Cosmetics And Personal Care Store Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

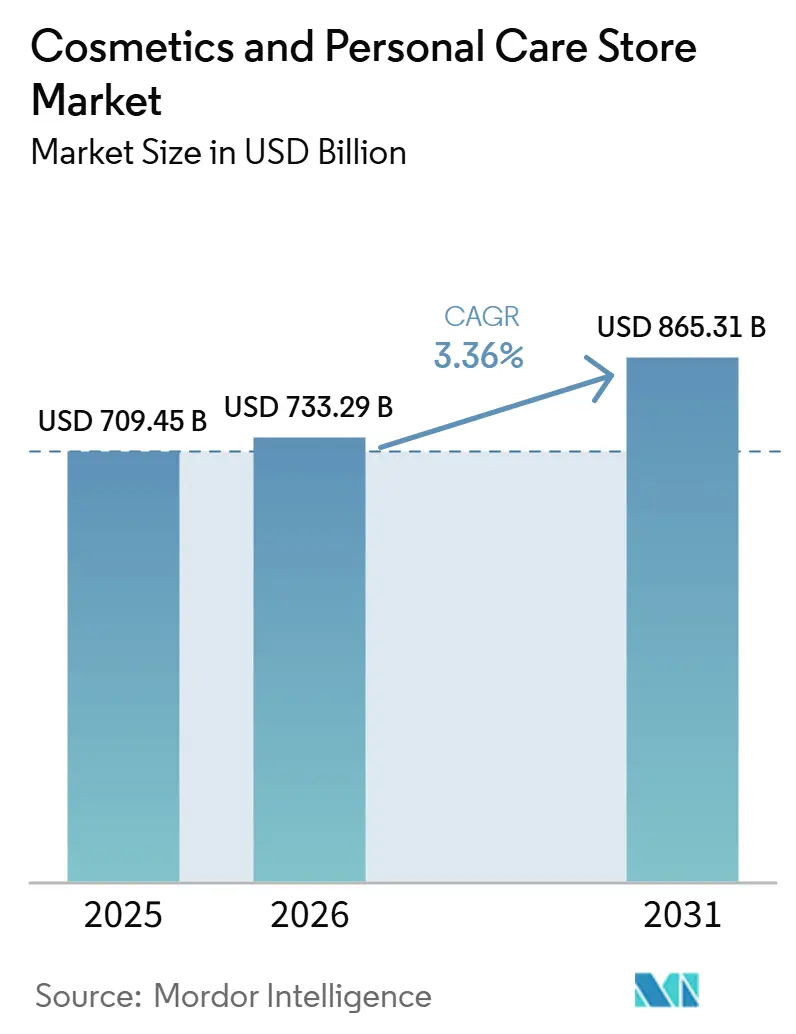

| Market Size (2026) | USD 733.29 Billion |

| Market Size (2031) | USD 865.31 Billion |

| Growth Rate (2026 - 2031) | 3.36% CAGR |

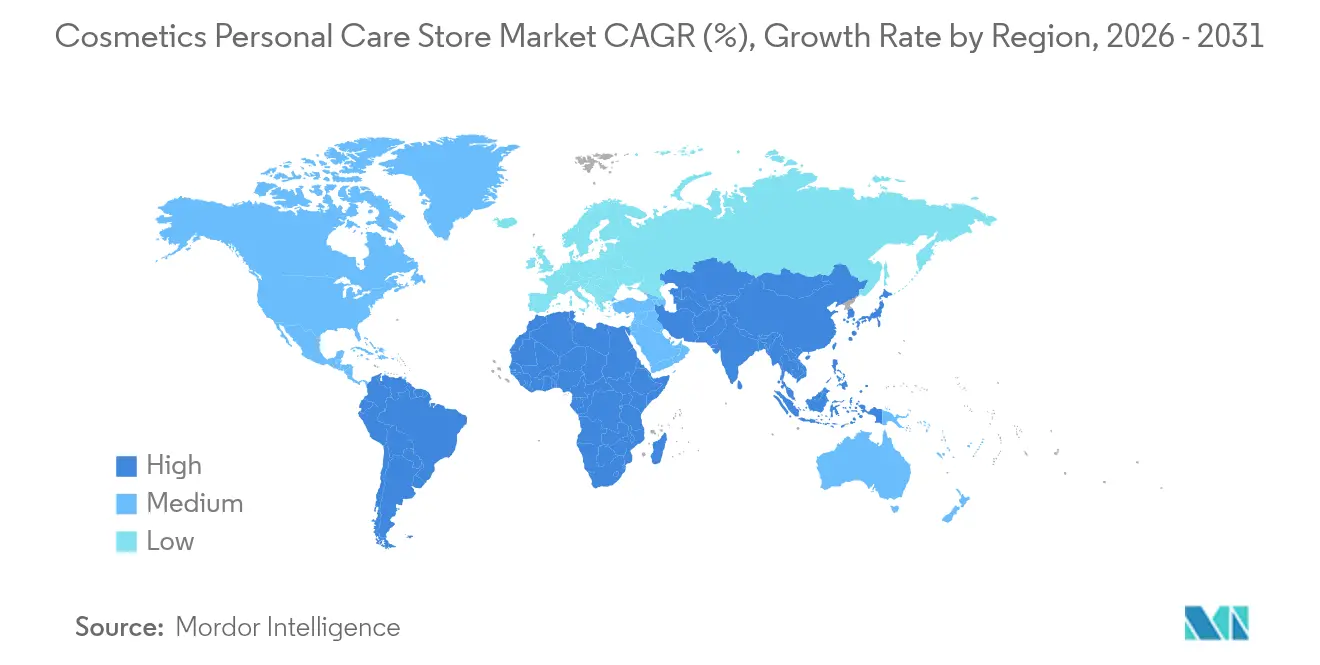

| Fastest Growing Market | Asia Pacific |

| Largest Market | South America |

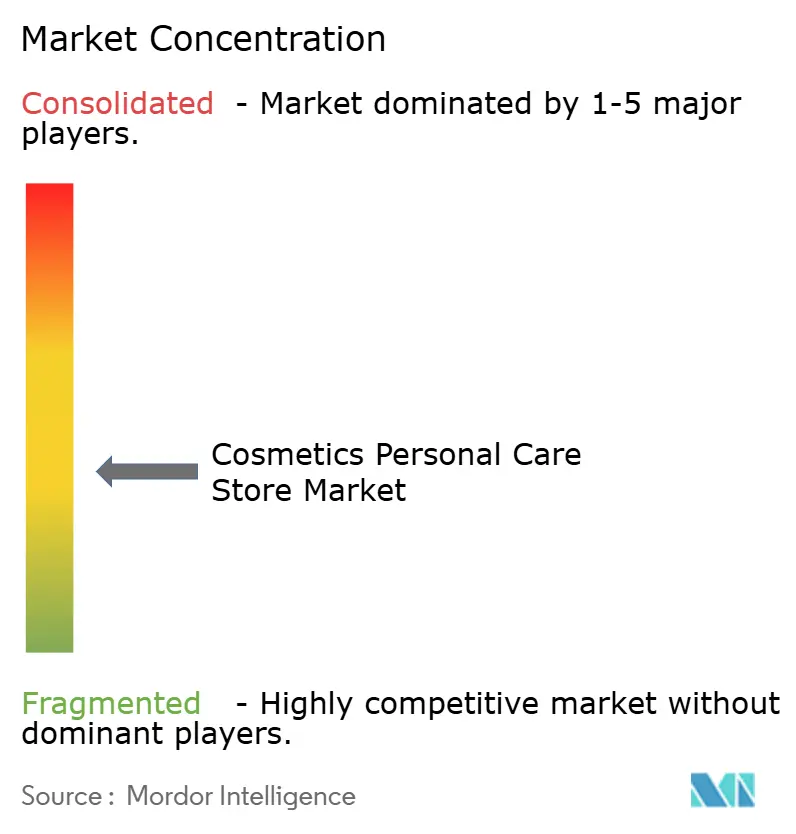

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cosmetics And Personal Care Store Market Analysis by Mordor Intelligence

The Cosmetics And Personal Care Store Market size is expected to grow from USD 709.45 billion in 2025 to USD 733.29 billion in 2026 and is forecast to reach USD 865.31 billion by 2031 at 3.36% CAGR over 2026-2031.

Sustained premiumization in Asia-Pacific, the resurgence of experiential flagships in mature regions, and a steady pivot toward omnichannel retail models underpin growth in the cosmetics and personal care store market. Leading chains rely on AI-based skin diagnostics, augmented-reality mirrors, and data-driven loyalty programs to lift average order values and retention rates, even as online-only challengers intensify pricing pressure. Intensifying regulatory oversight, particularly the Modernization of Cosmetics Regulation Act (MoCRA) in the United States, and proposed amendments to EU Regulation 1223/2009, raise compliance costs, favoring scale players capable of absorbing added testing and labeling requirements. Retailers also confront supply-chain headwinds and inflationary operating expenses; nevertheless, experiential upgrades such as beauty labs and in-store clinics support higher traffic and conversion levels in key urban corridors.

Key Report Takeaways

- By product type, skincare commanded a 31.88% share of the cosmetics and personal care store market in 2025, whereas haircare is projected to grow at a 8.87% CAGR through 2031.

- By distribution channel, supermarket/hypermarket stores led with 37.92% of the cosmetics and personal care store market share in 2025, while pharmacies/drug stores are forecast to expand at a 7.05% CAGR to 2031.

- By store format, flagship beauty stores represented 42.85% of the cosmetics and personal care store market size in 2025, whereas omni-channel concept stores exhibit the fastest trajectory at a 12.55% CAGR through 2031.

- By geography, Asia-Pacific held 37.40% of the global cosmetics and personal care store market share in 2025; South America is on track for a 8.89% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cosmetics And Personal Care Store Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable income in emerging markets | +1.2% | Asia-Pacific, South America | Medium term (2-4 years) |

| Growing demand for natural/organic cosmetics | +0.8% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Proliferation of specialty beauty chains | +0.9% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Omnichannel retail integration | +1.1% | Global | Short term (≤ 2 years) |

| Experiential in-store tech (AR mirrors, diagnostics) | +0.7% | North America, EU, urban APAC | Short term (≤ 2 years) |

| Subscription-based refill & zero-waste stations | +0.6% | Global, led by EU and sustainability-conscious markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Income in Emerging Markets

Middle-class expansion in Asia-Pacific and South America translates to higher per-capita spending on prestige beauty, with Watsons allocating USD 250 million to refurbish 6,000 regional outlets to experiential formats[1]Retail in Asia, “Watsons Invests USD 250 Million in Store Upgrades,” retailinasia.com. . L’Oréal treats Brazil as an “open-air laboratory,” using rapid test-and-learn rollouts to localize products and formats quickly. International brands capitalize on relatively streamlined approval cycles and supportive foreign-investment policies, enabling quicker shelf placement than in mature Western markets. Premiumization is further encouraged by social-media narratives that frame beauty as a marker of self-expression and success. Domestic retailers respond by layering concierge-style services and in-store diagnostics to boost conversion. Currency stabilization in several key markets improves imported product affordability, reinforcing demand for luxury SKUs. Overall, rising purchasing power remains a pivotal tailwind for the cosmetics and personal care store market revenue growth.

Growing Demand for Natural/Organic Cosmetics

Regulators and consumers alike scrutinize ingredient safety, driving retailers to expand clean-beauty assortments and initiate refill or recycling programs. Sephora has broadened its in-store refill stations, while The Body Shop extended its global refill initiative to more than 720 locations in 2024. Transparency mandates under MoCRA and the EU Green Deal raise the bar for documentation, nudging formulators toward plant-derived actives and biodegradable packaging. Specialty retailers position curated organic lines and third-party certifications as differentiators against mass competitors. Price premiums remain resilient because shoppers equate verified natural claims with health benefits and environmental responsibility. These dynamics foster margin-accretive product mixes for retailers able to secure stable, ethically sourced supply chains.

Proliferation of Specialty Beauty Retail Chains

Experiential destinations increasingly replace transactional stores: Mecca’s 4,000 m² Melbourne flagship offers beauty labs, aesthetic suites, and fragrance ateliers to encourage dwell time and higher tickets[2]WWD Editors, “Mecca Opens World’s Biggest Freestanding Beauty Store,” wwd.com. . Watsons’ “Beauty Playground” zones integrate content studios, encouraging social-media sharing and on-site tutorials aimed at Gen Z shoppers. These immersive environments differentiate brick-and-mortar from e-commerce, creating surrounds that online channels cannot replicate. Luxury brands also deploy standalone boutiques that blend spa services with retail, deepening emotional connections and fostering upsell opportunities. High-foot-traffic urban districts justify elevated real-estate costs because dwell-time gains translate into measurable revenue lifts. Retailers back such investments with data showing superior conversion versus legacy department-store concessions. Consequently, specialty chains capture incremental cosmetics and personal care store market size as shoppers trade up for elevated experiences.

Omnichannel Retail Integration in Beauty Sector

AI-enabled skin diagnostics, virtual try-on mirrors, and real-time inventory visibility underpin seamless customer journeys. L’Oréal’s Beauty Genius platform surpassed 100 million global users in 2023, validating consumer appetite for tech-augmented discovery[3]L’Oréal Investor Relations, “2024 Letter to Shareholders,” loreal-finance.com.. Ulta’s multiyear digital-architecture overhaul aims to triple spend among omnichannel users, who already outspend single-channel shoppers by threefold. Click-and-collect and same-day delivery reduce friction, while endless-aisle tools extend SKU breadth without carrying extra store inventory. Data privacy regulations such as GDPR and the California Consumer Privacy Act force retailers to refine consent frameworks, but compliant personalization still improves basket sizes. In emerging markets, mobile-first platforms leapfrog legacy POS systems, allowing rapid adoption of digital services. Collectively, these capabilities expand the cosmetics personal care store market share by intertwining physical and digital touchpoints.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High dependence on discretionary spending cycles | -1.0% | Global, with early impact in North America, South America | Short term (≤ 2 years) |

| Rising competition from direct-to-consumer e-commerce | -0.7% | North America, APAC, EU | Medium term (2-4 years) |

| Stringent cosmetic safety & labeling regulations | -0.6% | EU, North America | Long term (≥ 4 years) |

| Land-use restrictions limiting new brick-and-mortar sites | -0.3% | Urban markets in North America, EU, APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Dependence on Discretionary Spending Cycles

Beauty remains a non-essential category, so economic slowdowns quickly translate into traffic declines and lower average tickets. Bath & Body Works and other mid-tier chains reported softer footfall during inflationary spikes in 2024, prompting heavier promotion calendars. Ulta registered a 1.2% comp-store drop in Q2 2024, forcing management to trim full-year guidance despite later rebounds[4]GCI Magazine Staff, “Ulta Beauty Q2 2024 Results,” gcimagazine.com. . North and South American markets exhibit heightened sensitivity because consumer-confidence indices closely correlate with beauty expenditures. Retailers shelter margins by ramping up own-label ranges, offering bundle deals, and leveraging loyalty points to encourage repeat visits. Credit-card delinquency upticks in some regions signal potential further tightening of discretionary spending. The constraint underscores the importance of diversified geographic footprints and balanced channel mixes for retailers seeking steady cosmetics and personal care store market growth.

Rising Competition from Direct-to-Consumer E-Commerce

Digitally native beauty brands leverage influencer marketing and social-commerce storefronts to bypass traditional retailers, capturing younger cohorts. Glossier and Kylie Cosmetics exemplify how viral product drops translate into rapid revenue without brick-and-mortar overheads. High smartphone penetration and frictionless digital payments in Asia-Pacific and Europe further accelerate DTC adoption. Store-based chains counter by securing exclusive launches and deepening omnichannel loyalty perks that reward cross-channel engagement. In-store events featuring digital-first brands also help redirect traffic back to physical venues. While data-privacy laws may eventually temper hyper-targeted ads, the near-term effect remains traffic erosion for legacy formats. Retailers that cannot offer differentiated experiences risk ceding the cosmetics and personal care store market share to agile DTC entrants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Skincare Dominates, Haircare Accelerates

Skincare held 31.88% of the cosmetics and personal care store market share in 2025 on the strength of science-backed formulations and AI-enabled skin analyses that personalize regimens. Multinationals employ large R&D teams to launch serums, essences, and targeted dermo cosmetic lines that command premium pricing. Younger consumers gravitate toward preventative skin health, sustaining demand for SPF and barrier-repair products. Regulatory scrutiny surrounding ingredients such as parabens and PFAS encourages reformulation and cleaner label positioning in both mass and prestige tiers. Haircare, however, leads future growth at a 8.87% CAGR as scalp-health products and bond-repair treatments ride the “skinification” wave. Clinics and salons integrate diagnostic devices that migrate into retail, translating professional protocols into at-home regimens that lift average unit prices. Retailers dedicate expanded shelf space to trichology-inspired lines, diversifying the cosmetics and personal care store market size across categories.

Skincare’s maturity constrains incremental volume gains, so brands focus on adjacent sub-segments such as skin-microbiome boosters and blue-light protection sprays. In contrast, haircare benefits from under-penetration of premium price points in emerging markets, signaling ample runway for value-per-capita growth. Cross-category bundles pairing facial serums with scalp tonics encourage multi-item baskets and deepen loyalty-program engagement. Ingredient transparency regulations elevate switching costs by making consumers more discerning, thereby reinforcing brand equity for compliant players. At the same time, indie labels use plant-based actives to resonate with clean-beauty enthusiasts, nudging incumbents to accelerate green chemistry roadmaps. Collectively, product-mix shifts and premiumization efforts sustain cosmetics and personal care store market size expansion across both established and nascent categories.

By Distribution Channel: Supermarket/Hypermarket Leads, Pharmacies Surge

Supermarket and hypermarket chains controlled 37.92% of the cosmetics and personal care store market share in 2025 by positioning beauty adjacent to everyday essentials, making them convenient one-stop shops. Aggressive end-cap promotions and private-label rollouts secure price-sensitive shoppers seeking mass brands. Yet growth momentum is strongest in pharmacies and drug stores, forecast to post a 7.05% CAGR as chains like CVS and Walgreens refurbish front-end areas with prestige fixtures and trained beauty advisors. Pharmacist trust elevates perceived product credibility, especially for dermocosmetic lines that straddle healthcare and beauty. These outlets also benefit from cross-sell synergies with wellness categories, encouraging holistic basket building.

E-commerce’s encroachment pushes mass merchants to test mini shops curated by prestige partners, thereby upgrading assortments without overhauling entire footprints. Convenience stores maintain a niche for impulse purchases and travel-size SKUs, yet limited shelf space caps category breadth. Specialist beauty retailers remain crucial launch pads for innovation but face intensifying competition from omnichannel concept stores. Stricter labeling and adverse-event reporting rules disproportionately impact pharmacies, raising operating costs but also heightening consumer confidence. Overall, channel fluidity requires brands to orchestrate distribution strategies that protect price integrity while maximizing the cosmetics personal care store market size potential.

By Store Format: Flagship Stores Dominate, Omni-Channel Concepts Outpace

Flagship outlets delivered 42.85% of the cosmetics and personal care store market size in 2025 by transforming stores into destination playgrounds featuring masterclasses, spa cabins, and fragrance bars. Theatrical product walls and interactive displays encourage social sharing, amplifying organic reach and driving footfall. Capital expenditure is justified by higher dwell times and premium basket composition. Department-store beauty halls continue to anchor luxury brands but confront foot-traffic migration to standalone locations boasting deeper brand immersion. Pop-up and kiosk formats cater to limited-edition launches and seasonal spikes, ensuring tactical visibility in high-traffic zones.

Omni-channel concept stores integrated under strategies such as Watsons’ “O+O” model are forecast to grow at 12.55% CAGR, blending digital shelves, QR-driven tutorials, and click-and-collect counters. These formats capture digitally native consumers who expect fluid transitions between online research and physical testing. Real-time CRM platforms synchronize wish lists, loyalty points, and purchase history across channels, boosting personalization. Sustainability codes and accessibility mandates increasingly shape fit-outs, from energy-efficient lighting to wider aisles. Successful executions see conversion rates outpace legacy formats by double digits, underscoring their role in expanding the cosmetics and personal care store market share.

Geography Analysis

Asia-Pacific retained 37.40% of the cosmetics and personal care store market share in 2025, supported by Watsons’ USD 250 million overhaul of 6,000 stores across 15 markets and Mecca’s regional expansion. Rising disposable income, social-commerce influence, and government policies encouraging foreign direct investment sustain demand for both mass and prestige offerings. Flagship and concept-store counts proliferate in tier-one and tier-two cities where consumer appetite for experiential shopping is strongest. Regulatory frameworks remain supportive, with streamlined licensing in markets such as Thailand and Indonesia accelerating rollout timelines. South America tops the growth chart at a 8.89% CAGR, underpinned by Brazil’s fragrance boom and L’Oréal’s “open-air laboratory” strategy that tests localized SKUs before global release. Mexico attracts attention after Ulta partnered with Grupo Axo to build a multi-store network, broadening prestige accessibility. Economic reforms and expanding middle-class cohorts boost premium-segment volume, albeit currency fluctuations pose earnings-translation risks. Local champions like Natura leverage hybrid offline-online ecosystems to fend off international competition.

North America and Europe collectively exceed 30% of the cosmetics and personal care store market size, but display maturity. The Ulta-Sephora rivalry intensifies as both chains advance omnichannel investments and expand loyalty memberships past 40 million each. Europe grapples with cost pressures stemming from proposed EU ban extensions on PFAS and expanded safety-testing obligations, raising barriers for indie entrants. Nevertheless, refurbished department-store halls and AI-powered diagnostics refresh consumer interest. The Middle East & Africa and Oceania emerge as frontier opportunities. Printemps plans a New York flagship as a springboard for Gulf expansions, while brands such as La Mer invest in Southeast Asian flagships to capture luxury tourism flows. Diverse regulatory regimes require agile compliance capabilities, yet lower saturation levels create white-space potential. Collectively, geographic diversification mitigates macro volatility and unlocks incremental cosmetics personal care store market growth.

Competitive Landscape

The global cosmetics and personal care store market shows moderate concentration, led by a few dominant players shaping its direction. Key brands such as L’Oréal, Estée Lauder, Unilever, Procter & Gamble, and Shiseido continue to influence industry dynamics through strategic acquisitions and restructuring efforts. L’Oréal has strengthened its market leadership through high-profile acquisitions, while Estée Lauder is undergoing a major restructuring to streamline operations and improve profitability over the long term. Unilever has steadily expanded its luxury and dermocosmetics presence, building a focused portfolio through multiple acquisitions. Meanwhile, Procter & Gamble is exploring brand divestitures to concentrate on its most promising growth categories, and Shiseido is investing heavily in travel retail and digital partnerships to recover from pandemic-related slowdowns.

Technology is playing an increasingly critical role in defining success in the cosmetics retail space. Market leaders are deploying AI-driven personalization engines, enhancing customer experiences through virtual beauty assistants, personalized regimens, and streamlined digital interactions. Retailers like Ulta and Sephora are also overhauling their digital infrastructure to enable seamless omnichannel shopping, with capabilities like real-time inventory visibility, one-click checkout, and mobile-first loyalty programs. These innovations not only enhance convenience but also deepen customer engagement across both physical and digital touchpoints. As a result, companies that effectively integrate tech into their retail strategies are gaining a competitive edge.

At the same time, regulatory pressures and rising operational costs are reshaping the playing field. Larger brands are better equipped to absorb new compliance requirements, such as product testing mandates and documentation updates, in global markets. These puts added pressure on smaller players that lack the scale or infrastructure to meet these demands efficiently. The rise of private-label products in supermarkets and drugstores is also intensifying price competition, especially in mass-market segments. However, established brands continue to defend their market positions by leveraging strong R&D capabilities, product innovation, and brand heritage, all of which remain essential for standing out in an increasingly crowded and fast-evolving market.

Cosmetics And Personal Care Store Industry Leaders

L’Oréal Group

Estée Lauder Companies

Unilever (Beauty & Personal Care Division

Procter & Gamble (Beauty Segment)

Shiseido

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Mecca unveiled the world's largest freestanding beauty store in Melbourne, spanning 4,000 square meters and offering a full suite of experiential services.

- July 2025: L’Oréal has reportedly been interested only in acquiring Armani’s beauty business, not the full fashion house, reflecting a strategy focused on expanding its cosmetics portfolio rather than diversifying into non-beauty luxury sectors.

- July 2025: The EU has proposed updates to its Cosmetics Regulation (EC) No 1223/2009 to streamline safety, labeling, and ingredient rules. Key changes include faster approval of new ingredients, clearer processes for CMR substances, removing pre-notification for nanomaterials, and reducing duplicate reporting obligations.

- September 2024: La Mer has opened its first flagship store in Bangkok, Thailand, embracing the ‘Essence of the Sea’ theme to reflect its signature ingredient, Miracle Broth. The store includes a Spa de La Mer with facial treatment rooms and an esthetician, plus a gifting corner offering branded luxury packaging.

Global Cosmetics And Personal Care Store Market Report Scope

The cosmetics and personal care stores provide customers with cosmetic products that are used for cleaning, improving, or changing the complexion, skin, hair, nails, or teeth. The Cosmetics and Personal Care Stores Market is Segmented By Product Types (Decorative, Skincare, Haircare, Perfume, Oral Care, Bath and Shower), By Distribution Channels (Specialist Retail Stores, Supermarkets/Hypermarkets, Convenience Stores, Pharmacies/Drug Stores), and By Geography (North America, Europe, Asia-Pacific, South America, The Middle East, And Africa). The Report Offers Market Size and Forecasts for Cosmetics and Personal Care Stores in Volume and Value (USD) for All the Above Segments.

| Decorative |

| Skincare |

| Haircare |

| Perfume |

| Oral-Care |

| Bath & Shower |

| Specialist Retail Stores |

| Supermarket / Hypermarket |

| Convenience Stores |

| Pharmacies / Drug Stores |

| Flagship Beauty Stores |

| Department Store Beauty Halls |

| Pop-Up / Kiosk Stores |

| Omni-channel Concept Stores |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Product Type | Decorative | |

| Skincare | ||

| Haircare | ||

| Perfume | ||

| Oral-Care | ||

| Bath & Shower | ||

| By Distribution Channel | Specialist Retail Stores | |

| Supermarket / Hypermarket | ||

| Convenience Stores | ||

| Pharmacies / Drug Stores | ||

| By Store Format | Flagship Beauty Stores | |

| Department Store Beauty Halls | ||

| Pop-Up / Kiosk Stores | ||

| Omni-channel Concept Stores | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What was the cosmetics personal care store market size in 2026?

It reached USD 733.29 billion, with a projected rise to USD 865.31 billion by 2031 at a 3.36% CAGR.

Which region controls the largest share of cosmetics personal care store sales?

Asia-Pacific led with 37.40% of global revenue in 2025.

Which product segment is growing fastest in brick-and-mortar beauty retail?

Haircare is forecast to grow at a 8.87% CAGR through 2031, outpacing skincare.

Why are pharmacies gaining ground as a beauty channel?

Trust in healthcare professionals, coupled with refurbished beauty zones, is driving a 7.05% CAGR for pharmacy sales.

How does omnichannel strategy boost store performance?

Customers shopping both online and offline spend roughly triple compared with single-channel users, lifting overall revenue.

Which store format shows the highest growth potential?

Omni-channel concept stores are projected to expand at a 12.55% CAGR due to seamless digital-physical integration.

Page last updated on: