Market Overview

| Study Period | 2020 - 2031 |

|---|---|

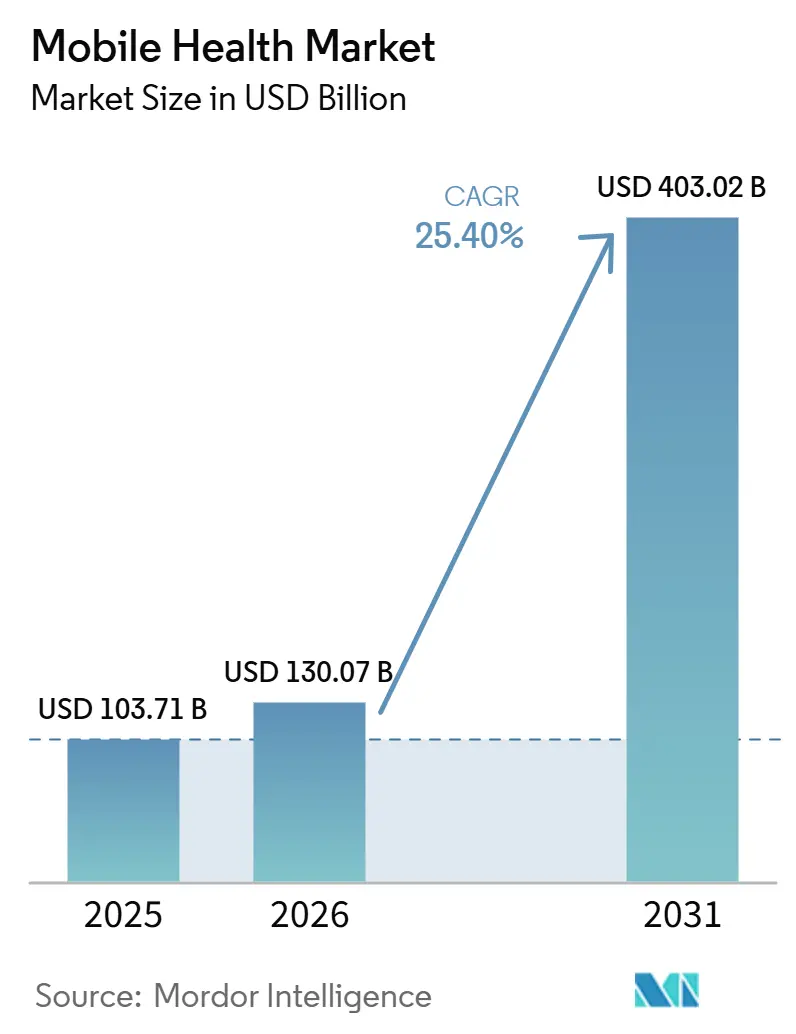

| Market Size (2026) | USD 130.07 Billion |

| Market Size (2031) | USD 403.02 Billion |

| Growth Rate (2026 - 2031) | 25.40% CAGR |

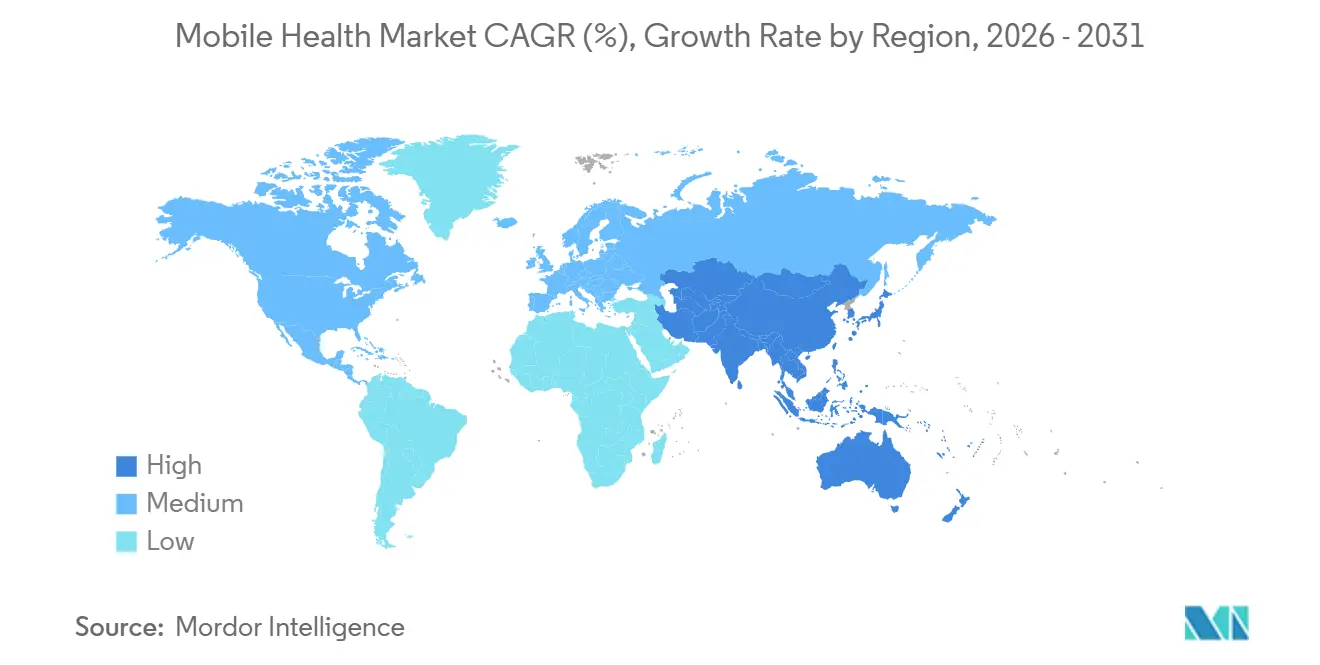

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players_Market_1.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mobile Health Market Analysis by Mordor Intelligence

Mobile health market size in 2026 is estimated at USD 130.07 billion, growing from 2025 value of USD 103.71 billion with 2031 projections showing USD 403.02 billion, growing at 25.4% CAGR over 2026-2031. Rapid smartphone adoption, falling data prices and the fusion of artificial intelligence with mobile platforms are accelerating real-time diagnostics and personalized care at scale. Asia-Pacific’s surge is beginning to erode North America’s long-held lead, prompting incumbents to rebalance regional portfolios while new entrants ride favorable demographics and supportive government policies. Diagnostics is outpacing the once-dominant monitoring segment as portable, hospital-grade sensors migrate into everyday wearables, reshaping product roadmaps and reimbursement negotiations. Competitive intensity is climbing as technology giants, medical-device leaders and nimble start-ups vie for data ownership that can anchor recurring revenue models. At the same time, evolving privacy regulations and patchy clinical-validation standards inject uncertainty that forces investors and providers alike to weigh speed-to-market against long-term compliance resilience.

Key Report Takeaways

- By geography, North America commanded 37.45% of market share in 2025, while Asia-Pacific is forecast to grow the fastest at a 28.7% CAGR through 2031.

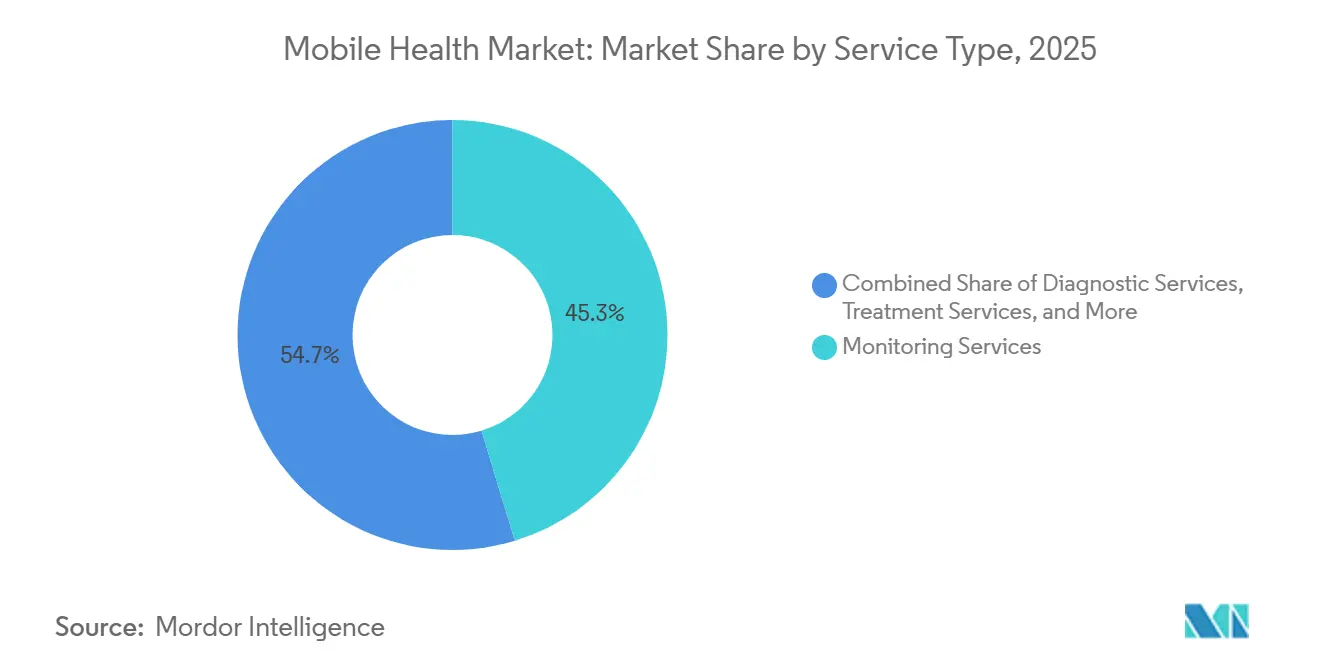

- By service type, Monitoring Services led with a 45.30% share in 2025; Diagnostic Services are set to expand at a 26.3% CAGR to 2031.

- By device type, Blood Glucose Monitors held 27.60% of revenue in 2025, whereas Respiratory Monitors show the strongest outlook with a 27.2% CAGR forecast for 2026-2031.

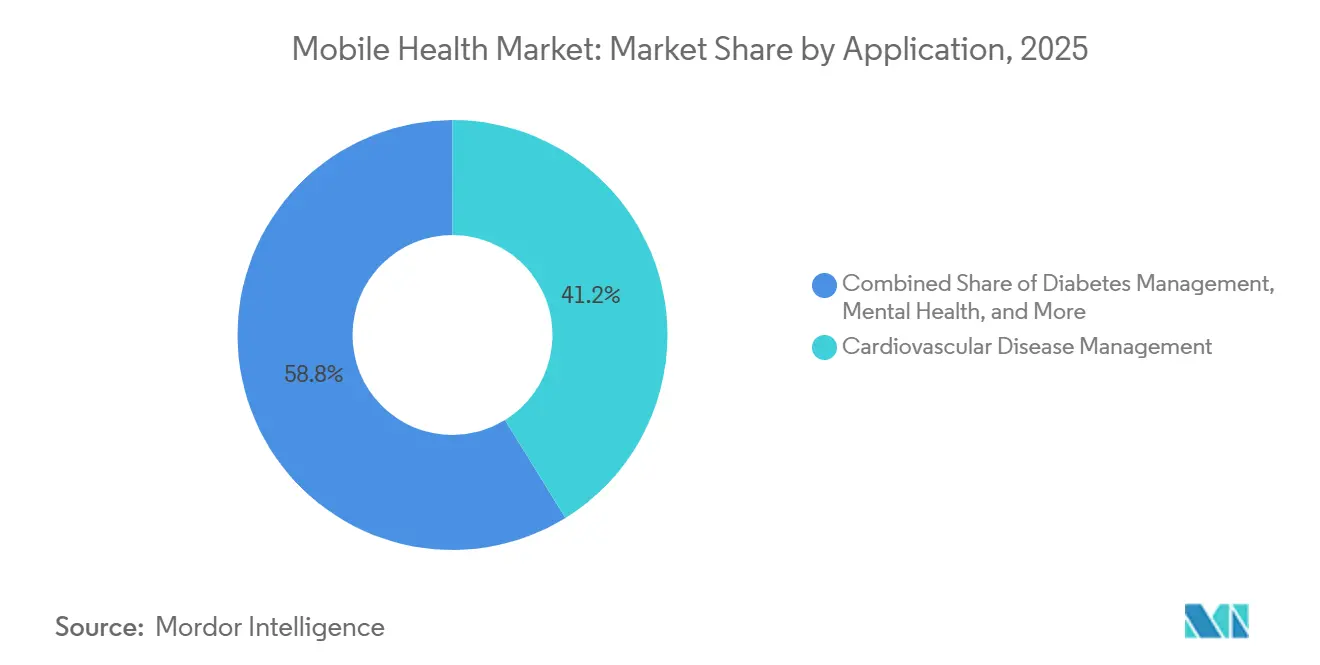

- By application, Cardiovascular Disease Management accounted for 41.20% of the market size in 2025, while Mental Health & Behavioral solutions are advancing at a 27.8% CAGR through 2031.

- By stakeholder, Application/Content Players captured 38.40% market share in 2025, and Healthcare Providers represent the fastest-growing group with a projected 26.9% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mobile Health Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration of mHealth Platforms with National EHR Systems Accelerating Clinical Adoption | +4.0% | North America, EU, GCC, Asia-Pacific | Medium term (3-4 years) |

| Expansion of Remote Patient-Monitoring Reimbursement Codes | +3.5% | North America, APAC, Western Europe | Short term (≤2 years) |

| Sensor Miniaturization & Battery Advances Enabling Medical-Grade Wearables | +2.8% | Global, with early gains in U.S., Japan, EU | Medium term (3-4 years) |

| Consumer Shift Toward On-Demand Virtual Care via App-Store Ecosystems | +2.3% | Global, especially U.S., India, China | Short term (≤2 years) |

| Corporate Wellness Programs Scaling App Subscriptions Through Bundled Health Insurance | +1.5% | North America, Europe, Japan | Medium term (3-4 years) |

| Source: Mordor Intelligence | |||

Integration of mHealth Platforms with National EHR Systems Accelerating Clinical Adoption

Mobile Health market adoption accelerates when data from apps flows directly into Electronic Health Records, a shift now visible in Gulf Cooperation Council hospitals where more than three-quarters of public facilities expose mobile interfaces. Clinical teams report fewer duplicate entries, suggesting that interoperability reduces cognitive load and frees time for patient engagement. An overlooked consequence is that vendors supplying robust application programming interfaces become de-facto gatekeepers of longitudinal patient information. This new dependency encourages health systems to negotiate long-term contracts with interoperability leaders, tilting purchasing decisions toward platforms over point solutions. The Mobile Health industry therefore sees integration talent emerge as a top hiring priority, an inference that suggests wage inflation for interface engineers in the short term. As more countries legislate data-sharing standards, competitive advantage will hinge on speed of compliance rather than on feature count alone.

Expansion of Remote Patient-Monitoring Reimbursement Codes

The latest Centers for Medicare & Medicaid Services rules introduce distinct payment pathways for Remote Physiologic Monitoring and Remote Therapeutic Monitoring, creating a clearer business case for Mobile Health market participants. Providers that once hesitated to prescribe connected devices now receive predictable revenue streams, which in turn drives hospital procurement teams to standardize on enterprise-wide platforms instead of pilot projects. A knock-on effect is a deeper partnership between financial officers and clinical leaders, because reimbursement optimization becomes inseparable from care-path redesign. This linkage is nudging technology suppliers to bundle billing analytics with sensor hardware, transforming their offering from device sales to margin-enhancement services. The fresh inference is that reimbursement literacy becomes a core competency for product managers, signaling a career pathway that did not exist five years ago. As payers replicate these codes outside the United States, first movers will likely transplant proven billing templates into new territories and shorten time to profitability.

Sensor Miniaturization & Battery Advances Enabling Medical-Grade Wearables

Breakthroughs in low-power electronics now allow ultrasound imagers and glucose sensors to fit inside wearables that remain comfortable for 24-hour use, closing the accuracy gap with hospital-grade equipment. Continuous hemodynamic data that once required intensive-care beds is entering consumer smartwatches, giving clinicians unprecedented visibility between appointments[1]University of California San Diego, “Wearable Ultrasound Patch for Continuous Cardiac Imaging,” ucsd.edu. This capability turns longitudinal monitoring into a standard of care rather than an exception, pushing insurers to rethink risk scoring models. Component suppliers experience an upside as demand for customized micro-batteries grows, but they must also navigate tougher clinical validation hurdles that come with medical-device classification. An emerging inference is that intellectual property around energy management, not just sensor design, becomes an acquisition target for conglomerates seeking to verticalize their Mobile Health industry footprint. Competitive differentiation may soon pivot on the number of charge cycles rather than on sensor count.

Consumer Shift Toward On-Demand Virtual Care via App-Store Ecosystems

Consumers accustomed to frictionless retail experiences increasingly expect health consultations to be available at the tap of an icon, a preference mirrored in the projection that app downloads will surpass 5 billion annually by 2025. Traditional providers respond by embedding scheduling, payment, and follow-up within a single interface, effectively bringing the clinic to the smartphone. This convenience raises patient satisfaction scores, which are now tied to reimbursement in many value-based contracts, illustrating how consumer delight converts into financial performance. An unspoken implication is that brick-and-mortar capacity planning must adapt to fluctuating in-person volumes as virtual visits absorb routine cases. The Mobile Health market therefore witnesses hospital systems repurposing real estate into logistics hubs for home-care teams. A new inference is that retail giants with expertise in last-mile delivery hold transferable skills that could disrupt pharmacy and diagnostics distribution.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Clinical Validation & Real-World Evidence | -2.2% | North America, EU, Japan | Short term (≤2 years) |

| Interoperability Challenges with Legacy Hospital IT | -1.8% | Global, acute in U.S., EU, MEA | Medium term (3-4 years) |

| Heightened Data-Privacy Concerns Reducing Patient Consent Rates | -1.5% | High-income markets, North America, EU | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Limited Clinical Validation & Real-World Evidence Undermining Physician Prescription of Apps

Although the Food and Drug Administration has cleared more than 500 artificial-intelligence tools, many lack longitudinal outcome data, and physicians hesitate to prescribe unvalidated apps. Comparative studies show consumer wearables detecting fewer atrial-fibrillation events than implantable monitors, reinforcing physician skepticism. This credibility gap leads to a dichotomy where patient-generated data proliferates but seldom informs clinical decisions, an inefficiency that frustrates both parties. Vendors respond by partnering with academic centers for pragmatic clinical trials that align with digital-tool development cycles, shortening evidence generation timelines. The Mobile Health industry consequently adopts hybrid business models that blend software iteration with randomized-controlled methodologies, an operational convergence once considered incompatible. The new inference is that statistical literacy becomes essential for go-to-market teams, as product claims must withstand peer review to win formulary placement.

Interoperability Challenges with Legacy Hospital IT Slowing Enterprise Deployments

Hospitals running on legacy information systems face costly data mapping and interface customization when integrating Mobile Health platforms, delaying enterprise rollouts. Small community providers feel this burden most acutely because they lack dedicated informatics staff, widening a digital divide within healthcare delivery. This fragmentation drives merger activity as health systems seek scale to afford modern interoperable infrastructure, indirectly reshaping regional care landscapes. Vendors perceive the pain point and position turnkey data-normalization layers as differentiators, accelerating a shift toward platform-as-a-service offerings. A fresh inference is that interoperability standards compliance becomes a hidden barrier to entry for start-ups, raising the strategic value of middleware partnerships. Policymakers aiming to foster innovation may need to subsidize interface development for smaller facilities to avoid entrenching disparities[2]Office of the National Coordinator for Health Information Technology, “Interoperability Standards Advisory,” healthit.gov.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Monitoring Services Lead While Diagnostics Accelerate

Monitoring services captured 45.30 % Mobile Health market share in 2025, anchored by robust reimbursement codes that secure predictable cash flows for providers. Their market size advantage stems from chronic-disease programs that rely on daily physiologic data to trigger timely interventions, a practice that lowers readmission penalties. Diagnostics, though smaller today, are forecast to expand at a 26.3 % CAGR to 2031 as AI-enhanced tools demonstrate specialist-level accuracy in early studies. This momentum suggests convergence: platforms increasingly bundle both monitoring and diagnostic functionality, blurring categorical boundaries. An immediate inference is that reimbursement frameworks may need revision to avoid double-counting services when a single device performs dual roles. Stakeholders that anticipate this merger of categories could pre-emptively align billing codes and secure first-mover advantage.

By Device Type: Glucose Monitors Maintain Lead as Respiratory Innovations Surge

Blood-glucose monitors account for 27.60 % of the Mobile Health market size in the device category, a dominance explained by global diabetes prevalence and the clinical imperative for tight glycemic control. Continuous innovation, such as rice-sized implantable sensors lasting up to a year, promises to extend replacement cycles and thus reshape revenue models toward subscription analytics. Respiratory monitors, projected at 27.2 % CAGR to 2031, ride a wave of post-pandemic awareness of pulmonary health and leverage machine-learning algorithms that flag deterioration before subjective symptoms emerge. An inference from these trajectories is that multi-sensor devices integrating glucose, respiratory, and cardiac data could cannibalize single-parameter hardware. Suppliers must therefore evaluate whether to protect niche leadership or pivot to platform strategies.

By Application: Cardiovascular Disease Management Dominates While Mental Health Accelerates

Cardiovascular disease management applications held 41.20 % Mobile Health market share in 2025, underpinned by value-based care contracts that reward reduced hospitalizations for diabetes, heart failure, and chronic obstructive pulmonary disease. Artificial-intelligence models personalize nudges and dosage adjustments, demonstrating tangible cost savings that resonate with payers. Mental health applications, forecast to grow 27.8 % annually, benefit from rising societal openness and the convenience of chat-based cognitive behavioral therapy. The juxtaposition indicates that payer willingness to reimburse digital behavioral interventions is catching up with physical-health counterparts, narrowing a historical funding gap. A fresh inference is that integrated care plans pairing metabolic and mental-health support could emerge as a new standard, given comorbidity correlations between depression and chronic illness.

By Stakeholder: App Developers Lead While Provider Adoption Accelerates

Application and content developers held a 38.40 % Mobile Health market share in 2025 because app-store distribution bypasses traditional procurement cycles and reaches consumers directly. Their agility in updating software weekly contrasts with hardware refresh timelines, allowing rapid response to user feedback. Healthcare providers, growing at 26.9 % CAGR, now deploy institution-branded apps that keep patients inside a curated ecosystem, reclaiming digital engagement previously ceded to consumer tech firms. This reclamation is aided by reimbursement reforms that reward virtual touchpoints. An inference is that co-development partnerships between providers and independent developers will proliferate, blending clinical credibility with design excellence to meet user expectations without sacrificing safety.

Geography Analysis

Asia-Pacific, projected to grow at 28.7% CAGR, benefits from large underserved populations and government investments in 5G hospital corridors. Indian health-tech start-ups draw global capital, while Chinese pilot programs for private standalone 5G networks showcase local innovation. The region’s willingness to integrate traditional medicine within digital platforms offers culturally tuned engagement models that could inspire global product adaptations. A new inference is that multinationals unable to localize content risk stagnation despite technical excellence.

Europe maintains a strong position owing to regulatory frameworks like the General Data Protection Regulation that balance innovation with patient safeguarding. The Middle East’s Vision 2030 initiatives foster public-private partnerships, propelling teleconsultation volumes and positioning the Gulf as a proving ground for AI triage tools. South America’s adoption curve reveals that affordability drives uptake: low-cost smartphones paired with prepaid data bundles broaden access in Brazil’s interior. An inference across these regions is that regulatory heterogeneity will compel vendors to modularize compliance features to scale efficiently.

Competitive Landscape

The Mobile Health market’s fragmented structure sees consumer electronics giants, medical device incumbents, and venture-backed start-ups jostling for relevance, often through partnerships that combine scale with niche expertise. Apple and Samsung leverage device ecosystems to collect continuous data streams, while Medtronic and Philips emphasize FDA-cleared precision. Comparative studies that favor implantable monitors over smartwatches highlight a credibility gap that consumer brands must close to penetrate clinical workflows. A fresh inference is that future competition may revolve around the quality of clinician dashboards rather than raw sensor accuracy, as decision support becomes the bottleneck.

White-space opportunities persist in women’s health, pediatrics, and rare diseases where unmet needs align with tailored digital interventions. Start-ups in these niches attract investment despite the broader market’s consolidation because differentiated clinical insight outweighs scale at early stages. Platform companies engage in roll-ups, illustrated by acquisitions such as Transcarent’s purchase of Accolade for USD 621 million, aiming to own more of the care continuum. The inference here is that valuation multiples increasingly correlate with breadth of covered therapeutic areas rather than single-product revenue.

Investment patterns reveal a flight to quality; later-stage funding gravitates toward firms demonstrating not just user growth but validated outcomes and reimbursement traction. Strategic investors from telecommunications and insurance join traditional venture capital, motivated by synergies in connectivity and risk management. This cross-industry interest accelerates global expansion for portfolio companies, yet also raises antitrust scrutiny as data aggregation aggregates power. An emerging inference is that regulators may impose data-sharing mandates on dominant platforms to maintain competitive plurality.

Mobile Health Industry Leaders

Medtronic PLC

Cisco Systems, Inc.

Koninklijke Philips N.V.

Samsung Electronics Co. Ltd.

Johnson & Johnson (Verily)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Mobile-health Network Solutions agreed to acquire Indopacific Health Technology Pte. Ltd. and its Lifepack pharmacy and telehealth units, indicating regional consolidation momentum.

- January 2025: Samsung India integrated Ayushman Bharat Health Account access into Samsung Health, exemplifying device-maker moves to embed national health-ID schemes within consumer apps.

- December 2024: DocGo expanded its partnership with SHL Telemedicine to deploy portable 12-lead ECG units in mobile clinics, showcasing a model for reaching underserved communities.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the mobile health (mHealth) market as the total annual value generated when smartphones, tablets, wearables, and connected sensors are paired with software and cloud services to deliver, support, or enhance clinical care, self-care, and wellness management. Revenue streams therefore include device sales, subscription or license fees for apps and platforms, and reimbursable remote-monitoring or tele-consult services.

Scope exclusion: laboratory-grade diagnostic hardware that cannot transmit data to a mobile device is left outside this assessment.

Segmentation Overview

- By Service Type

- Treatment Services

- Independent Aging Solutions

- Chronic Disease Management

- Diagnostic Services

- Monitoring Services

- Remote Patient Monitoring Devices

- Medical Call Centers Manned by Healthcare Professionals

- Tele-consultation

- Post-Acute Care Services

- Wellness & Fitness Solutions

- Other Services

- Treatment Services

- By Device Type

- Blood Glucose Monitors

- Cardiac Monitors

- Hemodynamic Monitors

- Neurological Monitors

- Respiratory Monitors

- Body & Temperature Monitors

- Remote Patient Monitoring Devices

- Other Device Types

- By Application

- Cardiovascular Disease Management

- Diabetes Management

- Mental Health & Behavioral Disorders

- Women's Health & Fertility Tracking

- Fitness & Lifestyle Tracking

- By Stakeholder

- Mobile Network Operators

- Healthcare Providers

- Application / Content Players

- Payers & Employers

- Other Stakeholders

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed clinicians running remote patient-monitoring programs, digital therapeutics product managers, hospital CIOs, and payer policy heads across North America, Europe, and Asia-Pacific. These discussions validated device life cycles, average selling prices, compliance hurdles, and uptake curves that rarely appear in public documents.

Desk Research

We began with structured reviews of tier-1 public domains such as WHO health-tech bulletins, OECD Health Statistics, US CMS utilization files, and Eurostat ICT surveys, which help us map device adoption and reimbursement shifts. Trade bodies like the Mobile Ecosystem Forum and the International Diabetes Federation add detail on handset penetration and disease pools, while filings and investor decks from leading digital-health vendors reveal pricing, user counts, and regional rollouts. Selected paid libraries, including D&B Hoovers for company financials and Dow Jones Factiva for deal alerts, round out the desk work. This list is illustrative; many other verified sources were mined for numbers and nuance.

Market-Sizing & Forecasting

A blended model underpins the estimates. A top-down construct starts with national smartphone bases and chronic disease cohorts, then applies prevalence-to-treated ratios and observed mHealth penetration to compute demand pools, which are further broken into service, device, and app revenues. Bottom-up cross-checks, such as supplier roll-ups, sampled RPM kit ASP × unit volumes, and app-store spend analytics, calibrate the totals. Key variables inside the model include 5G smartphone penetration, chronic disease incidence, RPM reimbursement claim volumes, average sensor ASP movement, annual app downloads, and connected wearable installed base. Forecasts rely on multivariate regression blended with scenario analysis to mirror policy or technology shocks, and gaps in bottom-up data are interpolated with three-year moving averages before peer review.

Data Validation & Update Cycle

Outputs pass sequential variance checks, senior analyst reviews, and reconciliation against independent health-tech funding trends. Models refresh annually, with interim updates triggered by regulatory or pricing events so clients always receive a current view.

Why Mordor's mHealth Baseline Commands Reliability

Published numbers often diverge because each firm picks its own service mix, pricing lens, and refresh rhythm. We acknowledge these differences upfront and outline them for users looking for clear comparisons.

Key gap drivers typically stem from whether reports count reimbursed clinical services, how they handle regional price dispersion, and how frequently assumptions are revisited. According to Mordor Intelligence, our study locks scope to revenue that can be traced to a mobile endpoint and is re-benchmarked every twelve months, whereas others may freeze outlooks for longer or omit clinical billing streams.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 103.71 B (2025) | Mordor Intelligence | - |

| USD 93.12 B (2024) | Global Consultancy A | Apps + wearables only; excludes service fees |

| USD 71.90 B (2024) | Industry Publisher B | Trend extrapolation, limited primary validation |

| USD 70.70 B (2022) | Research Journal C | Older base year, uniform global pricing assumption |

The comparison shows that our disciplined scope selection, annual refresh, and dual-track validation yield a balanced, transparent baseline that decision-makers can replicate and trust.

Key Questions Answered in the Report

What is the current Mobile Health market size and how fast is it growing?

The market stands at USD 130.07 billion in 2026 and is forecast to reach USD 403.02 billion by 2031, reflecting a 25.4 % CAGR.

Which region is expanding fastest within the Mobile Health industry?

Asia-Pacific leads growth with an expected 28.7 % CAGR, driven by rising smartphone penetration and supportive government programs.

Which application segment holds the largest Mobile Health market share?

Cardiovascular disease management applications dominate with 41.20 % share due to their role in reducing hospital readmissions.

What are the main barriers to wider physician adoption of Mobile Health apps?

Limited clinical validation and interoperability challenges with legacy hospital IT systems remain primary obstacles to routine prescription.

Why are corporate wellness programs important for Mobile Health adoption?

Bundled digital health subscriptions offered through employer insurance plans lower acquisition costs for app developers and boost sustained user engagement.

How is 5G influencing the Mobile Health market?

5G enables low-latency, high-bandwidth use cases such as remote surgery and real-time imaging, unlocking applications previously constrained by connectivity limits.

Page last updated on: