Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

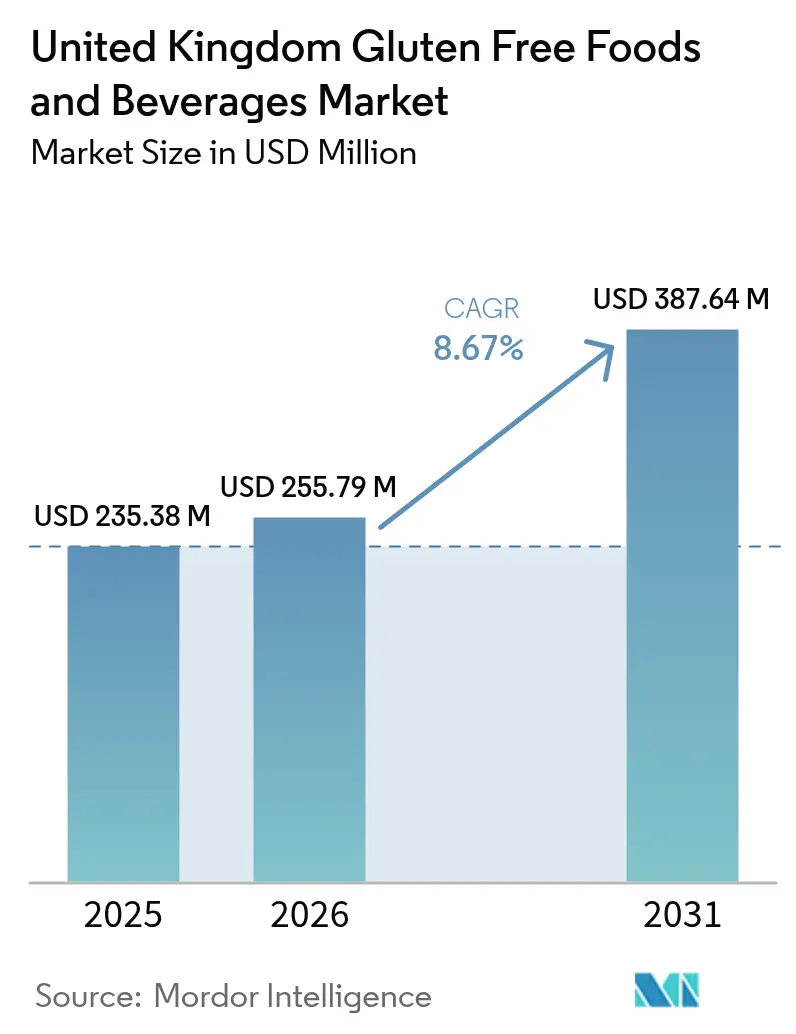

| Base Year Market Size (2025) | USD 235.38 Million |

| Market Size (2026) | USD 255.79 Million |

| Market Size (2031) | USD 387.64 Million |

| Growth Rate (2026 - 2031) | 8.67% CAGR |

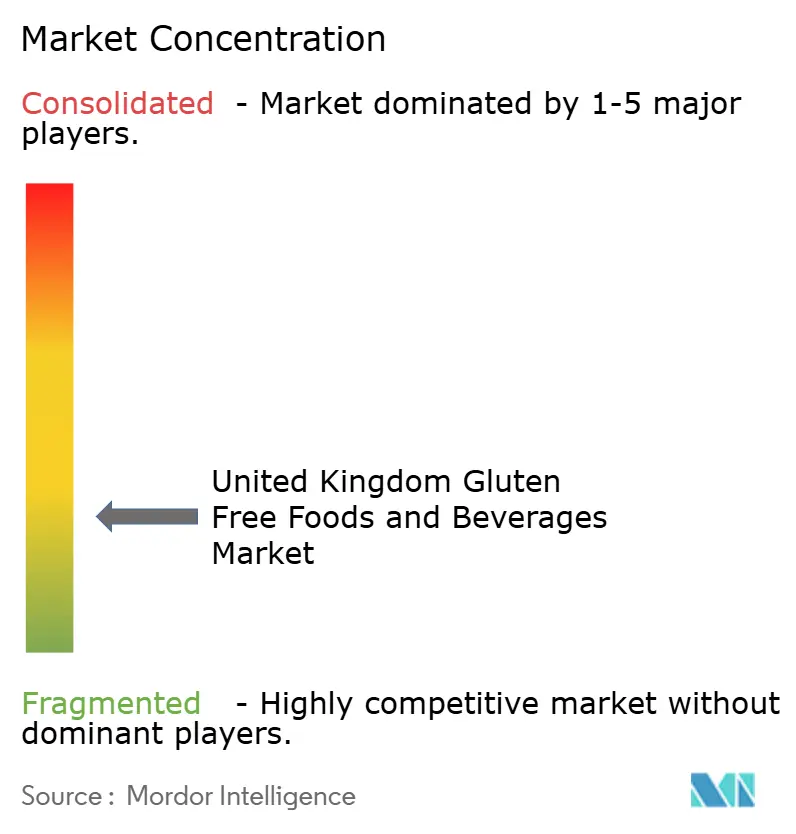

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United Kingdom Gluten Free Foods And Beverages Market Analysis by Mordor Intelligence

The United Kingdom gluten free food and beverage market size is expected to grow from USD 235.38 million in 2025 to USD 255.79 million in 2026 and is forecast to reach USD 387.64 million by 2031 at 8.67% CAGR over 2026-2031. This expansion is fueled by clinical demand from individuals diagnosed with coeliac disease and the increasing adoption of gluten-free products by health-conscious consumers. Many consumers are choosing gluten-free options not only to maintain health and alleviate gastrointestinal issues but also as part of a healthier lifestyle. Despite cost-of-living challenges, demand remains strong due to the essential nature of medically prescribed diets and the pursuit of perceived digestive benefits by wellness-focused individuals. Although premium pricing poses challenges, advancements in ingredient technology, expanded supermarket availability, and policy measures such as Wales’ subsidy card launching in autumn 2025 are improving accessibility. Manufacturers are prioritizing research and development to enhance product texture, while stricter Food Standards Agency (FSA) regulations enforcing the 20 mg/kg gluten threshold continue to strengthen consumer confidence.

Key Report Takeaways

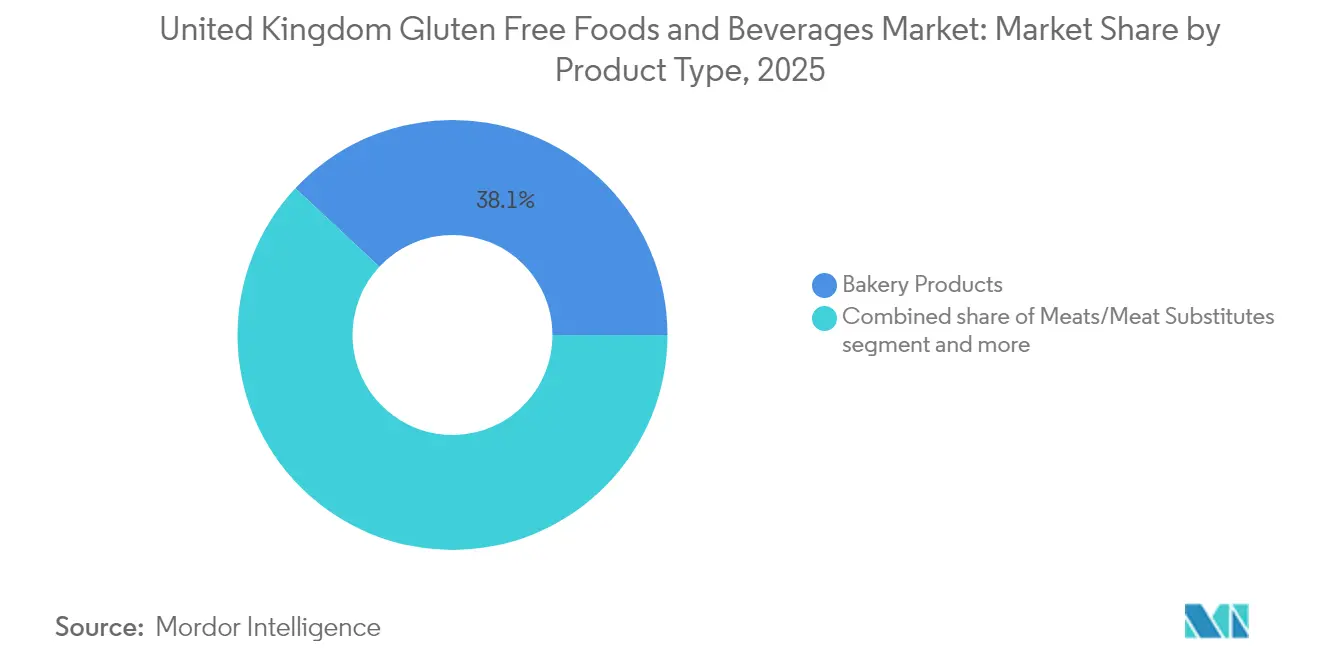

- By product type, bakery products led with 38.05% of the United Kingdom gluten-free food and beverage market share in 2025, while beverages recorded the fastest growth at an 8.79% CAGR through 2031.

- By nature, conventional items captured 75.12% share of the United Kingdom gluten-free food and beverage market size in 2025, whereas organic offerings are advancing at a 9.41% CAGR to 2031.

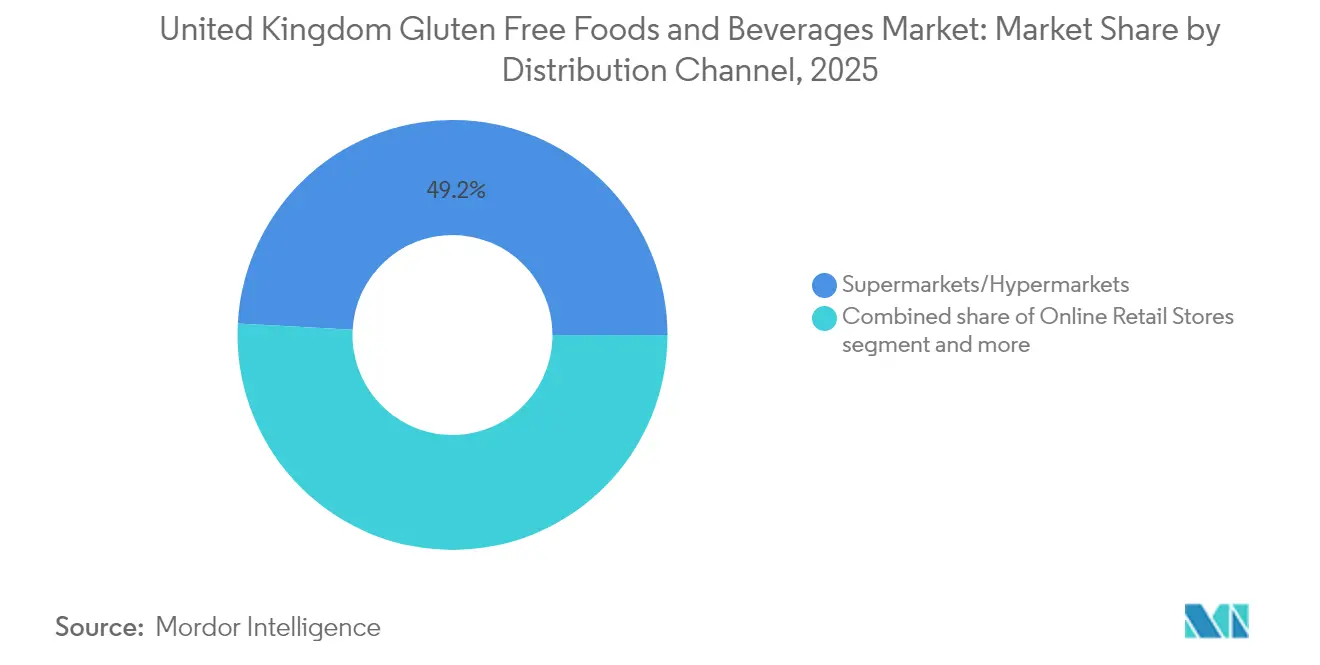

- By distribution channel, supermarkets and hypermarkets held 49.15% of the United Kingdom gluten-free food and beverage market size in 2025, and online retail stores are projected to expand at a 10.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Gluten Free Foods And Beverages Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of coeliac disease and gluten intolerances | +1.5% | National, higher urban concentration | Long term (≥ 4 years) |

| Trend towards specialized and clean label diets | +1.8% | National, premium segments in South East England | Medium term (2-4 years) |

| Growing consumer awareness of gluten-free health benefits | +1.2% | National, health-conscious demographics | Medium term (2-4 years) |

| Enhanced labelling regulations and certification schemes | +0.9% | National, FSA compliance requirements | Short term (≤ 2 years) |

| Expansion in product innovation | +1.1% | National | Medium term (2-4 years) |

| Consumer focus on allergen-free and plant-based diets | +0.7% | National, metropolitan penetration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of celiac disease and gluten intolerances

With advancements in NHS screening protocols and targeted awareness campaigns, clinical diagnosis rates for coeliac disease are increasing. NHS England's national centre for adult coeliac disease has implemented telemedicine and remote monitoring, improving access to specialist care and dietary guidance. This enhanced medical infrastructure supports patients in maintaining gluten-free nutrition protocols and drives consistent demand for certified gluten-free products. In 2024, the Coeliac Organization reports that approximately 500,000 individuals in the UK remain undiagnosed with coeliac disease[1]Source: Coeliac Organization, "Coeliac UK Awareness Month 2024", www.coeliac.org.uk. For those diagnosed, having access to safe, certified gluten-free products is essential for effective condition management. The market is further driven by healthcare efforts to identify and address undiagnosed cases. Additionally, some consumers are adopting gluten-free products due to gluten sensitivities or lifestyle preferences influenced by increased awareness of celiac disease.

Trend towards specialized and clean label diets

Consumers are shifting towards specialized diets not only for medical reasons but also due to a growing emphasis on wellness and ingredient transparency. In Europe, particularly among Generation Z, there is a clear trend of prioritizing high-quality, fresh, and healthier products. Notably, one in three consumers is willing to pay a premium for nutrition that focuses on health. This trend is driving market growth beyond the traditional coeliac patient base, as health-conscious individuals increasingly choose gluten-free products for perceived digestive benefits or general wellness. The clean-label trend complements the gluten-free movement, with manufacturers removing artificial preservatives, colors, and additives to meet the demand for ingredient transparency. For example, Schär focuses on preservative-free formulations across its product range. At the same time, emerging brands are targeting premium market segments by emphasizing minimal ingredient lists and organic certifications.

Growing consumer awareness of gluten-free health benefits

Educational initiatives led by NHS services and patient advocacy organizations have broadened awareness of gluten-related disorders beyond the traditional focus on coeliac disease. According to the NHS, coeliac disease affects approximately 1 in every 100 individuals in the UK[2]Source: National Health Service, "Overview-Coeliac disease", www.nhs.uk. Coeliac UK's educational campaigns, along with NHS guidance, highlight the necessity of strict gluten avoidance to prevent long-term complications such as malabsorption, increased cancer risks, and higher mortality rates. The organization's advocacy efforts have enhanced consumer trust in gluten-free labeling standards and cross-contamination prevention measures. The adoption of digital health platforms and telemedicine during the pandemic has improved access to dietary counseling and specialist support, aiding patients in maintaining gluten-free diets. Additionally, rising disposable income in the UK has driven greater consumer spending on health and wellness products. In 2023, the average equivalized disposable household income in the UK was GBP 34,462[3]Source: Office for National Statistics (UK), "The effects of taxes and benefits on household income", www.ons.gov.uk, supporting the growth of the gluten-free foods and beverages market.

Enhanced labelling regulations and certification schemes

The Food Standards Agency (FSA) has enhanced its enforcement mechanisms by introducing improvement notices. These notices provide a proportionate response to violations of nutrition and health claims, replacing immediate criminal prosecutions with a phased compliance approach. The FSA enforces a mandatory 20mg/kg gluten threshold as the legal standard for gluten-free claims, with technical guidance emphasizing robust production controls and testing protocols to ensure compliance. Under Natasha's Law, allergen information requirements have expanded, mandating full ingredient and allergen labeling for prepackaged-for-direct-sale products. This regulation significantly impacts bakeries, sandwich shops, and foodservice operators offering gluten-free options. Additionally, the FSA is consulting on best practice guidance for allergen information in non-prepacked foods, proposing mandatory written allergen information and trained staff requirements. By maintaining high standards of safety and transparency, these labeling regulations and certification schemes enhance consumer confidence, expand the gluten-free consumer base, and encourage manufacturers and retailers to increase their gluten-free product offerings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium price positioning limits mass adoption | -1.2% | National, acute in lower-income households | Short term (≤ 2 years) |

| Taste, texture and sensory limitations | -0.8% | National, mainstream consumer acceptance | Medium term (2-4 years) |

| Raw-material supply volatility | -0.6% | National, global grain dependencies | Short term (≤ 2 years) |

| Complex regulatory and certification requirements | -0.4% | National, FSA compliance standards | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium price positioning limits mass adoption

Affordability constraints continue to pose a significant challenge to the growth of the gluten-free market, as staple gluten-free products in major UK supermarkets are priced approximately 45% higher than their conventional counterparts. According to Coeliac UK, individuals with coeliac disease face an additional financial burden, spending about 35% more on weekly food shopping compared to the general population. Specifically, gluten-free loaves are priced 4.5 times higher, and bread rolls cost 3.1 times more on a gram-for-gram basis than standard alternatives. These affordability issues have been further exacerbated by rising cost-of-living pressures, which have driven consumers to downtrade and reduce spending on premium food categories. Recognizing these challenges, Wales introduced the UK's first gluten-free subsidy card in autumn 2025. This initiative is designed to improve the affordability of gluten-free foods, reduce the medicalization associated with accessing such products, and alleviate administrative burdens on NHS resources, thereby addressing both consumer and systemic challenges in the gluten-free market.

Taste, texture, and sensory limitations

Despite advances in formulation science, gluten-free products still lag behind their conventional counterparts in sensory quality, hindering their mainstream acceptance. In UK market tests, gluten-free products often fall short on taste, texture, and aroma, leaving consumer expectations for gluten-free bread largely unmet. Innovators are turning to functional ingredients like psyllium powder. When substituted at 50% with rice flour, it yields gluten-free bread rolls that boast improved volume, a softer texture, and greater consumer acceptance, albeit with a darker coloration. Prozymi Biolabs, hailing from Edinburgh, is crafting enzymatic solutions. These solutions aim to selectively break down immunogenic gluten proteins, retaining the desired texture. However, the technology still needs fine-tuning to ensure gluten levels are safe for celiac patients. Meanwhile, strategies that incorporate legumes, such as chickpea, lentil, and lupin flours, show promise in boosting protein content and enhancing texture, all while keeping the products gluten-free. Yet, for these innovations to thrive commercially, further formulation optimization is essential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bakery Products Anchor Sales Momentum

The bakery category generated 38.05% of the United Kingdom's gluten-free food and beverage market size in 2025, emphasizing the significance of bread, rolls, and breakfast items in the nation's diet. Companies such as Warburtons and Promise Gluten Free are expanding into crumpets and bagels, focusing on replicating traditional textures. Advances like rice-sourdough blends and psyllium supplementation are improving softness, a critical factor in attracting new consumers. Meanwhile, the beverage segment experienced the fastest growth with an 8.79% CAGR (2026-2031), driven by gluten-free craft beers and oat drinks targeting flexitarian consumers. This strong growth pattern is diversifying revenues for suppliers that previously concentrated on solid foods.

Pub operators are also leveraging this trend by offering inclusive menus featuring gluten-removed lagers and sorghum-based ales as staples. Snacks and ready-to-eat products are gaining popularity with options like brownie bites and mini honeygrams, catering to impulse purchases. While sauces and seasonings contribute a smaller but steady share, they highlight the importance of flavor enhancers in restricted diets. Meat and dairy alternatives are capturing incremental market share by appealing to those with lactose intolerance or a preference for plant-based proteins. As these segments develop further, cross-category multipacks and bundle promotions in supermarkets are expected to increase household penetration in the UK's gluten-free market.

By Nature: Conventional Dominance with Organic Upswing

Conventional products held a commanding 75.12% share of the UK's gluten-free food and beverage market in 2025. Their extensive availability, cost-effectiveness, and emphasis on staple products, supported by well-established brands, meet the needs of most gluten-free consumers. While conventional products dominate the market, primarily appealing to health-focused and lifestyle-oriented buyers, the organic segment is growing at a strong 9.41% CAGR (2026-2031). This growth stems from consumers linking gluten-free options with the broader clean eating trend. Brands are increasingly utilizing heritage grains, such as millet grown without synthetic pesticides, to achieve organic certification and support biodiversity goals. Corporate initiatives like Dr. Schär’s VitaMì pilot highlight a dedication to sustainable supply chains, which could shape future product offerings.

The organic segment's expansion is further supported by EU-UK equivalence rulings, which simplify cross-border logistics for certified inputs. Packaging with eco-labels communicates both allergen safety and environmental responsibility, appealing particularly to younger consumers. While conventional products remain essential for mass distribution channels—often the only tier eligible for reimbursement under subsidy programs—premium organic products are finding profitability in specialty retailers and online subscription services. This has prompted many suppliers in the UK gluten-free market to adopt a dual-track strategy, balancing conventional and organic product lines.

By Distribution Channel: Supermarkets Retain Bulk, Online Surges

Supermarkets and hypermarkets led the category, contributing 49.15% of its value in 2025. Shoppers preferred these outlets for their weekly grocery missions due to the convenience of one-stop shopping. Chains enhanced navigation with shelf-edge labeling and dedicated free-from bays, while many introduced private-label gluten-free assortments to improve affordability. Although traditional outlets experienced steady growth, the online segment grew significantly at a 10.05% CAGR (2026-2031). This growth was driven by product discovery tools, doorstep delivery, and recurring basket lists that simplified repeat purchases. Direct-to-consumer bakery subscriptions gained traction by offering freshness and variety, fostering brand loyalty in a category where texture deteriorates quickly.

Specialty health stores continued to strengthen their position in the market by offering curated assortments tailored to specific consumer needs and leveraging the expertise of their staff to provide personalized recommendations. Meanwhile, other distribution channels, such as pharmacies and health food stores, played a crucial role in serving niche markets. These channels were particularly important for prescription-eligible products and for offering specialized consultation services, catering to consumers with specific health and dietary requirements.

Geography Analysis

The United Kingdom boasts a well-established gluten-free market, complete with regulatory frameworks and widespread retail distribution. However, disparities in prescription policies and retail density across regions lead to uneven access and affordability of products. In autumn 2025, Wales pioneered the UK's first gluten-free subsidy card program, offering quarterly top-ups for contactless purchases in supermarkets and online. This policy innovation seeks to de-medicalize access to gluten-free foods and lighten the administrative load on GP practices and pharmacies, potentially setting a precedent for nationwide adoption. England, while home to the largest market concentration and a robust presence of both supermarkets and specialty retailers, grapples with inconsistent access to subsidized gluten-free staples due to varying prescription policies across Clinical Commissioning Groups.

Scotland, under the watchful eye of Food Standards Scotland, aligns its regulatory approach with FSA England to ensure uniform gluten-free labeling standards, all the while tailoring to local market nuances. Northern Ireland, navigating the complexities of the Windsor Framework, faces challenges with the expanded NIRMS Phase 3 labeling. Starting July 2025, broader categories of goods moving from Great Britain will require individual 'Not for EU' labels. Retail dynamics differ regionally: London leads in online grocery adoption, whereas the North East leans towards in-store shopping. This divergence shapes distribution strategies for gluten-free brands aiming at specific geographic segments.

Urban locales benefit from a dense supermarket presence and specialty retailers, ensuring better product availability and competitive pricing. In contrast, rural areas contend with limited selections and elevated transportation costs for gluten-free options. The FSA has raised alarms over local authorities' capacity to enforce food standards, hinting at potential geographic discrepancies in compliance monitoring and allergen labeling. This concern is especially pertinent for smaller producers and foodservice operators in regions with fewer inspection resources. While government-backed regulatory sandbox initiatives and new food approval pathways promise to spur innovation across the UK, market entry tends to favor metropolitan hubs before reaching secondary markets.

Competitive Landscape

The United Kingdom gluten-free market demonstrates moderate concentration, with established multinational companies maintaining strong positions through brand recognition, retail partnerships, and product innovation. Dr. Schär leads the market with its European dominance and a portfolio of over 200 gluten-free products across various categories, supported by its Warrington headquarters and Glasgow production facility. Domestic players like Warburtons utilize their expertise in mainstream bakery to expand their gluten-free product lines, including sandwich thins, crumpets, and white rolls, leveraging established supermarket relationships to secure shelf space and encourage consumer trials. Competition is intensifying as companies focus on direct-to-consumer strategies, premium positioning, and technological advancements rather than solely competing on price.

Emerging disruptors are concentrating on innovative ingredient technologies and specialized formulations to address ongoing taste and texture challenges that limit mainstream adoption. Innovation remains a critical area of competition. Prozymi Biolabs is developing enzyme technology that neutralizes immunogenic gluten fragments while preserving bread structure, attracting funding from Innovate UK. In August 2024, Lancaster Colony introduced frozen garlic Texas toast, produced in a dedicated gluten-free facility to ensure safe manufacturing practices.

Global giants are prioritizing geographical expansion as a key strategy to capture market share, while local players are focusing on product innovation to attract millennial consumers who are open to trying new products and are highly brand-conscious. This trend across various food industries is creating opportunities for manufacturers to diversify their offerings. Major players in the market include Dr. Schär, The Kraft Heinz Company, Warburtons Limited, Genius Foods, and Nestlé SA. The Competition and Markets Authority, empowered by the Digital Markets, Competition and Consumers Act 2024, has increased regulatory oversight on misleading labeling and anti-competitive practices, with penalties of up to 10% of global turnover for violations.

United Kingdom Gluten Free Foods And Beverages Industry Leaders

-

Dr. Schär

-

The Kraft Heinz Company

-

Warburtons Limited

-

Genius Foods

-

Nestle SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Warburtons has introduced two new additions to its free-from lineup: Gluten Free Soft Brown Pittas and Gluten Free Seeded Tiger Bloomer. These Soft Brown Pittas, rich in fiber, are certified by Cross Grain and are completely free from gluten, wheat, and milk.

- May 2025: Crave, the free-from snack brand, has introduced a gluten-free wafer biscuit to its sweet biscuit lineup in the UK. The new vanilla cream-filled wafers are branded as "Pink Cheetahs" and are aptly colored to match the name.

- April 2025: Haldiram, India's renowned snacks group, has launched its Khaas Collection, a premium range of gluten-free traditional sweets, targeting the UK market.

- October 2024: Dr. Schär has introduced three new gluten-free snacks: Peanut Butter Blondie Bites, Chocolate Brownie Bites, and Mini Honeygrams. The Peanut Butter Blondie Bites deliver a delightful mix of creamy and crunchy textures, whereas the Chocolate Brownie Bites boast a deep chocolate flavor complemented by a crispy wafer center.

United Kingdom Gluten Free Foods And Beverages Market Report Scope

Gluten-free food and beverages exclude foods containing gluten. Gluten is a protein found in wheat, barley, rye, and triticale. The UK gluten-free foods and beverages market is segmented by type into beverages, bakery and confectionery, condiments, seasonings and spreads, dairy/dairy substitutes, meat/meat substitutes, and other types. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, specialty stores, online retail stores, and other distribution channels. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

By Product Type

| Bakery Products |

| Meats/Meat Substitutes |

| Dairy/Dairy Substitutes |

| Sauces, Dressings, and Seasonings |

| Snacks and RTE Products |

| Beverages |

| Other Product Types |

By Nature

| Conventional |

| Organic |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| By Product Type | Bakery Products |

| Meats/Meat Substitutes | |

| Dairy/Dairy Substitutes | |

| Sauces, Dressings, and Seasonings | |

| Snacks and RTE Products | |

| Beverages | |

| Other Product Types | |

| By Nature | Conventional |

| Organic | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

Key Questions Answered in the Report

How large is the United Kingdom gluten free food and beverage market in 2026?

It stands at USD 255.79 million and is projected to climb to USD 387.64 million by 2031 at an 8.67% CAGR.

Which product category generates the highest revenue?

Bakery products command 38.05% of category value thanks to consumer reliance on bread and related staples.

What policy recently improved affordability for coeliac patients in Wales?

A subsidy card launched in July 2025 offers quarterly allowances that can be spent in supermarkets or online.

Why do some shoppers still hesitate to buy gluten-free items?

Premium price premiums of around 35% and ongoing taste or texture gaps restrain broader adoption.

Page last updated on: