Healthcare CRM Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 23.15 Billion |

| Market Size (2031) | USD 41.45 Billion |

| Growth Rate (2026 - 2031) | 12.34% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare CRM Market Analysis by Mordor Intelligence

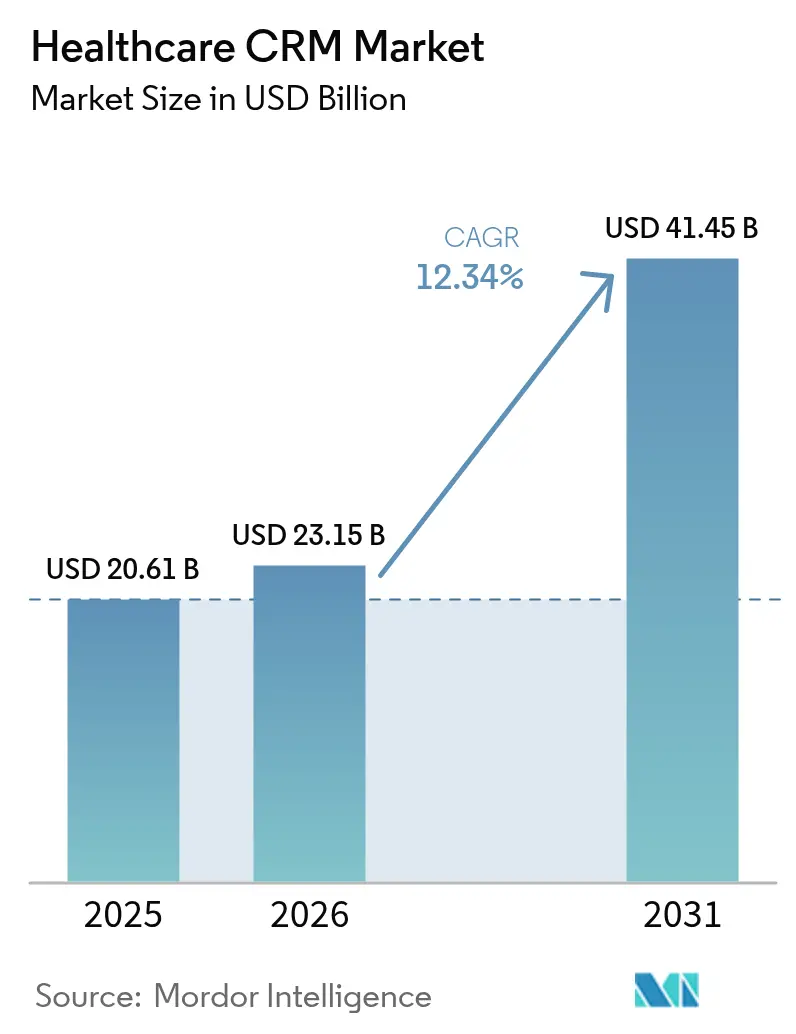

The healthcare CRM market size is expected to grow from USD 20.61 billion in 2025 to USD 23.15 billion in 2026 and is forecast to reach USD 41.45 billion by 2031 at 12.34% CAGR over 2026-2031. Growth reflects the healthcare sector’s rapid push toward patient-centric delivery models, broader adoption of cloud platforms, and continuous investments in digital transformation. Large provider networks are deploying advanced patient-engagement tools to improve care coordination and to manage rising consumer expectations for real-time communication. Vendors are embedding artificial intelligence into workflows that link telehealth, revenue-cycle, and population-health programs, creating unified views of the patient journey and opening new revenue streams. Intensifying competition and a rise in strategic partnerships are helping purchasers lower the total cost of ownership while accelerating feature roll-outs across diverse care settings.

Key Report Takeaways

- By component, software led with 65.12% revenue share in 2025; services show the fastest expansion at a 13.25% CAGR through 2031.

- By deployment model, the web/cloud segment controlled 77.65% of the healthcare CRM market size in 2025 and is also projected to be the fastest segment, growing at 12.46% CAGR to 2031.

- By organization size, large enterprises accounted for 69.95% healthcare CRM market share in 2025; small and medium enterprises are scaling faster at 12.97% CAGR over the forecast horizon.

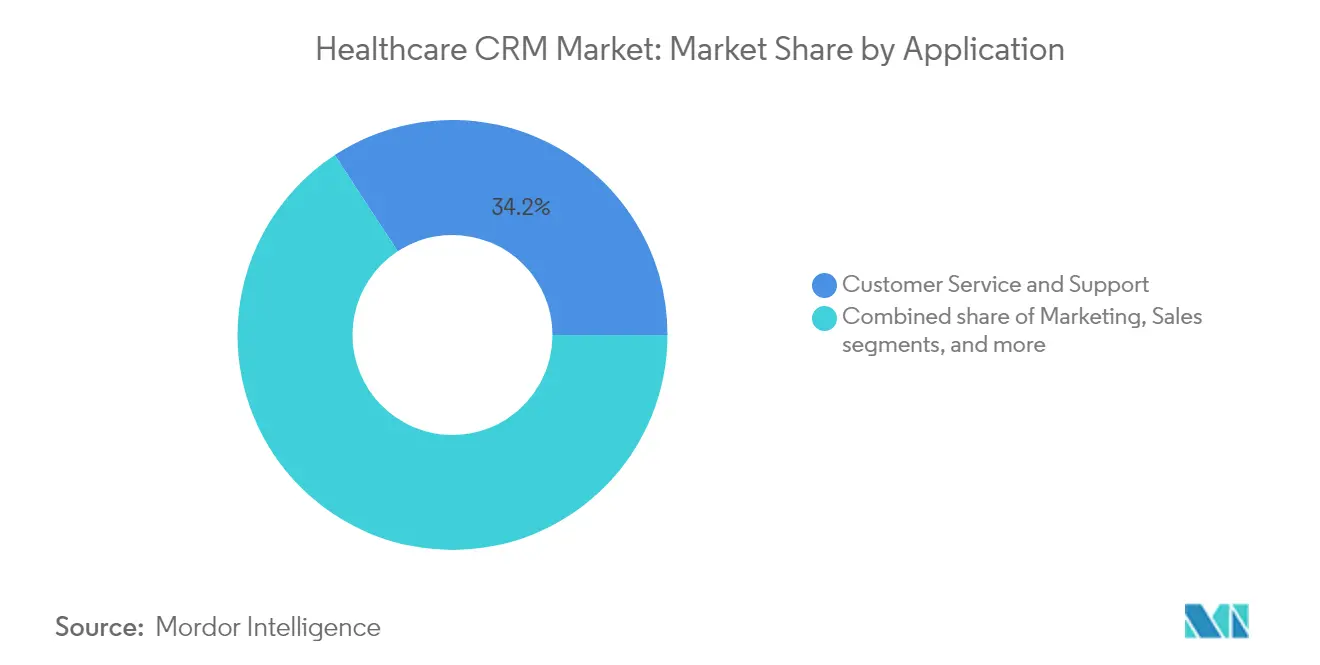

- By application, customer service and support held 34.22% of the healthcare CRM market size in 2025; patient information management is rising at a 13.36% CAGR.

- By end-user, hospitals captured 56.02% revenue share in 2025; ambulatory surgery centers and clinics are forecast to expand at 12.62% CAGR to 2031.

- By geography, North America retained 51.78% healthcare CRM market share in 2025, whereas Asia Pacific is set to grow the quickest at 13.62% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Healthcare CRM Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift to Value-Based Care Requiring Patient Engagement Platforms | +3.2% | North America & Europe, with emerging adoption in APAC | Medium term (2-4 years) |

| Rapid Adoption of Omnichannel Patient Communication Across Healthcare | +2.8% | Global, with higher impact in North America | Short term (≤ 2 years) |

| Government Interoperability Mandates Elevating Data Integration Demand | +2.1% | North America, Europe, with gradual expansion to APAC | Medium term (2-4 years) |

| Telehealth Expansion Driving CRM–Virtual Care Integration | +2.5% | Global, with strongest impact in North America & Europe | Short term (≤ 2 years) |

| Rise of Healthcare Consumerism & Personalized Patient Journeys | +1.9% | North America, Europe, urban APAC | Medium term (2-4 years) |

| Hospital Consolidation Catalyzing Enterprise-Wide CRM Roll-outs | +1.4% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift to Value-Based Care Requiring Patient Engagement Platforms

Health systems moving toward value-based reimbursement models need robust tools that monitor outcomes and enable proactive outreach. Organizations involved in value-based contracts are 36% more likely to invest in advanced patient-engagement software that ties clinical, financial, and behavioral data into a single record. The Centers for Medicare & Medicaid Services increased home-health payment rates by 2.7% for 2025, though adjustments lowered the net rise to 0.5%.[1]Centers for Medicare & Medicaid Services, “Calendar Year 2025 Home Health Prospective Payment System Final Rule Fact Sheet,” Centers for Medicare & Medicaid Services, cms.gov Providers are therefore intensifying efforts to track quality metrics and minimize penalties. Integrated healthcare CRM market platforms automate outreach, support care-gap closure, and simplify population-health analytics across multiple care settings, making them critical enablers of value-based success.

Rapid Adoption of Omnichannel Patient Communication Across Healthcare

The omnichannel trend is driving record levels of platform investment. Surveys show 92% of patients prefer digital intake forms and 91% expect rapid responses through portals, text, or email. Providers using coordinated SMS, portal, and voice workflows report appointment-adherence jumps of up to 35% and satisfaction increases of 28%. These gains translate directly into revenue retention by reducing no-shows and driving loyalty. As consumer expectations continue to align with retail-style experiences, the healthcare CRM market is moving quickly toward AI-driven chatbots and sentiment analysis that refine engagement strategies in real time.

Government Interoperability Mandates Elevating Data Integration Demand

Legislation such as the 21st Century Cures Act in the United States and the European Health Data Space in the EU mandates standardized data exchange, forcing care organizations to modernize legacy interfaces. The global interoperability solutions sector is projected to grow from USD 4.53 billion in 2024 to USD 7.75 billion by 2029, reflecting an 11.31% CAGR. Healthcare CRM market vendors with pre-built FHIR APIs and compatibility with major electronic health record systems are growing fastest because they reduce compliance risk and shorten project timelines. Interoperability readiness is becoming a top procurement criterion, particularly within integrated delivery networks managing multiple acute and ambulatory facilities.

Telehealth Expansion Driving CRM–Virtual Care Integration

Virtual care volumes remain elevated compared with pre-pandemic baselines, shifting provider attention to unified platforms that integrate telehealth data alongside in-person encounters. Teladoc Health added 4.2 million US members to its Integrated Care service in 2024 and boosted chronic-care program enrollment by 4%.[2]Teladoc Health, “2024 Annual Report,” q4cdn.com Providers are embedding scheduling, remote-monitoring, and payment workflows inside healthcare CRM market interfaces, giving clinicians longitudinal visibility into clinical and social determinants of health. Continuous engagement tools improve adherence within chronic-disease populations and help organizations qualify for shared-savings bonuses under value-based contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Data Silos from Fragmented Legacy IT | -1.8% | Global, with higher impact in North America & Europe | Medium term (2-4 years) |

| Stringent Data-Protection Regulations Prolonging Procurement Cycles | -1.2% | Europe (GDPR), North America (HIPAA), with increasing impact in APAC | Medium term (2-4 years) |

| Global Healthcare IT Talent Shortage Limiting Deployment Capacity | -1.1% | Global, with acute impact in emerging markets | Short term (≤ 2 years) |

| Clinician Resistance to Workflow Changes and Technology Uptake | -0.9% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Data Silos from Fragmented Legacy IT

Many health systems continue to maintain dozens of specialized applications that cannot easily exchange information, blocking efforts to create unified patient records. Dirty data costs the sector an estimated USD 300 billion each year and complicates analytics roll-outs. Implementations routinely require labor-intensive data mapping and transformation projects that inflate budgets and extend timelines. Vendors with in-house accelerators or partnerships for enterprise integration are gaining traction, yet the risk of budget overruns remains a deterrent for smaller organizations evaluating healthcare CRM market projects.

Stringent Data-Protection Regulations Prolonging Procurement Cycles

Regulators continue to tighten rules around personal-health information, lengthening due-diligence cycles for new contracts. Europe’s GDPR imposes strict penalties for misuse, and HIPAA enforcement in the United States shows no signs of easing. Privacy-impact assessments, business-associate agreements, and third-party penetration tests are now standard prerequisites for procurement sign-off. The extra scrutiny can delay go-live dates by several quarters, especially for cross-border cloud deployments. Vendors with strong encryption defaults, audit-ready reporting, and region-specific hosting options are best positioned to navigate these hurdles and secure long-term growth in the healthcare CRM market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Drive Incremental Value

The component landscape shows software accounting for 65.12% of revenue in 2025, yet services are expanding faster at a 13.25% CAGR. Cloud migrations, EHR integrations, and change-management programs demand specialist expertise that internal IT teams often lack. Health systems commonly bundle consulting, implementation, and managed-support contracts into multiyear deals to guarantee performance and user adoption. As artificial-intelligence modules become commonplace, advanced configuration and ongoing algorithm tuning further elevate services spend. The healthcare CRM market benefits when implementation partners accelerate time-to-value by harmonizing workflows across clinical, financial, and consumer-experience departments.

In parallel, platform vendors are unveiling low-code toolkits, but most providers still prefer external assistance for data-quality remediation and regulatory mapping. Early evidence indicates that service-supported roll-outs achieve 20–30% higher user-satisfaction scores compared with do-it-yourself deployments. These positive outcomes reinforce the services' growth story and encourage first-time buyers to select bundled engagements. As more mid-tier hospitals and ambulatory networks join the buyer pool, the healthcare CRM industry services ecosystem is poised to widen, creating new niches for niche system integrators.

By Deployment Model: Cloud First Remains the Norm

Web/cloud segment held a 77.65% share in 2025 and continue to grow at a 12.46% CAGR. Subscription pricing lowers upfront capital expenditure, while remote access supports hybrid workforce models. Providers gravitate toward single-tenant or regionally segregated arrangements that comply with data sovereignty rules. Legacy on-premise deployments linger within academic medical centers that co-locate research data and require ultra-low latency. Yet, the cost of hardware refresh cycles drives many toward managed hosting.

Elastic storage and integrated disaster-recovery features have reduced security concerns. Most vendors now achieve HITRUST, ISO 27001, and SOC2 certifications, removing significant procurement barriers. The shift also aligns with sustainability goals, as consolidated hosting often improves energy efficiency. Given these factors, the healthcare CRM market is expected to maintain a decisive cloud tilt throughout the decade.

By Organization Size: SMEs Narrow the Digital Gap

Large enterprises retained 69.95% share in 2025, but SMEs are anticipated to grow at a stronger 12.97% CAGR and continue to erode the gap. Smaller practices are adopting scalable bundles that marry appointment reminders, reputation management, and basic population-health dashboards. Quick-start templates and pay-as-you-go licensing minimize risk, while intuitive interfaces limit training overhead. Studies show that SMEs moving to healthcare CRM market platforms realize retention gains of 25–40% and operating-cost savings up to 35% through workflow automation.

Financing programs from technology vendors and regional grant initiatives further ease capital pressure. As consumerism intensifies competition, independent clinics view CRM as an essential lever to match the personalization offered by larger health systems. Integrations with point-of-sale and telehealth add-ons will likely extend adoption momentum in the small-practice segment.

By Application: Patient Information Management Gains Momentum

Customer service and support kept the largest revenue slice at 34.22% in 2025, yet patient information management applications are climbing at a 13.36% CAGR. Providers seek comprehensive, actionable profiles that blend EHR data, wearable-device feeds, and social-determinant indicators. Unified records permit targeted outreach, clinical-risk stratification, and personalized care-pathway design. A mature patient-information layer also underpins compliance with interoperability mandates, reinforcing demand.

Advanced analytics use the same data foundation to predict the likelihood of readmissions, optimize staffing, and guide preventive-care campaigns. Marketing and referral-management sub-segments are also expanding as competitive pressures rise, strengthening the overall healthcare CRM market value proposition.

By End-User: Ambulatory Settings Rise Quickly

Hospitals accounted for 56.02% revenue in 2025 due to their complex workflows and higher IT budgets, yet ambulatory surgery centers and clinics are accelerating at 12.62% CAGR. Outpatient settings favor streamlined check-in, digital consent, and automated follow-up because procedure volumes can exceed 20 cases per room each day. Integrated CRM dashboards improve throughput and capture downstream visits by maintaining continuous engagement after discharge. Diagnostic centers and home-health agencies follow similar logic, adopting modules that centralize scheduling, reminders, and results notifications. As payers push more elective procedures to outpatient locations, end-user diversification will intensify across the healthcare CRM market.

Geography Analysis

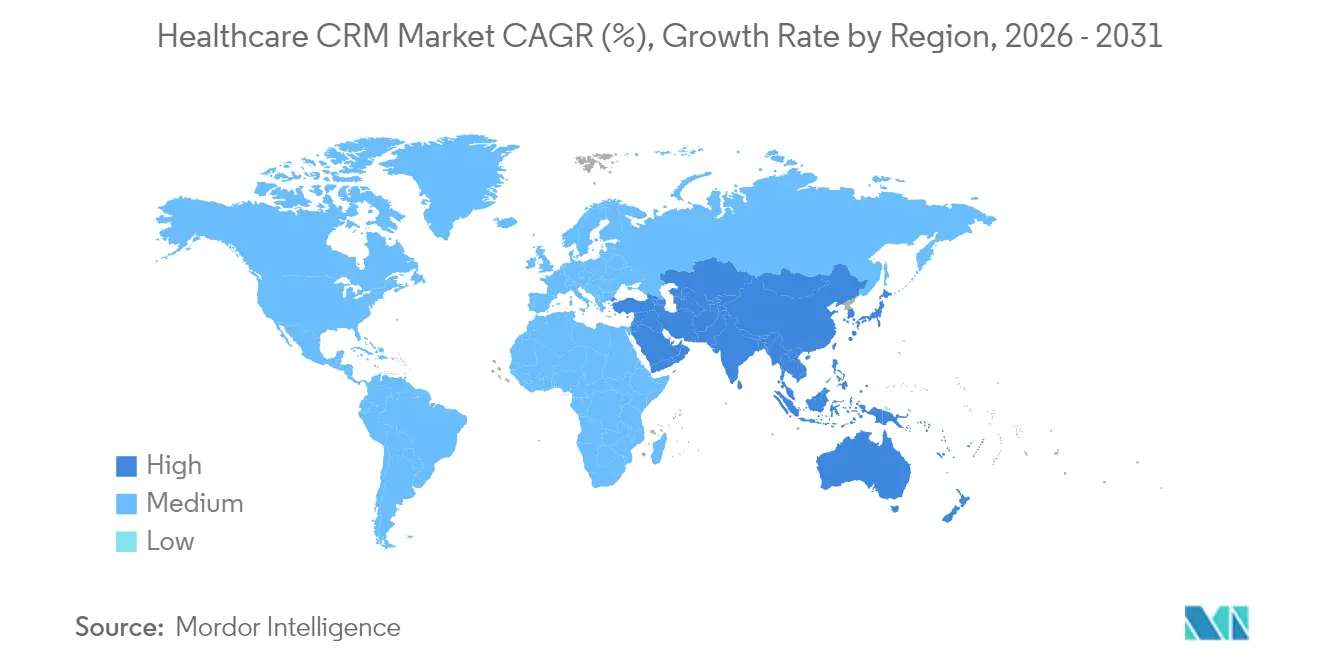

North America held 51.78% of global revenue in 2025, anchored by mature electronic-health-record penetration, advanced reimbursement models, and a dense vendor ecosystem. The region’s 11.98% CAGR to 2031 is solid though modest compared with emerging markets. Health systems concentrate on optimization projects that improve patient-experience metrics and unlock incremental value from prior IT spend. Federal incentives for interoperability, plus ongoing telehealth reimbursement parity within Medicare, keep demand high across integrated delivery networks and payer-provider hybrids.

Asia Pacific is the fastest-growing territory with 13.62% CAGR, propelled by large population bases, rapid digitization, and progressive national e-health programs. China and India are funneling budget toward regional cloud hubs, rural telemedicine, and mobile-first engagement. India’s Union Budget 2025 underlined plans to extend digital-health coverage and to incentivize broadband expansion into remote districts. These policies shorten deployment timelines for cloud-native solutions, directly boosting the healthcare CRM market.

Europe contributes a sizeable share and grows at 12.33% CAGR. The European Health Data Space, combined with GDPR privacy safeguards, drives organizations toward platforms with fault-tolerant encryption and audit trails. United Kingdom trusts and German university clinics are piloting AI-powered segmentation that tailors outreach to linguistic and socioeconomic profiles. Southern and Eastern European systems follow the path, often supported by EU structural funds that co-finance digital infrastructure. Middle East & Africa and South America expand at 13.41% and 12.88%, underpinned by private-sector investment, growing medical-tourism inflows, and demand for consumer-grade digital experiences.

Competitive Landscape

The healthcare CRM market shows moderate concentration. Salesforce, Microsoft Dynamics, and Oracle bring cross-industry platforms with robust ecosystems, while Epic, Veeva Systems, and hc1.com provide purpose-built modules tailored to clinical workflows. Salesforce’s strategic focus on Einstein AI and its Health Cloud upgrades intensifies the rivalry with Epic, whose Cheers solution is gaining traction among large US health systems. Microsoft collaborates with Epic through Microsoft Teams integrations that simplify virtual consults.

Strategic partnerships multiply as vendors bundle telehealth, analytics, and cybersecurity add-ons. Talkdesk integrated its contact-center suite with Epic Cheers in February 2025, improving real-time routing and SMS follow-up. Rubrik’s Healthcare Dashboard, released in December 2024, secures Epic environments with immutable backups and centralized compliance reporting rubrik.com. These moves reflect a shift toward ecosystem play, where cyber-resilience and communication workflows become critical differentiators.

Mergers and acquisitions target capability gaps and regional expansion. Innovaccer acquired Cured in January 2024 to broaden marketing-automation functionality, and Syllable purchased Actium Health in March 2024 to bolster conversational AI and process automation. Private-equity interest remains high, with deal multiples supported by strong recurring-revenue models. The competitive field is expected to remain dynamic as payers, life-science firms, and consumer-health startups enter adjacent spaces, driving continual innovation in the healthcare CRM market.

Healthcare CRM Industry Leaders

IBM Corporation

Microsoft Corporation

Oracle Corporation

Salesforce Inc

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Talkdesk integrated its contact-center tools into Epic Cheers to streamline omnichannel patient engagement.

- December 2024: Rubrik launched a Healthcare Dashboard that secures Epic environments and automates compliance reporting.

- March 2024: Syllable acquired Actium Health, adding advanced AI and CRM capabilities to its engagement platform.

- January 2024: Innovaccer purchased Cured to extend marketing and CRM automation for healthcare providers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the healthcare customer relationship management market as all provider and payer focused software and associated services that capture, connect, and activate longitudinal patient or member data to enhance engagement, scheduling, revenue-cycle touchpoints, and analytics. It covers on-premise and cloud deployments adopted by hospitals, ambulatory centers, diagnostics networks, insurers, and public payers worldwide.

Scope Exclusions: Platforms built purely for pharmaceutical salesforce automation or generic CRM modules not adapted to healthcare workflows sit outside this analysis.

Segmentation Overview

- By Component

- Software

- Services

- By Deployment Model

- On-Premise

- Web/Cloud

- By Organization Size

- Large Enterprises

- SMEs

- By Application

- Customer Service & Support

- Marketing

- Sales

- Patient Information Management

- Other Applications

- By End-User

- Hospitals

- Ambulatory Surgery Centers & Clinics

- Diagnostic Centers

- Other End-Users

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts supplemented desk findings through interviews and short surveys with hospital IT directors in North America and Europe, payer product leads across Asia-Pacific, and regional system integrators. These conversations refined average seat counts, integration pain points, and contract values that shape our model assumptions.

Desk Research

We began by mining open, tier-1 references such as the Centers for Medicare and Medicaid Services expenditure series, OECD Health Stats, Eurostat hospital discharge files, ONC interoperability dashboards, and releases from the Healthcare Information and Management Systems Society. These datasets anchored spending pools, technology adoption ratios, and regulatory milestones.

Annual reports and 10-Ks of listed CRM vendors, selected provider filings, reputable health IT journals, plus curated articles in Dow Jones Factiva supplied usage clues and average selling price signals. D&B Hoovers company intelligence and Questel patent analytics helped us gauge supplier footprints and innovation pace. The sources listed are illustrative, and many additional references informed our assessment.

Market-Sizing and Forecasting

A top-down demand pool build starts with national health spending, digital health budget shares, and CRM penetration, which are then checked against sampled vendor revenue roll-ups and average price times license tests for selective bottom-up validation. Key variables like inpatient admissions, insured member totals, cloud migration ratios, patient portal uptake, and AI add-on premiums feed a multivariate regression, and exponential smoothing extends the curve to 2030. Where bottom-up gaps remain, midpoint estimates vetted with interviewees fill the void.

Data Validation and Update Cycle

Model outputs pass anomaly screens, variance limits, and a second analyst review. We refresh numbers annually and issue interim updates after major funding rounds, regulatory shifts, or mega mergers, with a final walkthrough before publication.

Why Mordor's Healthcare CRM Baseline Commands Trusted Confidence

Published estimates often diverge because firms select different care settings, discount ladders, and update cadences. We acknowledge those spreads upfront and show the levers behind them.

Differences typically arise when other studies fold pharmaceutical SFA tools into scope, apply uniform price erosion across all regions, or project growth without rebasing to the latest national IT budgets. Mordor keeps a healthcare-only scope, converts currencies with quarterly averages, and injects fresh primary pulse checks before every refresh, keeping variance contained.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 20.61 B (2025) | Mordor Intelligence | |

| USD 19.69 B (2024) | Global Consultancy A | Year misalignment and inclusion of life sciences salesforce tools inflate next year growth delta |

| USD 20.78 B (2025) | Industry Portal B | Uses single price decline factor and omits cloud service revenue from managed partners |

The comparison shows values cluster closely, yet our disciplined scope, live primary checks, and transparent steps give decision makers a balanced baseline they can readily trace and reproduce.

Key Questions Answered in the Report

Why are healthcare payers increasingly outsourcing business-process operations?

Payers are looking to trim administrative overhead and accelerate digital transformation; outsourcing partners offer mature automation tools and domain talent that shorten processing cycles and enhance accuracy in core tasks such as claims intake and member services.

What role does artificial intelligence play in modern payer service contracts?

Generative AI and machine-learning models now underpin fraud detection, prior-authorization reviews, and customer support chatbots, helping insurers reduce manual workload while boosting decision quality.

How are tightening data-privacy rules influencing vendor selection?

New encryption and multi-factor authentication mandates require payers to favor partners with robust cybersecurity certifications and proven compliance frameworks, leading to longer due-diligence cycles and more stringent contract clauses.

Which application areas currently show the most innovation among service providers?

Fraud analytics, interoperability solutions using FHIR APIs, and cloud-native member engagement platforms are attracting concentrated R&D spending as outsourcers compete on differentiated technology capabilities.

Why are private-equity firms keen on the healthcare payer services space?

Investors see recurring revenue streams and opportunities to create integrated platforms by acquiring specialized vendors across claims, analytics, and IT services, then scaling them through shared technology and cross-selling.

How are payers addressing rising cybersecurity threats within outsourced environments?

Many now embed continuous monitoring, shared incident-response playbooks, and mandatory cyber-insurance coverage into contracts to ensure real-time visibility and rapid mitigation if a breach occurs.

Page last updated on: