Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Market Size (2026) | USD 2.01 Billion |

| Market Size (2031) | USD 2.46 Billion |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Feed Vitamins Market Analysis by Mordor Intelligence

The feed vitamins market size is expected to grow from USD 1.93 billion in 2025 to USD 2.01 billion in 2026 and is forecast to reach USD 2.46 billion by 2031 at 4.12% CAGR over 2026-2031. Growth rests on intensive livestock expansion, regulatory limits on antibiotic growth promoters, and encapsulation advances that guard vitamin potency during processing and storage. Demand also benefits from precision livestock farming, which enables real-time micronutrient dosing, while circular bio-economy projects recover vitamin intermediates from fermentation side streams. Raw-material price swings, stricter cross-contamination limits, and competition from phytogenic and postbiotic additives raise formulation costs and complexity, sharpening the focus on targeted delivery systems that stretch nutrient efficiency across species and geographies. Together, these forces keep the feed vitamins market on a steady but dynamic trajectory.

Key Report Takeaways

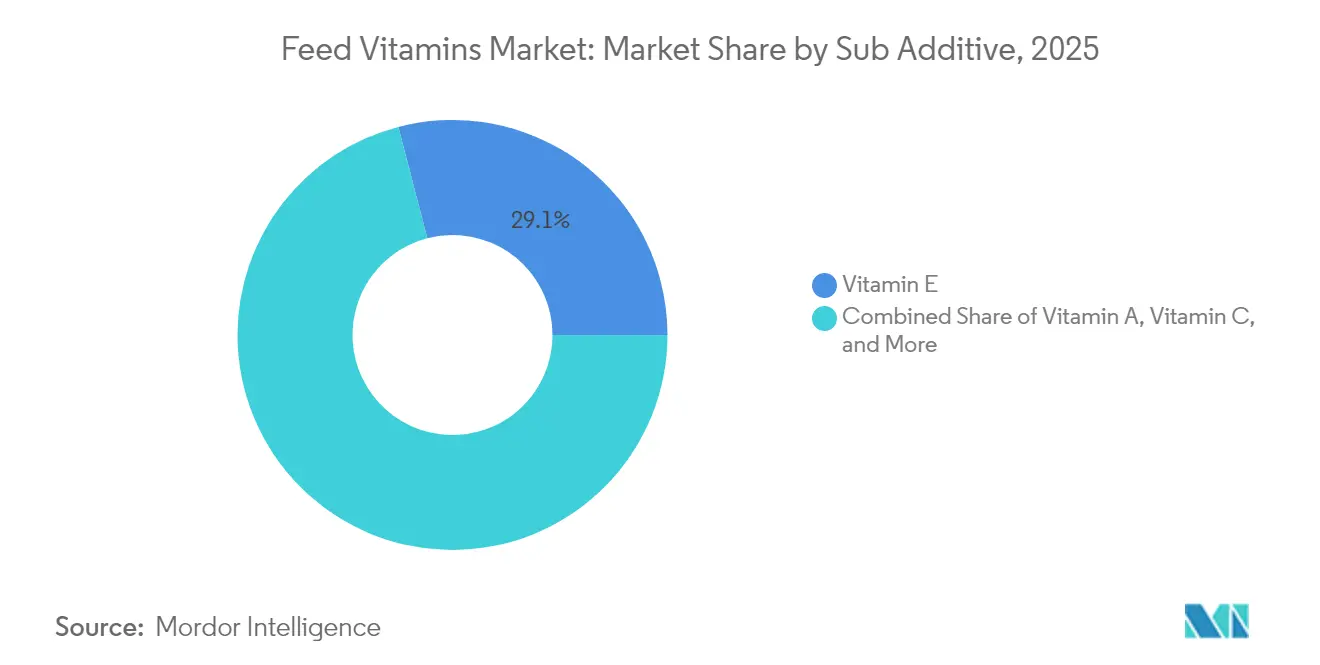

- By sub-additive type, Vitamin E led with 29.05% revenue share of the feed vitamins market in 2025, while the same segment is projected to expand at a 4.28% CAGR through 2031.

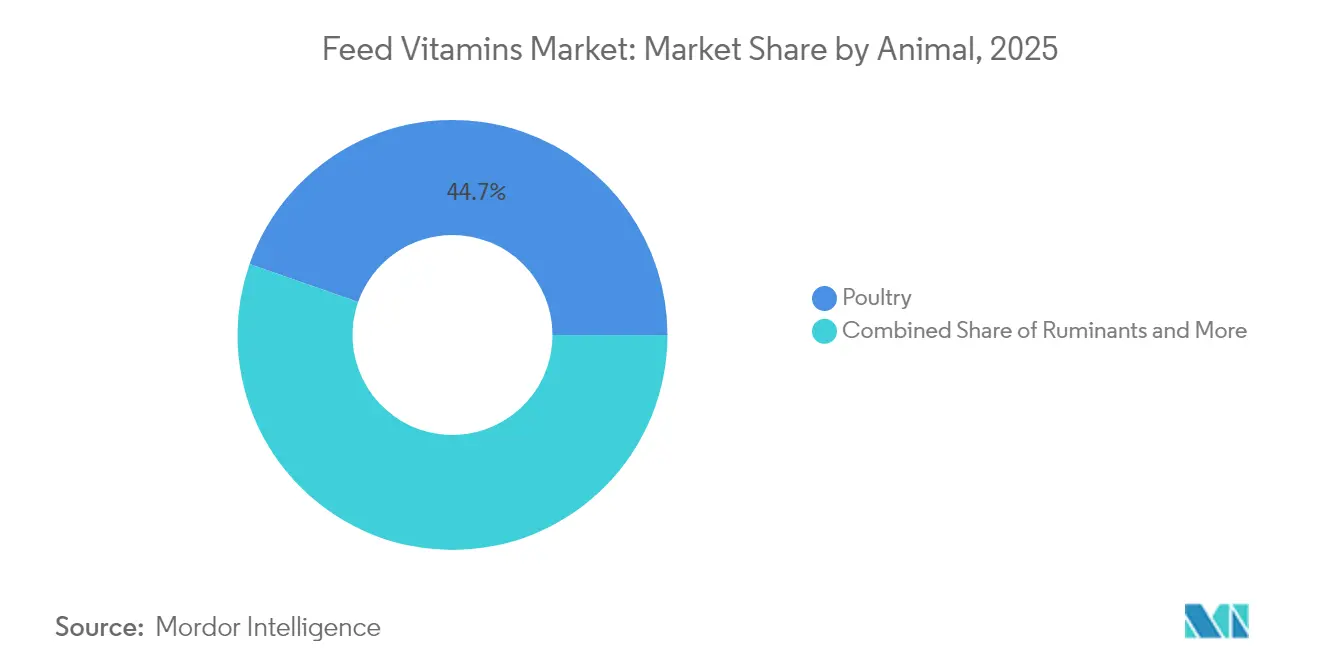

- By animal, poultry accounted for a 44.65% share of the feed vitamins market size in 2025, and ruminants are advancing at a 4.48% CAGR to 2031.

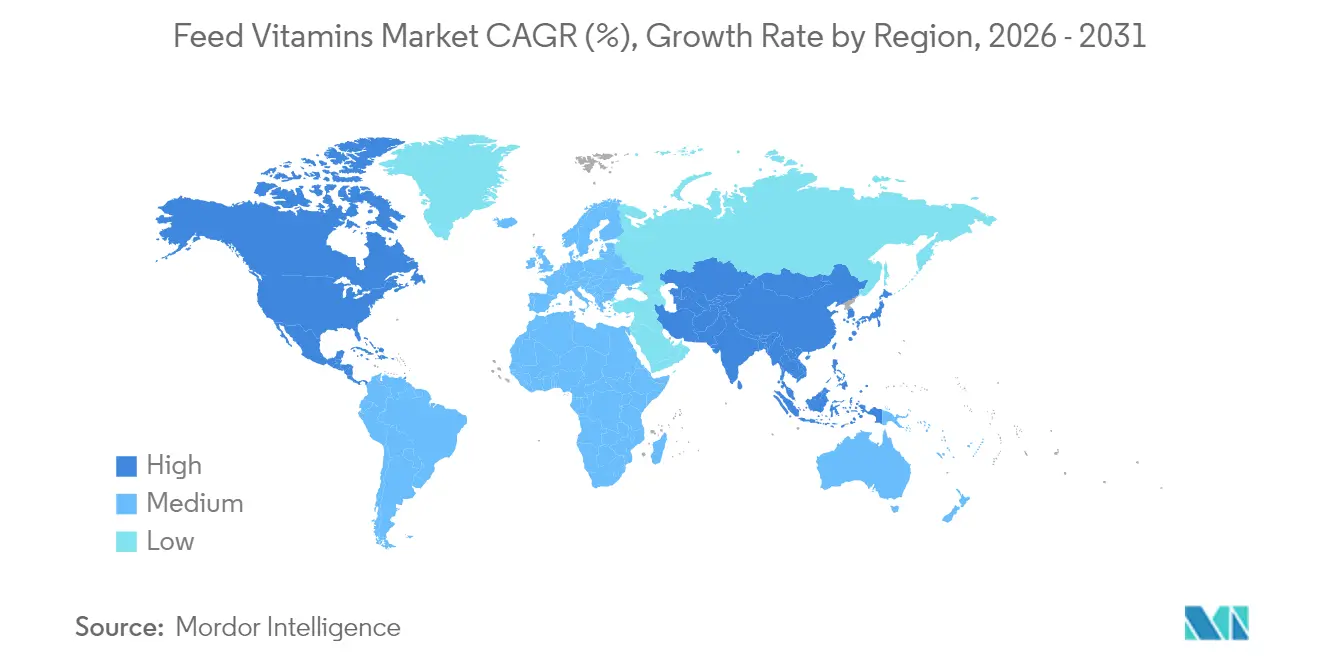

- By geography, Asia-Pacific commanded 31.60% of the feed vitamins market share in 2025, while North America records the highest projected CAGR at 5.05% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Feed Vitamins Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for animal protein and intensified livestock production | +1.2% | Global, strongest in Asia-Pacific and South America | Medium term (2-4 years) |

| Regulatory curbs on antibiotic growth promoters accelerating vitamin inclusion | +0.9% | EU and North America, widening to Asia-Pacific | Long term (≥ 4 years) |

| Advances in encapsulation technologies enhancing vitamin bioavailability | +0.7% | North America and EU, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Expansion of aquaculture requiring water-stable vitamin formulations | +0.6% | Asia-Pacific core, growth in South America and Africa | Long term (≥ 4 years) |

| Precision livestock farming enabling real-time micronutrient dosing optimization | +0.4% | North America and EU, early adoption in Australia | Long term (≥ 4 years) |

| Circular bio-economy valorizing fermentation by-products as vitamin sources | +0.3% | EU and North America, pilot projects in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for animal protein and intensified livestock production

Accelerating meat consumption in populous economies is tightening the performance targets of commercial farms, pushing vitamin inclusion beyond basal requirements. Intensive systems elevate oxidative and metabolic stress, making antioxidants such as Vitamin E indispensable for maintaining feed conversion efficiency. Producers in China and India are mirroring Western precision-nutrition protocols that align vitamin dosing with genetics, age, and ambient temperature. Investment in high-density housing and automated climate control further amplifies vitamin turnover, solidifying sustained demand across the feed vitamins market.

Advances in encapsulation technologies enhancing vitamin bioavailability

Spray-drying, lipid-matrix, and phosphate-stabilized encapsulation platforms are extending shelf life and improving digestive release profiles for sensitive vitamins. Ascorbyl-2-polyphosphate retains 80% potency after six-month storage versus 7% for unprotected ascorbic acid, which is crucial for pelleted aquafeeds that linger in inventory.[1]Source: U.S. Soybean Export Council, “Stable Forms of Vitamin C,” ussec.org Controlled-release coatings also permit lower inclusion rates without performance loss, trimming formulation costs, and mitigating run-off in aquatic environments. Adoption is fastest in North America, where high-temperature extrusion lines risk thermal degradation, reinforcing the region’s status as a technology incubator for the global feed vitamins market.

Expansion of aquaculture requiring water-stable vitamin formulations

Global aquaculture output is anticipated to rise in 2025, and demand for water-stable vitamins is escalating. Fish and shrimp lack endogenous synthesis for several vitamins, making dietary provision essential. BioMar’s 2025 decision to lift vitamin D across all salmon diets underscores the sector’s pivot toward micronutrient optimization. Leaching losses are countered with phosphate-ester derivatives and wax-based coatings that maintain integrity for the first critical minutes in water. Rapid aquaculture adoption, especially in the Asia-Pacific, funnels incremental revenue into the feed vitamins market.

Precision livestock farming enabling real-time micronutrient dosing optimization

Connected sensors, cloud analytics, and automated feeders are blending vitamins into rations based on live weight gain and environmental data. Early deployments in U.S. poultry barns have shown a 5% reduction in feed cost per kilogram of weight gain after implementing IoT-directed vitamin dosing strategies.[2]Source: FME, “Smart Farming Guide,” fme.nl EU dairy herds are following suit with rumen bolus transmitters that track pH and adjust vitamin buffers. Such precision cuts waste, minimizes excretion, and provides transparent audit trails, reinforcing sustainability narratives across the feed vitamins market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price volatility of key vitamin raw materials and intermediates | -0.8% | Global, hardest in price-sensitive markets | Short term (≤ 2 years) |

| Stringent cross-contamination limits raising premix production costs | -0.5% | EU and North America, spreading to Asia-Pacific | Medium term (2-4 years) |

| Photo-degradation of vitamins in transparent feed packaging reducing efficacy | -0.3% | Global, acute in tropical high-UV regions | Medium term (2-4 years) |

| Phytogenic and postbiotic additives cannibalizing vitamin inclusion rates | -0.4% | EU and North America core, early in premium segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High price volatility of key vitamin raw materials and intermediates

A 2024 fire at BASF’s Ludwigshafen site, one of three global vitamin A anchors, triggered a 38% spot-price spike that rippled through premix contracts. Concentrated production in China for vitamin C compounds is exposed to geopolitical or environmental disruptions. Such events compress producer margins and force feed formulators to renegotiate supply agreements, injecting uncertainty into the feed vitamins market.

Phytogenic and postbiotic additives cannibalizing vitamin inclusion rates

Essential oils, saponins, and postbiotic metabolites deliver immune modulation and antioxidant effects that overlap with vitamin functions. Trial results show oregano-based blends improving broiler feed conversion by 2.5%, tempting formulators to trim vitamin overages.[3]Source: MDPI, “Dietary Astaxanthin in Swimming Crabs,” mdpi.com Still, inconsistent efficacy and narrower regulatory definitions constrain full substitution, maintaining a defensive moat around premium vitamin segments within the feed vitamins market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vitamin Type: Vitamin E Steadies Leadership on Antioxidant Necessity

Vitamin E captured 29.05% of the feed vitamins market share in 2025 and advances at a 4.28% CAGR to 2031. Lipid-coated α-tocopherol powders withstand pelleting temperatures above 90 °C, sustaining antioxidant protection from mill to gut. Broiler integrators lift inclusion during pre-slaughter weeks to curb lipid oxidation, extending shelf life and color stability of meat. Swine producers deploy Vitamin E to buffer oxidative stress around weaning, while dairy herds lean on it to mitigate mastitis incidence in high-yield cows. Regulatory curbs on antibiotics underscore Vitamin E’s immune support role, preserving its dominance within the feed vitamins market.

The broader vitamin spectrum stays relevant. Vitamin B complex underpins energy metabolism; Vitamin D3, especially in aquaculture, fortifies skeletal health; Vitamin C’s phosphate-stabilized forms sell at premiums for shrimp rations that demand six-month stability. Vitamin A and K3 serve niche but non-negotiable functions in reproduction and coagulation. Rising specialization invites micro-encapsulated blends that target specific digestive tract sections, reinforcing value capture opportunities across the feed vitamins market.

By Animal: Poultry Systems Anchor Demand While Ruminants Accelerate

Poultry owned 44.65% of the feed vitamins market size in 2025, reflecting quick growth cycles and standardized premix use. Broiler operations intensify Vitamin E deployment for meat quality, whereas layer facilities focus on Vitamin D3 for shell robustness. Turkeys and ducks, though smaller, are adopting customized vitamin matrices as integrators chase uniform carcass grading. Sensor-guided feeders in U.S. houses now modulate vitamin pulses by flock age and barn climate, elevating precision further.

Ruminants grow fastest at 4.48% CAGR through 2031, energized by high-yield dairy cows that require Vitamin A and B variants for fertility and rumen health. Beef feedlots in Brazil add Vitamin E to limit dark-cutting syndrome, protecting carcass premiums. Aquaculture remains a specialized but high-margin slice; water-stable Vitamin C esters justify double-digit price differentials thanks to their 80% six-month potency. Swine demand stays solid amid genetic gains in feed efficiency, while companion and equine segments capture premium prices through chewables and drenches. This multi-species spread cushions cyclical shocks, reinforcing resilience in the feed vitamins market.

Geography Analysis

Asia-Pacific led with 31.60% share in 2025, propelled by China’s aquaculture scale and India’s expanding poultry belt. Exports of carp, tilapia, and shrimp drive vitamin uptake. Farms in Guangdong now stipulate phosphate-stabilized Vitamin C as standard. The region’s regulatory framework tightens; China’s SAMR (State Administration for Market Regulation) added new stability dossier demands in 2025, nudging formulators toward proven encapsulated products. Southeast Asian upstarts in Vietnam and Thailand deepen regional demand, embedding the feed vitamins market across a vast production landscape.

North America tops the growth chart at 5.05% CAGR. U.S. integrators harness IoT sensors that feed dosing algorithms, trimming vitamin wastage yet upping purchase frequency through smaller, fresher lots. Cargill’s September 2024 buyout of two feed mills expanded premix throughput and added logistics nodes that speed deliveries. Canada scales dairy capacity under quota relaxations, while Mexico’s poultry sector intensifies to meet domestic protein needs, channeling additional volume into the feed vitamins market.

Europe holds mature but premium positions, sustained by antibiotic bans and welfare mandates that prioritize dietary antioxidants and immune vitamins. EFSA’s upper-limit reviews catalyze reformulation waves, especially in Germany and the Netherlands where organic labels command price premiums. South America, led by Brazil, gains momentum; ADM’s August 2025 premix plant raises capacity 40%, widening regional supply, from Egypt’s layer mega-farms to Kenya’s smallholder dairies, edge forward, though cold-chain gaps and financing constraints still temper rapid penetration. Collectively, these diverse geographies underpin a broad-based expansion path for the feed vitamins market.

Competitive Landscape

The feed vitamins market shows moderate consolidation. DSM-Firmenich, BASF, and Adisseo hold pivotal synthesis capabilities, controlling large swaths of vitamin A, D3, and E output. BASF’s Ludwigshafen outage in 2024 exposed concentration risk, prompting integrators to dual-source and fuelling spot-market premiums. Regional challengers such as Zhejiang Garden Biochemical are investing in backward integration to secure bile-acid intermediates, reducing dependency on Western suppliers.

Strategic moves revolve around vertical integration and technology differentiation. DSM-Firmenich in June 2025 earmarked impressive gains for an Asia-Pacific longevity nutrition grant, nurturing next-gen vitamin applications. Novonesis and Novo Nordisk’s September 2025 pact on microbiome solutions could yield synergistic offerings blending postbiotics with vitamin matrices.

Technology acts as a wedge. BASF’s Lugavit DX platform couples encapsulated Vitamin D3 with blockchain tracing to authenticate origin, meeting retailer transparency mandates. Adisseo’s SmartLine digital portal lets customers model vitamin overage economics under shifting raw-material prices. Such services heighten switching costs and entrench brand loyalty, reinforcing competitive positions while elevating the sophistication bar for new entrants.

Feed Vitamins Industry Leaders

DSM-Firmenich

Adisseo (Bluestar)

Brenntag SE

ADM

Lonza

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: DSM-Firmenich partnered with Schothorst Feed Research to develop sustainable feed formulation methods. The collaboration focuses on optimizing vitamin inclusion in animal feed to improve nutrient efficiency and reduce environmental impact throughout the livestock production cycle.

- August 2025: Zhejiang NHU increased its feed-grade vitamin E price to USD 13,146.61/metric ton. The company's 40,000 metric tons annual production capacity and this price adjustment influence global vitamin E pricing in the animal nutrition market.

- July 2025: BioMar raised vitamin D inclusion across all salmon diets, underscoring nutrient optimization in aquaculture.

Global Feed Vitamins Market Report Scope

Vitamin A, Vitamin B, Vitamin C, Vitamin E are covered as segments by Sub Additive. Aquaculture, Poultry, Ruminants, Swine are covered as segments by Animal. Africa, Asia-Pacific, Europe, Middle East, North America, South America are covered as segments by Region.Sub Additive

| Vitamin A |

| Vitamin B |

| Vitamin C |

| Vitamin E |

| Other Vitamins |

Animal

| Aquaculture | Fish |

| Shrimp | |

| Other Aquaculture Species | |

| Poultry | Broiler |

| Layer | |

| Other Poultry Birds | |

| Ruminants | Beef Cattle |

| Dairy Cattle | |

| Other Ruminants | |

| Swine | |

| Other Animals |

Geography

| Africa | Egypt |

| Kenya | |

| South Africa | |

| Rest of Africa | |

| Asia-Pacific | Australia |

| China | |

| India | |

| Indonesia | |

| Japan | |

| Philippines | |

| South Korea | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific | |

| Europe | France |

| Germany | |

| Italy | |

| Netherlands | |

| Russia | |

| Spain | |

| Turkey | |

| United Kingdom | |

| Rest of Europe | |

| Middle East | Iran |

| Saudi Arabia | |

| Rest of Middle East | |

| North America | Canada |

| Mexico | |

| United States | |

| Rest of North America | |

| South America | Argentina |

| Brazil | |

| Chile | |

| Rest of South America |

| Sub Additive | Vitamin A | |

| Vitamin B | ||

| Vitamin C | ||

| Vitamin E | ||

| Other Vitamins | ||

| Animal | Aquaculture | Fish |

| Shrimp | ||

| Other Aquaculture Species | ||

| Poultry | Broiler | |

| Layer | ||

| Other Poultry Birds | ||

| Ruminants | Beef Cattle | |

| Dairy Cattle | ||

| Other Ruminants | ||

| Swine | ||

| Other Animals | ||

| Geography | Africa | Egypt |

| Kenya | ||

| South Africa | ||

| Rest of Africa | ||

| Asia-Pacific | Australia | |

| China | ||

| India | ||

| Indonesia | ||

| Japan | ||

| Philippines | ||

| South Korea | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Europe | France | |

| Germany | ||

| Italy | ||

| Netherlands | ||

| Russia | ||

| Spain | ||

| Turkey | ||

| United Kingdom | ||

| Rest of Europe | ||

| Middle East | Iran | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| North America | Canada | |

| Mexico | ||

| United States | ||

| Rest of North America | ||

| South America | Argentina | |

| Brazil | ||

| Chile | ||

| Rest of South America | ||

Market Definition

- FUNCTIONS - For the study, feed additives are considered to be commercially manufactured products that are used to enhance characteristics such as weight gain, feed conversion ratio, and feed intake when fed in appropriate proportions.

- RESELLERS - Companies engaged in reselling feed additives without value addition have been excluded from the market scope, to avoid double counting.

- END CONSUMERS - Compound feed manufacturers are considered to be end-consumers in the market studied. The scope excludes farmers buying feed additives to be used directly as supplements or premixes.

- INTERNAL COMPANY CONSUMPTION - Companies engaged in the production of compound feed as well as the manufacturing of feed additives are part of the study. However, while estimating the market sizes, the internal consumption of feed additives by such companies has been excluded.

| Keyword | Definition |

|---|---|

| Feed additives | Feed additives are products used in animal nutrition for purposes of improving the quality of feed and the quality of food from animal origin, or to improve the animals’ performance and health. |

| Probiotics | Probiotics are microorganisms introduced into the body for their beneficial qualities. (It maintains or restores beneficial bacteria to the gut). |

| Antibiotics | Antibiotic is a drug that is specifically used to inhibit the growth of bacteria. |

| Prebiotics | A non-digestible food ingredient that promotes the growth of beneficial microorganisms in the intestines. |

| Antioxidants | Antioxidants are compounds that inhibit oxidation, a chemical reaction that produces free radicals. |

| Phytogenics | Phytogenics are a group of natural and non-antibiotic growth promoters derived from herbs, spices, essential oils, and oleoresins. |

| Vitamins | Vitamins are organic compounds, which are required for normal growth and maintenance of the body. |

| Metabolism | A chemical process that occurs within a living organism in order to maintain life. |

| Amino acids | Amino acids are the building blocks of proteins and play an important role in metabolic pathways. |

| Enzymes | Enzyme is a substance that acts as a catalyst to bring about a specific biochemical reaction. |

| Anti-microbial resistance | The ability of a microorganism to resist the effects of an antimicrobial agent. |

| Anti-microbial | Destroying or inhibiting the growth of microorganisms. |

| Osmotic balance | It is a process of maintaining salt and water balance across membranes within the body's fluids. |

| Bacteriocin | Bacteriocins are the toxins produced by bacteria to inhibit the growth of similar or closely related bacterial strains. |

| Biohydrogenation | It is a process that occurs in the rumen of an animal in which bacteria convert unsaturated fatty acids (USFA) to saturated fatty acids (SFA). |

| Oxidative rancidity | It is a reaction of fatty acids with oxygen, which generally causes unpleasant odors in animals. To prevent these, antioxidants were added. |

| Mycotoxicosis | Any condition or disease caused by fungal toxins, mainly due to contamination of animal feed with mycotoxins. |

| Mycotoxins | Mycotoxins are toxin compounds that are naturally produced by certain types of molds (fungi). |

| Feed Probiotics | Microbial feed supplements positively affect gastrointestinal microbial balance. |

| Probiotic yeast | Feed yeast (single-cell fungi) and other fungi used as probiotics. |

| Feed enzymes | They are used to supplement digestive enzymes in an animal’s stomach to break down food. Enzymes also ensure that meat and egg production is improved. |

| Mycotoxin detoxifiers | They are used to prevent fungal growth and to stop any harmful mold from being absorbed in the gut and blood. |

| Feed antibiotics | They are used both for the prevention and treatment of diseases but also for rapid growth and development. |

| Feed antioxidants | They are used to protect the deterioration of other feed nutrients in the feed such as fats, vitamins, pigments, and flavoring agents, thus providing nutrient security to the animals. |

| Feed phytogenics | Phytogenics are natural substances, added to livestock feed to promote growth, aid in digestion, and act as anti-microbial agents. |

| Feed vitamins | They are used to maintain the normal physiological function and normal growth and development of animals. |

| Feed flavors and sweetners | These flavors and sweeteners help to mask tastes and odors during changes in additives or medications and make them ideal for animal diets undergoing transition. |

| Feed acidifiers | Animal feed acidifiers are organic acids incorporated into the feed for nutritional or preservative purposes. Acidifiers enhance congestion and microbiological balance in the alimentary and digestive tracts of livestock. |

| Feed minerals | Feed minerals play an important role in the regular dietary requirements of animal feed. |

| Feed binders | Feed binders are the binding agents used in the manufacture of safe animal feed products. It enhances the taste of food and prolongs the storage period of the feed. |

| Key Terms | Abbreviation |

| LSDV | Lumpy Skin Disease Virus |

| ASF | African Swine Fever |

| GPA | Growth Promoter Antibiotics |

| NSP | Non-Starch Polysaccharides |

| PUFA | Polyunsaturated Fatty Acid |

| Afs | Aflatoxins |

| AGP | Antibiotic Growth Promoters |

| FAO | The Food And Agriculture Organization of the United Nations |

| USDA | The United States Department of Agriculture |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms