Gluten-Free Ready Meals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.14 Billion |

| Market Size (2031) | USD 2.81 Billion |

| Growth Rate (2026 - 2031) | 5.56% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

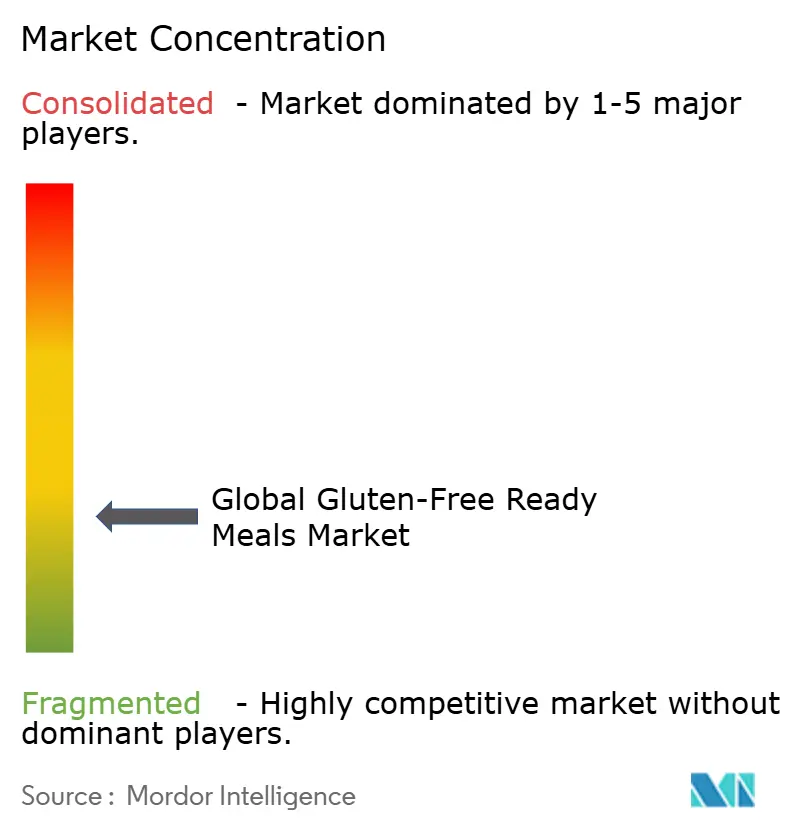

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Gluten-Free Ready Meals Market Analysis by Mordor Intelligence

The gluten-free ready meals market size in 2026 is estimated at USD 2.14 billion, growing from 2025 value of USD 2.03 billion with 2031 projections showing USD 2.81 billion, growing at 5.56% CAGR over 2026-2031. This growth trajectory reflects the intersection of regulatory standardization, demographic shifts, and technological innovations that have transformed gluten-free products from niche medical necessities into mainstream convenience foods. Technological advances in non-thermal preservation methods, including high-pressure processing and cold plasma treatments, are addressing the shelf-life constraints that have historically limited the expansion of premium products. These innovations, combined with the growing prevalence of diagnosed celiac disease and expanding consumer base seeking gluten-free options for perceived health benefits, position the market for sustained growth despite cost and quality challenges.

Key Report Takeaways

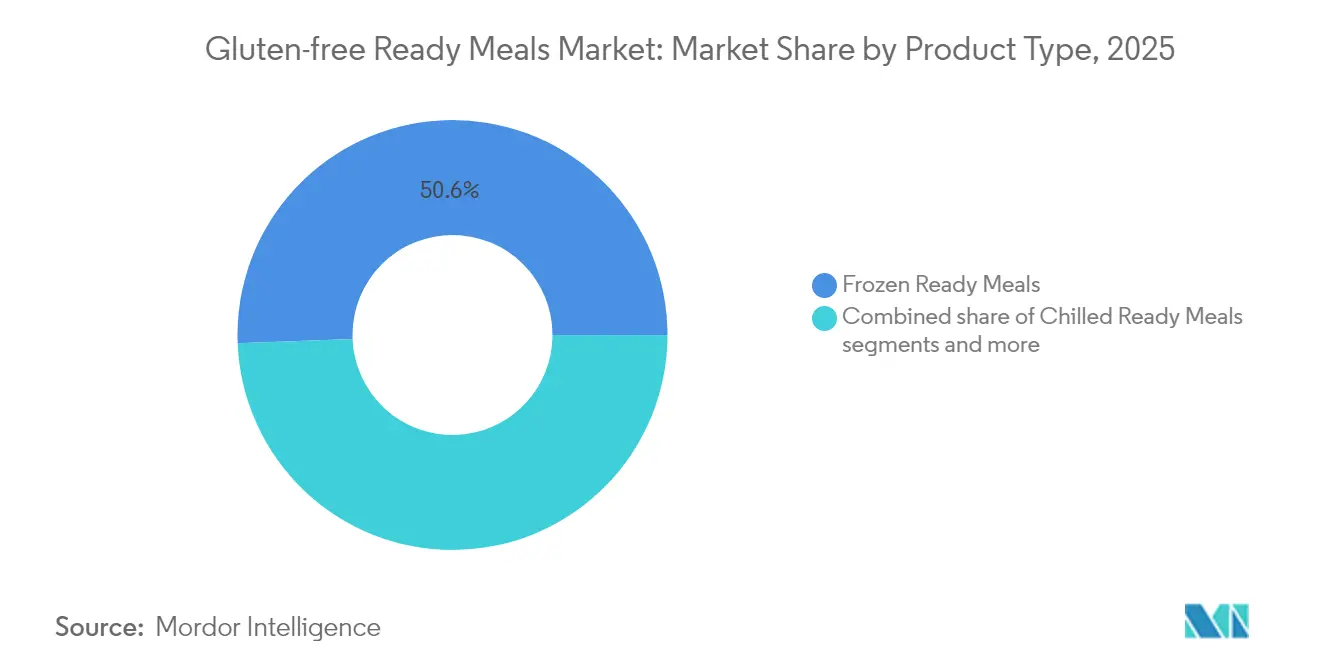

- By product type, frozen ready meals led with 50.62% of the gluten-free ready meals market share in 2025; chilled variants are forecast to expand at a 5.79% CAGR through 2031.

- By category, non-vegetarian options accounted for 57.84% share of the gluten-free ready meals market size in 2025, while vegetarian offerings are projected to grow at 6.18% CAGR between 2026-2031.

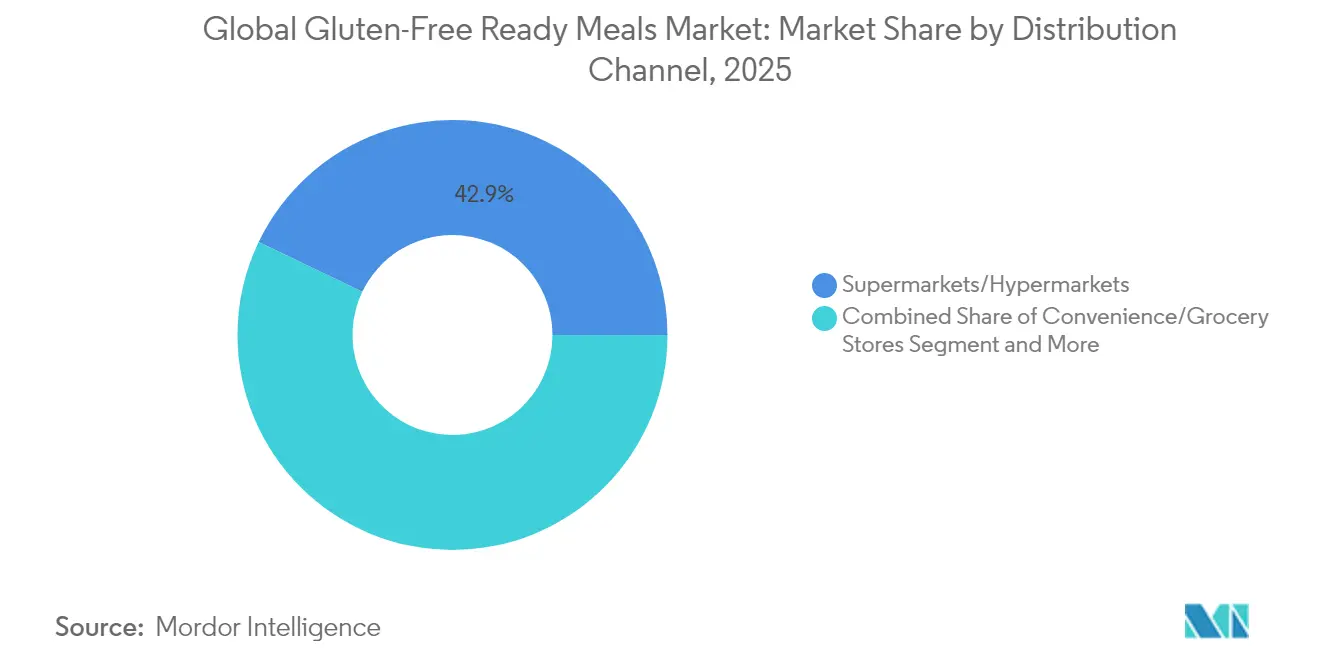

- By distribution channel, supermarkets and hypermarkets held 42.88% share of the gluten-free ready meals market size in 2025; online retail is anticipated to advance at 6.33% CAGR over 2026-2031.

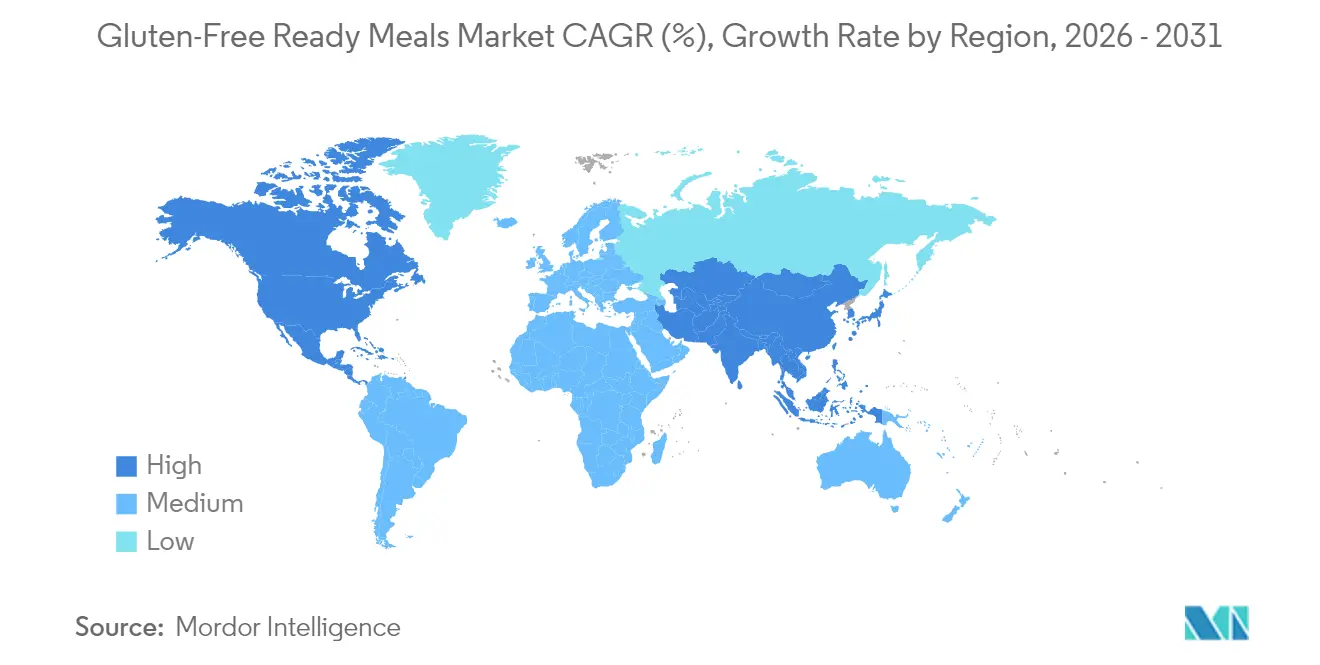

- By geography, North America captured 39.92% of the gluten-free ready meals market share in 2025, while Asia-Pacific is poised to record the highest regional CAGR at 6.71% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gluten-Free Ready Meals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Celiac Disease and Gluten Sensitivity | +1.2% | Global, with higher impact in North America and Europe | Long term (≥ 4 years) |

| Growing Health and Wellness Awareness | +0.9% | Global, strongest in developed markets | Medium term (2-4 years) |

| Innovation in Plant-Based and Alternative Proteins | +0.7% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Cultural and Ethnic Diversity | +0.5% | North America, Europe, urban Asia-Pacific centers | Long term (≥ 4 years) |

| Flavor and Culinary Trends | +0.4% | Global, led by developed markets | Short term (≤ 2 years) |

| Government Regulations and Labeling | +0.3% | Global, with regional variations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of celiac disease and gluten sensitivity

The medical demand for gluten-free ready meals primarily stems from celiac disease, which affects approximately 1% of the global population[1]National Library of Medicine, "Celiac Disease Affects 1% of Global Population," pubmed.ncbi.nlm.nih.gov.The United States Food and Drug Administration (FDA) estimates that 3 million Americans have celiac disease, forming a core consumer base that requires strict gluten avoidance[2]U.S. Food and Drug Administration, “Gluten and Food Labeling,” fda.gov. Beyond medical necessity, the market growth is driven by increasing health consciousness among consumers, rising disposable incomes, and growing awareness of gluten sensitivity. The convenience factor of ready-to-eat meals, combined with improved taste and texture of gluten-free products, has expanded the consumer base beyond those with medical requirements. Additionally, endorsements from healthcare professionals and nutritionists have contributed to the mainstream adoption of gluten-free products.

Growing health and wellness awareness

There is a significant consumer base across the globe following gluten-free diets, including individuals without celiac disease diagnoses. This dietary preference stems from self-reported gluten sensitivity, lifestyle choices, and health objectives. Gluten-free products appeal particularly to millennials seeking clean-label and allergen-free options, as these products are commonly associated with digestive health benefits, weight control, and wellness. The COVID-19 pandemic intensified health-conscious food choices, with factors such as healthy living practices, age, and income levels influencing gluten-free purchasing decisions. This consumer behavior has expanded the demand for gluten-free options across food categories, including bread, pasta, snacks, and desserts.

Innovation in plant-based and alternative proteins

Recent technological developments in plant-based proteins have improved the quality of gluten-free ready meals. Companies such as Roquette offer specialized ingredients like NUTRALYS® Fava S900M, a fava bean isolate with 90% protein content, for meat and dairy alternatives. Fava beans provide both sustainability advantages through nitrogen fixation and functional benefits, including high gel strength and stability. Research indicates that alternative protein sources improve the nutritional value of gluten-free products, with quinoa varieties influencing pasta structure and cooking characteristics. Sorghum-based products offer a lower glycemic index and higher fiber content compared to conventional gluten-free starches. The use of alternative flours such as buckwheat, lentil, and teff creates distinctive products that meet consumer health preferences while addressing the protein gaps typically found in gluten-free diets.

Cultural and ethnic diversity

Demographic shifts and cultural diversity significantly influence market dynamics, as celiac disease prevalence varies across ethnic groups. The increasing multicultural population composition in various regions drives product development and market expansion. Cultural factors beyond medical necessity affect product adoption, including perceived health benefits and dietary preferences within specific communities. The growing ethnic diversity in urban centers particularly shapes consumer demand patterns. Immigration patterns and acculturation impact dietary behaviors, highlighting the need for culturally appropriate nutrition solutions. The globalization of food preferences creates opportunities for ethnic-specific gluten-free ready meals. The rising ethnic population segments in developed markets create distinct consumer preferences and purchasing behaviors. Successful market penetration in diverse communities requires understanding how dietary restrictions align with cultural food traditions, creating opportunities for products that combine ethnic preferences with gluten-free requirements. This demographic driver continues to reshape product innovation, marketing strategies, and distribution channels in the gluten-free ready meals market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Production Costs | -1.1% | Global, most severe in developing markets | Medium term (2-4 years) |

| Short Shelf Life for Premium Products | -0.6% | Global, particularly cold chain dependent regions | Short term (≤ 2 years) |

| Taste and Quality Perception | -0.8% | Global, strongest impact in price-sensitive segments | Long term (≥ 4 years) |

| Limited Appeal in Rural Areas | -0.4% | Rural regions globally, severe in developing countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High production costs

Manufacturing costs for gluten-free ready meals are 2-2.5 times higher than conventional products, creating significant affordability barriers that restrict market expansion. Gluten-free products maintain substantial price premiums, with staple foods experiencing the highest cost differentials. The elevated costs result from multiple factors: specialized ingredient sourcing requiring strict quality controls, investment in dedicated production lines and equipment to prevent cross-contamination, smaller batch sizes reducing economies of scale, and comprehensive testing protocols to meet the FDA's 20 ppm gluten threshold. Additional cost factors include specialized storage facilities, enhanced quality control measures, and increased labor costs for trained personnel. In rural areas, distribution costs compound these manufacturing premiums due to lower population density and longer transportation routes, limiting market growth potential in underserved regions. These combined cost pressures make it challenging for manufacturers to maintain competitive pricing while ensuring product quality and safety, ultimately impacting market penetration and consumer adoption rates.

Taste and quality perception

Sensory characteristics pose significant restraints for the gluten-free ready meal market. The persistent quality gap between gluten-free products and conventional alternatives continues to limit market growth. Consumer preferences strongly favor sweet, porous, and soft textures, with a notable aversion to salty and rubbery characteristics. Despite technological advancements, various gluten-free bread products show improved texture and sensory qualities, with certain products matching wheat-based versions during storage periods. However, achieving optimal texture and flavor remains challenging, particularly in complex ready meal formulations where multiple ingredients interact. Previous experiences with lower-quality gluten-free products have created lasting negative impressions that continue to influence purchasing decisions, requiring manufacturers to prioritize product improvement and implement comprehensive consumer education programs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Frozen Dominance Faces Chilled Innovation

Frozen ready meals are expected to command a 50.62% market share in 2025, reflecting the established supply chain infrastructure and consumer familiarity with frozen convenience foods. The frozen segment benefits from extended shelf life and lower cold chain complexity, making it accessible across diverse retail formats, including convenience stores and rural markets. However, chilled ready meals emerge as the fastest-growing segment with 5.79% CAGR through 2031, driven by premiumization trends and perceived freshness advantages. Chilled products target health-conscious consumers willing to pay premiums for perceived quality, though they face shelf-life constraints that limit distribution reach.

Shelf-stable ready meals occupy a middle position, offering convenience without refrigeration requirements. Freeze-dried ready meals represent the smallest segment but show potential for outdoor recreation and emergency preparedness applications, with innovations in rehydration technology improving palatability. Advanced preservation technologies, including high-pressure processing and cold plasma treatments, are addressing shelf-life limitations across all segments, with research demonstrating significant microbial reduction while maintaining nutritional quality.

By Category: Plant-Based Momentum Challenges Meat Dominance

Non-vegetarian ready meals hold 57.84% market share in 2025. The non-vegetarian segment benefits from established taste profiles and protein content that appeals to mainstream consumers, particularly in markets where meat consumption remains culturally important. Non-vegetarian ready meals offer a quick protein fix without the need for cooking. Health-conscious consumers, seeking convenience, turn to gluten-free variants that still deliver animal protein. Diets such as keto, paleo, and carnivore prioritize animal proteins, often sidelining or restricting gluten-rich grains.

The vegetarian alternatives accelerate at 6.18% CAGR through 2031, reflecting shifting dietary preferences and protein innovation. The vegetarian growth is propelled by plant-based protein innovations, environmental consciousness, and health positioning that extends beyond traditional vegetarian demographics. The vegetarian segment growth also reflects demographic shifts, with younger consumers showing higher acceptance of plant-based alternatives and willingness to pay premiums for perceived health and environmental benefits.

By Distribution Channel: Digital Transformation Accelerates Specialty Access

Supermarkets and hypermarkets maintain a 42.88% market share in 2025, leveraging established gluten-free sections and consumer shopping habits for specialty dietary products. Supermarkets and hypermarkets are reshaping the shopping landscape by uniting a variety of frozen ready meal brands and catering to diverse consumer preferences all in one location. These venues prioritize convenience, boasting amenities such as expansive parking, play areas for children, food courts, and even banking services. Such offerings not only attract a larger consumer base but also propel the segment's expansion. Supermarkets and hypermarkets regularly run promotions, discounts, and loyalty programs that encourage shoppers to try new or premium gluten-free ready meals and increase purchases.

However, online retail stores emerge as the fastest-growing channel with a 6.33% CAGR through 2031. The online channel growth reflects several converging factors, including improved product discovery, subscription services that ensure regular availability, and detailed product information that helps consumers navigate gluten-free requirements. Consumers who are more inclined towards online grocery shopping, closely mirror the primary demographics of gluten-free consumers. This trend is driven by the increasing adoption of digital platforms, convenience, and the growing awareness of gluten-free diets among these groups. However, the online expansion grapples with challenges such as costs associated with cold chain logistics and a consumer habit of examining fresh products before buying. This scenario paves the way for hybrid models, seamlessly blending online orders with in-store pickups or delivery services.

Geography Analysis

North America commands 39.92% market share in 2025, reflecting mature regulatory frameworks, established consumer awareness, and higher celiac disease prevalence among key demographic groups. The region benefits from FDA gluten-free labeling standards implemented since 2013 and widespread retail acceptance of specialty dietary products. However, Asia-Pacific emerges as the fastest-growing region with 6.71% CAGR through 2031, driven by urbanization, rising disposable incomes, and increasing health consciousness among expanding middle-class populations. North America demonstrates mature market characteristics, including widespread retail acceptance, established supply chains, and consumer willingness to pay premiums for specialty dietary products.

Asia-Pacific's growth potential is particularly strong in developed markets like Japan, Australia, and Singapore, where regulatory frameworks support gluten-free labeling and retail infrastructure can accommodate specialty products. The region's growth trajectory depends on continued urbanization, rising disposable incomes, and gradual dietary westernization that creates receptivity to convenience foods. Companies targeting Asia-Pacific must navigate diverse regulatory environments, taste preferences, and price sensitivity while building distribution networks capable of supporting cold chain requirements for premium chilled and frozen products. Europe maintains steady growth supported by EU Regulation 828/2014 establishing harmonized gluten-free labeling requirements across member states, with products labeled 'gluten-free' containing no more than 20 mg/kg gluten. The region demonstrates strong consumer acceptance of premium food products and willingness to pay for quality, creating favorable conditions for chilled and organic gluten-free ready meals. Research across European markets confirms persistent cost premiums for gluten-free products, with staple foods showing the highest price differentials, yet consumer studies indicate growing satisfaction with product quality and availability. Emerging markets in South America, and the Middle East and Africa represent long-term opportunities as modern retail infrastructure expands and health awareness increases, though current penetration remains limited by distribution challenges, regulatory gaps, and price sensitivity that constrains premium product adoption.

Regulatory Landscape

Gluten-free ready meals operate under allergen and claim rules that hinge on measurable thresholds and documented controls. In the United States, FDA regulations define the gluten-free claim under 21 CFR 101.91, requiring foods to contain less than 20 ppm gluten. Manufacturers also face additional record-keeping considerations for fermented, hydrolyzed, or distilled ingredients, where testing can be less straightforward.

In the European Union, Commission Implementing Regulation (EU) No 828/2014 sets harmonized thresholds for gluten-free (less than 20 mg/kg) and very low gluten (less than 100 mg/kg), supporting cross-border labeling for ready meals sold through modern retail. Regulatory attention is also shifting toward cross-contact controls across the supply chain. In January 2026, the US FDA issued a Request for Information on labeling and preventing cross-contact of gluten for packaged foods, with the comment period extending into April 2026, and it flags data gaps around non-wheat gluten grains (barley, rye) and oat cross-contact. Alongside claim rules, EU Regulation (EU) No 1169/2011 requires mandatory disclosure of cereals containing gluten (wheat, rye, barley, oats) in ingredient lists, shaping formulation transparency and packaging workflows even when a gluten-free claim is not used.

Competitive Landscape

The gluten-free ready meals market exhibits fragmented concentration, creating opportunities for both established food conglomerates and specialized players to capture market share through differentiated positioning. Market leaders in the market include Nestlé SA, Conagra Brands, Amy’s Kitchen, Unilever PLC, and Nomad Foods Ltd. Major food companies are pursuing portfolio reshaping strategies. Strategic consolidation continues to reshape competitive dynamics.

Technology adoption emerges as a key differentiator, with companies investing in advanced preservation methods to address shelf-life constraints that historically limited premium product expansion. Non-thermal processing technologies, including high-pressure processing, cold plasma, and microwave-assisted sterilization, enable extended shelf life while maintaining nutritional and sensory qualities. Emerging disruptors focus on direct-to-consumer models and subscription services that bypass traditional retail limitations, though scalability remains constrained by cold chain logistics costs and consumer acquisition expenses.

In the gluten-free ready meals sector, companies are leveraging health trends while tackling challenges such as premium pricing and taste replication. Brands are innovating by introducing family-sized gluten-free meals and developing plant-based sub-brands targeting teens and adults. These moves highlight a broader trend towards personalization and sustainability. While major brands are ensuring gluten-free meals are affordable, flavorful, and widely available, smaller brands are prioritizing safety, health, and trustworthiness.

Gluten-Free Ready Meals Industry Leaders

-

Nestlé SA

-

Conagra Brands

-

Amy’s Kitchen

-

Nomad Foods Ltd.

-

Unilever PLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Product and ingredient innovation that improves texture, binding, and moisture retention creates more room for premium chilled and frozen gluten-free ready meals, where taste and quality perception remain a constraint and production costs are structurally higher than for conventional meals. Clean-label functional ingredients designed for allergen-controlled production can help manufacturers simplify formulations and improve repeatability at scale. For example, Riviana Foods showcased gluten-free, clean-label ingredient families such as instant precooked flour gels (including OryzaGEL and several pulse-based gels) produced in allergen-free facilities, targeting binding and texture performance relevant to ready-meal sauces, coatings, and assembled dishes.

On go-to-market, scaling through high-volume retail and digitally enabled discovery has widened access for specialized diets, while competition from larger portfolios and private label has intensified. The market draws demand from supermarkets and hypermarkets (42.88% share in 2025) alongside faster expansion in online retail, which supports broader assortment, subscription replenishment, and more detailed product information for strict gluten avoidance. The core opportunity is centered on dedicated allergen-safe manufacturing practices and verifiable cross-contact controls, which can support trust for multi-serve family formats and culturally varied menus as regulatory scrutiny and consumer expectations converge on traceability and compliance.

Recent Industry Developments

- June 2026: The FDA's January 2026 cross-contact labeling Request for Information continues to influence gluten-free labeling across the industry, with the comment period extending into April 2026. This points to continued tightening around gluten-free claims and cross-contact controls.

- May 2026: Amy's Kitchen announced expanded distribution into more than 150 Costco warehouses, including the launch of gluten-free Cheese Enchiladas. Placement in a high-velocity membership channel supports larger pack formats and faster household trial, helping scale frozen gluten-free meal volumes.

- October 2024: Feel Good Foods introduced gluten-free frozen chicken soup dumplings made with a rice flour blend wrapper. The launch broadened gluten-free frozen options into dumpling and comfort-food occasions, adding variety and raising the bar for texture and the eating experience in gluten-free convenience foods.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this sizing, the market covers retail sales of ready meals marketed as gluten-free that require only minimal preparation, such as heating or microwaving, before consumption. The scope includes frozen, chilled, dried, and shelf-stable complete meals sold in single-serve or family packs.

Scope exclusions: Meal kits, meal-replacement shakes, and gluten-free bakery or snack products are excluded from this market size.

Segmentation Overview

-

By Product Type

- Frozen Ready Meals

- Chilled Ready Meals

- Shelf Stable

- Freeze-Dried Ready Meals

-

By Category

- Vegetarian

- Non-vegetarian

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience/Grocery Stores

- Online Retail Stores

- Other Distribution Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East & Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started by mapping how gluten-free claims are defined and checked, because labeling rules determine which products can be counted. We referred to public sources such as US FDA gluten-free labeling guidance, Codex Alimentarius standards, and regulator food safety and labeling pages for key consuming regions.

Next, we used market context data to keep assumptions realistic, including statistics and publications from the USDA Economic Research Service and US Census Bureau trade and retail indicators, and broader World Bank references for income and inflation signals. Company annual reports, investor presentations, and credible press coverage were also reviewed to understand portfolio mix and pricing direction. Where disclosures were limited, a paid subscription for company financials and news was used to cross-check revenue exposure. This list is illustrative, and many other public and paid sources were also reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on discussions with packaged food manufacturers, private-label suppliers, distributors, and retail category managers, followed by checks with food labeling and compliance experts. Since this is a global market, we spread outreach across major consuming regions so price ladders, distribution shifts, and new product launches could be tested against real selling conditions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 18% | APAC: 46% |

| Mid tier: 42% | Functional/Unit leaders: 27% | EMEA: 32% |

| Smaller Players: 21% | Managers: 55% | Americas: 22% |

Market-Sizing & Forecasting

The core model is built using a top-down demand pool. We reconstruct ready-meal category consumption by region, then apply gluten-free penetration and labeled product availability filters. To keep the totals consistent, we corroborate them with selective bottom-up checks, including sampled SKU price points times estimated velocities, plus supplier and retailer channel checks that help flag over-counting risks.

Key inputs include the share of frozen versus chilled versus shelf-stable ready meals, the pace of gluten-free labeling adoption in prepared foods, average pack prices and promotion depth, distribution channel mix shifts between grocery and online, and regional inflation effects on shelf pricing. Where direct visibility was weaker, such as for smaller brands or private label, gaps were handled through range-based assumptions that were confirmed with distributors and retail buyers before being applied.

Forecasts were developed using scenario analysis. The base case reflects how experts expect gluten-free adoption and ready-meal convenience demand to move together, and sensitivity checks were run around pricing and distribution expansion. Assumptions were refreshed for major inputs each year so the model reflects what is being sold and how it is being priced.

Data Validation & Update Cycle

Outputs are checked against independent signals, including category growth rates, reported portfolio commentary from manufacturers, and observed price movements in major retail channels. When a region shows an unusual jump or drop, the driver is traced back to penetration, pricing, or channel mix, then the input is revisited before sign-off.

A second analyst reviews the logic and calculations. Re-contact is triggered when interview feedback conflicts with the desk view or when a key assumption shifts materially. Reports are refreshed annually, with interim updates when factors such as regulatory changes, major reformulations, or sharp inflation moves can alter the near-term picture. Before delivery, we run a final recency pass so clients receive the most up-to-date view available.

Mordor Intelligence's Gluten Free Ready Meals Market Estimate Compared With Other Published Estimates

Published market values for gluten-free ready meals can vary more than expected, mainly because firms do not count the same products and because they treat channels and pricing periods differently. Some studies lean on broad gluten-free packaged food pools, while others stay close to ready-meal shelves and the label rules used to define what is truly gluten-free.

Meal kits are a recurring mismatch, and they sit outside Mordor Intelligence's scope, which keeps the total tied to ready-to-eat or ready-to-heat meals sold as complete dishes. Differences also come from whether estimates use retail sales value versus shipment value, how local currencies are converted into USD, and how often assumptions are refreshed when promotions and input costs change quickly.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.14 B (2026) | |

| Trade Journal A | USD 1.80 B (2023) | Uses an earlier base year and appears to anchor sizing on a narrower retail set, with limited visibility into newer frozen and chilled gluten-free meal launches and their price ladders. |

| Industry Platform B | USD 1.32 B (2025) | Likely applies a conservative definition and a longer-range forecast setup, which can undercount premium pricing and the shift toward higher-value ready meals in modern grocery formats. |

Taken together, the spread is explained mostly by product inclusion choices, timing, and how value is measured at shelf prices versus other proxies. By keeping the count focused on labeled gluten-free ready meals and then validating with channel and pricing checks, the market size stays easier to trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the gluten-free ready meals market?

The market reached USD 2.14 billion in 2026 and is forecast to climb to USD 2.81 billion by 2031.

Which region leads the gluten-free ready meals market?

North America leads with 39.92% share in 2025, supported by clear FDA labeling rules and higher diagnosed prevalence of celiac disease.

Which product type segment is growing fastest?

Chilled ready meals are expanding at the highest rate, with a projected 5.79% CAGR during 2026-2031, driven by consumer preference for freshness.

How is e-commerce affecting the gluten-free ready meals market?

Online retail stores is the fastest-growing channel, expected to post a 6.33% CAGR as it improves product discovery and offers subscription convenience to consumers with dietary needs.

Page last updated on: