Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

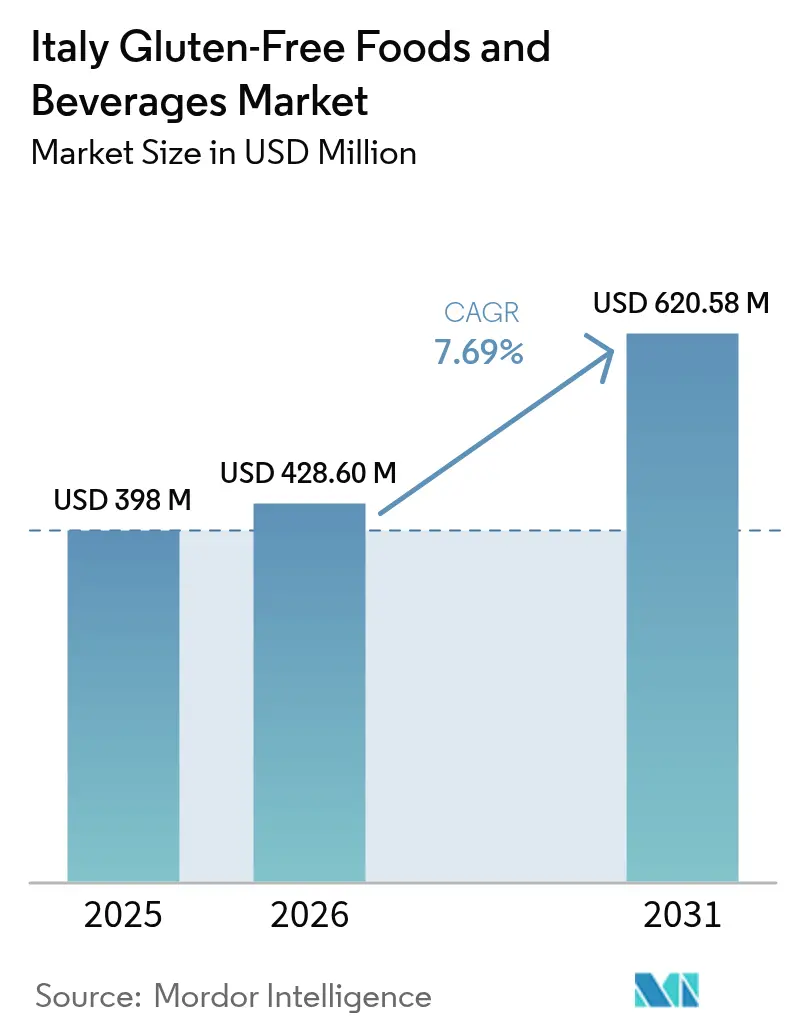

| Base Year Market Size (2025) | USD 398 Million |

| Market Size (2026) | USD 428.6 Million |

| Market Size (2031) | USD 620.58 Million |

| Growth Rate (2026 - 2031) | 7.69% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Italy Gluten-Free Foods And Beverages Market Analysis by Mordor Intelligence

The Italy gluten-free foods and beverages market size is expected to grow from USD 398 million in 2025 to USD 428.6 million in 2026 and is forecast to reach USD 620.58 million by 2031 at 7.69% CAGR over 2026-2031. The growth of Italy's gluten-free foods and beverages market is being driven by several key factors, including the implementation of mandatory nationwide celiac screenings, the increasing adoption of gluten-free lifestyles, and the strategic deployment of omnichannel retail approaches. These initiatives are effectively addressing long-standing challenges related to price sensitivity and product availability. Forward-thinking manufacturers are proactively reshaping their product portfolios to align with evolving consumer preferences, focusing on functional nutrition, organic sourcing, and protein diversification. Additionally, they are implementing stringent contamination control measures to safeguard brand reputation and consumer trust. The normalization of e-commerce as a primary food purchasing channel has enabled regional producers to expand their reach across the entire Italian peninsula. This development is redefining competitive dynamics within the market and accelerating the transition of gluten-free food products from niche offerings to mainstream consumer staples.

Key Report Takeaways

- By product type, Bakery Products led with 37.64% revenue share of the Italy gluten-free foods and beverages market in 2025; Beverages are projected to grow fastest at a 9.72% CAGR through 2031.

- By source, Plant-Based items held 61.85% of the Italy gluten-free foods and beverages market share in 2025, while Animal-Based alternatives are advancing at an 8.16% CAGR to 2031.

- By nature, Conventional offerings accounted for a 72.88% share of the Italy gluten-free foods and beverages market size in 2025, whereas Organic products will expand at a 10.32% CAGR.

- By distribution channel, Supermarkets/Hypermarkets captured 41.52% of the Italy gluten-free foods and beverages market in 2025; Online Retail Stores registered the top growth trajectory at 9.52% CAGR.

- By region, Northern Italy controlled 40.78% of the Italy gluten-free foods and beverages market in 2025; Southern Italy posts the fastest 8.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Gluten-Free Foods And Beverages Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Increased diagnosis and awareness of celiac disease and gluten sensitivity fuel demand | +2.1% | National, higher in Southern Italy | Medium term (2-4 years) |

| Government support for gluten-free labeling and reimbursement schemes encourages market growth | +1.8% | National | Long term (≥4 years) |

| Growing consumer preference for clean-label and allergen-free foods expands market base | +1.5% | Northern and Central Italy | Short term (≤2 years) |

| Shift toward healthier lifestyles and functional nutrition drives market expansion | +1.3% | National, urban focus | Medium term (2-4 years) |

| E-commerce growth enhances product accessibility across country | +0.9% | National, stronger in North | Short term (≤2 years) |

| Celebrity influences and media trends normalize gluten-free lifestyles | +0.6% | National, youth demographic | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Increased diagnosis and awareness of celiac disease and gluten sensitivity fuel demand

Italy's structured and systematic approach to identifying celiac disease serves as a robust foundation for sustained market expansion, extending its scope beyond traditional medical requirements. As reported by the Ministry of Health, the Lombardy region accounts for the highest number of diagnosed celiac disease cases, with 49,278 individuals in 2023[1]Source: Ministry of Health of Italy, "Annual report to Parliament on celiac disease", salute.gov.it. This growing awareness among consumers is not limited to clinical diagnoses but also reflects a shift toward lifestyle-oriented purchasing decisions. The implementation of a proactive diagnostic framework, strengthened by the mandatory screening requirements under Law 130/2023, is expected to significantly expand the addressable market by uncovering previously undiagnosed cases. Regional disparities in detection rates highlight that Southern Italy, in particular, is likely to witness a disproportionate increase in demand. This growth will be driven by ongoing improvements in healthcare infrastructure, enabling broader adoption of screening programs and facilitating market penetration in underserved areas.

Government support for gluten-free labeling and reimbursement schemes encourages market growth

Italy's regulatory framework strategically influences market dynamics by implementing financial assistance mechanisms that effectively reduce price sensitivity among celiac patients. This government intervention directly addresses the critical market challenge of premium pricing, enabling manufacturers to sustain higher profit margins while simultaneously increasing their market penetration. The Multi-annual National Control Plan (MANCP) for 2023-2027 underscores the importance of fraud prevention in gluten-free labeling. This initiative not only provides a competitive advantage to manufacturers adhering to compliance standards but also establishes significant entry barriers for opportunistic players attempting to exploit the market. The transparency and reliability of gluten-free labeling foster consumer trust, appealing to both diagnosed celiac patients and health-conscious individuals, thereby driving market growth. Furthermore, the integration of clear labeling regulations, reimbursement incentives, and comprehensive certification frameworks has catalyzed market expansion, spurred innovation, and reinforced consumer confidence in the gluten-free product segment.

Growing consumer preference for clean-label and allergen-free foods expands market base

With increasing health awareness and a growing demand for transparency in food production, consumers are actively shifting toward clean-label and allergen-free food products. This evolving preference is significantly expanding the gluten-free market, compelling manufacturers to diversify their portfolios by offering a broader range of minimally processed and natural product options. The gluten-free product segment, which initially catered to individuals with medical conditions, is now strategically positioned to address a wider spectrum of lifestyle-driven consumer demands. In the Italian market, health-conscious consumers are demonstrating a readiness to pay premium prices for products that emphasize sustainability and 'free from' claims, reflecting a shift in purchasing behavior. This trend aligns with a declining adherence to the traditional Mediterranean diet, creating a strategic window of opportunity for gluten-free product manufacturers to position their offerings as healthier and more sustainable alternatives. Supporting this market potential, the ARIANNA study indicates that 83.82% of Italian adults exhibit only medium adherence to the Mediterranean diet[2]Source: Graziano Bonifazi, “Consumer Attitudes toward Clean-Label Food in Italy,” Frontiers in Nutrition, frontiersin.org , signaling a disruption in dietary habits that gluten-free brands can strategically exploit to drive market growth.

Shift toward healthier lifestyles and functional nutrition drives market expansion

Italy's aging demographic and the increasing prevalence of obesity, particularly in the southern regions, are driving significant growth in the demand for functional food products designed to address specific health challenges. The consistent concentration of high obesity rates in Southern Italy, creates a strategic opportunity for gluten-free products positioned as effective weight management solutions. The Italian food industry is actively prioritizing innovation, as evidenced by research efforts focused on incorporating pea protein into gluten-free focaccia. This highlights manufacturers' commitment to meeting the rising consumer demand for functional nutrition, with a particular emphasis on protein enrichment and fiber fortification. Additionally, the growing consumer acceptance of biotechnological advancements in gluten-free product formulations reflects a readiness to adopt solutions that deliver enhanced nutritional value and align with evolving health and wellness trends.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High production costs of gluten-free products compared to conventional products limit market expansion | -1.4% | National, more pronounced in South | Long term (≥4 years) |

| Manufacturing processes face risks of cross-contamination, restricting growth | -0.8% | National | Medium term (2-4 years) |

| Strict regulatory requirements for gluten-free certification and labeling increase compliance costs | -0.6% | National | Long term (≥4 years) |

| Replicating the taste and texture of gluten-containing products proves challenging | -0.5% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High production costs of gluten-free products compared to conventional products limit market expansion

Despite the availability of government assistance programs, gluten-free manufacturers face significant cost structure disadvantages that limit their ability to penetrate the market effectively. In 2023, processed food prices in Italy experienced an inflationary increase of 8-11%, disproportionately impacting specialty products such as gluten-free alternatives[3]Source: ISTAT, “Consumer prices - September 2023,” istat.it, which are already positioned at a premium price point. The production of gluten-free products necessitates dedicated manufacturing lines, the use of specialized ingredients, and adherence to rigorous quality control protocols, all of which contribute to elevated structural costs. While government reimbursement schemes provide partial financial relief, they are insufficient to fully mitigate these expenses. Additionally, the reliance on naturally gluten-free grains, which typically have lower agricultural yields and shorter shelf lives, further exacerbates cost pressures. Gluten-free products are often formulated without preservatives to maintain freshness, resulting in a shorter shelf life compared to conventional wheat-based products. Furthermore, these products require specialized packaging solutions, such as air-tight and allergen-safe materials, to prevent contamination, thereby adding another layer of cost to the production process.

Manufacturing processes face risks of cross-contamination, restricting growth

Italian manufacturers are encountering substantial operational and reputational challenges as cross-contamination incidents persist, undermining consumer confidence and complicating compliance with stringent regulatory frameworks. The Ministry of Health's 2025 recalls of several gluten-free products, prompted by the detection of gluten, highlight ongoing weaknesses in manufacturing control systems, which continue to constrain the market's growth trajectory. Furthermore, inconsistencies in food handler training programs across different Italian regions, with many failing to incorporate comprehensive allergen management practices, further exacerbate the risks of contamination. These quality assurance shortcomings not only create competitive disadvantages for impacted manufacturers but also intensify consumer concerns about product reliability. This issue is particularly pronounced for smaller producers, who often lack the financial resources and operational infrastructure necessary to implement effective contamination prevention measures, thereby limiting their ability to compete and grow within the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bakery Dominance Faces Beverage Disruption

Italian shoppers still allocate the largest spend to gluten-free bread, biscuits, and cakes, giving Bakery Products 37.64% of the Italy gluten-free foods and beverages market in 2025. However, beverage innovation is expanding the category perimeter. Functional ready-to-drink (RTD) shakes, fortified plant-based milks, and collagen-infused waters are collectively achieving a robust CAGR of 9.72% (2026-2031). Their shelf-stable nature minimizes cross-contamination risks and facilitates market entry for new players, redefining consumer perceptions of a "gluten-free diet" beyond traditional bread substitutes.

To address consumer dissatisfaction with dense textures, bakeries are leveraging sourdough fermentation and native starch blends to close sensory gaps and protect market share. Pasta and noodles continue to be culturally significant in Italy. Semolina alternatives, such as rice, corn, or triticale, embody national pride and sustain consistent demand. Technological advancements like vacuum mixing in pasta production reduce cooking losses, ensuring the desired al dente texture. Furthermore, snacks, condiments, seasonings, and spreads are emerging as dynamic growth areas, capitalizing on on-the-go consumption trends and premium gifting opportunities. Consequently, the Italian gluten-free foods and beverages market is diversifying, reducing its dependence on bakery products and driving growth in beverage-centric consumption.

By Source: Plant-Based Leadership Challenged by Animal Innovation

In 2025, plant-based formulations, utilizing rice, maize, buckwheat, and legume flours, accounted for 61.85% of Italy's gluten-free foods and beverages market. The use of familiar Mediterranean ingredients enhances label transparency and supports price stability. Meanwhile, animal-based alternatives, such as egg white-enriched breads and whey-fortified meal replacements, are expanding at a CAGR of 8.16% (2026-2031), reflecting growing consumer demand for complete proteins and improved texture.

Advancements in pea protein are driving innovation, with hybrid formulations combining vegetable concentrates and milk peptides gaining popularity for their satiety and softness, strengthening “source of protein” claims. This convergence of ingredients highlights strategic opportunities within Italy's gluten-free foods and beverages sector to balance sensory appeal with nutritional value. Sourcing flexibility remains a critical factor. Disruptions in global pulse supplies emphasize the robustness of Italy’s dairy and egg supply chains, particularly in production hubs like Emilia-Romagna and Veneto. Forward-thinking producers mitigate risks by adopting multi-protein portfolios, ensuring formulation consistency and managing commodity price fluctuations, thereby maintaining their competitive position in Italy's gluten-free foods and beverages market.

By Nature: Organic Premium Gains Momentum

In 2025, conventional SKUs maintained a 72.88% value share but are increasingly challenged by the rapid growth of organic alternatives, which are projected to expand at a 10.32% CAGR (2026-2031). Retailers are strategically leveraging seasonal promotions, particularly during the national “Organic Week” campaigns, to highlight provenance-focused narratives. These campaigns effectively resonate with consumers, enabling them to justify premium spending on organic products. As a result, organic offerings are anticipated to continue outperforming category averages, contributing significantly to the growth of Italy's gluten-free foods and beverages market.

The robust supply chain infrastructure supports the creation of unique value propositions, such as heirloom sorghum and stone-ground chickpea flour, which are marketed with a strong emphasis on their terroir, similar to the branding of wine appellations. This approach enhances the competitive positioning of organic brands within Italy’s premium food segment. By aligning with the country’s quality-driven food culture, organic labels are successfully capturing the loyalty of health-conscious consumers and culinary enthusiasts, driving repeat purchases and reinforcing their market presence.

By Distribution Channel: Digital Transformation Accelerates

In 2025, supermarkets and hypermarkets represented 41.52% of transactions within Italy's gluten-free foods and beverages market. This dominance is supported by the presence of in-store dietitian corners, which provide personalized dietary guidance, and an extensive assortment of private-label gluten-free products that cater to diverse consumer preferences. However, online retail stores are emerging as the fastest-growing distribution channel, recording an impressive CAGR of 9.52% (2026-2031). Leading retail chains have established dedicated gluten-free microsites to enhance customer engagement, while nimble direct-to-consumer (D2C) bakeries are leveraging advanced flash-freeze technology to deliver high-quality artisan gluten-free loaves across the nation within 24 hours. Subscription-based models are gaining traction, addressing the recurring needs of medically dependent consumers while ensuring consistent and predictable revenue streams for suppliers. Concurrently, discount grocery chains are expanding their 'free-from' product offerings to attract cost-conscious shoppers, effectively reducing price disparities and driving broader acceptance of gluten-free products in the mainstream Italian market.

Specialist health shops and pharmacies continue to serve a loyal customer base, particularly those seeking expert pharmacist advice on managing diets for comorbid conditions. However, their collective market share is gradually declining. For emerging brands, adopting hybrid distribution strategies has proven effective. By stocking products in pharmacies, these brands gain credibility and trust among health-focused consumers, while simultaneously targeting online shoppers to achieve scalability. This dual approach optimizes early-stage brand visibility and mitigates potential risks associated with market entry.

Geography Analysis

In 2025, Northern Italy secures a 40.78% market share in the country's gluten-free foods and beverages industry, driven by its advanced logistics infrastructure, high-income households, and the presence of global food multinationals. The region exhibits strong demand, with per-capita spending exceeding the national average, supported by an efficient healthcare system that facilitates early diagnoses and extensive modern retail networks. The concentration of manufacturing facilities in Parma and Bolzano enhances logistical efficiency, while public-private laboratory collaborations accelerate innovation cycles. Additionally, food-processing companies have established visitor centers to increase transparency in gluten-free production, strengthening consumer confidence in the region's market leadership.

Central Italy serves as a culinary hub. The recovery of tourism to pre-pandemic levels has prompted restaurants and hotels to incorporate gluten-free options into their menus alongside traditional offerings. Regional SMEs are leveraging heritage grains, such as Senatore Cappelli durum, to produce artisanal gluten-free flatbreads that adhere to protected designation recipes. These premium products are marketed through agritourism channels, demonstrating how leveraging regional identity enhances the value proposition in Italy's gluten-free foods and beverages market.

Southern Italy is positioned for the highest growth, with a projected CAGR of 8.62% (2026-2031). EU-funded health hubs are expanding diagnostic capabilities, while reimbursement cards are addressing affordability challenges. Although the region's demographic profile is characterized by a younger population, larger households, and lower disposable income initially hindered market penetration, voucher schemes have mitigated these barriers. Improved road infrastructure is strengthening cold-chain logistics. Agribusiness cooperatives in Puglia and Calabria are capitalizing on favorable microclimates to engage in contract farming of quinoa and sorghum, reducing supply chain complexities and creating local employment opportunities. Combined with social media-driven health awareness campaigns, these factors are propelling Southern Italy's rapid growth in the Italian gluten-free foods and beverages market.

Regulatory Landscape

Italy applies the EU framework for gluten-related claims, led by Regulation (EU) No 828/2014, which sets the "gluten-free" claim at a maximum of 20 mg/kg (20 ppm) in the final food. At the national level, Italy also runs a specific pathway for foods "specifically formulated" for people with celiac disease, anchored in Law 123/2005 and supported by subsequent Ministry of Health decrees such as the Decree of 17 May 2016, which underpin inclusion in the National Health Service (SSN) reimbursement registry. Operationally, food businesses producing or offering gluten-free foods must manage official controls and local compliance processes, including notification to the local health authority (ASL/Azienda USL) via SUAP in line with EU hygiene requirements (Reg. (EC) No 852/2004) and HACCP-based allergen controls. Regional authorities may issue additional guidance for official control of gluten-free food businesses (for example, Emilia-Romagna regional guidelines), while Associazione Italiana Celiachia (AIC) provides an industry reference through its risk classification and practical guidance used to reduce cross-contamination in manufacturing and foodservice settings.

Competitive Landscape

Italy's gluten-free foods and beverages market is a moderately consolidated market and comprises numerous local and international competitors. Some of the major players operating in the Italian gluten-free foods and beverages market are Dr. Schär AG/SPA, Barilla Holding, Farmo SpA, The Kraft Heinz Company, and NT Food SpA. The leading players in the gluten-free product market have a wide range of products. These players focus on leveraging opportunities posed by emerging markets to expand their product portfolio, so that they can cater to the requirements for various product categories.

Mid-tier challengers focus on white-space, such as shelf-stable sauces and premium confectionery. Start-ups partner with university labs to iterate enzyme-treated doughs that mimic gluten elastic behavior, shaving development cycles to under 18 months. E-commerce-first entrants differentiate through limited-drop flavors and direct feedback loops, circumventing slotting fees and capturing micro-communities inside the Italy gluten-free foods and beverages market.

Strategic priorities in the market revolve around contamination control, ingredient transparency, and compelling storytelling to build consumer trust. The occurrence of high-profile product recalls has significantly increased consumer concerns, prompting companies to adopt advanced solutions such as real-time Certificate of Analysis (COA) dashboards and blockchain-enabled traceability applications. Additionally, mergers and acquisitions activity has intensified as businesses seek to achieve scale economies, which are critical for managing the high costs associated with segregation investments.

Italy Gluten-Free Foods And Beverages Industry Leaders

-

Dr. Schar AG/SpA

-

Barilla Holding

-

The Kraft Heinz Company

-

Farmo SpA

-

NT Food SpA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Reimbursement-linked demand and retail normalization create whitespace for brands that can satisfy both strict gluten control and consumer-friendly value propositions. The SSN reimbursement registry for products specifically formulated for celiacs, supported by ministerial rules (including the Decree of 17 May 2016), tends to reward manufacturers that invest in segregation, testing, and documentation, while also supporting wider shelf placement in pharmacies and mainstream retail through medically driven repeat purchasing. At the same time, Italy is seeing measurable expansion in modern retail exposure for gluten-free products, with AIC reporting a 25% increase in supermarket and hypermarket shelf space over the prior two years (as of March 2025). This broader footprint supports private label development and faster-growing subsegments such as functional, clean-label, and organic gluten-free offerings, where differentiation comes from nutrition (fiber/protein enrichment), ingredient transparency, and reliable contamination control that aligns with EU 828/2014 claim requirements. Industry data and standards work, including GS1 Italy guidance on gluten-related product attributes (2025), also supports better data quality for omnichannel execution, helping brands improve discoverability and reduce purchase friction online and in-store.

Recent Industry Developments

- July 2026: The FAO/WHO Codex Alimentarius Commission adopted new international guidance for precautionary allergen labeling (PAL) on July 9, 2026, including a reference dose approach for cereals containing gluten. This strengthens the global benchmark for how manufacturers communicate trace-gluten risk and can raise the bar for supplier controls and label substantiation for products sold in Italy under gluten-related claims.

- March 2026: An investment plan of EUR 28 million for 2026 covering production facilities across Italy, Spain, and Germany was announced by Dr. Schar. The plan strengthens gluten-free manufacturing capacity and tightens contamination-control execution, supporting broader assortment expansion in a category where recalls can quickly erode trust.

- January 2025: Barilla invested USD 30.5 million to enhance pasta production capabilities at its Foggia facility in southern Italy. The upgrade supports domestic manufacturing scale and supply reliability as gluten-free consumption expands beyond a strictly medical-need segment.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the value of packaged gluten-free foods and gluten-free beverages sold in Italy through organized retail and online channels, where products are labeled and positioned for gluten avoidance or celiac-friendly diets.

Scope exclusions: Foodservice-only sales that are not traceable through packaged retail equivalents are excluded from this sizing.

Segmentation Overview

-

By Product Type

-

Bakery Products

- Breads and Cakes

- Cookies and Biscuits

- Other Products

- Pasta and Noodles

- Snacks

- Beverages

- Condiments, Seasonings and Spreads

- Dairy and Dairy Substitutes

- Meats and Meat Substitutes

- Other Gluten-Free Products

-

Bakery Products

-

By Source

- Plant-Based

- Animal-Based

-

By Nature

- Conventional Gluten-Free Products

- Organic Gluten-Free Products

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Specialist Retailers

- Online Retail Stores

- Other Distribution Channels

-

By Region

- Northern Italy

- Central Italy

- Southern Italy

- Others

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the fact base for Italy, so the model starts from realistic consumption context, price points, and the channel structure before any forecast is applied. We referenced public sources such as national nutrition and health publications (including celiac-related guidance), Italian and EU food labeling rules, and trade statistics that indicate ingredient and packaged-food import and export flows.

On the market side, we also reviewed company annual reports, investor presentations, product catalogs, and reputable press coverage to map how gluten-free lines are priced and where they are sold in practice. Patent databases and an import and export shipment-level database were used selectively to sense innovation activity and cross-border movement for relevant packaged categories. These examples are not exhaustive, and we checked additional public and internal sources to collect, validate, and clarify inputs.

Primary Interviews and Surveys

Primary work was used to pressure-test what desk research cannot fully confirm in Italy, especially channel splits, pricing behavior, and the practical pace of category expansion. We spoke with a mix of manufacturers, distributors, retailers, and category specialists, and then validated assumptions with functional leaders who manage product, sales, or procurement decisions across the country.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 12% | |

| Mid tier: 61% | Functional/Unit leaders: 42% | |

| Smaller Players: 14% | Managers: 46% |

Market-Sizing & Forecasting

Sizing started with a top-down build where packaged-food and beverage demand pools were reconstructed using Italy-relevant consumption signals and the share that is plausibly gluten-free, followed by a channel allocation across supermarkets, specialist retail, convenience, and online. To keep the totals realistic, we ran selective bottom-up checks using sampled brand and private-label price points, shelf-level pack sizes, and a limited supplier and distributor roll-up where data visibility was strong.

Key inputs that shaped the model included gluten-free penetration in core staples (like bread and pasta), the rate of new product introductions, average selling price progression by pack format, promotional intensity in modern retail, and online share changes as e-commerce normalizes. When direct observations were missing for a niche product line, we handled gaps by using proxy categories with similar rotation and pricing, then adjusted through interview feedback.

For forecasting, scenario analysis was used to reflect how adoption differs under health-driven demand versus lifestyle-driven demand, and the scenarios were reconciled to a central case using expert consensus on pricing and distribution expansion over the forecast window.

Data Validation & Update Cycle

Outputs were validated through triangulation across channel splits, price ranges, and implied per-capita spend, and then checked against independent signals such as retail assortment growth and the category momentum described in interviews. When a variance looked too wide, we revisited the underlying assumptions and triggered follow-up calls to confirm whether the issue came from scope, pricing, or channel coverage.

Before sign-off, the model goes through multi-step internal reviews where totals, growth rates, and key drivers are tested for consistency year by year. The report is refreshed annually, with interim updates when material events affect demand, regulation, or pricing, and a final pre-delivery pass is completed so clients receive the latest view.

Mordor Intelligence's Italy Gluten Free Foods Beverages Market Market Sizing Compared With Other Published Estimates

Published estimates for Italy gluten-free foods and beverages often do not match because the product boundary and the anchor year are not the same, and because pricing and channel coverage are handled differently. Once these differences accumulate, the final market size can change even when published sources point to similar consumer trends.

Foodservice-only gluten-free meals and menu sales sit outside Mordor Intelligence's scope, which is why figures that blend in restaurant and bakery-counter servings can look higher even with similar growth assumptions. Another recurring gap is how pricing is treated, where some sources use a single average price, while others allow mix shifts and promotions to affect realized value over time, and currency timing can further widen the spread.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 398 M (2025) | |

| Global Consultancy A | USD 480 M (2024) | Uses a different base year and often reads as a broader "gluten-free products" framing, which can pull in adjacent packaged items beyond the foods and beverages set used here, and it can apply higher price growth assumptions in the outer years. |

| Industry Publisher B | USD 483.3 M (2023) | Anchors the series on an earlier valuation year and can reflect different channel weighting, especially if specialty stores are emphasized more heavily, which typically raises the average realized price versus a more balanced retail mix. |

Across the table, the variance is mainly driven by base-year selection, what is counted as in-scope packaged demand, and how channel mix is converted into an average selling price. By tying inputs to observable retail signals and then cross-checking them with interviews, the final value stays transparent and repeatable when assumptions are updated.

Key Questions Answered in the Report

How big is the Italy gluten-free food market in 2026?

The Italy gluten-free food market size stands at USD 428.6 million in 2026, with a forecast to surpass USD 620.58 million by 2031.

Which segment grows fastest within the Italy gluten-free food market?

Beverages take the lead, advancing at a 9.72% CAGR as consumers seek functional, on-the-go nutrition in gluten-free formats.

Why is Southern Italy important for future growth?

Mandatory screening, voucher subsidies, and higher obesity prevalence drive an 8.62% CAGR in the South, narrowing the gap with Northern consumption levels.

Are organic gluten-free products gaining traction?

Yes. Organic SKUs grow at 10.32% CAGR, leveraging Italy’s extensive organic farmland and consumer willingness to pay for sustainability and health benefits.

Page last updated on: