Golf Rangefinder Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

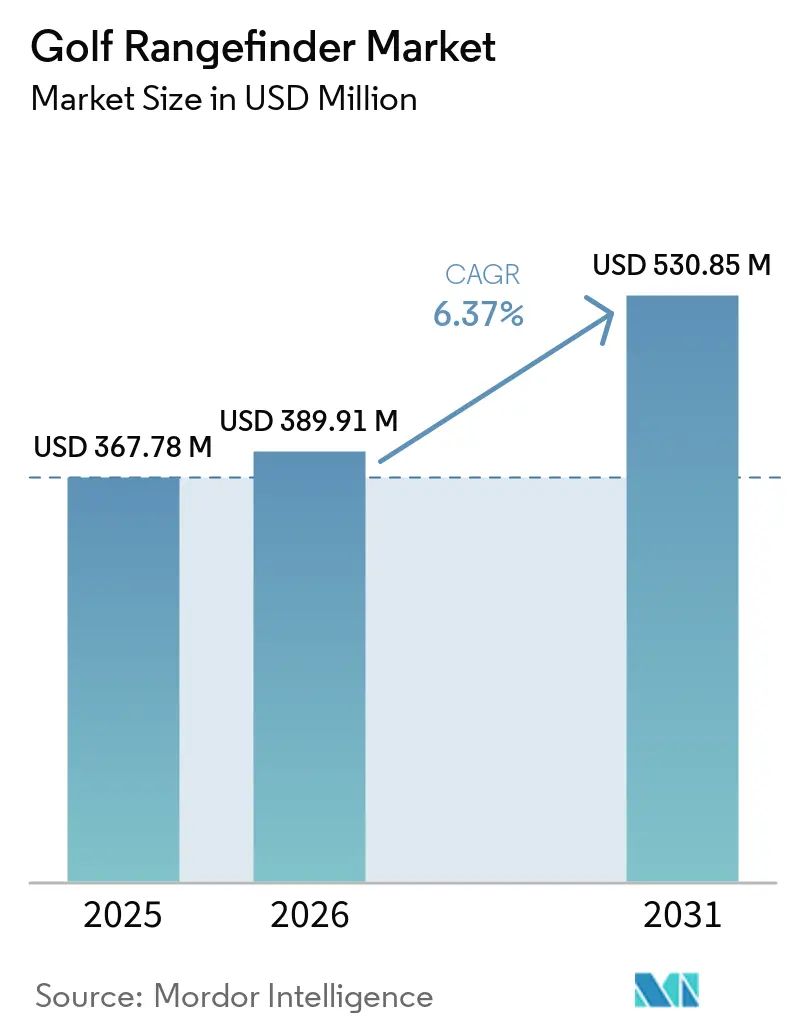

| Market Size (2026) | USD 389.91 Million |

| Market Size (2031) | USD 530.85 Million |

| Growth Rate (2026 - 2031) | 6.37% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

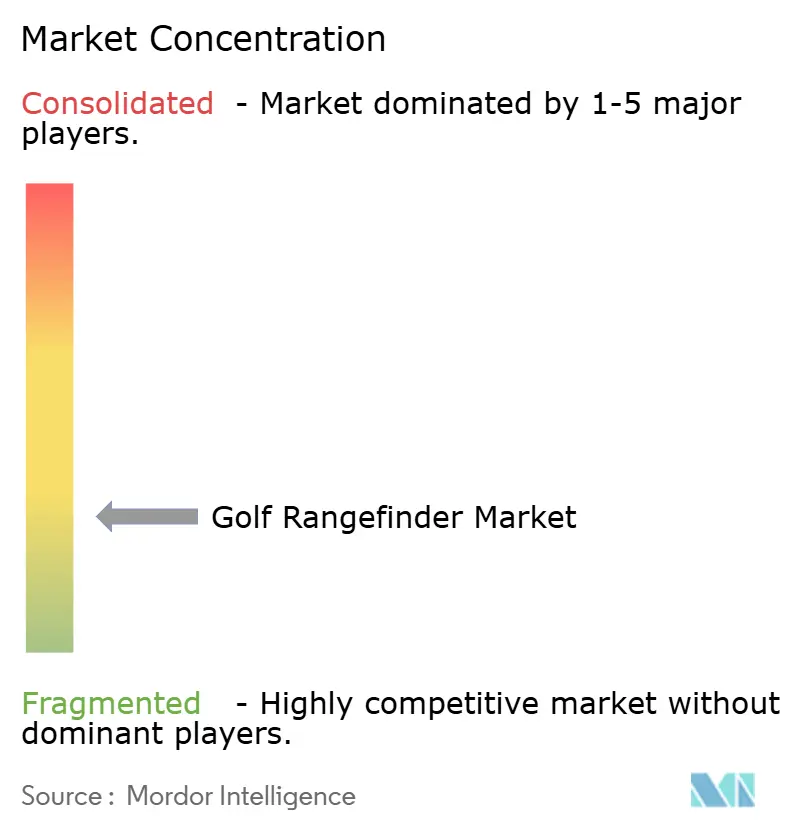

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Golf Rangefinder Market Analysis by Mordor Intelligence

The global golf rangefinder market size is expected to grow from USD 367.78 million in 2025 to USD 389.91 million in 2026 and is forecast to reach USD 530.85 million by 2031 at 6.37% CAGR over 2026-2031. The National Golf Foundation (NGF) reported a record 48.1 million golfers in the United States in 2025, underscoring a significant increase in demand for precision equipment within the global golf rangefinder market[1]Source: National Golf Foundation, "Golf Industry Facts," ngf.org. With a growing number of participants, there has been a clear shift as recreational golfers, golf clubs, and training centers increasingly recognize rangefinders as indispensable tools, resulting in an extended replacement and upgrade cycle. The market is experiencing advancements that integrate laser precision with global positioning system (GPS) functionalities. Additionally, there is a rising trend of premium product adoption, driven by lifestyle-oriented upgrades, alongside strategies that connect hardware sales to subscription-based digital service offerings. These developments position golf rangefinders as critical components of the modern, data-driven golfing ecosystem rather than mere accessories.

Key Report Takeaways

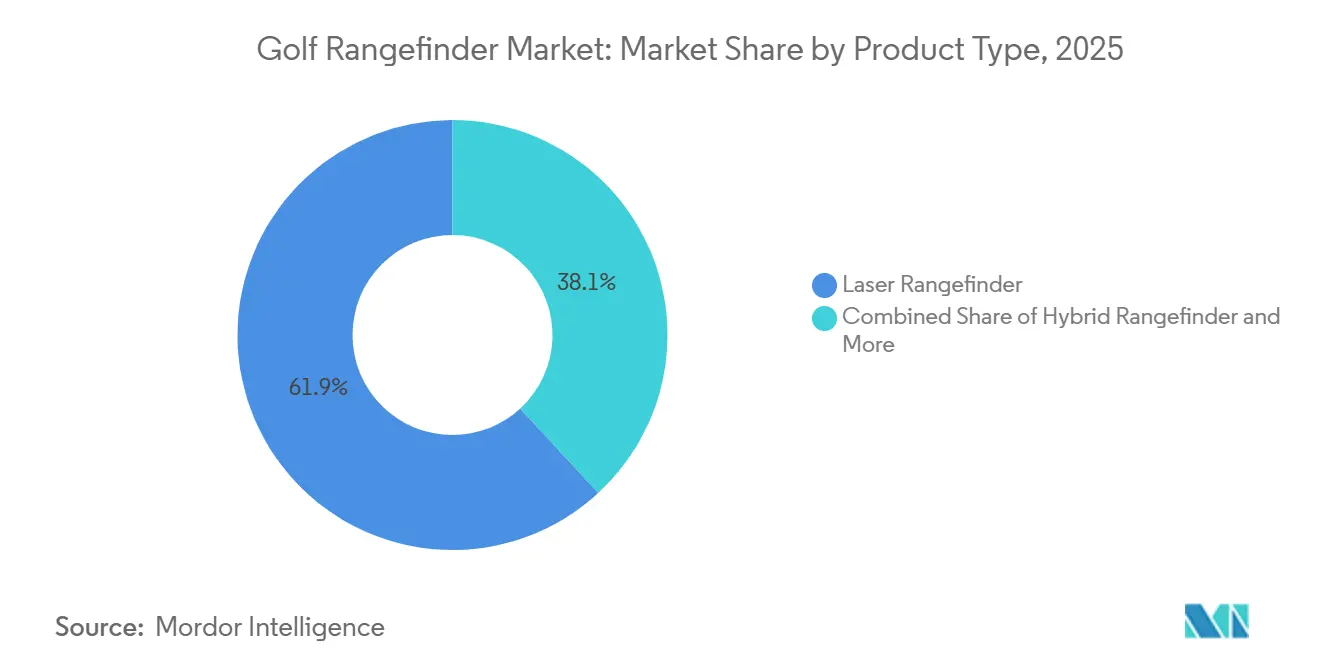

- By product type, laser rangefinders led the global golf rangefinder market with a share of 61.86% in 2025, while hybrid rangefinders are anticipated to register the fastest CAGR of 8.22% during 2026-2031.

- By category, mass retained 64.54% share in 2025, whereas premium is forecast to expand at a 7.99% CAGR through 2031.

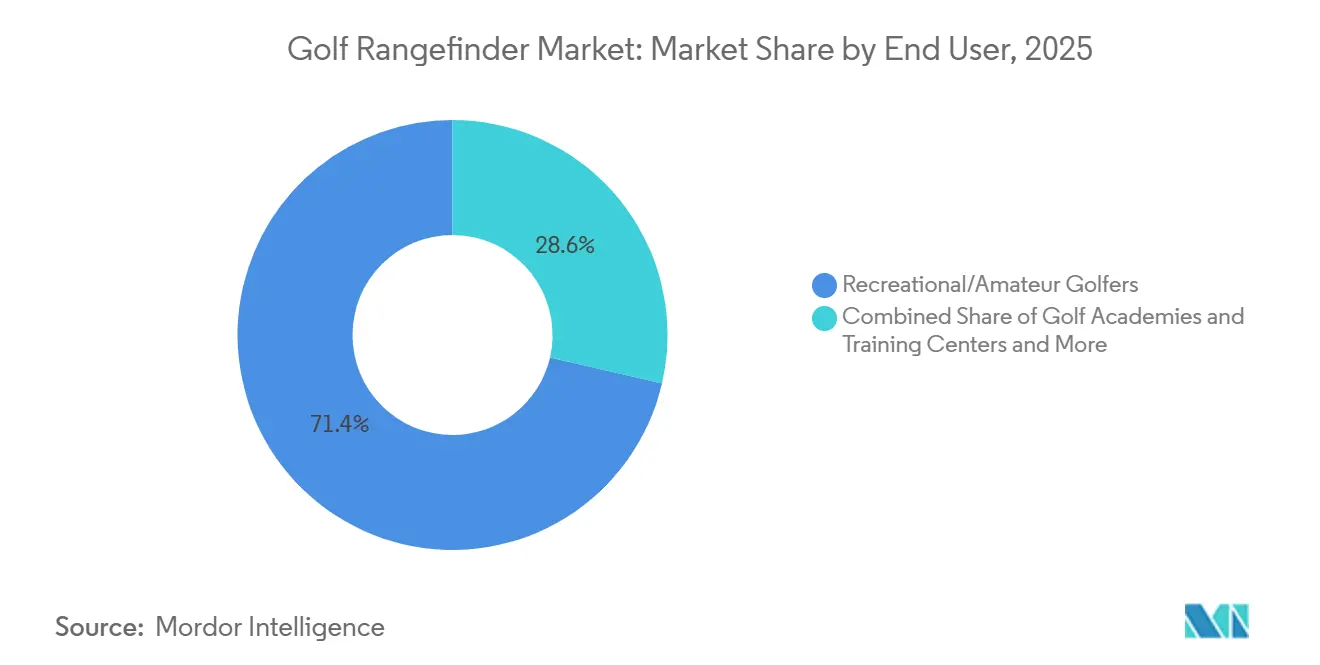

- By end user, recreational/amateur golfers held 71.37% of 2025 revenue, but golf academies and training centers are expected to grow fastest at 8.57% through 2031.

- By distribution channel, offline retail stores led the global golf rangefinder market with a share of 69.89% in 2025, while online retail stores are anticipated to register the fastest CAGR of 8.45% during 2026-2031.

- By geography, North America retained a 42.63% share in 2025, whereas Asia-Pacific is forecast to expand at a 7.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Golf Rangefinder Market Trends and Insights

Drivers Impact Table*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digitalization of golf performance tracking and course management | +1.0% | Global, strongest in North America and East Asia | Short term (≤ 2 years) |

| Rising popularity of data-driven and precision-based golf | +0.9% | North America, Europe, South Korea, Japan | Medium term (2-4 years) |

| Expanding global golf participation beyond traditional markets | +0.8% | Asia-Pacific core, spill-over to Middle East and Africa, and South America | Medium term (2-4 years) |

| Golf tourism boom stimulating equipment spending | +0.7% | North America, Europe, Asia-Pacific resort destinations | Medium term (2-4 years) |

| E-commerce platforms broadening access to golf technology | +0.6% | Global, especially Asia-Pacific and emerging markets | Short term (≤ 2 years) |

| Integration of artificial intelligence and smart features | +0.5% | North America, South Korea, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digitalization of golf performance tracking and course management

The digitalization of golf performance tracking is transforming the global golf rangefinder market, driving expectations for these devices beyond basic distance measurement. With United States golfer participation reaching a record 48.1 million in 2025, as reported by the National Golf Foundation, players are increasingly proficient in analyzing data, utilizing metrics such as shot dispersion and carry distance. Modern golf facilities are incorporating connected dashboards and real-time analytics, establishing rangefinders as critical data-collection tools within a comprehensive performance ecosystem. This development is redefining competitive standards: devices that integrate seamlessly with connected platforms and coaching systems are gaining prominence, while standalone products face the risk of becoming obsolete. For manufacturers, the strategic opportunity lies in aligning hardware innovation with software ecosystems, developing products that not only provide actionable insights but also enhance customer engagement through subscription-based models. In conclusion, the market is transitioning from hardware-centric differentiation to a framework where ecosystem connectivity and data-driven services are pivotal to sustaining long-term competitiveness.

Expanding global golf participation beyond traditional markets

Expanding global participation in golf is driving the growth of the golf rangefinder market, creating opportunities for increased adoption and upgrades of these devices. The Royal and Ancient Golf Club of St Andrews reported that by 2025, over 112 million adults and junior golfers were active worldwide, excluding the United States and Mexico, with Asia leading in adult participation[2]Source: Royal and Ancient Golf Club of St Andrews (R&A), "Junior golf growth helps drive sustained increase in global participation," randa.org. This significant growth in global interest expanded the demand pipeline for entry-level and mid-range golf devices. Additionally, the increasing participation of junior players ensured sustained long-term market growth, maintaining a steady influx of first-time buyers. For example, South Korea’s robust local ecosystem not only attracts specialist operators but also remains insulated from dominance by large conglomerates, fostering entrepreneurial innovation. Meanwhile, global brands are implementing strategic initiatives, as demonstrated by Garmin’s Approach Z10 launch in the Asia-Pacific region. Such regional product rollouts highlight a deliberate approach to balancing competitive pricing with accessibility, positioning rangefinders as essential tools in markets where golf is transitioning from a niche activity to a mainstream sport.

Golf tourism boom stimulating equipment spending

Golf tourism is driving significant growth in the global golf rangefinder market, as consumers increasingly allocate discretionary income toward premium precision equipment. As golfers navigate unfamiliar courses at popular destinations, the demand for advanced rangefinders, particularly those equipped with slope-adjusted technology and artificial intelligence (AI)-enhanced features, has risen substantially. These devices are now perceived as essential lifestyle assets rather than merely performance-enhancing tools. High-net-worth travelers, in particular, are inclined to invest in high-quality rangefinders, recognizing their value in enhancing the overall golfing experience. This trend further integrates rangefinders into the broader golf travel economy. Supporting this momentum, the Asian Golf Industry Federation reports a 41% increase in golf participation in the United States from 2019 to 2025, with the player base nearing 50 million[3]Source: Asian Golf Industry Federation, "Research Confirms Golf’s Growth Era," agif.asia. This highlights not only the sustained demand but also the structural growth of the precision equipment market.

E-commerce platforms broadening access to golf technology

As e-commerce platforms gain traction, they are not just reshaping the golf rangefinder market; they are redefining the entire landscape of brand-consumer interactions. These platforms are tightening traditional distribution margins, allowing brands to engage directly with consumers. This shift, characterized by direct-to-consumer (DTC) models and marketplace-driven discoveries, has altered the competitive landscape. It empowers challengers to offer advanced specifications at more attractive price points, sidestepping the typical green-grass retail markups. For example, devices such as Blue Tees Golf’s Captain Air and Shot Scope’s PRO L5 demonstrate how brands utilize online channels not only to sell hardware but also to integrate subscription-based ecosystems. This approach positions their rangefinders as essential performance tools and entry points into data-driven coaching services. The strategic insight is evident: in this evolving market, mastering the digital channel equates to owning the customer relationship and the invaluable performance data. This shift diminishes the dominance of traditional retail hierarchies, emphasizing long-term competitiveness rooted in connectivity and ecosystem integration over mere shelf presence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory restrictions on slope functions during competitive play | -0.5% | Global | Medium term (2-4 years) |

| Counterfeit and low-cost imported products intensifying price competition | -0.7% | Global, especially Asia-Pacific and online marketplaces | Short term (≤ 2 years) |

| Smartphone golf applications challenging dedicated device adoption | -0.4% | Global, strongest in casual/recreational segment | Medium term (2-4 years) |

| Premium price tags limiting penetration among recreational players | -0.2% | Emerging markets, Southeast Asia, Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory restrictions on slope functions during competitive play

Regulatory constraints on slope functionality present a significant challenge to the global golf rangefinder market, particularly impacting its most profitable features. Governing bodies such as the United States Golf Association (USGA) and The Royal and Ancient Golf Club of St Andrews have prohibited the use of slope-adjusted distances during tournament play. This regulation was further reinforced by the Professional Golfers' Association (PGA) Tour's 2025 device trials, which required the deactivation of slope and course-mapping features. Manufacturers now face a dual-market challenge: developing devices that cater to recreational golfers who prioritize slope data while also meeting the compliance requirements of competitive players. This dual-mode functionality increases development costs, raises the risk of accidental feature activation, and limits marketing strategies focused on slope features. Consequently, these constraints hinder seamless brand positioning across both professional and recreational market segments.

Counterfeit and low-cost imported products intensifying price competition

Counterfeit and low-cost imports are significantly restraining the global golf rangefinder market, eroding brand trust and undermining first-purchase confidence. Often sold at a fraction of the price of authentic devices, these counterfeit products compromise on accuracy and reliability. As a result, many first-time buyers form a skewed perception of the entire category, rather than just the flawed product. This misjudgment not only tarnishes the reputation of legitimate brands but also curtails genuine trials, especially in price-sensitive regions dominated by online sales. Established manufacturers face a dual challenge: safeguarding their intellectual property (IP) and convincing consumers of the precision and durability of their authentic devices. The overarching consequence is a market where trust and credibility rival innovation in importance. This reality compels brands to channel investments into anti-counterfeiting measures, consumer education, and unique value propositions, all in a bid to ensure sustained long-term growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hybrid Devices Converge Competing Formats Into a Unified Value Proposition

In 2025, laser rangefinders command a dominant 61.86% share of the global golf rangefinder market. Their market leadership is attributed to their unmatched accuracy, speed, and reliability, offering sub-yard precision and trusted pin-lock feedback. Decades of brand recognition, combined with a strong presence in professional retail channels, have established durable customer loyalty among experienced golfers. However, this mature segment faces significant challenges: innovation remains incremental, research and development costs are high, and achieving differentiation is increasingly difficult. These factors collectively constrain growth despite the segment's entrenched market position.

Conversely, hybrid rangefinders represent the fastest-growing category, with a projected CAGR of 8.22% from 2026 to 2031. By integrating Global Positioning System (GPS) visualization with laser precision, hybrid rangefinders offer a comprehensive value proposition. For example, products such as Bushnell’s Tour Hybrid and Garmin’s Approach Z10 consolidate the functionalities of multiple devices while enhancing ecosystem connectivity through smartwatch integration and real-time data transmission. This growth trajectory reflects evolving consumer preferences for convenience and interconnected performance. However, the segment faces its own set of challenges: higher engineering complexity, increased production costs, and the difficulty of balancing affordability with advanced functionality. These factors will influence the transition of hybrid rangefinders from niche adoption to mainstream relevance.

By Category: Premium Segment Bifurcation Signals AI as the Next Pricing Tier

In 2025, the mass category commanded a 64.54% share, highlighting that most buyers prioritize practicality, seeking both affordability and dependable distance measurements. This segment has seen a surge from direct-to-consumer (DTC) brands and online marketplaces, leading to reduced entry-level prices. Consequently, rangefinders are increasingly viewed as essential tools rather than luxury items. While this broad appeal drives sales volume, it also limits brand differentiation, forcing companies to compete primarily on price and minor enhancements instead of groundbreaking innovations.

On the other hand, the premium segment is witnessing the fastest growth, with a CAGR of 7.99% from 2026 to 2031. This surge is fueled by advancements like artificial intelligence (AI)-driven yardage platforms, cutting-edge display technologies, and global positioning system (GPS) integrations. Take Mileseey’s GenePro S1, for instance: it showcases how premium devices can provide weather-adjusted “play-like” distances, bridging the gap between everyday users and professional tour calculations. This segment's expansion signals a paradigm shift: premium buyers are leveraging enhanced data not just for distance measurement, but for informed shot decisions. Thus, with a focus on innovation, connectivity, and ecosystem integration, premium rangefinders are solidifying their status as the market's primary growth driver.

By End User: Golf Academies and Training Centers Shift Procurement Toward Institutional Formats

In 2025, recreational and amateur golfers dominated the global golf rangefinder market, accounting for 71.37% of demand. This trend aligns with broader participation patterns in the sport, as many players adopt these devices to enhance their accuracy and overall performance on the course. Golf clubs and courses contribute to this segment by procuring rangefinders for rental fleets and instructional programs, with a focus on durability and standardized specifications. While this ensures consistent demand, it also limits innovation opportunities. The majority of purchases prioritize basic functionality over advanced features, restricting brands' ability to differentiate within this key segment.

Golf academies and training centers represent the fastest-growing end-user category, with a CAGR of 8.57% projected from 2026 to 2031. This growth is driven by the global expansion of technology-driven coaching environments. Institutions such as GOLFZON Leadbetter and TrackMan installations exemplify how structured lesson programs and integrated data-driven training environments incorporate precision measurement into standardized coaching frameworks. This shift in institutional procurement highlights a structural transformation in the market: rangefinders are increasingly being purchased not only by individual golfers but also by academies and training centers. These organizations demand fleet-level durability, seamless ecosystem integration, and scalable pricing models. As a result, this segment is redefining demand dynamics, positioning business-to-business (B2B) procurement as a critical growth driver for the industry.

By Distribution Channel: DTC Ecosystems Accelerate Online Channel Displacement of Traditional Retail

In 2025, offline retail stores command a dominant 69.89% share of the global golf rangefinder market. Consumers' preference for hands-on evaluation of optical products, combined with the expertise provided by trained retail staff, significantly influences purchasing decisions. Green-grass professional shops hold particular importance for professional and club-level golfers, who prioritize proximity and fitting expertise. While this well-established presence reinforces offline retail's dominance, its reliance on traditional sales models limits operational flexibility and exposes it to margin compression, particularly as digital alternatives continue to gain momentum.

On the other hand, online retail is the fastest-growing distribution channel, achieving a CAGR of 8.45% from 2026 to 2031. This growth is driven by direct-to-consumer ecosystems and subscription-based business models. Digital competitors such as Blue Tees Golf and Shot Scope are transforming online platforms from simple sales outlets into comprehensive gateways for connected performance ecosystems. In these ecosystems, devices function as entry points to advanced analytics and coaching services. This evolving "device-as-a-service" model is fundamentally reshaping distribution economics, disrupting brand hierarchies that have been established over decades in traditional retail, and accelerating the transition toward digital-first engagement. For manufacturers, the online channel represents not only a significant growth opportunity but also a strategic imperative, as owning the digital customer relationship increasingly determines long-term competitiveness.

Geography Analysis

In 2025, North America commands the largest share of the golf rangefinder market, boasting a 42.63% stake. This dominance is largely driven by the United States, which, with over 16,000 golf facilities as of 2025, according to National Golf Foundation, sees consistent demand for replacements and upgrades, fueled by a growing participant base. Major brands like Bushnell, Garmin, Blue Tees, and Shot Scope vie for prominence in the region, pouring resources into pro-shop visibility, forging ties with the Professional Golfers' Association (PGA), and strategically positioning themselves in the marketplace. Furthermore, the United States Golf Association's (USGA) regulatory standards not only influence product design but also shape marketing narratives, cementing North America's status as the benchmark for global distribution strategies.

Asia-Pacific is on a rapid ascent, projected to grow at a CAGR of 7.86% from 2026 to 2031, marking it as the region with the most pronounced medium-term growth potential. Countries like Japan, South Korea, China, India, and nations in Southeast Asia are witnessing a surge in golf participation, spurring demand for both high-end and competitively priced devices. While domestic brands like CaddyTalk and Voice Caddie flourish in these tech-savvy markets, global giants like Garmin are strategically launching products, keeping regional price sensitivities in mind. This indicates that the Asia-Pacific market demands a nuanced competitive approach, rather than a one-size-fits-all premium strategy. The region's burgeoning golf infrastructure, coupled with rising disposable incomes and a youthful demographic increasingly taking to the greens, solidifies its position as a key driver of future demand.

Europe stands as the second-largest market, with Germany, the United Kingdom, the Netherlands, and France leading in volume. The continent enjoys robust participation from both adults and juniors, bolstering demand for entry-level and mid-range products. Notably, compliance standards established in the United Kingdom are influencing retail norms across Europe. Meanwhile, regions like South America and the Middle East and Africa are making their mark. Institutional ventures, such as GOLFZON Leadbetter’s academy in Brazil and Saudi Arabia’s Vision 2030 golf infrastructure initiatives, underscore a burgeoning structured demand. Though these markets are smaller, they are carving out credible avenues for rangefinder adoption, especially through institutional purchases and a base of premium golfers.

Competitive Landscape

The global golf rangefinder market is characterized by fragmented competition. Prominent players, including Bushnell and Garmin, capitalize on their strong brand equity and extensive distribution networks. They maintain their premium market positions through distinctive product launches and strategic investments in advanced technologies such as sensor fusion and data transmission. Conversely, Nikon and Leupold & Stevens focus on their expertise in optical technology and product durability, targeting golfers who prioritize lens precision over technological connectivity. This approach helps them mitigate pricing pressures prevalent in the mid-range market segment.

Emerging challenger brands are redefining the market by shifting the focus from optical performance to ecosystem-driven economics. Shot Scope, supported by venture capital funding, is transforming the rangefinder into a data-collection tool for its analytics-based coaching platform. Blue Tees Golf is disrupting online sales channels by offering artificial intelligence (AI)-enabled features at competitive price points. Meanwhile, Asian brands such as CaddyTalk and Voice Caddie strengthen their domestic market positions through localized software solutions and partnerships with regional golf academies. Mileseey exemplifies the effectiveness of direct-to-consumer business models, delivering premium-like features while bypassing traditional retail margins, thereby intensifying market competition.

An emerging growth opportunity lies in the integration of artificial intelligence (AI)-powered caddies that comply with United States Golf Association (USGA) and The Royal and Ancient Golf Club of St Andrews (R&A) regulations. Currently, only a limited number of products incorporate dynamic shot-recommendation systems that align with tournament compliance while offering recreational intelligence. This development signals a transformative phase in the competitive landscape: companies that successfully scale compliant AI-driven decision-making capabilities are poised to redefine market leadership, shifting the industry focus from hardware-based differentiation to value creation through integrated ecosystems.

Golf Rangefinder Industry Leaders

-

Bushnell Golf

-

Garmin

-

Nikon

-

Leupold & Stevens

-

Blue Tees Golf

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Garmin Malaysia introduced the Approach Z10, a laser rangefinder designed for golfers who sought faster and more accurate distance readings, reducing the need to second-guess club selection. This compact device measured distances to the pin from up to 350 yards. It featured six times magnification, enabling players to gain a clearer view of their target before taking a shot. Weighing less than 180g and smaller than most smartphones, the Approach Z10 was engineered for portability, providing golfers with additional data to enhance their game.

- February 2026: Blue Tees Golf introduced its Captain Series, comprising the Captain Air and Captain Pro, at the 2026 PGA Show. Both models were designed to integrate seamlessly with the Blue Tees GAME app, consolidating GPS mapping, shot tracking, and post-round analytics into a unified ecosystem.

- September 2025: Arccos, a leading provider of AI-powered golf performance tracking solutions, announced the launch of the Arccos Smart Laser Rangefinder. This groundbreaking laser, the first of its kind, was developed using AI and advanced software. Unlike conventional rangefinders that provided only a single yardage, the Arccos device delivered an advanced, real-time "plays like" distance. It achieved this by integrating live hyper-local weather data, precise GPS positioning, and detailed global mapping for over 40,000 courses, ensuring unmatched accuracy in its calculations.

Global Golf Rangefinder Market Report Scope

A golf rangefinder is a specialized device designed to help golfers measure the precise distance to a target on the course, such as the flagstick, a bunker, or a hazard, so they can make more confident club selections and improve shot accuracy. By eliminating guesswork, it enhances both performance and decision-making during play.

The global golf rangefinder market is segmented based on product type, category, end user, distribution channel, and geography. By product type, the market is segmented into laser rangefinders, GPS rangefinders, and hybrid rangefinders. By category, the market is segmented into mass and premium. By end user, the market is segmented into recreational/amateur golfers, professional golfers, golf clubs and courses, and golf academies and training centers. By distribution channel, the market is segmented into online retail stores and offline retail stores. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The market forecasts are provided in terms of value (USD).

| Laser Rangefinder |

| GPS Rangefinder |

| Hybrid Rangefinder |

| Mass |

| Premium |

| Recreational/Amateur Golfers |

| Professional Golfers |

| Golf Clubs and Courses |

| Golf Academies and Training Centers |

| Online Retail Stores |

| Offline Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Laser Rangefinder | |

| GPS Rangefinder | ||

| Hybrid Rangefinder | ||

| By Category | Mass | |

| Premium | ||

| By End User | Recreational/Amateur Golfers | |

| Professional Golfers | ||

| Golf Clubs and Courses | ||

| Golf Academies and Training Centers | ||

| By Distribution Channel | Online Retail Stores | |

| Offline Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the global golf rangefinder market?

The market was valued at USD 367.78 million in 2025 and is projected to reach USD 530.85 million by 2031, growing at a CAGR of 6.37% during 2026–2031.

Which product type holds the largest share?

Laser rangefinders are the largest product type, accounting for 61.86% of the market in 2025, driven by their accuracy and reliability.

What is the largest category by pricing tier?

The mass segment dominates with 64.54% share in 2025, reflecting strong demand for affordable, utilitarian devices.

Who are the largest end users?

Recreational and amateur golfers represent 71.37% of demand in 2025, aligning with broad participation trends.

What is the dominant distribution channel?

Offline retail stores held 69.89% share in 2025, supported by consumer preference for hands-on evaluation and pro-shop expertise.

Which region leads the market?

North America is the largest region, holding 42.63% share in 2025, anchored by strong participation and dense golf infrastructure.

Page last updated on: