Feed Carotenoids Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.41 Billion |

| Market Size (2031) | USD 4.59 Billion |

| Growth Rate (2026 - 2031) | 6.14% CAGR |

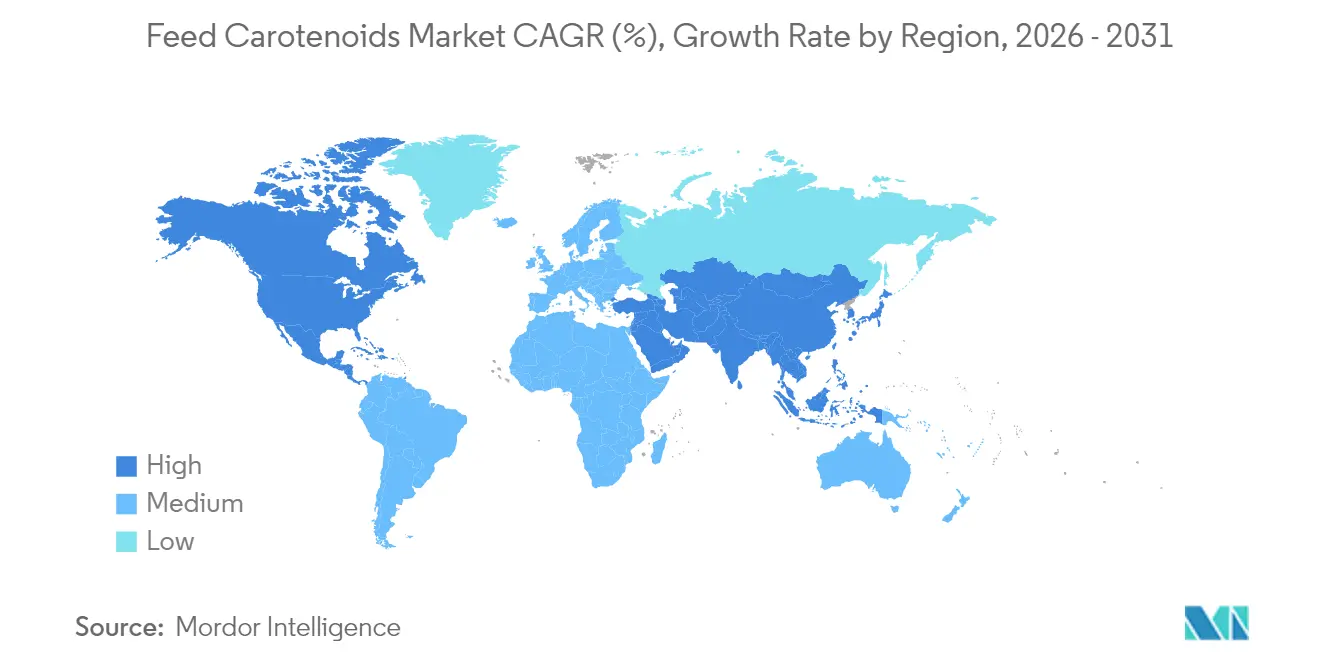

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

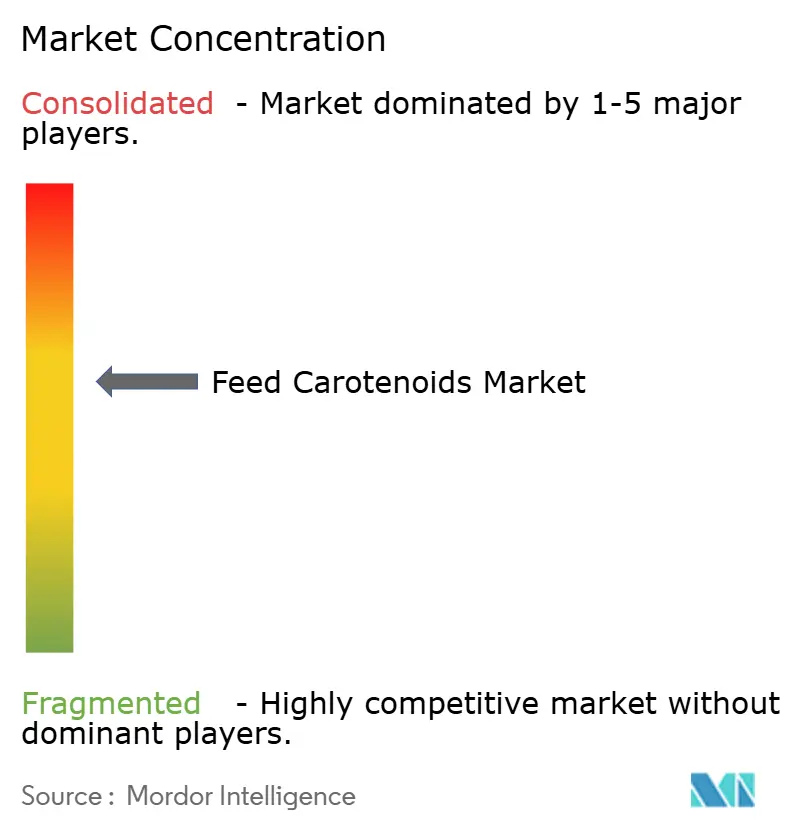

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Feed Carotenoids Market Analysis by Mordor Intelligence

feed carotenoids market size in 2026 is estimated at USD 3.41 billion, growing from 2025 value of USD 3.21 billion with 2031 projections showing USD 4.59 billion, growing at 6.14% CAGR over 2026-2031. The upward trajectory persists even after severe supply chain shocks, underscoring the market’s structural resilience. Salmonid aquaculture, industrial-scale poultry, and rapid technology adoption together spur demand, while procurement teams hedge against single-source dependencies by approving multiple suppliers and encouraging precision-fermentation breakthroughs. The BASF SE and DSM-Firmenich outages realigned pricing power, rewarding producers able to guarantee on-time shipment of stabilized beadlets in tropical lanes. Natural carotenoids have regulatory momentum in Europe and branding advantages in North America, although synthetic variants keep cost leadership in value-focused Asia-Pacific feed formulations.

Key Report Takeaways

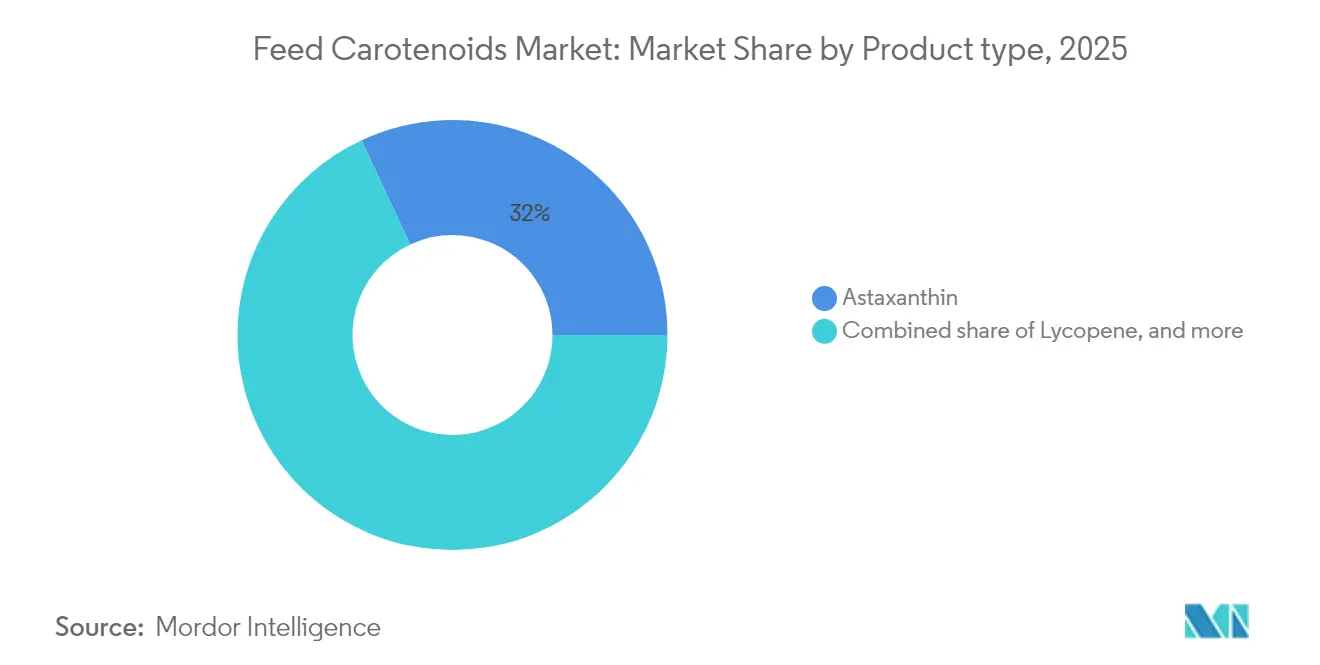

- By product type, astaxanthin led with 31.95% revenue share in 2025, and same projected to expand at a 7.36% CAGR to 2031.

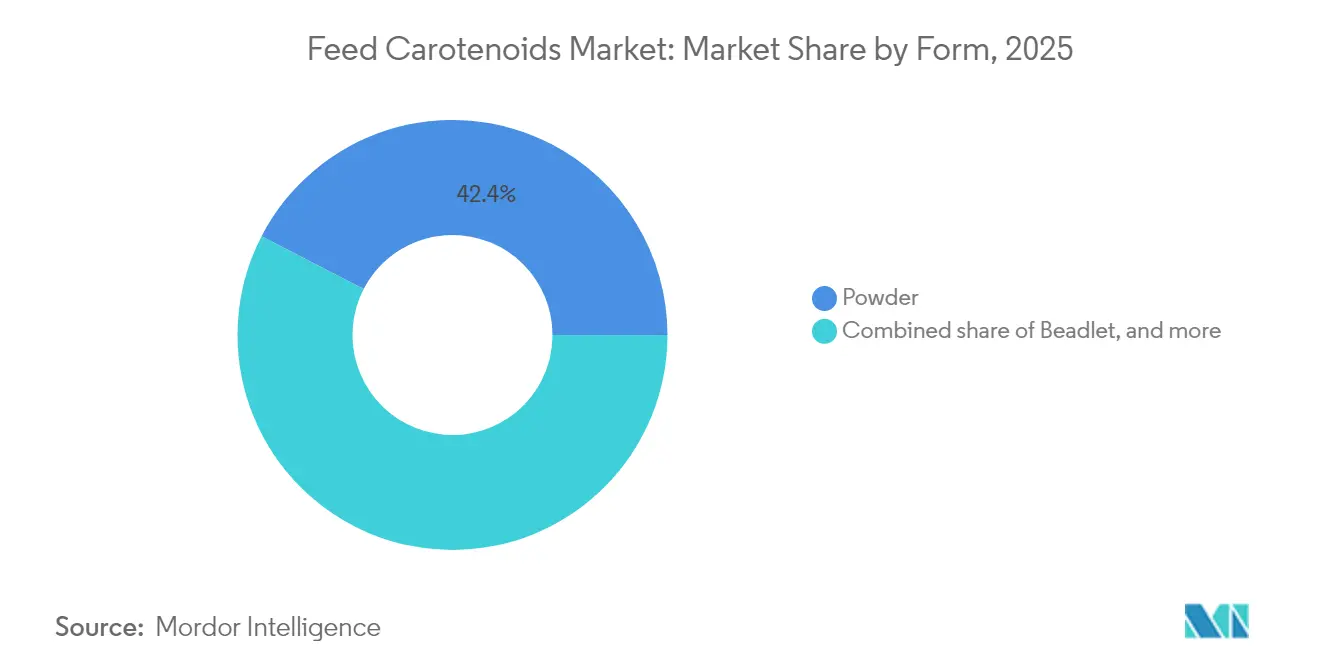

- By form, powder formats captured 42.40% of the feed carotenoids market size in 2025, and beadlets are projected to advance at an 8.05% CAGR through 2031.

- By animal type, poultry accounted for 38.35% of the feed carotenoids market share in 2025, and aquaculture is projected to register an 7.92% CAGR from 2026 to 2031.

- By geography, the Asia-Pacific region retained a 29.55% share of the market in 2025, and North America is projected to demonstrate the fastest CAGR of 7.55% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Feed Carotenoids Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for salmonid aquafeed pigmentation | +1.2% | Global, concentrated in Norway, Chile, and Scotland | Medium term (2-4 years) |

| Industrial-scale poultry production in emerging economies | +0.8% | Asia-Pacific core, spill-over to South America | Long term (≥ 4 years) |

| Shift from synthetic to natural carotenoids | +1.1% | Europe and North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Microalgae and precision-fermentation cost breakthroughs | +0.9% | Global, early adoption in Europe and North America | Long term (≥ 4 years) |

| Tariff-driven reshoring of carotenoid supply chains | +0.7% | North America and Europe, bilateral trade impacts | Short term (≤ 2 years) |

| AI-enabled pigment optimization for species-specific outcomes | +0.6% | Global, technology leaders in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Salmonid Aquafeed Pigmentation

Salmon farmers link flesh coloration directly with consumer premium willingness, and Norwegian producers report a 15 – 20% price uplift for optimally pigmented fish. The European Food Safety Authority's 2024 reaffirmation of astaxanthin safety limits at 100 mg/kg for ornamental fish provides regulatory clarity that supports expanded usage in commercial aquaculture[1]Source: European Food Safety Authority, “Astaxanthin Safety Reaffirmation,” efsa.europa.eu. Freight cost for temperature-controlled carotenoids reaches 12% of ingredient value in remote sites, pushing farms to secure nearby warehousing and on-farm stability testing.

Industrial-Scale Poultry Production in Emerging Economies

Poultry sector consolidation in Asia-Pacific markets creates concentrated demand for standardized pigmentation solutions that ensure consistent egg yolk coloration and broiler skin appearance across large production volumes. The shift from traditional smallholder systems to integrated operations creates opportunities for premium carotenoid suppliers who can provide technical support and quality assurance programs. Brazil's poultry export growth necessitates compliance with international color standards, driving the adoption of standardized carotenoid supplementation protocols that ensure consistent product appearance across diverse genetic lines and production environments.

Shift from Synthetic to Natural Carotenoids

Regulatory frameworks increasingly favor natural carotenoids as consumer preferences and sustainability mandates reshape ingredient selection criteria across major feed markets. The European Union's stricter evaluation criteria for synthetic additives create competitive advantages for natural alternatives, while North American markets show growing preference for clean-label feed ingredients that support premium product positioning. The transition creates supply chain challenges as natural production requires longer lead times and more complex quality control procedures compared to synthetic alternatives.

Microalgae and Precision-Fermentation Cost Breakthroughs

Biotechnology advances in 2024 achieved commercial viability for several alternative carotenoid production pathways that previously remained economically uncompetitive with synthetic manufacturing. CB Therapeutics developed sustainable retinol production via precision fermentation in May 2024, demonstrating scalable approaches that could extend to other carotenoid compounds. The technology enables the production of novel carotenoid variants and enhanced bioavailability formulations that cannot be achieved through traditional synthesis or extraction approaches.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in carotenoid-rich biomass supplies | -0.4% | Global, acute in regions dependent on agricultural extraction | Short term (≤ 2 years) |

| Regulatory uncertainty around novel fermentation strains | -0.3% | Europe and North America, strict approval processes | Medium term (2-4 years) |

| Photodegradation losses during tropical feed logistics | -0.2% | Tropical and subtropical regions, supply chain dependent | Short term (≤ 2 years) |

| Sub-clinical toxicity risks at supra-nutritional doses | -0.1% | Global, species-specific sensitivity variations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Carotenoid-Rich Biomass Supplies

Agricultural extraction of carotenoids from marigold petals, paprika, and other plant sources faces increasing volatility due to climate variability and competing land use pressures that affect raw material availability and pricing. Weather disruptions in major growing regions can create price swings within single seasons, forcing feed manufacturers to maintain larger inventory buffers that increase working capital requirements. The concentration of extraction facilities in specific geographic regions creates supply chain vulnerabilities, as demonstrated by recent disruptions that affected multiple ingredient categories simultaneously. Alternative sourcing strategies require extensive validation and regulatory approvals that can take 18-24 months to complete, limiting short-term flexibility in responding to supply disruptions.

Regulatory Uncertainty Around Novel Fermentation Strains

The distinction between genetically modified organisms and novel food classifications remains unclear for many fermentation-derived carotenoids, creating regulatory pathway uncertainty that affects commercial planning and investment decisions[2]Source: European Food Safety Authority, “Novel Foods Applications Portal,” efsa.europa.eu. Different regulatory approaches across major markets require parallel approval processes that increase development costs and time-to-market for new carotenoid production methods. Companies must navigate complex safety assessment requirements that vary significantly between synthetic, extracted, and fermentation-derived carotenoids, even when the final molecular structures are identical.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Astaxanthin Anchors Premium Applications

Astaxanthin held 31.95% feed carotenoids market share in 2025, driven by salmon pigmentation premiums. It leads growth at a 7.36% CAGR as retailers promote non-synthetic seafood labels. The feed carotenoids market size attributable to beta-carotene remains sizable in poultry and swine due to its dual Vitamin A role. Lutein retention in table-egg programs supports differentiated shell-egg Stock keeping units (SKU), while canthaxanthin usage stays constrained by dosage ceilings.

The dominance of astaxanthin creates a price umbrella enabling niche carotenoids such as zeaxanthin to float at specialty premiums. Salmon processors tie bonus payments to fillet hue metrics, cementing steady demand even during feed cost inflation cycles. The regulatory landscape creates competitive advantages for astaxanthin and beta-carotene alternatives that offer similar pigmentation benefits without associated safety concerns. Other carotenoid types, including zeaxanthin and capsanthin, target niche applications where specific color profiles or functional benefits justify premium pricing compared to mainstream alternatives.

By Form: Powders Set Benchmarks, Beadlets Accelerate

Powder formats held 42.40% feed carotenoids market share in 2025 due to decades-long familiarity in premix lines. Stable flow properties suit vertical screw feeders and deliver a coefficient of variation below 5% in vitamin lines. Beadlets, growing at 8.05% CAGR, encapsulate actives in starch or protein matrices that resist oxidation and release in targeted gut pH bands, boosting bioavailability.

In tropical routes, powder potency drop exceeds 10% during two-month coastal warehousing, whereas beadlets lose under 4%. The payback from tighter inclusion rates offsets higher per-kilogram price, steering integrators in Indonesia, Thailand, and West Africa toward beadlet adoption. Stability testing under various environmental conditions becomes critical for tropical markets where temperature and humidity fluctuations can degrade carotenoid potency during extended storage periods.

By Animal Type: Poultry Volumes, Aquaculture Velocity

Poultry applications command 38.35% market share in 2025, reflecting the sector's large-scale production volumes and consistent pigmentation requirements for both egg yolk coloration and broiler skin appearance. Aquaculture represents the fastest-growing segment at 7.92% CAGR, driven by expanding salmon farming operations and premium pricing for well-pigmented fish products. Ruminant applications focus primarily on reproductive health benefits of beta-carotene supplementation, while swine operations utilize carotenoids for both pigmentation and antioxidant functions.

The aquaculture segment's growth reflects increasing consumer sophistication and willingness to pay premium prices for visually appealing seafood products. Salmon farming operations report that optimal astaxanthin supplementation can increase market value compared to pale alternatives, creating strong economic incentives for consistent carotenoid inclusion. Other animal types, including pet food applications, represent emerging opportunities where premium positioning and health claims justify higher carotenoid inclusion rates.

Geography Analysis

Asia-Pacific contributed 29.55% of the feed carotenoids market in 2025. China accounts for a significant share of the world's aquaculture harvest, and the consolidation of mega-farms accelerates the standardization of nutrients. India and Vietnam adopt European-style broiler genetics, demanding higher carotenoid density for export-grade skin coloration. Regional governments subsidize recirculating aquaculture systems, magnifying astaxanthin uptake per metric ton of fish produced.

North America is projected to register the fastest CAGR of 7.55% from 2026 to 2031. North America posts steady gains backed by large poultry complexes and a regulatory environment that balances innovation speed with safety. FDA approvals for fermentation-derived inputs move faster than EU processes, enticing venture investors to build United States manufacturing. Canada’s Atlantic salmon farms secure supply contracts that include delivery contingencies tied to BASF SE and DSM outage risk mitigation. South America leverages Brazil’s poultry export surge to integrate standardized pigmentation protocols, whereas Africa’s emerging tilapia farms explore low-cost beadlets to raise harvest value.

Europe, with Norway’s salmon value chain and Germany’s premix hubs acting as anchor demand centers. EFSA’s stringent review procedures tilt formulations toward natural inputs, and Germany offers technical hubs that refine beadlet encapsulation lines. Nordic aquafeed factories fine-tune astaxanthin dosage to comply with 25 mg/kg fillet targets and minimize residual loss.

Competitive Landscape

The market shows moderate concentration. BASF SE and DSM-Firmenich outages in 2024 exposed vulnerabilities, and combined, the events resulted in the loss of over one-quarter of the world's synthetic capacity for several months. Zhejiang NHU filled part of the gap, capturing short-term volume through nimble capacity allocation. Corbion’s 2024 acquisition of full control of its Brazilian algae plant underscores a pivot to vertical integration and natural differentiation[3]Source: Corbion, “Acquisition of AlgaPrime Facility,” corbion.com.

Supply assurance now trumps lowest-cost bidding. Feed groups add supplier scorecards, weighting on-time delivery, multi-plant networks, and rapid turnaround of QC documents. Firms with fermentation pipelines, such as CB Therapeutics, receive strategic equity from integrators keen to lock future volumes. AI formulation specialists partner with carotenoid vendors to bundle dosage algorithms, deepening customer lock-in.

Technology racelines split between catalyst optimization in legacy synthetic routes and metabolic-pathway engineering in fermentation. Capital intensity also diverges, and citral expansions require multi-hundred-million-dollar complexes, whereas modular fermenters scale in 5,000-liter increments, enabling staged deployment that matches demand curves.

Feed Carotenoids Industry Leaders

BASF SE

Kemin Industries, Inc.

Cargill Inc.

DSM-Firmenich AG

Archer-Daniels-Midland Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Synthite Industries formed a strategic partnership with Corbion to develop algae-based natural carotenoid production using Corbion's fermentation expertise and Synthite's extraction and formulation capabilities. The partnership targets the growing demand for natural astaxanthin in European aquaculture markets.

- August 2024: Wanhua Chemical commissioned the world's largest single-unit citral production facility with 48,000 metric tons per year capacity, providing key intermediates for aroma and nutrition applications including carotenoid synthesis pathways. The facility's scale advantages could influence upstream cost structures for synthetic carotenoid production.

- January 2024: Archer-Daniels-Midland completed acquisition of Trouw Nutrition, expanding the company's animal nutrition capabilities and potentially affecting carotenoid distribution channels and customer relationships in key regional markets.

Global Feed Carotenoids Market Report Scope

Feed carotenoids are compounds used in animal feed as a coloring pigment to enhance various livestock-based products, including egg yolks, broiler skin, fish, and crustaceans. The Feed Carotenoids Market is segmented by Type (Beta-Carotene, Lycopene, Lutein, Astaxanthin, Canthaxanthin, and Other Types), Animal Type (Ruminant, Poultry, Swine, Aquaculture, and Other Animal Types), and Geography (North America, Europe, Asia-Pacific, South America, and the Middle-East and Africa). The report offers market size and forecasts for the feed carotenoids market in terms of value (USD million) for all the above segments.

| Beta-Carotene |

| Lycopene |

| Lutein |

| Astaxanthin |

| Canthaxanthin |

| Other Types |

| Beadlet |

| Powder |

| Oil Suspension |

| Emulsion |

| Ruminant |

| Poultry |

| Swine |

| Aquaculture |

| Other Animal Types |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | Beta-Carotene | |

| Lycopene | ||

| Lutein | ||

| Astaxanthin | ||

| Canthaxanthin | ||

| Other Types | ||

| By Form | Beadlet | |

| Powder | ||

| Oil Suspension | ||

| Emulsion | ||

| By Animal Type | Ruminant | |

| Poultry | ||

| Swine | ||

| Aquaculture | ||

| Other Animal Types | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the feed carotenoids market in 2026?

It totals USD 3.41 billion and is on track to reach USD 4.59 billion by 2031, translating to a 6.14% CAGR.

Which product dominates current demand?

Astaxanthin leads with 31.95% share, mainly because salmonid farms link strong pigmentation with premium retail pricing.

Why are natural carotenoids gaining popularity?

European labeling rules and U.S. clean-feed claims favor plant- and algae-derived sources, boosting natural variants at a 9.48% CAGR.

Which region is growing fastest?

North America posts the highest 7.55% CAGR, driven by large aquaculture industry and emerging intensive poultry systems across the region.

What form factor is expanding most rapidly?

Beadlet technology grows at 8.05% CAGR owing to enhanced bioavailability and heat-stable logistics advantages.

How did the 2024 production outages affect the market?

BASF and DSM-Firmenich disruptions tightened synthetic supplies, shifted purchasing toward diversified sources, and elevated the strategic value of reliable delivery schedules.

Page last updated on: