Gluten Free Meat Substitutes Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

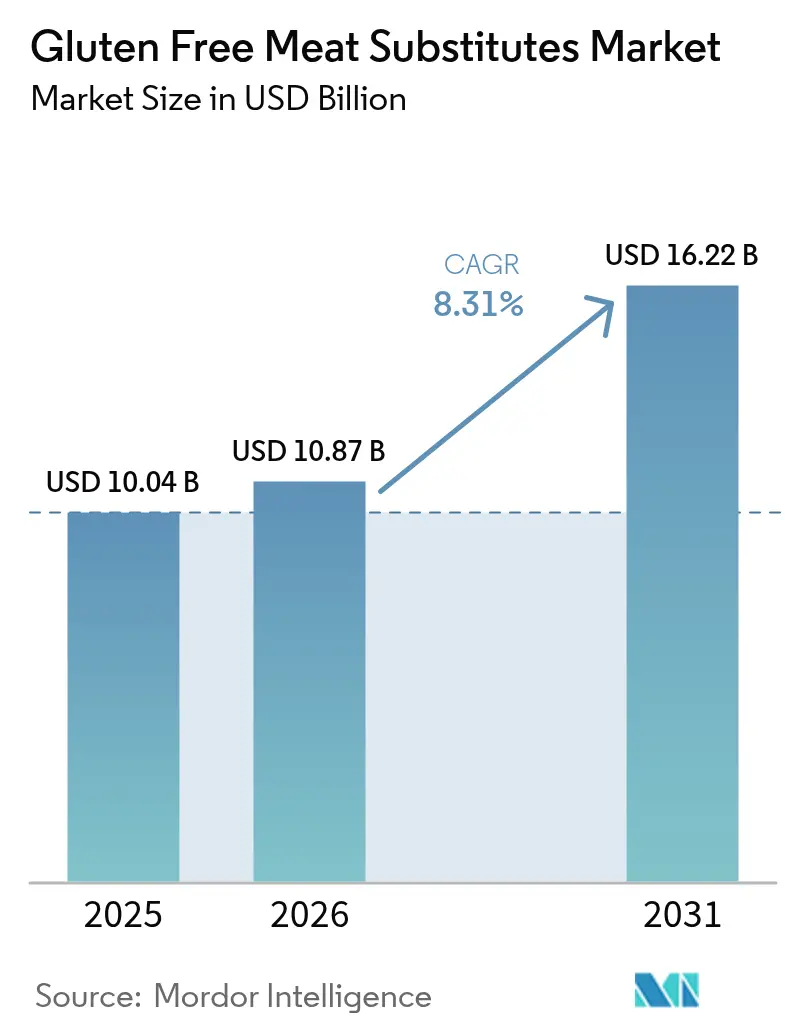

| Market Size (2026) | USD 10.87 Billion |

| Market Size (2031) | USD 16.22 Billion |

| Growth Rate (2026 - 2031) | 8.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Gluten Free Meat Substitutes Market Analysis by Mordor Intelligence

The gluten-free meat alternatives market size is expected to grow from USD 10.04 billion in 2025 to USD 10.87 billion in 2026 and is forecast to reach USD 16.22 billion by 2031 at 8.31% CAGR over 2026-2031. Improvements in ingredient processing—especially high-moisture extrusion and precision flavor masking—have closed historical taste and texture gaps, while younger shoppers show higher intent to pay a premium for certified products. Manufacturers also benefit from capital inflows triggered by government sustainability mandates and corporate decarbonization targets, which position plant-based proteins as cost-effective climate tools. Product launches that highlight reduced saturated fat or allergen-friendly positioning attract health-centric buyers and help the gluten-free meat alternatives market penetrate mainstream retail assortments.

Key Report Takeaways

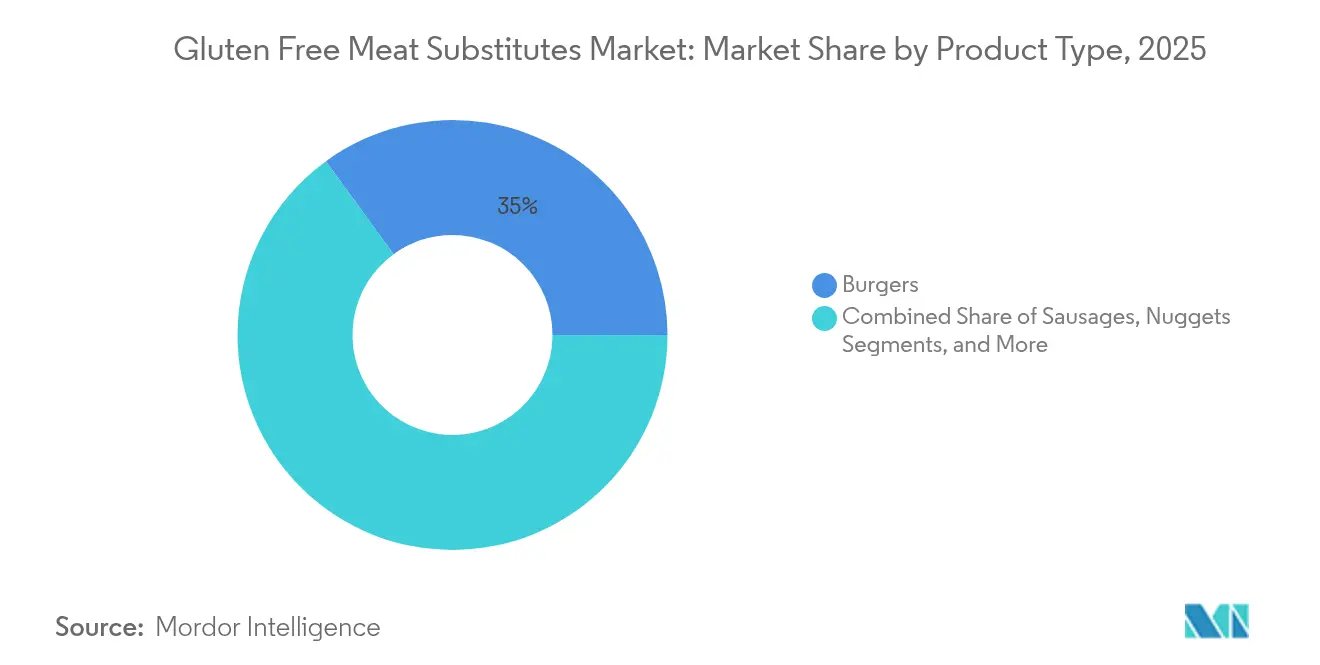

- By product type, burgers held 35.02% of the gluten-free meat substitutes market share in 2025; nuggets are projected to grow at a 10.24% CAGR between 2026-2031.

- By source, the tofu segment led with 27.05% revenue share in 2025, while pea protein formats are forecast to expand at 9.32% CAGR to 2031.

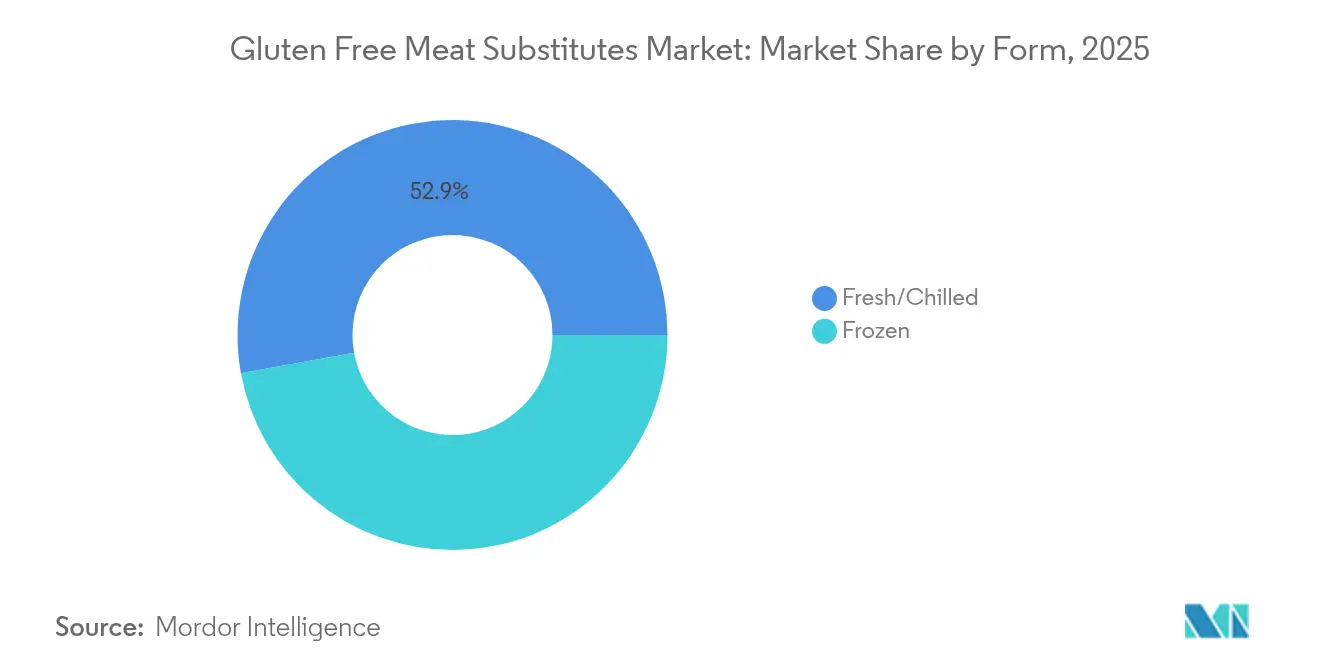

- By form, frozen segment commanded 47.15% share of the gluten-free meat substitutes market size in 2025; fresh/chilled segment is set to climb at 8.58% CAGR through 2031.

- By distribution channel, off-trade outlets controlled 63.88% sales in 2025, whereas on-trade demand is expected to accelerate at an 8.74% CAGR during the period 2026-2031.

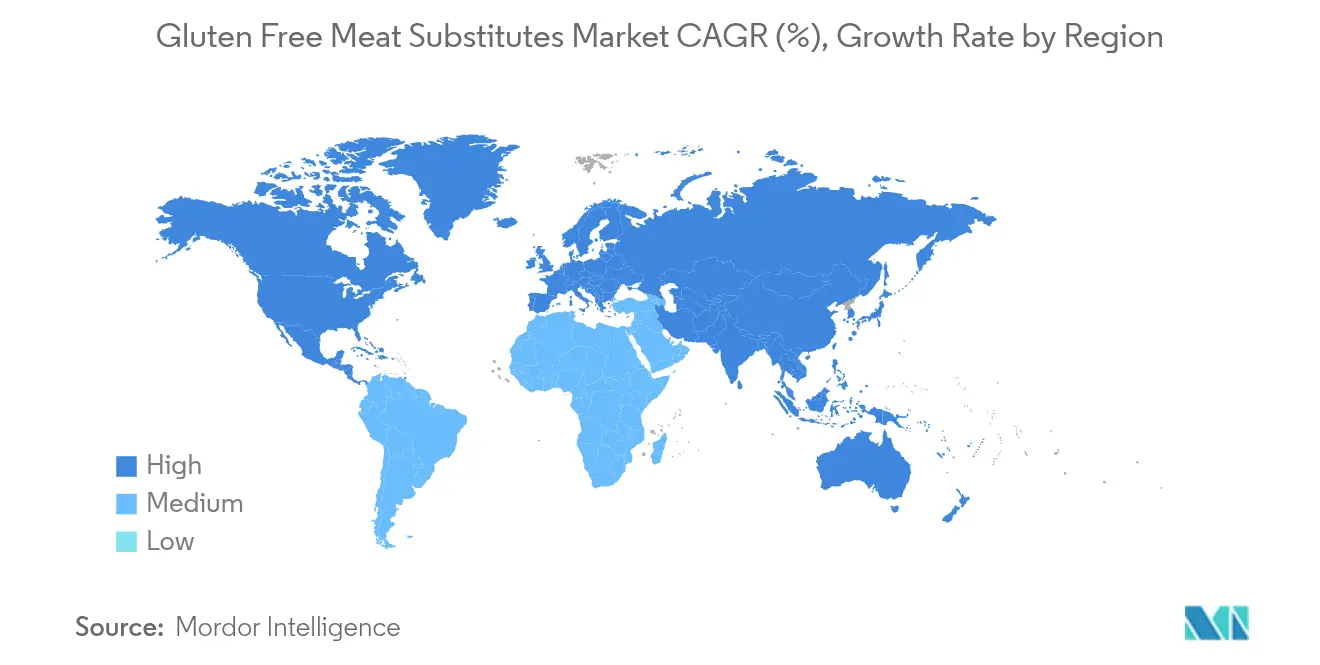

- By geography, North America contributed 34.62% of 2025 revenue; Asia-Pacific is poised for the fastest 9.14% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gluten Free Meat Substitutes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing gluten intolerance and celiac disease cases | +1.80% | Global, with higher impact in North America and Europe | Medium term (2-4 years) |

| Innovations in product development and flavor enhancement | +1.50% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Growing adoption of vegan and vegetarian diets | +1.20% | Global, strongest in developed markets | Long term (≥ 4 years) |

| Increased availability of gluten-free products in retail stores | +1.00% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Advancements in food processing technologies | +0.90% | Global, technology centers in North America and Europe | Long term (≥ 4 years) |

| Strategic advertisements and brand promotions | +0.80% | Global, concentrated in urban markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing gluten intolerance and celiac disease cases

The escalating prevalence of celiac disease in developed markets creates sustained demand for gluten-free alternatives that extends beyond traditional dietary restrictions. European countries, particularly Finland and Italy, demonstrate significant celiac disease populations. In 2023, the prevalence of celiac disease in the Italian population was 1%, according to the Ministry of Health [1]National Institute of Health, "Annual report to Parliament on celiac disease: 2023 data", epicentro.iss.it. The data indicates that Aosta Valley, the Autonomous Province of Trento, and Tuscany registered the highest prevalence of this disease. Market expansion is driven by healthcare providers improving diagnostic pathways and increasing awareness of gluten-related disorders through patient awareness campaigns. The FDA's gluten-free labeling requirements strengthen consumer confidence in product safety and enable manufacturers to command premium pricing for certified alternatives. The long-term market potential is further amplified by the demographic shift toward younger consumers, who demonstrate higher rates of dietary restriction adoption and maintain purchasing power as these cohorts age.

Innovations in product development and flavor enhancement

Technological breakthroughs in protein texturization and flavor masking have transformed gluten-free meat alternatives from specialized health products to mainstream food options that compete with conventional meat on taste and texture. The combination of 3D printing technology and simultaneous infrared cooking allows manufacturers to create complex textures that replicate muscle fiber structures while maintaining gluten-free formulations. High-moisture extrusion processes enable plant proteins to achieve meat-like textures, while artificial intelligence optimization improves consistency and reduces production variations. Companies like Roquette have developed specialized ingredients such as NUTRALYS® Fava S900M, a fava bean protein isolate with 90% protein content, designed for gluten-free applications with enhanced gel strength and viscosity control. These technical improvements address consumer concerns about taste and texture, facilitating wider market acceptance beyond health-conscious consumers.

Growing adoption of vegan and vegetarian diets

The rising popularity of plant-based diets reflects changing consumer preferences driven by health awareness, environmental concerns, and ethical considerations. This shift has increased the demand for gluten-free meat substitutes globally. According to the British Council, approximately 1.5 billion people worldwide do not consume meat. While some individuals choose vegetarianism for ethical, environmental, or health reasons, others abstain from meat consumption due to limited access or affordability constraints. [2]The United Kingdom's international organisation for cultural relations and educational opportunities, "World Vegetarian Day", britishcouncil.org. This dietary transformation has created market opportunities for clean-label, gluten-free meat alternatives that address various cultural and dietary requirements. The environmental impact of plant-based alternatives includes reduced food-related emissions comparable to decarbonizing major industries, appealing to environmentally conscious consumers. Government initiatives support this trend, with Canada, Denmark, and Germany providing substantial funding for plant-based research and development, which strengthens consumer confidence and promotes innovation in the market.

Increased availability of gluten-free products in retail stores

The distribution of gluten-free meat alternatives has expanded significantly from specialty health food stores to mainstream grocery retailers, who now allocate substantial dedicated shelf space to plant-based products. Major retailers strategically position these items in both frozen and ambient sections to increase product visibility, accommodate different shopping preferences, and enhance consumer accessibility. The rapid growth of e-commerce platforms has transformed product accessibility, allowing manufacturers to establish direct-to-consumer distribution channels that bypass traditional retail constraints and geographical limitations. The online retail channels have also enabled sophisticated inventory tracking and demand forecasting systems, helping retailers optimize their stock levels, reduce wastage, and maintain consistent product availability across multiple locations. Despite this widespread retail expansion and technological advancement, consumers continue to report difficulties finding specific gluten-free products, presenting a significant opportunity for retailers to strengthen their distribution networks, improve inventory management systems, and better meet growing consumer demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production costs compared to conventional meat products | -1.40% | Global, most pronounced in emerging markets | Medium term (2-4 years) |

| Perception challenges related to nutritional value | -1.10% | Global, stronger in traditional meat-consuming regions | Long term (≥ 4 years) |

| Intense competition from traditional meat products | -0.90% | Global, varies by regional meat consumption patterns | Short term (≤ 2 years) |

| Limited consumer awareness in emerging markets | -0.70% | Asia-Pacific, Middle East and Africa, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High production costs compared to conventional meat products

Gluten-free meat alternatives cost 2 to 2.5 times more than conventional meat products, limiting their widespread adoption and market penetration among price-sensitive consumers [3]Good Food Institute, "Reducing the price of alternative proteins", gfi.org. The higher costs stem from specialized ingredients such as quinoa, chickpea flour, and rice protein, along with dedicated manufacturing facilities to prevent cross-contamination, and smaller production scales compared to traditional meat processing. The gluten-free certification process requires extensive testing, documentation, and regular audits, adding substantial compliance costs that manufacturers must absorb or pass on to consumers. These pricing factors particularly affect emerging markets, where lower disposable incomes restrict consumer access to premium products, limiting global market growth. The price disparity also impacts retail distribution channels, as many retailers allocate limited shelf space to higher-priced alternatives, further constraining market expansion.

Intense competition from traditional meat products

Conventional meat products maintain a strong market position through established supply chains, consumer familiarity, and competitive pricing, which creates entry barriers for gluten-free alternatives. Traditional meat producers have enhanced their competitive position by improving quality, lowering prices, and highlighting nutritional benefits, making it challenging for alternatives to differentiate beyond dietary requirements. The meat industry's marketing capabilities and retail distribution networks provide competitive advantages that alternative protein companies must address through innovation or targeted market positioning. Consumer research indicates skepticism about the nutritional content and safety of plant-based alternatives, particularly regarding processing methods and ingredient composition. These market conditions require alternative protein companies to allocate significant resources to consumer education and product development, which affects profitability and market expansion capabilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Burgers Lead While Nuggets Drive Innovation

Burgers dominate the market with a 35.02% share in 2025, driven by consumer familiarity and manufacturers' success in replicating conventional meat characteristics. The segment's growth is supported by extensive foodservice partnerships with major restaurant chains and strategic retail positioning in high-traffic store locations. This positioning increases product visibility and enables consumer trial across multiple channels, including quick-service restaurants, casual dining establishments, and retail stores. The burger segment's success is further enhanced by continuous product improvements in taste, texture, and cooking performance, making them increasingly comparable to traditional meat options.

Nuggets are emerging as the fastest-growing segment with a projected CAGR of 10.24% through 2031. This expansion reflects convenience-driven consumption patterns and successful product launches, including Impossible Foods' Disney-themed products that target families and address the growing demand for accessible plant-based options. Sausages maintain steady growth through diversification into breakfast and snack categories while retaining strong performance in traditional meals. Patties continue to see robust demand in foodservice, where restaurants can integrate plant-based alternatives without substantial menu modifications.

By Source: Pea Protein Gains Ground Against Tofu Dominance

Tofu commands a 27.05% market share in 2025, supported by well-established supply chains and strong acceptance in Asian markets where soy-based proteins are integrated into traditional cuisines and daily diets. Its versatility in cooking applications, from stir-fries to desserts, combined with its high protein content and affordable price point, maintains its market leadership position. Additionally, tofu's minimal processing requirements and established manufacturing infrastructure contribute to its cost-effectiveness and widespread availability. Pea protein appeals to consumers with dietary restrictions due to its hypoallergenic and gluten-free properties, while its neutral taste enables broad application across product categories.

Pea protein exhibits the strongest growth trajectory with a 9.32% CAGR through 2031, driven by advancements in protein extraction and processing technologies that improve its functionality and taste. Tempeh presents substantial growth opportunities, offering enhanced digestibility and nutritional benefits through fermentation compared to standard protein isolates. Emerging protein sources, including fava beans and lupins, contribute to addressing sustainability requirements while delivering improved product functionality.

By Form: Fresh/Chilled Gains Momentum Despite Frozen Leadership

The frozen format dominates with a 47.15% market share in 2025, driven by extended shelf life, established cold chain infrastructure, and consumer acceptance of frozen convenience foods. Frozen products enable manufacturers to achieve economies of scale in production and distribution while maintaining quality and safety standards for gluten-free certification. The format's success stems from its ability to preserve nutritional value, reduce food waste, and provide year-round availability of seasonal products. Additionally, frozen products offer consistent quality, simplified inventory management, and reduced transportation costs due to bulk shipping capabilities.

The fresh/chilled segment demonstrates a higher growth rate at 8.58% CAGR through 2031, as consumers increasingly prefer products perceived as fresher and less processed. Fresh products generate higher prices and margins but require sophisticated supply chain management. Improved packaging and preservation technologies extend fresh product shelf life, enabling expansion beyond premium market segments. Companies successfully managing fresh product operations can capture increased market value as consumer preference for minimally processed options grows.

By Distribution Channel: On-Trade Growth Accelerates Despite Off-Trade Dominance

Off-trade channels account for 63.88% of the market share in 2025, with supermarkets and hypermarkets functioning as the primary distribution points for gluten-free meat alternatives. These retail outlets provide extensive product visibility through dedicated shelf space, strategic in-store placement, and targeted merchandising opportunities that increase category awareness. Online retail within the off-trade segment facilitates direct consumer relationships through personalized marketing, flexible delivery options, and subscription models, improving customer retention and purchase frequency.

The on-trade segment is expected to grow at 8.74% CAGR through 2031, driven by restaurants and foodservice operators incorporating plant-based alternatives into their menus. Quick-service restaurants, casual dining establishments, and institutional foodservice providers are expanding their plant-based offerings to meet growing consumer demand. This distribution pattern demonstrates the category's transition from niche health products to mainstream food options, with both channels contributing to market expansion through diverse consumer touchpoints and consumption occasions.

Geography Analysis

North America dominates with a 34.62% market share in 2025, supported by well-established celiac advocacy groups and stringent labeling regulations. The region's retail infrastructure demonstrates significant market penetration, with stores maintaining approximately 150 plant-based product variants per location. Venture capital funding plays a crucial role in the market's development, enabling startups to accelerate product innovation and efficiently bring new offerings to consumers. The strong presence of health-conscious consumers and increasing dietary awareness further reinforces North America's market position.

Asia-Pacific emerges as the fastest-growing region with a 9.14% CAGR through 2031. The market expansion is primarily driven by state climate policies that actively encourage institutional buyers to reduce animal protein consumption. The region's evolving market infrastructure, combined with increasing consumer awareness of health benefits and environmental sustainability, strengthens its industry position. Growing urbanization and rising disposable incomes in key markets contribute to the sustained demand for plant-based alternatives.

Europe maintains its position as the second-largest market, supported by EU investments of EUR 38 million in sustainable protein research and development for 2024. Germany's funding for texture research facilities and retail restrictions in Sweden and the Netherlands contribute to increased plant-based sales. While South America and the Middle East/Africa show initial interest from urban millennials, market expansion depends on competitive pricing and consumer awareness. Public procurement policies and evolving consumer preferences across these regions establish a foundation for future growth.

Competitive Landscape

The gluten-free meat alternatives market is moderately fragmented, with the top five players Beyond Meat Inc., Impossible Foods Inc., Conagra Brands, Inc., Abbot’s Butcher, Inc., and Maple Leaf Foods Inc. accounting for a significant portion of the revenue. This dominance leaves room for regional disruptors to establish themselves in the market. Beyond Meat and Impossible Foods have successfully retained their market presence through extensive deployments in quick-service restaurants (QSRs) and aggressive brand storytelling. However, their gross margins remain vulnerable to fluctuations in the cost of pea protein, a key ingredient in their products.

Technological advancements are emerging as a critical factor in gaining a competitive edge within the market. Companies that invest in innovations such as continuous-flow high-moisture extruders and inline spectroscopy can achieve reduced batch variability, which is essential for maintaining consistent product quality. These advancements also help build long-term retailer confidence, a crucial aspect of sustaining market share. On the other hand, start-ups lacking access to such technologies are focusing on untapped opportunities, such as allergen-compliant “top-8-free” product formats and whole-food ingredient lists with fewer isolates, to differentiate themselves and cater to niche consumer demands.

Strategic collaborations are becoming increasingly prevalent as companies seek to mitigate costs and enhance operational efficiency. Partnerships involving ingredient co-development and shared pilot plants are gaining traction across the gluten-free meat alternatives market. These alliances enable firms to pool resources, reduce production costs, and accelerate product innovation. As the market continues to evolve, such collaborative efforts are expected to play a significant role in shaping the competitive landscape and driving growth in the forecast period.

Gluten Free Meat Substitutes Industry Leaders

-

Beyond Meat Inc.

-

Impossible Foods Inc.

-

Conagra Brands, Inc.

-

Abbot’s Butcher, Inc.

-

Maple Leaf Foods Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Beyond Meat launched its Beyond Steak vegan product in the UK through 650 Tesco stores nationwide. The product contains 24 g of protein per 100 g with minimal saturated fat and replicates traditional beef characteristics. The product has received multiple recognitions, including Platinum at the 2024 Plant-Based Excellence Awards, Gold at the 2023 Casual Dining Awards, and the American Heart Association's certification as a heart-healthy plant-based product.

- March 2025: CV Sciences, a U.S.-based natural ingredients specialist, introduced Lunar Fox Food Co., offering gluten-free, plant-based products through select retailers and online platforms. The product range includes dairy-free cheese, egg substitutes for cooking, and two meatless crumbles - Italian-style "Mangia!" and Mexican-style "Fiesta!" The company also offers a meat-free Italian "Bolognese!" sauce incorporating the Mangia! crumble.

- October 2024: Chunk Foods, an Israeli food-tech startup, entered the U.S. retail market with its plant-based whole-cut steaks in Los Angeles and New York City stores. The product line features high-protein options including 4 oz and 6 oz steaks, a 10 oz slab, and 8 oz pulled meat. The products are manufactured using a proprietary solid-state fermentation process that enhances texture and flavor without additives. The steaks are clean-label, soy-based, non-GMO, and fortified with iron and B12.

- May 2023: Switch Foods, a UAE-based food-tech startup established in 2022, opened its first plant-based meat production facility in Abu Dhabi's Khalifa Economic Zone (KEZAD). The 20,000 ft² facility, supported by UAE Minister of Climate Change and Environment Mariam Almheiri, produces GMO-free, allergen-free, gluten-free, soy-free, vegan, and halal-certified meat alternatives. The product range includes kebabs, kofta/kafta, soujuk, minced meat, burger patties, and plant-based chicken using pea protein.

Global Gluten Free Meat Substitutes Market Report Scope

The global gluten-free meat substitutes market has been segmented by source (which includes Soy and Mycoprotein); by category (which includes Frozen/Refrigerated and unfrozen) and by geography (which includes North America, Europe, Asia-Pacific, South America and Middle East and Africa).

| Burgers |

| Sausages |

| Nuggets |

| Patties |

| Other Product Types |

| Pea |

| Tofu |

| Tempeh |

| Other Sources |

| Fresh/Chilled |

| Frozen |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| On-Trade |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Netherlands | |

| Italy | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Nigeria | |

| Saudi Arabia | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Burgers | |

| Sausages | ||

| Nuggets | ||

| Patties | ||

| Other Product Types | ||

| By Source | Pea | |

| Tofu | ||

| Tempeh | ||

| Other Sources | ||

| By Form | Fresh/Chilled | |

| Frozen | ||

| By Distribution Channel | Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| On-Trade | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Netherlands | ||

| Italy | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Nigeria | ||

| Saudi Arabia | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the gluten-free meat alternatives market?

The market is worth USD 10.87 billion in 2026 and is projected to hit USD 16.22 billion by 2031.

Which product type leads revenue currently?

Burgers hold the largest 35.02% share of 2025 sales, benefiting from wide foodservice penetration.

Which geographic region is growing fastest?

Asia-Pacific is forecast to post a 9.14% CAGR through 2031 as middle-class consumers trade up to certified plant proteins.

Why are production costs still high?

Specialized gluten-free facilities, premium protein isolates and certification audits keep costs at 2-2.5 × conventional meat levels.

Page last updated on: