Grain Processing Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

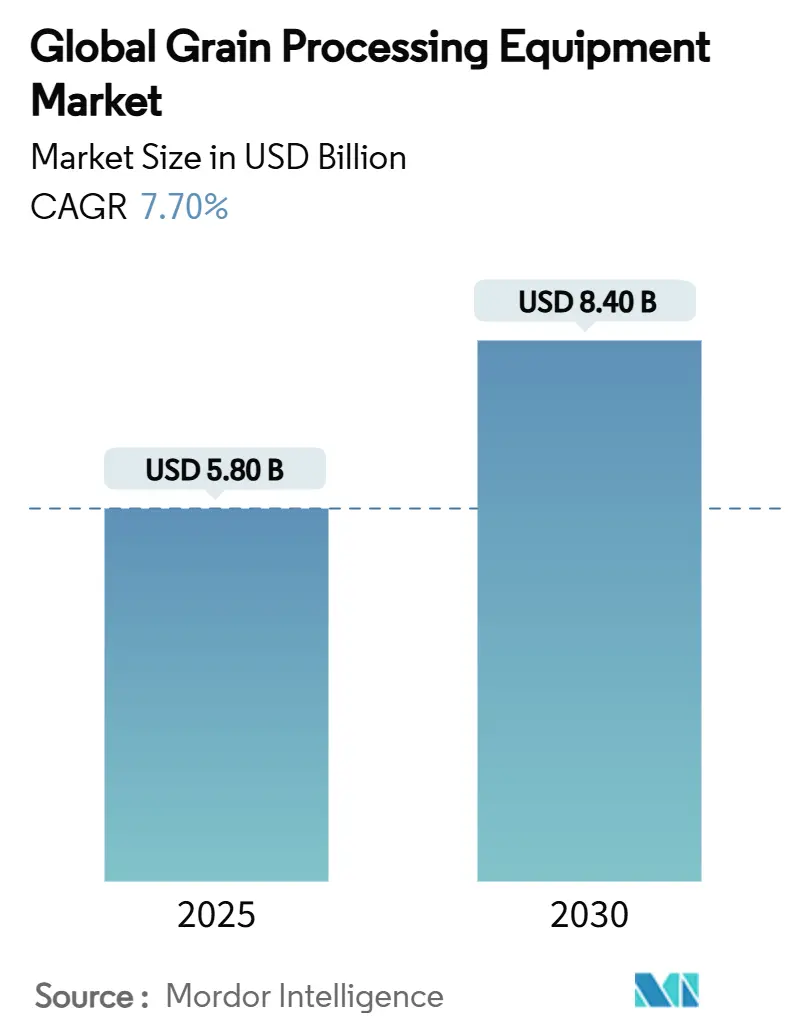

| Market Size (2025) | USD 5.80 Billion |

| Market Size (2030) | USD 8.40 Billion |

| Growth Rate (2025 - 2030) | 7.70% CAGR |

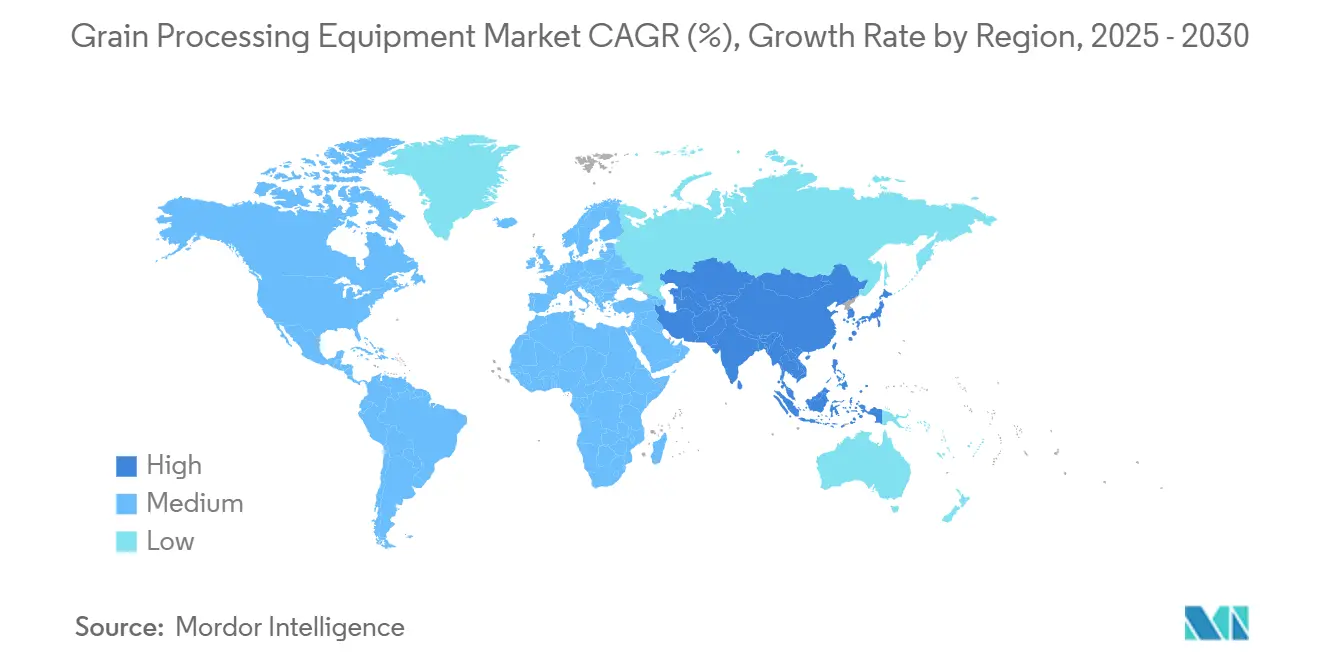

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Grain Processing Equipment Market Analysis by Mordor Intelligence

The grain processing equipment market size stood at USD 5.8 billion in 2025 and is projected to reach USD 8.4 billion by 2030, advancing at a 7.7% CAGR over the forecast period. Accelerating demand for fortified foods, the shift toward sustainable milling practices, and heightened investments in automated plants anchor the expansion of the grain processing equipment market. Heightened geopolitical risk, rising logistics costs, and strict food-safety laws reinforce the business case for regional processing hubs, while equipment makers race to embed artificial intelligence, blockchain, and advanced optical sorting in next-generation lines. In early 2025, Satake Corporation and Kubota formed a partnership to develop automated grain sorting systems with enhanced traceability features in response to stricter regulations in the European Union and the Asia-Pacific regions. This collaboration demonstrates how companies are investing and partnering to address regulatory requirements and technological advancements.

Key Report Takeaways

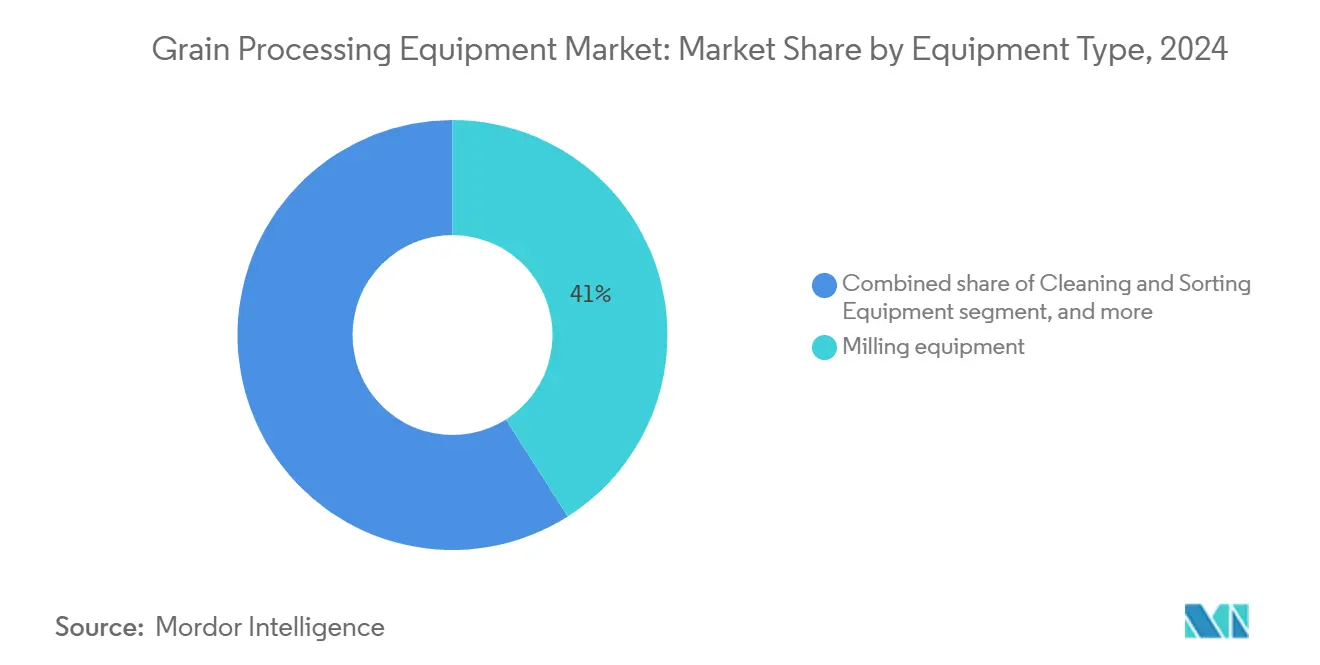

- By equipment type, milling equipment led with 41% of the grain processing equipment market size in 2024, whereas extrusion and expelling equipment posted the fastest growth at a 9.6% CAGR through 2030.

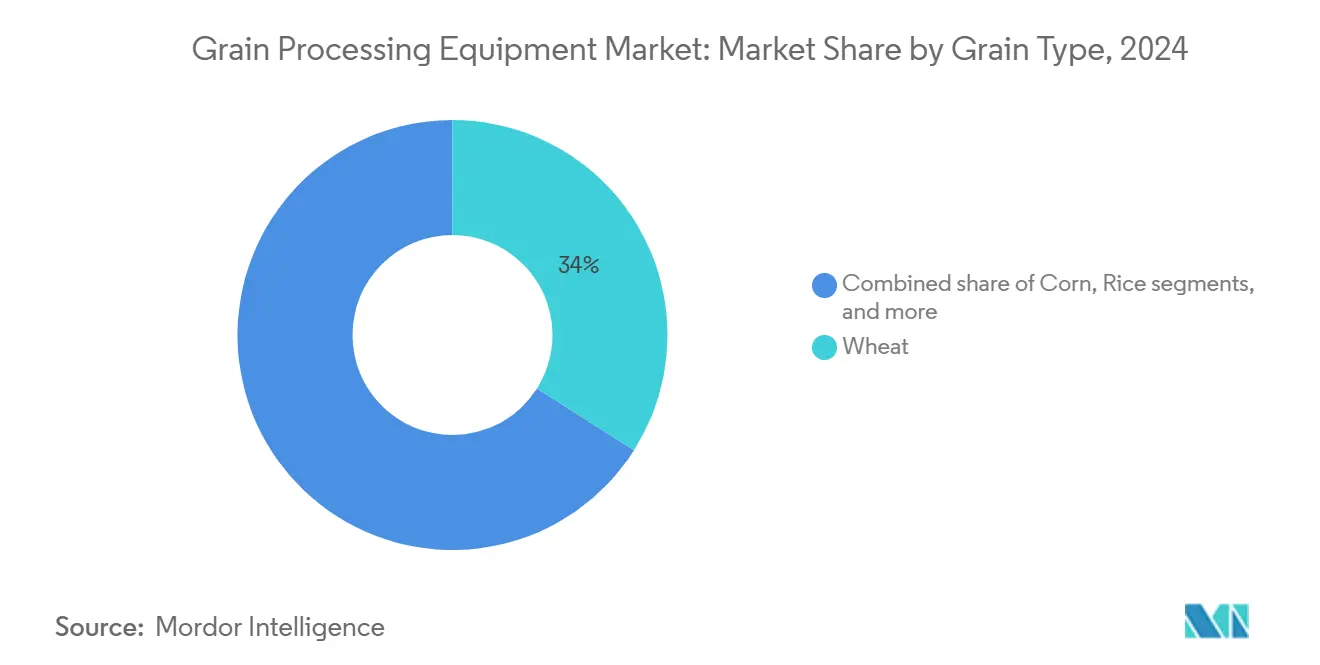

- By grain type, wheat accounted for a 34% slice of the grain processing equipment market size in 2024, and soybean processing is forecast to register an 8.4% CAGR between 2025 and 2030.

- By geography, Asia-Pacific commanded 31% of grain processing equipment market size in 2024 and is also the fastest growing, which is projected to rise at a 9.1% CAGR through 2030.

- Buhler Group, AGCO Corporation, Satake Corporation, TOMRA Systems ASA, and Alapala controlled 51% of global sales in 2024, positioning the grain processing equipment market as moderately concentrated.

Global Grain Processing Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustained demand for fortified processed grains | +1.2% | Global and Asia-Pacific core | Medium term (2-4 years) |

| Rapid automation of large-scale mills | +1.8% | North America and Europe | Long term (≥ 4 years) |

| Rise of extrusion in plant-based protein foods | +1.5% | Global and Europe leading | Short term (≤ 2 years) |

| Stringent food-safety mandates in emerging economies | +0.9% | Asia-Pacific and Africa | Medium term (2-4 years) |

| AI-based predictive maintenance of milling lines | +0.7% | North America and Europe | Long term (≥ 4 years) |

| Upcycling of grain side-streams into high-margin ingredients | +0.6% | Europe and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sustained Demand for Fortified Processed Grains

Government-led public health initiatives and widespread micronutrient deficiencies sustain robust interest in fortified staples. AGI’s fortified rice kernel line uses twin-screw extrusion to embed vitamins and minerals directly into rice, addressing malnutrition in over 2 billion people worldwide. Mandatory fortification policies across Asia deepen the installed base for precision coating and dosing solutions. Producers seek equipment that can maintain nutrient integrity under high-throughput conditions, fostering R&D in low-shear extrusion and micro-encapsulation modules. The trend also feeds new revenue for suppliers offering turnkey validation and traceability packages aligned to evolving regulations. As fortified rice, wheat, and maize products penetrate school meals and relief programs, demand for high-capacity, hygienic fortification lines rises in tandem with multilateral funding flows. Equipment makers able to balance cost, scalability, and compliance objectives are set to capture enlarged order books throughout the medium term.

Rapid Automation of Large-Scale Mills

The deployment of Industrial Internet of Things (IIoT) technology is transforming mill economics. North American and European mills have installed thousands of wireless sensors that transmit real-time process data to cloud analytics platforms, generating annual savings of USD 320,000 per mill through reduced downtime. Labor shortages, with 2.4 million vacant positions in farming and processing anticipated in 2024, combined with increasing wages, are driving operators to implement automated facilities. The integration of automated roll gap adjustments, computer-vision quality control systems, and self-optimizing energy management solutions improves yield rates while reducing waste. Equipment vendors now provide predictive maintenance systems that analyze vibration and temperature patterns through machine learning algorithms to extend bearing life and prevent system failures. Companies that have adopted these technologies early report 8% increases in throughput and 5-10% reductions in electricity consumption, establishing efficiency standards that competitors must achieve to maintain profitability.

Rise of Extrusion in Plant-Based Protein Foods

High-moisture extrusion unlocks fibrous textures that mimic meat, catalyzing equipment capex as plant-based protein moves mainstream. Baker Perkins and Buhler commercialized twin-screw lines capable of converting soy, pea, and emerging protein sources into texturized vegetable protein at an industrial scale. Demand surges as flexitarian diets expand across Europe and North America, while new entrants exploit premium pricing in alternative meat. Processors need extruders with precise temperature, pressure, and screw-speed control to preserve amino-acid profiles. Equipment must also handle high-viscosity dough and swift product changeovers for flavor diversity. Fast-growing startups prioritize short lead times and modularity, pushing incumbents to revamp supply chains and offer rental or leasing models. The convergence of consumer ethics, climate concerns, and protein diversification positions extrusion solutions as a pivotal growth throughout the future.

Stringent Food-Safety Mandates in Emerging Economies

Regulatory tightening across Asia-Pacific and Africa prompts a wave of retrofits in aging mills. FDA’s FSMA 204 rule mandates end-to-end traceability by 2026, spurring the adoption of hygienic design, automated record-keeping, and blockchain integration. Regional blocs such as the East African Community lower aflatoxin limits to 5 µg/kg, obliging investments in optical sorting, UV detection, and mycotoxin remediation. Financing from development banks accelerates technology diffusion, while multinational snack brands impose supplier audits that mirror Global Food Safety Initiative protocols. Equipment vendors respond with stainless-steel frames, open accessibility for dry cleaning, and CIP-ready conveying lines. Demand also rises for inline spectroscopy units that document compliance in real time, creating ancillary software revenue streams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in grain commodity prices | -1.4% | Global | Short term (≤ 2 years) |

| High upfront capital expenditure for modern plants | -1.1% | Africa and South America | Medium term (2-4 years) |

| Skilled labor shortages in rural processing hubs | -0.8% | North America and Europe | Long term (≥ 4 years) |

| Rising explosion-hazard insurance premiums for mills | -0.5% | North America and Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Grain Commodity Prices

Geopolitical conflicts, export bans, and extreme weather have sent wheat and corn prices swinging by more than 30%, compressing processor margins and freezing equipment budgets. Trade tensions exacerbate volatility as tariffs reconfigure global flows and lift procurement uncertainty. During price spikes, processors delay capex, favor asset-light upgrades, and renegotiate delivery schedules, disrupting OEM order books. Hedging provides partial relief but cannot offset prolonged downturns. Equipment vendors counter cyclicality by diversifying into aftermarket services and subscription-based digital solutions to cushion revenue. However, persistent volatility remains a drag on capital commitments, particularly among mid-tier millers with thin balance sheets.

High Upfront Capital Expenditure for Modern Plants

State-of-the-art facilities routinely cost tens of millions. Green Acres Milling’s new oats plant in Minnesota will require USD 55 million, illustrating the steep barrier for newcomers. Emerging-market processors often face double-digit financing rates and limited collateral, while international lenders demand comprehensive feasibility studies before releasing funds. Integration complexity drives costs as plants incorporate AI, blockchain, and high-efficiency dryers. Extended payback periods deter investment unless subsidies or long-term offtake agreements soften risk. To ease entry, vendors promote modular micro-mills and lease-to-own options, yet adoption remains slow where access to hard currency is constrained.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Milling Dominance Meets Extrusion Innovation

Milling equipment captured 41% of the grain processing equipment market size in 2024, underpinned by worldwide demand for flour and meal staples. The segment benefits from continuous design optimizations such as Buhler’s Mill E3, which trims building volume by 30% and slashes energy use by 10%. Beyond cost savings, digitized roll-gap settings and predictive bearing analytics bolster uptime. Cleaning and sorting machinery is propelled by stricter aflatoxin and mycotoxin thresholds. Handling and storage systems are increasingly incorporate IoT sensors for grain-quality tracking during long-haul storage.

Extrusion and expelling equipment recorded the fastest 9.6% CAGR through 2030, fueled by plant-based meat analogs, breakfast cereal innovations, and fortified rice production. High-moisture twin-screw lines that craft meat-like fibers now run alongside traditional dry extruders for snacks. Processors seek modular screws and streamlined changeover kits to accommodate diverse protein inputs. Other specialized machines, including pearling units for ancient grains enjoy premium margins as wellness trends diversify diets.

By Grain Type: Wheat Leadership Challenged by Diversification

Wheat processing represented 34% of the grain processing equipment market size in 2024, reflecting entrenched consumption of bread, pasta, and noodles worldwide. However, gluten-free products and low-carb diets introduce competitive tension, nudging millers to add sorghum and millet capabilities. Corn accounted for the second-largest market share, buoyed by ethanol mandates and feed demand, with processors integrating wet-milling and fermentative capacity for starch derivatives [1]Source: Oklahoma State University, “Cattle Grain Processing Symposium Proceedings,” okstate.edu. Rice also occupied a significant share, dominated by Asia-Pacific mills, where Bühler solutions handle around 30% of the global harvest.

Soybean led growth with an 8.4% CAGR forecast, driven by protein isolates for alt-meat formulations and biodiesel feedstock expansions. New crush plants incorporate solvent-free extraction and enzymatic degumming to lift oil yields and lower carbon footprints. Remaining grains such as quinoa and amaranth surged in health-conscious consumer segments, prompting equipment suppliers to tailor small-batch, allergen-segregated lines for premium brands [2]Source: CBI, “The European Market Potential for Specialty Grains with Added Value,” cbi.eu.

Geography Analysis

Asia-Pacific generated 31% of global revenue in 2024 and is forecast to climb at 9.1% CAGR through 2030, which makes it the fastest-growing region on the back of China’s grain consumption plan and India’s accelerated food-processing build-out. Government subsidies covering up to 50% of capex spur local mill upgrades, while public-private storage projects such as Egypt’s USD 153 million Suez Canal complex showcase regional appetite for modern infrastructure. Regional OEMs such as Satake capitalize on rice-specific knowledge to expand into Indonesia, Vietnam, and the Philippines.

North America occupied a significant market share in 2024, expanding at a moderated CAGR. The United States and Canada prioritize automation retrofits, carbon-neutral operations, and specialty grain diversification. High-profile investments, including Ocrim’s 610-metric tons-per-day projects for North Dakota Mill, underscore the region’s focus on energy efficiency and remote monitoring.

Europe held a major share, driven by stringent sustainability rules and demand for organic grains. Plants retrofit regenerative burners and low-emission dryers to satisfy the European Union's Green Deal targets, while upcycling ventures capture European Union grants to valorize bran fractions. Africa, although it has a smaller market share, is the second-fastest-growing region. Rapid urbanization and food security agendas stimulate investments in regional processing through donor-funded projects that package turnkey silos, mills, and cold-chain logistics to reduce post-harvest losses. South America’s 6% share increases by 6.2% due to rising soybean crush and export volumes. Middle Eastern processors, spurred by sovereign food security funds, are increasing capacity by 6.8% annually, exemplified by Modern Mills’ USD 40 million expansion in Saudi Arabia.

Competitive Landscape

The market concentration in the grain processing equipment market is moderate, with the top five firms controlling a major share of 51% in 2024, leaving scope for regional specialists and tech-focused challengers. Buhler commanded a major market share, leveraging turnkey solutions, global service depots, and its newly opened Uzwil innovation center to deepen customer lock-in. AGCO retained its pre-divestiture, sharpening its focus on core agricultural machinery after selling its Grain and Protein unit for USD 700 million [3]Source: AGCO Corporation, "AGCO Completes Divestiture of Grain & Protein Business", agcocorp.com.

Satake Corporation, TOMRA Systems ASA, and Alapala are also playing key roles by addressing specialized needs and technology‑driven differentiation. Satake’s expertise in rice and cereal processing, supported by developments in optical inspection and husking technology, has kept it highly competitive in Asian markets. TOMRA Systems has leveraged its strong background in sensor‑based sorting to provide advanced sorting solutions for grain and seed processing, with recent AI‑driven sorter launches expanding its adoption among premium grain processors. Alapala, known for turnkey milling plants and customized project execution, has boosted its market share through investments in modular mill designs and partnerships that shorten project timelines and improve cost efficiency.

Technology remains the key battlefield. Suppliers embed blockchain traceability for allergen management, while patent filings in aflatoxin reduction and pneumatic conveying automation proliferate. Start-ups leverage configurable Digital Twins to win pilot projects in specialty milling, forcing incumbents to expand partner ecosystems. Sustainability credentials, measured via lifecycle carbon audits, increasingly determine tender outcomes, prompting incumbents to invest in regenerative energy systems and recyclable packaging lines.

Grain Processing Equipment Industry Leaders

-

Satake Corporation

-

TOMRA Systems ASA

-

Alapala

-

AGCO Corporation

-

Buhler Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: AGCO Corporation has reported an investment of USD 95 million in a new 84,000-square-meter parts distribution center in Amnéville, France. This facility aims to enhance after-sales support for its GSI and Cimbria grain brands. Scheduled to commence operations by the end of 2026, the center will serve Europe and the Middle East, while also acting as the master depot for parts shipments to the Americas and the Asia-Pacific region. The low-emission, sustainable facility will feature automated storage, packaging, and scanning systems to support 24/7 e-commerce ordering.

- December 2024: CPM completed the acquisition of Jacobs Global, expanding its product portfolio in hammermill hammers, screens, and pellet mill dies. The acquisition increases CPM's manufacturing capacity and global market presence to serve its customer base. The integration of Jacobs Global's products enhances CPM's position in the feed markets by providing comprehensive processing solutions.

- October 2024: Buhler has opened its new Grain Innovation Center (GIC) in Uzwil, Switzerland, a five-story, 2,000 m² facility focused on advancing grain processing technology for food and animal feed. The GIC replaces the 1951-era Grain Technology Center and features over 70 systems for cleaning, optical sorting, grinding, sifting, mixing, protein concentration, pelleting, dehulling, and hygienization. The facility supports production-scale trials of up to 5 t/h, allowing customers to test new processes and products, including ancient grains, pulses, by-products, and non-food biomass.

- August 2024: AGI's partnership with Boa Safra Ag LLC provides grain farmers access to digital technologies and comprehensive grain management solutions. The collaboration offers cost incentives, online resources, and educational programs to help farmers improve operational efficiency, grain quality, safety, and profitability.

Global Grain Processing Equipment Market Report Scope

| Milling Equipment |

| Cleaning and Sorting Equipment |

| Extrusion and Expelling Equipment |

| Handling and Storage Equipment |

| Other Equipment |

| Wheat |

| Corn |

| Rice |

| Soybean |

| Other Grains |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| Russia | |

| Italy | |

| Spain | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| Philippines | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Equipment Type | Milling Equipment | |

| Cleaning and Sorting Equipment | ||

| Extrusion and Expelling Equipment | ||

| Handling and Storage Equipment | ||

| Other Equipment | ||

| By Grain Type | Wheat | |

| Corn | ||

| Rice | ||

| Soybean | ||

| Other Grains | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| Russia | ||

| Italy | ||

| Spain | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| Philippines | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the grain processing equipment market?

The grain processing equipment market size was USD 5.8 billion in 2025.

How fast will the grain processing equipment market grow by 2030?

The market is forecast to expand at a 7.7% CAGR, reaching USD 8.4 billion by 2030.

Which equipment type generates the largest revenue?

Milling equipment leads with 41% of the grain processing equipment market share in 2024.

Which region is growing the fastest?

Asia-Pacific is projected to post the highest growth at a 9.1% CAGR through 2030 because of large-scale government modernization programs.

Page last updated on: