Biscuits Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Market Size (2026) | USD 142.05 Billion |

| Market Size (2031) | USD 181.83 Billion |

| Growth Rate (2026 - 2031) | 5.05% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Europe |

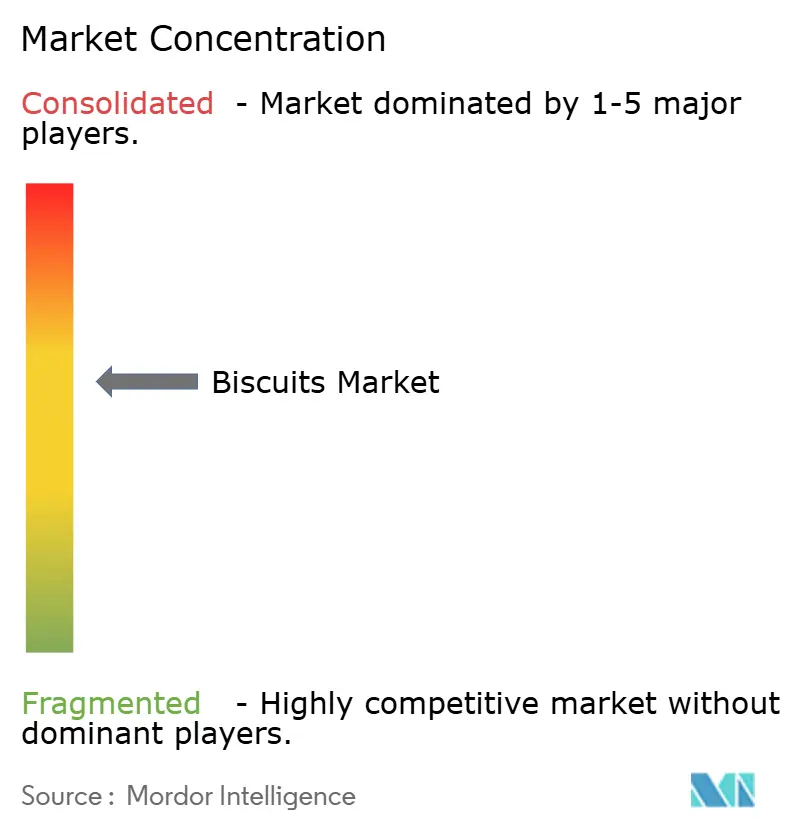

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Biscuits Market Analysis by Mordor Intelligence

The biscuit market size is expected to grow from USD 135.21 billion in 2025 to USD 142.05 billion in 2026 and is forecast to reach USD 181.83 billion by 2031 at 5.05% CAGR over 2026-2031. This growth stems from continuous household consumption patterns, expanding urban middle-class demographics, and established snacking behaviors. Manufacturers are reformulating their product lines to include reduced-sugar and fiber-enriched variants while maintaining their traditional indulgent offerings, addressing both health-conscious consumers and those seeking treats. E-commerce expansion has facilitated premium product distribution and direct-to-consumer channels, with single-serve packaging formats capturing the on-the-go consumption segment. Major manufacturers are fortifying their supply chains through strategic acquisitions and geographical expansion initiatives to mitigate raw material cost fluctuations.

Key Report Takeaways

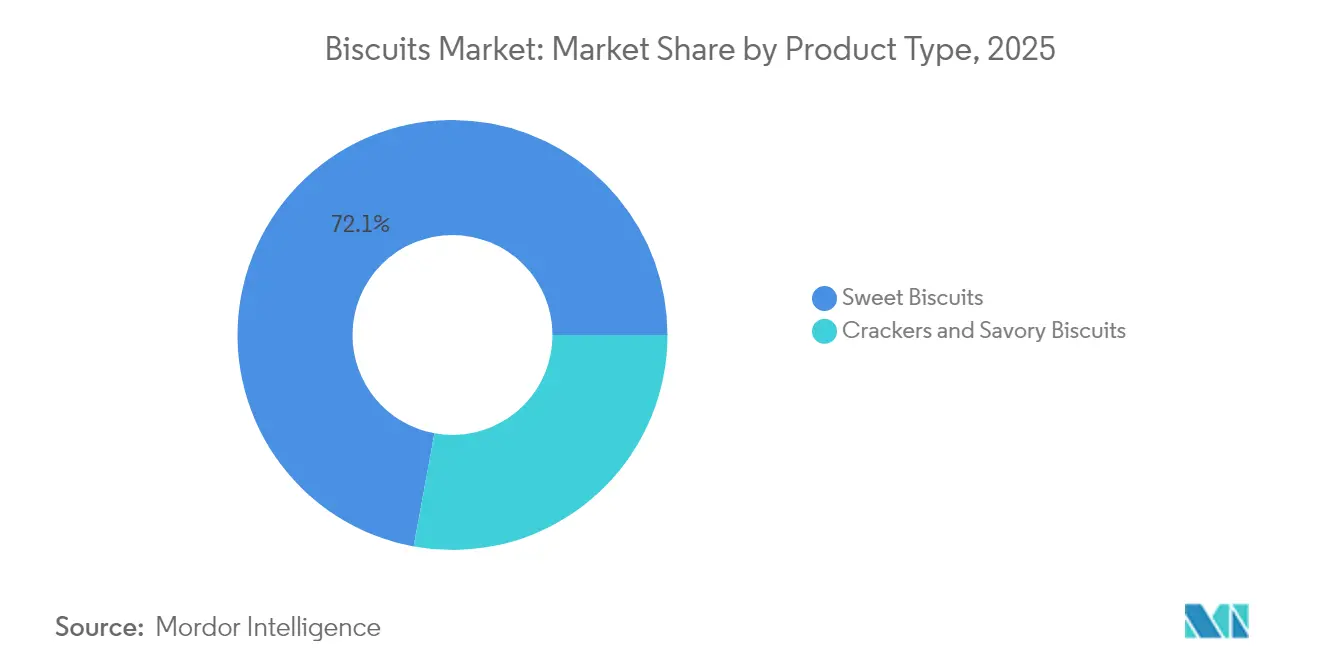

- By product type, sweet biscuits led with 72.11% revenue share in 2025; crackers and savory biscuits are projected to advance at a 6.21% CAGR through 2031.

- By packaging type, plastic packets and on-the-go pouches held 57.96% of the biscuit market share in 2025, while boxes are set to grow at 4.03% CAGR to 2031.

- By category, conventional wheat-based SKUs captured 84.74% of the biscuit market size in 2025; free-from options are expanding at 6.28% CAGR between 2026-2031.

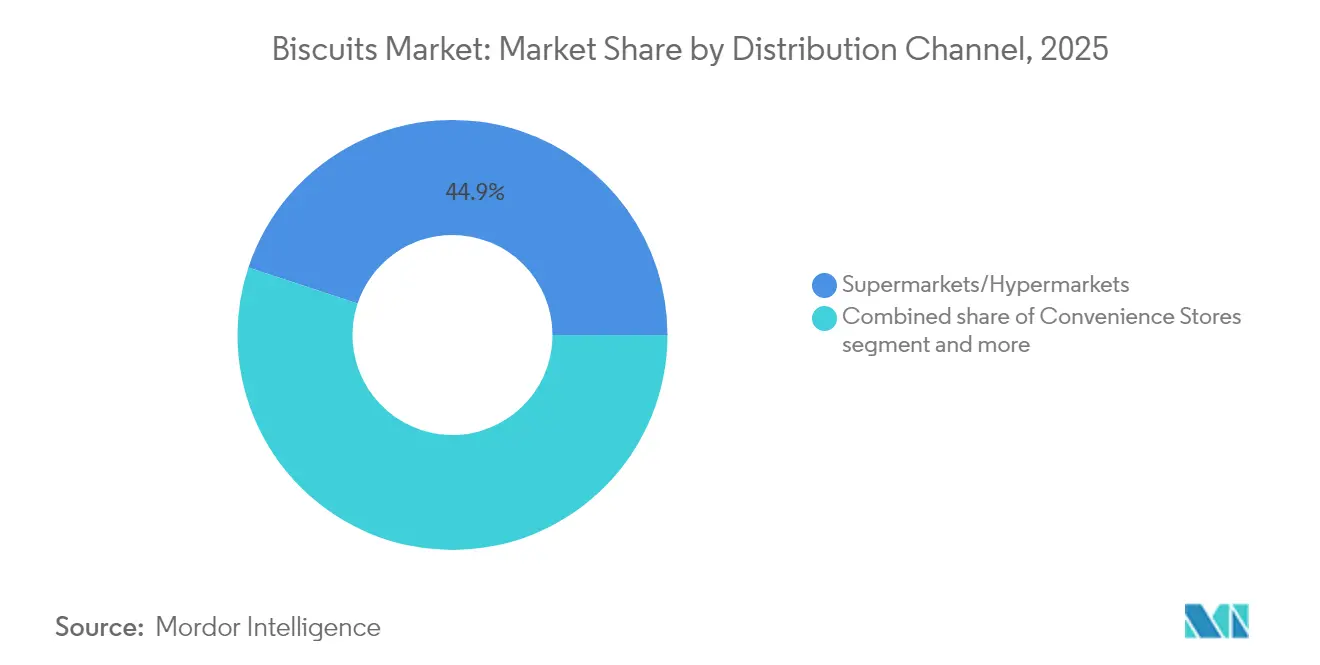

- By distribution channel, supermarkets and hypermarkets accounted for 44.92% of the biscuit market in 2025, whereas online retail is climbing at an 7.92% CAGR to 2031.

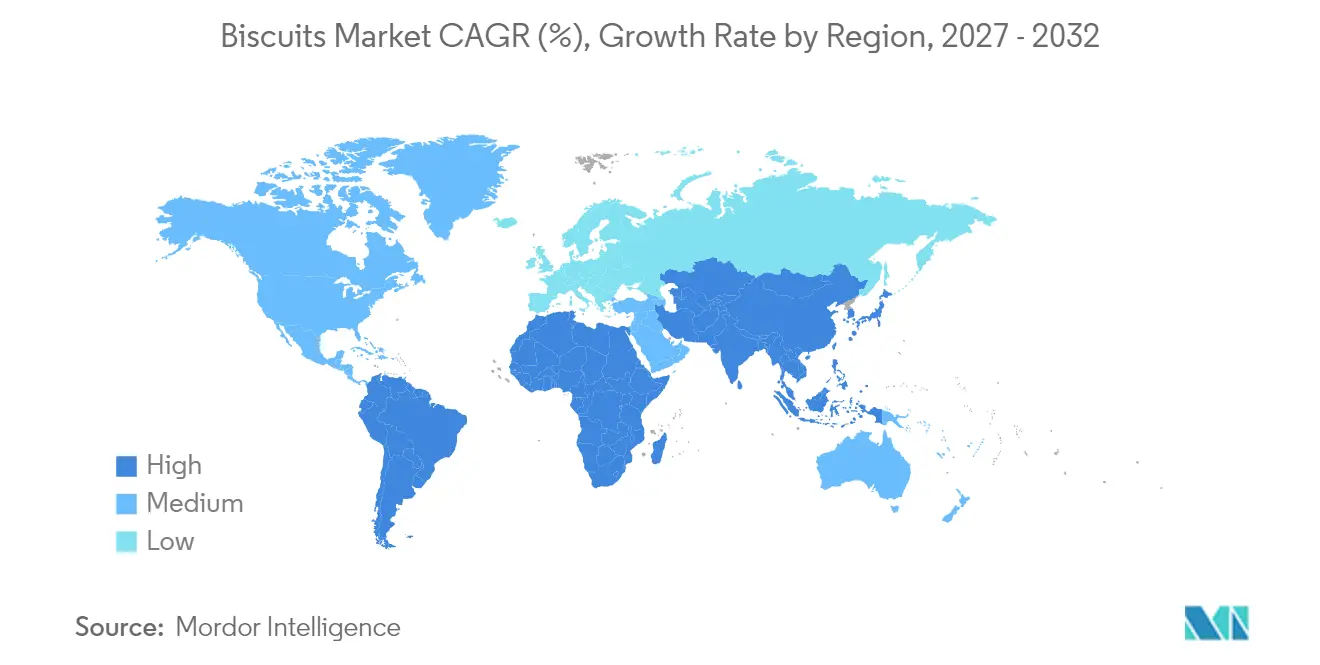

- By geography, Europe dominated with a 27.55% share of the biscuit market size in 2025; the South America region is on course for the fastest 6.84% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Biscuits Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for indulgent snack occasions | +1.2% | Global, with higher impact in North America and Europe | Medium term (2-4 years) |

| Health-oriented reformulations driving fiber-enriched biscuit | +1.0% | Global, with early adoption in Europe and North America | Long term (≥ 4 years) |

| Premiumization trend fueling single-serve portion packs | +0.8% | North America, Europe, and urban APAC | Medium term (2-4 years) |

| Product innovation and flavor varieties | +0.7% | Global, with higher impact in developed markets | Medium term (2-4 years) |

| Expansion of retail and e-commerce channels. | +0.6% | Global, with accelerated growth in APAC and MEA | Short term (≤ 2 years) |

| Rising demand for organic and natural ingredient biscuits | +0.4% | North America, Europe, and urban APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Indulgent Snack Occasions

Consumer behavior is shifting from traditional meals to more frequent snacking. Biscuits, once occasional treats, are now functional meal alternatives, driving growth in the category through premium product innovations. Roland Foods' 2025 industry trends report highlights rising demand for compact, flavor-rich portions, expanding biscuit consumption. Convenience, affordability, and psychological factors fuel this shift, as post-pandemic consumers seek indulgent yet cost-effective options for emotional well-being. For example, Mayora Indah achieved 15% growth in 2024 despite economic challenges. Younger consumers increasingly prefer globally-inspired snacks, seeking diverse flavors. This trend highlights opportunities for innovation and sustained growth in the biscuit market.

Health-Oriented Reformulations Driving Fiber-Enriched Biscuit

Regulatory requirements and increasing consumer health consciousness are driving extensive reformulation efforts in the biscuit industry. In Ireland, the Food Reformulation Taskforce has established comprehensive targets for 2025, requiring a 20% reduction in sugar and calories, alongside a 10% reduction in saturated fats and salt across biscuits and other priority food categories [1]Source: The Food Reformulation Task Force (FRTF), "Food Reformulation Task Force: Priority Food Categories for Reformulation in Ireland", fsai.ie. Manufacturers are implementing strategic reductions in sugar, salt, and fat content while enhancing the overall nutritional value of their products. This shift aligns with evolving consumer preferences, as 62% of Americans consider healthfulness as a key driver for food and beverage purchases, as per the International Food Information Council's 2024 health survey report. The current market dynamics create opportunities for manufacturers to develop premium biscuit products that successfully combine nutritional benefits with appealing taste profiles.

Premiumization Trend Fueling Single-Serve Portion Packs

The market is growing due to premiumization and demand for single-serve packs. Rising disposable incomes and changing lifestyles are driving interest in high-quality snacks. Premium biscuits, made with top-tier ingredients and innovative flavors, are now lifestyle symbols for urban consumers. Health-conscious buyers prefer clean-label, organic, and fortified options, pushing brands toward sustainable packaging and responsible sourcing. Seasonal and multicultural flavors help brands diversify and expand. Competition is intensifying as private labels and established brands focus on differentiation and innovation. Digital marketing, social media, and online promotions are key to building loyalty and driving sales. Advances in packaging enhance freshness, shelf life, and visual appeal, reinforcing premium positioning. The biscuit market is evolving rapidly, shaped by consumer preferences, sustainability trends, and technological progress, driving continued growth as manufacturers innovate to meet diverse demands.

Product Innovation and Flavor Varieties

Manufacturers in the biscuit market are leveraging global flavors and unique combinations to meet evolving consumer preferences. Wellness-focused ingredients like lavender and black garlic are gaining popularity for their health benefits and distinct flavors. In the savory cracker segment, gluten-free options with innovative flavors such as Everything, Toasted Onion, and Cracked Pepper are appealing to health-conscious consumers. Flavor innovation now serves functional roles, with umami-rich seaweed enhancing taste while meeting the demand for plant-based alternatives. This approach satisfies consumers' desire for unique, healthier, and sustainable options. A key example is ITC Sunfeast's Sunfeast Wowzers, set to launch in January 2025. Featuring a 14-layer enrobed design for unmatched crunch, Wowzers offers Cheese Crème and Lemon Crème variants, adding a sweet twist to savory crackers. Targeting homemakers and young adults, ITC Sunfeast positions Wowzers as a standout in the competitive biscuit market.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent HFSS advertising curbs limiting biscuit promotions | -0.8% | Europe, North America, with gradual expansion globally | Medium term (2-4 years) |

| Fluctuating wheat and sugar prices affect profit margins. | -0.9% | Global, with higher impact in import-dependent and emerging markets | Short term (≤ 2 years) |

| Competition from traditional savory snacks | -0.5% | Global, with higher impact in North America and Europe | Short term (≤ 2 years) |

| Intense private label competition | -0.6% | Europe, North America, with expansion to organized retail markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent HFSS advertising curbs limiting biscuit promotions

Advertising restrictions on high fat, sugar, and salt (HFSS) products are transforming marketing approaches in the biscuit industry, with European markets experiencing the most significant impact. The UK's HFSS advertising regulations specifically limit product promotions during peak viewing hours and on digital platforms that attract younger audiences. In response, companies like PepsiCo and Well & Truly are strategically reformulating their products to achieve non-HFSS compliance by 2025, primarily through salt reduction and nutritional improvements [2]Source: Action on Salt and Sugar, "Crisps, Nuts and Popcorn Opportunities for Reformulation", actiononsugar.org. Manufacturers have shifted their communication focus from taste alone to highlighting ingredient quality, portion control, and functional benefits. This strategic transformation demands considerable investment in consumer education and alternative marketing channels, creating entry barriers for smaller companies while favoring brands that successfully communicate health benefits without compromising their indulgence positioning.

Fluctuating wheat and sugar prices affect profit margins.

Biscuit manufacturers face margin pressures due to volatile wheat and sugar prices. Beyond cost management, they must develop pricing strategies balancing consumer sensitivity and profitability in an inflationary environment. In fiscal year 2024, Fox's Burton's Companies reported revenue growth driven by higher sales volumes and inflation-induced price adjustments. Import-reliant markets face added challenges from currency fluctuations, complicating forecasting and financial planning. Supply chain disruptions, as highlighted by Essfeed, have further hindered stable production and cost structures. To address these issues, manufacturers are adopting hedging strategies, diversifying suppliers, and reformulating products to maintain quality and competitiveness in a volatile market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sweet Biscuits Dominate While Savory Accelerates

Sweet biscuits dominate with a 72.11% market share in 2025, establishing their position as the primary product category across global markets. The segment's continued success stems from innovative product development, exemplified by Britannia's 'Pure Magic Choco Stars' featuring chocolate cream in a distinctive star-shaped cavity. Manufacturers maintain market momentum by balancing health regulation compliance with superior taste profiles. ITC's Dark Fantasy Choco Fills illustrates this approach through strategic premium positioning in a value-focused category.

The crackers and savory biscuits segment exhibits robust growth at 6.21% CAGR (2026-2031), propelled by evolving consumer preferences for diverse flavors and functional benefits. This expansion reflects the growing snacking trend, where consumers increasingly gravitate toward international flavors that combine satisfaction with health benefits. Food Business News reports rising consumer interest in umami flavors derived from seaweed and black garlic, particularly in plant-based offerings. The segment's evolution is further demonstrated by Absolutely! Gluten Free's introduction of Everything, Toasted Onion, and Cracked Pepper crackers, which successfully merge health considerations with distinctive flavor profiles.

By Packaging Type: Plastic Pouches Lead While Premium Boxes Gain Ground

Plastic packets and on-the-go pouches hold 57.96% market share in 2025, due to their combination of cost-effectiveness, product protection, and convenience. The growth of quick commerce and evolving shopping patterns has strengthened this format's position, as manufacturers adapt packaging for various retail channels and consumption scenarios. The format serves both value and premium market segments effectively. In response to environmental concerns, companies are developing sustainable solutions, with Greggs aiming to reduce packaging by 25% by 2025 from 2019 levels.

Box packaging is projected to grow at 4.03% CAGR from 2026 to 2031, driven by premium product trends and increased gift-giving occasions. Consumers demonstrate greater willingness to pay higher prices for enhanced presentation, while boxes provide opportunities for brand storytelling and reuse. The growth aligns with the broader premium biscuit segment, where packaging differentiates products in competitive retail environments. The expansion of e-commerce further supports box packaging adoption, as it provides superior product protection during shipping while enhancing the consumer unboxing experience.

By Category: Conventional Wheat Maintains Dominance Amid Free-From Surge

Conventional wheat-based biscuits command an 84.74% market share in 2025, underscoring the enduring consumer preference for traditional formulations. The segment's prominence reflects manufacturers' successful adaptation through strategic reformulation that addresses health concerns while preserving familiar taste profiles. Companies systematically reduce sugar, salt, and fat content while maintaining product appeal, as evidenced by the Food Reformulation Taskforce in Ireland's 2025 targets: 20% reduction in sugar and calories, and 10% reduction in saturated fats and salt in biscuits. The segment's market leadership continues through comprehensive availability across price points and distribution channels.

Free-from varieties lead market growth at 6.28% CAGR (2026-2031), signaling broader consumer acceptance of dietary restriction-friendly products. This expansion stems from significant improvements in taste and texture profiles that eliminate previous barriers to widespread adoption. FoodNavigator reports accelerating sales of gluten-free products, highlighting their evolution from niche to mainstream offerings. Frontier Biscuit Company illustrates this transformation through its gluten-free and vegan biscuits, featuring alternative flours such as almond and chickpea, with products like Jowar Stick varieties that fulfill dietary requirements without compromising taste quality.

By Distribution Channel: Traditional Retail Leads While Digital Transforms

Supermarkets and hypermarkets dominate the distribution landscape with a 44.92% share in 2025. These retail formats sustain their market leadership through widespread geographic presence, strategic pricing models, and integrated shopping solutions. Their strong market position results from extensive product portfolios and targeted promotional campaigns that resonate with multiple consumer segments. The food retail environment in emerging markets, notably Saudi Arabia, showcases a distinct shift toward modern retail formats, as hypermarkets become the preferred shopping destinations. These retail channels continue to evolve by optimizing in-store experiences while seamlessly integrating digital capabilities .

The online retail segment projects a growth rate of 7.92% CAGR from 2026 to 2031, driven by accelerated digital transformation post-pandemic and strengthened delivery networks. Consumer purchasing behaviors have fundamentally transformed toward digital platforms, which deliver accessibility, comprehensive product ranges, and personalized shopping journeys. ITC Foods illustrates this transformation by strategically repositioning its market presence to align with quick commerce platforms. The e-commerce expansion facilitates direct consumer interactions and data-driven marketing initiatives. Additionally, the platform enables emerging brands to reach consumers without extensive physical retail infrastructure requirements.

Geography Analysis

In 2025, Europe holds 27.55% of the global biscuit market, with Germany, France, and the UK leading health-focused and premium product innovations. Biscuit International's acquisition of Patisserie Casteleijn on January 1, 2025, highlights the industry's response to strict sugar content and HFSS advertising regulations, driving product reformulation. In North America, 28% of US and Canadian consumers check ingredient lists, reflecting a preference for premium and health-centric products. The FDA's upcoming ban on Red Dye No. 3, effective January 15, 2027, emphasizes food safety . Advanced retail infrastructure and digital adoption are boosting online sales and direct-to-consumer marketing.

South America is the fastest-growing market, with a 6.84% CAGR (2026-2031), driven by urbanization and a growing middle class demanding convenient, affordable snacks. Local brands are innovating with traditional Latin American flavors to compete with global players. Economic volatility and currency fluctuations challenge raw material costs and pricing in Brazil and Argentina. However, a shift toward healthier biscuits with reduced sugar and added fiber creates opportunities for premium products. Expanding modern retail and e-commerce enhance accessibility, driving market growth.

Asia-Pacific is set for growth, driven by urbanization, rising incomes, and changing consumption habits. Mayora Indah achieved 15% growth in 2024 through strategic placements and celebrity endorsements. In China, artisanal bakeries and a preference for Western-style baked goods drive demand for premium offerings and innovative flavors. The Middle East and Africa are also growing. CBL Group's entry into Kenya highlights East Africa's potential. In Saudi Arabia, rising incomes and changing diets boost the packaged food market. Health-centric regulations push manufacturers toward reformulations. The UAE and South Africa stand out as growth hubs, benefiting from urbanization and modern retail. A youthful demographic and digital media engagement accelerate the adoption of products blending global and local flavors.

Competitive Landscape

The biscuit market is moderately consolidated, characterized by a mix of dominant multinational corporations and an increasing number of regional and private-label players. Leading companies such as Mondelēz International, Inc., Britannia Industries Limited, Parle Products Private Limited, ITC Limited, and Yildiz Holding A.Ş. maintain their market dominance through robust distribution networks, extensive product portfolios, and continuous innovation. However, the rising consumer preference for healthier, specialty, and artisanal products has created opportunities for smaller brands to establish a competitive presence. Additionally, private-label products are gaining traction due to their cost-effectiveness and expanding retail penetration. This competitive balance fosters a dynamic market environment, combining stability with innovation, which defines the moderately consolidated nature of the market.

Strategic differentiation is pivotal in navigating the evolving competitive landscape. Companies like ITC Foods have adopted a dual-speed strategy, balancing rural-focused offerings with premium products to address inflationary pressures while building long-term brand equity. This approach is increasingly critical as the market diversifies across health-conscious, indulgence-driven, and value-oriented segments. Furthermore, the adoption of advanced technologies, such as data analytics and social listening, has become a significant competitive advantage. These tools enable companies to gain deeper insights into consumer preferences and respond swiftly to emerging trends, ensuring they remain relevant in a fragmented market.

Acquisition strategies are playing a crucial role in shaping the competitive dynamics of the market. For example, Ferrero's affiliate, CTH Invest, is negotiating the acquisition of Michel et Augustin from Danone to strengthen its position in the premium biscuits segment. This move aligns with CTH's previous acquisitions of Burton's Biscuit Company, Fox's, Kelsen Group, and Delacre, reflecting a strategic focus on expanding its premium product portfolio. Meanwhile, supply chain disruptions continue to challenge manufacturers, impacting production levels and ingredient sourcing. These disruptions underscore the importance of resilient supply chain strategies to ensure consistent production and availability of raw materials.

Biscuits Industry Leaders

-

Mondelēz International, Inc.

-

Britannia Industries Limited

-

Parle Products Private Limited

-

Yildiz Holding A.Ş.

-

ITC Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: McVitie’s has expanded its biscuit product range in Ghana with the launch of new varieties including Digestive Multigrain, Speculars Ginger, Choco Chips, Shortbread Bites, and Chocolate Shortbread, each offering distinctive flavors and wholesome ingredients for diverse snacking occasions.

- February 2025: Britannia has partnered with Warner Bros. Discovery Global Consumer Products to launch limited-edition Harry Potter-themed Pure Magic Choco Frames biscuits, each pack featuring five biscuits inspired by the four Hogwarts houses—Gryffindor, Slytherin, Ravenclaw, and Hufflepuff.

- February 2025: Mondelez International has partnered with the Wisconsin-based, family-owned cheese company Sargento to launch a new line of cheese crackers called Sargento cheese bakes. Made with Sargento cheese and herbs, the crackers come in three flavors: aged white cheddar and rosemary, pepper jack, and Parmesan and oregano, according to Mondelez.

- January 2025: Oreo introduced several new treats to start 2025, including Oreo Loaded with more creme and cookie pieces, and Oreo Minis Peanut Butter. The brand also have limited-time flavors like football-themed Oreo Game Day and Oreo Irish Creme Thins. Additionally, the company introduced frozen Oreo Bites and Mini Bars, along with Double Chocolate Cakesters and Golden Birthday Cake Cakesters.

Global Biscuits Market Report Scope

Biscuits are flour-based baked food products, typically hard, flat, and unleavened.

The biscuit market is segmented by type, distribution channel, and geography. By type, the market is segmented into crackers and savory biscuits and sweet biscuits. Crackers and savory biscuits are further sub-segmented into plain crackers and flavored crackers. On the other hand, sweet biscuits are further sub-segmented into plain biscuits, cookies, sandwich biscuits, chocolate-coated biscuits, and other sweet biscuits. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, specialist retailers, online retail stores, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, the Middle East and Africa.

The market sizing has been done in value terms in USD for all the abovementioned segments

| Crackers and Savory Biscuits | |

| Sweet Biscuits | Plain Biscuits |

| Cookies | |

| Sandwich Biscuits | |

| Chocolate-Coated Biscuits | |

| Others |

| Boxes |

| Plastic Packets/On-the-Pouches |

| Others |

| Conventional |

| Free-From |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Specialty and Gourmet Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Netherlands | |

| Italy | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| SIngapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Nigeria | |

| Saudi Arabia | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Crackers and Savory Biscuits | |

| Sweet Biscuits | Plain Biscuits | |

| Cookies | ||

| Sandwich Biscuits | ||

| Chocolate-Coated Biscuits | ||

| Others | ||

| By Packaging Type | Boxes | |

| Plastic Packets/On-the-Pouches | ||

| Others | ||

| By Category | Conventional | |

| Free-From | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Specialty and Gourmet Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Netherlands | ||

| Italy | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| SIngapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Nigeria | ||

| Saudi Arabia | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Biscuit market?

The Biscuit market stood at USD 142.05 billion in 2026 and is projected to reach USD 181.83 billion by 2031 at a 5.05% CAGR.

Which region holds the largest Biscuit market share?

Europe leads with 27.55% of global revenue, with Germany, France, and the UK leading health-focused and premium product innovations.

What product segment is growing the fastest within the biscuit market?

Crackers and savory biscuits are expected to expand at a 6.21% CAGR through 2031 owing to diverse flavor innovation and functional positioning.

How big is the online channel in the biscuit market size?

Online retail is the fastest-advancing channel, rising at a 7.92% CAGR, reflecting the boom in quick-commerce and direct-to-consumer models.

Page last updated on: