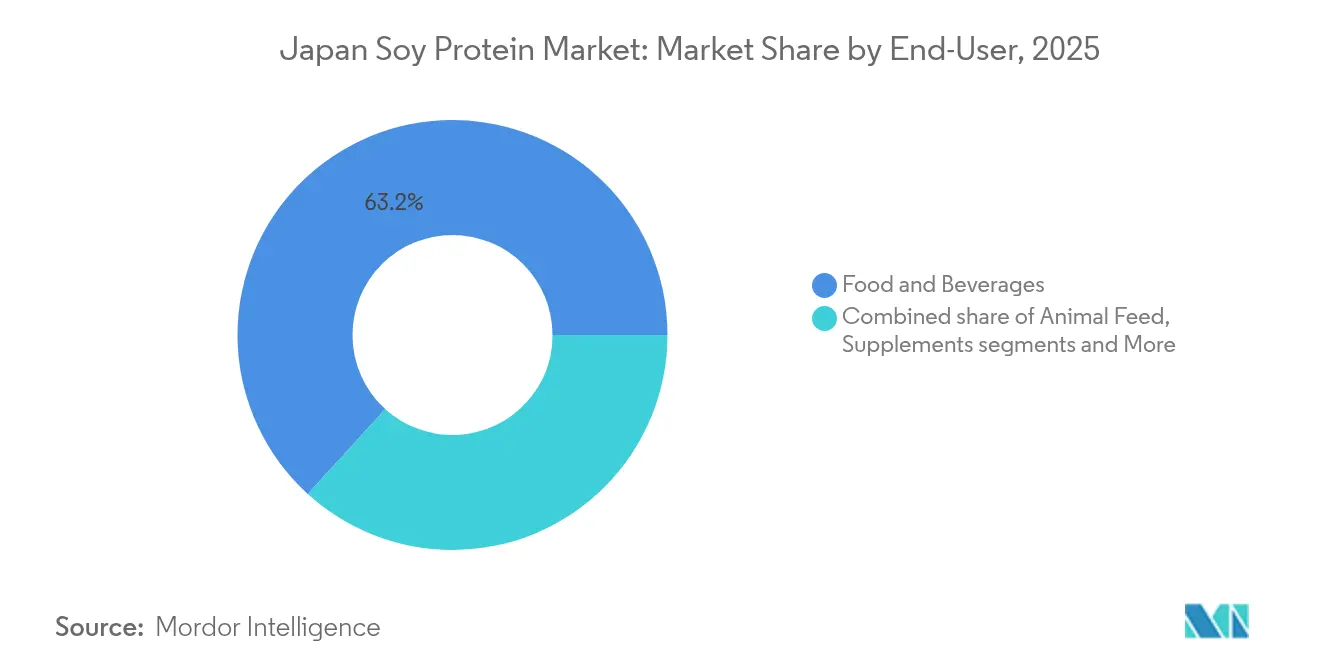

- By end-user, food and beverages commanded 63.25% of the Japan soy protein market size in 2025; the supplements segment is advancing at a 3.91% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Soy Protein Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Aging population and muscle-health focus | +0.7% | National, concentrated in urban centres | Long term (≥ 4 years) |

| Rising flexitarian eating habits | +0.5% | Tokyo, Osaka, Kyoto | Medium term (2-4 years) |

| Government self-sufficiency programmes | +0.4% | National, especially agricultural regions | Long term (≥ 4 years) |

| Ready-to-eat protein-enriched meals | +0.3% | Urban areas | Short term (≤ 2 years) |

| Convenience-food expansion | +0.3% | Metropolitan zones | Medium term (2-4 years) |

| Processing-technology advances | +0.2% | Industrial hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging population and muscle-health focus

Japan's aging population represents the highest elderly proportion globally, creating substantial market opportunities in protein-enriched clinical nutrition. This demographic transformation drives manufacturers to develop specialized soy protein products for sarcopenia prevention and management. Food companies are actively reformulating their product portfolios to address age-specific nutritional requirements, establishing sustained market growth. The increasing adoption of hydrolyzed soy proteins reflects their enhanced digestibility and absorption characteristics, particularly beneficial for elderly consumers with diminished digestive capabilities. This trend shapes product development strategies across the clinical nutrition segment, influencing both domestic and international market dynamics.

Rising flexitarian eating habits

Japanese urban households are increasingly adopting flexitarian diets by substituting plant-based proteins for animal protein in one or two meals per week. Young consumers associate plant proteins with environmental sustainability and weight control, and favor brands that combine authenticity with convenience. Manufacturers have responded by introducing hybrid products such as patties and dumplings that combine chicken or seafood with soy concentrates, reducing fat content while maintaining price points. This approach extends soy protein's market reach beyond the vegan segment in Japan, increasing the total addressable market. Young consumers associate plant protein with eco-friendliness and weight control, favoring brands that balance authenticity with contemporary convenience. In turn, manufacturers are introducing hybrid patties and dumplings, combining chicken or seafood with soy concentrates. This innovation reduces fat and saturated fat content without raising prices. By adopting this broader strategy, soy is now appealing not just to strict vegans, but to a wider audience, thereby enlarging the potential market for soy protein in Japan.

Government self-sufficiency programmes

The Japanese Ministry of Agriculture, Forestry and Fisheries (MAFF) has implemented a Basic Plan for Food, Agriculture and Rural Areas that focuses on increasing domestic soybean production. The plan includes subsidies for high-protein soybean varieties, automation equipment grants, and research funding for improved farming methods. Pilot farms in Hokkaido are growing specialized soybean varieties for protein extraction, achieving yields of 3.4 tonnes per hectare compared to the national average of 2.2 tonnes[1]Ministry of Agriculture, Forestry and Fisheries, “Basic Plan for Food, Agriculture and Rural Areas,” maff.go.jp. These initiatives reduce exposure to international commodity price fluctuations while enhancing product traceability, enabling manufacturers to market products with "Japanese-grown soy" labels that appeal to consumers concerned about food security. According to JPPFA, the Domestic production volume of soy proteins in Japan in 2024 was estimated to be ~41 '000 tons 2024 [2]JPPFA, “Production Volume of Soy Proteins in Japan,”protein.or.jp.

Processing technology advances

Ajinomoto's transglutaminase enzyme creates networks that replicate the texture of minced pork, while Fuji Oil's solvent-free extraction at low temperatures maintains natural isoflavones that attract health-focused consumers. These technological developments reduce the functional differences between soy and animal proteins, enabling broader applications from bakery products to sports nutrition. Production costs have improved, with enzymatically modified isolates now manufactured at lower costs compared to previous years, helping maintain profit margins despite inflation. Innovations are bridging the functional gaps between soy and animal proteins, easing formulation challenges. This expansion now spans applications, from bakery fillings to sports gels. Additionally, cost dynamics are shifting: factory trials reveal that enzymatically modified isolates are now produced at a 12% lower unit cost than five years prior, bolstering margin stability amidst inflationary pressures.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High dependence on imported soybeans | -0.7% | National | Medium term (2-4 years) |

| Persisting soy allergen concern | -0.4% | National | Long term (≥ 4 years) |

| Competition from alternative plant proteins | -0.6% | National | Long term (≥ 4 years) |

| Price volatility of soybeans | -0.5% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High dependence on imported soybeans

Japan's soybean supply chain remains vulnerable due to its substantial reliance on imports from the United States, Brazil, and Canada. The country's dependence on international markets makes it susceptible to supply disruptions and geopolitical tensions, which became evident during recent trade disputes and weather-related challenges in commodity markets. While Japan's limited agricultural land continues to restrict domestic production despite government support, companies are taking proactive steps to build more resilient supply chains. These businesses are forming long-term partnerships with international suppliers and investing in vertical integration projects. Significant initiative involves the collaboration between Protein Industries Canada, Alinova Canada Inc., and Marusan Ai Co., who are working together to build a specialized soy processing facility in Ontario dedicated to producing soy milk powder for Japanese consumers. The Observatory of Economic Complexity (OEC) reports that Japan's soybean imports reached 288 billion yen in 2024, with the United States, Brazil, and Canada maintaining their positions as the main suppliers [3]Observatory of Economic Complexity (OEC), “Soybeans in Japan,” oec.world.

Price volatility of soybeans

Global soybean price volatility presents a persistent challenge for Japanese soy protein manufacturers. The volatility is amplified by currency effects, particularly the yen's depreciation. Price instability creates significant margin pressure for manufacturers, especially those serving price-sensitive market segments where passing cost increases to customers is difficult. Weather-related disruptions in major soybean-producing regions and changing global demand patterns contribute to price unpredictability, complicating long-term planning and investment decisions. While manufacturers implement hedging strategies and explore alternative sourcing arrangements to mitigate price risk, these measures add operational complexity and cost. The volatility particularly affects smaller processors who lack the scale to implement comprehensive risk management programs, creating competitive advantages for larger, more financially stable companies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Isolates Lead While Hydrolysates Gain Momentum

The Japanese market has embraced Soy Protein Isolates, which now command a substantial 43.60% market share in 2025. These isolates have become essential ingredients for food manufacturers, offering a neutral flavor profile and functional properties that enable effective protein fortification across food products. In the meat alternatives segment, their gelling and water-binding properties create authentic meat-like textures that resonate with consumers. The hydrolyzed soy protein segment shows promise with an anticipated growth rate of 3.42% from 2026 to 2031, as these proteins offer improved digestibility and bioavailability, key factors for Japan's aging population. Meanwhile, Soy Protein Concentrates continue to serve manufacturers in the mid-market segment by balancing cost-effectiveness with protein content requirements.

The market's evolution has been significantly shaped by advancements in enzymatic hydrolysis technology, which has become instrumental in protein modification. Recent research demonstrates the effectiveness of specialized hydrolysis processes, with modified soybean protein hydrolysates achieving 68.86% protein content while reducing bitterness by four-fold compared to standard hydrolysates. These improvements have transformed the competitive landscape across market segments, offering manufacturers more options to meet consumer demands.

By Nature: Organic Growth Outpaces Conventional

In 2025, conventional products dominated Japan's soy protein market, seizing a 90.85% share, thanks to their abundant supply, familiar ingredients, and cost-effectiveness. J-Oil Mills, a key player, is enhancing taste and dispersibility through solvent-free dehulling and advanced deodorization, ensuring mainstream acceptance joilmills.co.jp. These advancements not only improve product quality but also cater to consumer preferences for better-tasting and easily mixable soy protein options. With ongoing efficiency improvements, conventional producers are poised to maintain their market share, even as consumers lean towards ethically sourced products. Additionally, the established infrastructure and economies of scale further strengthen the position of conventional soy protein in the market.

While organic soy protein currently holds a modest share, it boasts a robust 4.92% CAGR through 2031, outpacing the broader market. As urban affluence rises and concerns over pesticide residues tighten, consumers are willing to shell out a 30-40% premium. Driven by MAFF’s 2024 Organic Vision, which simplifies certification for smaller farms maff.go.jp, the market size for organic soy protein in Japan is set to surpass USD 28.73 million by 2031. Clean-label snacks, smoothies, and meal-replacement sachets lead the charge, with digital platforms emphasizing soil-to-shelf traceability, bolstering health-conscious millennials' willingness to pay. This growth is further supported by increasing awareness of sustainable farming practices and the perceived health benefits of organic products, making organic soy protein a compelling choice for a niche but growing consumer base.

By End-User: Supplements Segment Accelerates Beyond Food Applications

The food and beverages segment holds a substantial 63.25% share of the Japan soy protein market in 2025. The meat alternatives sub-segment demonstrates notable growth as flexitarian consumers increasingly seek products that offer familiar textures while reducing their environmental footprint. Through high-moisture extrusion technology, manufacturers produce protein fibers that effectively mimic meat textures, while the combination of soy proteins with traditional Japanese seasonings ensures alignment with local taste preferences. In the beverage industry, companies incorporate protein isolates to improve product stability and nutritional content in drinks such as lattes and smoothies. Despite being a mature market, the segment continues to expand through consistent product innovations in convenience stores.

The supplements segment demonstrates promising growth prospects with a projected CAGR of 3.91% from 2026 to 2031. Companies are responding to the needs of Japan's aging population by developing targeted products, including single-serve supplements that combine isoflavones, calcium, and vitamin D to support bone health. The sports nutrition category, particularly products that integrate branched-chain amino acids with hydrolyzed soy peptides, is experiencing significant growth through online sales channels, highlighting the market's receptiveness to products backed by scientific evidence.

Geography Analysis

Japan's soy protein market shows clear differences between regions, with urban areas driving new product development while rural regions build up their production capabilities. The strategic placement of food manufacturing facilities in industrial zones near cities gives them a natural advantage in distribution and logistics. With high disposable incomes, premium products thrive; for instance, a probiotic-enriched soy milk, priced 35% higher than the standard, flew off the shelves within weeks of its debut at a top urban grocery chain. Urban cafés are now infusing soy isolates into their specialty drinks, broadening the occasions for out-of-home consumption. To maintain a consistent buzz, manufacturers are collaborating with department-store food halls to craft seasonal SKUs.

Companies near farming areas enjoy lower transportation costs and can source fresher raw materials, helping them produce better quality isolates that beverage makers prefer. Many facilities have started handling multiple steps of production in-house, from extracting oil to making protein concentrates, which helps keep more economic value within their regions.

Food manufacturers have found success by adding protein concentrates to traditional recipes, giving consumers more protein while keeping familiar flavors. Local marketing efforts connect with consumers by explaining how soy's nutritional benefits align with both traditional preferences and modern dietary needs. This balanced approach helps maintain steady demand and supports processing facilities across different regions.

Competitive Landscape

The Japanese soy protein market maintains a moderate concentration, where domestic companies and international firms work alongside each other in healthy competition. Prominent market players include Fuji Oil Holdings Inc., Archer Daniels Midland Company, Ajinomoto Co. Inc., Cargill Incorporated, and International Flavors & Fragrances Inc. Instead of engaging in price wars, businesses focus their efforts on developing superior product functionality and building expertise in various applications. Companies are increasingly moving towards vertical integration to ensure they have reliable access to raw materials and can maintain strict quality standards throughout their operations. A good example of this approach is Fuji Oil Holdings, which introduced its Responsible Soybeans and Soy Products Sourcing Policy to achieve community-level traceability by 2025.

The market presents significant opportunities in specialized nutrition for Japan's growing elderly population, an area where targeted protein formulations for specific health conditions remain largely unexplored. Companies are setting themselves apart by advancing their technological capabilities and developing unique processing methods to improve protein functionality. We can see this in practice with Ajinomoto, whose enzyme technologies, particularly their use of transglutaminase to enhance soy protein texture, showcase how innovation in processing methods can create a competitive edge.

The market is seeing new players emerge in the form of specialized ingredient technology firms that concentrate on fermentation and enzymatic modification of plant proteins. The industry's commitment to innovation is reflected in patent activities, with companies like Fuji Oil, Amano Enzyme, and Nissin Foods taking the lead in filing patents for alternative protein technologies in Japan.

Japan Soy Protein Industry Leaders

Fuji Oil Holdings Inc.

Archer Daniels Midland Company

Ajinomoto Co. Inc.

Cargill, Incorporated

International Flavors & Fragrances

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: In a strategic move, Idemitsu Kosan Co. Ltd., a top player in Japan's petroleum sector, has secured a substantial stake in Fuji Oil Company Ltd., bolstering both firms' market competitiveness and synergy.

- September 2024: Ajinomoto Co. Inc. joined the World Business Council for Sustainable Development (WBCSD). Through this membership, the Ajinomoto Group contributes to the Agriculture and Food Pathway and the Climate Imperative. The group aims to enhance its environmental impact by reducing greenhouse gas emissions through collaboration with stakeholders across various industries within WBCSD.

- May 2024: Fuji Oil Holdings Inc. will implement an organizational restructuring by transitioning to a business holding company structure on April 1, 2025. This change aims to improve profitability and sustainability in the company's soy-based ingredients business by optimizing resource allocation across business units to strengthen its market position.

Japan Soy Protein Market Report Scope

Soy protein is extracted from the processing of soy. Soy protein is used in different food products to increase their nutritional value.

Japan's soy protein market is segmented by type, nature, and end-user. By type, the market is segmented into concentrates, hydrolysates, and isolates. By Nature, the market is segmented into natural and organic. By end user, the market is segmented into food and beverages, animal feed, personal care and cosmetics, and supplements. The food and beverage segment is further segmented into bakery, beverages, breakfast cereals, condiments/sauces, dairy and dairy alternative products, RTE/RTC food products, and snacks. The supplements segment is further segmented into baby food & infant formula, elderly & medical nutrition, and sport/performance nutrition.

For each segment, the report offers the market size in value terms in USD for all the abovementioned segments.

By Type

| Soy Protein Isolates |

| Soy Protein Concentrates |

| Textured/Hydrolyzed Soy Protein |

By Nature

| Conventional |

| Organic |

By End-User

| Food and Beverages | Bakery |

| Beverages | |

| Breakfast Cereals | |

| Meat/Poultry/Seafood and Meat Alternative Products | |

| Condiments/Sauces | |

| Dairy and Dairy Alternative Products | |

| RTE/RTC Food Products | |

| Snacks | |

| Animal Feed | |

| Personal Care and Cosmetics | |

| Supplements | Baby Food and Infant Formula |

| Elderly and Medical Nutrition | |

| Sport/Performance Nutrition |

| By Type | Soy Protein Isolates | |

| Soy Protein Concentrates | ||

| Textured/Hydrolyzed Soy Protein | ||

| By Nature | Conventional | |

| Organic | ||

| By End-User | Food and Beverages | Bakery |

| Beverages | ||

| Breakfast Cereals | ||

| Meat/Poultry/Seafood and Meat Alternative Products | ||

| Condiments/Sauces | ||

| Dairy and Dairy Alternative Products | ||

| RTE/RTC Food Products | ||

| Snacks | ||

| Animal Feed | ||

| Personal Care and Cosmetics | ||

| Supplements | Baby Food and Infant Formula | |

| Elderly and Medical Nutrition | ||

| Sport/Performance Nutrition | ||

Key Questions Answered in the Report

What is the current size of the Japan soy protein market?

The Japan soy protein market is valued at USD 205.56 million in 2026 and is projected to reach USD 237.73 million by 2031 at a 2.95% CAGR.

Which product type leads the market?

Soy protein isolates hold the lead with a 43.60% share in 2025 due to their high purity and broad functionality, and they are projected to maintain steady growth.

Why is hydrolysed soy protein growing so fast?

Enhanced digestibility and quick absorption make hydrolysates attractive for senior nutrition and sports recovery, resulting in a 3.42% forecast CAGR through 2031.

What risks could slow market growth?

Dependence on imported soybeans and price volatility pose supply-chain and margin challenges, while allergen concerns and competition from pea and oat proteins add pressure.

Page last updated on: