Grain Storage Silos Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

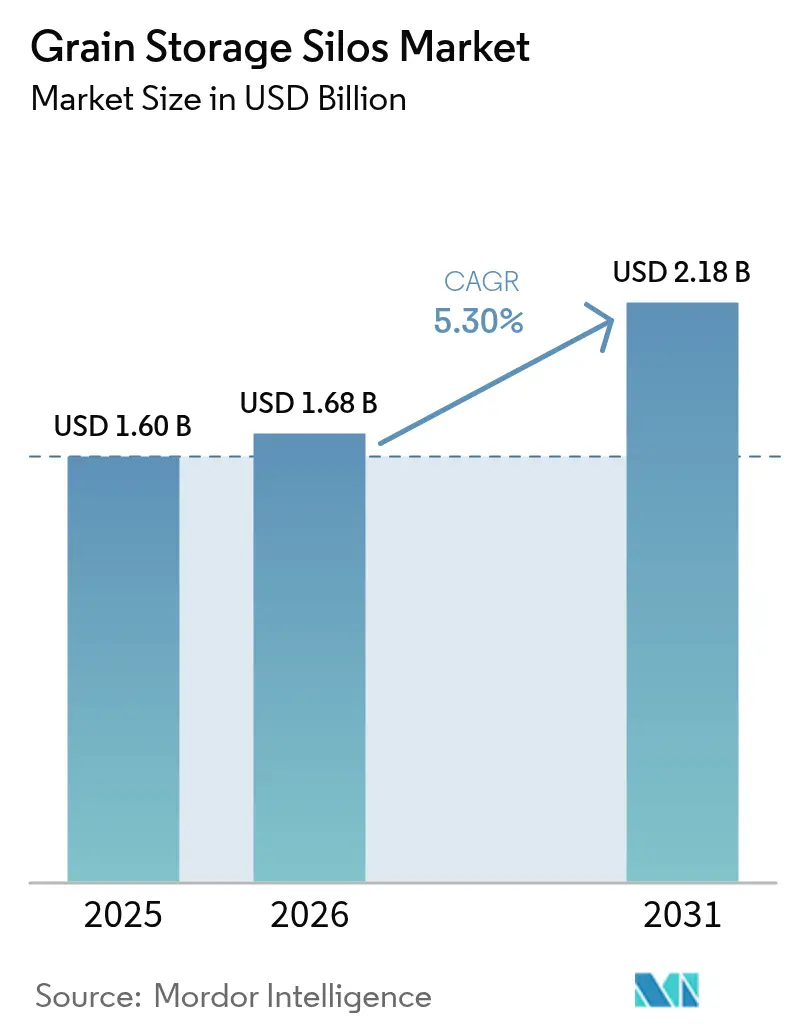

| Market Size (2026) | USD 1.68 Billion |

| Market Size (2031) | USD 2.18 Billion |

| Growth Rate (2026 - 2031) | 5.30% CAGR |

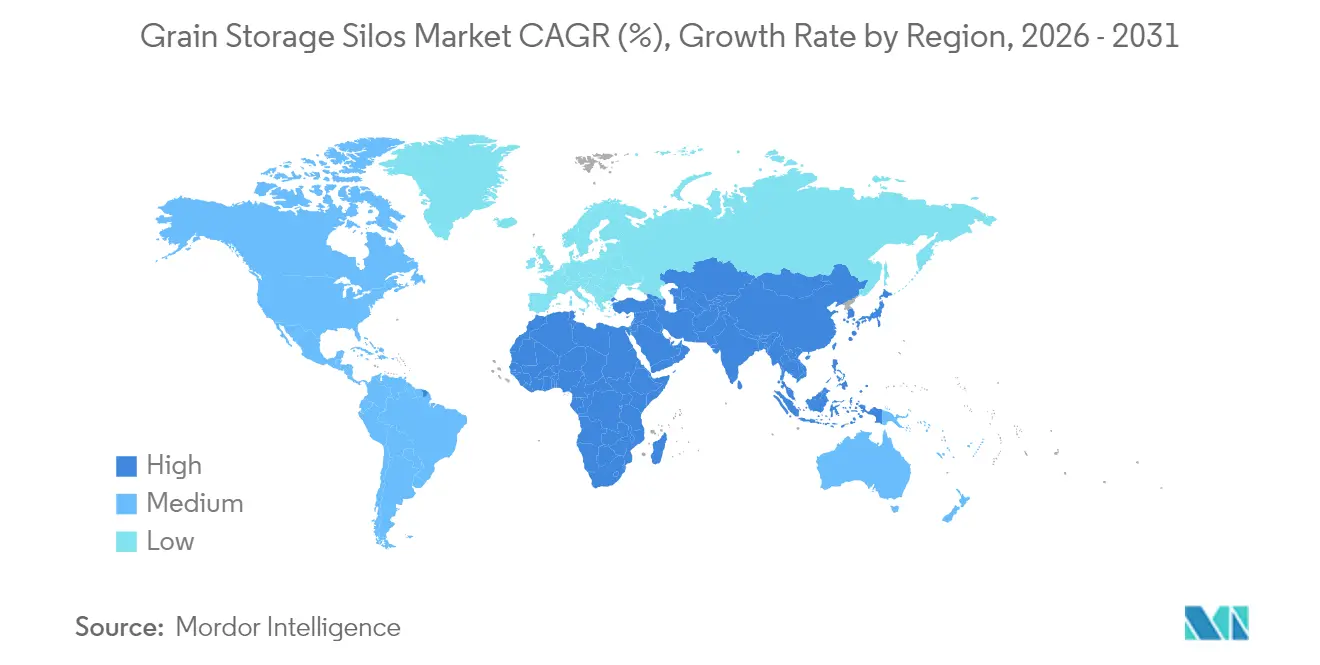

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Grain Storage Silos Market Analysis by Mordor Intelligence

The grain storage silos market size in 2026 is estimated at USD 1.68 billion, growing from 2025 value of USD 1.60 billion with 2031 projections showing USD 2.18 billion, growing at 5.3% CAGR over 2026-2031. Digitally enabled monitoring, accelerating sovereign grain-reserve programs, and widening production volatility are pivotal growth levers. Government stimulus in Asia, large port-side projects in North America, and rapid warehouse build-outs in Africa are creating a multi-speed demand landscape. Manufacturers are prioritizing modular designs that shorten construction cycles and lower up-front capital exposure, while coating technologies such as Magnelis extend asset life and cut lifetime ownership costs. Wider adoption of predictive aeration and CO₂-based spoilage alerts is lowering operating expenses, positioning connected silos as a cornerstone of modern food-security strategies.

Key Report Takeaways

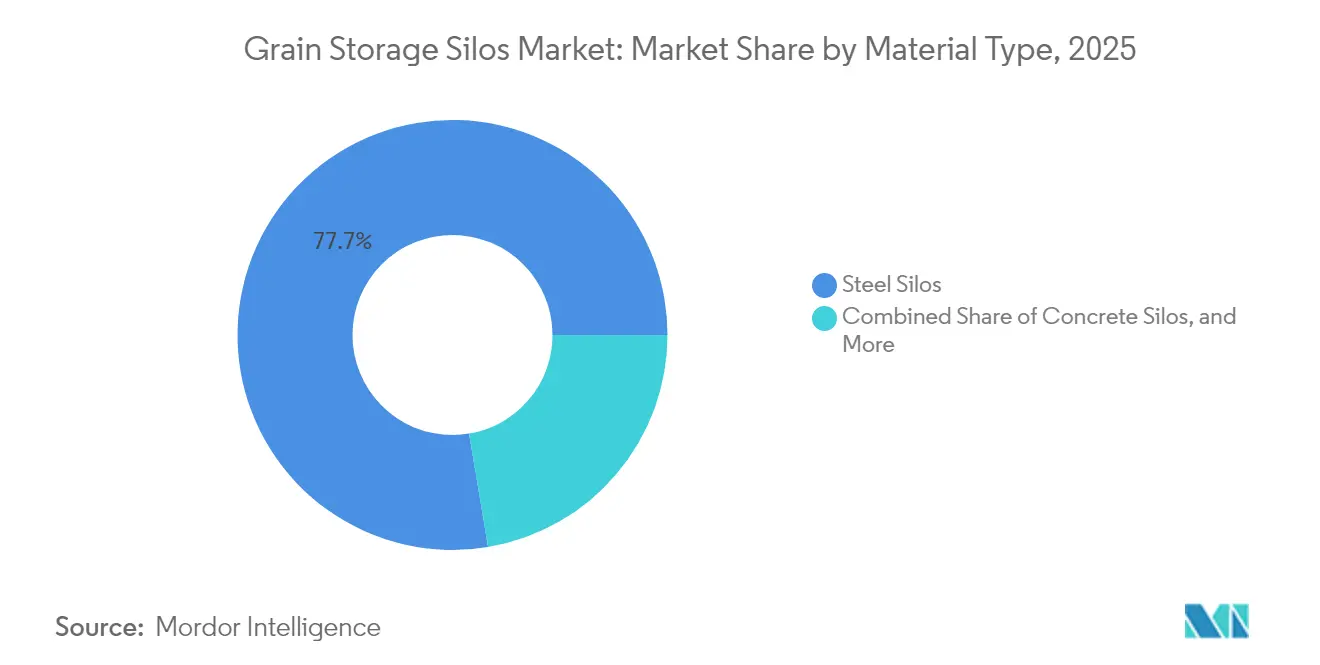

- By material type, steel silos led with 77.65% grain storage silos market share in 2025, whereas metal silos are projected to expand at a 6.55% CAGR through 2031.

- By grain type, corn commanded 32.45% of market share in 2025, whereas soybeans are projected to expand at a 9.10% CAGR through 2031

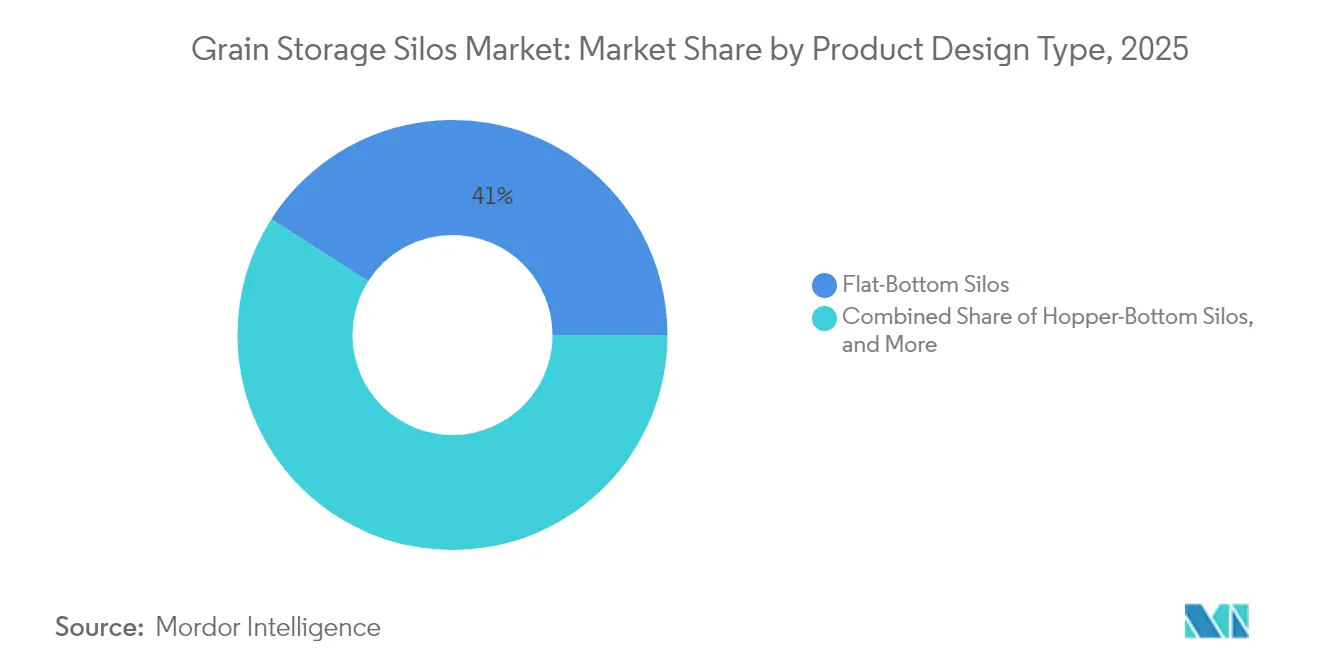

- By product design, flat-bottom units accounted for 40.95% of the grain storage silos market size in 2025, while square and rectangular systems are set to grow at a 5.18% CAGR to 2031.

- By geography, Asia-Pacific held 35.05% of 2025 revenue, yet Africa is poised for the fastest 6.08% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Grain Storage Silos Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital monitoring and IoT-enabled grain-quality sensors | +1.2% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Government-backed strategic grain-reserve expansions | +1.5% | Asia-Pacific core and North America | Long term (≥ 4 years) |

| Surge in on-farm storage demand for price arbitrage | +0.8% | North America and Europe, expanding to Brazil and Argentina | Short term (≤ 2 years) |

| Rising production volatility requires buffer storage | +1.0% | Global, with acute needs in climate-vulnerable regions | Medium term (2-4 years) |

| Shift toward bulk-export infrastructure | +0.7% | Coastal regions globally, Black Sea corridor priority | Long term (≥ 4 years) |

| Adoption of modular square and composite silos | +0.4% | Global, with faster uptake in land-constrained markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital monitoring and IoT-enabled grain-quality sensors

Connected sensors now provide real-time temperature, moisture, and CO₂ readings that flag spoilage trends weeks in advance, enabling predictive aeration that trims unplanned downtime by USD 320,000 per facility each year[1]Source: “Unlocking Efficiency in Grain Processing with IIoT,” Grain Journal, grainjournal.com . Cloud dashboards aggregate data across multiple locations, transforming silo management from manual inspection to analytics-driven oversight. Payback periods often drop below two harvests as energy consumption falls and quality premiums rise. Technology suppliers are integrating wireless probes into galvanized panels at the factory, turning hardware and software into a single value proposition. Momentum is strongest in North America, but fast-growing pilot projects in Southeast Asia signal broadening adoption.

Government-backed strategic grain-reserve expansions

China lifted its 2025 grain stockpiling budget to secure domestic supply buffers, while India approved a USD 15 billion cooperative plan that triples wheat capacity to 9 million metric tons by 2028[2]Source: "World's largest Grain Storage Plan in Cooperative sector", cooperative.gov.in. Tunisia, backed by multilateral lenders, is upgrading 206,000 metric tons of legacy silos and adding 181,000 metric tons of fresh space to stabilize import bills. These national programs prioritize high-capacity flat-bottom designs with automated fumigation, driving orders for turnkey installations above 50,000 metric tons. Long-term contracts give manufacturers pricing visibility and underpin the shift toward domestically fabricated panels to curb currency risk.

Surge in on-farm storage demand for price arbitrage

Low-interest Farm Storage Facility Loans encourage United States growers to install mid-scale bins that enable them to hold corn and soybeans until basis levels improve, thereby boosting average returns. Economic modeling indicates internal rates of return exceeding 14%, positioning storage as a low-risk hedge against harvest-time discounts. Wireless fan controls and remote moisture probes reduce labor dependence, a valuable advantage as rural labor pools become increasingly scarce. Similar trends are emerging in Brazil and Argentina, where grain bags are giving way to permanent metal bins as futures market participation deepens.

Rising production volatility requiring buffer storage

Extreme weather is amplifying yield swings that strain just-in-time logistics. Research links climate change to a 10% drop in global wheat yields over 50 years, underscoring the need for flexible buffer capacity[3]Source: “A half-century of climate change in major agricultural regions,” PNAS, pnas.org. Multi-compartment silos that segregate grades and moisture levels preserve market access when harvests include a larger share of sub-prime grain. Governments in climate-vulnerable regions are prioritizing storage in rural resilience plans, while insurers increasingly discount policies for facilities equipped with automated condition monitoring.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High up-front capital and steel-price volatility | -0.9% | Global, with an acute impact in price-sensitive markets | Short term (≤ 2 years) |

| Pest infestation and mold risk are inflating OPEX | -0.6% | Humid climates and developing regions primarily | Medium term (2-4 years) |

| Regulatory curbs on fumigation chemicals | -0.4% | Europe and North America are leading, global adoption following | Long term (≥ 4 years) |

| Fragmented aftermarket service in emerging markets | -0.3% | Africa, Southeast Asia, and North America focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High up-front capital and steel-price volatility

Spot hot-rolled coil prices surged 18% in early 2025 on tariff uncertainty, lifting bin costs for basic builds. Contractors now insert price-escalation clauses that share risk with growers, nevertheless, many smallholders pivot to hermetic bags despite their shorter life. Index-based steel hedging remains underused in agriculture, although larger cooperatives are experimenting with swaps to cap exposure. Suppliers of square silos claim 15% less steel per metric ton of capacity, an advantage gaining traction among price-sensitive buyers.

Pest infestation and mold risk inflating OPEX

Resistance to phosphine is spreading, compelling operators to rotate chemistries or adopt controlled-atmosphere treatments, which can increase annual pest-control budgets. Warm, humid regions incur higher aeration and fumigation costs. In West Africa, storage pests destroy stored maize within six months. Real-time CO₂ monitoring identifies infestation hotspots earlier but requires investment in sensor platforms and data plans. Food-safety standards such as ISO 22000 embed stringent documentation that adds administrative overhead.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Steel dominance anchors capacity expansion

Steel silos captured 77.65% of 2025 revenue, cementing their role as the workhorse solution for high-volume elevators. They benefit from standardized panel designs that allow rapid mass production and easy global shipping. Magnelis-coated sheets lengthen service life to 25 years without repainting, curbing the total cost of ownership. The grain storage silos market size for steel units is forecast to grow at a steady clip as replacement cycles converge with new builds in Asia. Metal silos, largely aluminum-alloy variants, are advancing at a 6.55% CAGR by 2031, propelled by lighter structures that require smaller foundations, a boon in soft-soil geographies. Composite and hybrid systems remain an early-stage niche but deliver moisture resistance prized for rice and seed storage.

In concrete, demand concentrates in port terminals and ethanol plants where 200,000 metric tons blocks offer seismic stability and minimal upkeep. Galvanized steel, however, is gaining share in North America after code revisions raised wind-load and roof-strength standards. Original equipment manufacturers (OEMs) responded with bins that assemble in under 12 days. Smart sensors now arrive factory-fitted, and some vendors embed fiber-optic cables during panel rolling, teeing up structural-health monitoring subscriptions. Sustainability audits favor steel for its recyclability at end-of-life, bolstering its dominance in the grain storage silos market.

By Grain Type: Corn leadership amid soybean growth acceleration

Corn storage held 32.45% grain storage silos market share in 2025, reflecting its position as the most produced cereal and its central role in feed, ethanol, and food industries. Soybean storage is projected to register a 9.10% CAGR through 2031 as global demand for plant-based protein and edible oils soars. Wheat storage keeps steady momentum through government-backed reserve targets. India alone is tripling wheat capacity to 9 million metric tons. Rice storage demands specialized low-moisture environments in the Asia-Pacific, where export premiums hinge on appearance and aroma retention.

Temperature management tech is evolving by grain type. Soybeans require tighter thermal control to prevent oil rancidity, prompting manufacturers to integrate variable-speed fans and high-precision probes. Corn benefits from standardized handling, but ethanol expansion is driving silo clusters near processing plants to trim logistics costs. Geographic patterns persist, with corn storage concentrated in the United States, Brazil, and Argentina, while soybean investments follow acreage growth in South America and Southeast Asia. These trends reinforce product-tailored innovation as the grain storage silos market scales.

By Product Design: Flat-bottom efficiency meets modular rethink

Flat-bottom silos accounted for 40.95% of sales in 2025, due to their compatibility with sweep augers and high-capacity bucket elevators that enable continuous processing operations. They represent the cornerstone infrastructure for terminal elevators pushing throughputs above 1 million metric tons per year. Conversely, square and rectangular designs are climbing a 5.18% CAGR through 2031 as land costs surge near railheads and ports. A four-cell square block can raise capacity by 20% on the same footprint versus a round alternative, a decisive factor in East Asian industrial parks. Gravity-flow hopper-bottom units serve feed mills that need complete discharge and allergen segregation but cost 10–15% more per metric ton of storage.

Farm silos are scaling in diameter. Sukup’s 156-foot bin, yet modular bolt-on rings let growers start small and double capacity later without altering foundations. Feed hoppers carved out a niche for finishing operations where daily turnover is high and inventory visibility is paramount. Manufacturers now run structural simulations to optimize stiffener placement, saving up to 4% steel weight per project. Across designs, the grain storage silos market share for smart-ready bins is rising, with more than half of new orders specifying at least one IoT feature in 2025.

Geography Analysis

The Asia-Pacific region retained a 35.05% revenue lead in 2025, driven by expansive reserve strategies in China and India. China’s enlarged 2025 stockpiling budget and India’s USD 15 billion cooperative build-out funnel orders toward domestic fabricators and global Original equipment manufacturers (OEMs) partnering on turnkey complexes. Projects in Bangladesh and Thailand underscore cross-border spillover as exporters upgrade terminals for bulk rice. Yet challenges persist in China, where on-farm corn losses reach 2.41% because many bins lack forced aeration, indicating a rural upcycle in small and mid-scale steel units.

Africa is the fastest-growing region at a projected 6.08% CAGR, driven by hunger mitigation efforts targeting the continent’s 282 million undernourished citizens. Donor-funded warehouses in Nigeria and Kenya combine metal silos with solar aeration to cut diesel reliance. Research in Uganda has shown that improved metal designs can slash insect prevalence by 87%, with 4.5-year payback periods. Countries along the Sahel are evaluating community-scale banks to reduce post-harvest losses that hover near 30%.

North America and Europe move steadily as technology retrofits offset mature capacity. American co-ops are replacing 1970s bins with corrosion-resistant panels and rooftop safety cages that meet Occupational Safety and Health Administration's (OSHA) 2025 ladder rules. Europe is phasing in fumigant-free storage, prompting investments in gas-tight construction and automated refrigeration tunnels for malting barley. South America faces a critical gap. Brazil’s current assets cover only 55% of production, leading to costly field piles and quality downgrades. Meanwhile, Middle Eastern importers layer strategic reserves on top of port terminals to secure staple cereals, with Saudi and United Arab Emirates financiers underwriting 200,000 metric ton builds that include ambient-control rooms for desert climates.

Mordor Intelligence provides coverage of the grain storage silos market across other key regional markets. Detailed country-level analysis extends to United States incorporating local coverage and market participation, as required.

Competitive Landscape

The grain storage silos market features moderately fragmented competition with a technological pivot reshaping leadership dynamics. North American brands, such as Brock Grain Systems and Meridian Manufacturing, concentrate on jumbo commercial bins, often exceeding 2,449 metric tons per unit. European firms like Symaga, S.A.U. leverage modular kits and global Engineering, Procurement, and Construction (EPC) partnerships to land turnkey contracts across Asia and Africa. Rising entrants tout hermetic composite panels that promise chemical-free storage, encroaching on traditional galvanized incumbents.

Innovation is the primary battleground. ArcelorMittal’s Magnelis coating, with self-healing zinc-magnesium, extends warranty terms, compelling rivals to upgrade surface treatments. IoT alliances pair hardware builders with analytics startups. One vendor bundles a five-year predictive-maintenance subscription that claims 20% Operating Expenses (OPEX) savings. To defend their market share, incumbents are establishing regional service hubs that guarantee 48-hour delivery of spare parts. Compliance with ISO 22000 and Hazard Analysis and Critical Control Points (HACCP) drives a premium segment where larger agribusinesses pay extra for traceability and food-grade sealants.

Geographic expansion continues apace. Symaga, S.A.U.’s 69,664 m³ terminal in Bangladesh and 49,660 m³ rice complex in Thailand demonstrate the exportability of European engineering. Chinese builders gain traction in Belt and Road corridors by bundling supplier credit with construction. Price competition intensifies in Africa, where local steel mills collaborate with OEMs to localize panel stamping, shaving logistics cost and import duties. The emerging consensus places smart, modular, and environmentally compliant silos at the center of long-term competitive advantage.

Grain Storage Silos Industry Leaders

-

Sioux Steel Company

-

Symaga, S.A.U.

-

Grain Systems Inc. (AGCO Corporation)

-

SCG Silos Grupo (Silos Cordoba Grupo)

-

Brock Grain Systems (CTB Inc. - Berkshire Hathaway)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: China raised its 2025 grain-stockpiling budget to bolster domestic output and storage capacity.

- March 2025: India scaled up the cooperative grain storage plan after pilot success, selecting 500 additional local societies for storage capacity rollout.

- November 2024: United States Department of Agriculture unveiled the USD 140 million Commodity Storage Assistance Program to help producers rebuild bins damaged by hurricanes.

- January 2024: The Port of New Orleans secured a USD 226.2 million federal grant for the USD 1.8 billion Louisiana International Terminal, incorporating large-scale grain silos.

Global Grain Storage Silos Market Report Scope

A grain storage silo is a structure used to store grain in bulk for the agriculture industry. The grain storage silos market is an important segment of the grain storage facility industry, which boosts the agricultural output supply when needed. The Grain Storage Silos Market is segmented by type (steel silos, metal silos, and other types), product (flat bottom silos, hopper bottom silos, feed hoppers, and farm silos), and geography (North America, Europe, Asia-Pacific, South America, and Middle-East and Africa). The report offers market size and forecast value in (USD) for all the above segments.

| Steel Silos |

| Concrete Silos |

| Metal Silos |

| Other Materials |

| Flat-Bottom Silos |

| Hopper-Bottom Silos |

| Square/Rectangular Silos |

| Feed Hoppers |

| Farm Silos |

| Corn |

| Wheat |

| Soybean |

| Rice |

| Barley and Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Material Type | Steel Silos | |

| Concrete Silos | ||

| Metal Silos | ||

| Other Materials | ||

| By Product Design | Flat-Bottom Silos | |

| Hopper-Bottom Silos | ||

| Square/Rectangular Silos | ||

| Feed Hoppers | ||

| Farm Silos | ||

| By Grain Type | Corn | |

| Wheat | ||

| Soybean | ||

| Rice | ||

| Barley and Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the grain storage silos market in 2026?

The grain storage silos market size is USD 1.68 billion in 2026 and is forecast to reach USD 2.18 billion by 2031 at a 5.3% CAGR.

Which material dominates silo construction today?

Steel retains leadership with 77.65% 2025 revenue, owing to durability and standardized production.

What region is growing fastest for new silo installations?

Africa is projected to expand at a 6.08% CAGR through 2031 because of post-harvest loss reduction programs.

Why are IoT sensors becoming standard in new silos?

Connected monitoring cuts unplanned downtime by roughly USD 320,000 per facility each year through predictive aeration.

Page last updated on: