Pancake Mixes Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

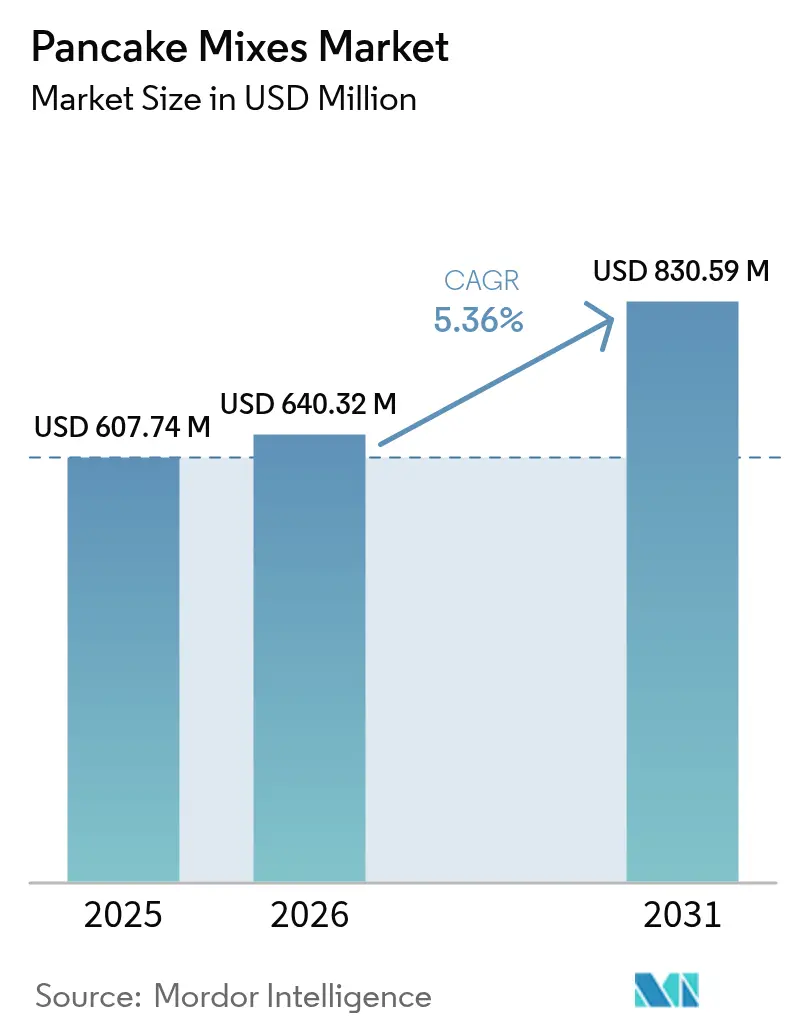

| Market Size (2026) | USD 640.32 Million |

| Market Size (2031) | USD 830.59 Million |

| Growth Rate (2026 - 2031) | 5.36% CAGR |

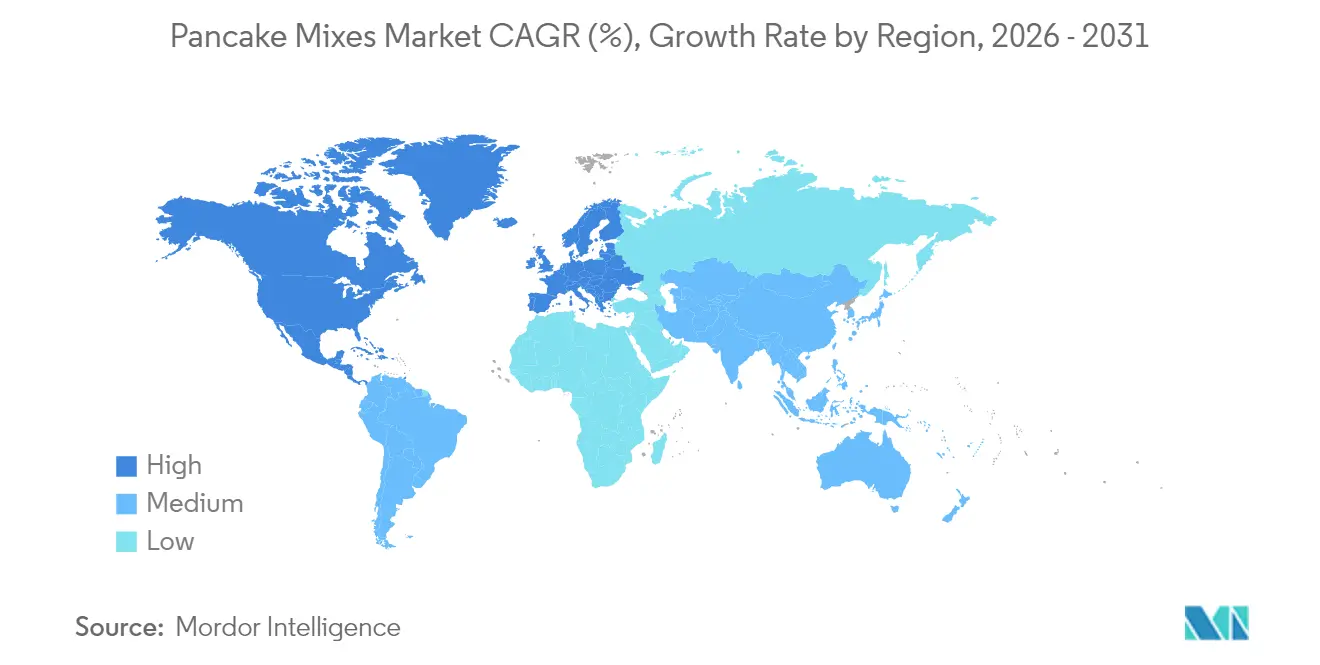

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

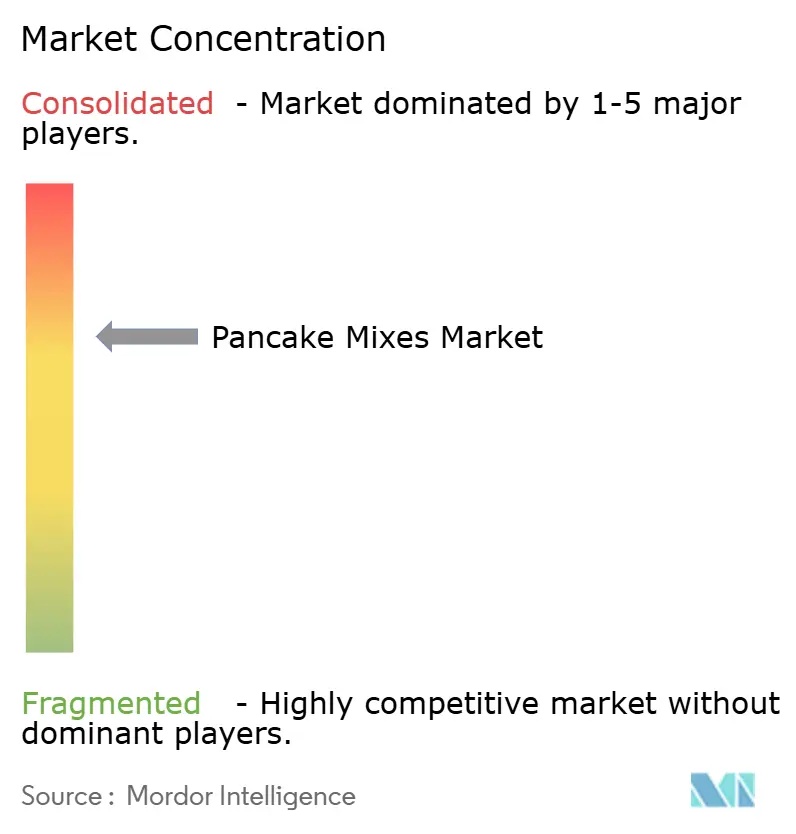

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Pancake Mixes Market Analysis by Mordor Intelligence

pancake mix market size in 2026 is estimated at USD 640.32 million, growing from 2025 value of USD 607.74 million with 2031 projections showing USD 830.59 million, growing at 5.36% CAGR over 2026-2031. The market's growth is fueled by a consistent consumer demand for convenient yet nutritious breakfasts, the rising trend of fitness-oriented diets, and dynamic product launches that seamlessly blend plant-based proteins with traditional flavors. Additionally, a survey from Japan's Ministry of Agriculture, Forestry, and Fisheries, conducted in November 2024, highlighted that over 78% of Japanese consumers partake in breakfast daily[1]Source: Japan's Ministry of Agriculture, Forestry, and Fisheries, "Survey report on dietary education 2025", maff.go.jp. Manufacturers are not only adopting regenerative agriculture practices but are also utilizing recyclable pouches, aligning with environmental expectations and aiming for premium shelf placements. The swift rise of online grocery shopping has democratized the market, allowing niche brands to enter more easily, thereby heightening competition and broadening consumer choices. While North American giants are expanding their global footprint, local innovators in the Asia-Pacific region are customizing flavors and portion sizes to resonate with regional tastes, altering the competitive landscape.

Key Report Takeaways

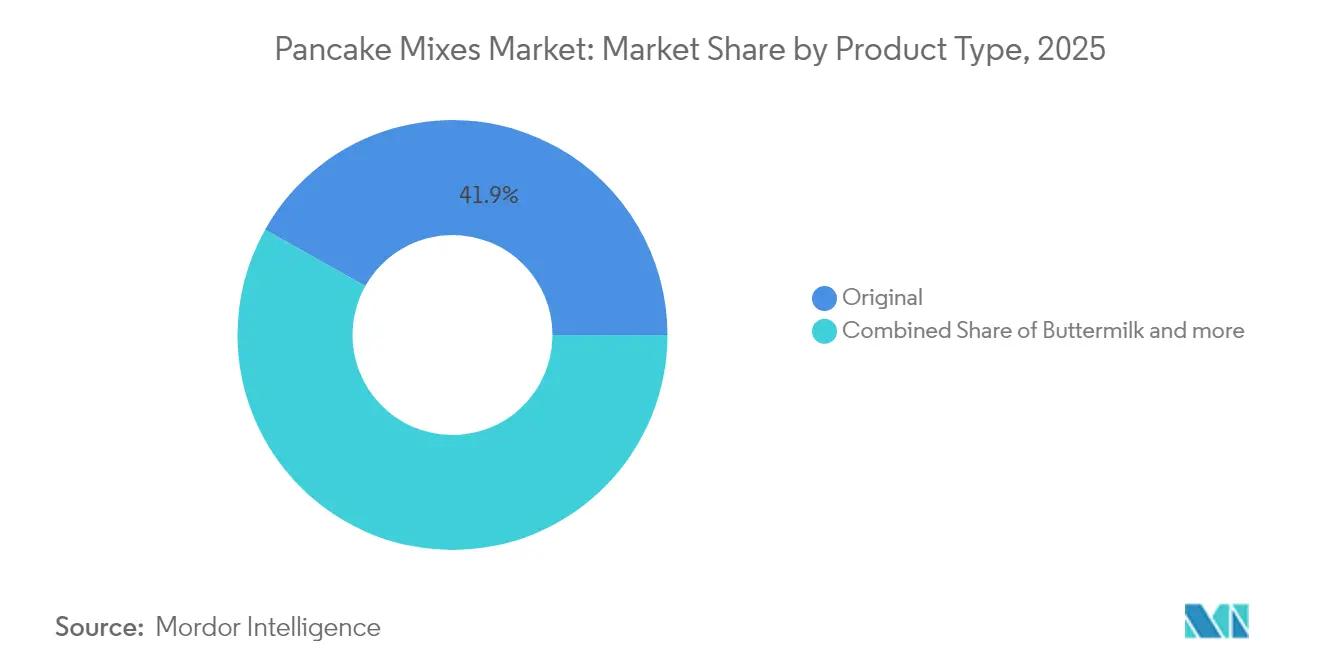

- By product type, original mixes led with 41.85% of the pancake mix market share in 2025, while buttermilk variants are projected to grow at a 5.67% CAGR through 2031.

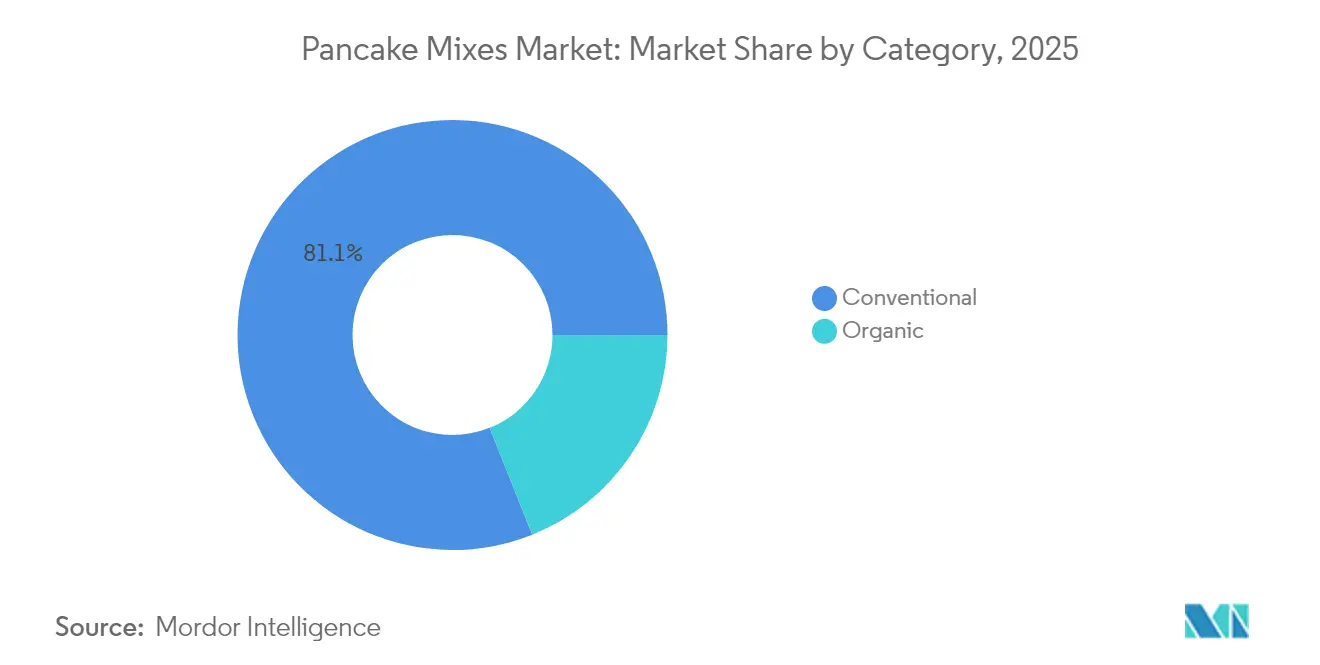

- By category, conventional offerings accounted for 81.05% of the pancake mix market size in 2025, and organic and health-labeled products are expanding at a 6.31% CAGR to 2031.

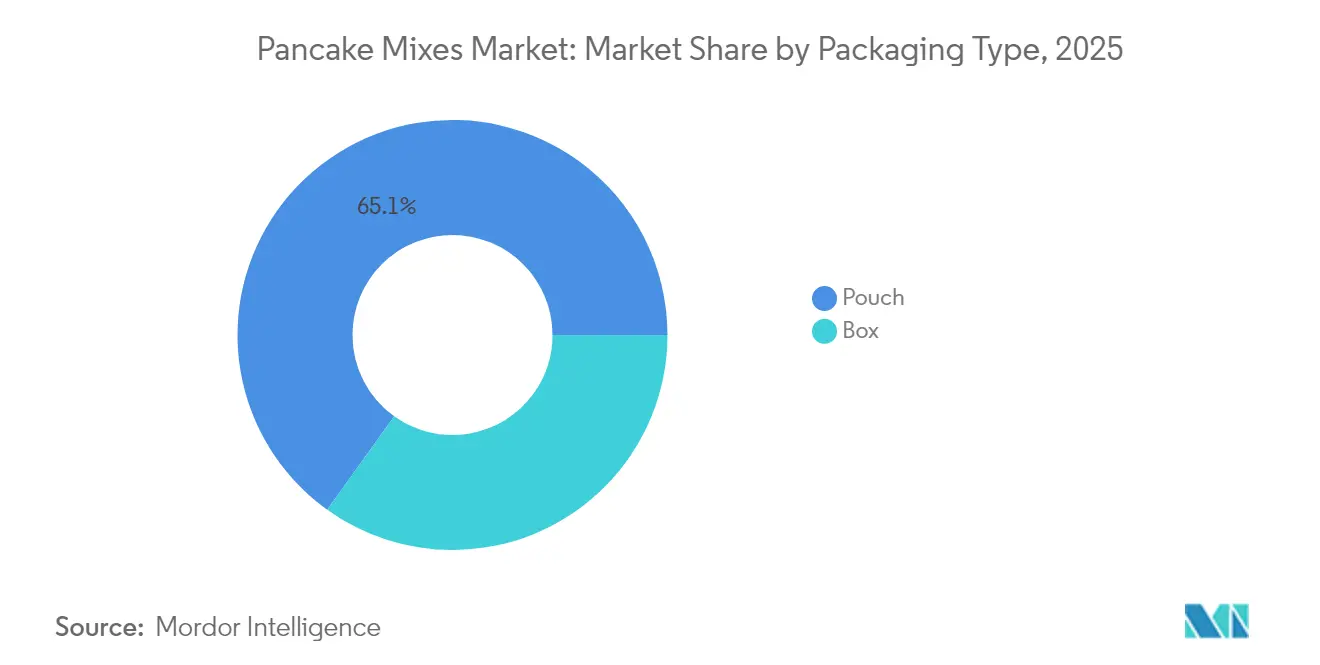

- By packaging, pouches captured 65.10% share of the pancake mix market in 2025, and box formats are advancing at a 5.79% CAGR over the same horizon.

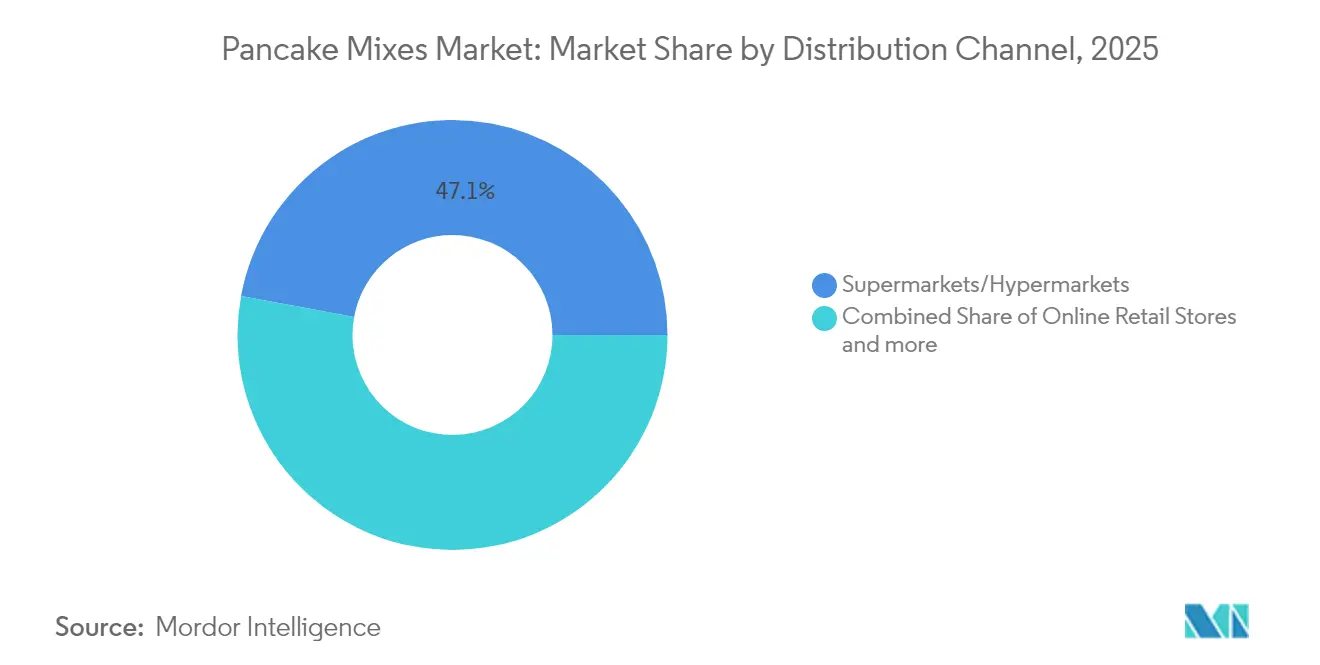

- By distribution channel, supermarkets and hypermarkets held 47.10% share of the pancake mix market in 2025, whereas online retail is registering the fastest 6.14% CAGR to 2031.

- By geography, North America commanded a 41.95% share of the pancake mix market in 2025, and Asia-Pacific is on track for the highest 5.44% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pancake Mixes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased health and wellness consciousness | +1.2% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Product innovation and variety | +0.9% | Global, led by North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Growth of home cooking and baking | +0.8% | Global, accelerated post-pandemic | Short term (≤ 2 years) |

| Sustainability trends in packaging and sourcing | +0.6% | Europe and North America primary, spreading globally | Long term (≥ 4 years) |

| Technological advancements in food processing | +0.4% | Developed markets first, scaling to emerging regions | Medium term (2-4 years) |

| Westernization of diets in emerging markets | +0.7% | Asia-Pacific core, spill-over to Latin America and the Middle East, and America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increased Health and Wellness Consciousness

Driven by health-conscious choices, consumers are increasingly turning to protein-enriched and gluten-free pancake mix alternatives. This surge in demand aligns with projections of growth in the global gluten-free market. However, this trend isn't solely about dietary restrictions. It's part of a broader wellness movement, where consumers are on the lookout for products boasting enhanced nutritional profiles. These include features like plant-based proteins, ancient grains, and lower sugar content. The pancake mix segment is reaping the rewards of this trend, especially with the rise of fitness culture and the growing trend of meal replacements. Today, many see breakfast as a chance for functional nutrition, not just a meal. Supporting this trend, the International Health, Racquet and Sportsclub Association reported that in 2024, the U.S. boasted approximately 77 million members in fitness centers and health clubs[2]Source: Health, Racquet & Sportsclub Association, "Number of memberships at fitness centers and health clubs in the United States", healthandfitness.org. Furthermore, regulatory frameworks, such as FDA guidelines on protein content labeling, empower manufacturers. These regulations not only clarify how to communicate nutritional benefits but also foster consumer trust through transparent ingredient disclosure.

Product Innovation and Variety

Pancake mix manufacturers are rapidly innovating, introducing unique ingredients like einkorn wheat, buckwheat flour, and soy protein concentrates to stand out and command premium prices. A notable example is Betty Crocker's Cinnamon Toast Crunch pancake mix, showcasing how brand collaborations can craft distinct flavors appealing to targeted consumers. Leveraging technology, manufacturers are precisely formulating gluten-free options with rice flour and xanthan gum. Meanwhile, sustainable innovations, such as recyclable pouches, tackle environmental issues while ensuring product freshness. In saturated markets, where traditional products risk becoming commodities, these innovations emerge as vital competitive advantages.

Growth of Home Cooking and Baking

Post-pandemic, home cooking trends have reshaped consumer behavior. Notably, a surge in baking activities has led to a lasting demand for convenient mix solutions. The trend of premiumization in home baking has evolved. It's no longer just about basic functionality; consumers now desire an experiential touch. They aim for restaurant-quality results, turning to enhanced mix formulations and advanced preparation techniques. In September 2024, Krusteaz introduced refrigerated "Pour and Bake" batters at major retailers. These convenience formats seamlessly blend scratch cooking with instant preparation. They appeal to time-pressed consumers who prioritize both convenience and quality. This shift in behavior presents manufacturers with a unique opportunity. They can craft hybrid products that cater to the dual demands of convenience and culinary ambition. This is especially pertinent in urban markets, where limited kitchen space drives a preference for compact and versatile solutions.

Sustainability Trends in Packaging and Sourcing

Companies like Simple Mills are leading the charge in reshaping supply chain strategies through partnerships in regenerative agriculture. These initiatives not only bolster demand for biodiverse crops but also champion soil health. In response to consumer preferences and looming regulatory mandates in major markets, there's a pronounced shift towards packaging innovations that prioritize recyclable materials and curtail plastic usage. By weaving sustainability metrics into product development, manufacturers are not just fostering brand loyalty among eco-conscious consumers but are also positioning themselves to command premium pricing. Governed by the USDA National Organic Program standards, organic certification requirements offer a structured approach to sustainable sourcing. However, they also erect barriers, safeguarding established organic players from conventional competitors eager to carve out their market share.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Alternative breakfast products | -0.8% | Global, strongest in urban markets | Medium term (2-4 years) |

| Refined ingredients and additives | -0.6% | Developed markets primarily | Short term (≤ 2 years) |

| Homemade and artisanal pancakes | -0.7% | Global, strongest in urban markets | Short term (2-3 years) |

| Varying regulations and market maturity | -0.4% | Developed markets primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Alternative Breakfast Products

Alternative breakfast solutions, such as protein bars, ready-to-drink smoothies, and instant oatmeal, are directly competing with pancake mixes by offering similar convenience and enhanced portability. The protein bar market, fueled by on-the-go consumption and a rising fitness culture, poses a significant challenge to the positioning of protein pancake mixes. Health-conscious consumers, who once leaned towards traditional meals, are now prioritizing convenience. For instance, the Good Food Institute reported that in the 52 weeks ending December 2024, U.S. sales of plant-based protein bars surpassed USD 290 million, up from USD 286 million the previous year. Meanwhile, the rise of meal replacement shakes and breakfast smoothie bowls offers time-strapped urban professionals, a prime demographic for premium pancake mixes, nutritionally similar options without the prep time. As breakfast categories become more fragmented, competition for consumer attention and spending intensifies. This landscape compels pancake mix manufacturers to define unique value propositions that extend beyond mere nutrition and convenience.

Refined Ingredients and Additives

As consumers grow wary of processed foods and artificial additives, conventional pancake mixes, especially those with preservatives and artificial flavors, face mounting challenges. The clean label movement, which champions recognizable ingredients and minimal processing, stands in stark contrast to traditional manufacturing methods that prioritize shelf stability and uniform texture. Data from the International Food Information Council reveals that in 2023, about 29% of U.S. consumers regularly chose food and beverages for their "clean ingredients" labels[3]Source: International Food Information Council, "Food & Health Survey 2023", ific.org. Heightened regulatory scrutiny, especially from the FDA on artificial colors and preservatives, casts a shadow of uncertainty over ingredient approvals and labeling mandates. Such scrutiny could lead to expensive reformulation endeavors. This evolving landscape poses a significant challenge for mass-market brands, which often compete on price. Clean-label alternatives, demanding premium ingredients and specialized processing, not only inflate production costs but may also compromise shelf life and distribution efficiency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Buttermilk Variants Drive Innovation

In 2025, original pancake mixes command a dominant 41.85% market share, underscoring their widespread appeal and consumer familiarity across various demographics. Yet, buttermilk variants are on a rapid ascent, boasting a robust 5.67% CAGR projected through 2031. This surge is attributed to their perceived authenticity and superior taste, allowing them to adopt premium pricing strategies. Tied to traditional Southern cooking and an artisanal touch, the buttermilk segment positions itself as a refined alternative to standard offerings. Meanwhile, fruit-based mixes are carving out a niche, especially among health-conscious consumers who prioritize natural flavors over artificial additives. Buttermilk variants are particularly popular because they naturally produce a rich flavor and a desired fluffy texture due to the reaction between the lactic acid and baking soda. The market has witnessed several significant developments, driven by growing demand. For instance, in June 2024, Premier Nutrition launched a new line of high-protein pancake and waffle mixes to cater to health-focused consumers, while in May 2024, Nella's introduced a Cassava Pancake and Waffle Mix, a gluten-free alternative, in response to growing demand for diverse and dietary-specific products. Additionally, in May 2024, King Arthur Baking Company acquired Plymouth Pancake Company to expand its product portfolio. In March 2024, Quaker Oats partnered with a food technology company to develop plant-based protein pancake mixes.

Product innovation is increasingly leaning towards functional ingredients. For instance, protein-enhanced variants are now integrating whey isolates and plant-based proteins, targeting the fitness-conscious demographic. Furthermore, ancient grain formulations, featuring einkorn wheat and buckwheat flour, not only boost nutritional value but also emphasize clean-label appeal, setting them apart in the premium market. On the manufacturing front, technological advancements are ensuring consistent texture profiles, even with diverse ingredient bases. This progress addresses past challenges, especially with gluten-free and protein-enriched formulations that struggled with density and mixing.

By Category: Organic Segment Accelerates Despite Conventional Dominance

In 2025, conventional pancake mixes dominate the market, holding an 81.05% share, thanks to their established distribution networks, competitive pricing, and widespread acceptance among consumers of all income levels. Yet, even with this stronghold, organic and health-focused variants are on the rise, boasting a notable 6.31% CAGR growth projected through 2031. This surge underscores the success of their premium positioning and a growing consumer readiness to invest in perceived quality. Notably, the organic segment enjoys a distinct advantage: USDA certification frameworks not only set clear differentiation standards but also pose entry challenges for traditional manufacturers. Government and association sources are also influential; the U.S. Food and Drug Administration (FDA) approved a new natural preservative in April 2025, enabling manufacturers to achieve longer shelf life for clean-label products without artificial additives. Additionally, in India, initiatives like the National Programme for Organic Production (NPOP) and the Jaivik Bharat initiative provide a framework for certification and labelling, building consumer trust and promoting the domestic and international organic market.

Health-focused variants, including gluten-free, non-GMO, and protein-enhanced options, cater to specific dietary needs and command premium prices. Moreover, the blending of health and sustainability messages amplifies their appeal, especially among affluent consumers who prioritize alignment with their personal values and lifestyle. Retailers, spearheaded by Walmart's Great Value brand, are pushing private labels into the organic arena. This move not only broadens access to health-oriented products but also heightens price competition with established brands.

By Packaging Type: Pouch Dominance Faces Box Format Revival

In 2025, pouch packaging commands a dominant 65.10% market share, thanks to its ability to retain freshness, optimize storage, and cater to consumers' preference for resealable formats. The demand for pouch-packed pancake mixes is growing globally primarily due to the increasing consumer focus on convenience, portability, and product freshness, which aligns with modern, fast-paced lifestyles. This packaging innovation directly addresses the needs of busy households and on-the-go consumers who seek quick and easy meal solutions without compromising quality or contributing to food waste. Furthermore, a growing interest in sustainability is driving consumer preference for pouches, which typically use less material and have a lower carbon footprint during transportation compared to heavier options such as glass or cardboard. In line with this, players are also offering a variety of product types, which support the market's growth. For instance, in September 2025, the brand Krusteaz expanded its offerings with a line of refrigerated "Pour & Bake" batters, likely utilizing innovative, easy-to-use spout pouches, which further simplify the preparation process for maximum convenience.

Meanwhile, box packaging surprises many with a robust 5.79% CAGR growth projected through 2031. This growth is bolstered by a strategic emphasis on sustainability and associations with premium brands, which adeptly use traditional packaging cues to convey messages of quality and authenticity. Notably, the box format finds favor in gift-giving scenarios and specialty retail outlets, where an appealing shelf presentation can sway purchase decisions. Today's packaging innovations go beyond merely choosing a format. They delve into sustainable materials and added functionalities, such as portion control and recipe integration, enhancing consumer value beyond mere product protection. Compliance with regulations, from FDA nutrition labeling to state-specific packaging waste laws, not only shapes material and design choices but also opens avenues for brands to differentiate themselves through a strong environmental stance. A noteworthy trend is the rise of hybrid packaging solutions, merging the convenience of pouches with the aesthetic appeal of boxes, catering to diverse consumer preferences in a single product.

By Distribution Channel: Online Retail Disrupts Traditional Patterns

In 2025, supermarkets and hypermarkets command a 47.10% share of the market, skillfully tapping into established consumer shopping habits. They adeptly position pancake mixes alongside other breakfast staples, capitalizing on cross-merchandising opportunities. Meanwhile, online retail channels are on a remarkable trajectory, boasting a 6.14% CAGR growth rate projected through 2031. This surge is largely attributed to the rise of subscription services, the allure of bulk purchasing, and access to specialty products, advantages that traditional retail struggles to match. Additionally, the growth in this channel is driven by the immediate availability of a wide assortment of products, allowing consumers to make quick, in-person purchasing decisions alongside other grocery staples. In-store sampling and cross-merchandising opportunities further enhance customer engagement.

Notably, the online realm is a boon for specialty and premium brands, enabling them to establish direct connections with consumers and secure more favorable profit margins. This channel is particularly beneficial for niche, premium, and artisanal brands (e.g., gluten-free, organic, plant-based) that can reach a global audience without relying on extensive physical retail footprints. Convenience stores and specialist retailers carve out unique niches in the market. Convenience formats cater to impulse buys and quick, on-the-go consumption. In contrast, specialty retailers emphasize premium and artisanal offerings, necessitating informed selling and carefully curated selections. As distribution channels evolve, mirroring the broader retail landscape, brands that thrive are those adopting omnichannel strategies. These strategies ensure optimal product positioning and pricing across a myriad of consumer touchpoints.

Geography Analysis

In 2025, North America dominated the protein pancake mix market, claiming a 41.95% share. This stronghold is bolstered by a deep-rooted breakfast culture and extensive retail presence. With high disposable incomes, consumers are increasingly opting for protein-enriched and gluten-free variants. Additionally, established diner chains play a pivotal role in driving foodservice volume. Regional manufacturers benefit from advanced cold-chain logistics, allowing them to introduce refrigerated batters seamlessly.

Asia-Pacific is on a rapid ascent, projected to grow at a 5.44% CAGR through 2031. In China and Southeast Asia, rising urban incomes and the spread of western-style cafés are making pancake breakfasts a norm. However, localizing flavors, like incorporating matcha or red-bean mixes, is crucial. Moreover, domestic e-commerce giants are streamlining distribution for these niche imports, further boosting their adoption.

Europe is witnessing steady growth, driven by consumers' focus on organic and sustainable products. Strict regulations on packaging and ingredients benefit brands that can showcase low-carbon footprints and clean labels. Germany's vast grocery market, coupled with a surge in online shopping, offers a significant platform for premium products. Meanwhile, Latin America and the Middle East are emerging hotspots. Here, social media is igniting interest in protein-rich breakfasts, but brands must navigate price sensitivities with value-engineered offerings. This geographic diversification not only lessens reliance on the mature North American market but also positions brands to tap into the burgeoning global demand.

Regulatory Landscape

In the United States, pancake mixes are governed by FDA food safety and labeling requirements under FSMA and 21 CFR nutrition labeling rules. The FSMA Food Traceability Rule (21 CFR Part 1, Subpart S) is a notable compliance milestone for packaged food supply chains, with a compliance date currently proposed for July 20, 2028. This reinforces investments in digital recordkeeping and supplier documentation even for shelf-stable mixes. Labeling execution also follows established FDA frameworks, including serving size and Nutrition Facts requirements (21 CFR 101.9). Key grain inputs (cereal flours) used in mixes align with standards of identity and labeling provisions in 21 CFR Part 137, shaping ingredient declarations and formulation choices, including optional flour treatment agent disclosures where applicable.

In the European Union, rules governing food additives and their specifications are central for pancake mixes that use hydrocolloids, stabilizers, and related texture systems. Regulation (EU) 2026/196, published on January 28, 2026, amended additive use specifications for selected substances, including carrageenan, gums, and pectins, and set transition provisions. It includes an August 18, 2026 cutoff for goods newly placed on the market under prior specifications, with sell-through allowed to minimum durability or use-by. EFSA also updated its guidance for food additive applications submitted under Regulation (EC) No 1333/2008, taking effect on July 20, 2026, which raises documentation expectations for suppliers and brand owners planning reformulations or new additive-based claims in Europe.

Competitive Landscape

The global pancake mixes market is moderately concentrated, with key players focusing on product innovation, health-oriented offerings, and strategic distribution to strengthen their market share. Leading companies, such as PepsiCo (Quaker Oats), General Mills (Betty Crocker), and Continental Mills (Krusteaz), capitalize on brand recognition and extensive distribution networks to maintain their market dominance. Meanwhile, specialty brands such as Bob's Red Mill Natural Foods, King Arthur Baking Company, and Birch Benders are establishing significant market positions in niche segments. The market's competitive dynamics are driven by increasing demand for convenient breakfast solutions, consumer preferences for fortified or dietary-specific products (e.g., gluten-free, protein-rich, organic), and advancements in processing and packaging technologies.

Brands are actively expanding into niche markets through strategic initiatives. For instance, Premier Nutrition launched a high-protein pancake mix line in June 2024, while King Arthur Baking Company acquired Plymouth Pancake Company in May 2024 to enhance its specialty product portfolio. Similarly, Nella introduced a gluten-free cassava mix in May 2024, catering to the growing demand for dietary-specific options. An omnichannel retail strategy is becoming increasingly critical, with companies leveraging both traditional supermarkets and rapidly growing online platforms to maximize consumer reach and convenience.

The competitive landscape is further intensified by private label brands offering cost-effective alternatives, compelling national brands to continuously innovate and invest in marketing to strengthen brand equity. Smaller, innovative players are also making their mark by utilizing targeted digital marketing and specialized product formulations to directly engage with consumers. This dynamic environment underscores the importance of innovation and strategic positioning for companies aiming to thrive in the pancake mixes market.

Pancake Mixes Industry Leaders

-

Continental Mills, Inc.

-

General Mills

-

PepsiCo Inc

-

Hometown Food Company

-

Kodiak Cakes

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear whitespace is forming around functional and free-from reformulation that maintains taste and texture while meeting stricter ingredient scrutiny. Product work in 2026 points to practical differentiation paths for pancake mix brands: DA-PhilRice and DSFT-CLSU developed a gluten-free pancake premix using okara (soybean pulp) and fermented pigmented rice bran to raise protein and fiber content. The approach signals how brands can use upcycled or by-product ingredients while keeping nutrition-led positioning. Academic research published in 2026 on microencapsulation approaches, including zein-pectin microparticles to deliver plant-derived extracts in vegan and gluten-free pancakes, also suggests an active innovation pipeline focused on improving sensory performance and stability in specialty mixes.

Brand activity further supports opportunities in protein-forward and flavor-led line extensions sold through online and specialty channels. In April 2026, Project #1 Nutrition launched a Blueberry Protein Pancake and Waffle Mix with freeze-dried blueberry inclusions, reflecting continued momentum behind protein-enhanced formats that add recognizable ingredients rather than relying only on sweeteners or flavors. At the same time, tightening EU additive specifications under Regulation (EU) 2026/196 and updated EFSA guidance effective July 2026 create operational pressure for suppliers and mix manufacturers to simplify ingredient decks and standardize compliant stabilizer systems for cross-border SKUs, which can support faster international assortment expansion when paired with omnichannel distribution.

Recent Industry Developments

- May 2026: General Mills launched Bisquick Cinnamon Toast Crunch pancake and baking mix, extending a well-known cereal brand into the baking and breakfast-mix aisle. The launch strengthens branded flavor collaboration as a lever to defend shelf space and drive premium mix trade-up versus standard original and buttermilk offerings.

- May 2026: Hometown Food Company issued an allergy alert and initiated a limited, voluntary recall for a single lot code of Birch Benders 12 oz Sweet Potato Pancake Mix due to undeclared egg. The incident underscores the category need for stronger allergen controls and accurate label management as brands broaden into plant-based and free-from positioning.

- September 2025: Krusteaz expanded its offerings with refrigerated "Pour and Bake" batters across major retailers, using a ready-to-use format that removes measuring and mixing steps. The launch broadened the competitive set beyond shelf-stable mixes and elevated convenience as a key differentiator for at-home breakfast and baking occasions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The pancake mixes market covers packaged dry and ready-to-prepare pancake mix products sold through retail and foodservice channels, measured in value terms at manufacturer or brand level before consumer cooking and preparation.

Scope exclusions: Excludes plain flour and baking staples sold without a pancake mix claim, and it also excludes ready-to-eat cooked pancakes sold as refrigerated or frozen finished foods.

Segmentation Overview

-

By Product Type

- Original

- Buttermilk

- Other Fruit Based Mixes

-

By Category

- Conventional

- Organic/Free-from/Healthy labeled

-

By Packaging Type

- Box

- Pouch

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Specialist Retailers

- Online Retail

- Other Distribution Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Rest of South America

-

Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Sweden

- Belgium

- Poland

- Netherlands

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Thailand

- Singapore

- Indonesia

- South Korea

- Australia

- New Zealand

- Rest of Asia-Pacific

-

Middle East and Africa

- United Arab Emirates

- South Africa

- Saudi Arabia

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the demand pool and the selling environment for packaged pancake mixes across major regions, and then to set realistic guardrails for the model. We leaned on public, non-paywalled references such as USDA and other national agriculture statistics, US Census and other official household expenditure datasets, UN Comtrade trade flows for relevant food preparations, Codex and national food labeling rules, and peer-reviewed food science and nutrition journals for ingredient and fortification trends.

To translate these signals into a market model, company annual reports, investor presentations, and reputed business press were reviewed for category commentary, channel mix, and pricing actions. We also used paid subscriptions for company financials and intelligence, plus shipment-level import and export tracking where it helped validate cross-border supply. The sources listed here are illustrative only, and many other public and paid references were also checked for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on checking what is actually counted as pancake mix at shelf and in foodservice purchasing, then stress-testing price and volume assumptions region by region. We spoke with mix manufacturers, ingredient suppliers, distributors, retailers, and foodservice buyers across APAC, EMEA, and the Americas, which helped clarify pack-size splits, private label presence, and online penetration, so the final numbers stayed practical.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 18% | APAC: 39% |

| Mid tier: 45% | Functional/Unit leaders: 22% | EMEA: 36% |

| Smaller Players: 18% | Managers: 60% | Americas: 25% |

Market-Sizing & Forecasting

Sizing starts with a top-down demand reconstruction where household breakfast-at-home frequency, relevant packaged food spend, and modern retail plus e-commerce reach are used to build a realistic consumption pool for mixes. Those totals are then cross-checked with selective bottom-up approximations like sampled brand and private label shelf pricing, pack-size weighted ASPs, and channel checks on sales velocity in key countries, which helps correct for underreported channels or unusually high promo intensity.

Inputs that were watched closely include mix price per pound or kilogram, share of flavored and better-for-you mixes, packaging shift from boxes to pouches, online grocery penetration, and foodservice menu adoption for breakfast and brunch. For forecasting, scenario analysis was used, where growth drivers and constraints from interviews were translated into yearly assumptions on price progression, distribution gains, and trade-down or trade-up behavior. When country data was thin, gaps were handled by using proxy indicators from similar markets, then rebalancing shares so regional totals stayed consistent with the independent checks.

Data Validation & Update Cycle

Outputs were validated through several checks so the numbers did not rely on one data stream. We compared model results against independent signals such as trade movements, channel expansion patterns, and pricing trends, and then reviewed any large variances at the country and region level before sign-off.

Anomalies triggered follow-ups with interviewees and a second pass on assumptions like pack-size mix and promotion intensity. The report is refreshed annually, and interim updates are made when material events occur, such as major labeling changes or sharp input-cost swings. Before delivery, a final analyst review is done to ensure the latest information has been reflected in the sizing and forecast.

Mordor Intelligence's Pancake Mixes Market Sizing Compared With Other Published Estimates

Published market sizes for pancake mixes can look far apart even when everyone is describing the same breakfast occasion, and it usually comes back to scope and measurement choices. Differences in whether foodservice is counted, how private label is treated, and what is assumed for price per unit often explain most of the spread.

Ready-to-eat frozen pancakes sit outside Mordor Intelligence's scope, which keeps the model tied to packaged mixes rather than finished breakfast foods, and some published figures appear to blend these adjacent categories or use broader "batter and mix" definitions. Gaps also show up when a forecast assumes a fast premiumization curve without validating promo depth, or when currency conversion timing is not aligned to the stated year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 607.74 M (2025) | |

| Industry Publisher A | USD 566.47 M (2024) | Uses an earlier base year and appears to lean more on reported value by channel, which can undercount smaller formats and private label in markets where disclosure is limited. |

| Research House B | USD 6.36 B (2024) | Figure looks inflated relative to mix-only sizing, likely due to a broader definition that can bundle other breakfast mixes or adjacent prepared foods, plus different unit and currency normalization choices. |

The table shows that most variation is driven by what is included as a "mix" versus adjacent breakfast products, and by how price and channel coverage are normalized across countries. By keeping the inputs traceable to pack-level pricing, channel availability, and realistic consumption indicators, we arrive at a balanced number that can be repeated and updated without hidden assumptions.

Key Questions Answered in the Report

What is the current value of the protein pancake mix market?

The protein pancake mix market size is USD 640.32 million in 2026 and is projected to reach USD 830.59 million by 2031.

Which region leads sales of protein pancake mixes?

North America holds a 41.95% share of global revenue due to an entrenched breakfast culture and broad retail coverage.

Which product type is growing fastest within protein pancake mixes?

Buttermilk variants are expanding at a 5.67% CAGR through 2031, outpacing other flavor formats.

How quickly is online retail growing for protein pancake mixes?

E-commerce sales are registering a 6.14% CAGR as consumers embrace subscription deliveries and specialty assortments.

What packaging trends are shaping the category?

Resealable pouches dominate, yet recyclable box formats are gaining momentum with a 5.79% CAGR because of sustainability appeal.

What factors most influence market growth?

Health-driven protein demand, flavor innovation, and sustainability initiatives collectively add 4.6 percentage points to forecast CAGR.

Page last updated on: