Urgent Care Apps Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.90 Billion |

| Market Size (2031) | USD 28.84 Billion |

| Growth Rate (2026 - 2031) | 37.32% CAGR |

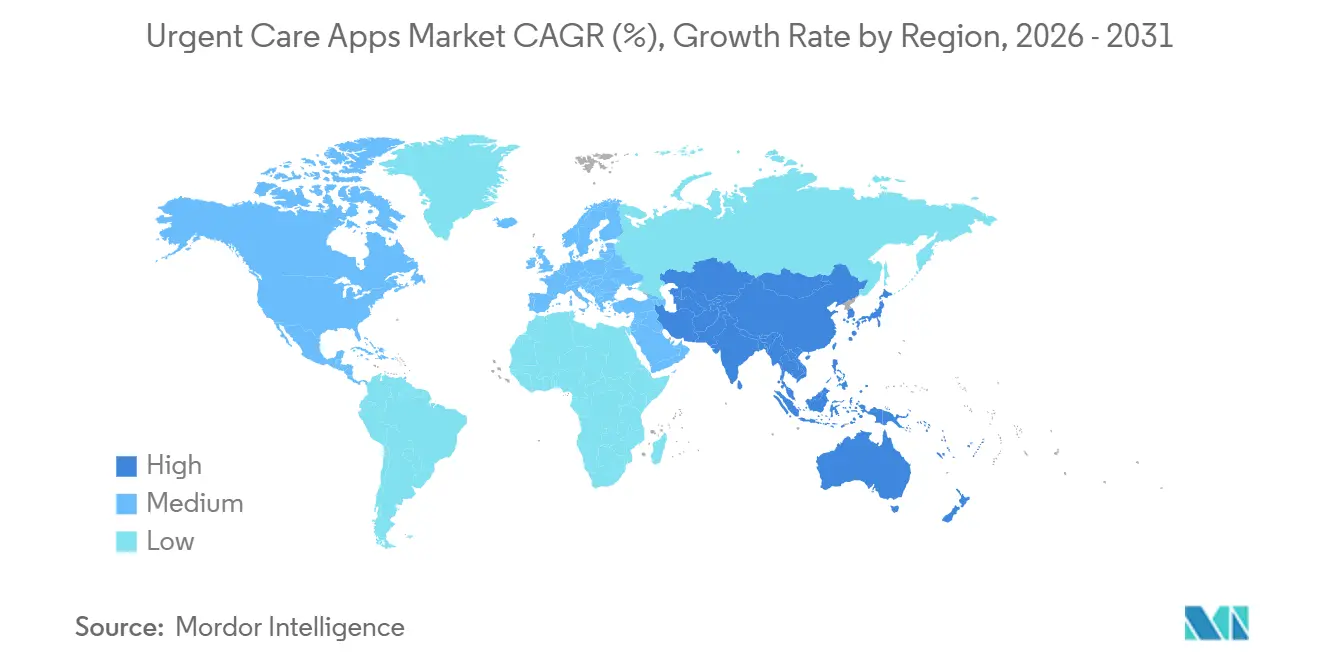

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Urgent Care Apps Market Analysis by Mordor Intelligence

The urgent care apps market size is expected to grow from USD 4.30 billion in 2025 to USD 5.90 billion in 2026 and is forecast to reach USD 28.84 billion by 2031 at 37.32% CAGR over 2026-2031. Payment-parity statutes now cover 43 U.S. states, removing revenue friction for virtual visits and accelerating adoption of urgent care apps market platforms. Health-system spending on “digital front doors” lifted patient self-service encounters, with ThedaCare’s Ripple app posting 312% download growth in ten months, underscoring rising consumer demand for the urgent care apps market. AI-triage engines already outperform physicians on certain infection detections, evidencing how algorithmic triage compresses diagnosis timelines inside the urgent care apps market. EHR-to-app interoperability mandated through federal FHIR API rules unlocks richer data exchange, reinforcing clinical credibility for every urgent care apps market transaction.

Key Report Takeaways

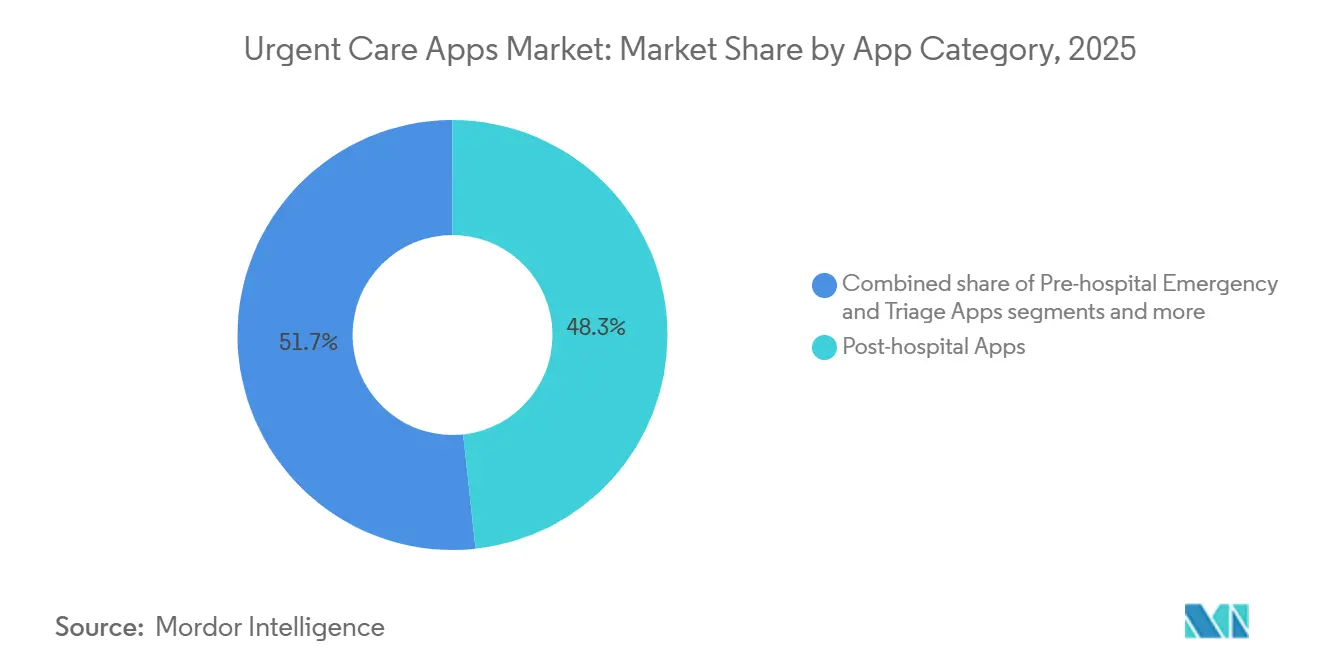

- By app category, post-hospital care-coordination applications held 48.30% of the urgent care apps market share in 2025. Pre-hospital emergency and triage tools are forecast to expand at a 37.85% CAGR through 2031, representing the fastest-growing slice of the urgent care apps market.

- By platform, iOS commanded 53.45% of the urgent care apps market size in 2025. Android installations are poised to grow at a 38.40% CAGR to 2031, eroding historical platform imbalance inside the urgent care apps market.

- By clinical area, trauma area led with 41.35% of urgent care apps market share in 2025, whereas stroke care solutions are projected to post a 39.10% CAGR through 2031.

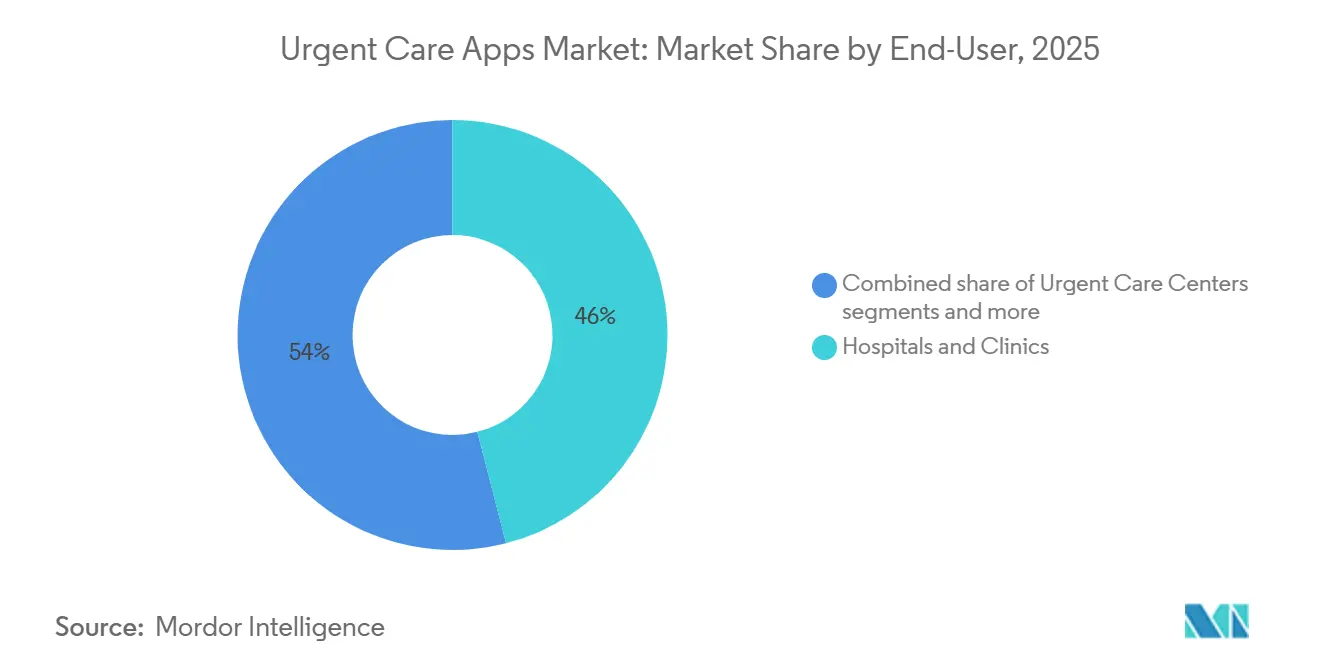

- By end-user hospitals and clinics accounted for 46.00% of the urgent care apps market size in 2025. Emergency Medical Services will register the highest growth, advancing at a 39.60% CAGR to 2031 within the urgent care apps market.

- By business model, B2B contracts represented 53.10% of urgent care apps market share in 2025, while hybrid models are expected to expand at a 40.20% CAGR, reshaping commercial dynamics.

- By geography, North America led with 41.70% of urgent care apps market share in 2025, yet Asia-Pacific is set to climb at a 40.60% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Urgent Care Apps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Payer Reimbursement Parity for Virtual Visits | +12.5% | Global, with North America leading adoption | Medium term (2-4 years) |

| Explosion of "Digital Front-Door" Investments by Health Systems | +10.8% | North America & Europe, expanding to APAC | Short term (≤ 2 years) |

| Integration of AI-Triage into EMS Workflows Cuts Hand-Off Time | +8.2% | Global, with early gains in urban centers | Medium term (2-4 years) |

| Smartphone-Based Clinician Collaboration Tools Replacing Pagers | +6.1% | Global, with UK and US leading transition | Short term (≤ 2 years) |

| Government Mandates for EHR-to-App Interoperability (FHIR APIs) | +7.4% | US-focused, with EU following similar frameworks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Payer Reimbursement Parity for Virtual Visits

Forty-three states now enforce some form of payment parity, eliminating the revenue gap that previously hindered the urgent care apps market. UnitedHealthcare revised commercial policies in 2024 to reimburse e-visits, virtual check-ins, and remote monitoring, boosting provider adoption of urgent care apps market solutions. CMS extended telehealth waivers through December 2024, offering economic predictability that encourages permanent integration of urgent care apps market workflows. Hospital groups consequently fast-track chatbot triage modules that link directly to billing systems, reducing uncompensated encounters in the urgent care apps market. As payment certainty rises, competitive focus shifts toward user experience and clinical depth across the urgent care apps market.

Explosion of “Digital Front Door” Investments by Health Systems

ThedaCare’s Ripple app recorded a 312% download surge within ten months, proving that patients now expect mobile first access routes into urgent care workflows. Sturdy Health automated intake and scheduling through an AI-powered front door, cutting manual touches per encounter by one-third and redirecting staff time toward clinical tasks. Fabric Health secured USD 20 million to fuse ED check-ins with post-discharge follow-ups, confirming investor belief that unified patient journeys lower churn across urgent care apps. CIO surveys show 74% of U.S. hospital executives now rank digital front doors as a top-three capital priority, rivaling imaging equipment for budget share. The momentum forces late-stage telehealth vendors to embed seamless onboarding flows or risk losing high-value encounters to health-system branded urgent care apps.

Integration of AI-Triage into EMS Workflows Cuts Hand-Off Time

Cedars-Sinai researchers found AI triage models outperformed physicians at detecting antibiotic-resistant infections during video consults, reducing misclassification by 11 percentage points. Benchmark testing with 2,000 real cases showed large language models improved diagnostic accuracy and shaved four minutes from EMS-to-ED hand-off, a material gain for trauma and stroke survival rates. Twelve U.S. cities now issue smartphones loaded with decision-support apps that stream vitals and GPS in real time to receiving hospitals, tightening coordination inside the urgent care apps market. Early data indicate a 9% decline in unnecessary ambulance transports when algorithms reroute low-acuity calls to virtual urgent care teams instead of ED bays. These gains translate into payer savings, reinforcing reimbursement support for AI-first urgent care apps.

Smartphone-Based Clinician Collaboration Tools Replacing Pagers

The U.K. NHS formerly spent GBP 6.6 million each year on pagers but now funds secure messaging apps such as Smartpage to accelerate team response. U.S. hospitals adopting similar tools report 24% faster acknowledgement of critical labs compared with legacy one-way paging, directly improving urgent care turnaround. Two-way mobile threads integrate with EHR alerts so cardiologists join trauma chats without duplicate data entry, reducing clinician burnout. Payors incentivize hospitals that cut left-without-being-seen rates, making modern collaboration tools a compliance as well as an efficiency imperative. The resulting workflow gains feed demand for fully integrated urgent care apps rather than stand-alone chat clients.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented State-Level Telehealth Licensure in the U.S. | -4.3% | United States primarily | Medium term (2-4 years) |

| Limited 5G/Broadband in Rural & Low-Income Areas | -6.7% | Global, particularly affecting rural regions | Long term (≥ 4 years) |

| Rising Patient Privacy-Breach Litigation Costs | -3.2% | Global, with North America and Europe leading regulatory enforcement | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented State-Level Telehealth Licensure in the U.S.

Only 36 states offer limited waivers, so clinicians still purchase multiple licenses to treat traveling patients, inflating compliance costs for urgent care apps. Providers can spend up to USD 10,000 yearly on renewals and jurisprudence exams, a burden that deters small practices from joining national urgent care platforms. Compact membership accelerates approval but requires physicians to maintain home-state licenses plus fees in each additional state, preserving administrative drag inside the urgent care apps market. Some vendors hire clinicians as 1099 contractors under employer-of-record entities, yet legal uncertainty around cross-state practice persists and limits venture investment confidence. National legislation remains stalled, meaning licensure complexity will continue to temper adoption curves for the urgent care apps market through 2028.

Limited 5G/Broadband in Rural & Low-Income Areas

Only 46% of households in rural U.S. health-care deserts hold broadband subscriptions, compared with 71% in metro regions, directly suppressing virtual visit completion rates for urgent care apps. A western Tennessee study found patients in ZIP codes with 80-100% broadband were twice as likely to complete tele-urgent visits versus those in 0-20% areas, highlighting infrastructure gaps as a chief bottleneck. Globally, 2.6 billion people lack reliable high-speed internet, meaning large swaths of APAC and Africa remain beyond the urgent care apps market’s effective reach. Satellite broadband pilots offer promise but cost per gigabyte still exceeds affordability thresholds for low-income patients, delaying mass impact until after 2028. Consequently, developers build low-bandwidth chat and store-and-forward modes, although these fall short of full video capabilities envisioned for urgent care apps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By App Category: Post-Hospital Coordination Dominates Transition-of-Care Workflows

Post-hospital apps captured 48.30% of urgent care apps market share in 2025 by bundling discharge summaries, medication reminders, and vitals logging that cut 30-day readmissions by up to 18% among heart-failure cohorts. Payers reimburse these remote-monitoring bundles, giving vendors predictable revenue streams and hospitals shared-savings upside within the urgent care apps market. Pre-hospital emergency and triage tools are set to grow at a 37.85% CAGR as consumers seek AI-guided symptom checks before selecting care settings, easing ED overload. In-hospital collaboration apps hold smaller share yet anchor vendor stickiness by embedding secure chat and lab alerts into clinician workflows, making switching costly for enterprise buyers inside the urgent care apps market. Competitive data show churn below 6% for top post-hospital vendors, highlighting defensible network effects around longitudinal patient datasets.

Segment momentum illustrates a strategic pivot whereby post-acute platforms extend into chronic-care coaching, while triage specialists court employer contracts that monetize avoided ER claims in the urgent care apps market. Interoperability upgrades further secure post-hospital leads because automatic FHIR data exchange makes vendor replacement disruptive to clinical governance. New entrants now carve niches in pediatric follow-up and peri-operative orthopedic care, supported by CPT codes that reimburse specific specialty monitoring inside the urgent care apps market. As employers broaden virtual benefits, post-hospital apps integrate back-to-work certifications, expanding revenue beyond payer contracts. Together these factors sustain double-digit growth across all care-coordination subsegments of the urgent care apps market.

By Platform: iOS Retains Premium Users, Android Broadens Reach

iOS devices represented 53.45% of urgent care apps market size in 2025 because enterprise security officers prefer Apple’s hardware encryption and App Store vetting for HIPAA compliance. Hospital BYOD policies therefore lean iPhone-first, driving clinician usage habits that reinforce iOS dominance in the urgent care apps market. Android downloads, however, are forecast to climb at a 38.40% CAGR as low-cost handsets penetrate APAC and Latin America, expanding total addressable users for urgent care apps. Progressive Web App frameworks now deliver near-native speed across both platforms, letting developers achieve feature parity without doubling code bases inside the urgent care apps market. Web-based portals sustain relevance for older adults who prefer desktops, preserving omnichannel touchpoints even as mobile remains primary for urgent care apps.

Cross-platform biometric sensor parity narrows historic functionality gaps because mid-tier Android phones now ship with FDA-cleared SpO₂ and single-lead ECG chips useful for urgent care triage. Cyber-liability insurers increasingly mandate multi-factor authentication regardless of operating system, further evening the security playing field for urgent care apps. Developers thus reallocate budgets from OS-specific hardening toward AI personalization engines that improve engagement metrics inside the urgent care apps market. As handset prices fall below USD 150 in India and Indonesia, Android adoption is set to accelerate equitable access to urgent care apps, supporting global expansion goals.

By Clinical Area: Trauma Retains Priority, Stroke Apps Surge

Trauma-oriented platforms held 41.35% of the urgent care apps market share in 2025, anchored in established pre-hospital protocols that require rapid scene-to-OR coordination. Integrated mapping shortens ambulance routing by overlaying trauma-center availability in real time. The urgent care apps market size attributed to stroke care is forecast to climb at a 39.10% CAGR, driven by telestroke reimbursement expansion and AI-enabled imaging triage that identifies large-vessel occlusions within minutes. Cardiac apps benefit from wearable ECG feeds but grow slower given earlier tele-cardiology saturation. Other clinical areas—including dermatology and pediatrics—aggregate the remainder, with mental-health add-ons rising post-pandemic.

Segment spread aligns with outcome sensitivity to minutes saved; trauma and stroke survival curves sharply improve when door-to-needle intervals shrink. Consequently, hospital groups allocate capital toward algorithms that flag ischemic patterns mid-transport. Partnerships between stroke-unit neurologists and rural EMS agencies exemplify the upside: video consults initiated in the ambulance raised tPA eligibility rates by 14% year-on-year.

By End-User: Hospitals Anchor Volume, EMS Adoption Accelerates

Hospitals and clinics controlled 46.00% of the urgent care apps market size in 2025 because integrated delivery networks convert existing patient portals into urgent care entry points. They overlay AI triage chat to redirect non-emergent cases, thus preserving ED capacity. EMS agencies, however, will log a 39.60% CAGR by 2031, outfitting crews with decision-support tablets that pull allergy data before medication administration. Urgent care centers leverage apps to publish wait times and secure upfront payment, whereas direct-to-consumer platforms carve share via subscription models targeting millennials seeking frictionless care.

The shift spotlights growing interoperability between EMS dispatch software and hospital EHRs, enabling automatic population of demographic fields upon patient arrival. This single source of truth trims charting errors and accelerates billing cycles. Hospitals deepen moat by bundling urgent care modules with patient-reported outcomes surveys, feeding quality-based reimbursement metrics.

By Business Model: B2B Stability, Hybrid Momentum

B2B contracts represented 53.10% of the urgent care apps market share in 2025 as payers and employers embraced per-member-per-month fees that hedge utilization risk. Hybrid models, blending institutional deals with self-pay consumer tiers, are expected to scale at 40.20% CAGR because they diversify revenue and widen funnel visibility. Pure B2C firms compete on marketing spend and patient experience but face acquisition cost headwinds that squeeze margins.

Hybrid leaders package white-label urgent care services for health plans while selling direct upgrades—like travel telemedicine passes—to individuals. The multi-channel stance reduces churn; enterprise contracts deliver stable baseline revenue while consumer upsell drives margin. As venture funding tightens, unit economics favor operators that amortize fixed R&D across both channels

Geography Analysis

North America held 41.70% of the urgent care apps market share in 2025, benefiting from payment-parity statutes, 5G rollout across 83% of populated areas, and employer-sponsored telehealth benefits adoption topping 64%. The urgent care apps market size in the United States is forecast to keep expanding in double digits, although growth moderates as penetration among insured adults plateaus. Canada boosts regional totals by leveraging a single-payer model that reimburses virtual visits nationwide, offsetting shortages of rural clinicians. Mexico’s IMSS digital strategy indicates early momentum yet faces fragmentation across private insurers.

Asia-Pacific will post a 40.60% CAGR through 2031, driven by India’s Ayushman Bharat Digital Mission and China’s 5G-enabled hospital networks. Smartphone ownership exceeds 70% in urban India, translating to wider addressable bases for Android-first urgent care apps. Japan and South Korea enact regulatory sandboxes that streamline device approval, accelerating integration of wearables with triage software. However, linguistic diversity and physician-shortage clusters complicate unified deployment; thus, localization partnerships remain critical.

Europe grows steadily on back of NHS England’s Long Term Plan, which earmarks GBP 2.8 billion for digital urgent and emergency pathways. Germany’s DiGA Act allows reimbursement for certified health apps, spurring German-language triage tools. Scandinavia achieves near-universal broadband and leads on 112-app tie-ins that route emergency calls with video feeds. Southern Europe lags due to fragmented private-public payment systems but shows upside in expatriate populations demanding English-language telehealth.

South America and the Middle East & Africa contribute smaller shares but feature compelling pockets: Brazil’s SUS-supported tele-emergency program triples encounter volume annually, while Gulf Cooperation Council states subsidize 5G to attract medical tourists. Infrastructure gaps persist—4G coverage remains below 50% in Sub-Saharan Africa—but satellite broadband trials by low-Earth-orbit constellations may compress timelines.

Competitive Landscape

First-mover scale and data network effects define current advantage, yet moderate fragmentation persists as specialized challengers differentiate on AI depth or vertical integration. Teladoc Health posted USD 2.6 billion revenue in 2023 and completed 18.4 million visits, leveraging a pan-condition portfolio spanning urgent care, chronic management, and mental health [SEC.GOV]. American Well serves 50 health plans and 115 health systems, reinforcing B2B strength through white-label modules. CVS Health integrates retail clinics, payer data, and pharmacy fulfillment, forging an end-to-end consumer journey that rivals pure-play platforms.

Niche innovators like K Health secure loyalty via AI-driven symptom triage that resolves 80% of encounters asynchronously, reducing clinician touchpoints and price. Pulsara and Allm specialize in EMS-hospital hand-off, embedding HIPAA-secure chat, timelines, and vitals feeds that slice transfer delays. TigerConnect and DexCare focus on clinician-workflow optimization, while Ada Health and Buoy Health license symptom-checking APIs to insurers seeking top-of-funnel engagement.

Acquisition themes center on behavioral-health capacity and employer footprint expansion. Teladoc bought UpLift for USD 30 million and Catapult Health for USD 65 million in 2025, adding shared-savings chronic-condition modules. Avel eCare’s purchase of Amwell Psychiatric Care extends tele-psychiatry to 46 states, preserving market relevance as mental-health parity laws tighten. Strategic investors increasingly tilt toward workflow orchestration rather than standalone video consult tools, betting that stickiness hinges on deep EHR integration.

White-space opportunities lie in rural markets starved of broadband, where store-and-forward or low-bandwidth chat may unlock latent demand. Pediatric urgent care remains underserved outside metro hubs, and occupational health for gig-economy workers lacks coherent national networks. Players able to combine AI triage, prescription delivery, and asynchronous care inside licensure-compliant shells stand to seize these niches.

Urgent Care Apps Industry Leaders

CommuniCare Technology, Inc. (Pulsara)

Stryker (Vocera Communications)

Twiage Solutions Inc.

Allm Inc.

Baxter International (Hill-Rom)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Hartford HealthCare partnered with K Health to launch an AI-powered virtual primary-care platform, tightening links between urgent and longitudinal care

- January 2025: Avel eCare acquired Amwell Psychiatric Care to widen behavioral health coverage to 46 states

Global Urgent Care Apps Market Report Scope

Urgent care apps are used by healthcare facilities to manage and connect various departments and physicians. These communication apps have higher data privacy security and often meet compliance requirements, such as the Health Insurance Portability and Accountability Act (HIPAA).

The urgent care apps market is segmented by type, clinical area, and geography. By type, the market is segmented into pre-hospital emergency care & triaging apps, in-hospital communication & collaboration apps, and post-hospital apps. By clinical area, the market is segmented into trauma, stroke, cardiac conditions, behavioral health, and other clinical areas. By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World). The report offers the value (in USD) for the above segments.

| Pre-hospital Emergency & Triage Apps |

| In-hospital Communication & Collaboration Apps |

| Post-hospital Care-coordination Apps |

| iOS |

| Android |

| Web-based |

| Trauma |

| Stroke |

| Cardiac Conditions |

| Other Clinical Areas |

| Hospitals & Clinics |

| Urgent Care Centers |

| Emergency Medical Services (EMS) |

| Patients / Consumers |

| B2B |

| B2C |

| Hybrid |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa |

| By App Category | Pre-hospital Emergency & Triage Apps | |

| In-hospital Communication & Collaboration Apps | ||

| Post-hospital Care-coordination Apps | ||

| By Platform | iOS | |

| Android | ||

| Web-based | ||

| By Clinical Area | Trauma | |

| Stroke | ||

| Cardiac Conditions | ||

| Other Clinical Areas | ||

| By End-User | Hospitals & Clinics | |

| Urgent Care Centers | ||

| Emergency Medical Services (EMS) | ||

| Patients / Consumers | ||

| By Business Model | B2B | |

| B2C | ||

| Hybrid | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the projected value of urgent care apps worldwide by 2031?

The market is expected to reach USD 28.84 billion, growing at a 37.32% CAGR over 2026-2031.

Which segment currently holds the largest share within urgent care applications?

Post-hospital care-coordination apps led in 2025 with a 48.30% share.

Which geographic region shows the fastest growth outlook for urgent care applications?

Asia-Pacific is set to expand at a 40.60% CAGR through 2031.

How are health systems improving patient access through technology?

They deploy digital front-door apps that integrate scheduling, AI triage, and EHR data, driving triple-digit download growth.

Page last updated on: