Home Healthcare Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

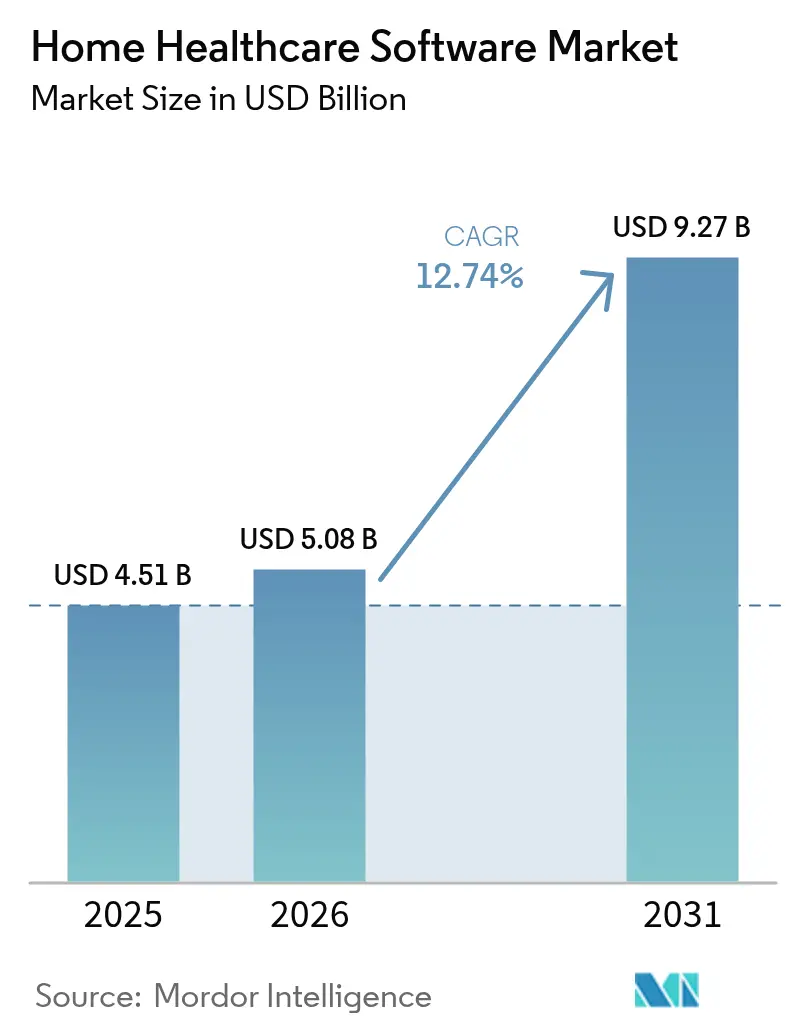

| Market Size (2026) | USD 5.08 Billion |

| Market Size (2031) | USD 9.27 Billion |

| Growth Rate (2026 - 2031) | 12.74% CAGR |

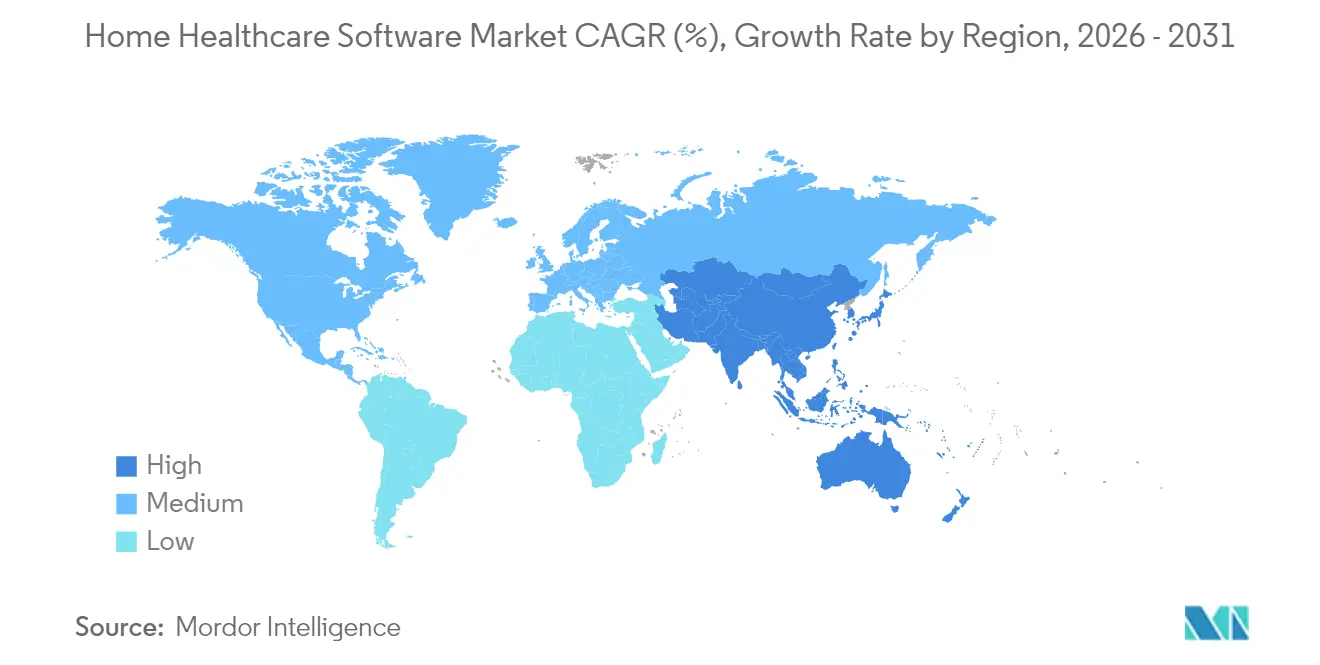

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Home Healthcare Software Market Analysis by Mordor Intelligence

The home healthcare software market size is expected to grow from USD 4.51 billion in 2025 to USD 5.08 billion in 2026 and is forecast to reach USD 9.27 billion by 2031 at 12.74% CAGR over 2026-2031. Demand is rising as payers reward value-based care, health systems push more complex treatments into the home, and reimbursement rules increasingly link payment to documented outcomes. Electronic visit verification (EVV) mandates, especially those tied to Medicaid funding, further increase software adoption by making digital documentation a condition for payment. Cloud deployment lowers total cost of ownership by about 77% versus on-premises alternatives, making the delivery model attractive for agencies of all sizes[1]BioT Medical, “Benefits of Moving from On-Premises to Cloud-Based Solutions for Medical Devices,” biot-med.com. Strong venture funding and strategic acquisitions by established vendors accelerate innovation in analytics, remote monitoring, and AI-driven revenue cycle tools. Finally, payers and providers are experimenting with hospital-at-home programs, which depend on interoperable platforms capable of orchestrating acute care in residential settings.

Key Report Takeaways

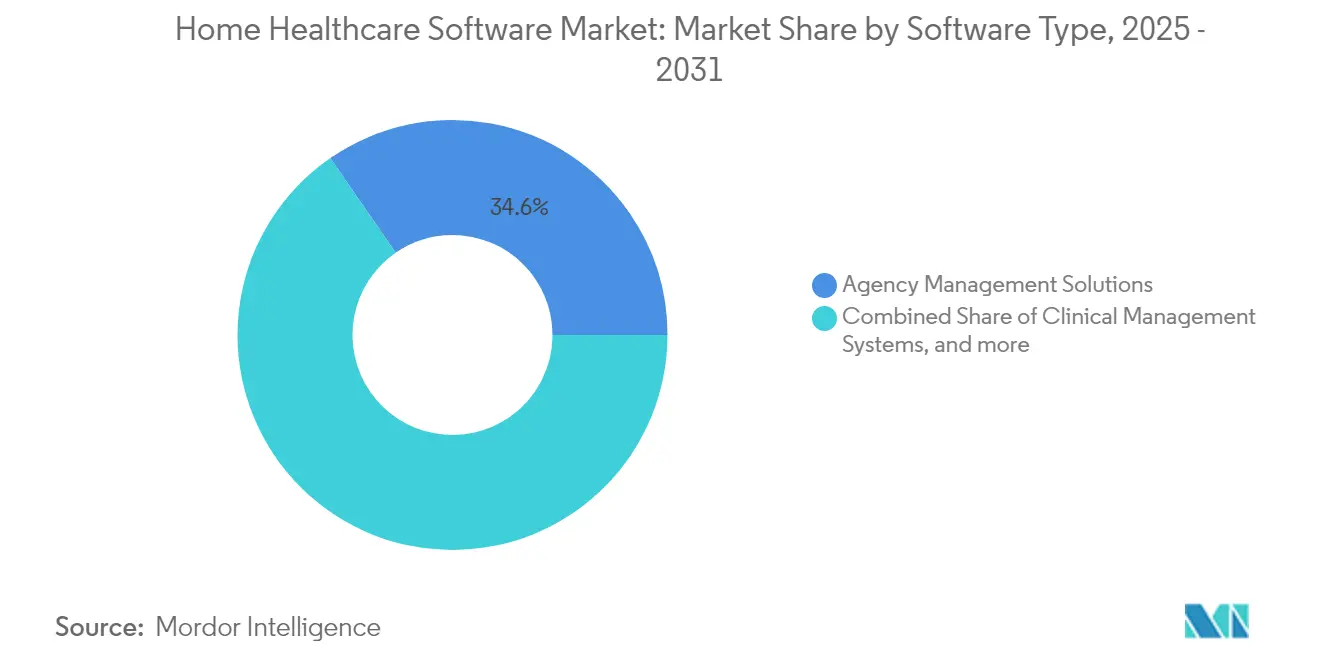

- By software type, Agency Management Solutions led with 34.62% revenue share in 2025; Other Software is projected to expand at a 14.97% CAGR to 2031.

- By service, Skilled Nursing held 41.28% of the home healthcare software market share in 2025, while Infusion Therapy is advancing at a 13.72% CAGR through 2031.

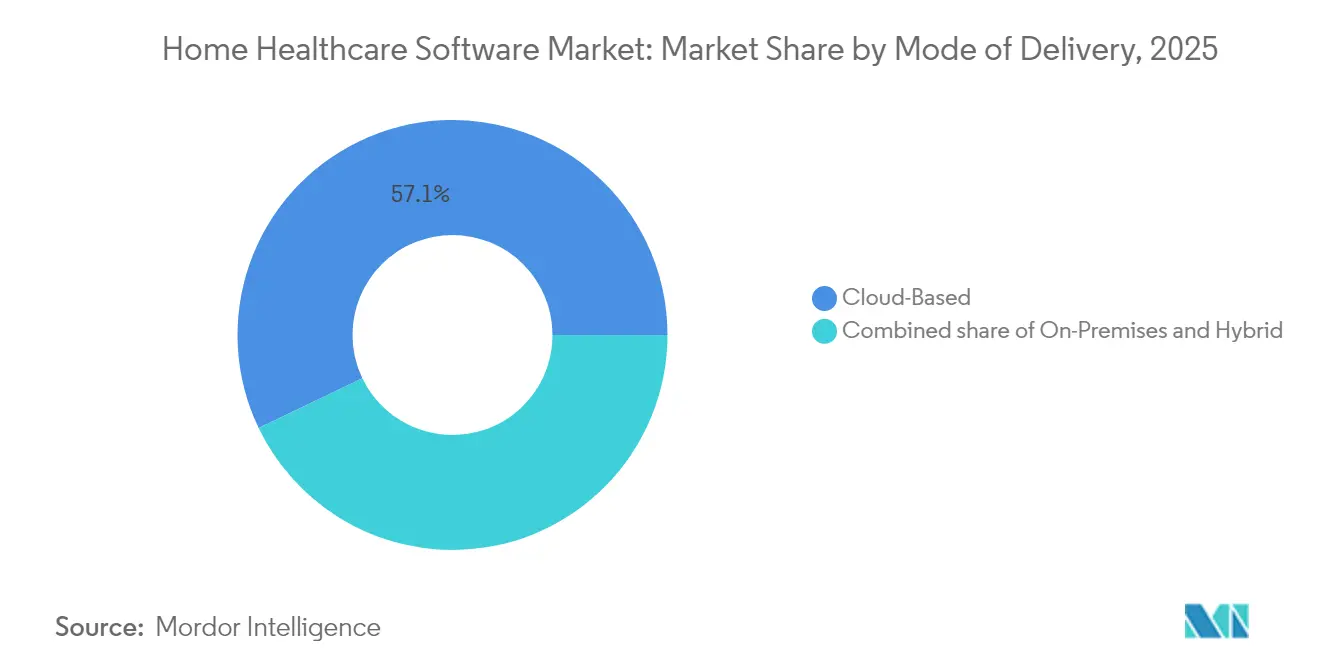

- By mode of delivery, Cloud-based platforms captured 57.12% of the home healthcare software market size in 2025 and will grow at 14.22% CAGR between 2026-2031.

- By end-user, Home Health Agencies accounted for 60.02% of the home healthcare software market size in 2025; the Other End-Users segment is rising fastest at 12.98% CAGR.

- By region, North America accounted for the highest market share of 41.55%; Whereas, Asia-Pacific is anticipated to frow at a fastest CAGR of 13.66% by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Home Healthcare Software Market*

| Drivers Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift to value-based care | +2.1% | North America | Medium term (2-4 years) |

| EVV compliance mandates | +1.5% | North America, Europe | Short term (≤2 years) |

| Cloud deployment economics | +1.2% | Global | Long term (≥4 years) |

| Chronic disease management demand | +1.0% | Global | Long term (≥4 years) |

| Interoperability push across acute, post-acute, and payer systems | +1.3% | Global | Medium term (2-4 years) |

| Venture funding & M&A accelerating digital home-care innovation | +1.1% | Global | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Shift to Value-Based Care Transforming Software Requirements

Payers continue to pivot away from fee-for-service toward models that reward measurable outcomes. UnitedHealth Group reports that coordinated home care can lower hospital admissions by as much as 25% for chronically ill patients[2]UnitedHealth Group, “A Path Forward to a Modern, High-Performing Health System,” unitedhealthgroup.com. Providers now purchase platforms with embedded analytics that track quality metrics, risk scores, and clinical pathways. In states piloting the Home Health Value-Based Purchasing framework, agencies see reimbursement bonuses when software supplies timely, accurate outcome reports. Vendors integrate predictive algorithms to alert staff when patients approach thresholds for readmission, thereby protecting margins in capitated contracts. As pay-for-performance expands, the home healthcare software market becomes mission-critical infrastructure rather than an optional tool.

Electronic Visit Verification Mandates Accelerating Digital Adoption

The 21st Century Cures Act locks EVV into Medicaid reimbursement. States such as Pennsylvania and New York require 85% and 90% EVV compliance respectively by 2025, with payment denials for failures. EVV platforms must verify six data points—service type, recipient, date, location, provider, and time—often through GPS-enabled mobile apps or fixed devices[3]Essential EVV System for Home Care,” timeero.com. Smaller agencies that once relied on paper processes are now adopting digital visit capture to stay licensed. Vendors bundle EVV modules into broader suites, creating a gateway to upsell scheduling, billing, and clinical documentation. These mandates compress adoption timelines, producing a step-change in addressable demand for the home healthcare software market.

Cloud-Based Solutions Dominating Market Growth

Cloud deployment holds 58% share and grows 14.5% annually as providers seek lower upfront costs and elastic scalability. Total ownership costs fall by more than three-quarters relative to on-premises setups when factoring maintenance, hardware, and upgrade labor. Asia-Pacific agencies are particularly receptive: rapid digital health initiatives mean cloud workloads now outpace on-prem deployments in new projects[4]Cloud Computing in Healthcare: A Comprehensive Overview,” neklo.com. Interoperability improves because vendors expose APIs and FHIR-based data layers natively in the cloud. Clinicians gain mobile access to schedules, documentation, and real-time patient vitals, which is essential for field-based workflows in home care. The cost advantage, coupled with regulatory support for secure, auditable cloud services, cements the model’s dominance in the home healthcare software market.

Chronic Disease Management Driving Specialized Software Demand

Prevalence of diabetes, heart failure, and COPD is rising, pushing payers to shift monitoring to the home. About 3.2 million patients received home infusion therapy in 2020, and volumes continue to climb as hospitals seek to reduce inpatient drug administration costs. Vendors respond with modules that integrate Bluetooth-enabled glucose meters, blood pressure cuffs, and infusion pumps, allowing nurses to oversee adherence remotely. Telehealth usage remains 38 times higher than pre-pandemic baselines, demonstrating sustained patient comfort with virtual check-ins. AI engines triage alerts so clinicians act on only the most urgent exceptions, preserving labor resources and improving satisfaction scores. As chronic care consumes a growing slice of healthcare spending, the home healthcare software market evolves toward disease-specific functionality layered on foundational agency workflows.

Restraints Impact Analysis of Home Healthcare Software Market*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data security concerns | −1.6% | North America, Europe | Short term (≤2 years) |

| Reimbursement complexity | −1.3% | United States | Medium term (2-4 years) |

| Limited IT budgets & change-management barriers in small agencies | −1.2% | Global | Short term (≤2 years) |

| Integration complexity with legacy EHRs and medical devices | −1.0% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Security Concerns Creating Implementation Barriers

Healthcare remains a prime cyber-crime target. A surge in ransomware hits during 2024 forced agencies to reassess risk tolerance, especially when HIPAA fines span USD 100 to USD 50,000 per incident. Smaller providers lack dedicated security staff, slowing decisions on new platforms. Vendors add end-to-end encryption, granular role-based permissions, and audit trails, yet clients still face recurring penetration-testing and compliance audit costs. In Europe, GDPR stipulates strict breach notification windows, raising potential penalties and reputational damage. These factors lengthen sales cycles in the home healthcare software market even as the operational need for digital tools grows unchecked.

Reimbursement Complexity Hampering Software ROI

CMS announced a headline 2.7% payment update for 2025, but after budget-neutral adjustments the effective increase is only 0.5%. Margins remain tight, and agencies scrutinize every technology purchase for rapid payback. Each payer imposes unique requirements for documentation and coding, forcing software to support multiple billing workflows out of the box. Configuring these rules prolongs implementation and delays revenue cycle benefits. The problem is acute for single-state agencies managing dozens of commercial plans on top of Medicare and Medicaid contracts. Vendors invest in AI-powered coding assistance and pre-bill audits to shorten denial resolution time, yet the multiplicity of rules still suppresses the attainable ROI for many buyers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Home Healthcare Software Market Segment Analysis

By Software Type:

Agency Management Solutions Lead While Specialized Tools AccelerateAgency Management Solutions accounted for 34.62% of total revenue in 2025, reflecting their role as the operational backbone for most providers. These platforms consolidate scheduling, payroll, and compliance reporting, enabling even small agencies to coordinate distributed workforces efficiently. Leading suites such as Homecare Homebase and MatrixCare secure long-term contracts by pairing reliable uptime with deep regulatory updates every quarter. The home healthcare software market relies on these core systems as entry points for broader digital transformation.

Growth momentum is shifting toward the Other Software segment, which combines telehealth, remote monitoring, and AI-assisted clinical decision support. That segment is posting a 14.97% CAGR through 2031, outpacing the overall home healthcare software market. Virtual visit platforms maintain usage levels far above pre-pandemic norms, and AI scribes now draft encounter notes directly from video calls. Vendors tightly integrate these niche modules into core agency systems, creating seamless data flows and richer analytics. As payers reimburse remote services at parity with in-person care, specialized solutions carve out growing wallet share across providers.

By Service:

Skilled Nursing Dominates While Infusion Therapy Shows Strongest GrowthSkilled Nursing commands 41.28% of 2025 revenues, confirming its primacy in home-based post-acute care. Hospitals discharge complex cases earlier, and they partner with agencies to prevent readmissions during the 30-day window that affects quality scores. Software for Skilled Nursing prioritizes wound care templates, medication reconciliation, and interdisciplinary care plan coordination. Because nursing visits generate high documentation volume, natural-language processing utilities help clinicians complete notes faster, preserving visit capacity in the home healthcare software market.

Infusion Therapy, though smaller today, advances at a 13.72% CAGR and is the fastest-growing service line. Expensive biologics and specialty drugs once confined to inpatient settings now move to the home, where administration costs drop sharply. Platforms embed inventory management to track bag lot numbers and auto-reorder supplies, minimizing waste. Telepharmacy links let clinicians adjust doses in real-time based on patient vitals, improving safety. The segment’s dynamism illustrates how service diversification broadens the home healthcare software market size for vendors targeting therapy-specific workflows.

By Mode of Delivery:

Cloud-Based Solutions Driving Market TransformationCloud-based deployments hold 57.12% share in 2025 and post the fastest expansion at 14.22% CAGR. Start-ups enter the home healthcare software market with cloud-native architectures that rely on microservices, giving clients continuous feature releases without downtime. Agencies welcome subscription pricing because it aligns cash flows with revenue. Moreover, hospital-at-home models depend on always-on connectivity between hospital command centers and nurses in the field. The resulting demand enlarges the home healthcare software market size available to cloud vendors.

On-premises solutions linger, favored by some hospital-affiliated agencies that integrate directly with in-house EHRs. Hybrid architectures gain traction, placing sensitive PHI behind the firewall while moving scheduling or reporting modules to the public cloud. This transitional posture reassures boards focused on security, yet it still introduces agencies to lower maintenance burdens. Over time, cost comparisons tilt decisively toward full cloud adoption, eroding the legacy footprint in the home healthcare software market.

By End-User:

Home Health Agencies Lead While Diversification AcceleratesHome Health Agencies account for 60.02% of 2025 demand. Their scale ranges from small rural operations to multi-state chains, each looking for platforms that blend compliance, billing, and point-of-care documentation. Because they deliver both post-acute and chronic care, agencies need configurable workflows that span skilled and unskilled services. Vendor roadmaps add integrated learning modules to support onboarding in a tight labor market. This breadth cements agency leadership in the home healthcare software market.

Growth is strongest among Other End-Users such as private duty firms, equipment suppliers, and hospital-at-home operators, which together rise 12.98% annually. Acute-level care in the home requires orchestration across pharmacy, respiratory therapy, and remote diagnostics. Platforms offering open APIs win these contracts because they plug into hospital command centers and payer authorization systems. Hospice providers, representing a stable slice of the home healthcare software market share, seek tools tailored to HOPE reporting requirements and bereavement tracking, further diversifying vendor product lines.

Geography Analysis

North America Home Healthcare Software Market

North America retains 41.55% of global revenue in 2025, propelled by advanced reimbursement models and stringent EVV enforcement that mandates software for every Medicaid visit. The United States alone contributes more than four-fifths of regional spending, while Canada’s single-payer structure supports province-wide platform procurements. Cross-border interoperability remains an agenda item, as agencies serving snowbird populations require data exchange with multiple state Medicaid systems.

APAC Home Healthcare Software Market

Asia-Pacific records the briskest expansion at 13.66% CAGR. Governments in India, China, and Indonesia sponsor digital health missions that fund cloud pilots and telehealth networks. Large private hospital chains open home health divisions to capture post-discharge revenue and reduce inpatient congestion. Rapid smartphone penetration enables mobile clinician workflows without heavy hardware investment, allowing new entrants to leapfrog legacy deployments. These trends enlarge the home healthcare software market size for international vendors capable of local language support and data residency compliance.

EMEA and South America Home Healthcare Software Market

Europe ranks second by revenue, with demand concentrated in Germany, the United Kingdom, and France. Regulators promote cross-border data portability through laws such as the Interoperable Europe Act, creating incentives to invest in standards-based platforms. Agencies must also align with GDPR, reinforcing focus on encryption and consent management. Private insurers in the region pilot outcome-based contracts that mirror U.S. value-based payment schemes, strengthening the case for advanced analytics within the home healthcare software market. Emerging regions in the Middle East, Africa, and South America grow from a smaller base but adopt cloud solutions quickly due to scarce legacy infrastructure.

Competitive Landscape

The top five vendors capture about 45.0% of annual sales, indicating moderate concentration. Homecare Homebase and MatrixCare dominate core agency systems, while WellSky and Netsmart expand via targeted acquisitions such as Bonafide for durable medical equipment management. HHAeXchange strengthened its EVV and billing footprint by acquiring Cashé Software in 2024. Consolidation provides scale advantages in R&D and compliance updates, keeping barriers to entry high for small newcomers.

Technology leadership now hinges on AI. Iodine Software’s AwarePre-Bill audits discharge documentation and can recover USD 3–4 million per month for hospitals by preventing coding gaps. FDA guidance on machine learning in software as a medical device gives vendors clearer pathways to market. Players embed predictive models for staffing optimization, sepsis risk identification, and supply inventory forecasting, deepening their differentiation in the home healthcare software market.

Vertical integration blurs traditional vendor boundaries. UnitedHealth Group’s plan to acquire Amedisys signals payer interest in controlling home-based clinical capacity, which may steer technology procurement toward internally developed or captive solutions. Large electronic health record vendors observe these moves and weigh entry, raising the possibility of future platform convergence. Jonas Software’s 2025 purchase of TurnPoint shows private-equity appetite for niche regional providers that can be rolled into broader portfolios. Overall, rivalry balances between scale efficiencies, speed of AI adoption, and the race to own longitudinal patient data.

Home Healthcare Software Industry Leaders

WellSky Corp.

NetSmart Technologies

MatrixCare (Brightree & ResMed)

Homecare Homebase LLC

PointClickCare Technologies

- *Disclaimer: Major Players sorted in no particular order

Home Healthcare Software Market Companies Covered in this Report

- WellSky Corp.

- Netsmart Technologies

- MatrixCare (Brightree & ResMed)

- Homecare Homebase LLC

- PointClickCare Technologies

- Axxess Technology Solutions

- AlayaCare Inc.

- Delta Health Technologies

- Allscripts

- Meditech

- Oracle Health (Cerner)

- Mckesson

- CARECENTA

- AxisCare LLC

- Thornberry Ltd.

- Kinnser Software

- ClearCare (WellSky Personal Care)

- HealthCare Provider Solutions Inc.

- Epic Systems (Home Health module)

- GE Healthcare Digital

- Teladoc Health

Recent Industry Developments in Home Healthcare Software Market

- May 2025: Iodine Software launched AwarePre-Bill, an AI-driven post-discharge auditing tool projected to save hospitals USD 3-4 million monthly by closing documentation gaps.

- February 2025: Jonas Software acquired TurnPoint Software, extending integrated compliance and care management offerings to community care providers.

- January 2025: The U.S. Department of Health and Human Services set a 2025 goal for an interoperable health IT ecosystem, energizing demand for open APIs and FHIR-native platforms.

- October 2024: WellSky bought Bonafide to add durable medical equipment functionality to its home care suite.

- June 2024: HHAeXchange finalized its purchase of Cashé Software, expanding its EVV and revenue cycle tools for Medicaid providers.

Home Healthcare Software Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the home healthcare software market as all commercially licensed, interoperable applications that schedule visits, document clinical notes, bill payers, and exchange patient data for services delivered in a patient's residence. The model covers agency management, clinical, hospice, and telehealth modules deployed on-premise or in the cloud, across every major geography.

Scope exclusion: Hardware, disposable medical supplies, and labor revenues from home care services are outside the present estimate.

Segments Covered in This Report

- By Software Type

- Agency Management Solutions

- Clinical Management Systems

- Hospice & Palliative Care Software

- Other Software

- By Service

- Rehabilitation

- Infusion Therapy

- Respiratory Therapy

- Pregnancy & Post-partum Care

- Skilled Nursing

- Other Services

- By Mode of Delivery

- Cloud-Based

- On-Premises

- Hybrid

- By End-User

- Home Health Agencies

- Hospice Agencies

- Other End-Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Qualitative discussions with agency executives, clinical directors, state Medicaid program officers, and regional distributors across North America, Europe, and Asia-Pacific helped us stress test adoption barriers, verify user counts, and calibrate cloud migration rates that secondary sources only hinted at.

Desk Research

Our analysts first assembled foundational data from tier-one public sources such as the US Centers for Medicare & Medicaid Services, the Centers for Disease Control and Prevention, Eurostat, and the World Health Organization, which quantify addressable patient pools, reimbursement levels, and chronic disease prevalence. Industry associations, including the Home Care Association of America and HIMSS, offered usage benchmarks and regulatory timelines (for example, Electronic Visit Verification). Financial filings, investor decks, and press releases from leading software vendors were screened in D&B Hoovers and Dow Jones Factiva to capture average selling price ranges, new logo wins, and maintenance renewal rates that anchor revenue conversion factors. The sources listed are illustrative; many additional public and paid references supported data collection, validation, and clarification.

Market-Sizing & Forecasting

A top-down demand pool was reconstructed from home health expenditure and visit volumes, then multiplied by verified software penetration and spend per user ratios; selective bottom-up roll-ups of vendor revenues and channel checks served as a control. Key variables tracked include visit intensity per patient, license to services revenue mix, cloud price erosion, mandated EVV rollouts, and agency formation rates. Multivariate regression with lagged macro health indicators underpins the 2025-2030 forecast, while scenario analysis adjusts for reimbursement shocks or cybersecurity incidents.

Data Validation & Update Cycle

Outputs pass an internal three-layer review that screens out anomalies against external benchmarks and prior editions. Mordor analysts refresh models annually and trigger interim updates when policy changes, funding rounds, or M&A shift market structure; just before publication, each figure is rerun so clients receive the latest view.

How Mordor Intelligence's Home Healthcare Software Market Size Compares to Other Published Estimates

Published estimates often diverge because firms slice the market differently, rely on unvetted assumptions, or freeze exchange rates. By aligning scope strictly with software revenues and rechecking both demand side and supply side signals every year, Mordor Intelligence delivers a balanced baseline users can track back to measurable drivers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.51 B (2025) | Mordor Intelligence | - |

| USD 5.00 B (2024) | Regional Consultancy A | Treats private label custom builds as packaged software, inflating totals |

| USD 5.34 B (2024) | Industry Association B | Applies uniform 14 percent CAGR without validating price compression or churn |

| USD 7.79 B (2024) | Global Consultancy C | Bundles care management BPO fees and remote monitoring devices with software |

The comparison shows that once differing scopes, price mix assumptions, and refresh cadences are stripped away, Mordor's disciplined approach offers the most transparent, reproducible starting point for planning and investment.

Key Questions Answered in the Report

What is the current value of the home healthcare software market?

The home healthcare software market stands at USD 5.08 billion in 2026 and is projected to reach USD 9.27 billion by 2031.

Which software type generates the most revenue?

Agency Management Solutions hold the lead with 34.62% of 2025 revenue, reflecting their role as core operational platforms.

Why are cloud-based deployments expanding so quickly?

Cloud solutions cut total ownership costs by about 77%, deliver continuous updates, and support mobile workflows, driving a 14.22% CAGR in this delivery mode.

How do EVV mandates influence technology adoption?

By making digital visit verification a condition for Medicaid payment, EVV rules compel agencies to implement compliant software, accelerating overall market uptake.

Which service segment is growing fastest?

Infusion Therapy leads growth at 13.72% CAGR as payers shift expensive specialty drug administration from hospitals to home settings.

What competitive factors define vendor success?

Scale for regulatory updates, AI-driven analytics, and the ability to integrate across the care continuum are now decisive differentiators among leading suppliers.

Page last updated on: