Grain Protectants Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 1.40 Billion |

| Market Size (2030) | USD 1.86 Billion |

| Growth Rate (2025 - 2030) | 5.80% CAGR |

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

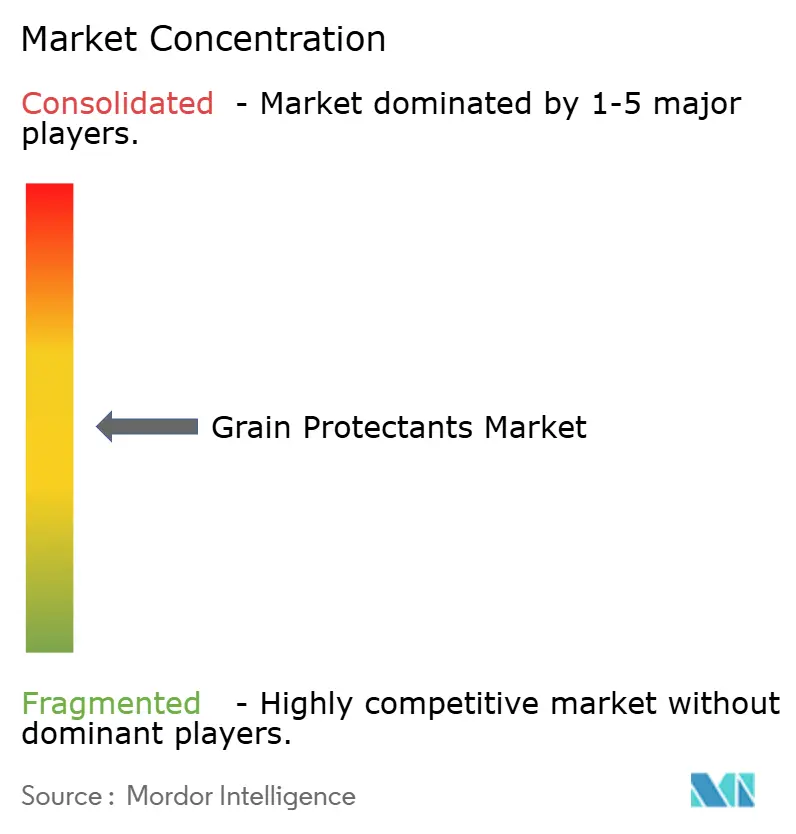

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Grain Protectants Market Analysis by Mordor Intelligence

The grain protectants market size is estimated at USD 1.40 billion in 2025 and is projected to reach USD 1.86 billion by 2030, growing at a 5.8% CAGR from 2025 to 2030. Escalating post-harvest losses, climate-linked food security mandates, and rising investment in modern storage infrastructure keep demand resilient. Tightened residue regulations, rapid adoption of AI in silo monitoring, and accelerated registration of low-toxicity actives collectively reshape product portfolios. Competitive dynamics hinge on how quickly incumbent chemical suppliers adapt to biological solutions, while technology firms integrate predictive analytics into their storage operations. The Asia-Pacific’s infrastructure boom, Africa’s climate adaptation programs, and regulatory activism in Europe and North America are defining the most influential regional growth vectors.

Key Report Takeaways

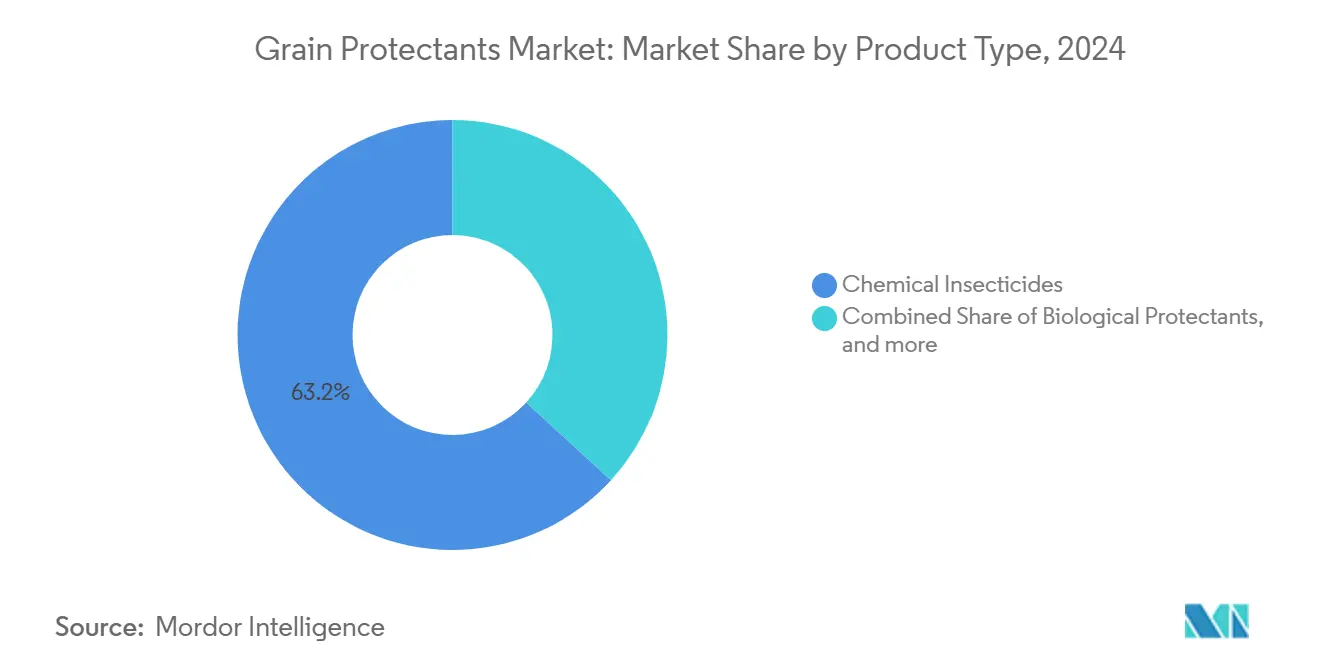

- By product type, chemical insecticides led with 63.2% revenue share in 2024, whereas biological protectants are projected to grow at a 12.4% CAGR to 2030.

- By grain type, wheat held 30.4% of the grain protectants market share in 2024, while rice is forecast to expand at a 7.5% CAGR through 2030.

- By application method, fumigation commanded a 45.7% share of the grain protectants market in 2024; grain coating is forecasted to grow at a 9.1% CAGR from 2025 to 2030.

- By end user, commercial grain storage facilities accounted for a 41.5% share of the grain protectants market size in 2024, with food processing companies projected to register an 8.6% CAGR to 2030.

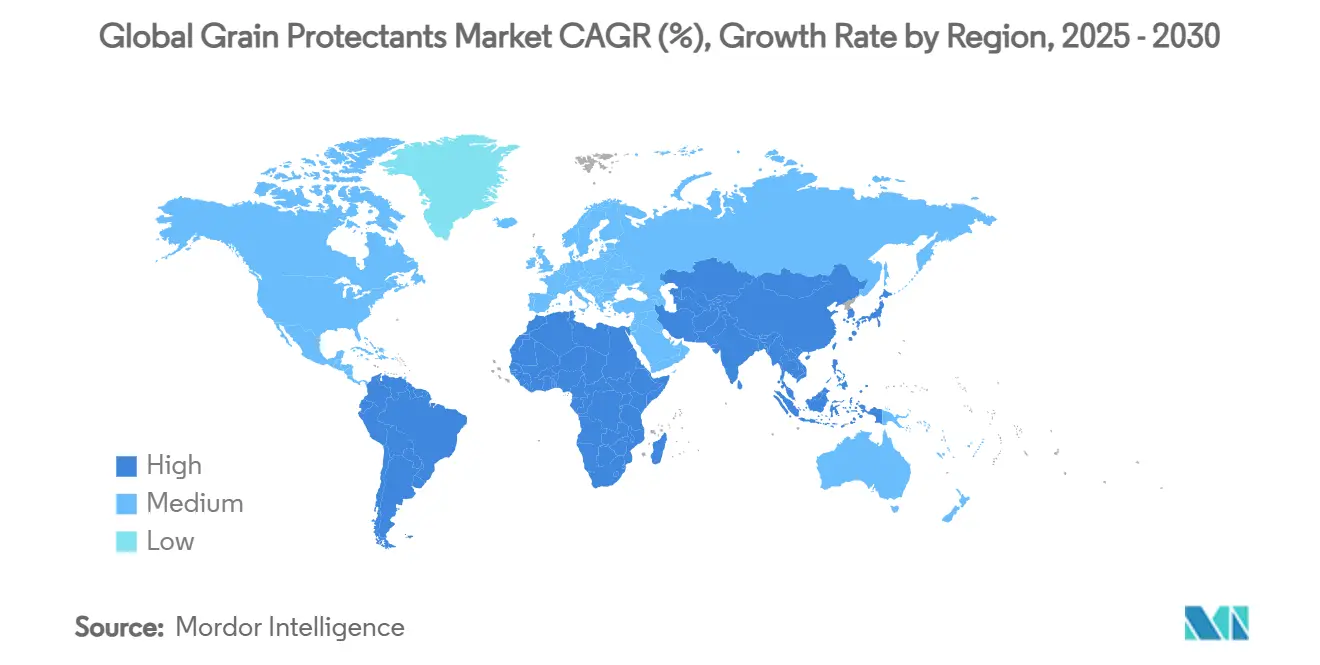

- By geography, the Asia-Pacific region is the largest, occupying 34% of the grain protectants market size in 2024. Meanwhile, Africa is growing faster, with a CAGR of 7.6% during the forecast period.

- Bayer AG, BASF SE, Corteva Agriscience, Syngenta AG, and FMC Corporation together controlled a significant market share of 52% in the grain protectants market size in 2024, underscoring moderate market concentration.

Global Grain Protectants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate-linked post-harvest losses reduction mandates | +1.2% | Asia-Pacific and Africa highest | Medium term (2-4 years) |

| Expansion of bulk grain trade corridors | +1.5% | Asia-Pacific, Middle East, and Africa | Long term (≥ 4 years) |

| Rising fungicide-resistant pest strains | +0.8% | North America and Europe acute | Short term (≤ 2 years) |

| Shift toward residue-free biological protectants | +0.9% | North America and Europe leading | Medium term (2-4 years) |

| AI-enabled silo condition monitoring integration | +0.7% | North America and Europe early | Long term (≥ 4 years) |

| Accelerated registration of low-toxicity actives | +0.6% | Developed markets fastest | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Climate-Linked Post-Harvest Losses Reduction Mandates

National food security programs require advanced grain protection systems, as temperature and humidity variations affect traditional storage methods. Regulatory frameworks, including the European Union's Farm to Fork Strategy, which aims to reduce pesticide use by 50% by 2030, are promoting the adoption of low-dose, high-efficacy protectants that perform effectively across temperatures ranging from 15 °C to 35 °C [1]Source: European Commission, “Farm to Fork Strategy,” ec.europa.eu. These factors drive the development and implementation of new grain protection solutions designed for climate-stressed storage conditions. India’s mandatory grain storage insurance scheme ties coverage to certified protectant use, effectively institutionalizing demand. Parallel initiatives in Sub-Saharan Africa push storage operators toward technologies capable of sustaining multi-year reserves.

Expansion of Bulk Grain Trade Corridors

Large-scale logistics upgrades lengthen storage windows between farm and processing, raising the bar for long-acting protectants. Egypt’s USD 153 million Suez Canal grain hub now requires multi-mode treatments that remain potent during extended port dwell times [2]Source: Egyptian Ministry of Supply, “Suez Canal Grain Facility Expansion,” supply.gov.eg. The China-Russia corridor handles more than 5 million metric tons annually, exposing cargoes to divergent climates that favor combination chemical-biological regimens for sustained efficacy. Similar corridor expansions bridging African growers with Middle Eastern buyers underpin steady demand for advanced formulations.

Rising Fungicide-Resistant Pest Strains

The evolution of pest resistance is driving increased adoption of multi-mode protectant systems, as single-active ingredient formulations become less effective against adapted insect populations. Research in the Journal of Stored Products Research shows that Sitophilus zeamais populations have developed significant resistance to organophosphate treatments, with resistance ratios exceeding 10-fold in certain regions. This resistance development has increased the demand for combination products that incorporate different modes of action, enabling manufacturers to command premium prices for products with proven long-term effectiveness. The resistance issue is most severe in areas with continuous grain storage cycles, where pest populations face repeated exposure to identical active ingredients. Formulations containing entomopathogenic fungi, particularly Beauveria bassiana, are emerging as effective alternatives against resistant pest populations.

AI-Enabled Silo Condition Monitoring Integration

Systems such as AgroLog TMS6000 deliver real-time temperature and insect activity analytics that automate protectant dosing, trimming usage by up to 30% while improving control consistency. This integration of smart monitoring with protectant application is driving demand for technologically advanced grain protection solutions. GrainSense wireless sensors give operators moisture data every few minutes, enabling interventions before infestations escalate. Digital tools are quickly standardizing across commercial sites in the United States, Canada, Germany, and Japan.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent maximum residue level harmonization | -0.9% | Europe and North America highest | Short term (≤ 2 years) |

| Grain protectant price volatility tied to petro feedstock | -0.7% | Developing markets most exposed | Medium term (2-4 years) |

| Growing consumer pushback on chemical residues | -0.8% | Global, led by Western retail | Medium term (2-4 years) |

| Limited efficacy data for emerging biologicals | -0.6% | Global, approvals delayed | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Maximum Residue Level Harmonization

The European Union's implementation of 0.01 mg/kg maximum residue levels (MRLs) for banned pesticides has created significant market access barriers for chemical protectants. The new European Union's MRLs for fluxapyroxad, lambda-cyhalothrin, metalaxyl, and nicotine established in 2024 have eliminated several commonly used grain protectants from European markets[3]Source: European Commission, “Updated MRL List 2024,” ec.europa.eu. These regulatory changes require manufacturers to either reformulate their products or exit the market, causing supply disruptions that benefit biological alternatives while increasing market volatility. This harmonization trend is expanding globally, with countries such as China implementing similar strict standards that affect agricultural trade flows. The regulatory requirements pose specific challenges for phosphine-based fumigants, which face increased scrutiny despite their effectiveness against resistant pest strains.

Grain Protectant Price Volatility Tied to Petro Feedstock

The volatility in phosphine derivative prices, directly linked to petrochemical feedstock costs, creates margin pressure for manufacturers and end-users. The relationship between crude oil prices and phosphine production costs increases supply chain planning challenges, particularly affecting developing market customers without hedging capabilities. Geopolitical tensions impacting petrochemical supply chains further amplify this volatility, resulting in unpredictable cost structures that limit long-term protection adoption. The impact is especially significant for aluminum phosphide formulations, where raw materials account for 60-70% of production costs. The limited development of alternative feedstocks makes the market vulnerable to petroleum price fluctuations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Biological Protectants Drive Innovation Despite the Dominance of Chemical Insecticides

Chemical insecticides retained 63.2% share of the grain protectants market size in 2024, owing to proven broad-spectrum efficacy and entrenched distributor networks. Biological protectants, while smaller in absolute terms, log a robust 12.4% CAGR because residue regulations increasingly disadvantage conventional actives. Integrated pest management packages that match reduced rates of synthetic fumigants with microbial inoculants gain traction as operators seek certainty against resistant pests. Biological suppliers benefit from faster approvals and premium farm-gate prices that offset higher production costs. FMC’s tie-up with AgroSpheres in 2024 to co-develop RNA-interference solutions exemplifies strategic research and development redirection.

Second-generation chemical products pursue lower-toxicity profiles to remain permissible under tightening MRL regimes. Phosphine alternatives based on controlled-release magnesium phosphide tablets offer safer handling while preserving efficacy, but price sensitivity restrains adoption in emerging markets. As residue thresholds fall, combined biological-chemical regimens deliver the compromise many millers and exporters now demand.

By Grain Type: Wheat Dominance Challenged by Rice Growth

Wheat accounted for 30.4% of the grain protectants market size in 2024, reflecting its central role in national buffer stocks and cross-border trade. Rice, however, is pacing growth at 7.5% CAGR as Asia-Pacific exporters upgrade storage assets to meet premium import quality grades. Temperature and humidity sensitivity in paddy storage necessitate formulations that sustain activity under saturated air conditions, furthering demand for coated biological protectants. Corn continues to serve feed markets, maintaining a sizable slice of demand, particularly in Brazil and the United States. Barley and specialty grains attract targeted treatments driven by malting and niche food requirements, underscoring the diversity of application needs.

Climate change impacts on grain storage are creating differentiated demand patterns across grain types, with rice requiring specialized humidity control systems that favor biological protectants over traditional fumigation methods. Research published in the Journal of Stored Products Research indicates that rice storage faces unique challenges from temperature fluctuations that affect both pest development and protectant efficacy. Wheat's market leadership reflects its extensive global trade network and established storage protocols, while corn's growth is supported by expanding livestock feed demand in developing markets. The segmentation dynamics are shifting as climate-adapted storage systems favor protectants that maintain efficacy across broader temperature ranges.

By Application Method: Fumigation Leads While Coating Innovates

The fumigation method is projected to lead with a 45.7% share of the grain protectant market size in 2024, reflecting its established efficacy against diverse pest species and compatibility with existing storage infrastructure. Grain coating emerges as the fastest-growing application method, with a 9.1% CAGR through 2030, driven by its ability to provide targeted protection with minimal environmental impact. Spraying applications serve specific market niches where surface treatment is preferred, while dusting methods remain relevant for specialized storage conditions. The application method segmentation reflects the industry's evolution toward precision treatment approaches that optimize protectant efficacy while minimizing usage volumes.

CaptSystems' introduction of PhosCapt-MP fumigation technology demonstrates the segment's innovation in improving gas distribution and enhancing safety protocols. This technological advancement addresses traditional fumigation challenges while maintaining the method's broad-spectrum efficacy advantages. Grain coating technologies are benefiting from advances in polymer science, which enable controlled-release formulations, providing extended protection periods that reduce the frequency of applications. The method's growth is supported by regulatory preferences for targeted application approaches that minimize environmental exposure while maintaining pest control efficacy.

By End User: Commercial Grain Storage Facilities Lead Infrastructure Modernization

Commercial grain storage facilities dominate the grain protectant market with 41.5% share in 2024, reflecting the industry's consolidation toward centralized, technology-enabled storage systems. Food processing companies represent the fastest-growing end-user segment at 8.6% CAGR through 2030, driven by vertical integration strategies and quality control requirements. Farmers and on-farm storage maintain significant market presence despite infrastructure limitations, while government reserve agencies represent a specialized but important segment with distinct preservation requirements. The end-user segmentation reflects the grain storage industry's evolution toward professional management and technology integration.

Food processing companies are driving demand for residue-free protectants as they implement zero-tolerance policies for chemical residues in raw materials. Government reserve agencies are modernizing storage protocols to meet climate-resilient food security objectives, creating demand for protectants that maintain efficacy under variable environmental conditions. The segmentation trend toward professional storage management is creating opportunities for integrated protectant systems that combine multiple preservation technologies.

Geography Analysis

The Asia-Pacific region leads the grain protectants market, accounting for a 34% revenue share in 2024, driven by substantial infrastructure investments and the expansion of grain storage capacity across the region. China's grain reserve modernization program and India's post-harvest infrastructure investments, exceeding USD 5 billion annually, are creating substantial demand for advanced protection systems. The region reflects rapid economic development and growing awareness of food security among governments. Japan and Australia contribute to market growth through technology adoption and quality standards that favor premium protectant solutions. The region's growth is supported by the expansion of grain trade corridors connecting production areas to consumption centers, requiring extended storage capabilities that exceed traditional preservation methods.

Africa emerges as the fastest-growing regional market at 7.6% CAGR through 2030, driven by infrastructure development and climate adaptation initiatives that prioritize post-harvest loss reduction. The continent's grain storage challenges, where losses can reach 40% in some regions, create urgent demand for effective protectant solutions.

South America is experiencing significant growth, driven by Brazil’s robust export pipeline and the nation’s USD 780 million biopesticide market, which normalizes microbial formulations in bulk cereals. North America and Europe, although mature, provide fertile ground for AI and low-residue innovations driven by regulatory and retail influence. The European Commission’s strict MRL enforcements create blueprint standards emulated in other continents. Strategic grain corridor expansions and national food security programs in the United Arab Emirates and Saudi Arabia are projected to drive the Middle East market during the forecast period.

Competitive Landscape

The grain protectants market remains moderately concentrated, with five companies, such as Bayer AG, Syngenta Group, BASF SE, Corteva Agriscience, and FMC Corporation, holding a market share of 52% in 2024. Bayer AG and Syngenta Group maintain their market positions through extensive global registration capabilities and diverse product portfolios. However, stricter regulations on phosphine and organophosphates have driven these companies to pursue acquisitions and expand into biological solutions and new formulations. FMC Corporation sold its Global Specialty Solutions division in 2024 for USD 350 million to increase investment in RNAi-based bioinsecticide research and development. Central Life Sciences introduced Gravista-D, a ready-to-use product combining insect growth regulator and adulticide components. BASF SE and Corteva Agriscience have strengthened their product offerings through investments in controlled-release technologies and microbial alternatives.

New market entrants are challenging established companies by incorporating biotechnology and artificial intelligence into their products and services. Sumitomo Chemical Co., Ltd acquired a fungal biopesticide license in 2023 to achieve its target of 20-25% biopesticide revenue by 2030. Agricultural technology companies are integrating sensors and analytics into fumigation systems to provide real-time pest monitoring and predictive maintenance capabilities, which grain handlers and insurers increasingly require.

Partnerships between technology companies and grain elevator operators are transforming traditional market dynamics. The industry continues to move toward integrated, sustainable, and technology-enhanced grain protection methods.

Grain Protectants Industry Leaders

BASF SE

Corteva Agriscience

FMC Corporation

Bayer AG

Syngenta Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Central Life Sciences launched “Bugs on the Move,” an educational campaign to raise awareness about stored product pests and promote integrated pest management solutions for grain storage facilities.

- May 2024: FMC Corporation and AgroSpheres have entered into a multi-year collaboration to accelerate the development of RNAi-based bioinsecticides for grain storage. This partnership aims to leverage AgroSpheres' bioencapsulation technology to enhance the stability and efficacy of RNAi molecules, thereby making them more suitable for commercial use in crop protection.

- January 2024: Central Life Sciences launched its all-new insecticide formulated for stored grains called Gravista-D. The new product is a ready-to-use solution that combines an insect growth regulator with an adulticide to kill a broad spectrum of adult insects.

Global Grain Protectants Market Report Scope

| Chemical Insecticides |

| Biological Protectants |

| Integrated Pest Management Solutions |

| Wheat |

| Corn (Maize) |

| Rice |

| Barley |

| Others (Sorghum, Oats, etc.) |

| Fumigation |

| Spraying |

| Dusting |

| Grain Coating |

| Farmers and On-farm Storage |

| Commercial Grain Storage Facilities |

| Food Processing Companies |

| Government Reserve Agencies |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | Chemical Insecticides | |

| Biological Protectants | ||

| Integrated Pest Management Solutions | ||

| By Grain Type | Wheat | |

| Corn (Maize) | ||

| Rice | ||

| Barley | ||

| Others (Sorghum, Oats, etc.) | ||

| By Application Method | Fumigation | |

| Spraying | ||

| Dusting | ||

| Grain Coating | ||

| By End User | Farmers and On-farm Storage | |

| Commercial Grain Storage Facilities | ||

| Food Processing Companies | ||

| Government Reserve Agencies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the grain protectants market?

The grain protectants market size is USD 1.40 billion in 2025 and is projected to reach USD 1.86 billion by 2030 at a 5.8% CAGR.

Which product type is growing fastest?

Biological protectants exhibit the fastest growth, expanding at a 12.4% CAGR through 2030.

Why is Asia-Pacific the largest regional market?

Massive investments in modern storage, China’s reserve modernization, and India’s USD 5 billion annual infrastructure spending drive Asia-Pacific’s 34% revenue share.

How are residue regulations affecting product demand?

Stricter maximum residue levels in Europe and North America limit some chemistries, accelerating adoption of residue-free biological alternatives.

Page last updated on: