Muffins Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 11.21 Billion |

| Market Size (2031) | USD 12.86 Billion |

| Growth Rate (2026 - 2031) | 5.15% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Muffins Market Analysis by Mordor Intelligence

The muffins market size is estimated at USD 10.81 billion in 2025 and is projected to grow to USD 11.21 billion in 2026, reaching USD 12.86 billion by 2031 at a CAGR of 5.15% during 2026–2031. The muffins market growth is being driven by strong demand for convenient breakfast options, increasing consumer preference for premium artisanal products, and ongoing technological advancements in large-scale baking operations. Urban income surges in the Asia-Pacific continue to support the muffins market, bolstered by cold-chain logistics and automation adoption among top bakers, helping stabilize costs amid ingredient volatility and further underpinning this growth. Concurrently, the US FDA's clear regulatory stance on preventive controls benefits established players with advanced quality systems. Digital traceability tools empower these incumbents to swiftly adapt to evolving consumer demands for supply-chain transparency. Moreover, product innovations like gluten-free, high-protein, and low-sugar muffins resonate with health-conscious consumers, amplifying the market's allure. In 2024 and 2025, industry giants such as Hostess, General Mills, and Britannia unveiled functional variants, probiotic-rich and fiber-enhanced muffins, while regional brands rolled out locally inspired flavors to captivate niche audiences. The burgeoning e-commerce landscape and the rise of café continue to strengthen the muffins market. This blend of convenience, health consciousness, and diverse flavors propels the global muffin consumption surge.

Key Report Takeaways

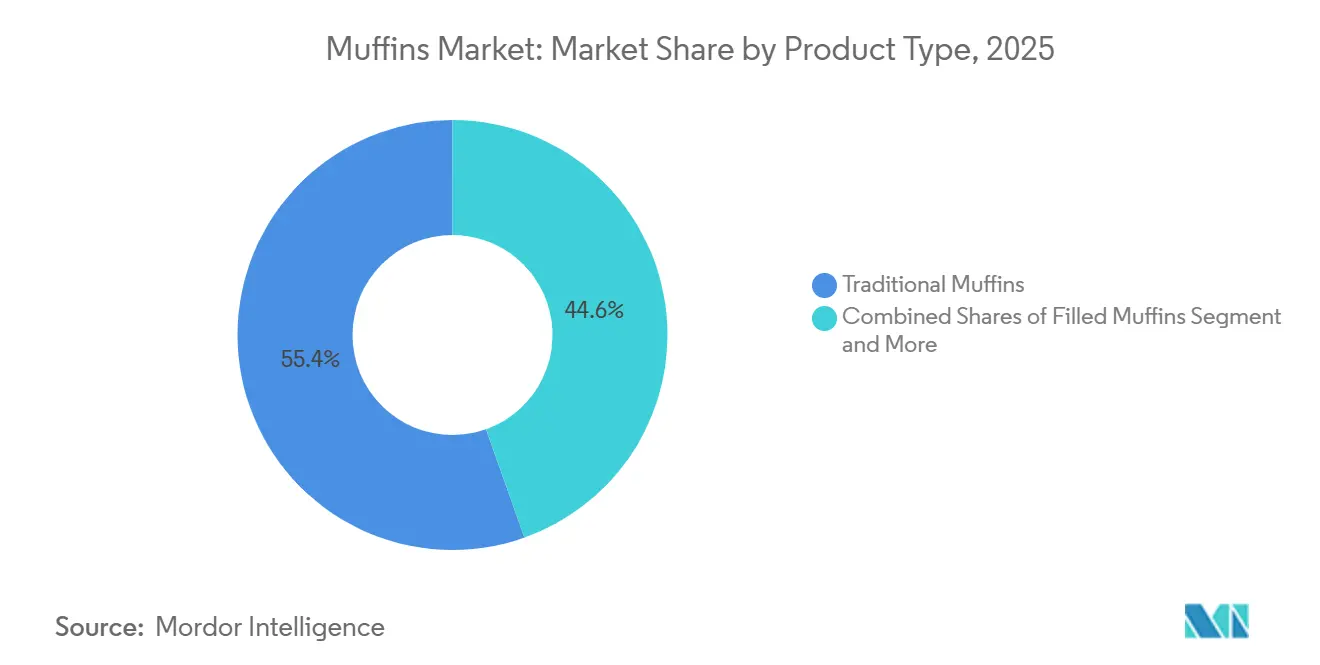

- By product type, traditional muffins held 55.43% of the muffin market share in 2025, whereas filled formats are forecast to expand at a 6.53% CAGR through 2031.

- By category, conventional formats captured 62.36% of the muffin market size in 2025, while gluten-free lines are projected to advance at a 6.67% CAGR during 2026-2031.

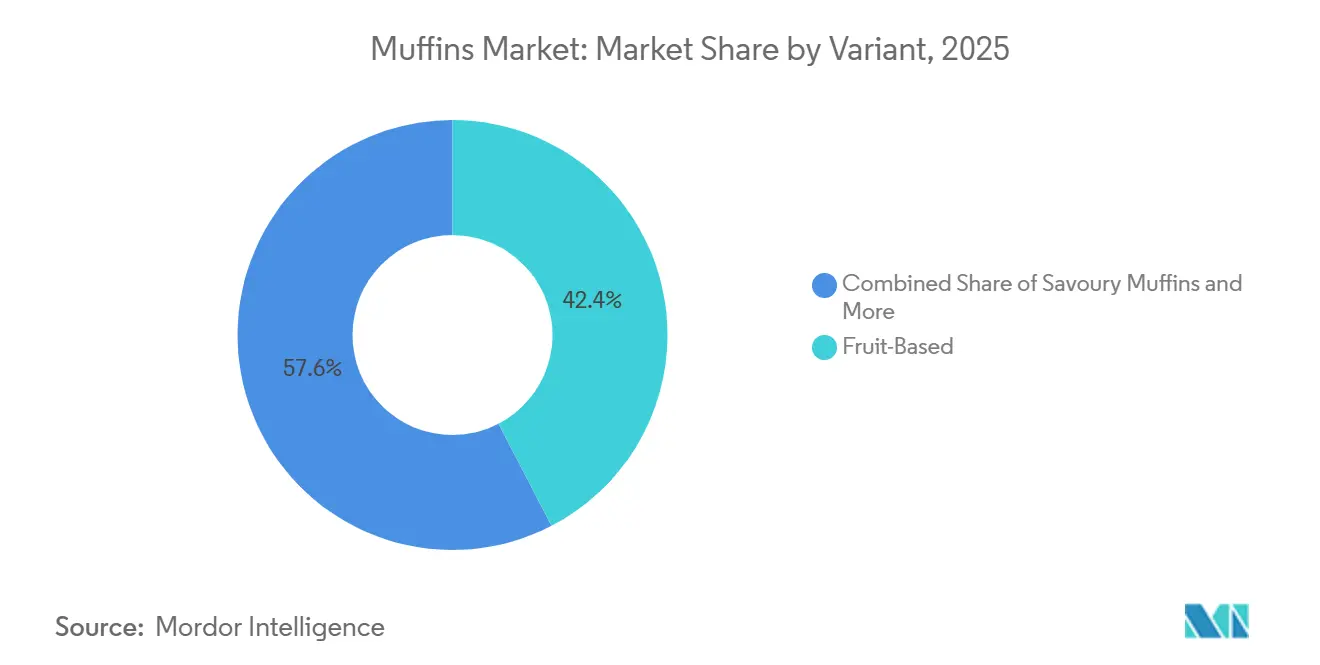

- By variant, fruit-based recipes accounted for 42.38% of 2025 revenue, and chocolate options are expected to grow at a 7.01% CAGR to 2031.

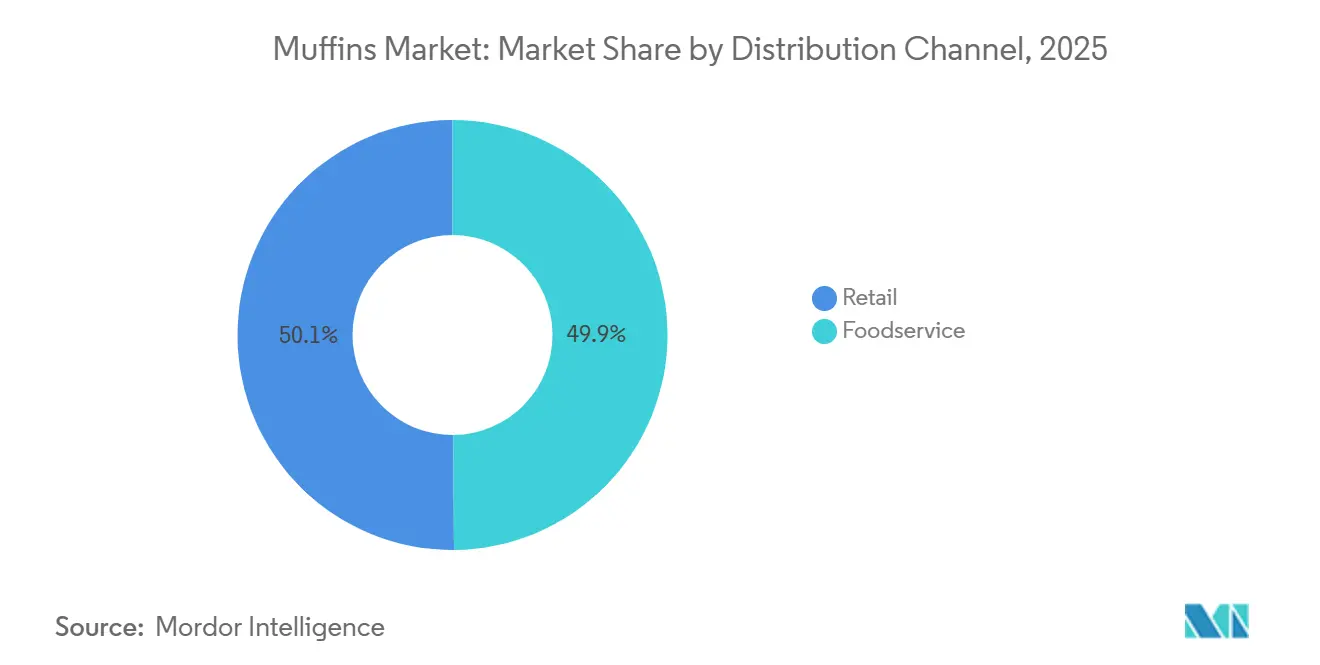

- By distribution channel, retail commanded 50.12% of 2025 sales, yet foodservice outlets are set for 6.35% CAGR growth through 2031.

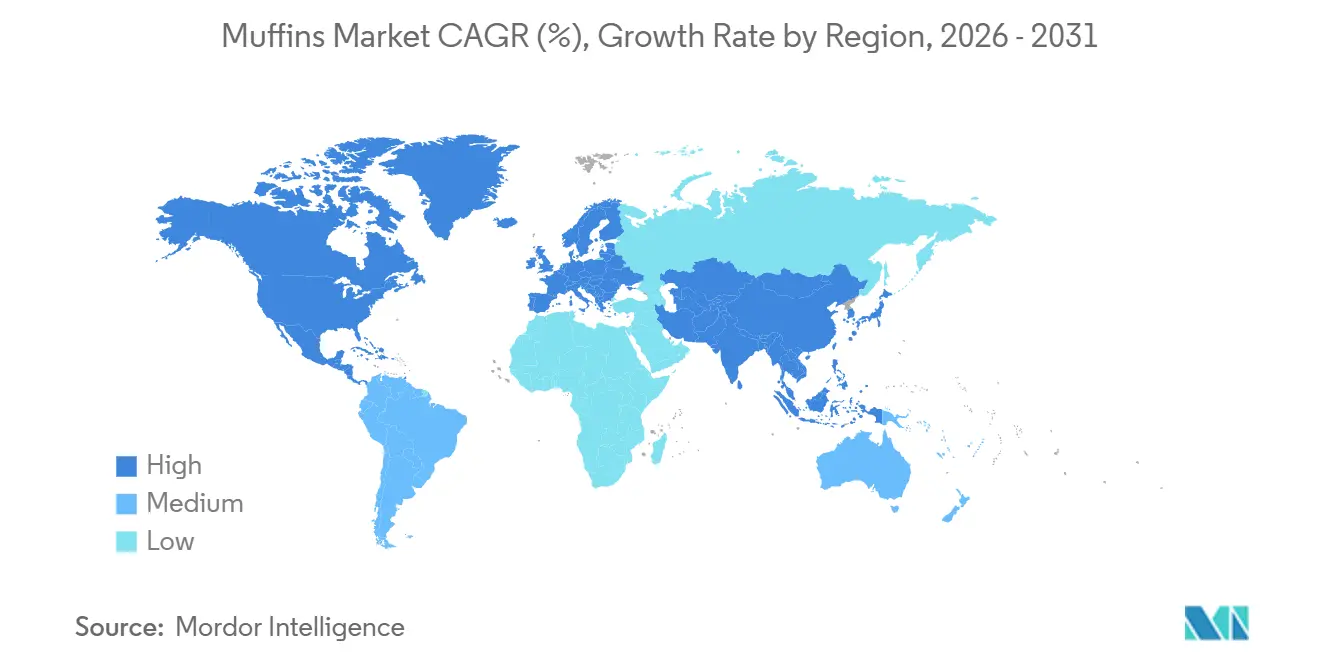

- By geography, Europe generated 40.12% of 2025 turnover, but Asia-Pacific’s muffins market will rise at a 6.61% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Muffins Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Health Awareness Fueling Demand For Gluten‑Free Low‑Sugar And Protein‑Enriched Muffins | +1.2% | Global, with concentration in North America and Western Europe | Medium term (2-4 years) |

| Growing Preference For Grab‑And‑Go Breakfast And Snack Options | +0.9% | Global, strongest in urban centers across North America, Europe, and Asia-Pacific | Short term (≤ 2 years) |

| Innovations In Flavors Fillings And Plant‑Based Varieties | +0.8% | Global, led by North America and Europe, expanding into Asia-Pacific | Medium term (2-4 years) |

| Increasing Vegan And Clean‑Label Product Trends | +0.7% | North America, Europe, and urban Asia-Pacific markets | Medium term (2-4 years) |

| Growth In Foodservice Networks Like Cafes Offering Fresh Muffins | +0.6% | Global, with emphasis on North America, Europe, and emerging Asia-Pacific urban centers | Long term (≥ 4 years) |

| E‑Commerce And Modern Retail Channels Improving Product Accessibility | +0.5% | Global, particularly strong in North America, Europe, and China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Health Awareness Fueling Demand for Gluten-Free, Low-Sugar, and Protein-Enriched Muffins

In the muffins market, functional reformulation is no longer a niche play but a mainstream imperative, with protein-enriched muffins now appearing in mass retail alongside traditional formats. Premier Protein launched microwaveable muffin cups in early 2026, delivering 15 grams of whey isolate per serving and positioning the product as a two-minute breakfast solution that competes directly with protein bars. ADM introduced its HarvestEdge Gold Digestive Support Flour Blend at the 2025 IBIE Innovation Showcase, a prebiotic and postbiotic wheat blend designed to improve fiber performance in baked goods without compromising crumb structure, a technical hurdle that has historically limited high-fiber muffin adoption. Miller Milling's self-sweetening flour, which uses enzyme blends to convert starch into sugar, enables up to 60% reduction in added sugars while preserving sweetness perception, addressing both regulatory pressure and consumer demand for cleaner labels. The challenge lies in replicating the moisture retention and shelf stability of gluten-containing formulations, where clean-label enzymes are increasingly replacing synthetic emulsifiers to maintain texture over refrigerated storage

Growing Preference for Grab-and-Go Breakfast and Snack Options

Urbanization and compressed morning routines continue to drive the muffins market, embedding portable bakery into daily consumption patterns, with muffins capturing share from sit-down breakfast formats and competing with bars and yogurt for on-the-go occasions. Single-serve and mini formats are gaining popularity across the muffins market, driven by portion-control preferences and the ability to command higher per-unit margins while reducing waste at retail. Convenience stores and transit-adjacent retail are expanding bakery assortments, with muffins positioned as ambient-stable, high-margin SKUs that require no refrigeration or reheating, critical advantages over sandwiches and prepared meals. E-commerce penetration in U.S. baked goods is growing at 19.3% annually through 2029, with direct-to-consumer brands leveraging subscription models and bundled offerings to build loyalty. Dutch Bros began testing muffin tops in 2025 to capture the breakfast daypart, illustrating how beverage-led chains view bakery as a traffic driver and ticket-size enhancer. The shift toward snackification, where consumers eat smaller, more frequent meals across dayparts, is expanding muffin consumption beyond breakfast into mid-morning and afternoon occasions, particularly in Asia-Pacific markets where Western snacking habits are still maturing.

Innovations in Flavors, Fillings, and Plant-Based Varieties

Flavor complexity and textural contrast are driving premiumization in the muffins market, as brands compete for social-media visibility and repeat purchases. Filled muffins are expanding at 6.53% annually through 2031, outpacing traditional formats, with caramel, Biscoff, and fruit compotes driving premiumization. Starbucks rolled out globally inspired pastries featuring matcha, yuzu, and pistachio across U.S. locations in 2025, signaling that pan-Asian flavors are transitioning from limited-time offers to core assortments. Hybrid formats such as cruffins, croissant-muffin fusions, saw 224% year-over-year menu increases in 2025, reflecting consumer appetite for laminated textures and premium positioning. Plant-based formulations are expanding opportunities across the muffins market, with egg replacers and butter alternatives now delivering sensory parity in quick breads and muffins, enabling brands to target flexitarian consumers without sacrificing taste or texture. Sourdough fermentation is crossing into sweet applications, with sourdough muffins and sweet focaccia variants offering longer shelf life and flavor depth that justify premium pricing. The challenge is balancing novelty with scalability, as limited-edition flavors generate social engagement but require agile supply chains and co-manufacturing partnerships to avoid inventory risk.

Increasing Vegan and Clean-Label Product Trends

Clean-label formulations are becoming a key competitive factor in the muffins market, as regulators tighten ingredient-disclosure rules and consumers scrutinize unfamiliar additives. The European Food Safety Authority updated allergen thresholds and labeling requirements in 2025, raising compliance costs for brands using synthetic emulsifiers or preservatives[1]Source: European Food Safety Authority, “Allergen Thresholds and Labeling Requirements,” efsa.europa.eu. Cultured dextrose and fermented wheat solutions are replacing calcium propionate and other synthetic mold inhibitors, enabling "no artificial preservatives" claims while maintaining microbiological shelf life. Manildra's GemPro Max, a wheat protein designed to replace synthetic emulsifiers, improves volume and crumb structure while supporting clean-label positioning, critical for brands targeting health-conscious consumers willing to pay premium prices. Vegan muffins are expanding beyond specialty retailers into mainstream grocery stores, with Muffits LLC launching ready-to-eat, individually wrapped protein muffins that are gluten-free, dairy-free, and seed-oil-free, containing 13 grams of protein, collagen, and omega-3s per serving. The company recently expanded its baking facility to meet demand and retail sell-outs, illustrating how small-scale disruptors can capture share by addressing unmet needs for indulgent, better-for-you formats. The risk lies in over-engineering formulations to meet multiple claims, gluten-free, vegan, high-protein, low-sugar, which can compromise taste and texture, the primary drivers of repeat purchase.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Food Safety And Labeling Regulations | -0.4% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| High Sugar And Calorie Content Raising Health And Obesity Concerns | -0.5% | Global, with emphasis on North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Fluctuating Costs Of Key Ingredients Like Flour Eggs And Sugar | -0.6% | Global, with acute impact in import-dependent regions | Short term (≤ 2 years) |

| Supply Chain Disruptions Affecting Ingredient Sourcing And Distribution | -0.3% | Global, with concentration in regions reliant on long-haul logistics | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Food Safety and Labeling Regulations

Regulatory tightening remains a major challenge for the muffins market and accelerating consolidation as smaller producers struggle to meet updated allergen-disclosure, gluten-threshold, and nutritional-labeling requirements. The U.S. FDA finalized updated allergen thresholds and gluten-disclosure rules in 2025, requiring more granular ingredient sourcing documentation and raising the cost of certification for gluten-free claims[2]Source: U.S. Food and Drug Administration, “Food Labeling and Nutrition,” fda.gov. The European Food Safety Authority updated allergen thresholds in 2025, mandating clearer labeling of cross-contamination risks and tightening limits on certain additives, which disproportionately affect co-manufacturing facilities that produce both conventional and allergen-free products. Compliance with ISO 22000 and FSSC 22000 food-safety management systems is becoming a de facto requirement for suppliers to multinational retailers and foodservice chains, adding audit and certification costs that favor larger, vertically integrated producers. The shift toward clean-label formulations, driven partly by regulatory pressure and partly by consumer demand, is forcing reformulation cycles that require R&D investment and shelf-life validation, delaying time-to-market for new SKUs. The strategic implication is that regulatory complexity is a moat for incumbents with scale and a barrier for regional specialists and startups, accelerating M&A as smaller players seek the compliance infrastructure and distribution reach of larger acquirers.

High Sugar and Calorie Content Raising Health and Obesity Concerns

Public-health campaigns and evolving dietary guidelines continue to influence the muffins market to reformulate, even as taste and texture remain the primary drivers of repeat purchase. Traditional muffins often contain 30-40 grams of sugar and 300-500 calories per serving, positioning them closer to dessert than a functional breakfast in the eyes of health-conscious consumers. Miller Milling's self-sweetening flour enables up to 60% reduction in added sugars by enzymatically converting starch into sugar, preserving sweetness perception while lowering total sugar content, a technical solution that addresses both regulatory risk and consumer demand. However, reformulation carries execution risk, as reducing sugar or fat can compromise moisture retention, shelf life, and mouthfeel, leading to consumer rejection and waste. The rise of low-sugar and no-sugar variants reflects this tension, with brands attempting to balance health positioning and sensory appeal. The challenge is that functional claims- high-protein, high-fiber, low-sugar- often require ingredient combinations that increase cost and complexity, compressing margins unless brands can command premium pricing. The strategic implication is that mid-tier brands lacking either scale or differentiation face a margin squeeze, as they cannot absorb reformulation costs or justify premium pricing, accelerating consolidation and private-label encroachment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Filled Variants Outpace Traditional Formats

In 2025, traditional muffins held a 55.43% share of the muffins market, maintaining their dominance in retail and foodservice. However, filled muffins are the fastest-growing product segment in the muffins market, with a 6.53% growth rate annually through 2031, driven by premiumization and textural complexity. These variants, featuring ingredients like caramel and chocolate ganache, command 20-30% price premiums and higher margins, helping brands offset rising costs. Artisanal muffins, marketed as small-batch or locally sourced, are gaining traction in specialty retail and cafes, though their scale remains limited. Savory and hybrid formats, such as cruffins, are moving mainstream, with Japan's CAINZ offering 20 varieties, including meal-replacement options.

Filled muffins' growth reflects a shift toward experiential eating, where sensory novelty and social-media appeal outweigh basic satiation. Finsbury Food Group highlights the success of indulgent stuffed formats like cookies and cakes, which justify premium pricing. Artisanal producers are differentiating with sourdough fermentation and heritage grains, offering extended shelf life and health-conscious appeal. Traditional muffins remain volume leaders in convenience stores and foodservice due to their stability and familiar flavors. Brands must now choose between defending volume in traditional formats or pursuing higher margins in filled and artisanal segments through R&D and quality ingredients.

By Category: Gluten-Free Gains as Conventional Holds Volume

In 2025, conventional muffins dominated the muffin market with a 62.36% market share due to their affordability, broad appeal, and established supply chains. Gluten-free muffins, growing at 6.67% annually through 2031, are driven by increased celiac awareness, non-celiac gluten sensitivity, and demand for "free-from" products. Advances in alternative flours like almond, coconut, and oat, along with clean-label enzymes, are improving gluten-free formulations. Vegan muffins are gaining popularity as plant-based egg and butter substitutes meet consumer expectations for taste and sustainability. Low-sugar variants are expanding, supported by innovations like Miller Milling's self-sweetening flour, which reduces added sugars by 60% while maintaining sweetness.

Conventional muffins benefit from economies of scale, co-manufacturing partnerships, and wide distribution, making them a preferred choice for price-sensitive consumers and foodservice operators. However, their growth is slowing as health-conscious consumers shift to gluten-free, vegan, or low-sugar options, and private-label products gain traction. Gluten-free muffins are growing rapidly, driven by diagnosed celiac cases and a broader perception of gluten-free as healthier. Vegan muffins are moving into mainstream grocery, with brands like Muffits LLC offering gluten-free, dairy-free, and seed-oil-free protein muffins. Low-sugar muffins face challenges in balancing health claims with taste, as reduced sugar can impact moisture and mouthfeel, risking consumer rejection.

By Variant: Chocolate Accelerates as Fruit Retains Lead

In 2025, fruit-based muffins accounted for the largest 42.38% share of the muffins market, reflecting their strong breakfast association and health-focused image. Chocolate-based muffins, growing at 7.01% annually through 2031, are driven by hybrid flavors like miso-caramel and yuzu-chocolate. Their versatility across meal occasions and premium inclusions, such as dark chocolate chunks, support higher price points. Savory muffins, though niche, are expanding in foodservice, with Japan's CAINZ offering meal-replacement options. Hybrid formats like cruffins and multi-texture combinations are gaining traction, while Ardent Mills' wheat-based cocoa replacer helps manage costs for chocolate muffins.

Fruit-based muffins dominate due to their breakfast alignment and perceived health benefits, with blueberry, banana, and apple-cinnamon as top flavors. Exotic fruits like mango and yuzu are being introduced to command premiums. Chocolate muffins grow faster, leveraging indulgent flavors like salted caramel and hazelnut to attract younger consumers. Savory muffins, featuring cheese and vegetables, are moving into mainstream foodservice as meal replacements. While fruit-based muffins retain volume leadership, chocolate and savory variants offer higher growth and margin potential, especially in foodservice and specialty retail markets.

By Distribution Channels: Foodservice Gains as Retail Holds Half

In 2025, retail channels dominated the muffins market with a 50.12% market share, led by supermarkets, hypermarkets, and convenience stores offering diverse assortments and competitive pricing. Foodservice is projected to grow at 6.35% annually through 2031, driven by cafes and quick-service restaurants incorporating muffins into menus beyond breakfast. Supermarkets and hypermarkets dominate with private-label and branded muffins at various price points, leveraging in-store bakery counters to compete with specialty bakeries. Convenience stores are expanding bakery options, positioning muffins as high-margin, ambient-stable products requiring no refrigeration or reheating. Online sales are growing rapidly, with U.S. baked-goods e-commerce expected to expand at 19.3% annually through 2029, supported by subscription models and niche targeting.

Foodservice growth stems from cafes, quick-service restaurants, and institutional operators viewing muffins as high-margin, low-labor items requiring minimal preparation. Over 90% of foodservice operators use frozen bakery products for consistency, labor savings, and waste reduction, with ready-to-bake formats enabling fresh-baked sensory cues. In 2025, Starbucks expanded its U.K. Signature Bakery Collection, while Muffin Break introduced globally inspired flavors and premium inclusions to boost traffic and ticket sizes. Prairie City Bakery launched its Coffee House Muffin line, optimized for thaw-and-serve or quick reheating to meet operators' speed and consistency needs. Retail faces challenges defending share against foodservice and online channels, while foodservice must differentiate as offerings become similar. Retail will remain the volume driver, but growth and margins are shifting to foodservice and online platforms, where brands can justify premium pricing and build direct consumer relationships.

Geography Analysis

In 2025, Europe accounted for the largest 40.12% share of the global muffin market, supported by well-established breakfast and tea traditions. The U.K. leads in per-capita muffin consumption, with Starbucks rolling out its Signature Bakery Collection nationwide. In Germany, artisanal bakeries are consolidating, while discounters are promoting private-label muffins. France, with a bakery consumption of 70.4 kg, indicates a saturation point in unit growth, shifting the competition towards premium SKUs. Bridor's USD 696 million acquisition of Panamar expands frozen distribution in Spain and Portugal, demonstrating a strategic approach to increasing market share. Additionally, stricter EFSA labeling regulations are raising costs for regional artisans, accelerating their collaborations with industrial co-packers.

Asia-Pacific is the fastest-growing region in the muffins market, with an annual growth rate of 6.61%. China's bakery market is expected to reach USD 118.4 billion by 2029. However, its per-capita consumption remains just a tenth of France's, highlighting significant growth potential for muffins. Automation currently covers 30% of Chinese production lines, with projections indicating an increase to 35% by 2026. In Japan, CAINZ has cumulatively sold 28 million muffins by 2025, showcasing the scalability of specialty retail. India and Southeast Asia face challenges with cold-chain logistics, necessitating the adoption of shelf-stable or frozen products to drive growth. Meanwhile, mature markets like Australia and South Korea are focusing on gluten-free and protein-rich offerings to sustain market value.

North America remains an important innovation hub for the muffins market, though nearing saturation, remains a hub for innovation. E-commerce deliveries in the U.S. are growing rapidly, with products like Premier Protein's 2026 cups targeting breakfast-skipping consumers. According to the Agriculture and Agri Food Canada data from 2025, retail sales of baked goods in the United States was USD 86,641.3 million[3]Source: Agriculture and Agri-Food Canada, "Bakery products in the United States", agriculture.canada.ca.Tim Hortons' upgraded English muffin highlights how brands are leveraging bakery items to boost beverage sales. In Canada, there is a strong focus on clean-label ingredients, supported by Puratos' R&D center in Montreal. In Mexico, urban markets are quickly adopting packaged muffins, although peso volatility creates pricing challenges. In South America, Brazil leads the region, benefiting from the expansion of modern retail. However, currency fluctuations continue to impact input costs. Argentina and Chile are willing to pay premiums for artisanal imports, while Peru and Colombia rely on convenience stores in secondary cities. Success in this region will depend on flexible production and a focus on localized flavors. The Middle East and Africa represent long-term opportunities; affluent consumers in the UAE and Saudi Arabia prefer premium imports, while South Africa and Nigeria face infrastructure limitations that hinder the development of cold-chain bakeries.

Competitive Landscape

The global muffins market is highly competitive; major multinational bakers and numerous regional players compete for dominance. Industry leaders such as Grupo Bimbo, The J.M. Smucker Company, ARYZTA, Britannia, Flowers Foods, and McKee Foods Corporation utilize product innovation, extensive distribution networks, and economies of scale to maintain their leadership. Companies in the muffins market frequently engage in intense competition by introducing new flavor variants, developing healthier formulations, and forming strategic partnerships. For example, in April 2025, Entenmann's Little Bites, a brand under Grupo Bimbo, expanded its offerings by adding Vanilla as a permanent flavor and launching Tropical Pineapple as a seasonal option, appealing to nostalgia and seasonal excitement. Additionally, in March 2025, Krusteaz targeted home bakers with the release of a Cheesecake Muffin Mix.

However, these major players face challenges from a wide range of smaller entities and the strong in-store bakery sections of retailers. These competitors focus on freshness, artisanal qualities, and local flavors. Furthermore, the intensified competition, along with a significant threat from substitutes, including other bakery items, snacks, and breakfast alternatives, emphasizes the industry's ongoing pursuit of differentiation.

Competition within the muffins market has intensified as functional bakery segment has also grown stronger. For instance, in 2024, Hostess introduced a protein-enhanced muffin line, which received positive consumer feedback. Additionally, Britannia's 2024 launch of artisanal muffins in urban India highlighted the growing demand for localized, premium products. In summary, while industry giants demonstrate their strength in product development and marketing, agile regional and niche brands continue to strengthen competition in the muffins market by catering to health, premium, and convenience-driven consumer segments.

Muffins Industry Leaders

-

ARYZTA AG

-

Grupo Bimbo SAB de CV

-

Flowers Foods Inc.

-

The J.M. Smucker Company

-

McKee Foods Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Nestlé Professional expanded its sweet bakery portfolio with the launch of a new range of branded muffins developed in collaboration with Cherrytree Bakery. The range includes three variants inspired by Nestlé’s popular confectionery brands, Aero, Rolo, and Munchies

- May 2026: Wonder Bread, a heritage bakery brand owned by Flowers Foods, announced its first-ever entry into the breakfast aisle with the nationwide launch of Wonder Bagels and Wonder English Muffins. The new breakfast portfolio includes Classic and Sourdough English Muffins.

- March 2025: Krusteaz, a baking brand with a 93-year legacy of innovation and culinary creativity, launched Cheesecake Muffin Mix. The 17-oz. boxed muffin mix, which yields a dozen standard muffins with a creamy cheesecake center, was launched at USD 3.99. Krusteaz Cheesecake Muffin Mix was made available at Kroger and Meijer.

- February 2025: In celebration of World Muffin Day, Europastry and Nestlé Professional introduced the Muffin Lion, combining tulip-style muffin dough with Lion chocolate‑caramel biscuit filling. The launched products were made available in foodservice (bulk) and retail 2‑packs.

Global Muffins Market Report Scope

| Traditional |

| Filled |

| Artisanal |

| Other Types |

| Conventional |

| Gluten-free |

| Vegan |

| low/no-Sugar |

| Fruit Based |

| Chocolate Based |

| Savory |

| Others |

| Foodservice | |

| Retail | Supermarket/Hypermarket |

| Convenience Stores | |

| Online Stores | |

| Other Retail Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type | Traditional | |

| Filled | ||

| Artisanal | ||

| Other Types | ||

| By Category | Conventional | |

| Gluten-free | ||

| Vegan | ||

| low/no-Sugar | ||

| By Variant | Fruit Based | |

| Chocolate Based | ||

| Savory | ||

| Others | ||

| By Distribution Channels | Foodservice | |

| Retail | Supermarket/Hypermarket | |

| Convenience Stores | ||

| Online Stores | ||

| Other Retail Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will global muffin sales be by 2031?

The muffins market size is forecast to reach USD 12.86 billion by 2031, expanding at a 5.15% CAGR from 2026.

Which region shows the strongest growth outlook?

Asia-Pacific leads with a projected 6.61% CAGR as Western-style snacking penetrates emerging urban centers.

What product formats are growing fastest?

Filled muffins are rising 6.53% a year, driven by indulgent centers such as caramel and ganache.

How are health trends influencing formulations?

Gluten-free lines are advancing 6.67% annually, while enzymatic flours and protein fortification cut sugar and boost nutrition.

Page last updated on: