Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

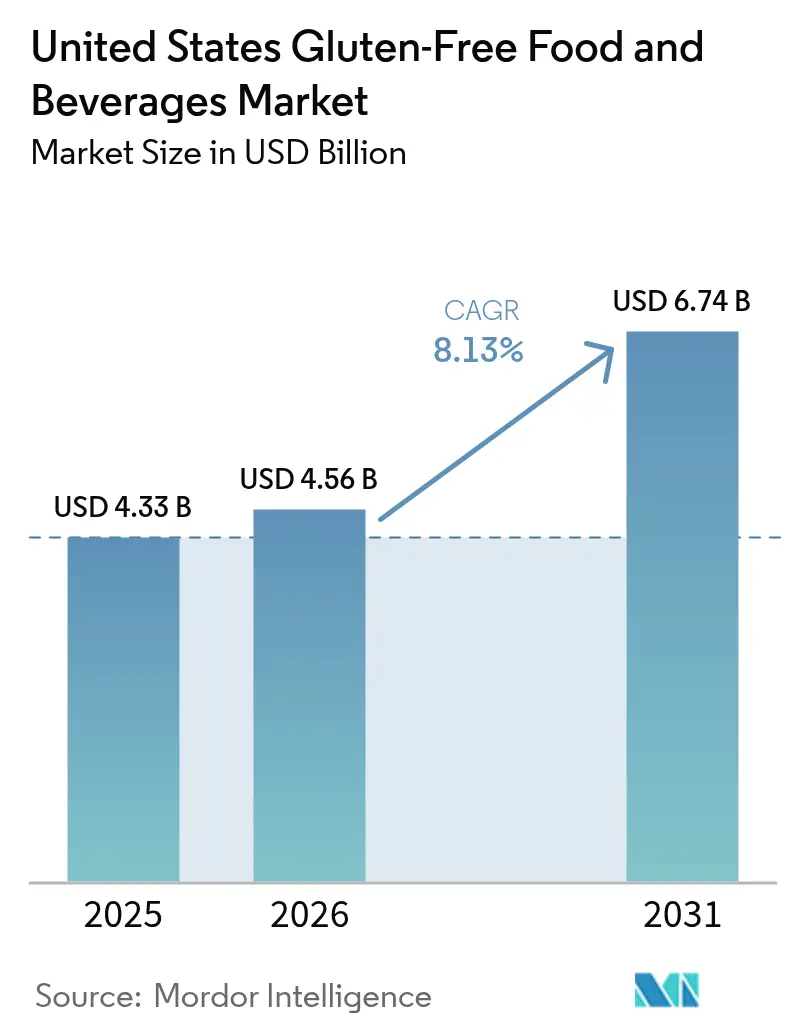

| Base Year Market Size (2025) | USD 4.33 Billion |

| Market Size (2026) | USD 4.56 Billion |

| Market Size (2031) | USD 6.74 Billion |

| Growth Rate (2026 - 2031) | 8.13% CAGR |

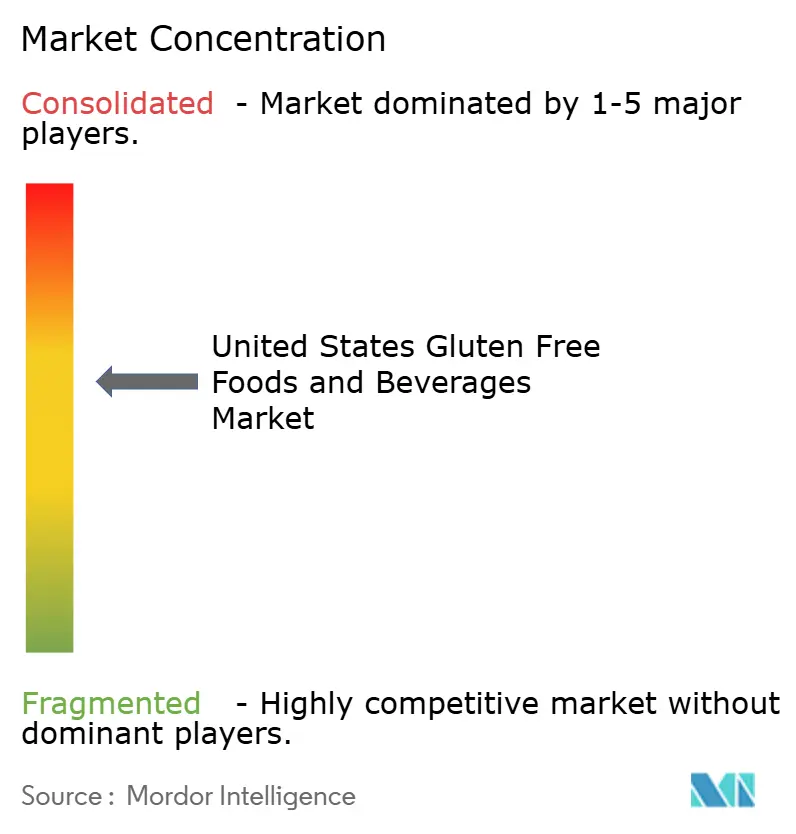

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Gluten-Free Food And Beverages Market Analysis by Mordor Intelligence

The United States gluten-free food and beverages market size is expected to grow from USD 4.33 billion in 2025 to USD 4.56 billion in 2026 and is forecast to reach USD 6.74 billion by 2031 at 8.13% CAGR over 2026-2031. Robust growth stems from a structural shift in demand that reaches well beyond medically diagnosed consumers and into a wellness-driven mainstream. FDA enforcement of the ≤20 ppm gluten limit has standardized on-pack claims, so retailers confidently expand dedicated shelf space while reducing shopper confusion. Formulation advances, ranging from enzyme-modified rice flour to fermented sorghum, have narrowed the sensory gap with wheat-based products, supporting higher repeat-purchase rates. Consumer interest in gut-health optimization, coupled with clean-label expectations, reinforces premium pricing power. Finally, the channel mix is evolving as subscription e-commerce captures value-conscious yet brand-loyal households.

Key Report Takeaways

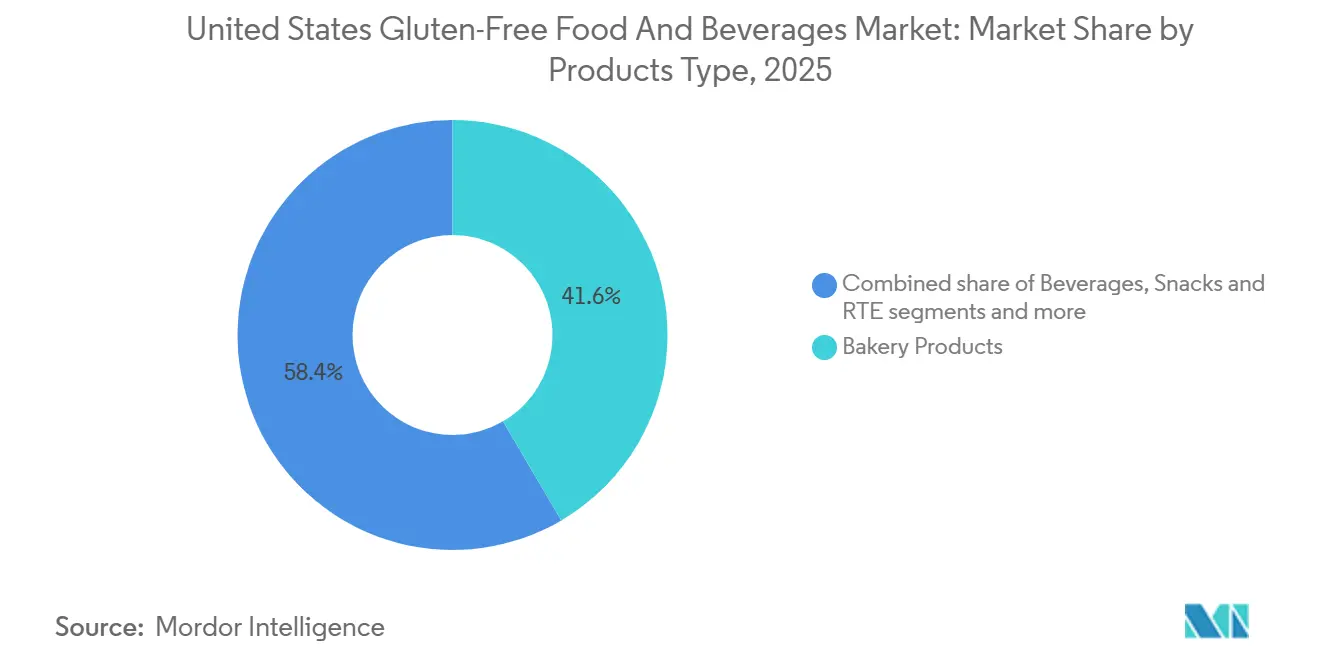

- By product type, bakery products led with 41.57% revenue share in 2025, while beverages are projected to advance at a 9.05% CAGR through 2031.

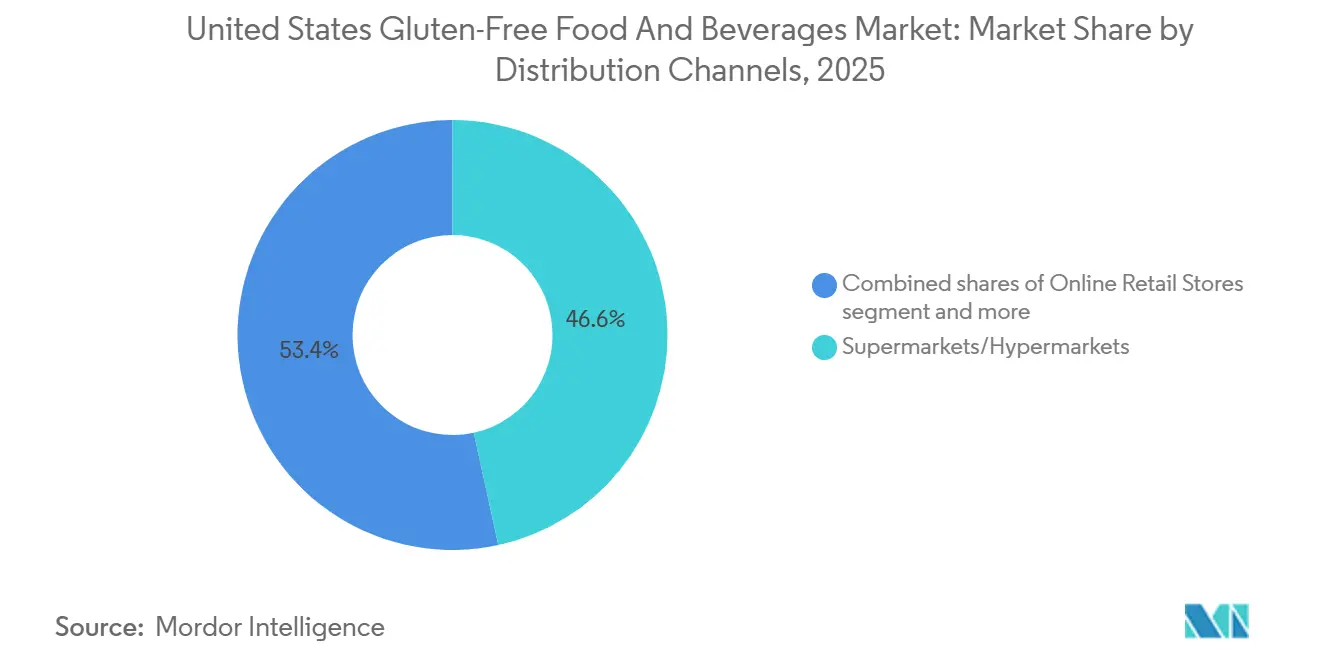

- By distribution channel, supermarkets and hypermarkets held 46.58% of the United States gluten-free food and beverages market share in 2025, whereas online retail stores recorded the highest projected CAGR at 9.53% through 2031.

- By geography, the West commanded 27.65% of 2025 sales, and the South is poised to expand at a 9.15% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Gluten-Free Food And Beverages Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising diagnosis rates of celiac disease and gluten sensitivity | +1.2% | National, with higher impact in Northeast and West Coast | Medium term (2-4 years) |

| Government regulations supporting gluten-free labeling | +0.8% | National, with early gains in California, New York, Illinois | Long term (≥ 4 years) |

| Continuous product innovation in taste, texture, and formulation | +1.5% | National, strongest in urban metropolitan areas | Short term (≤ 2 years) |

| Increased awareness through social media influencers and wellness content | +1.1% | National, with concentration in tech-savvy demographics | Short term (≤ 2 years) |

| Expanding perception of gluten-free products as part of a healthier and cleaner lifestyle | +0.9% | National, premium markets in West and Northeast | Medium term (2-4 years) |

| Growing focus on gut health and microbiome-friendly diets | +0.7% | National, social media-driven demographics | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising diagnosis rates of celiac disease and gluten sensitivity

The prevalence of celiac disease in the United States is approximately 1%, with enhanced screening methods revealing varying diagnosis rates across ethnic groups: 1.08% in White populations, 0.36% in Hispanic populations, and 0.16% in Black Americans [1]Source: Agency for Healthcare Research and Quality, “Celiac Disease Screening Update,” ahrq.gov. Greater use of serological screening tools, such as tissue transglutaminase antibody tests, drives higher confirmed diagnoses, even though the overall prevalence holds a very small percentage of the population. Pediatric referrals rose between 2024 and 2025, creating a medically compelled cohort that shows strong brand loyalty and low-price elasticity. The Northeast and Midwest record the most diagnoses because dense specialist networks support earlier testing. Manufacturers committed to GFCO certification capture stable household spending, while pharmacies reinforce retail visibility by grouping certified staples near over-the-counter digestive remedies. Higher medical awareness thus converts latent demand into predictable volume.

Government regulations supporting gluten-free labeling

The FDA's 21 CFR 101.91 regulation requires products labeled "gluten-free" to contain less than 20 parts per million (ppm) of gluten. In 2024, the FDA expanded documentation requirements to include fermented and hydrolyzed foods [2]Source: Food and Drug Administration, “Gluten-Free Labeling,” fda.gov. National standards boost interstate commerce and bolster consumer confidence. However, they pose compliance hurdles, especially for smaller producers lacking testing capabilities. In contrast, larger manufacturers, benefiting from economies of scale, can more easily shoulder these compliance costs. They often leverage certifications as a market edge. The regulatory landscape nudges companies to invest in specialized production facilities and testing labs. This not only broadens product variety but also mitigates cross-contamination risks. Such infrastructure investments and stringent quality control enable manufacturers to uphold consistent gluten-free standards and align with FDA regulations. Moreover, the harmonization of gluten-free standards has refined supply chain management and intensified supplier verification across the board.

Expanding perception of gluten-free products as part of a healthier and cleaner lifestyle

A significant number of U.S. adults now purchase gluten-free products despite lacking a medical diagnosis, viewing gluten avoidance as synonymous with clean eating and reduced inflammation. This lifestyle segment prioritizes products with short ingredient lists, non-GMO verification, and organic certification, often paying a premium over conventional alternatives. The halo effect extends to adjacent categories: consumers who buy gluten-free bread are statistically more likely to purchase plant-based milk and probiotic supplements, enabling cross-promotional strategies at retail. However, this perception is not uniformly evidence-based; clinical trials have shown no metabolic advantage to gluten-free diets in individuals without celiac disease or wheat allergy, yet the narrative persists in wellness media. Brands that transparently communicate the absence of health benefits for non-celiac consumers risk alienating a lucrative segment, creating a strategic tension between scientific accuracy and marketing efficacy.

Increased awareness through social media influencers and wellness content

Instagram and TikTok influencers with followings exceeding 500,000 routinely showcase gluten-free meal prep, recipe hacks, and product reviews, generating millions of impressions per post. The growth of online channels has also increased product variety and competitive pricing, benefiting both consumers seeking specific dietary options and manufacturers looking to expand their market presence. According to the United States Department of Agriculture data from 2023, 1 in 5 shoppers in the country reported buying groceries online at least once in 30 days [3]Source: United States Department of Agriculture, " Online Grocery Shopping", usda.gov. However, influencer-driven awareness often lacks scientific rigor; many creators conflate gluten-free with weight loss or detoxification, claims unsupported by peer-reviewed research. This dynamic creates a double-edged sword for brands: heightened visibility comes with the risk of regulatory scrutiny if influencer partnerships imply unapproved health benefits. The Federal Trade Commission has issued warning letters to brands whose influencer campaigns made disease-treatment claims without substantiation, underscoring the compliance risks inherent in social-media-driven growth strategies

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Higher production and ingredient costs for gluten-free formulations | -1.8% | National, with higher impact in lower-income demographics | Long term (≥ 4 years) |

| Taste and texture inconsistencies in certain gluten-free bakery and staple products | -0.9% | National, affecting all production facilities | Medium term (2-4 years) |

| Intense competition from other health-positioned categories | -1.1% | Global, particularly affecting bakery and pasta segments | Medium term (2-4 years) |

| Regulatory compliance and certification requirements for gluten-free labeling | -0.6% | National, with regulatory gaps in smaller manufacturers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher production and ingredient costs for gluten-free formulations

Gluten-free flours such as almond, coconut, and chickpea command wholesale prices 2-3 times higher than wheat flour, compressing margins for manufacturers who compete on price with conventional products. Dedicated gluten-free production lines require rigorous cleaning protocols and separate storage to prevent cross-contamination, adding to operational costs relative to shared facilities. Smaller manufacturers often lack the scale to negotiate favorable terms with specialty ingredient suppliers, forcing them to accept spot-market pricing that fluctuates with crop yields. For instance, a 2024 drought in California's almond-growing regions drove almond flour prices up 22%, squeezing margins for brands that had locked in retail pricing with distributors. Large players such as General Mills Inc. and Conagra Brands mitigate cost pressures through vertical integration and long-term supply contracts, but mid-tier brands face a strategic dilemma: absorb costs and sacrifice profitability, or raise prices and risk losing share to private-label alternatives.

Taste and texture inconsistencies in certain gluten-free bakery and staple products

Despite formulation advances, many gluten-free breads and pasta products still exhibit crumbly textures, off-flavors, or rapid staling that deter repeat purchases. The absence of gluten's viscoelastic network makes it difficult to achieve the chewiness and structural integrity that consumers expect in baked goods, particularly in artisan-style breads and pizza crusts. Some manufacturers compensate by increasing fat and sugar content, which improves palatability but undermines the health-halo positioning that attracts lifestyle buyers. This creates a segmentation challenge: products optimized for celiac patients prioritize safety and compliance, while those targeting wellness consumers emphasize taste and macronutrient profiles, often requiring separate SKUs and marketing strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bakery Dominates, Beverages Accelerate

Bakery products captured 41.57% of the 2025 value, reinforcing the everyday relevance of gluten-free bread, cookies, and cakes for medically driven households. The United States gluten-free food and beverages market size for bakery is projected to rise steadily, even as volume growth moderates, because premium formulations such as brioche justify higher pricing. Snacks and ready-to-eat lines exploit portability trends; Quinn Foods’ pretzel twists in resealable pouches target office and travel occasions. Condiments and spreads, although smaller, reduce hidden cross-contact risk and therefore carry outsized trust value.

Beverages register the fastest trajectory at a 9.05% CAGR through 2031 as enzyme-treated beers, kombucha, and functional RTDs flourish. Consumers perceive liquid formats as lower risk for gluten contamination, a belief that enlarges trial propensity. Dairy and meat substitute brands pursue certification to widen appeal, illustrating convergence between plant-based and gluten-free propositions. Lentil and chickpea pasta adds protein, attracting fitness-minded shoppers. Collectively, these innovations widen category boundaries and lift repeat occasions, strengthening the United States gluten-free food and beverages market.

By Distribution Channel: Online Gains, Supermarkets Hold

Supermarkets and hypermarkets still anchor 46.58% of 2025 sales, owing to dedicated aisles and end-cap promotion that foster impulse discovery. Cross-merchandising with plant-based milk or keto snacks further amplifies basket size. Private-label expansion by Walmart intensifies price competition, compelling branded players to differentiate through certification depth and ingredient provenance. Major retailers strengthen their positions through same-day pickup services and temperature-controlled home delivery, while online-only retailers implement subscription-based models to maintain consistent monthly sales. These digital platforms offer enhanced product filtering, allergen information, and personalized recommendations.

Online retail grows at a 9.53% CAGR to 2031. Subscription models lock predictable revenue while eliminating slotting fees, beneficial for mid-sized challengers. Amazon’s integration of store pickup options blurs channel distinctions and attracts shoppers who want hands-on packaging inspection before purchase. Meal-kit providers now offer gluten-free plans, adding a service-oriented sub-channel. Specialist retailers maintain high SKU breadth for newly diagnosed customers requiring staff guidance, whereas convenience stores add portable options for travellers, rounding out the omnichannel landscape of the United States gluten-free food and beverages market. Small manufacturers use direct-to-consumer channels to test products and build brand presence before entering traditional retail. The growth of online shopping contributes to balanced market expansion across urban and rural regions in the United States gluten-free food and beverages market, supported by improved logistics networks and cold chain infrastructure.

Geography Analysis

The West region held 27.65% of market value in 2025, driven by California's early adoption of health trends and a dense concentration of natural food retailers such as Whole Foods and Sprouts Farmers Market. The South is forecast to grow at 9.15% CAGR through 2031, the fastest rate among all regions, as rising Hispanic populations and increased awareness of celiac disease among previously underdiagnosed demographics expand the addressable market. Texas and Florida, the South's largest states, have seen a proliferation of gluten-free product launches tailored to regional tastes, including tortilla chips made from cassava and plantain that align with Latin American culinary traditions.

The Northeast exhibits the highest per-capita consumption of gluten-free products, reflecting dense urban populations, elevated healthcare access, and cultural affinity for European food trends where gluten-free adoption has been more pronounced. New York and Massachusetts have enacted state-level menu-labeling laws that require restaurants to disclose gluten-free options, indirectly boosting retail demand as consumers become accustomed to gluten-free availability. The West's dominance is further reinforced by Silicon Valley's quantified-self movement, where consumers track dietary inputs via apps and wearables, creating a feedback loop that sustains demand for gluten-free and other functional foods.

Regional differences in retail infrastructure also shape distribution strategies. The West's high density of natural food stores supports premium-priced, artisan gluten-free brands, while the South's reliance on mass-market chains such as Walmart and Kroger favors value-oriented products and private labels. The Midwest's agricultural heritage has enabled the emergence of regional gluten-free brands that emphasize local sourcing and farm-to-table narratives, differentiating themselves from national players. The Northeast's concentration of food-allergy advocacy groups and celiac-disease support networks creates a more informed consumer base that demands rigorous certification and transparent labeling, raising the bar for market entry.

Competitive Landscape

The United States gluten-free food and beverages market exhibits moderate fragmentation, indicating that no single player commands a dominant share, but a handful of large conglomerates exert disproportionate influence. General Mills Inc., Conagra Brands, and Kellanova leverage scale economies to absorb higher ingredient costs and secure favorable shelf placement, yet they face margin pressure from private-label offerings that undercut branded products. Smaller specialists such as Namaste Foods, Quinn Foods, and Amy's Kitchen capture premium segments by emphasizing single-origin grains, transparent sourcing, and certifications that resonate with highly engaged consumers.

The competitive dynamic is further complicated by cross-category entrants: plant-based brands such as Beyond Meat and dairy-alternative producers like Oatly have pursued gluten-free certification to broaden appeal, intensifying rivalry for health-conscious shoppers. White-space opportunities exist in the intersection of gluten-free and other dietary frameworks, particularly keto-gluten-free and paleo-gluten-free hybrids that address multiple consumer concerns within a single product.

Technology adoption is uneven; larger players deploy predictive analytics to optimize SKU assortment and reduce out-of-stocks, while smaller brands rely on direct-to-consumer channels to gather real-time feedback and iterate formulations rapidly. General Mills Inc.'s patent filings in 2024 for enzyme-treated gluten-free doughs signal an intent to defend technological advantages, though the enforceability of such patents remains untested in court. Emerging disruptors include regenerative-agriculture brands that position gluten-free grains as environmentally superior to conventional wheat, tapping into sustainability narratives that appeal to younger consumers.

United States Gluten-Free Food And Beverages Industry Leaders

-

General Mills Inc.

-

Conagra Brands Inc.

-

PepsiCo Inc.

-

The Hain Celestial Group Inc.

-

Bob's Red Mill Natural Foods, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Eshbal Functional Food Inc. entered a production partnership with Queen St. Bakery (Toronto-based gluten-free baked foods manufacturer) to produce and scale its gluten-free products for the North American market.

- May 2025: Feast Fast brand launched a range of plant-based, non-GMO, gluten-free, sugar-free, and low-carb cookies designed to support intermittent fasting, keto diets, and blood glucose management. The products are available in Peanut Butter, Chocolate Donut, Cinnagraham, and Chocolate Chip.

- February 2025: Absolutely Gluten-Free introduced its Absolutely! Gluten-Free Frozen Cookie Dough in three varieties: Chocolate Chip, Double Chocolate, and Sugar Cookie. The dough comes in individually wrapped 12-oz portions that make 12 cookies per package, retailing at USD 5.99.

United States Gluten-Free Food And Beverages Market Report Scope

Gluten-free food and beverages do not contain gluten. Gluten is a protein in cereal grains that provides an elastic structure to the dough. The United States Gluten-Free Food and Beverages Market is Segmented by Product Type (Bakery Products, Snacks and RTE Products, Beverages, and More), Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Specialist Retailers, and More), and Geography (Northeast, Midwest, South, and West). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Bakery Products | Breads and Cakes |

| Cookies and Biscuits | |

| Others | |

| Snacks and RTE Products | |

| Beverages | |

| Condiments, Seasonings, and Spreads | |

| Dairy and Dairy Substitutes | |

| Meat and Meat Substitutes | |

| Others |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Specialist Retailers |

| Online Retail Stores |

| Others |

By Geography

| Northeast |

| Midwest |

| South |

| West |

| By Product Type | Bakery Products | Breads and Cakes |

| Cookies and Biscuits | ||

| Others | ||

| Snacks and RTE Products | ||

| Beverages | ||

| Condiments, Seasonings, and Spreads | ||

| Dairy and Dairy Substitutes | ||

| Meat and Meat Substitutes | ||

| Others | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Specialist Retailers | ||

| Online Retail Stores | ||

| Others | ||

| By Geography | Northeast | |

| Midwest | ||

| South | ||

| West |

Key Questions Answered in the Report

How large will the United States gluten-free food and beverages market be in 2031?

It is forecast to reach USD 6.74 billion by 2031, rising at a 8.13% CAGR between 2026 and 2031.

Which product category leads sales today?

Bakery products account for 41.57% of 2025 revenue due to daily-use items such as bread and cookies.

What is the fastest-growing product segment through 2031?

Beverages are projected to expand at a 9.05% CAGR as enzyme-treated beers, kombucha, and RTDs gain traction.

Which sales channel is gaining the most momentum?

Online retail stores forecast a 9.53% CAGR because subscription models bypass slotting fees and improve convenience.

Page last updated on: