Patient-centric Health Care App Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

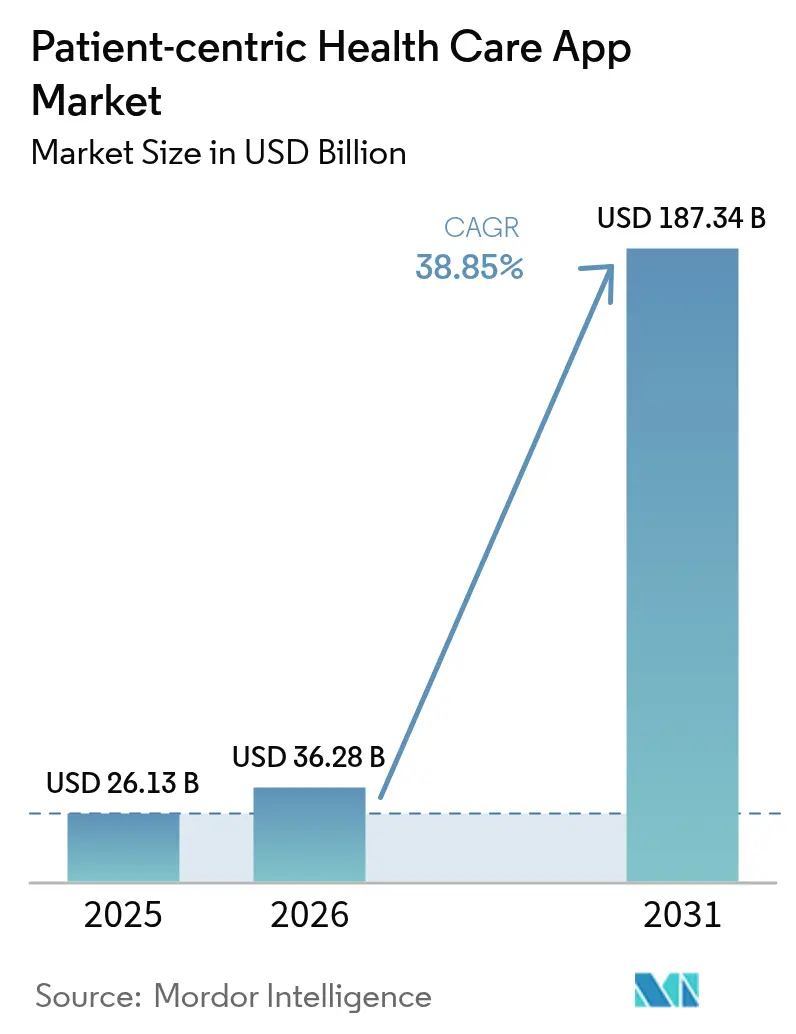

| Market Size (2026) | USD 36.28 Billion |

| Market Size (2031) | USD 187.34 Billion |

| Growth Rate (2026 - 2031) | 38.85% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Patient-centric Health Care App Market Analysis by Mordor Intelligence

The patient centric healthcare app market size was valued at USD 26.13 billion in 2025 and estimated to grow from USD 36.28 billion in 2026 to reach USD 187.34 billion by 2031, at a CAGR of 38.85% during the forecast period (2026-2031). Consumer demand for self-service care, payer pressure to contain chronic-disease costs, and government rules that force application programming interface (API) access to medical records are combining to pull digital engagement from the fringes of care into its operational core. Continued reimbursement for remote physiologic monitoring, the ascendance of value-based contracts, and the roll-out of TEFCA-aligned data-exchange networks are widening the competitive field, allowing technology vendors, pharmaceutical sponsors, and device makers to bypass traditional gate-keepers. Intensifying investment in artificial-intelligence features—Epic alone has moved more than 100 AI tools into production—signals a pivot from stand-alone apps to continuously learning platforms that can personalize engagement at population scale. Taken together, these forces establish a long runway for the patient centric healthcare app market, particularly in chronic-disease management, mental-health support, and preventive-wellness services.

Key Report Takeaways

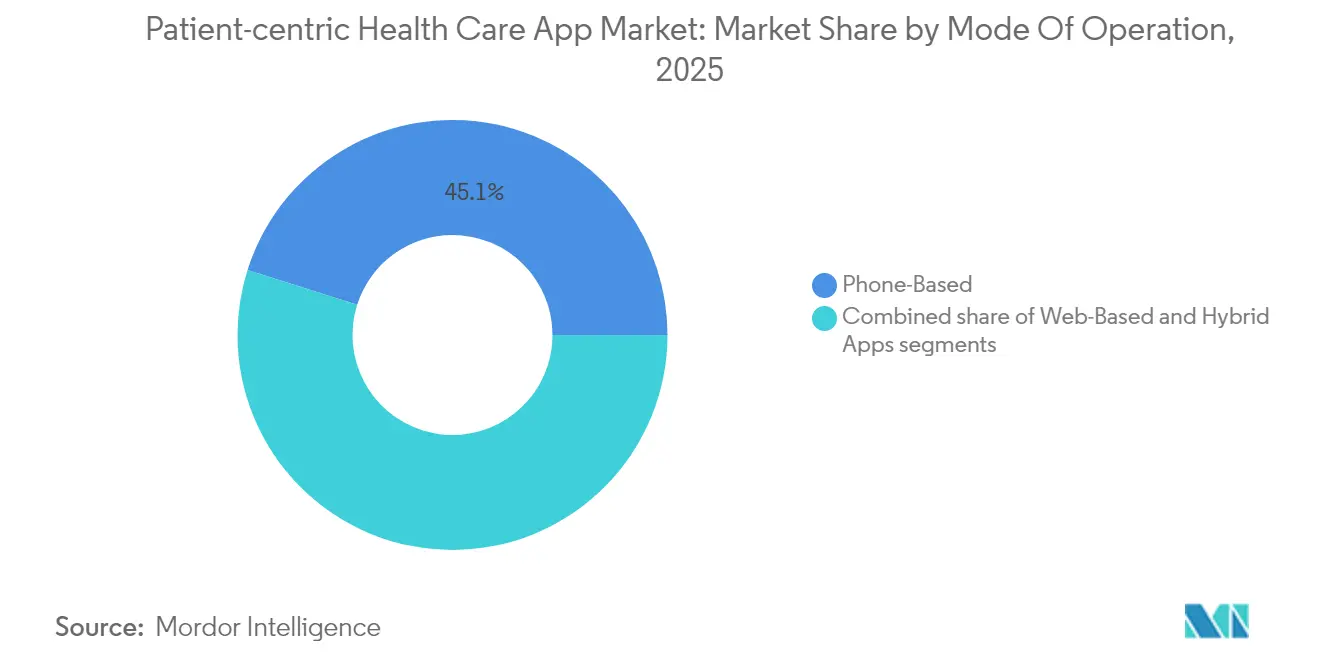

- By mode of operation, Phone-Based applications led with 45.12% of patient centric healthcare app market share in 2025, while Hybrid Apps are projected to compound at 41.02% CAGR through 2031.

- By application, Wellness Management retained 38.02% share of the patient centric healthcare app market size in 2025; Mental Health & Mindfulness is expanding at a 42.11% CAGR to 2031.

- By delivery platform, Cross-Platform/Progressive Web Apps dominated with 55.10% share in 2025, whereas iOS solutions are forecast to surge at 41.33% CAGR through 2031.

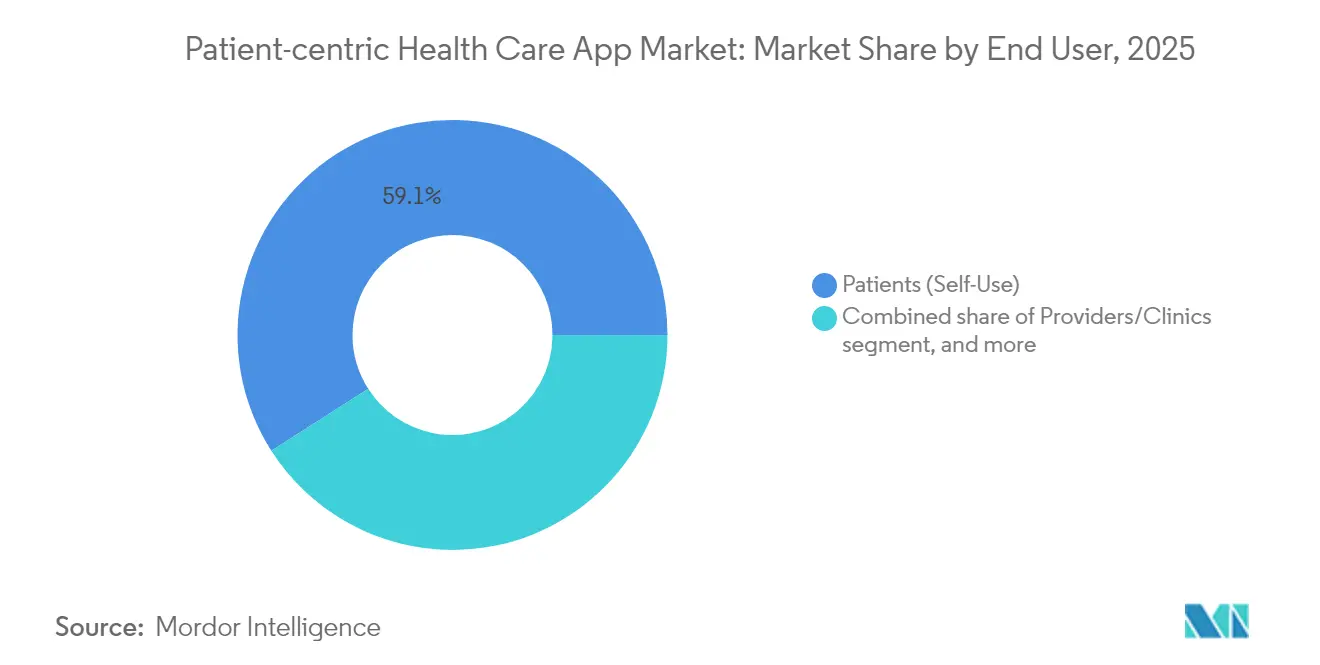

- By end user, Patients (Self-Use) held 59.05% share in 2025, yet Pharma & Med-Tech Sponsors represent the fastest-growing constituency at 41.89% CAGR during 2026-2031.

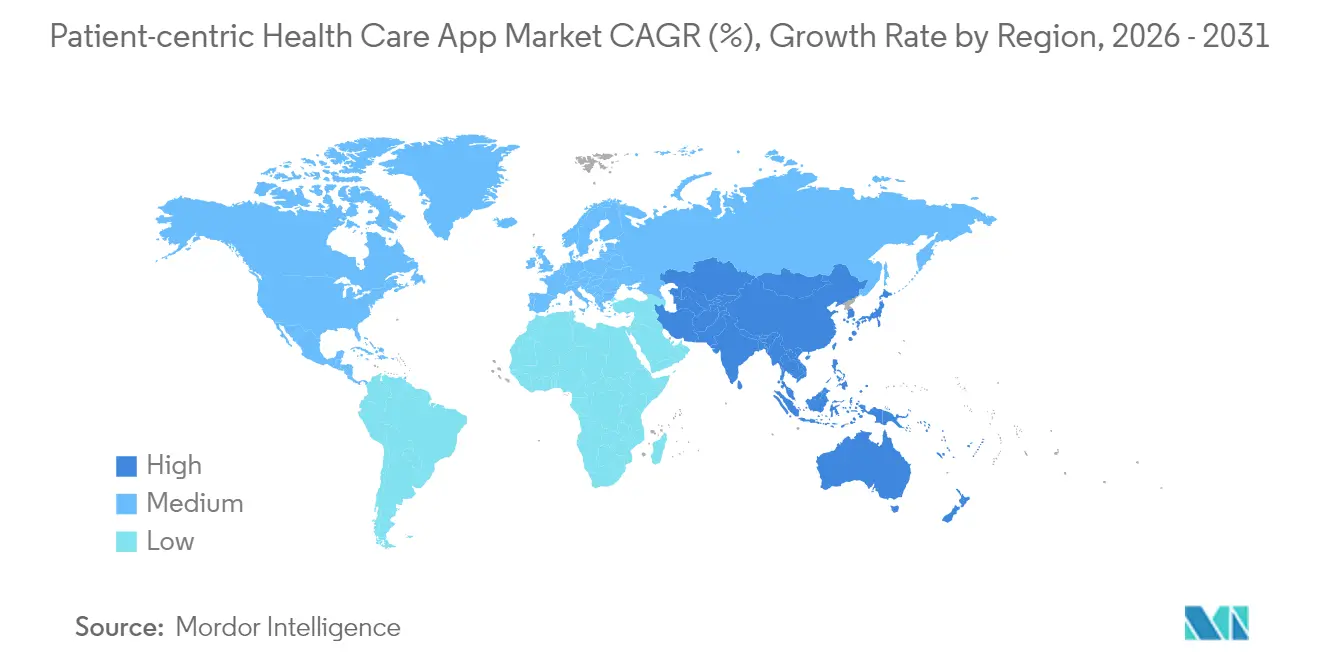

- By geography, North America captured 41.78% of patient centric healthcare app market share in 2025; Asia-Pacific is on track for a 39.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Patient-centric Health Care App Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Burden Of Chronic Diseases And Aging Population | +8.2% | Global; concentrated in North America and Europe | Long term (≥ 4 years) |

| Technological Advancements In Mobile And Cloud Connectivity | +9.1% | Asia-Pacific core; spill-over to global markets | Medium term (2-4 years) |

| Growing Acceptance Of Digital Health Post-Pandemic | +7.8% | Global; accelerated adoption in developed markets | Short term (≤ 2 years) |

| Transition Toward Value-Based Care And Outcome-Linked Reimbursements | +6.4% | North America & EU; expanding to APAC | Medium term (2-4 years) |

| Increasing Focus On Patient Engagement And Adherence Solutions | +5.7% | Global; emphasis on chronic-disease management | Medium term (2-4 years) |

| Strategic Collaborations Between Pharmaceutical And Health-Tech Companies | +4.9% | Global; concentrated in major pharmaceutical hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Chronic Diseases and Aging Population

Non-communicable illnesses now account for 74% of worldwide deaths, prompting public-health authorities to push continuous monitoring outside clinical walls. Data from a 2,883-person trial in China showed that an app-enabled diabetes program lowered fasting glucose by 1.68 mmol/L and HbA1c by 0.45 percentage points, with stronger outcomes among high-adherence users. Novo Nordisk has built commercial alliances around connected-pen technology that transmits dose data directly to coaching apps, aligning pharmaceutical revenue with measurable adherence. Teladoc Health reports that 58% of participants in its diabetes program reach remission-level A1c after one year, while 88% of hypertension users improve or maintain blood pressure, validating digital pathways as complements to pharmacotherapy. As life expectancy lengthens, these results underscore why payers are tilting budgets toward proactive digital engagement.

Technological Advancements in Mobile and Cloud Connectivity

Asia-Pacific added USD 880 billion in mobile-economy value in 2023, buoyed by 5G roll-outs and edge-compute pilots that stream clinical-grade signals in real time. The U.S. Food and Drug Administration cleared OMRON’s connected blood-pressure monitor featuring atrial-fibrillation algorithms that achieved 95% sensitivity and 98% specificity in validation studies. Epic Systems pledged to plug 280 million patient records into the government-backed TEFCA network by 2025, opening a national spine for low-latency data exchange. Smartphone-camera application FibriCheck passed FDA review with 98.3% sensitivity for atrial-fibrillation detection, proving that consumer devices can meet Class II medical-device thresholds. Collectively, these milestones reinforce the technology stack that underpins the patient centric healthcare app market.

Growing Acceptance of Digital Health Post-Pandemic

Hospital systems report sustained 69% engagement in preventive-care apps originally launched as emergency services during lockdowns. CMS embedded three Digital Mental Health Treatment billing codes (GMBT1-3) into its 2025 Physician Fee Schedule, legitimizing software interventions as reimbursable therapy. Virtual-first intensive-outpatient programs have become routine for mood-disorder treatment, with BetterHelp maintaining record visit volumes even as in-person clinics reopen. International Data Corporation projects that 80% of patients will use hybrid (virtual plus physical) pathways by 2028, powered by digital-twin risk stratification. These behavior shifts keep the patient centric healthcare app market on a steep adoption curve.

Transition Toward Value-Based Care and Outcome-Linked Reimbursements

Medicare wants every beneficiary tied to an accountable-care contract by 2030, elevating the commercial stakes for platforms that can document quality gains and cost offsets. The Shared Savings Program’s 2025 final rule lets accountable-care organizations draw prepaid budgets to fund patient-engagement technologies, particularly in underserved communities. Humana disclosed 23.2% lower medical costs for value-based enrollees versus fee-for-service seniors, with 30.1% fewer inpatient admissions—indicators that digital tools which reinforce adherence will continue to gain budget priority. Digital-health vendors able to prove outcome gains therefore command premium contract structures, magnifying the growth potential of the patient centric healthcare app market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack Of Interoperability And Data Standardization | −5.8% | Global; acute challenges in fragmented health systems | Medium term (2-4 years) |

| Clinician Resistance Due To Workflow Integration Challenges | −4.2% | North America & EU; variations by practice size | Short term (≤ 2 years) |

| Evolving Regulatory Framework For Artificial Intelligence And Digital Health | −3.9% | Global; heightened scrutiny in North America, EU, and select APAC economies | Medium term (2-4 years) |

| Persistent Digital Divide And Limited Access In Low-Resource Settings | −4.6% | Emerging markets in Africa, Latin America, and parts of South Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lack of Interoperability and Data Standardization

Only six certified IT vendors had committed to extended USCDI+ Cancer data elements by late 2024, underscoring the slow march toward uniform data semantics[1]Office of the National Coordinator, “HTI-2 Proposed Rule,” healthit.gov. The Sequoia Project’s roadmap schedules QHIN-to-QHIN FHIR pilots for 2025, meaning that true plug-and-play exchange will remain partial for several budget cycles. Patients still juggle download portals, login credentials, and PDF discharge summaries, complicating the longitudinal views that engagement apps depend on. Until governance bodies enforce common identifiers and version control, fragmentation will temper growth in the patient centric healthcare app market.

Clinician Resistance Due to Workflow Integration Challenges

Surveyed physicians cite diagnostic-error liability and documentation overhead as top reasons for slowing digital uptake, even though mobile references shorten drug-lookup times at the point of care[2]Harvard Business Review, “Why Physicians Resist Digital Tools,” hbr.org. German doctors must screen for digital literacy before prescribing DiGA-listed therapies, adding admin steps that many practices cannot absorb. Emergency departments, burdened by overcapacity, struggle to insert new dashboards without delaying triage, further fueling skepticism. Where leadership funds role-based training and ties incentives to digital adoption, resistance wanes, suggesting that change-management budgets will be a prerequisite for unlocking the full value of the patient centric healthcare app market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Operation: Hybrid Solutions Drive Convergence

Phone-Based programs controlled 45.12% of patient centric healthcare app market share in 2025, benefiting from the global reach of iOS and Android storefronts. Hybrid Apps are on track for a 41.02% CAGR to 2031 as healthcare systems seek code-once-deploy-anywhere economics that sidestep device-fragmentation costs. Cross-compatibility also simplifies privacy updates and security patching, critical in regulated environments. Epic’s approach—native mobile front ends that draw decision logic from cloud micro-services—illustrates how hybrid stacks absorb emerging AI modules without rewriting user interfaces. Consequently, developers aligned to hybrid toolchains are positioned to expand faster than single-platform peers inside the patient centric healthcare app market.

The pivot is equally fueled by payer requirements. Health plans increasingly demand multi-channel outreach—short message service, app push, and email—so that members can select their preferred modality. Hybrid frameworks reuse business logic across those messaging pipes, cutting upgrade time. As provider organizations chase value-based bonuses tied to engagement, demand for lower-cost cross-platform builds will support sustained double-digit revenue expansion.

By Application: Mental-Health Acceleration Reshapes Priorities

Wellness Management commanded 38.02% of patient centric healthcare app market size in 2025, propelled by weight-loss coaching, sleep tracking, and preventive-care reminders. Regulatory momentum, however, is shifting attention to evidence-based Mental Health & Mindfulness, forecast to surge at 42.11% CAGR through 2031. The FDA cleared Rejoyn for depression and SleepioRx for chronic insomnia, formalizing software-as-therapy pathways. CMS billing codes for digital cognitive-behavioral programs further legitimize reimbursement, encouraging employers to include subscription apps in health benefits packages. Consumer willingness to pay out-of-pocket also expands the total addressable base, especially among Gen Z users for whom asynchronous chat and meditation sessions are comfort zones. These factors combine to keep mental-health use-cases at the vanguard of innovation within the patient centric healthcare app market.

By End User: Pharma Sponsorship Models Emerge

Patients (Self-Use) accounted for 59.05% of market revenue in 2025, yet pharmaceutical and med-tech sponsors are registering the fastest CAGR—41.89%—as they wrap medications with engagement modules that guide dosing, side-effect reporting, and efficacy tracking. Bayer’s collaboration with Mahana Therapeutics to offer gut-health coaching alongside over-the-counter remedies exemplifies the companion-app archetype. Providers and clinics remain steady adopters, particularly for peri-operative pathways that shorten length of stay, while payers evaluate formulary-like frameworks that rank apps by clinical-economic return. As real-world-evidence demands rise, pharma sponsorship will continue to swell its revenue share inside the patient centric healthcare app market.

By Delivery Platform: Cross-Platform Dominance with iOS Momentum

Cross-Platform/Progressive Web Apps led with 55.10% share in 2025, but iOS builds are accelerating at 41.33% CAGR thanks to Apple’s Project Mulberry AI coach scheduled for native integration in iOS 19.4. Hospital examples such as Emory Hillandale’s all-Apple deployment demonstrate how tight hardware-software coupling can streamline staff training and security patch cadence. Android maintains traction where price-sensitive markets dominate, illustrated by the offline-capable AHOMKA hypertension app in Ghana. The coexistence of premium iOS experiences and mass-market Android penetration suggests that vendor roadmaps must retain cross-compile agility to capture the full span of the patient centric healthcare app market.

Geography Analysis

North America retained 41.78% share in 2025, anchored by TEFCA-driven interoperability rules and the FDA’s mature digital-therapeutic frameworks. CMS added Advanced Primary Care Management codes (GPCM1-3) to its 2025 fee schedule, ensuring that remote coaching and biometric monitoring can bill under risk-stratified capitations. Epic’s pledge to onboard its customer base to TEFCA by 2025 will extend high-fidelity data feeds to 280 million individual records, making the region a test bed for outcome-based contracts. Nonetheless, clinician resistance in smaller practices and persistent rural broadband gaps temper the region’s growth ceiling.

Asia-Pacific is the fastest-growing cluster at a 39.95% CAGR, propelled by mobile-first health-system builds and government mandates that fold digital services into universal-coverage agendas. India’s health-tech economy is on track to hit USD 25 billion in 2025, with telemedicine leading transaction counts and AI-driven radiology reads improving throughput at district hospitals. China’s inclusion in the WHO-backed Global Initiative on Digital Health accelerates standardization, while operators explore private 5G for hospital campuses to cut latency in remote-surgery pilots. Southeast Asian deal-flow—Halodoc’s USD 100 million Series E and Doctor Anywhere’s USD 40.8 million raise—signals continued venture appetite, underscoring why multinationals are localizing interfaces into Bahasa and Thai.

Europe registers steady mid-teens expansion under the European Health Data Space program, with Germany leading Class II digital-therapeutic clearances and the United Kingdom embedding AI algorithms in National Health Service triage lines. Harmonized privacy rules expedite cross-border roll-outs, yet adoption remains uneven due to localized reimbursement rules. The Middle East & Africa and South America offer long-run upside as smartphone penetration climbs, but infrastructure and digital-literacy constraints delay revenue realization, positioning them as secondary waves for the patient centric healthcare app market.

Competitive Landscape

Competition spans electronic-health-record incumbents, pure-play tele-health scale-ups, consumer-electronics giants, and pharma-tech joint ventures. Epic Systems leverages its install base to integrate MyChart with AI-drafted patient responses, reducing physician inbox time and defending its channel to 305 million U.S. patients.

Teladoc Health broadened preventive-care reach through its USD 65 million purchase of Catapult Health, layering at-home diagnostics onto virtual consults. Apple continues to invest in on-device health algorithms, positioning the App Store as a gatekeeper for premium therapeutic downloads. Otsuka’s new digital-health unit and Sanofi’s BrightInsight alliance illustrate how big pharma is internalizing software competencies to extend molecule lifecycles.

Entry barriers remain low for niche point solutions, yet scale advantages accrue to platforms capable of straight-through integration with claims adjudication, dispensing, and remote monitoring. Consequently, while the top five vendors control meaningful penetration in EHR-linked sub-segments, the overall patient centric healthcare app market remains only moderately concentrated.

Patient-centric Health Care App Industry Leaders

Apple Inc. (CareKit)

Google LLC (Fit/Health Connect)

Koninklijke Philips N.V.

Teladoc Health Inc.

Epic Systems Corp. (MyChart)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Teladoc Health acquired Catapult Health for USD 65 million to add at-home preventive testing to its connected-care ecosystem.

- January 2025: Chugai Pharmaceutical, SoftBank, and SB Intuitions formed a generative-AI research pact aimed at compressing drug-development timelines.

- January 2025: Teladoc Health joined Amazon’s Health Benefits Connector so eligible users can self-enroll in cardiometabolic programs.

- January 2025: Health Catalyst agreed to acquire Upfront Healthcare Services to merge engagement analytics with population-health datasets.

- January 2025: OMRON Healthcare secured FDA De Novo clearance for a blood-pressure monitor with atrial-fibrillation detection algorithms.

- November 2024: Teladoc Health introduced an AI-powered Virtual Sitter that lets a single technician observe multiple in-patient rooms.

Global Patient-centric Health Care App Market Report Scope

As per the scope of the report, patient-centric health care apps are applications that run on various technological devices and help patients with their health conditions, and physicians deliver the services on their premises. These apps help provide easier access to health information, such as series of cardiac events, dehydration levels in the body, the number of calories consumed, and other medical insights that improve quality of life. The global patient-centric health care app market is segmented by mode of operation (phone-based, web-based, and hybrid patient-centric apps), application (wellness management, disease and treatment management, and other applications), and geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the segments mentioned above.

| Phone-Based |

| Web-Based |

| Hybrid Apps |

| Wellness Management |

| Disease & Treatment Management |

| Mental Health & Mindfulness |

| Medication Adherence |

| Other Applications |

| Patients (Self-Use) |

| Providers / Clinics |

| Payers |

| Pharma & Med-Tech Sponsors |

| IOS |

| Android |

| Cross-Platform / Progressive Web Apps |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Mode Of Operation | Phone-Based | |

| Web-Based | ||

| Hybrid Apps | ||

| By Application | Wellness Management | |

| Disease & Treatment Management | ||

| Mental Health & Mindfulness | ||

| Medication Adherence | ||

| Other Applications | ||

| By End User | Patients (Self-Use) | |

| Providers / Clinics | ||

| Payers | ||

| Pharma & Med-Tech Sponsors | ||

| By Delivery Platform | IOS | |

| Android | ||

| Cross-Platform / Progressive Web Apps | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the patient centric healthcare app market in 2026?

The patient centric healthcare app market size is USD 36.28 billion in 2026, with a projected 38.85% CAGR to 2031.

Which segment expands fastest between 2026-2031?

Mental Health & Mindfulness apps record the highest forecast CAGR at 42.11%, thanks to FDA-cleared therapeutics and new CMS billing codes.

What share does North America hold today?

North America accounts for 41.78% of patient centric healthcare app market share, supported by TEFCA-aligned data networks and reimbursement pathways.

Why are hybrid apps gaining traction?

Hybrid frameworks allow code-once deployment across iOS, Android, and web, cutting maintenance costs and speeding regulatory updates.

How are pharmaceutical firms participating?

Pharma sponsors fund companion apps that track dosing and outcomes, with the segment growing at a 41.89% CAGR through 2031.

What inhibits faster clinician adoption?

Workflow-integration hurdles and data-standard gaps lower physician willingness to prescribe or integrate apps, dampening CAGR by an estimated 4.2%.

Page last updated on: