Healthcare Software As A Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

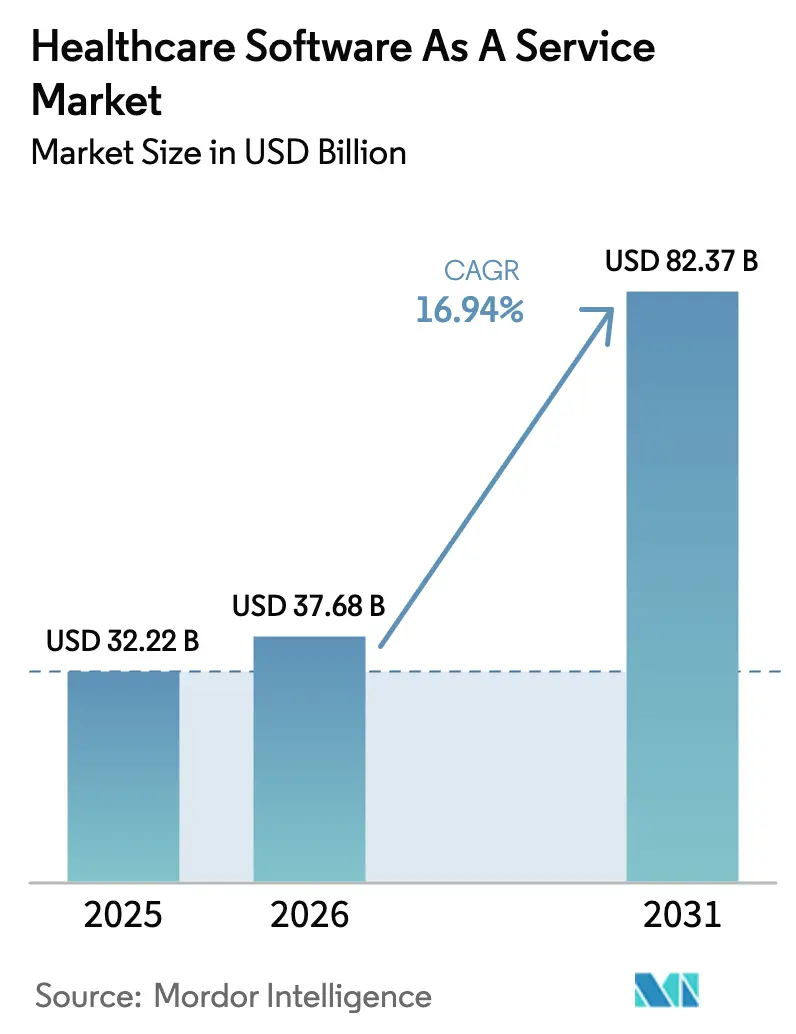

| Market Size (2026) | USD 37.68 Billion |

| Market Size (2031) | USD 82.37 Billion |

| Growth Rate (2026 - 2031) | 16.94% CAGR |

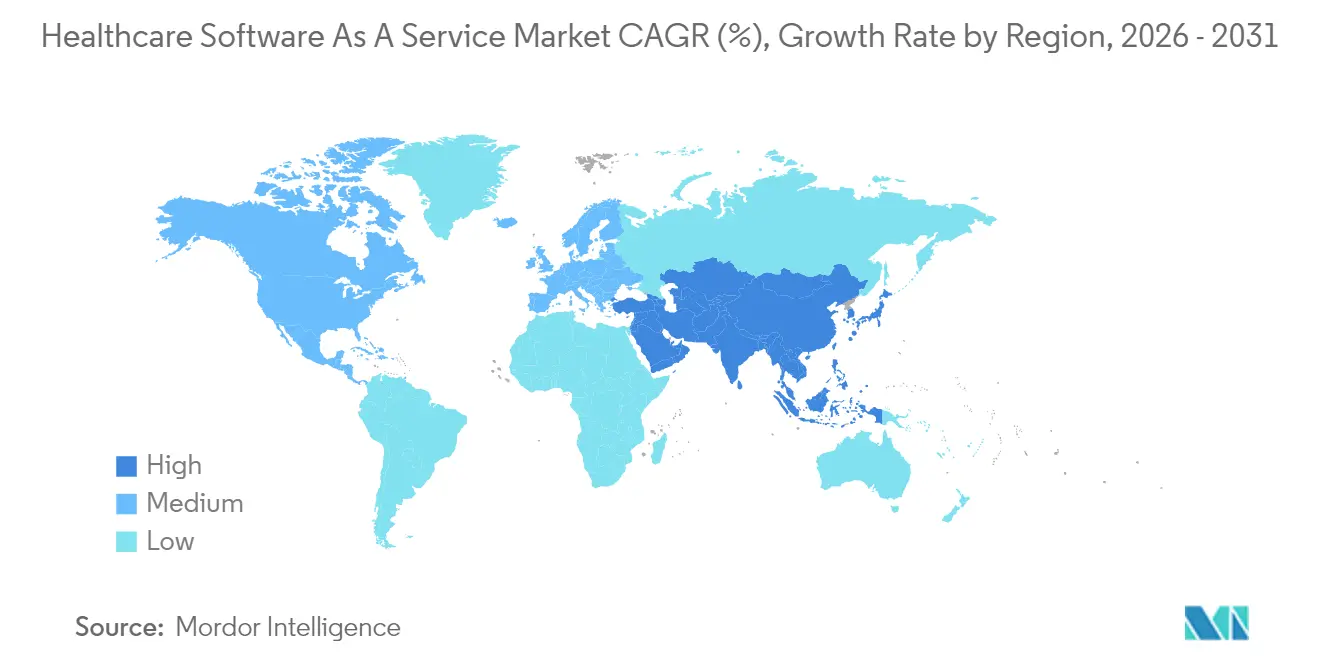

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Software As A Service Market Analysis by Mordor Intelligence

The healthcare software as a service market size was valued at USD 32.22 billion in 2025 and estimated to grow from USD 37.68 billion in 2026 to reach USD 82.37 billion by 2031, at a CAGR of 16.94% during the forecast period (2026-2031). The current healthcare software as a service market is propelled by cloud-native EHR replacement cycles, payer-driven revenue-cycle automation, and strict interoperability mandates that favor scalable subscription models. Health systems cite payment realization periods falling from 90 to 40 days after adopting AI-enabled SaaS revenue-cycle tools, underscoring clear financial benefits. Regulatory momentum created by the 21st Century Cures Act pushes vendors to expose standardized APIs, accelerating real-time data exchange and lowering integration costs. At the same time, 92% of enterprises reported at least one cyberattack in 2024, elevating demand for zero-trust SaaS stacks with built-in resilience. Collectively, these forces reinforce the premium that providers place on vendors able to combine compliance, performance, and robust security in one cloud-delivered platform.

Key Report Takeaways

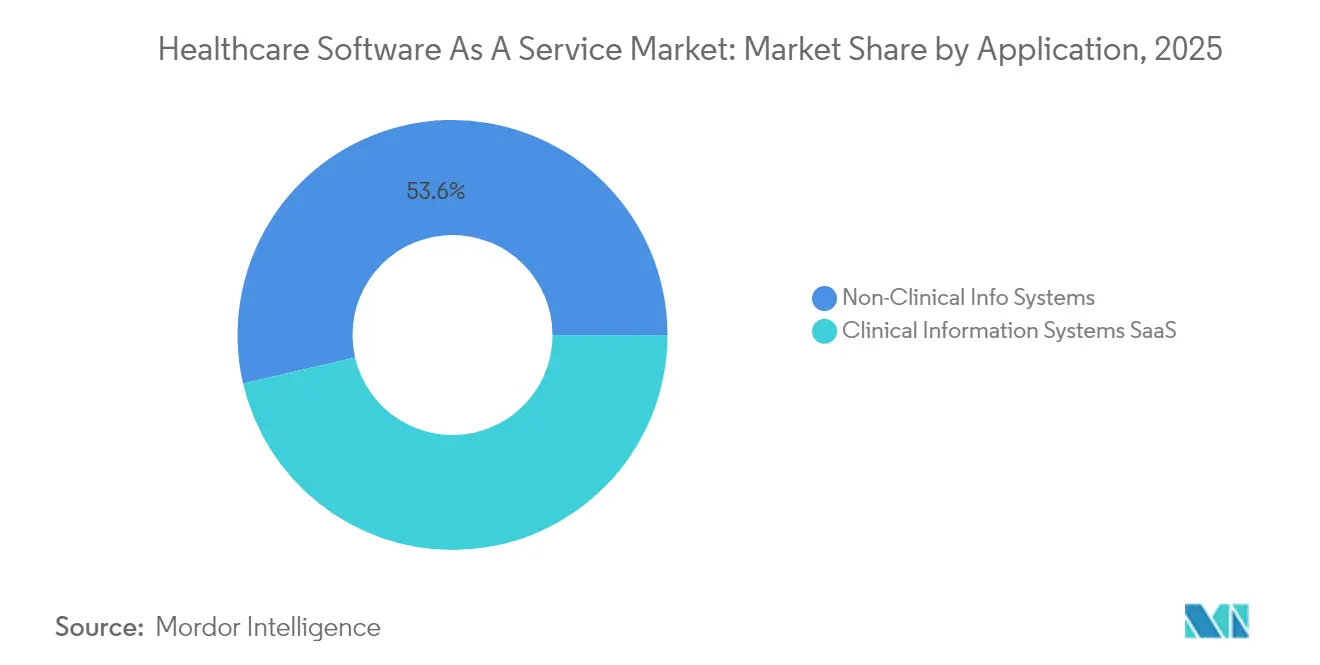

- By application, non-clinical information systems led with 53.62% of healthcare software as a service market share in 2025, while clinical information systems are advancing fastest at an 18.12% CAGR through 2031.

- By deployment model, private cloud accounted for 46.10% of 2025 revenue; hybrid cloud is projected to post the highest 18.35% CAGR to 2031.

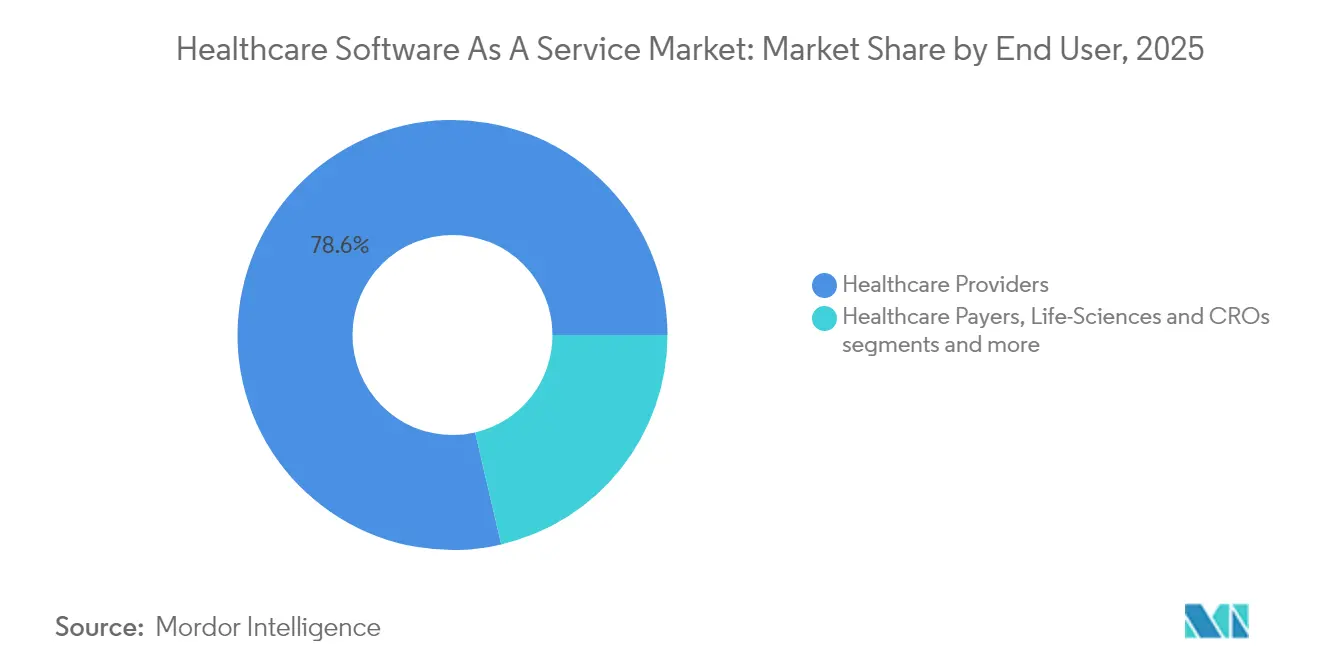

- By end-user, healthcare providers held a dominant 78.64% share in 2025 and also represent the fastest-growing segment with a 18.62% CAGR.

- By geography, North America captured 54.88% of revenue in 2025; Asia-Pacific shows the highest regional growth at 18.97% CAGR to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Healthcare Software As A Service Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-first EHR replacement cycles | +3.2% | Global; North America leads | Medium term (2-4 years) |

| Telehealth platform integration into core EMRs | +2.8% | Global; APAC and rural markets accelerate | Short term (≤ 2 years) |

| Mandatory interoperability & patient-access rules | +4.1% | North America and EU expanding | Long term (≥ 4 years) |

| Cost-saving push by payers for SaaS revenue-cycle tools | +3.5% | North America core | Medium term (2-4 years) |

| AI-native vertical SaaS for niche clinical pathways | +2.4% | Advanced healthcare markets | Long term (≥ 4 years) |

| Growing hospital demand for cyber-resilient zero-trust stacks | +1.8% | North America and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cloud-first EHR replacement cycles

Hospitals are bringing forward modernization roadmaps as legacy on-premises contracts expire. Epic added 176 new facilities in 2024, its single-largest annual gain, largely because CIOs value built-in regulatory compliance and readily available integrations. Oracle Health plans to counter with an AI-enabled EHR that launches in 2025, featuring voice-assisted workflows, yet early pilots indicate that customers still prioritize customer-support depth over feature parity. Useful-life calculations for EHRs now weigh cloud migration costs more heavily than license fees, shifting board-level ROI discussions toward predictable subscription outlays. As replacement activity snowballs, the healthcare software as a service market benefits from accelerated multiyear contracts that lock in double-digit growth trajectories.

Telehealth platform integration into core EMRs

Providers increasingly view virtual-care modules as standard EHR functionality rather than bolt-on services. OpenLoop Health cut implementation timelines to seven weeks by exposing pre-built APIs, a benchmark that redefines time-to-value expectations for new rollouts. Integration sharply improves physician scheduling, clinical documentation, and billing accuracy because encounter data flows automatically into the patient’s longitudinal record. Rural facilities experience the most dramatic gains in specialist coverage, although broadband gaps still limit synchronous video in isolated regions. These workflow efficiencies explain why virtual-care adoption patterns now closely track core EHR refresh cycles, further reinforcing SaaS demand.

Mandatory interoperability & patient-access rules

Enforcement of information-blocking penalties under the 21st Century Cures Act has rendered closed architectures financially untenable for developers. Certified health IT must deliver standardized FHIR APIs, driving providers toward vendors able to update codebases rapidly in the cloud. The upcoming USCDI v3 deadline in January 2026 will widen the gap between cloud-first and legacy suppliers, while the European Health Data Space regulation places similar pressure on EU markets. Vendors that embed TEFCA connectivity and bulk-data export into their core offerings continue to win competitive bids, directly boosting the healthcare software as a service market.

Cost-saving push by payers for SaaS-based revenue-cycle tools

Administrative overhead remains a top expense bucket for health systems, so CFOs increasingly direct capital toward AI-driven claims automation. Industry surveys reveal 74% of U.S. hospitals deploying at least one automated prior-authorization or denial-management module in 2025. Reported time savings reach 70% in health-information-management workflows, delivering six-month payback windows. These outcomes encourage payers to embed automation requirements in reimbursement contracts, effectively making cloud-delivered revenue-cycle software a cost-of-doing-business standard.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating ransomware premiums & data-sovereignty regulation | -2.1% | EU and other regulated markets | Short term (≤ 2 years) |

| Skills gap in cloud DevSecOps within hospital IT | -1.8% | Rural and mid-tier markets | Medium term (2-4 years) |

| Vendor lock-in concerns around hyperscaler ecosystems | -1.4% | North America and EU | Long term (≥ 4 years) |

| Lagging broadband quality in rural care settings | -0.9% | Developing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating ransomware premiums & data-sovereignty regulation

Average ransom demands hit USD 5.7 million in 2024, while insurers tightened underwriting standards, forcing CIOs to divert budget from innovation to coverage. Parallel legislation in Germany and the United States restricts cross-border data flows, adding compliance complexity for multinational providers. These headwinds temper near-term spending but also nudge late adopters toward mature vendors that already comply with localization mandates.

Skills gap in cloud DevSecOps within hospital IT

Two-thirds of healthcare CIOs expect to rely on contractors to fill specialist roles in 2025, prolonging rollout timelines and inflating project costs[1]Source: CereCore, “CIOs on Facing 2024 Challenges,” cerecore.net . Smaller rural facilities face even deeper shortages, widening the digital divide and slowing the healthcare software as a service market’s rural penetration curve.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Administrative dominance, clinical momentum

Non-clinical information systems maintained a 53.62% share of 2025 revenue, confirming that organizations first target financial and supply-chain pain points. Within this bucket, AI-enabled revenue-cycle platforms illustrate why the healthcare software as a service market size allocated to back-office optimization continues to rise. Patient engagement portals also gain traction as payers link reimbursement to experience metrics, compelling hospitals to invest in modern web self-service.

Clinical information systems grow at an 18.12% CAGR, the segment’s fastest, as interoperability deadlines converge with telehealth demand. EHR and imaging modules increasingly ship with embedded algorithms that surface decision-support prompts at the point of care. This convergence shortens diagnosis-to-treatment intervals and justifies premium subscription tiers. Collectively, these trends shift wallet share from administrative to clinical budgets, yet non-clinical platforms will likely retain a plurality through 2031.

By Deployment Model: Hybrid strategies evolve

Private cloud deployments accounted for 46.10% of 2025 spending, reflecting security and data-governance concerns among large health systems. These buyers maintain on-premises hosting but outsource software management, seeing it as an acceptable trade-off between control and convenience. Hybrid cloud, however, registers an 18.35% CAGR, the highest in the matrix. The approach keeps sensitive information within enterprise walls while shifting analytics or burst-capacity workloads to public clouds.

Epic’s reference architectures illustrate how a hybrid footprint can balance performance and security without overhauling network topology. Conversely, pure public-cloud adoption stalls when procurement teams flag potential vendor lock-in. Nonetheless, hyperscalers are responding with price-transparency programs and sovereign-cloud offerings designed to soothe data-residency fears. As these initiatives mature, hybrid models may serve as a transitional stage rather than an end state.

By End-User: Providers consolidate

Providers commanded 78.64% of 2025 revenue, underscoring their central role in purchasing decisions. Integrated delivery networks drive bulk contracts that bundle EHR, ERP, and patient-engagement modules across multiple campuses. Such economies of scope create high switching costs, which in turn increase the healthcare software as a service market share held by a small set of entrenched vendors.

The same provider cohort also posts the fastest 18.62% CAGR because community hospitals and ambulatory centers are migrating to cloud solutions to match the digital experience offered by larger peers. Payers, life-sciences companies, and public-health agencies together account for the remaining 21.36%; they favor analytics and population-health suites but upgrade cycles occur less frequently. The resulting concentration intensifies competition for provider contracts while leaving niche openings in payer analytics and clinical-trial orchestration.

Geography Analysis

North America retained 54.88% market share in 2025 owing to early adoption of cloud EHRs, stable reimbursement structures, and mature cybersecurity regulations. U.S. health systems continue to allocate capital toward AI-enabled clinical decision support and revenue-cycle automation, although rural hospitals still report connectivity speeds below 10% of recommended thresholds. Canada’s provincial digitization roadmaps and Mexico’s private-sector investments add steady incremental demand.

Asia-Pacific delivers the strongest 18.97% CAGR as governments scale national health-record projects and venture funding floods regional start-ups. Indonesia, Vietnam, and the Philippines accounted for a combined USD 6.1 billion digital-health market in 2024, providing fertile ground for mobile-first SaaS rollouts. China and India accelerate EHR mandates tied to universal-health-coverage initiatives, while Japan embeds IoT monitoring into elder-care programs. Australia transitioned 191 public hospitals to Epic, demonstrating that proven U.S. products can succeed when localized for regional privacy rules.

Europe’s outlook hinges on the European Health Data Space regulation that harmonizes interoperability across member states by 2030. Germany’s Cloud-Computing Act imposes stricter hosting criteria, prompting providers to examine sovereign-cloud or hybrid configurations. The United Kingdom, France, and the Nordics lead on cloud usage but remain watchful of vendor lock-in and GDPR liabilities. Latin America and the Middle East & Africa represent long-run opportunities once broadband, regulatory clarity, and clinical-coding standards improve at scale.

Competitive Landscape

Epic Systems widened its hospital footprint by 176 facilities in 2024, boosting its share to 42.3% and cementing its position as anchor tenant for enterprise EHR contracts. Oracle Health’s integration of Cerner slowed new sales and triggered 74 hospital defections, yet the vendor’s forthcoming voice-first EHR aims to regain relevance. MEDITECH, MEDHOST, and CPSI defend community-hospital niches by emphasizing price and implementation speed. Collectively, the top three firms control enough accounts to influence interface standards, thereby shaping the trajectory of the healthcare software as a service market.

Cloud hyperscalers Microsoft Azure and Amazon Web Services avoid direct EHR competition, instead partnering with software vendors to supply GPU-enabled AI services. Their vertical industry teams co-develop solutions, such as GE HealthCare’s imaging-AI models on AWS, to embed infrastructure revenue inside larger clinical workflows. Smaller disruptors pursue specialist pathways: ConcertAI provides oncology-specific analytics, while Evolent Health integrates AI-based prior-authorization engines to reduce payer friction.

Cybersecurity has become a competitive differentiator. Vendors advertise zero-trust reference architectures and independent penetration-test certifications to reassure boards and insurers. M&A trends also reflect functionality gaps, with HEALWELL AI acquiring Orion Health to gain interoperability assets and Net Health buying Limber Health to extend outpatient coverage. Because switching an EHR remains costly, strategic features—rather than price concessions—now drive market-share movement.

Healthcare Software As A Service Industry Leaders

Pager, Inc.

CorroHealth

CareCloud, Inc.

Veradigm LLC

Flatiron Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Epic Systems announced work on a healthcare-specific ERP suite covering workforce, finance, and materials management, signaling expansion beyond core EHR functions

- March 2025: Microsoft and Wolters Kluwer integrated UpToDate into Microsoft Copilot Studio, delivering conversational clinical decision support within existing clinician workflows

- January 2025: Amazon One Medical partnered with Montefiore Health System to open primary-care clinics offering coordinated virtual and in-person services

Global Healthcare Software As A Service Market Report Scope

As per the scope of the report, healthcare software as a service refers to cloud-based software applications designed for the healthcare industry. These medical SaaS solutions help healthcare organizations manage and streamline various aspects of their operations, such as patient management, clinical documentation, revenue cycle management, and more. The healthcare software as a service market is segmented into application, deployment model, end-user, and geography. By application, the market is segmented into patient portal, telemedicine, mobile communication, ePrescribing, EHR systems, medical billing, and by others, the market is segmented into clinical decision support and healthcare analytics. By deployment model, the market is segmented into private cloud, public cloud, and hybrid cloud. By end-users, the market is segmented into healthcare providers and healthcare payers. By geography, the market is segmented into North America, Europe, Asia-Pacific, and the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (in USD) for the above segments.

| Clinical Information Systems SaaS | EHR / EMR |

| Telehealth & Virtual Care | |

| Clinical Decision Support | |

| Imaging & PACS | |

| Non-Clinical Information Systems SaaS | Revenue Cycle Management |

| Practice Management | |

| Supply-Chain / Inventory | |

| Patient Engagement & CRM | |

| HR & Workforce Management |

| Public Cloud |

| Private Cloud |

| Hybrid & Virtual Private Cloud |

| Healthcare Providers | Hospitals & Health Systems |

| Ambulatory Care Centres | |

| Home-health Agencies | |

| Specialty Clinics |

| Healthcare Payers |

| Life-Sciences & CROs |

| Other Stakeholders (Public Health Agencies etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Application | Clinical Information Systems SaaS | EHR / EMR |

| Telehealth & Virtual Care | ||

| Clinical Decision Support | ||

| Imaging & PACS | ||

| Non-Clinical Information Systems SaaS | Revenue Cycle Management | |

| Practice Management | ||

| Supply-Chain / Inventory | ||

| Patient Engagement & CRM | ||

| HR & Workforce Management | ||

| By Deployment Model | Public Cloud | |

| Private Cloud | ||

| Hybrid & Virtual Private Cloud | ||

| By End-User | Healthcare Providers | Hospitals & Health Systems |

| Ambulatory Care Centres | ||

| Home-health Agencies | ||

| Specialty Clinics | ||

| Healthcare PayersLife-Sciences & CROs | Healthcare Payers | |

| Life-Sciences & CROs | ||

| Other Stakeholders (Public Health Agencies etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the healthcare software as a service market?

The healthcare software as a service market stands at USD 37.68 billion in 2026 and is forecast to reach USD 82.37 billion by 2031, growing at a 16.94% CAGR during the forecast period (2026-2031).

Which application segment grows fastest through 2031?

Clinical information systems lead with an 18.12% CAGR, driven by EHR modernization and telehealth integration.

Why is hybrid cloud adoption accelerating among hospitals?

Hybrid deployments balance on-premises data control with the scalability of public-cloud analytics, producing the highest 18.35% CAGR among deployment models.

How large is North America’s share of the healthcare software as a service market?

North America captured 54.88% of 2025 revenue, anchored by strict interoperability mandates and robust cloud infrastructure.

What cybersecurity trend most influences purchasing decisions?

Rising ransomware threats push providers toward SaaS vendors that embed zero-trust architectures and continuous monitoring.

Page last updated on: