Patient Engagement Solution Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

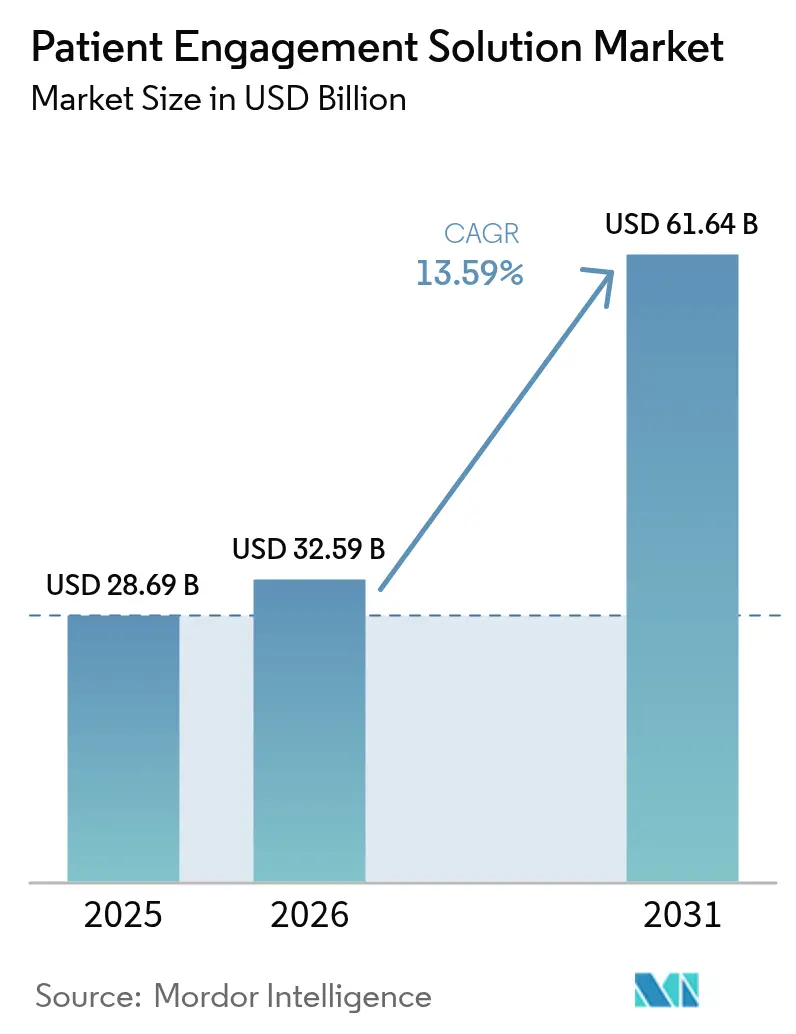

| Market Size (2026) | USD 32.59 Billion |

| Market Size (2031) | USD 61.64 Billion |

| Growth Rate (2026 - 2031) | 13.59% CAGR |

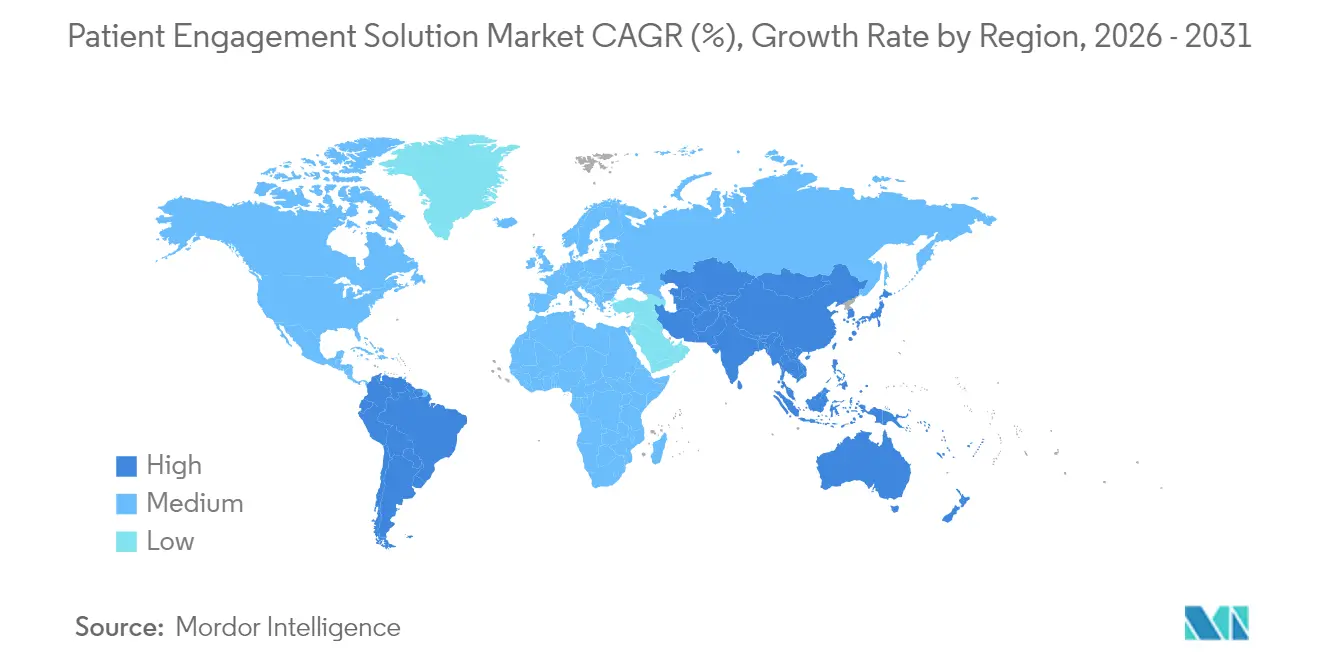

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Patient Engagement Solution Market Analysis by Mordor Intelligence

The Patient Engagement Solution Market size is expected to grow from USD 28.69 billion in 2025 to USD 32.59 billion in 2026 and is forecast to reach USD 61.64 billion by 2031 at 13.59% CAGR over 2026-2031.

Growth is propelled by the healthcare sector’s pivot toward value-based care, the rapid maturation of AI-enabled engagement platforms, and mounting evidence that connected patients are more adherent to treatment plans. North America continues to set the pace, but Asia-Pacific’s digital-health momentum, broad smartphone access, and favorable policy shifts position the region for outsized gains. Cloud deployment, omni-channel engagement, and tighter EHR interoperability are solidifying competitive advantages for vendors that can offer turnkey, enterprise-grade solutions. Despite strong demand signals, data-security compliance and persistent talent shortages present headwinds that could temper adoption in the near term.

Key Report Takeaways

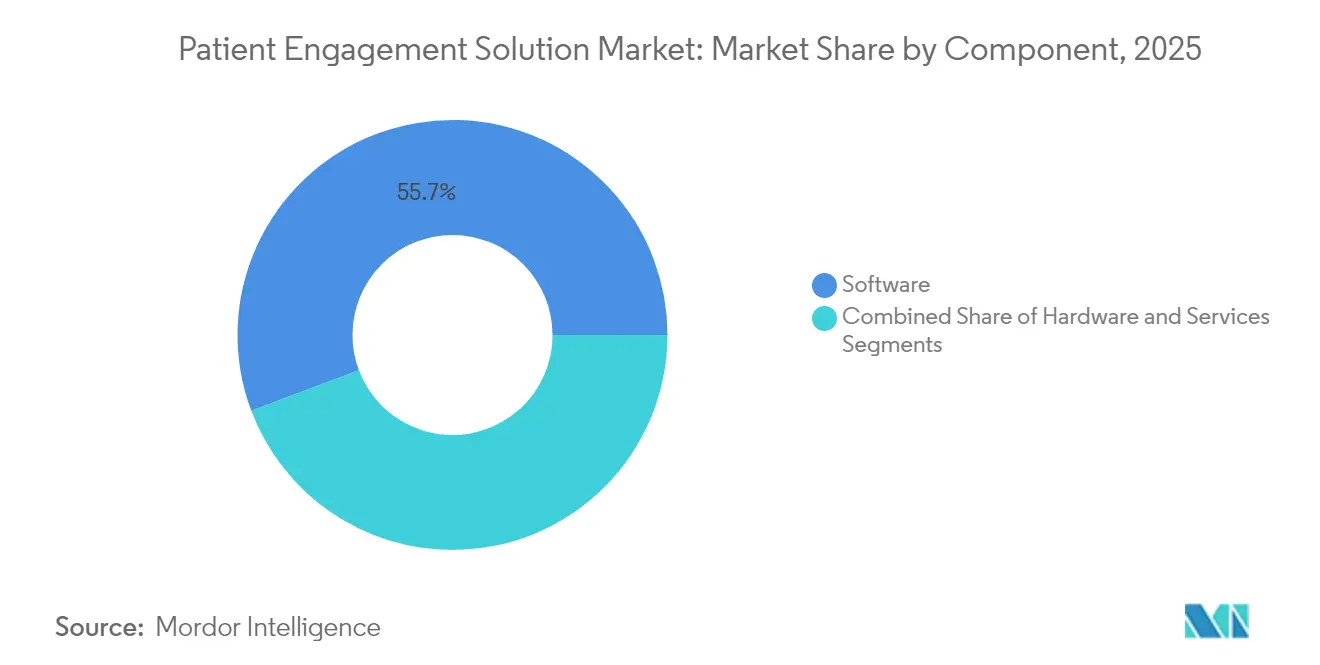

- By component, software accounted for 55.74% of the patient engagement solution market share in 2025, while services are projected to grow at 15.88% CAGR to 2031.

- By delivery mode, cloud-based platforms captured 18.45% of the patient engagement solution market's growth rate between 2026 and 2031, the fastest among delivery models. In 2025, the web- and cloud-based segment held 69.62% of the market share.

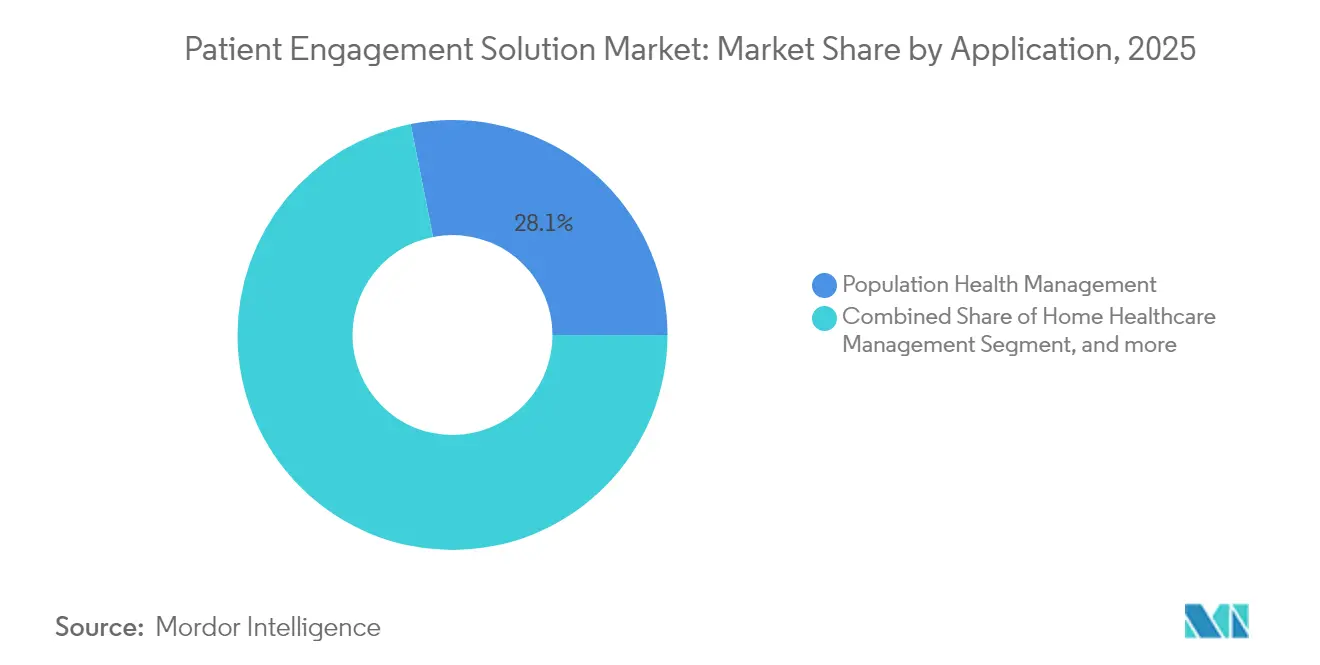

- By application, population health management led with 28.12% revenue share in 2025; home healthcare management is advancing at a 17.41% CAGR through 2031.

- By end user, providers held 53.28% of the patient engagement solution market size in 2025, whereas payers are forecast to record a 14.36% CAGR through 2031.

- By geography, North America retained 41.62% of 2025 revenue; Asia-Pacific is set to grow at 17.52% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Patient Engagement Solution Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of AI-Driven Engagement Platforms in Hospitals | + 4.2% | Global, with early adoption in North America & Europe | Medium term (2-4 years) |

| Rising Trend of Mobile Health Applications | +3.5% | Global, with higher impact in Asia-Pacific & North America | Short term (≤ 2 years) |

| Growing Popularity of Patient Engagement Solutions Among the Aging Population | +2.8% | North America, Europe, Japan | Medium term (2-4 years) |

| Rising Investments and Technological Advancements | +3.1% | Global, with concentration in North America & Asia-Pacific | Medium term (2-4 years) |

| Shift from Fee-for-Service to Risk-Sharing Contracts Fuelling Payer Demand | +2.5% | North America & Europe, with expansion to Asia-Pacific | Medium term (2-4 years) |

| Integration of Remote Patient Monitoring with Value-Based Care Reimbursement | +2.2% | North America, with early adoption in Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of AI-Driven Engagement Platforms in Hospitals

Hospitals are embedding conversational AI, predictive analytics, and automated triage into front-office and clinical workflows. Eighty-two percent of health systems surveyed plan to implement AI-enabled engagement tools within two years.[1]Journal of Medical Internet Research, “Hospital AI Adoption Survey,” jmir.org Early adopters report shorter wait times, smoother care transitions, and higher clinician satisfaction, largely because virtual assistants pre-populate charts and handle routine queries. Philips found that 85% of executives now allocate specific budgets for generative-AI engagement projects.[2]Philips, “Future Health Index 2024,” philips.comAs algorithms mature, hospitals see improved appointment adherence and a decline in no-shows, producing measurable revenue uplift while strengthening patient loyalty.

Rising Trend of Mobile Health Applications

Smartphone-centric care pathways give patients real-time access to their medical data, chatbots, and behavioral nudges, which has helped lift portal log-in rates across large health systems. Asia-Pacific leads mobile-health downloads, yet North American providers record the highest per-user session length. Health organizations are layering video visits, secure messaging, and remote vitals capture into single apps, building an omni-channel presence that mirrors consumer-tech experiences. The approach reduces inbound call-center volume and accelerates follow-up scheduling, delivering cost savings and better care continuity.

Growing Popularity Among the Aging Population

Engagement platforms tailored for older adults feature large icons, voice navigation, and medication reminders compatible with smart speakers. Remote patient monitoring kits ship with simplified setup guides, enabling seniors to transmit vitals without technical assistance. Providers that implemented such programs saw 49% declines in readmissions and 68% drops in emergency-department visits. These outcomes validate the financial case for sustained investment in senior-friendly engagement technology.

Rising Investments and Technological Advancements

Venture capital poured USD 10.1 billion into digital health firms in 2024, channeling funds into blockchain-secured data exchange, IoT-enabled monitoring devices, and AI-powered clinical decision support. Health-system boards now classify digital engagement as a strategic imperative; 67% achieved positive ROI within 18 months of deployment. Continuous funding accelerates feature rollouts and shortens payback periods, intensifying competitive pressure on slower-moving incumbents.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Protection of Patient Information | -2.1% | Global, with higher impact in Europe & North America | Short term (≤ 2 years) |

| Lack of Skilled IT Professionals in the Healthcare Industry | -1.8% | Global, with acute impact in developing regions | Medium term (2-4 years) |

| Persistent Interoperability Gaps Between EHR & Third-Party Engagement Apps | -1.5% | Global, with higher impact in fragmented healthcare systems | Medium term (2-4 years) |

| Sub-Optimal Reimbursement Codes for Home-Health Engagement | -1.3% | North America & Europe, with spillover to other regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Protection of Patient Information

Data security concerns represent a significant restraint on market growth, as healthcare organizations must balance enhanced patient engagement with stringent data protection requirements. With over 5,000 reported healthcare data breaches from 2009 to 2022, the industry faces mounting pressure to implement robust security frameworks while maintaining user-friendly engagement solutions. The implementation of regulations like HIPAA in the US and GDPR in Europe creates compliance challenges that can slow adoption, particularly for smaller healthcare providers with limited IT resources. Healthcare organizations are increasingly turning to frameworks like the HITRUST Common Security Framework (CSF) to address these challenges, but implementation requires significant investment in both technology and expertise. The need for secure authentication mechanisms that don't compromise user experience presents a particular challenge, as cumbersome security measures can reduce patient engagement rates and limit the effectiveness of otherwise valuable solutions.

Lack of Skilled IT Professionals in the Healthcare Industry

The shortage of healthcare IT professionals with specialized knowledge in patient engagement technologies is constraining market growth, particularly as solutions become more sophisticated and integrated with clinical workflows. Healthcare organizations face significant challenges in recruiting and retaining IT talent capable of implementing and maintaining complex engagement platforms, especially when competing with technology companies offering higher compensation. This talent gap is particularly acute for specialized skills in AI implementation, data analytics, and cybersecurity, which are increasingly critical for effective patient engagement solutions. The shortage is exacerbated by the rapid pace of technological change, which requires continuous upskilling of existing staff to maintain effectiveness. Healthcare providers are exploring various strategies to address this challenge, including partnerships with technology vendors, outsourced IT services, and investments in training programs, but the fundamental supply-demand imbalance continues to limit the speed and scale of patient engagement solution adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominates Digital Transformation

Software commands the largest share of the Patient Engagement Solution Market at 55.74% in 2025, serving as the cornerstone of digital transformation initiatives across healthcare organizations. This dominance stems from software's ability to integrate seamlessly with existing healthcare IT infrastructure while providing the functionality necessary for meaningful patient interactions. Patient portals, mobile applications, and telehealth platforms represent the most widely adopted software solutions, with features ranging from appointment scheduling to secure messaging and access to medical records. The services segment, while currently smaller, is experiencing the fastest growth at a CAGR of 15.88% for 2026-2031, as healthcare organizations increasingly recognize the importance of implementation support, training, and ongoing maintenance to maximize their technology investments. Hardware components, including kiosks, tablets, and wearable devices, play a supporting but essential role in the overall ecosystem, particularly in clinical settings where direct patient interaction is required.

The software landscape is evolving rapidly with AI integration emerging as a defining trend, as 85% of healthcare leaders invest in generative AI to enhance clinician productivity and patient engagement. Interoperability has become a critical focus area, with healthcare organizations prioritizing solutions that can exchange data seamlessly across disparate systems to create a unified patient experience. The shift toward cloud-based software delivery models is accelerating, driven by advantages in scalability, accessibility, and reduced IT overhead. Services providers are expanding their offerings beyond basic implementation to include strategic consulting, workflow optimization, and continuous improvement programs that help healthcare organizations maximize the value of their patient engagement investments. The component ecosystem continues to evolve in response to changing healthcare delivery models, with an increasing emphasis on solutions that support care delivery outside traditional clinical settings.

By Delivery Mode: Cloud Adoption Accelerates

Web and cloud-based solutions collectively dominate the market with a 69.62% share in 2025, reflecting healthcare's decisive shift away from legacy on-premise systems. Cloud-based solutions specifically are experiencing explosive growth at a CAGR of 18.45% for 2026-2031, as healthcare organizations recognize the advantages in scalability, accessibility, and reduced IT burden. The economic case for cloud adoption is compelling, with cloud deployments being 77% cheaper than on-premises systems and offering significant reductions in maintenance costs. On-premise solutions retain relevance primarily in settings with specific security requirements or connectivity limitations, but their market share continues to decline as cloud security capabilities mature and connectivity infrastructure improves.

The transition to cloud-based delivery models is enabling new capabilities that were previously impractical, including real-time data analytics, seamless multi-device experiences, and rapid feature updates that keep pace with evolving healthcare needs. Healthcare organizations are increasingly adopting hybrid approaches that combine cloud and on-premise elements to balance security, compliance, and accessibility requirements. The cost structure of cloud solutions, typically following a 'per user per month' model, is proving particularly attractive for smaller healthcare organizations that lack the capital for large upfront investments. Security concerns that previously limited cloud adoption are being addressed through advanced encryption, multi-factor authentication, and compliance certifications, with many cloud providers now exceeding the security capabilities of traditional on-premise deployments. The flexibility of cloud-based solutions is proving especially valuable during healthcare disruptions, enabling rapid deployment of new engagement capabilities in response to changing patient needs and care delivery models.

By Application: Home Healthcare Management Gains Momentum

Population Health Management leads application segments with a 28.12% market share in 2025, as healthcare systems leverage patient engagement to address chronic disease management and preventive care initiatives. The application's dominance reflects its alignment with value-based care models that prioritize outcomes over volume, with engagement solutions providing the tools necessary to maintain ongoing patient relationships outside traditional care settings. Home Healthcare Management is emerging as the fastest-growing application segment with a projected CAGR of 17.41% for 2026-2031, driven by the convergence of remote monitoring technologies, telehealth capabilities, and patient engagement platforms. Social and Behavioral Management applications are gaining traction as healthcare organizations recognize the impact of behavioral factors on health outcomes, while Fitness and Health Management solutions are expanding beyond wellness programs to become integral components of preventive care strategies. Financial Management applications are addressing growing patient demand for transparency and control over healthcare costs, particularly as out-of-pocket expenses continue to rise.

The integration of AI and predictive analytics is transforming application capabilities across segments, enabling more personalized and proactive engagement strategies that anticipate patient needs rather than simply responding to them. Remote patient monitoring is becoming increasingly sophisticated, with 99% of U.S. health system leaders viewing digital transformation as essential for improving patient care through innovations like predictive analytics and telehealth. Population Health Management applications are evolving to incorporate social determinants of health data, enabling more holistic approaches to patient engagement that address non-clinical factors affecting health outcomes. Financial Management applications are expanding to include price transparency tools, payment plans, and financial counseling services that help patients navigate the increasingly complex healthcare financial landscape. The boundaries between application categories are blurring as vendors develop more comprehensive platforms that address multiple aspects of the patient journey, from clinical care to financial management and behavioral support.

By End User: Providers Lead, Payers Gain Ground

Healthcare providers dominate the end-user landscape with a 53.28% market share in 2025, reflecting their direct relationship with patients and primary responsibility for care delivery. Hospitals, clinics, and Accountable Care Organizations (ACOs) are implementing patient engagement solutions to improve care coordination, enhance patient satisfaction, and support value-based care initiatives. Payers represent the fastest-growing end-user segment with a CAGR of 14.36% for 2026-2031, as insurance companies recognize the strategic value of patient engagement in reducing claims costs and improving health outcomes. The payer's focus on transitions of care is particularly noteworthy, with a study published in the American Journal of Managed Care demonstrating that payer-led engagement programs can reduce hospital readmissions by up to 52% and emergency department visits by 45% through improved follow-up care and patient education.Patients and caregivers are becoming increasingly active participants in the engagement ecosystem, driving demand for consumer-facing solutions that provide greater control over health information and care decisions.

Pharmaceutical companies are expanding their engagement initiatives beyond traditional adherence programs to include comprehensive support services that address the entire patient journey. The integration of engagement solutions with value-based care models is accelerating adoption across end-user segments, with 83% of ambulatory center stakeholders acknowledging the importance of patient engagement strategies for financial success. Pharmacies and retail health chains are leveraging engagement solutions to extend their role in the care continuum, particularly for chronic disease management and preventive care services. Provider organizations are increasingly focused on reducing the burden on clinical staff, with 95% of executives stressing the need for engagement solutions that integrate seamlessly with existing workflows. The boundaries between traditional end-user categories are blurring as healthcare ecosystems become more integrated, creating new opportunities for collaborative engagement strategies that span the entire care continuum.

Geography Analysis

North America maintains its dominant position in the Patient Engagement Solution Market with a 41.62% share in 2025, driven by advanced healthcare infrastructure, favorable reimbursement policies, and early adoption of digital health technologies. The region's leadership is reinforced by strong regulatory support for patient engagement initiatives, including Meaningful Use requirements and value-based care programs that incentivize provider investments in engagement technologies. A comprehensive survey by the Healthcare Information and Management Systems Society (HIMSS) indicates that 61% of U.S. healthcare organizations have prioritized patient experience and engagement initiatives in their strategic plans, with 72% planning to increase investments in digital patient engagement technologies by 2026. The integration of AI-powered engagement solutions is particularly advanced in this region, with applications ranging from automated appointment scheduling to personalized health recommendations and virtual health assistants. Canada and Mexico are following similar adoption trajectories, though at a somewhat slower pace due to differences in healthcare system structures and funding mechanisms.

Asia-Pacific represents the fastest-growing regional market with a projected CAGR of 17.52% for 2026-2031, fueled by rapidly expanding healthcare infrastructure, increasing smartphone penetration, and growing middle-class populations with higher healthcare expectations. China leads regional growth with substantial investments in digital health infrastructure and patient-centered care initiatives, while India is experiencing accelerated adoption driven by government digital health programs and a burgeoning telehealth sector. Japan's aging population is creating unique engagement challenges and opportunities, with solutions increasingly focused on remote monitoring and chronic disease management for elderly patients. Australia and South Korea are at the forefront of integrating advanced technologies like AI and IoT into patient engagement platforms, creating more personalized and proactive care experiences. The region's growth is further supported by increasing healthcare expenditure and a strong focus on improving healthcare accessibility in both urban and rural areas.

Europe holds a significant market share, with countries like Germany, the United Kingdom, and France leading adoption of patient engagement solutions. The region's strict data protection regulations, particularly GDPR, have shaped the development of engagement platforms with enhanced privacy features and transparent data governance practices. The Middle East and Africa region, while currently representing a smaller market share, is experiencing growing adoption particularly in Gulf Cooperation Council (GCC) countries where healthcare modernization initiatives are driving investments in patient engagement technologies. South America shows promising growth potential, with Brazil leading regional adoption as healthcare providers seek to address access challenges through digital engagement solutions. The global nature of the patient engagement market is increasingly evident, with solutions being adapted to address region-specific healthcare challenges while maintaining core functionality that transcends geographic boundaries.

Competitive Landscape

The Patient Engagement Solution Market exhibits moderate fragmentation with a diverse mix of established EHR vendors, specialized engagement solution providers, and emerging technology disruptors competing for market share. The competitive dynamics are evolving rapidly as traditional EHR vendors expand their engagement capabilities through both internal development and strategic acquisitions, while specialized providers differentiate through deeper functionality in specific engagement domains. Market concentration is increasing through merger and acquisition activity, with healthcare IT companies expanding their offerings to meet diverse customer needs.

Strategic partnerships have emerged as a key competitive approach, with technology vendors collaborating with healthcare providers to develop solutions that address specific clinical and operational challenges. The integration of AI and machine learning capabilities represents a critical competitive battleground, with vendors racing to incorporate these technologies into their engagement platforms. White-space opportunities exist particularly in addressing the needs of underserved healthcare segments, including rural providers, behavioral health organizations, and post-acute care facilities. The competitive landscape is further shaped by the growing influence of non-traditional players, including retail giants and technology companies that are leveraging their consumer engagement expertise to enter the healthcare market. Epic's continued market share gains, adding 176 multispecialty hospitals in 2024 alone, highlight the importance of vendor stability and interoperability capabilities in healthcare organizations' purchasing decisions.

Patient Engagement Solution Industry Leaders

Allscripts Healthcare Solutions Inc

Athenahealth Inc

Cerner Corporation

Mckesson Corporation

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Artera (formerly Well Health) was recognized as the "Best Overall Patient Engagement Company" in the MedTech Breakthrough Awards, highlighting its growing influence in the patient engagement solution market

- April 2025: eClinicalWorks launched healow Genie, an AI-powered patient engagement solution designed to transform how patients interact with healthcare providers through personalized communication and improved care coordination

- March 2025: Health Catalyst, Inc. has unveiled its acquisition of Upfront Healthcare Services, Inc. for USD 86 million, bolstered by a potential earnout of USD 33.4 million. This strategic maneuver, aimed at bolstering patient engagement, is set to finalize in 2025.

- October 2024: RadiantGraph, a patient engagement platform, has secured USD 11M in Series A funding. This announcement comes shortly after the company revealed its integration capabilities with AWS, Google Cloud, Databricks, and Snowflake.

- September 2024: AiCure, a prominent in AI and advanced data analytics for monitoring patient behavior and enabling remote engagement in clinical trials, has introduced its groundbreaking H.Code platform as a key development. The launch took place at the 14th Annual DPHARM, where AiCure also served as a proud sponsor. The H.Code platform is designed to streamline trial participation through a unified approach, representing a significant advancement in clinical trial management.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the patient engagement solutions market as all software, connected hardware, and associated services that enable two-way digital interaction between healthcare providers, payers, and patients across the care continuum, from appointment scheduling and teleconsultation to education, adherence reminders, and remote monitoring. The valuation includes revenues earned from perpetual and subscription licenses, maintenance, implementation, and managed services delivered through web-based, cloud, or on-premise deployments worldwide.

Standalone EHR platforms that lack a patient-facing interface are not included.

Segmentation Overview

- By Component

- Hardware

- Software

- Services

- By Delivery Mode

- Web-Based and Cloud-Based

- On-Premise

- By Application

- Social and Behavioral Management

- Fitness and Health Management

- Home Healthcare Management

- Financial Management

- Population Health Management

- By End User

- Providers (Hospitals, Clinics, ACOs)

- Payers (Public and Private Insurers)

- Patients & Caregivers

- Pharmaceutical Companies

- Pharmacies and Retail Health Chains

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We supplemented desk findings with telephone and on-site interviews involving hospital CIOs, payer IT leads, digital therapeutics managers, and health-tech investors across North America, Europe, Asia-Pacific, and the Middle East. Their inputs clarified average selling prices, deployment lead times, and regional reimbursement triggers, allowing assumptions to be stress-tested before model lock-in.

Desk Research

Mordor analysts began with wide-ranging desk work, screening tier-1 public sources such as the US Centers for Medicare & Medicaid Services, the Office of the National Coordinator for Health IT, OECD Health Statistics, the European Commission eHealth Observatory, and World Health Organization Digital Health Atlas. Industry association white papers, SEC 10-Ks, and investor decks supplied baseline cost curves and platform adoption metrics. Select paid databases, D&B Hoovers for company financials and Dow Jones Factiva for deal flow, helped size vendor revenue pools. The sources listed illustrate the breadth of materials reviewed; many additional references informed data gathering and validation.

Market-Sizing & Forecasting

A blended top-down and bottom-up model underpins the estimates. Country-level healthcare IT spend, chronic disease prevalence, and internet penetration were mapped to potential user pools, which are then adjusted by solution adoption rates gathered from primary research. Supplier roll-ups of 35 listed and private vendors plus sampled ASP x install-base checks acted as a reasonableness filter. Key variables like HIPAA-aligned cloud migration rates, value-based-care incentive outlays, smartphone penetration among seniors, and remote monitoring episode volumes drive scenario levers. Five-year forecasts employ multivariate regression supported by ARIMA trend smoothing to capture cyclical budget shifts, after which analyst judgment aligns the output with policy pipelines. Gap pockets in vendor disclosures were bridged with median margins observed in audited peers.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated variance flags, peer analyst cross-checks, and senior review before sign-off. We refresh every twelve months and re-open models sooner if material events, major regulations, megamergers, or pandemics shift the market. A final pre-publication sweep ensures clients receive the freshest view.

Why Mordor's Patient Engagement Solution Baseline Commands Reliability

Published figures often diverge because each firm selects different components, deployment tiers, and refresh cadences. By tethering scope to patient-facing modules only, indexing all currencies to the same mid-year rate, and validating with active buyer interviews, Mordor Intelligence delivers a balanced midpoint that decision-makers can audit with ease.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 28.69 Bn (2025) | Mordor Intelligence | - |

| USD 27.63 Bn (2024) | Global Consultancy A | Excludes connected hardware and applies uniform 20% ASP uplift without region weighting |

| USD 25.77 Bn (2024) | Industry Publisher B | Uses limited hospital sample and reports gross vendor billings, not net healthcare spend |

| USD 22.50 Bn (2023) | Trade Journal C | Older base year and omits managed services revenues |

Taken together, the comparison shows that scope breadth, base year choice, and revenue recognition rules explain most variance; by harmonizing all three and layering continuous expert feedback, Mordor's baseline remains the most dependable starting point for strategic planning.

Key Questions Answered in the Report

What is the current value of the patient engagement solution market?

The market stands at USD 32.59 billion in 2026 and is forecast to reach USD 61.64 billion by 2031, reflecting a 13.59% CAGR.

Which region grows fastest in patient-engagement solutions?

Asia-Pacific is projected to register a 17.52% CAGR through 2031, driven by smartphone ubiquity and large-scale government digital-health programs.

Why are cloud-based platforms gaining popularity?

Cloud solutions cut deployment costs by 77%, scale on demand, and support continuous feature updates, which boosts provider agility and reduces maintenance burdens.

How do AI technologies improve patient engagement?

AI powers virtual assistants, predictive outreach, and automated documentation, which trim administrative workload and personalize care pathways, lifting appointment adherence and patient satisfaction.

What is the chief barrier to wider adoption?

Compliance with stringent data-privacy rules such as HIPAA and GDPR remains the top challenge, especially for smaller providers lacking extensive cybersecurity resources.

Page last updated on: