Global Personal Health Records Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.56 Billion |

| Market Size (2031) | USD 16.47 Billion |

| Growth Rate (2026 - 2031) | 9.32% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

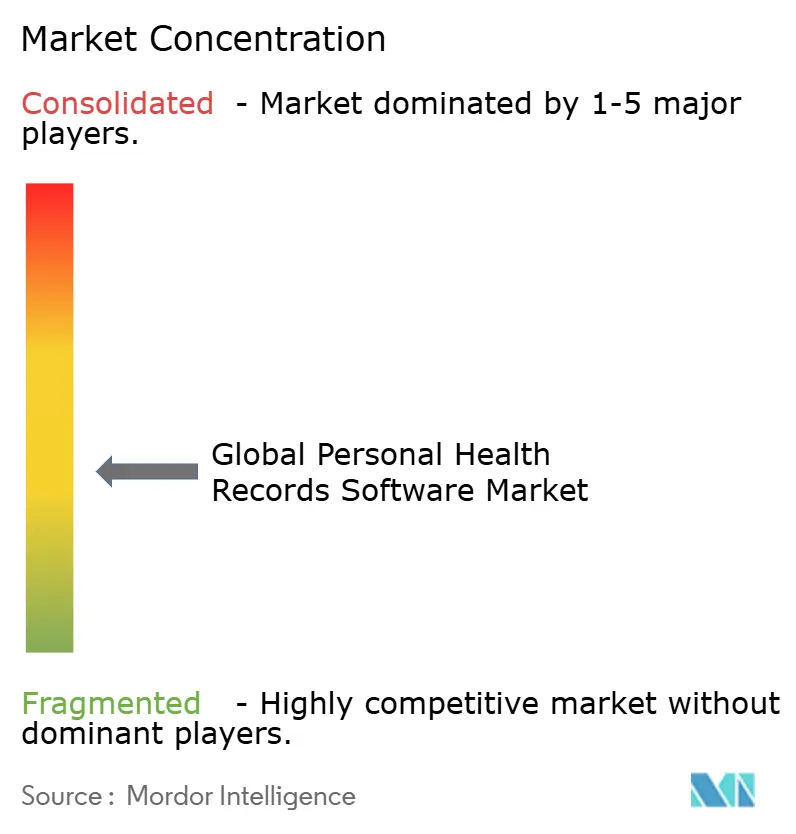

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Personal Health Records Software Market Analysis by Mordor Intelligence

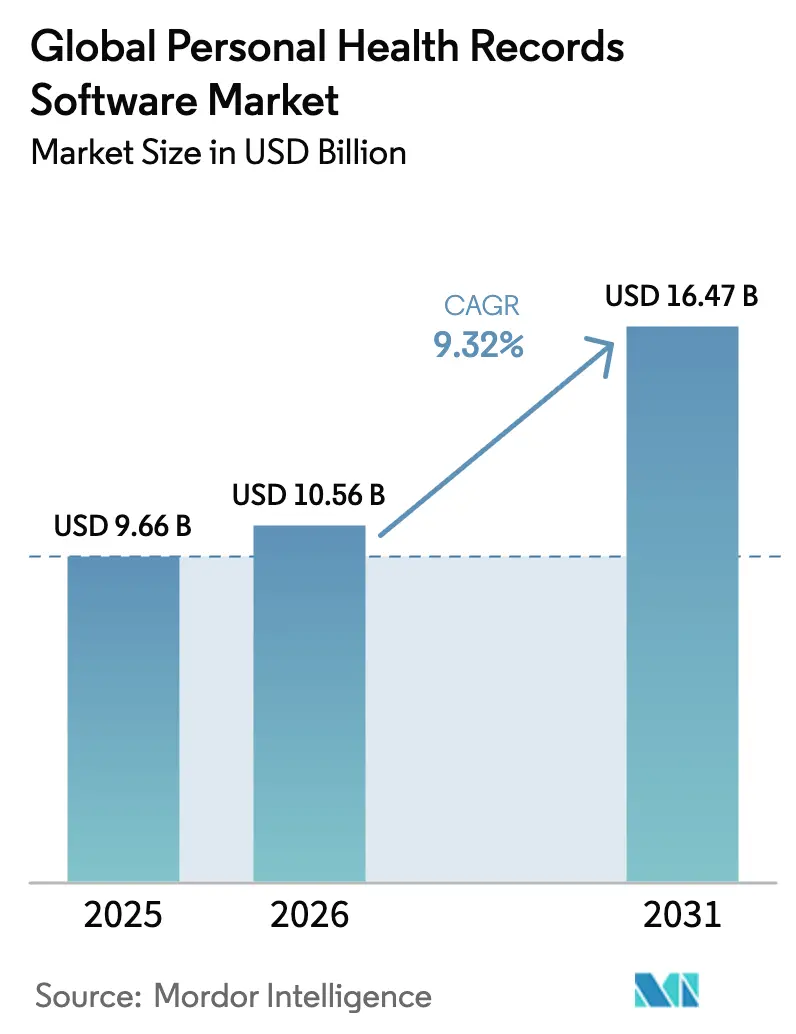

The Personal Health Records Software market size is expected to grow from USD 9.66 billion in 2025 to USD 10.56 billion in 2026 and is forecast to reach USD 16.47 billion by 2031 at 9.32% CAGR over 2026-2031.

This robust personal health records software market expansion mirrors the move to patient-centered care, the proliferation of cloud deployment, and the growing need for real-time data exchange between consumers, providers, and payers. Interoperability mandates such as the CMS Patient Access API rule, the fast uptake of wearable devices, and the convergence of telehealth and remote patient monitoring are reinforcing adoption momentum. Mounting cybersecurity spending, artificial-intelligence-driven analytics, and service-centric business models are redefining competitive positioning. Vendors that blend strong privacy safeguards with friction-free cross-platform user experiences are expected to capture a disproportionate share of future growth in the personal health records software market.

Key Report Takeaways

- By component type, Software & Mobile Apps led with 54.10% of personal health records software market share in 2025, while Services is projected to record a 11.12% CAGR to 2031.

- By deployment mode, cloud-based systems captured 50.35% of the personal health records software market size in 2025 and are advancing at a 13.05% CAGR through 2031.

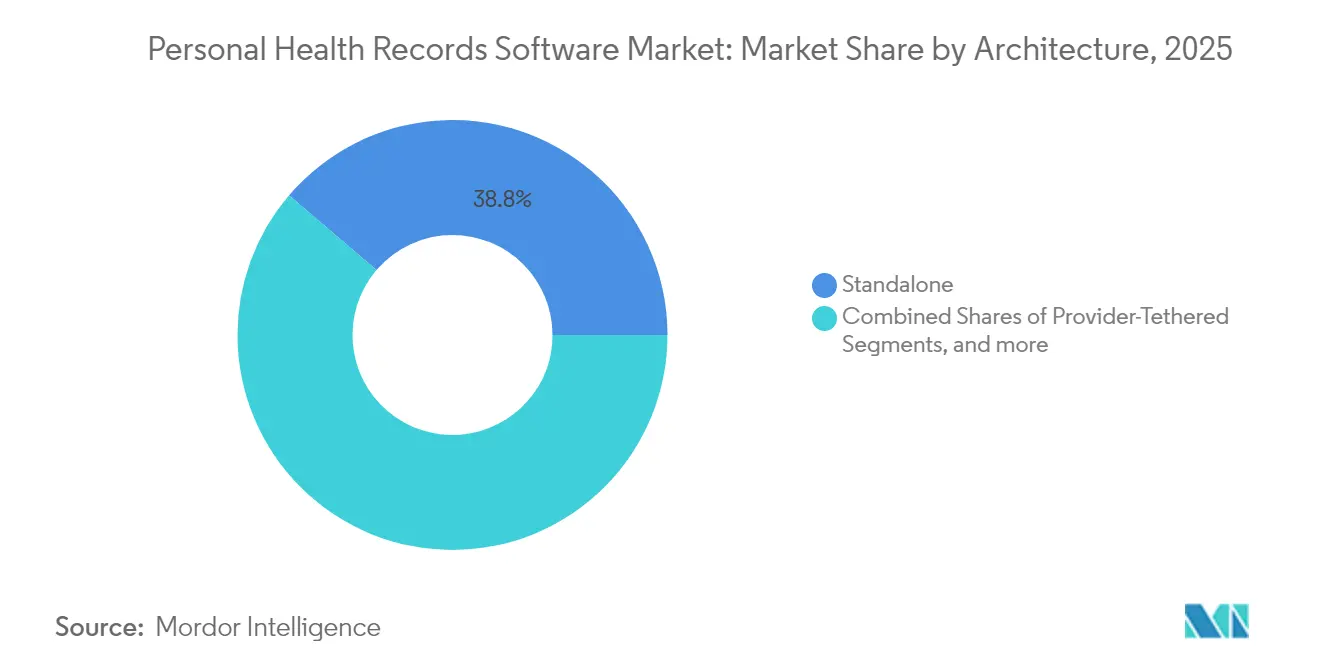

- By architecture, standalone solutions accounted for 38.75% of personal health records software market size in 2025; interoperable/third-party platforms are forecast to expand at a 11.85% CAGR.

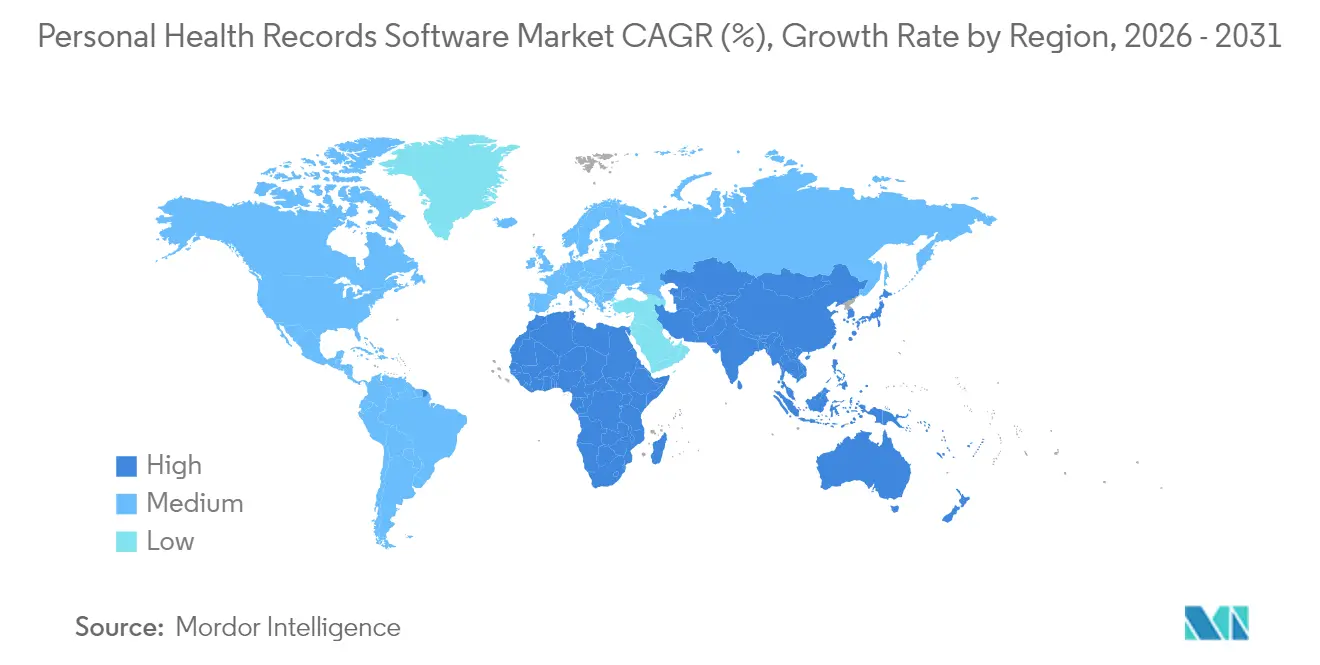

- By geography, North America held 53.30% of personal health records software market share in 2025, whereas Asia-Pacific is set to grow 11.60% annually during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Personal Health Records Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Need for Streamlined Healthcare Information and Rising Initiatives to Encourage Patient Centric Personal Care | 2.6% | Global, with stronger impact in North America and Europe | Medium term (2-4 years) |

| Rising Government Initiatives for Online Data Integration | 2.3% | North America, Europe, and emerging Asia-Pacific markets | Medium term (2-4 years) |

| Surging Chronic Disease Burden Driving Continuous Patient Engagement Needs | 1.7% | Global, with significant impact in aging populations (Japan, Europe, North America) | Long term (≥ 4 years) |

| Telehealth & Remote Monitoring Expansion Requiring Seamless Data Exchange | 1.4% | North America, Europe, and urban centers in Asia-Pacific | Short term (≤ 2 years) |

| Smartphone Surge Enabling Mobile-First PHR Adoption | 1.2% | Asia-Pacific, Latin America, and emerging markets globally | Short term (≤ 2 years) |

| Cloud Cost-Optimization Expanding SaaS PHRs | 1.0% | Global, with particular impact on SMEs and cost-conscious organizations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Streamlined information & patient-centric care

Healthcare data sit in multiple silos, pushing patients to demand one-stop visibility into medications, test results, and visit notes. The 21st Century Cures Act bans information blocking, triggering portal log-ins that show 90% of users reviewing lab values and 70% reading clinical notes.[1]U.S. Department of Health & Human Services, “21st Century Cures Act Fact Sheet,” hhs.gov Smartphone comfort levels remain high, with 51% of Americans accessing records on mobile apps. Providers deploying intuitive portals report higher satisfaction metrics, and cross-industry consumer expectations continue to pressure laggard systems. The personal health records software market therefore benefits from better clinical workflows, easier data aggregation, and growing provider incentives tied to value-based contracts.

Government online data-integration mandates

Public-sector policies now require standardized APIs that give consumers friction-free control over data. The CMS Patient Access, Provider Access, and Payer-to-Payer APIs must all be live by 2027.[2]Federal Register, “Patient Access and Interoperability Requirements,” federalregister.gov India’s Ayushman Bharat Digital Mission has already created more than 7.3 billion health accounts, providing a model of mobile-first enrollment. The CDC’s USD 500 million Data Modernization Initiative is modernizing surveillance and reporting pipelines.[3]Centers for Disease Control and Prevention, “Data Modernization Initiative Overview,” cdc.gov Indonesia’s FHIR-based Satusehat platform underscores the global preference for the HL7 FHIR standard. These mandates collectively accelerate the adoption curve in the personal health records software market by lowering vendor integration barriers.

Rising chronic-disease burden

Sixty percent of U.S. adults now live with at least one chronic condition, expanding demand for continuous engagement tools. Medicare reimburses remote patient monitoring when at least 16 days of data are captured within 30 days, powering AI-driven early-warning algorithms. Evidence in Nature shows that digital interventions using feedback, reminders, and social support increase adherence to self-care behaviors nature.com. As vendors embed predictive analytics into PHR dashboards, the personal health records software market is transitioning from passive repositories into active disease-management platforms.

Telehealth & RPM expansion

Eighty percent of providers are raising health-IT budgets in 2025, prioritizing interoperability that merges telehealth video consults, connected-device feeds, and clinic visits. Validic now pushes continuous glucose-monitoring streams directly into Epic and Oracle Health EHR fields. Physician groups foresee comprehensive patient engagement powered by wearables, AI summarization, and integrated coaching. Seamless aggregation of multimodal data differentiates solutions in the personal health records software market, boosting both clinical efficiency and patient retention.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Security Concerns Regarding the Software | -1.6% | Global, with higher impact in North America and Europe | Medium term (2-4 years) |

| Lack of Awareness Among Rural Patients | -1.1% | Rural areas globally, with significant impact in developing regions | Long term (≥ 4 years) |

| Cyber-Liability Insurance Cost Spike Limiting SME Adoption | -0.8% | North America and Europe, particularly affecting small healthcare providers | Short term (≤ 2 years) |

| Fragmented HIT Standards Hindering Payer-Tethered Interoperability | -0.9% | Global, with particular impact in regions with diverse healthcare systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Security concerns regarding software

Ninety-two percent of healthcare organizations suffered cyberattacks in 2024, and breaches cost an average USD 9.8 million. The Change Healthcare incident alone exposed data on 190 million individuals. Health records fetch up to 50 times the price of financial data on dark web markets, prompting CIOs to assign 19% of IT budgets to security. Staffing shortages persist, with 53% of firms citing inadequate in-house expertise. Blockchain pilots aim to restore trust by giving patients granular consent controls while meeting HIPAA requirements. Unless addressed, these threats may slow conversions in the personal health records software market.

Lack of awareness among rural patients

Rural physicians show 21% lower odds of certified-EHR adoption and record lower Promoting Interoperability scores (80 vs 92 urban). Lower smartphone ownership, patchy broadband, and limited digital-literacy programs constrain PHR on-boarding. Socioeconomic hurdles deepen the divide as rural patients lose out on preventive insights, thereby widening health-equity gaps. Infrastructure grants, easy-language interfaces, and community-based training schemes are needed to sustain personal health records software market penetration in remote geographies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component Type: Services Outpace Software Growth

The Software & Mobile Apps segment commanded 54.10% of the personal health records software market in 2025, buoyed by high smartphone penetration and AI-enabled personalization dashboards. Yet only 2% of users currently combine information from multiple portals, revealing interoperability pain points. Predictive algorithms now summarize lab results, flag medication conflicts, and recommend lifestyle interventions, thereby lifting patient engagement scores and retention. Vendors differentiate through UX design, low-code configuration, and seamless FHIR APIs.

Services held 45.90% in 2025 but will grow faster at 11.12% annually as organizations seek implementation partners for workflow redesign, staff training, and data-quality audits. Managed-service models help smaller clinics bypass capital outlays, while large systems rely on consultants to meet value-based reporting demands. Generative-AI documentation reduces clinician burden, and troubleshooting hot-lines strengthen user loyalty. The personal health records software market size for services is projected to expand more quickly than that for software, giving professional-services firms a larger revenue slice by 2031.

By Deployment Mode: Cloud Solutions Dominate Market

Cloud platforms carried 50.35% of the personal health records software market in 2025 and remain the fastest-growing deployment at 13.05% CAGR. Their subscription model lowers upfront hardware costs; a five-year ownership estimate of USD 58,000 per provider attracts small practices. Seventy-two percent of physicians note better anywhere-access; 85% cite higher patient convenience. Native elasticity supports AI model training and voice-note transcription workflows. Integration blueprints now standardize SSO, MFA, and audit logging, easing compliance.

Web-based/on-premise installs still hold 49.65% but face slower uptake. They satisfy organizations with strict data-sovereignty rules, yet updates lag behind cloud peers. Maintenance cycles and patch management inflate total cost and complicate scalability. As AI adoption accelerates—77% of providers budget for AI CapEx—cloud supremacy in the personal health records software market should widen.

By Architecture: Interoperability Drives Future Growth

Standalone systems represented 38.75% personal health records software market share in 2025, favored by privacy-conscious consumers who aggregate data manually. Only 11% of U.S. adults maintain such a record, and just 5 of 19 audited portals met more than half of patient-desired functions. Manual data entry suppresses engagement frequency, particularly among chronic-disease cohorts needing automated device uploads.

Interoperable/third-party models, although smaller, will rise at 11.85% CAGR. FHIR-ready connectors sync with hospital EHRs, pharmacy databases, and home sensors, turning PHRs into hubs for longitudinal health analytics. Provider-tethered and payer-tethered approaches offer convenience but restrict cross-provider visibility; hybrid orchestration layers are therefore emerging. As API economies mature, the personal health records software market size attributed to interoperable platforms will grow faster than any other architecture class.

Geography Analysis

North America secured 53.30% of the personal health records software market in 2025 on the back of HITECH-funded infrastructure and early consumer portal mandates. The CMS final rule forcing Patient Access APIs promises to tighten integration baselines further by 2027. Nonetheless, cybersecurity remains a caveat; three in four Americans were touched by a breach in 2024. Market resilience stems from payer incentives, mature cloud ecosystems, and a tech-savvy consumer base favoring mobile-first access.

Asia-Pacific is the fastest-growing territory at 11.60% CAGR. India’s Ayushman Bharat Digital Mission enrolled 7.3 billion health IDs, while Indonesia’s Satusehat platform demonstrates scalable FHIR adoption. High smartphone penetration and government e-health grants accelerate pilot rollouts in urban clinics. Domestic vendors partner with telecom operators to deliver SMS-based reminders, ensuring inclusion of feature-phone users. By 2030 the regional personal health records software market size is expected to rival Europe’s current level.

Europe commands considerable share anchored by the General Data Protection Regulation and the forthcoming European Health Data Space. Estonia already migrated from CDA to FHIR, proving national-scale semantic interoperability. Data-localization rules increase vendor compliance costs yet also engender consumer trust. Communications regulators in France and Germany are evaluating mobile-SIM authentication frameworks to streamline access. Meanwhile, Middle East & Africa plus South America are in the early digitization phase but benefit from leapfrog mobile strategies. Refugee and migrant health programs highlight the utility of portable EPHRs amid continuity-of-care challenges.

Competitive Landscape

The personal health records software market is moderately concentrated. Epic’s MyChart remains the most widely used patient portal in U.S. hospital systems and continues to cross-sell telehealth modules. Oracle Health holds a major share in acute-care EHR share and courts defense and Veterans Affairs facilities. Apple Health Records and Microsoft Azure Health Data Services leverage consumer ecosystems and hyperscale cloud to elevate UI expectations.

Strategic integrations redefine value propositions. Validic’s continuous-glucose feed into Epic and Oracle Health reduces manual data reconciliation. Samsung’s collaboration with Eka Care embeds India-specific e-wallet IDs into its wearables. Experity’s tie-up with ChartSwap expedites urgent-care record exchange, minimizing claimant wait times.

Artificial intelligence now tips the playing field. In February 2025, Validic released a generative-AI engine that auto-summarizes RPM streams, shaving minutes off each encounter. Oracle updated its EHR to include AI-driven note suggestions and population-health forecasting. White-space opportunities persist in rural connectivity, low-literacy UX, and blockchain-verified consent management. Vendors excelling at security, simplicity, and standards alignment are set to broaden their footprint in the personal health records software market.

Global Personal Health Records Software Industry Leaders

Innovaccer, Inc.

Healthspek

Zapbuild

kaaspro

Validic

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Validic launched Generative AI-powered insights for remote patient monitoring, automating the creation of patient data summaries and progress notes within electronic health records to simplify data interpretation for healthcare providers

- February 2025: Experity partnered with ChartSwap to enhance digital record retrieval processes specifically for urgent care clinics, streamlining access to personal health records and improving efficiency in urgent care settings

- January 2025: Samsung, the consumer electronics giant, has partnered with health tech company Eka Care to introduce the "Health Records" feature on the Samsung Health app. This collaboration aims to provide users with a more comprehensive approach to managing their health.

- October 2024: Oracle's announced cutting-edge electronic health record (EHR) system, enhanced with advanced cloud and artificial intelligence features, represents a key development in its health-care portfolio. This launch is Oracle's most significant update since its USD 28 billion acquisition of Cerner, a leading name in medical records, in 2022. With this new EHR, Oracle aims to strengthen its position in the highly competitive EHR market, where it has faced challenges in recent years.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the personal health records (PHR) software market as all cloud- or web-based applications that let patients create, store, and selectively share longitudinal clinical information, including diagnoses, test results, medications, immunizations, care plans, and visit notes, outside the provider's core EHR environment.

Scope Exclusion: Modules locked inside hospital or payer systems without a stand-alone patient view are excluded.

Segmentation Overview

- By Component Type

- Software and Mobile Apps

- Services

- By Deployment Mode

- Cloud-Based

- Web-Based

- By Architecture

- Provider-Tethered

- Payer-Tethered

- Standalone

- Interoperable / Third-Party

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured interviews with hospital IT heads, digital-health founders, insurer data officers, and patient-advocacy leaders across North America, Europe, and Asia-Pacific. These dialogues converted anecdotal usage and churn patterns into measurable adoption curves and clarified price corridors, security hurdles, and upgrade cycles.

Desk Research

We began with tier-one public datasets from the World Bank, OECD Health, and the U.S. Office of the National Coordinator for Health IT that track digital-record adoption. We then scanned bodies such as HIMSS, AHIMA, and the Asia eHealth Information Network for interoperability mandates. Company 10-Ks and investor days offered active-user counts and subscription pricing that anchor vendor economics. Patent abstracts on Questel, plus news archives in Dow Jones Factiva, revealed feature roadmaps, for example, smartphone biometric log-ins. Regional health-ministry tender portals and Volza shipment records helped approximate device bundles carrying pre-installed PHR apps, while IMF inflation tables and Federal Reserve currency series normalized historical revenues. The sources listed illustrate the range; many additional open reports and filings were reviewed for cross-checks.

Market-Sizing & Forecasting

Our top-down model starts with smartphone penetration, adult chronic-disease prevalence, and provider portal roll-out rates. Survey-validated sign-up ratios convert these pools into active PHR users. Supplier revenue roll-ups and sampled price x user checks are then overlaid. Key variables tested in sensitivity runs include hosting-cost deflation, CMS Patient Access API deadlines, cyber-insurance premiums, and telehealth visit volumes. Forecasts to 2030 employ multivariate regression with ARIMA smoothing and are finalized in expert workshops.

Data Validation & Update Cycle

Outputs pass anomaly flags if they deviate more than five points from ONC download statistics or credit-card spend on health apps, after which an analyst peer review and manager audit certify traceability. Reports refresh annually, with interim updates triggered by material policy or breach events.

Why Mordor's Personal Health Records Software Baseline Inspires Confident Decisions

Published estimates diverge because firms select different scopes, currencies, or usage metrics, and some quote license bookings while others cite active users. The widest gaps arise when embedded EHR portals or free wellness apps are folded in, or when average selling prices remain flat. Mordor removes those elements and applies yearly exchange rates, producing a cleaner stand-alone software view.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 9.66 B (2025) | Mordor Intelligence | - |

| USD 9.67 B (2024) | Regional Consultancy A | Includes payer-portal modules; relies on booking values |

| USD 10.60 B (2024) | Global Consultancy B | Counts free wellness apps; single-year FX conversion |

Differences narrow once scope and currency are aligned, and our disciplined filtration plus annual refresh cadence leave Mordor Intelligence's figure as the most reproducible baseline for strategic planning.

Key Questions Answered in the Report

What is the current personal health records software market size and growth outlook?

The personal health records software market size is USD 10.56 billion in 2026 and is projected to hit USD 16.47 billion by 2031, a 9.32% CAGR during 2026-2031.

Which deployment mode leads the market?

Cloud-based platforms held 50.35% personal health records software market share in 2025 and will expand at a 13.05% CAGR through 2031.

Which region is growing the fastest?

Asia-Pacific is the fastest-growing region, expected to register a 11.60% CAGR during 2026-2031 thanks to large-scale government digital-health programs.

What is the biggest restraint to adoption?

Cybersecurity concerns remain the top barrier, with breaches costing USD 9.8 million per incident on average and driving up security spending to 19% of health-IT budgets.

Which emerging technology is most influential?

Artificial intelligence, especially generative-AI summarization of remote patient monitoring data, is becoming a key differentiator for vendors targeting clinical-workflow efficiency.

Page last updated on: