Healthcare Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.83 Billion |

| Market Size (2031) | USD 2.72 Billion |

| Growth Rate (2026 - 2031) | 26.92% CAGR |

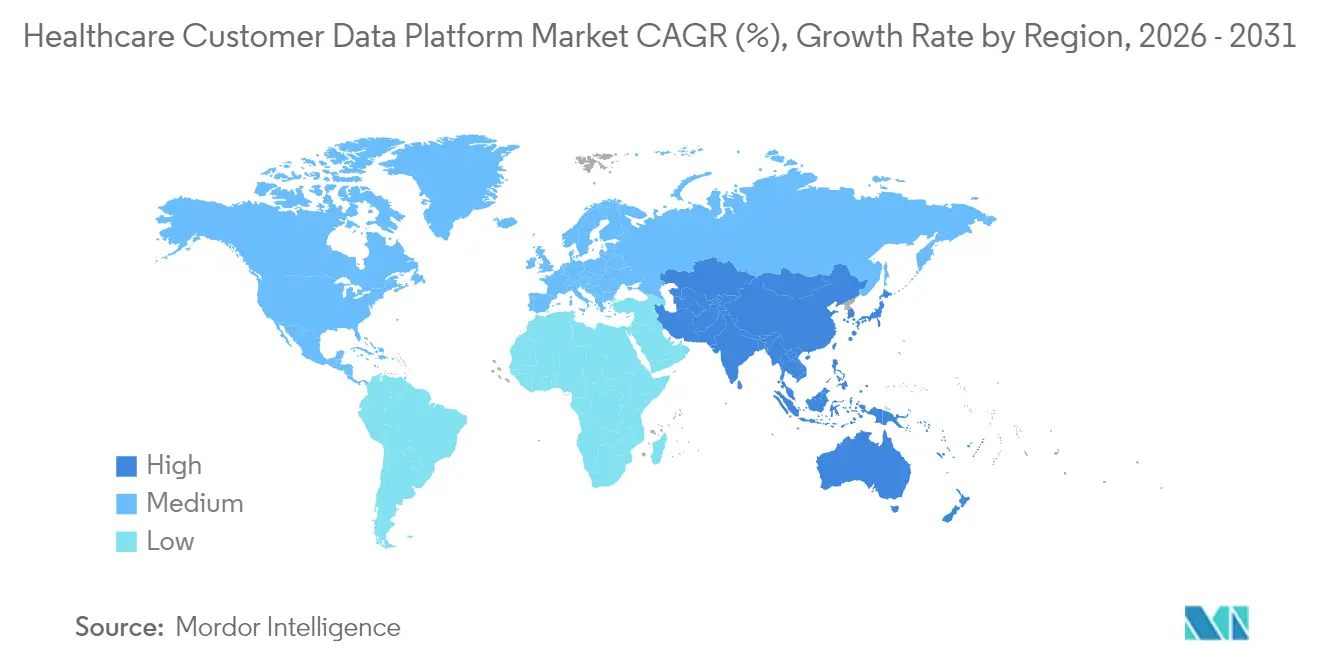

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Customer Data Platform Market Analysis by Mordor Intelligence

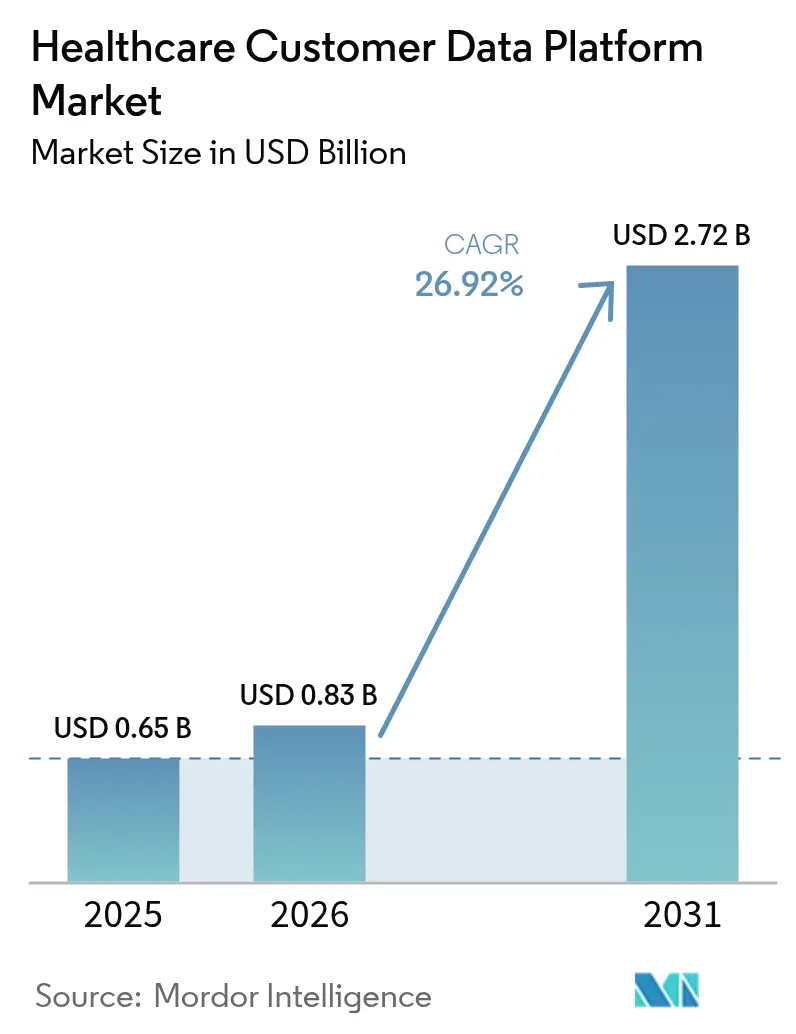

The healthcare customer data platform market size is expected to grow from USD 0.65 billion in 2025 to USD 0.83 billion in 2026 and is forecast to reach USD 2.72 billion by 2031 at 26.92% CAGR over 2026-2031. Expanding cloud adoption, accelerating value-based care contracts, and TEFCA-driven interoperability deadlines are prompting providers, payers, and health-tech firms to prioritize data-centric architectures that support real-time analytics. Heightened demand for AI-ready data pipelines and composable platform design is pulling investment toward vendors that bundle governance, identity resolution, and consent management in a single stack. Meanwhile, the shift toward outcome-based reimbursement is widening the addressable base as even mid-tier hospitals look for tools that convert raw records into engagement-ready insights. North America still commands the largest installed base, yet Asia-Pacific’s rapid digital-health build-out positions it as the growth engine for the next five years.

Key Report Takeaways

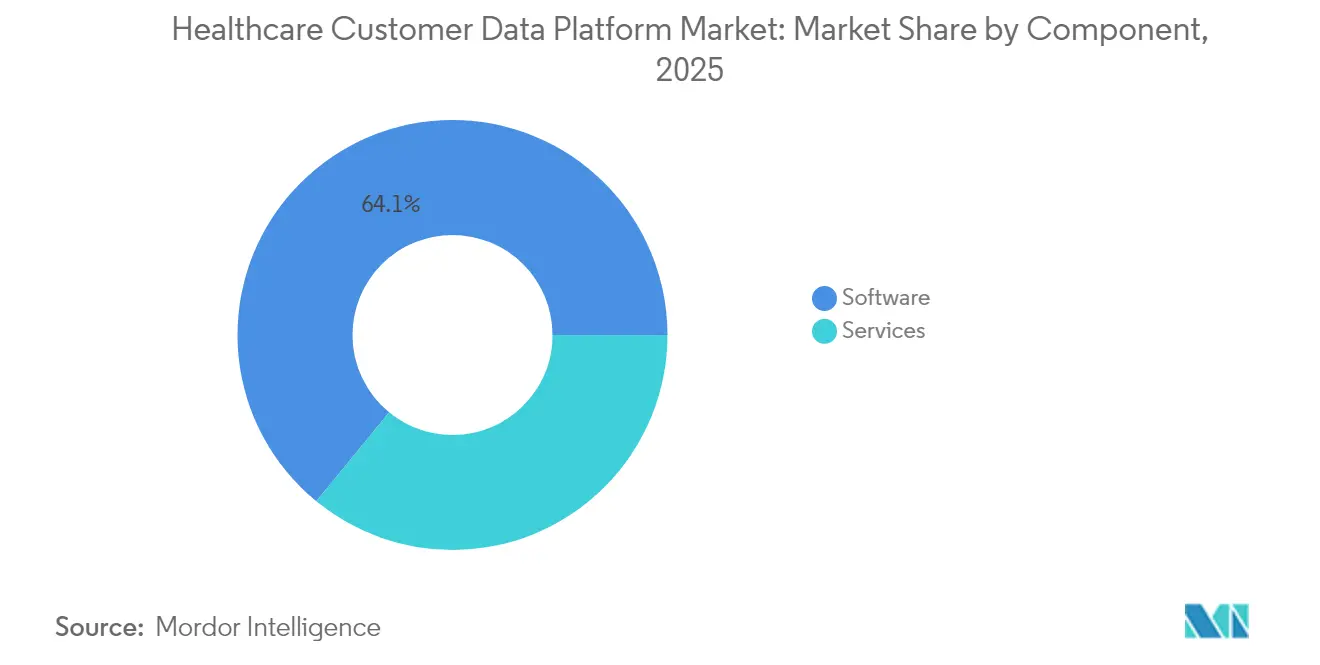

- By component, software solutions led with 64.08% revenue share in 2025, while services are projected to expand at a 27.74% CAGR through 2031.

- By deployment mode, cloud platforms captured 30.22% of the healthcare customer data platform market share in 2025; on-premise deployments are forecast to grow 27.22% annually to 2031.

- By organization size, SMEs accounted for the highest growth, advancing 27.41% each year, whereas large enterprises held 22.21% revenue share in 2025.

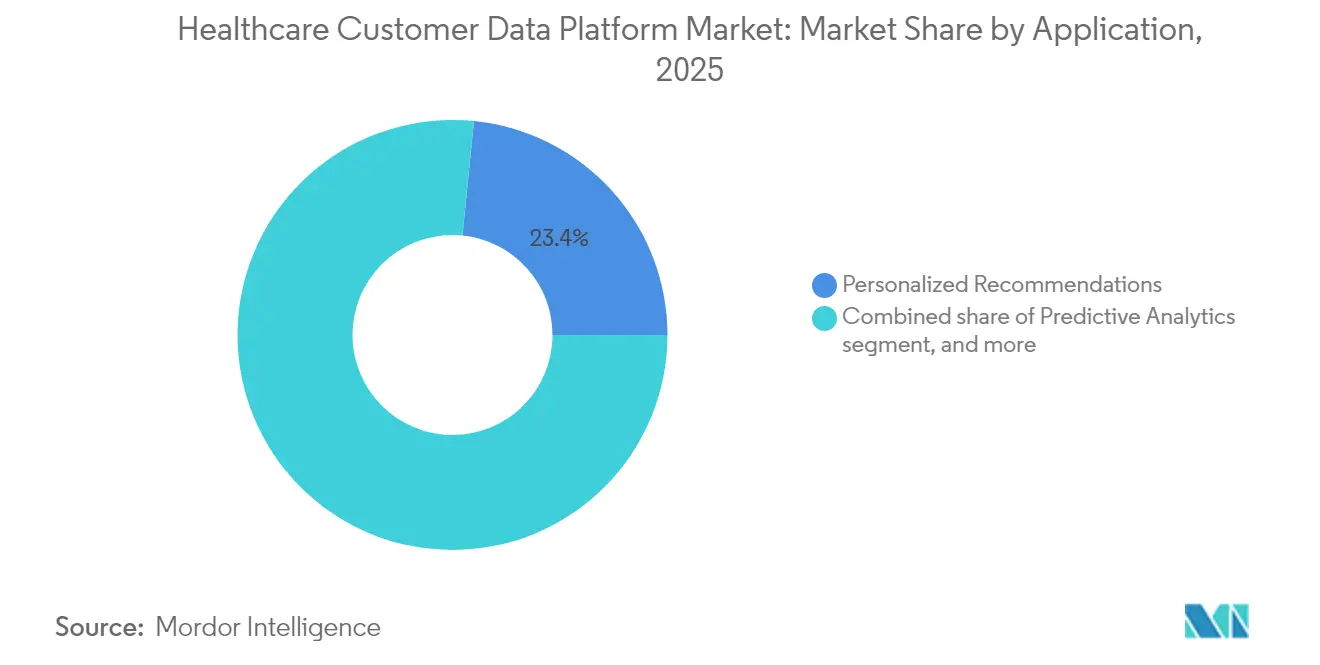

- By application, personalized recommendation engines commanded 23.41% of the healthcare customer data platform market size in 2025, but customer retention tools are set to rise 27.85% per year through 2031.

- By end user, healthcare providers held 25.30% share in 2025; health-tech startups record the fastest uptake with a 28.71% CAGR.

- By geography, North America dominated with 41.98% share in 2025, while Asia-Pacific is pacing at a 27.96% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Healthcare Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Digital Transformation Across Healthcare Ecosystem | +8.2% | Global, with North America and Europe leading adoption | Medium term (2-4 years) |

| Regulatory Push For Data Interoperability Standards | +6.8% | North America primary, expanding to APAC and Europe | Long term (≥4 years) |

| Rising Demand For Personalized Patient Engagement | +5.4% | Global, higher penetration in developed markets | Short term (≤2 years) |

| Growth Of Value-Based Care And Risk-Sharing Models | +4.1% | North America and Europe core, emerging in APAC | Medium term (2-4 years) |

| Proliferation Of Cloud-Native And Composable Data Platforms | +3.8% | Global, accelerated by remote-care trends | Short term (≤2 years) |

| Expansion Of Retail And Consumer-Led Healthcare Channels | +2.9% | North America and Europe primary, selective APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Digital Transformation Across Healthcare Ecosystem

Hospitals, payers, and life-science firms are modernizing data stacks to break silos, support omnichannel care, and cut operating cost. A multinational drugmaker now processes 9 TB of multi-source data daily to power 200+ analytics use cases that span clinical trial optimization, supply-chain visibility, and patient services. Similar modernizations are multiplying as CIOs replace patchwork integrations with unified customer data environments capable of real-time rules-based orchestration. The healthcare customer data platform market is consequently shifting toward native connectors for leading EHR suites, FHIR-compliant data models, and low-code configuration that reduces implementation windows from quarters to weeks. Demand is strongest where cloud spending and DevOps culture are mature; yet even conservative systems adopt pilot platforms to prepare for inevitable interoperability mandates.

Regulatory Push for Data Interoperability Standards

The Trusted Exchange Framework and Common Agreement (TEFCA) rollout and the HTI-2 rule compel providers to offer FHIR-based APIs and expanded USCDI v4 data sets. Compliance deadlines mean organizations must unify consent, identity reconciliation, and audit logging in a scalable platform rather than bolt-on modules. Vendors that provide pre-certified policy engines and automated data provenance tracking gain clear advantage in the healthcare customer data platform market. Forward-thinking health systems treat the rule set as a catalyst to monetize data partnerships and enable pan-regional care coordination[1]U.S. Department of Health & Human Services, “Trusted Exchange Framework and Common Agreement (TEFCA),” hhs.gov.

Rising Demand for Personalized Patient Engagement

Consumers increasingly weigh digital convenience and tailored communications when selecting providers. Surveys show 69% would switch if messaging preferences are unmet, putting direct revenue at risk. Successful outreach programs—such as text-based mammography reminders that delivered a 45% response rate—illustrate how granular segmentation boosts both health outcomes and service line revenue. Customer data platforms with built-in next-best-action engines now integrate clinical, behavioral, and social-determinant signals to trigger proactive nudges, improve adherence, and reduce no-show rates. As competitive healthcare markets mimic retail loyalty tactics, targeted engagement will remain a headline driver of the healthcare customer data platform market[2]Artera Health, “Patient Engagement Case Studies,” artera.io.

Growth of Value-Based Care and Risk-Sharing Models

The migration from fee-for-service toward capitation and shared-savings contracts depends on longitudinal data that pinpoints high-risk cohorts and tracks outcome metrics in near real time. National payer portfolios already cover tens of millions of value-based lives, forcing provider groups to operationalize risk adjustment, quality gap closure, and cost management analytics. Platforms that ingest claims, EHR, device, and community data to produce on-demand population heat maps are becoming table stakes. These capabilities directly link to payer incentive structures, propelling adoption among accountable-care organizations and primary-care disruptors alike.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Fragmentation Of Legacy Health IT Systems | -4.6% | Global, higher impact in established healthcare markets | Long term (≥4 years) |

| Escalating Compliance And Data Privacy Expenditures | -3.2% | North America and Europe primary, expanding globally | Medium term (2-4 years) |

| Acute Shortage Of Skilled Health Data Professionals | -2.8% | Global, with severe shortages in developed markets | Long term (≥4 years) |

| Vendor Lock-In And Integration Complexity | -2.1% | Global, particularly affecting large healthcare systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Fragmentation of Legacy Health-IT Systems

Decades of acquisitions and departmental best-of-breed purchases leave health systems juggling multiple EHR instances, radiology archives, and bespoke registries that resist open standards. Harmonizing vocabularies, patient identifiers, and master data is costly and slow, delaying platform rollouts and dampening near-term ROI. Organizations often consult third-party integrators to map old interfaces to HL7 FHIR while sustaining daily operations. This complexity subtracts 4.6 percentage points from the forecast CAGR, making legacy rationalization a prerequisite for broad platform penetration.

Acute Shortage of Skilled Health Data Professionals

By 2037, shortages are projected to include 207,980 registered nurses and 113,930 addiction counselors; parallel deficits exist for data engineers, informaticists, and analytics translators. The talent crunch inflates salary demands and lengthens hiring cycles, forcing providers to outsource configuration and managed services. Vendors with turnkey implementation blueprints or AI-driven data quality automations can offset skill gaps, but staffing scarcity remains a brake on expansion until workforce pipelines mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominance Drives Platform Innovation

Software captured 64.08% revenue in 2025 as buyers gravitated toward end-to-end suites that deliver patient identity resolution, consent management, and predictive analytics out of the box. The healthcare customer data platform market size for software stood at USD 0.42 billion and is tracking a healthy double-digit CAGR supported by modular upgrades and subscription pricing. Services, however, are climbing faster at 27.74% per year because complex migrations require deployment, data-mapping, and change-management expertise.

Over 2026-2031, managed services bundling hosting, monitoring, and template analytics are expected to gain share as hospitals move to opex-friendly contracts. Vendors increasingly package clinical content libraries and pre-trained AI to compress time-to-value for mid-tier providers. This momentum will gradually narrow the gap, yet software will remain the primary revenue engine of the healthcare customer data platform market.

By Deployment Mode: Cloud Migration Accelerates Despite Security Concerns

Cloud deployments held 30.22% of the healthcare customer data platform market share in 2025, fueled by the scalability needed for compute-hungry AI workloads and remote-care use cases. Many networks adopt hybrid models, retaining PHI-heavy workloads on-premise while bursting analytics into public clouds, to meet sovereignty rules.

On-premise solutions, growing 27.22% annually, still appeal to institutions bound by stricter regional privacy statutes or limited bandwidth. Edge appliances that synchronize with cloud cores are bridging the divide, enabling algorithm training without exporting raw patient data. This coexistence will persist, reflecting divergent risk appetites and regulatory nuance across jurisdictions.

By Organization Size: SMEs Drive Innovation While Enterprises Scale

Large enterprises represented 22.21% revenue in 2025, leveraging big budgets to stitch platforms into sprawling, multi-site frameworks. Their adoption path often spans multi-phase rollouts anchored by center-of-excellence teams and six-figure service engagements.

Conversely, SMEs are expanding 27.41% yearly as SaaS offerings reduce capital outlay and pre-integrated connectors sidestep IT bottlenecks. Pay-as-you-grow licensing and template use cases, population outreach, referral leakage analysis, no-show prediction, help smaller hospitals punch above weight. This shift democratizes advanced capabilities and injects fresh product feedback that shapes vendor roadmaps.

By Application: Customer Retention Emerges as Strategic Priority

Personalized recommendation engines held 23.41% of segment revenue in 2025 thanks to proven lifts in care-gap closure, medication adherence, and ancillary service uptake. Yet customer retention modules are forecast to outpace all cohorts at 27.85% CAGR as competition intensifies for lifetime patient value.

Predictive churn scores, loyalty program triggers, and social-determinant alerts sit at the heart of these modules, directing staff to intervene before dissatisfaction escalates. Marketing segmentation, care coordination, and security management round out the toolkit, reflecting the platform’s evolving role from engagement support to full-cycle relationship orchestration within the healthcare customer data platform industry.

By End User: Health-Tech Startups Accelerate Market Innovation

Providers commanded 25.30% of revenue in 2025, propelled by reimbursement pressure and population-health mandates. Their implementations emphasize bidirectional EHR connectors and quality reporting dashboards.

Health-tech startups, surging 28.71% annually, leverage nimble governance structures to pilot AI-enabled triage bots, digital-front-door apps, and at-home monitoring loops. Their rapid iteration drives vendor innovation and often seeds white-label offerings for larger incumbents. Payers, med-tech, and life-science firms add incremental demand via clinical-trial recruitment and member portal personalization, underscoring the ecosystem-wide relevance of the healthcare customer data platform market.

Geography Analysis

North America held 41.98% of global revenue in 2025, a position reinforced by early TEFCA milestones, mature cloud penetration, and large-scale value-based contracts that depend on robust data orchestration. Multi-state networks such as Kaiser Permanente deploy enterprise platforms that span claims, EHR, and consumer apps, validating scalability and influencing procurement standards across the healthcare customer data platform market.

Asia-Pacific is on a 27.96% CAGR trajectory to 2031 thanks to government-funded digital-health programs, fast-growing middle classes, and venture-backed provider disruptors. China, India, Japan, and Australia lead spend, but Southeast Asia’s hospital chains and insurance hybrids are closing the gap through cloud-first greenfield builds. As electronic health-record density rises, regional stakeholders harness platforms to enable remote consults, chronic-disease management, and cross-border medical tourism.

Europe’s steady progression is shaped by stringent GDPR safeguards that elevate demand for consent orchestration, federated analytics, and anonymization modules. Initiatives to create pan-EU health-data spaces position customer data platforms as foundational infrastructure for research and secondary-use governance. Emerging markets in the Middle East, Africa, and South America remain nascent yet increasingly prioritize national-level interoperability frameworks that mirror TEFCA principles, opening long-tail expansion opportunities over the next decade.

Regulatory Landscape

In the United States, HIPAA remains the core compliance baseline for healthcare customer data platforms handling ePHI, with HHS OCR pushing initiatives that raise security and documentation requirements for covered entities and business associates. In December 2024, OCR issued a proposed rule to modify the HIPAA Security Rule to strengthen cybersecurity protections, while court-driven adjustments tied to the 2024 Reproductive Health Care Privacy Rule set a February 16, 2026 compliance date for specific NPP modifications. This combination increases pressure on providers, payers, and their CDP vendors to tighten patient-facing transparency and downstream data-handling workflows.

In Europe, EHDS Regulation EU 2025/327 entered into force in March 2025, and Commission Implementing Regulation (EU) 2026/771 established the EHDS Board to coordinate Member State implementation. For CDP deployments, the shift elevates consent orchestration, auditability, and standardized exchange across the EU. ISO/TS 27790:2026 and WHO SMART Guidelines efforts reinforce structured document registry and interoperability patterns, favoring platforms built around common data models and exchange frameworks rather than bespoke integrations.

Competitive Landscape

Competition is moderate, with diversified tech majors and healthcare-focused specialists jockeying for share. Microsoft, Salesforce, and Oracle leverage existing cloud ecosystems and enterprise footprints to cross-sell customer data modules bundled with analytics and collaboration suites. Epic Systems embeds patient-centric data hubs into its EHR backbone, lowering integration friction for its extensive customer base.

Specialists such as Innovaccer, Health Catalyst, and Treasure Data differentiate through healthcare-specific ontologies, out-of-the-box quality-measure libraries, and clinician-friendly UX that reduce training overhead. Innovaccer’s platform scored 93.6/100 in a 2024 customer satisfaction survey, reflecting the premium on real-world outcomes.

Strategic alliances and M&A are intensifying: HEALWELL acquired Orion Health to combine interoperability IP with AI pipelines, while Reveleer folded Curation Health into its value-based care suite to deepen clinical-insight capture. Cloud vendors court domain expertise through co-innovation labs—AWS pairs with venture fund General Catalyst to incubate AI prediction models—signaling that ecosystem collaboration is the next battleground for the healthcare customer data platform market.

Healthcare Customer Data Platform Industry Leaders

Microsoft

Salesforce.com

Adobe

Oracle

Innovaccer Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory-operational interoperability requirements are expanding CDP use cases beyond marketing and engagement into administratively governed data exchange, with a clearer line to API performance outcomes. Under CMS interoperability policy, payers began annual reporting of Patient Access API usage metrics to CMS in January 2026 for calendar year 2025, with reporting due by March 2026, and CMS-0057-F provisions began taking effect in January 2026. This creates a tighter fit for CDPs that unify identity resolution, consent, and audit logging across member and patient data, while also producing compliance-grade usage metrics and supporting FHIR-based workflows, including prior authorization APIs.

ASTP/ONC released USCDI v7 in January 2026, and HL7 US Core updates continue alongside the FHIR roadmap. In parallel, Oracle launched the Life Sciences AI Data Platform in January 2026, and CVS Health partnered with Google Cloud in March 2026 to rework consumer engagement and experiences, both of which raise expectations for privacy-by-design, scalable identity, and AI-enabled orchestration.

Recent Industry Developments

- May 2026: Qualtrics completed the acquisition of Press Ganey Forsta for USD 6.75 billion to expand its experience management platform with large healthcare experience datasets. The transaction strengthens consolidation around experience and engagement data, increasing competitive pressure to connect sentiment, service, and clinical-adjacent signals to unified customer profiles. It also raises the bar for CDP and analytics vendors that position patient experience as an input to retention and outreach orchestration.

- March 2026: CVS Health and Google Cloud announced a strategic partnership focused on reimagining healthcare consumer engagement and experiences, including plans connected to an AI-native engagement platform. The initiative signals greater investment by large healthcare incumbents in cloud-based data and AI foundations that can activate first-party consumer data across channels. CDP vendors face heightened requirements for interoperability, privacy controls, and integration into broader cloud ecosystems used by payers and providers.

- January 2026: Oracle announced the Oracle Life Sciences AI Data Platform, a generative AI-enabled solution designed to unify customer data with de-identified longitudinal Oracle Health real-world data. This extends the CDP adjacency into life sciences and commercialization workflows, where governed data linking and scalable identity resolution are central.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the healthcare customer data platform (CDP) market covers software platforms used by healthcare organizations to unify patient or member data from multiple systems into a single profile that supports engagement, analytics, and compliant data use.

Scope exclusions: We exclude generic CRM and marketing suites when they do not have CDP-grade identity resolution and profile unification built into the core product.

Segmentation Overview

- By Component

- Software

- Services

- By Deployment Mode

- On-Premise

- Cloud-Based

- By Organization Size

- Large Enterprises

- Small & Medium-Sized Enterprises

- By Application

- Personalized Recommendations

- Predictive Analytics

- Marketing Data Segmentation

- Customer Retention & Engagement

- Security Management

- Other Applications

- By End User

- Healthcare Providers

- Payers

- Life-Science & Med-Tech Firms

- Healthtech Start-Ups

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by mapping what a healthcare CDP is expected to do in real deployments, then listing the demand points where it is purchased and used. We refer to public sources such as ONC interoperability updates (including FHIR-related programs), CMS rules and program documentation, and HHS HIPAA guidance to keep the compliance and data-handling boundaries aligned.

For digital adoption and spending direction, we also use sources such as OECD health statistics, the World Bank for macro indicators, and peer-reviewed articles indexed in repositories like PubMed to cross-check adoption drivers such as patient engagement and data integration needs.

Next, we connect these demand inputs to market supply signals using company filings, earnings call commentary, product notes, and reputable press coverage. This helps validate what vendors position as a CDP versus adjacent tools. Where available, paid database subscriptions support company financials and news screening, patent lookups inform identity resolution and consent workflow details, and contract or tender tracking helps identify larger health system and public sector purchases. The desk sources above are illustrative rather than exhaustive, since many additional public documents and datasets were also consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary research was used to confirm how buyers define a healthcare CDP in practice and what typically gets budgeted under this line item, especially across payers, provider systems, and digital health operators. We interviewed and surveyed product leaders, data and analytics heads, marketing and patient engagement owners, and implementation partners across major regions. This approach was used to check and correct assumptions on deployment mix, pricing, and adoption timing.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 15% | APAC: 48% |

| Mid tier: 50% | Functional/Unit leaders: 34% | EMEA: 31% |

| Smaller Players: 19% | Managers: 51% | Americas: 21% |

Market-Sizing & Forecasting

Sizing is built using top-down and bottom-up logic together. The top-down view is anchored on healthcare IT spend direction and the share of that spend that typically flows into customer and patient data unification platforms. We then corroborate the totals using selective bottom-up approximations, where sampled vendor revenue splits, typical contract values by buyer type, and channel checks from implementation partners are used to sanity check the overall range.

When a product bundle includes adjacent modules, we handle gaps by applying interview-backed allocation rules so only CDP-relevant revenue is counted. Key model inputs include the pace of cloud adoption in healthcare data workloads, the rollout of interoperability and data access requirements, the number of covered lives and patient volumes served by large payers and provider networks, the rate of digital front door and patient engagement program expansion, and the typical pricing progression as deployments move from pilots to enterprise scale.

Forecasting mainly uses scenario analysis, since regulation timing, budget cycles, and platform consolidation can shift adoption faster or slower. Scenarios are then reviewed with experts to select a practical base case.

Data Validation & Update Cycle

Validation is done through a set of cross-checks so the final number aligns with what buyers can reasonably purchase and deploy in the period. We compare outputs against independent signals such as large health system digital investment announcements, contract activity, and the direction of healthcare software revenue commentary. We also investigate any spikes that do not fit observed adoption patterns.

Before sign-off, a second analyst reviews the model math, key assumptions, and currency conversions to explain and document any variance. Reports are refreshed annually, and interim updates are made when material events arise, such as major regulation changes, a large acquisition that reshapes product scope, or a clear pricing shift. Right before delivery, we run a final review pass to ensure the client gets the most current view available at that time.

Mordor Intelligence's Healthcare Customer Data Platform Market Sizing Compared With Other Published Estimates

Published market sizes for healthcare CDPs often differ because firms draw the product scope differently and do not always treat bundled modules the same way. Timing also affects results, because some estimates use older base years, and currency handling can shift USD totals.

By checking inclusion rules for identity resolution and profile unification, and refreshing base-year allocation assumptions, Mordor Intelligence keeps the number focused on CDP platforms used in healthcare, instead of counting broader CRM suites or data warehousing tools that may be purchased alongside.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.83 B (2026) | |

| Industry PR Release A | USD 0.54 B (2023) | This estimate uses an earlier base year and is often presented with combined software and services, which can compress the platform-only total and make later adoption waves harder to see. |

| Publisher Release B | USD 0.88 B (2024) | The described scope is broad, and the result can shift depending on whether adjacent engagement modules and data infrastructure are included as part of the CDP spend line. |

Overall, the spread in values is mainly explained by base-year choice and how closely the model separates CDP platform revenue from neighboring healthcare software categories. Our steps are designed to be repeatable because key inputs are tied to adoption signals, pricing checks, and interview confirmations before the totals are finalized.

Key Questions Answered in the Report

What is driving the rapid growth of the healthcare customer data platform market?

Growth stems from regulatory interoperability mandates, rising demand for personalized patient engagement, and the migration to value-based care models that require unified, analytics-ready data sets.

How large is the healthcare customer data platform market today?

The healthcare customer data platform market size stands at USD 830 million in 2026 and is forecast to reach USD 2.72 billion by 2031.

Why are small and medium-sized healthcare organizations adopting these platforms?

SMEs benefit from SaaS pricing, pre-configured healthcare data models, and low-code interfaces that deliver enterprise-grade analytics without large IT teams.

Which component segment is expanding the fastest?

Services are growing quickest at a 27.74% CAGR because providers need implementation, integration, and optimization support as platforms become more complex.

Which region will add the most new revenue by 2031?

Asia-Pacific is projected to contribute the most incremental revenue, pacing at a 27.96% CAGR as governments invest in digital-health infrastructure.

How does a customer data platform improve value-based care performance?

By aggregating claims, clinical, and social-determinant data, the platform enables real-time risk stratification and targeted interventions that directly influence quality scores and shared-savings payouts.

Page last updated on: