Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

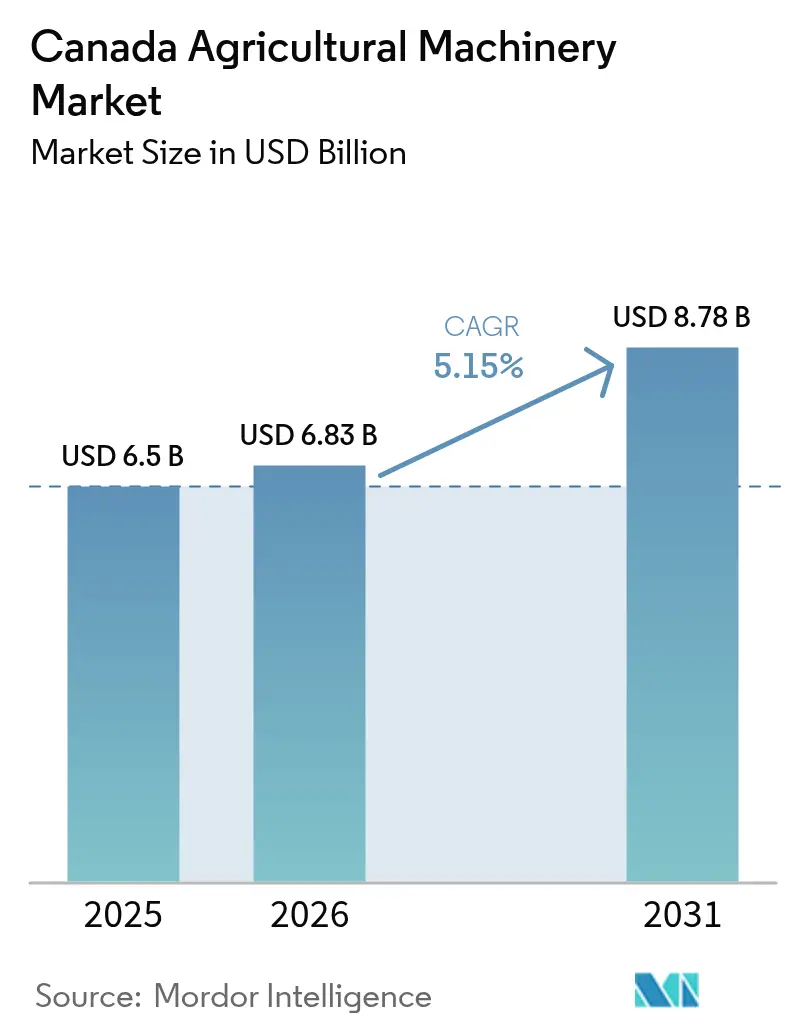

| Base Year Market Size (2025) | USD 6.50 Billion |

| Market Size (2026) | USD 6.83 Billion |

| Market Size (2031) | USD 8.78 Billion |

| Growth Rate (2026 - 2031) | 5.15% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Agricultural Machinery Market Analysis by Mordor Intelligence

The Canada agricultural machinery market size is expected to grow from USD 6.50 billion in 2025 to USD 6.83 billion in 2026 and is forecast to reach USD 8.78 billion by 2031 at 5.15% CAGR over 2026-2031. Structural labor shortages, the USD 3.5 billion Sustainable Canadian Agricultural Partnership, and accelerating uptake of precision technologies have created a resilient demand foundation despite financing headwinds. Farmers are replacing human labor with autonomous and semi-autonomous machines while simultaneously modernizing fleets to capitalize on carbon-credit incentives and water-efficient irrigation systems. Competitive intensity has risen as digital-first newcomers pressure incumbent Original Equipment Manufacturers (OEMs), leading to faster product cycles, retrofit solutions, and integrated hardware-software offerings. These dynamics underpin a steady expansion path for the Canada agricultural machinery market, particularly in Western provinces where large-scale grain operations and supportive policy frameworks converge.

Key Report Takeaways

- By product type, tractors accounted for 44.55% of the Canada agricultural machinery market share in 2025, while irrigation machinery is advancing at a 5.68% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Agricultural Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of agricultural labor | +1.2% | National, with highest impact in Alberta and Saskatchewan | Medium term (2-4 years) |

| Government subsidies and tax incentives for mechanization | +0.9% | National, with enhanced support in Ontario and Quebec | Short term (≤ 2 years) |

| Technological advancements in precision and autonomous machinery | +1.1% | National, with early adoption in Prairie provinces | Long term (≥ 4 years) |

| Aging tractor fleet replacement cycle | +0.8% | National, with concentration in established farming regions | Medium term (2-4 years) |

| Diversification toward multi-crop systems increasing demand for versatile implements | +0.7% | Prairie provinces and Ontario | Medium term (2-4 years) |

| Carbon-credit monetization propelling low-emission equipment adoption | +0.5% | National, with emphasis on livestock-intensive regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of Agricultural Labor

Canada’s farm labor gap is forecast to hit 113,800 positions by 2025 and 123,000 by 2030, forcing producers to invest in autonomous tractors, robotic harvesters, and remote-operation platforms. Temporary foreign workers already cover roughly 75% of seasonal needs, yet elevated turnover and rising wage expectations persist[1]Source: The Conference Board of Canada, “Sowing the Seeds of Growth: Temporary Foreign Workers in Agriculture,” CFA-FCA.CA. OEMs (Original Equipment Manufacturers) such as Deere & Company and AGCO Corporation are fast-tracking autonomous retrofit kits and full-electric self-driving tractors aimed at commercial launch by 2026. Larger machines that cover more acres per hour now command premium pricing as operators seek to maximize output per remaining worker. As a result, mid-range horsepower segments are stagnating while high-horsepower and specialty robotics segments capture incremental Canada agricultural machinery market demand.

Government Subsidies and Tax Incentives for Mechanization

Federal and provincial grants cover up to 50% of eligible equipment costs under the Agricultural Clean Technology Program, with awards ranging from USD 25,000 to USD 2 million[2]Source: Government of Canada, “Agricultural Clean Technology Program,” CANADA.CA. British Columbia tops provincial support with a 65% cost-share on technology purchases up to USD 100,000, accelerating small-farm modernization. The Sustainable Canadian Agricultural Partnership injects USD 3.5 billion into competitiveness initiatives over five years, directly subsidizing precision sprayers, low-emission tractors, and smart irrigation pivot retrofits. Interest-free advances up to USD 250,000 under the Advance Payments Program further soften financing costs, particularly for grain growers facing volatile commodity cycles. Subsidy stacking creates a multiplier effect on private capital, prompting a near-term spike in Canada agricultural machinery market orders ahead of funding windows.

Technological Advancements in Precision and Autonomous Machinery

More than 50.4% of Canadian farms already deploy at least one precision feature, such as GPS guidance or variable-rate application, and adoption is rising fastest among Prairie grain operations. Olds College runs Canada’s first on-farm autonomous equipment test bed, proving commercial viability for driverless platforms in harsh climates. OEMs address connectivity gaps by integrating satellite-based IoT modules that minimize data latency and enable over-the-air software updates. These enablers translate into expanding Canada agricultural machinery market revenue streams rooted in subscription analytics, remote diagnostics, and autonomy-as-a-service models.

Aging Tractor Fleet Replacement Cycle

The average workhorse tractor in Canada now exceeds 12 years of service, with replacement intervals lengthening amid high capital costs. Deferred purchases have inflated the used-equipment pool’s average listing age to a decade, while OEM order backlogs for new high-horsepower units stretch 12 to 15 months. Manufacturers respond with factory-approved retrofit kits that retrofit auto-steer, telematics, and partial autonomy onto legacy units, extending economic life spans at a fraction of the cost of new equipment. Economic depreciation studies show high-horsepower tractors deliver optimal ROI when replaced every 8 years, creating pent-up demand that could unlock a strong replacement wave once interest rates ease. This dynamic supports the service and parts side of the Canada agricultural machinery market even during new-unit downturns.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront procurement and maintenance cost | -0.8% | National, with greater impact on smaller operations | Short term (≤ 2 years) |

| Security and data-privacy risks in connected machinery | -0.4% | National, with concentration in precision agriculture adopters | Medium term (2-4 years) |

| Rising interest rates constraining equipment financing | -0.9% | National, with particular impact on debt-financed purchases | Short term (≤ 2 years) |

| Tariff volatility on U.S.-sourced components | -0.6% | National, with emphasis on import-dependent manufacturers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Procurement and Maintenance Cost

Large self-propelled machines now list between USD 400,000 and USD 1.2 million, while annual maintenance can consume up to 20% of operating budgets[3]Source: Agriculture.com, “Interest Rates and Equipment Prices: the Case for Leasing Farm Equipment,” AGRICULTURE.COM. Farmers increasingly scour auction sites for late-model equipment, but competition from U.S. buyers inflates bids, narrowing domestic supply. Software subscriptions for precision platforms add recurring expenses, pressing smaller growers to consider cooperative ownership or equipment-as-a-service agreements. Despite OEM extended-warranty offerings, cash-strapped operators continue delaying purchases, tempering near-term Canada agricultural machinery market growth.

Security and Data-Privacy Risks in Connected Machinery

Connected tractors transmit agronomic data via cloud platforms, exposing farms to potential cyber intrusions that could manipulate application rates or compromise proprietary yield maps. OEMs deploy encrypted networks and token-based access, yet liability remains ambiguous under Canadian privacy statutes, deterring certain growers from adopting telematics. Integration with third-party analytics multiplies attack surfaces, prompting insurers to demand robust cyber-hygiene practices or levy higher premiums. Until federal standards clarify data ownership and breach responsibility, precision machinery adoption may lag among risk-averse operators within the Canada agricultural machinery market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tractors Retain Core Position as Irrigation Accelerates

Tractors generated 44.55% of the Canada agricultural machinery market share in 2025, reflecting their indispensable role across row-crop, forage, and specialty operations. High-horsepower categories (≥ 100 HP) experienced a 4.3% annual demand uptick, driven by farm consolidation, autonomous retrofits, and labor substitution needs. In contrast, mid-range 40-99 HP sales dipped 6% as cash constraints led operators to extend service life rather than upgrade mid-class units.

Irrigation machinery represents the fastest-growing segment with a 5.68% CAGR. Drip systems gain traction in specialty crops across British Columbia and Ontario, while variable-rate pivots spread through Prairie grain farms seeking precise soil-moisture management. Water-use regulations and climate risk adaptation drive demand for soil-sensor networks that integrate with pivot controllers, creating cross-sell opportunities with agronomic software vendors. OEMs differentiate through energy-efficient pumps, remote fault detection, and modular add-ons that retrofit existing pivots. These advances attract government rebates aimed at water conservation, further catalyzing irrigation sales inside the Canada agricultural machinery market.

Geography Analysis

Alberta anchors the Canada agricultural machinery market with significant operating revenue of the national total. Large grain and oilseed enterprises dominate procurement, prioritizing high-horsepower tractors, combines, and precision sprayers that optimize broad-acre productivity. Auto-steer adoption exceeds 80% among Alberta operations, and drone-based scouting is becoming mainstream. This innovation mindset positions the province at the forefront of autonomy pilots and electric-drive retrofits, sustaining demand for advanced machinery despite cyclical commodity swings.

Saskatchewan and Manitoba form the second demand tier, collectively generating nearly half of the national wheat and canola output. Their extensive cropland underpins steady replacement cycles for tractors and air seeders. Conservation tillage covers more than 75% of Prairie acreage, encouraging investment in no-till drills equipped with sectional control and seed-population sensors. Dealers in these provinces emphasize robust service networks to support long-distance customers and maintain uptime during compressed planting windows, driving healthy parts revenue even in downturns.

Ontario showcases a highly diversified agricultural structure spanning cash crops, dairy, poultry, and intensive horticulture. Smaller field sizes and higher land values tilt purchasing toward versatile mid-horsepower tractors, self-propelled forage harvesters, and specialized implements. The province leads renewable-energy adoption on farms, installing rooftop solar panels that power electric irrigation pumps and barn automation systems.

Competitive Landscape

The Canada agricultural machinery market features moderate concentration. Global majors Deere & Company, CNH Industrial N.V., and AGCO Corporation dominate high-horsepower segments, leveraging extensive dealer networks and integrated telematics ecosystems. Mid-tier firms such as Kubota Corporation and Claas KGaA mbH carve out shares in specialty and compact tractor classes, whereas domestic implement manufacturers compete on niche functionality and localized agronomic knowledge.

Competitive dynamics have intensified as technology companies enter with cloud-based analytics and autonomy solutions. Brilliant Harvest’s AI-powered efficiency platform integrates seamlessly with multiple equipment brands, prompting OEMs to enhance open-API capabilities. Strategic acquisitions highlight a pivot toward vertical integration; Linamar’s purchase of Bourgault adds seeding expertise, while AGCO Corporation’s OutRun retrofit kit expands its aftermarket footprint.

Dealer consolidation continues, with multi-store groups improving service coverage and financing options, raising entry barriers for smaller OEMs. Growing customer expectation for bundled solutions equipment, software, agronomic advice, and financing pushes manufacturers to build end-to-end platforms. As autonomy matures, hardware margins may compress, shifting profit pools toward data services and predictive maintenance. The Canada agricultural machinery market is therefore evolving into an ecosystem play, rewarding players that couple reliable iron with seamless digital experiences.

Canada Agricultural Machinery Industry Leaders

Deere & Company

CLAAS KGaA mbH

AGCO Corporation

Kubota Corporation

CNH Industrial N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Farm Credit Canada announced a USD 2 billion commitment through 2030 to accelerate agtech innovation, signaling institutional confidence in technology-driven machinery demand.

- May 2025: Ag Growth International issued USD 75 million in unsecured debentures to fund global expansion, reaffirming a 2025 EBITDA outlook of at least USD 225 million.

- April 2025: AGCO expanded its dealer footprint with Carter Agri-Systems in Utah and Delta Ag Equipment’s launch of Mississippi’s first full-line Fendt and Massey Ferguson outlet, enhancing market access for advanced machinery.

Canada Agricultural Machinery Market Report Scope

Agricultural machinery relates to the devices and mechanical structures used in farming or other agriculture. For this report, the machinery used in agricultural operations has been considered. The report does not cover machinery used for industrial and construction purposes or multi-purpose tractors, machinery, and equipment used for both agricultural and non-agricultural operations.

The Canada Agricultural Machinery Market is segmented by Type into Tractors (Less than 40 HP, 40 HP to 99 HP, and Greater than 100 HP), Ploughing and Cultivating Machinery (Plows, Harrows, Rotavators and Cultivators, and Other Equipment), Planting Machinery (Seed Drills, Planters, Spreaders, and Other Planting Machinery), Sprayers, Irrigation Machinery (Drip Irrigation, Sprinkler Irrigation, and Other Irrigation Machinery), Harvesting Machinery (Combine Harvesters and Other Harvesting Machinery), Haying and Forage Machinery (Mowers and Conditioners, Balers, and Other Haying and Forage Machinery), and Other Types. The report offers the market size and forecasts for agricultural machinery in value (USD) for all the above segments.

By Product Type

| Tractors | Less than 40 HP |

| 40-99 HP | |

| More than 100 HP | |

| Plowing and Cultivating Machinery | Plows |

| Harrows | |

| Rotovators and Cultivators | |

| Other Equipment | |

| Planting Machinery | Seed Drills |

| Planters | |

| Spreaders | |

| Other Planting Machinery | |

| Sprayers | |

| Irrigation Machinery | Drip Irrigation Systems |

| Sprinkler Irrigation Systems | |

| Other Irrigation Machinery | |

| Harvesting Machinery | Combine Harvesters |

| Other Harvesting Machinery | |

| Haying and Forage Machinery | Mowers and Conditioners |

| Balers | |

| Other Haying and Forage Machinery | |

| Other Types |

| By Product Type | Tractors | Less than 40 HP |

| 40-99 HP | ||

| More than 100 HP | ||

| Plowing and Cultivating Machinery | Plows | |

| Harrows | ||

| Rotovators and Cultivators | ||

| Other Equipment | ||

| Planting Machinery | Seed Drills | |

| Planters | ||

| Spreaders | ||

| Other Planting Machinery | ||

| Sprayers | ||

| Irrigation Machinery | Drip Irrigation Systems | |

| Sprinkler Irrigation Systems | ||

| Other Irrigation Machinery | ||

| Harvesting Machinery | Combine Harvesters | |

| Other Harvesting Machinery | ||

| Haying and Forage Machinery | Mowers and Conditioners | |

| Balers | ||

| Other Haying and Forage Machinery | ||

| Other Types | ||

Key Questions Answered in the Report

How large is the Canadian agricultural equipment market in 2026?

The Canadian agricultural equipment market size is USD 6.83 billion in 2026.

What is the forecast CAGR for Canadian agricultural equipment through 2031?

Market value is projected to grow at a 5.15% CAGR from 2026 to 2031.

Which segment leads current sales?

Tractors command 44.55% of 2025 Canadian agricultural equipment market share.

Which product category is growing fastest?

Irrigation machinery is advancing at a 5.68% CAGR through 2031.

How does labor scarcity affect equipment demand?

Acute worker shortages push producers toward autonomous and semi-autonomous machinery, accelerating modernization plans.

Page last updated on: