Golf Simulator Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.14 Billion |

| Market Size (2031) | USD 3.35 Billion |

| Growth Rate (2026 - 2031) | 9.37% CAGR |

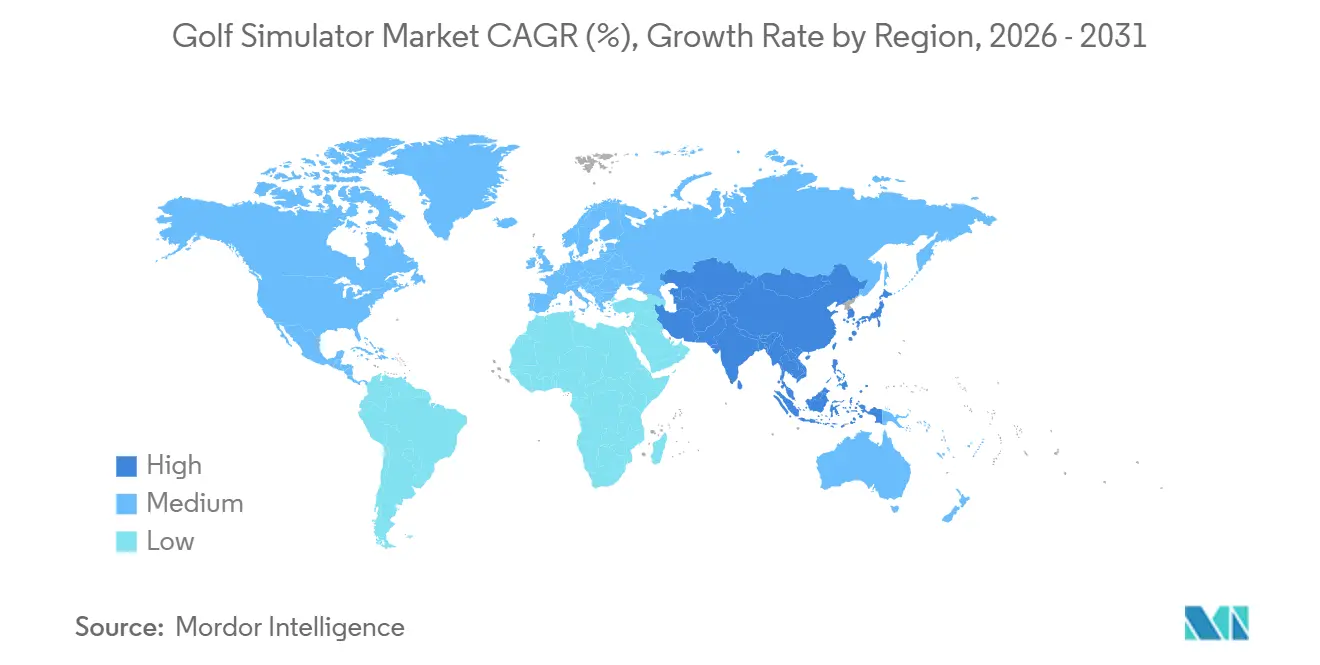

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Golf Simulator Market Analysis by Mordor Intelligence

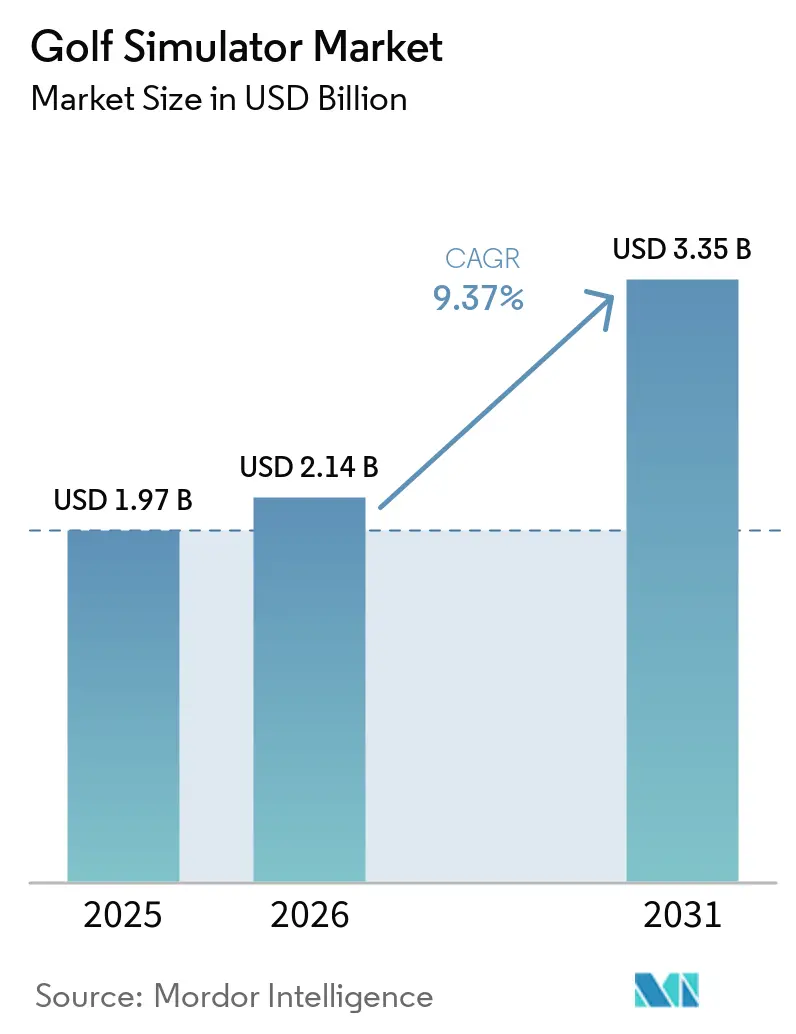

The golf simulator market size was valued at USD 1.97 billion in 2025 and estimated to grow from USD 2.14 billion in 2026 to reach USD 3.35 billion by 2031, at a CAGR of 9.37% during the forecast period (2026-2031). The expansion of the golf simulator market is tied to two broad shifts that now look durable: year-round demand for indoor play and the wider acceptance of off-course golf as a regular leisure option rather than a niche activity. In the United States alone, 48.1 million people participated in golf activities in 2025, including 19 million who played only in off-course settings such as simulator venues and tech-enabled ranges, indicating that the sport’s growth is no longer tied solely to traditional courses, according to the National Golf Foundation. The golf simulator market is also benefiting from a shift in how operators generate revenue, as software access, content libraries, and analytics subscriptions are becoming recurring revenue streams with better margin potential than one-time hardware sales. Buyer interest is widening at the same time, because commercial venues continue to invest in immersive indoor formats while more households are considering garage-ready or compact systems as prices become easier to justify. Regional demand remains uneven, but the golf simulator market is strongest where golf participation is already high, indoor entertainment formats are familiar, and weather or space limitations make off-course play a practical substitute for part of the year.

Key Report Takeaways

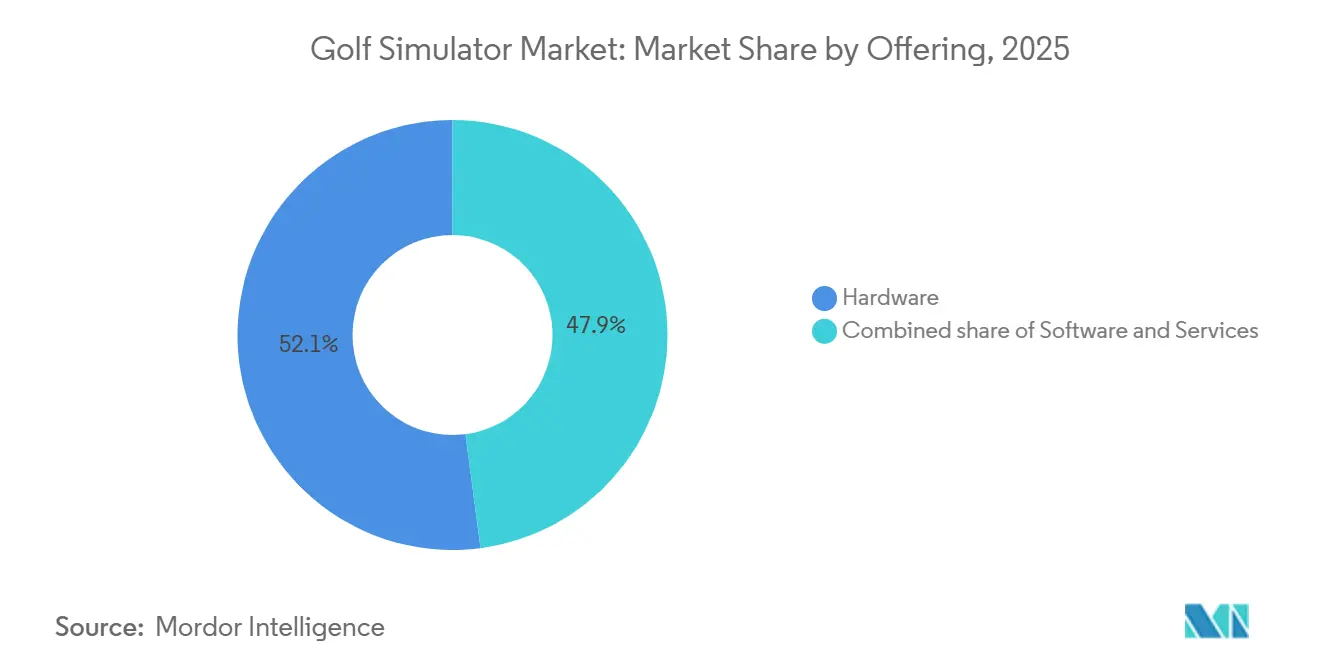

- By offering, hardware held 52.07% share in 2025, while services posted the highest forecast CAGR at 10.62% through 2031.

- By product type, portable simulators retained 64.16% share in 2025, whereas built-in simulators are forecast to expand at a 11.37% CAGR through 2031.

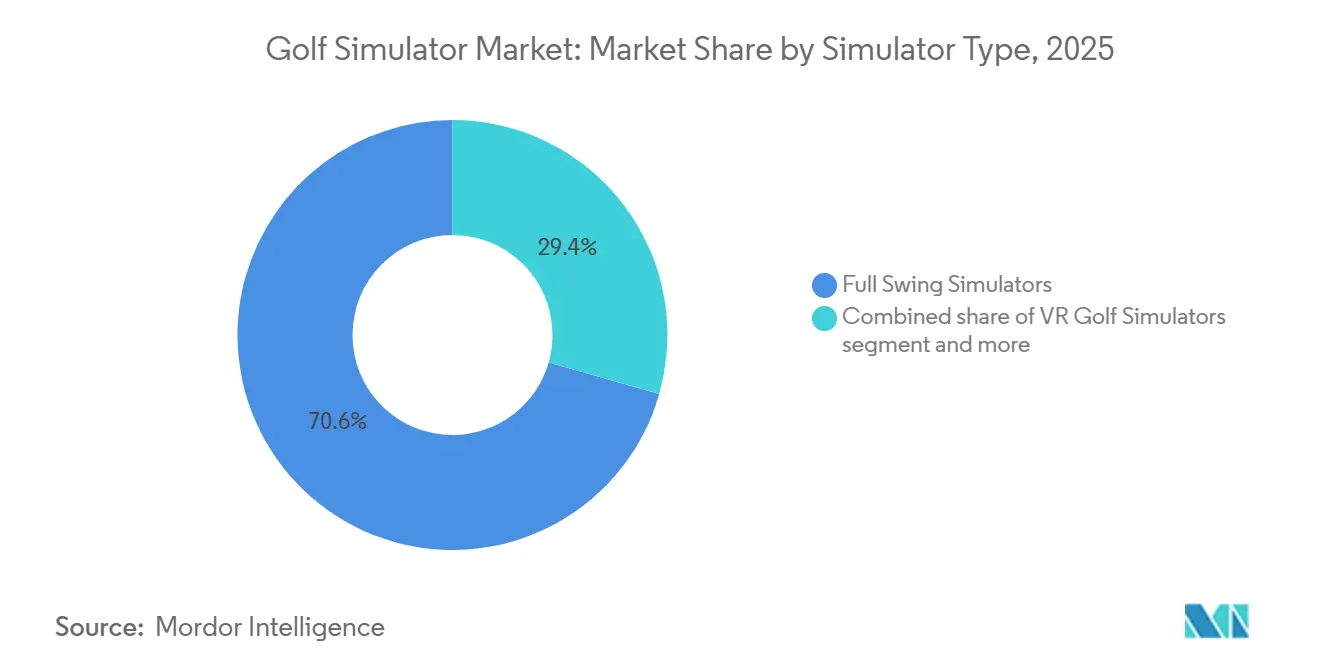

- By simulator type, full-swing simulators accounted for 70.58% of 2025 revenue, but VR golf simulators are expected to grow fastest at 10.86% through 2031.

- By technology, camera-based technology led the golf simulator market with a 53.34% share in 2025, while AI-enabled analytics is anticipated to register the fastest CAGR of 12.03% during 2026-2031.

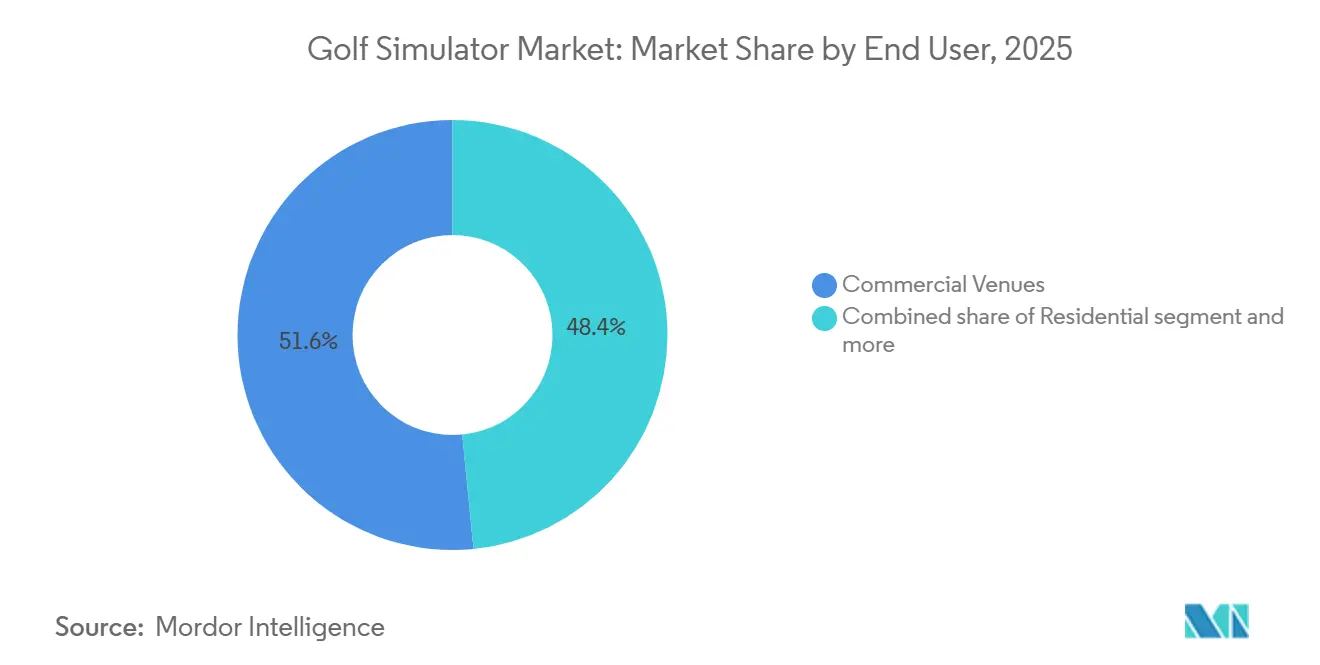

- By end user, commercial venues captured 51.56% share in 2025, while residential users posted the fastest growth at 11.59% through 2031.

- By geography, North America accounted for the largest share of the golf simulator market, at 40.87% in 2025, while Asia-Pacific is projected to grow at the fastest CAGR of 10.32% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Golf Simulator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Year-Round Indoor Golf | +2.5% | Global, concentrated in North America and Northern Europe | Short term (≤ 2 years) |

| Growth of Home Entertainment and Practice Setups | +1.7% | North America, Asia-Pacific | Short term (≤ 2 years) |

| AI-Enabled Swing Analytics and Shot Capture | +1.5% | Global | Medium term (2-4 years) |

| Portable and Space-Efficient System Adoption | +1.2% | North America, Asia-Pacific | Short term (≤ 2 years) |

| Growth of Golf Academies and Coaching Centers | +0.8% | North America, Asia-Pacific, MEA | Medium term (2-4 years) |

| Subscription Content and Ecosystem Monetization | +0.9% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for year-round indoor golf

The golf simulator market continues to gain support from a simple consumer need: golfers want a way to play and practice when outdoor conditions are poor or schedules are tight. The NGF white paper from April 2025 found that 59% of simulator users cited weather-independent play as their main reason for using these systems, confirming that convenience is one of the strongest demand drivers in the category. The same study showed that facility adoption was higher in colder U.S. regions, with simulator penetration at 8.4% in the Midwest and 7.9% in the North, compared with 4% in the South, where outdoor play remains more accessible year-round[1]Source: National Golf Foundation, “The Golf Simulator Opportunity,” National Golf Foundation, ngf.org. Operator economics also support faster rollouts, as positive returns on investment were reported within 7 months on average, and 80% of operators turned profitable within the first year. The golf simulator market, therefore, benefits not only from individual user demand but also from peer pressure among operators, as successful installations tend to encourage competing facilities in the same region to adopt similar setups. This matters because indoor golf is no longer being treated only as a winter add-on; it is becoming part of the regular participation model in markets where weather, time, and booking convenience affect how often people can engage with the sport.

Growth of home entertainment and practice setups

The golf simulator market is also expanding because at-home golf practice has become easier to justify for buyers who want recreation and performance feedback in the same setup. Portable simulators already accounted for 64.16% of the product type segment in 2025, underscoring the market's preference for flexible systems that fit ordinary residential spaces and do not require extensive renovation. The NGF white paper found that 72% of non-adopting U.S. facilities still cited space as a barrier, which explains why compact and garage-ready formats have become more important for both homes and light commercial users. Over 20% of U.S. golf facilities already own at least 1 portable launch monitor, indicating that entry-level and modular products are often the first step before a buyer considers a larger, enclosed simulator environment. The residential side of the golf simulator market is growing at 11.6% through 2031, and that pace suggests that more demand is now coming from households that value casual use, family entertainment, and regular swing work in one purchase. This shift is important because it broadens the buyer base beyond avid golfers and academy operators, giving the golf simulator market a more balanced demand mix than it had when premium commercial installations accounted for most of the category.

AI-enabled swing analytics and ecosystem monetization

The golf simulator market is moving beyond ball tracking and visual playback, and buyers are now expecting systems to deliver coaching value, personalized feedback, and usable performance data. This is why AI-enabled analytics is the fastest-growing technology segment at 12.03% through 2031, while the services segment is also growing quickly at 10.62% as more revenue shifts into subscriptions, platform access, and add-on content. Foresight Sports continued to formalize this model in 2025 through tiered subscription access to simulation features and club mode tools, demonstrating how brands are building ongoing customer relationships after the original hardware sale. The same direction was visible in early 2026, when Foresight previewed its next-generation Premiere software with a rebuilt physics engine and redesigned interface, signaling that software upgrades are becoming a central part of customer retention and installed-base monetization[2]Source: Foresight Sports, “GC3s, Launch Pro, and Launch Pro Indoor Subscriptions, Updated Subscription Options,” Foresight Sports Help Center, foresightsports.com. In the golf simulator market, this creates a clearer divide between firms that sell devices and those that control the broader user experience through content, analytics, and recurring access. That divide matters because the customer who depends on platform features and data services is harder to displace than the customer who only bought a launch monitor or screen bundle once.

Growth of golf academies and coaching centers

The golf simulator market is also benefiting from the steady adoption of simulator-led instruction in academies, coaching centers, and other structured training environments. These buyers are less focused on entertainment value alone and more focused on repeatable swing analysis, shot pattern evaluation, lesson programming, and year-round player development. The role of youth and early-stage participation is especially important here, because NGF research showed that demand for simulator-based golf training has risen among younger players in recent years. That pattern matters for the golf simulator market because it supports future replacement demand, software attachment, and stronger academy procurement cycles over time. It also helps explain why commercial coaching facilities continue to support premium systems even as lower-cost consumer products improve, since academy operators need accuracy, throughput, and structured lesson integration rather than just basic shot display. As coaching models become more data-driven and less dependent on weather or range access, the golf simulator market gains a stable demand base tied to instruction outcomes rather than casual recreation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost of Premium Simulator Systems | -1.4% | Global, most acute in residential markets and developing economies | Short term (≤ 2 years) |

| Space Requirements Limiting Residential Adoption | -0.9% | Global, most acute in Asia-Pacific and European urban centers | Medium term (2-4 years) |

| Installation Complexity for Full Simulator Bays | -0.7% | North America, Europe | Medium term (2-4 years) |

| Competition from Outdoor Golf and Driving Ranges | -0.5% | North America, Australia, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High upfront cost and installation complexity

The golf simulator market still faces a clear adoption barrier: premium system pricing, especially when buyers need a full bay, enclosure, projector, sensors, software, and a professional setup. The NGF white paper reported that 53% of U.S. golf facility operators without simulators cited initial investment as a major obstacle, and the average cost per bay was USD 45,000, making the purchase difficult to justify for smaller operators or price-sensitive households. The challenge is not only the sticker price, because fixed-bay installations often require structural work, network configuration, projector alignment, calibration, and ongoing maintenance, which further raise the effective cost. This pushes much of the golf simulator market toward a split structure, with premium buyers choosing accuracy and immersive setups, while lower-budget users settle for simpler systems with fewer features. That split slows penetration in developing economies and in mid-tier commercial locations where traffic volumes are not high enough to recover the investment quickly. Until full-bay installations become easier to deploy and less capital-intensive, the golf simulator market will continue to grow unevenly across customer groups and geographies.

Space requirements and competition from outdoor golf

The golf simulator market also faces a physical limitation that technology alone cannot overcome: many homes and smaller venues simply do not have the right dimensions for a full simulator environment. The NGF white paper stated that a standard simulator installation typically requires 15 feet of width, 13 feet of height, and 21 feet of depth, excluding a large share of urban homes and older commercial properties from built-in formats. This is especially important in dense Asian cities and established European urban centers, where residential space is limited and retrofitting older buildings can be costly or impractical. The golf simulator market also competes with a very healthy outdoor game, because U.S. rounds exceeded 500 million in 2025 for the sixth straight year, showing that traditional play remains a strong use of time and discretionary spending. In warm-weather regions, outdoor ranges and social driving range formats continue to attract casual players who might otherwise visit indoor simulator venues. That means the golf simulator market often grows fastest where weather and space constraints support indoor demand, rather than in every golf market at the same rate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software and Services Disrupting a Hardware-Led Market

Hardware accounted for 52.07% of the golf simulator market share in 2025, confirming that screens, launch monitors, sensors, and projection systems remain the largest revenue base for the category. This leadership is supported by the need for physical equipment across both commercial and residential setups, regardless of whether the buyer is focused on training, entertainment, or mixed use. The golf simulator market still needs hardware to scale, but the role of hardware is becoming less decisive in long-term value capture as the category matures. Buyers now expect a system to stay useful through updates, content additions, and analytics features after the first installation. That is why the services segment is projected to grow at 10.62% through 2031, faster than any other offering category.

This shift is changing how suppliers think about profitability in the golf simulator market. Foresight Sports has already tied important simulation features and access levels to annual subscriptions, demonstrating how brands are protecting recurring revenue even as hardware refresh cycles slow. The planned release of the Premiere simulation platform in late 2026 also points to a model where software launches drive customer re-engagement and upgrade demand from the installed base. In practical terms, this means the most resilient firms in the golf simulator industry are likely to be those that sell hardware once but monetize usage many times. It also means that operators choosing a platform are increasingly evaluating the depth of software support, content roadmap, and ecosystem reliability, not only launch accuracy or screen quality.

By Product Type: Portability Dominates Today, Built-In Systems Define Tomorrow

Portable simulators held a 64.16% share in 2025, making them the clear volume leader in the golf simulator market at the product level. Their strength comes from lower setup demands, better fit for ordinary residential spaces, and easier adoption by smaller venues that cannot commit to permanent structural changes. The golf simulator market has therefore expanded faster at the entry and mid-range levels than it would have if fixed commercial bays were the only realistic option. Portable products also give buyers a lower-risk way to test whether simulator use becomes a routine habit before spending on a larger enclosed environment. This helps explain why portable formats dominate current unit demand even though they do not always deliver the most immersive experience.

Built-in simulators are still the fastest-growing product type, with an 11.37% CAGR through 2031, and that growth says a lot about where premium commercial demand is heading. The golf simulator market is seeing increased interest from venues seeking standardized bays, strong visual immersion, and reliable throughput for group bookings, coaching sessions, and events. These buyers value consistency, realism, and branded experience more than portability, which is why built-in systems are gaining ground despite the higher cost and installation burden. The result is a two-track structure where portable products widen access and built-in systems define the premium commercial model. Over time, that gap may become even clearer, because residential and casual users often prioritize affordability and convenience, while commercial operators focus on repeat traffic, session pricing, and customer experience.

By Simulator Type: Full Swing Leads, VR Emerges as the Next Engagement Layer

Full-swing simulators accounted for 70.58% of the market in 2025, giving them the strongest position across simulator formats. Their lead reflects how well they serve both serious golfers and entertainment venues through complete shot tracking, broad course play, group competition, and more familiar use patterns. The golf simulator market still relies heavily on this format because it most closely aligns with how people understand golf practice and indoor golf entertainment. Simulators and optical sensor formats remain relevant, but they tend to address narrower use cases, such as short-game work or fitting support. Full-swing setups, therefore, remain the reference point for many commercial buyers when deciding how much to invest in simulator infrastructure.

VR golf simulators are growing at 10.86% through 2031, making them the fastest-rising format, even from a smaller base. The golf simulator market is drawing value from VR because it can appeal to younger users, gaming-oriented consumers, and non-golfers who may be more attracted by immersion than by launch data. TruGolf and Digital Legends followed this direction in 2025 when they introduced AI-driven recreations of golf legends on the E6 APEX platform, demonstrating how personality-driven content can extend simulator use beyond traditional practice. While VR is not yet replacing standard full swing setups, it is giving the golf simulator market another path to widen consumer engagement. As headset comfort, visual quality, and haptic support improve, VR is likely to become a stronger complement to mainstream simulator use rather than just a novelty layer.

By Technology: Camera Systems Lead, AI Analytics Redefine Value

Camera-based systems accounted for 53.34% of the market share in 2025, making them the leading technology among core tracking approaches. Their advantage lies in a strong balance of accuracy, affordability, and installation flexibility across both home and commercial environments. The golf simulator market has rewarded technologies that can work in different room layouts and price bands without large sacrifices in core performance. Radar systems remain important at the premium end, while infrared products still serve lower-cost users and projection technology supports the visual side of most full-bay systems. This gives camera-based technology a broad middle position that is difficult to displace.

AI-enabled analytics is the fastest-growing technology segment at 12.03% through 2031, and that growth shows where value is shifting in the golf simulator market. The key change is that users increasingly want systems to interpret data rather than simply display it, which makes analytics, training prompts, and adaptive simulation features more commercially important. Zen Golf’s integrated TrackMan solution, presented in January 2026, showed how this logic is advancing, with an active-terrain hitting surface that adjusts to virtual course conditions in real time. That kind of integration matters because it narrows the gap between indoor simulation and outdoor playing conditions, which is one of the biggest long-term challenges for the golf simulator market. The more these systems can merge data, realism, and physical feedback, the more pricing power premium suppliers are likely to preserve.

By End User: Commercial Venues Anchor Revenue, Residential Drives Future Growth

Commercial venues held a 51.56% share in 2025, making them the largest end-user segment in the golf simulator market by revenue. Indoor golf lounges, entertainment venues, resorts, and mixed-use hospitality sites continue to support this lead because they can spread hardware costs across many paying users. The golf simulator market has gained meaningful scale through these venues, as they introduce new consumers to indoor golf who may not yet be ready to buy a home-use system. The NGF found that 77% of commercial facility operators believed simulators increased customer engagement and satisfaction, while 65% said the systems helped attract new customers. This confirms that commercial buyers often view simulators as demand-building assets rather than only as direct revenue tools.

Residential users remain the fastest-growing end-user group, with a 11.59% CAGR through 2031, signaling a wider shift in the golf simulator market toward home adoption. This is closely linked to younger off-course participation, as more than 7 million U.S. adults aged 18 to 34 participated only in off-course golf formats in 2025, giving the category a consumer base already comfortable with non-course play. The golf simulator market is therefore not depending only on avid traditional golfers for future residential demand. Educational institutions, corporate buyers, and hospitality venues also add depth to the market, but the home segment stands out because it can expand unit volume as product prices become easier to absorb. If current adoption patterns hold, residential demand will remain one of the main forces reshaping the customer mix of the golf simulator market over the forecast period.

Geography Analysis

North America accounted for 40.87% of the golf simulator market share in 2025, keeping the region well ahead of other geographies in current revenue terms. The region benefits from a large active golfer base, stronger consumer familiarity with launch monitor technology, and a commercial network that already understands how to package indoor golf with food, beverage, coaching, and social events. The NGF reported that 8.1 million people in the United States used simulators or screen-golf formats in 2024, up from 3.6 million 5 years earlier, and indicated that facility penetration could move from 6.5% to 10%-11% within 2 years as more operators commit capital. That installed-base momentum matters because it creates more repeat-user exposure, which, in turn, improves the long-term economics of software, memberships, lesson packages, and content subscriptions in the golf simulator market. North America also remains important as a testing ground for venue concepts, as operators there are actively refining the mix of practice, competition, and hospitality that makes indoor golf commercially sustainable year-round.

Europe remains a meaningful but more mixed region for the golf simulator market, because demand is shaped by weather, urban density, existing golf culture, and the role of hospitality-led installations. Markets such as Germany and the United Kingdom remain important because they support both coaching use cases and commercial venue formats, while secondary markets are gaining interest where resort operators and urban entertainment concepts want indoor golf as part of a wider offer. The region’s growth is still tied to practical conditions, especially the ability to turn limited seasonal access to outdoor golf into repeat indoor usage. At the same time, space limitations in older buildings and city locations can slow full-bay deployments, which means compact and modular systems continue to matter in the European golf simulator market. This gives Europe a more selective adoption pattern than North America, but it also means that buyers who do invest are often looking for clearly differentiated systems that can justify pricing through performance, coaching value, or premium guest experience.

Asia-Pacific is the fastest-growing region in the golf simulator market size, with a forecast CAGR of 10.83% through 2031, and that pace reflects a different mix of strengths from the Western markets. South Korea remains the most established simulator ecosystem in the world in terms of screen-golf penetration and consumer familiarity, while Japan continues to support compact and high-tech indoor formats that fit local space conditions and usage habits. China adds another layer of opportunity because large urban markets can support simulator-led entertainment where land access and environmental constraints limit the expansion of traditional courses. The golf simulator market in Asia-Pacific therefore benefits from conditions that are structural rather than temporary, including dense city living, technology acceptance, and the practicality of off-course golf. South America and the Middle East and Africa remain much earlier in their adoption curve, but they are still relevant because they show where academy-led growth and premium hospitality installs may open the next set of smaller but commercially important demand pockets for the golf simulator market.

Competitive Landscape

The golf simulator market remains moderately concentrated, with GOLFZON, TrackMan, Revelyst, Foresight Sports, Full Swing Golf, and TruGolf forming the core group that shapes product standards, operator expectations, and the direction of premium competition. No single firm controls every part of the golf simulator market, because leadership is split across venue scale, professional credibility, software depth, and installed-base monetization. GOLFZON stands out for the breadth of its platform and the way it connects simulator hardware with content, venue formats, and branded commercial experiences. TrackMan remains especially influential in performance-led settings where measurement credibility and training use matter most. Foresight Sports, now under the broader Revelyst Golf Technology umbrella, is pushing hard on software continuity and ecosystem coherence, which is important in a market where recurring platform use is becoming more valuable than the initial device sale.

Strategic behavior in the golf simulator market increasingly follows 3 patterns: control of the technology stack, expansion of branded venue relationships, and stronger software retention models. Troon’s announcement of a new Golfzon Social location in the Chicago area in 2025 showed how indoor golf is being built into hospitality-oriented venue formats rather than sold only as a training tool. Zen Golf’s integration with TrackMan iO, shown at the 2026 PGA Show, highlighted a different path, where premium suppliers try to create a more realistic performance environment through integrated hardware and active terrain response. Foresight Sports also used the 2026 PGA Show to preview Premiere under the Revelyst Golf Technology identity, which signals that platform refreshes and ecosystem redesigns are now major competitive tools in the golf simulator market. These moves show that the leading firms are not competing on sensor accuracy alone, they are trying to shape how operators and consumers stay inside their ecosystem over time.

The competitive pressure is also rising at the middle and lower ends of the golf simulator market, where product access is improving and brand loyalty is less fixed than it is in tour-grade or academy-grade systems. This is why software support, content access, and user experience matter so much, because the supplier that holds the ongoing relationship has a better chance of protecting margins as basic hardware becomes easier to compare. SkyTrak’s rollout of Course Play powered by Foresight Sports in April 2025 is a useful example, since it strengthened the software side of its offer without requiring a complete reinvention of the hardware proposition[3]Source: SkyTrak, “SkyTrak Launches Course Play Powered by Foresight Sports,” SkyTrak, skytrakgolf.com. In the golf simulator market, that kind of move matters because it improves retention and perceived system value even when buyers are not ready to replace their device. Over the next few years, firms that can connect hardware, software, content, and venue relevance in one coherent offer are likely to be better positioned than firms that compete only on price or only on raw measurement performance.

Golf Simulator Industry Leaders

GOLFZON Co., Ltd.

TrackMan A/S

Revelyst Inc.

Full Swing Golf, Inc.

TruGolf Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Zen Golf unveiled a prototype integration of its Swing Stage 2.0 with TrackMan iO at the 2026 PGA Merchandise Show, demonstrating an active-terrain hitting surface that automatically adjusts physical slope and gradient to match virtual fairway conditions in real time, described by both companies as the first system of its kind and developed at the Tuxen Innovation Lab at TrackMan's global headquarters.

- January 2026: Revelyst Golf Technology debuted at the 2026 PGA Merchandise Show, uniting Foresight Sports, Bushnell Golf, and GolfLogix under a single brand umbrella led by Revelyst CEO Eric Nyman. The company previewed next-generation Foresight simulation software, branded Premiere, with a rebuilt physics engine and overhauled UI, scheduled for release in late 2026.

- April 2025: SkyTrak launched Course Play powered by Foresight Sports, adding 30 simulated courses, including Pebble Beach Golf Links, to SkyTrak's simulation software ecosystem through a strategic collaboration with Foresight Sports, strengthening its competitive position in the mid-market software tier.

Global Golf Simulator Market Report Scope

Golf simulators are technology-enabled systems that replicate real-world golfing experiences by using hardware, software, and analytics to provide virtual gameplay, training, and performance analysis. The golf simulator market is segmented by offering, product type, simulator type, technology, end user, and geography. By offering, the market includes hardware, software, and services. Based on product type, the market is segmented into portable, built-in, and free-standing simulators. By simulator type, the market covers full-swing simulators, VR golf simulators, putting simulators, and optical-sensor simulators. Based on technology, the market includes camera-based, radar-based, infrared, projection, and AI-enabled analytics. By end user, the market is segmented into residential, commercial venues, golf academies and training centers, educational institutes, and corporate and hospitality venues. By geography, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East and Africa, with market size and forecasts provided for each region. The golf simulators market size has been calculated in USD for all the above-mentioned segments.

| Hardware |

| Software |

| Services |

| Portable Simulators |

| Built-In Simulators |

| Free-Standing Simulators |

| Full Swing Simulators |

| VR Golf Simulators |

| Putting Simulators |

| Optical Sensor Simulators |

| Camera-Based Technology |

| Radar-Based Technology |

| Infrared Technology |

| Projection Technology |

| AI-Enabled Analytics |

| Residential |

| Commercial Venues |

| Golf Academies and Training Centers |

| Educational Institutes |

| Corporate and Hospitality Venues |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Offering | Hardware | |

| Software | ||

| Services | ||

| By Product Type | Portable Simulators | |

| Built-In Simulators | ||

| Free-Standing Simulators | ||

| By Simulator Type | Full Swing Simulators | |

| VR Golf Simulators | ||

| Putting Simulators | ||

| Optical Sensor Simulators | ||

| By Technology | Camera-Based Technology | |

| Radar-Based Technology | ||

| Infrared Technology | ||

| Projection Technology | ||

| AI-Enabled Analytics | ||

| By End User | Residential | |

| Commercial Venues | ||

| Golf Academies and Training Centers | ||

| Educational Institutes | ||

| Corporate and Hospitality Venues | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2031 outlook for golf simulators?

The golf simulator market is forecast to reach USD 3.35 billion by 2031, rising from USD 1.97 billion in 2025 at a 9.37% CAGR over 2026 to 2031.

Which product category is leading demand today?

Portable simulators led with 64.16% share in 2025 because they fit more homes and smaller venues and require less structural work than built-in systems.

Which customer group is expanding the fastest?

Residential users are the fastest-growing end-user group, with an 11.59% CAGR through 2031, supported by broader off-course participation and easier entry points for home use.

Which region is growing the fastest?

Asia-Pacific is the fastest-growing region, with a 10.83% CAGR through 2031, supported by strong simulator culture in South Korea, compact indoor demand in Japan, and expanding urban entertainment formats in China.

Page last updated on: