Modern Trade Retail Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.75 Trillion |

| Market Size (2031) | USD 7.01 Trillion |

| Growth Rate (2026 - 2031) | 4.05% CAGR |

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

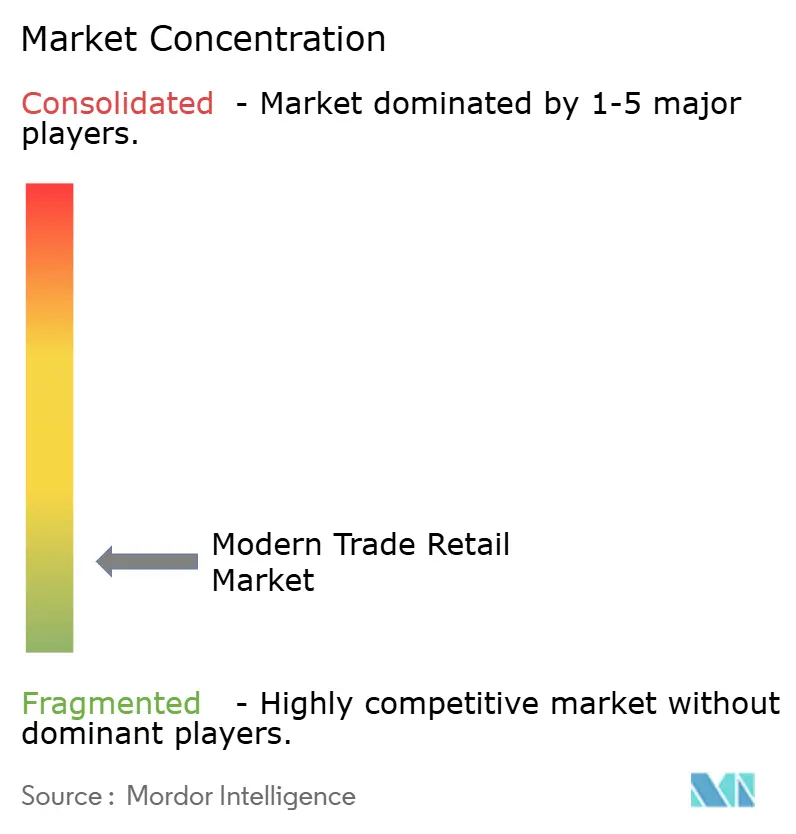

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Modern Trade Retail Market Analysis by Mordor Intelligence

The modern trade retail market size is expected to grow from USD 5.53 trillion in 2025 to USD 5.75 trillion in 2026 and is forecast to reach USD 7.01 trillion by 2031 at 4.05% CAGR over 2026-2031. Current expansion builds on resilient household spending, faster urbanization, and the sector-wide shift to omnichannel business models that blend physical stores with digital engagement. Investments in artificial intelligence for inventory planning and dynamic pricing widen gross margins even as price competition continues. Asia-Pacific remains the demand anchor, supported by large middle-class populations and improving logistics networks, while Africa delivers the fastest growth as supermarket penetration accelerates. Retailers prioritize private-label programs, automated fulfillment, and regional consolidation to capture margin upside and defend share against pure-play e-commerce rivals.

Key Report Takeaways

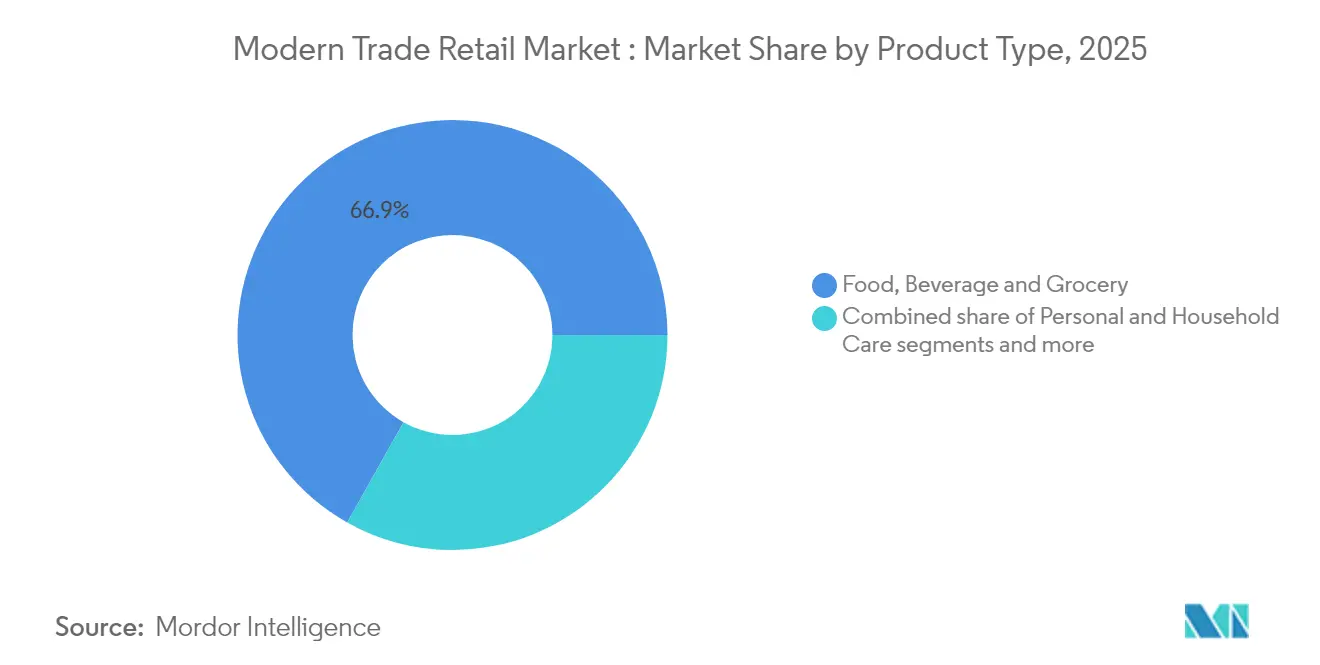

- By product type, food, beverage & grocery led with 66.85% of modern trade retail market share in 2025; toys, hobby & appliances is projected to record a 12.74% CAGR through 2031.

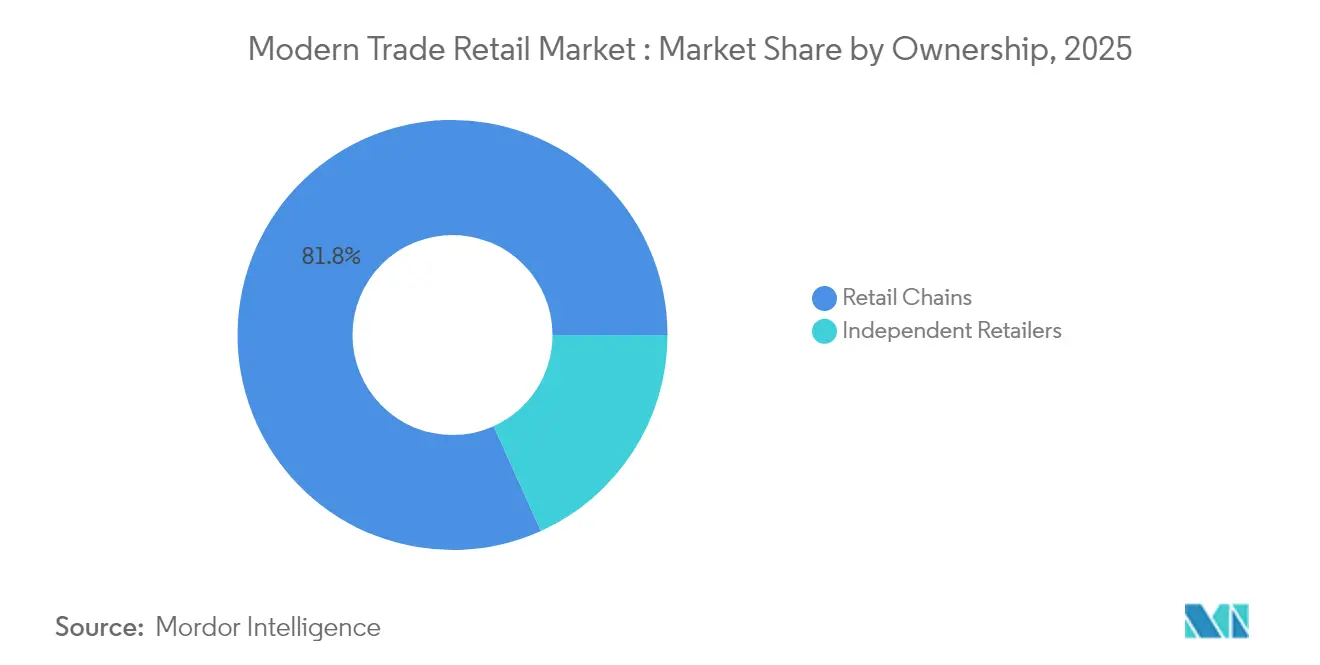

- By ownership, retail chains controlled 81.75% of the modern trade retail market size in 2025, while independent retailers are advancing at a 9.96% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets accounted for 54.12% of the modern trade retail market size in 2025, and online channels are expanding at a 13.88% CAGR through 2031.

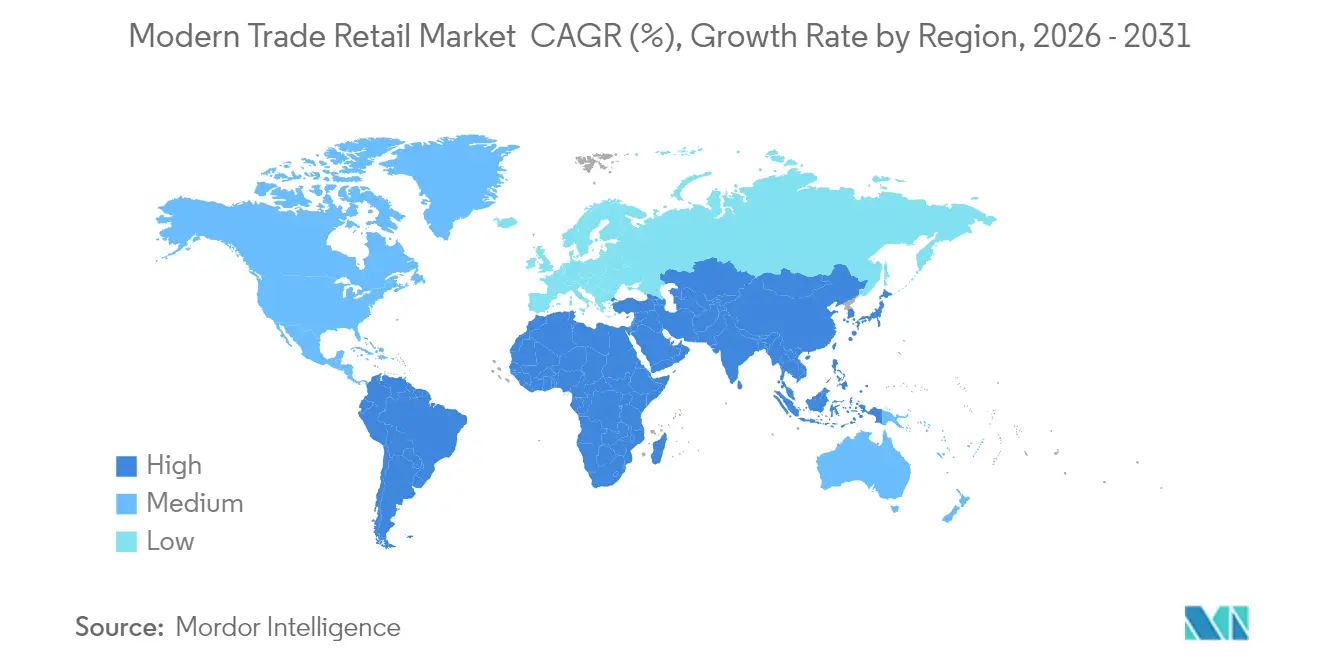

- By geography, Asia-Pacific captured 37.10% of the modern trade retail market share in 2025and Africa is forecast to expand at a 12.03% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Modern Trade Retail Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising urban middle-class disposable income | +1.2% | APAC core, spill-over to MEA and South America | Medium term (2-4 years) |

| Proliferation of private-label brands | +0.8% | Global, with strongest impact in North America & Europe | Long term (≥ 4 years) |

| Omnichannel retail & click-and-collect expansion | +0.9% | Global, early gains in North America, Europe, urban APAC | Short term (≤ 2 years) |

| Under-penetrated tier-2/3 city supermarkets in Asia & Africa | +1.1% | APAC and MEA focused, limited North America relevance | Long term (≥ 4 years) |

| AI-driven dynamic pricing & inventory forecasting | +0.6% | Global, with faster adoption in developed markets | Medium term (2-4 years) |

| Sustainability-led demand for traceable supply chains | +0.4% | Europe and North America leading, spreading globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Urban Middle-Class Disposable Income

Urban household income expansion in emerging markets creates a multiplier effect beyond simple basket size increases, fundamentally altering category mix toward higher-margin discretionary goods. In India, urban households with annual incomes above USD 10,000 are projected to grow from 31 million in 2024 to 100 million by 2030, driving demand for premium private-label products and imported goods that carry 15-25% higher margins than commodity categories. This demographic shift enables retailers to justify investments in store format upgrades and technology infrastructure that were previously uneconomical in price-sensitive markets. The income elasticity of retail spending in tier-2 and tier-3 cities often exceeds 1.5, meaning a 10% income increase translates to 15% higher retail spending, creating sustainable growth momentum independent of overall economic cycles.

Proliferation of Private-Label Brands

Private-label penetration has evolved from a defensive margin strategy to an offensive differentiation tool, with leading retailers achieving 25-40% of total sales from own-brand products that generate gross margins 20-30 percentage points higher than national brands. Walmart's private-label sales exceeded USD 100 billion in 2024, representing nearly 25% of its total revenue and demonstrating the scale advantages available to large format retailers[1]Walmart Inc., “2024 Annual Report,” Walmart.com.. The strategic shift involves moving beyond commodity categories into premium segments, with retailers launching organic, sustainable, and health-focused private-label lines that command price premiums while maintaining superior margins. This trend accelerates as supply chain transparency requirements under regulations like the EU's Corporate Sustainability Due Diligence Directive enable retailers to better control product provenance and quality narratives.

Omnichannel Retail & Click-and-Collect Expansion

Click-and-collect services have matured from pandemic necessity to permanent competitive advantage, with adoption rates reaching 60-70% among frequent shoppers in developed markets and driving 15-20% increases in average order values. The operational efficiency gains are substantial: retailers report 40-50% lower fulfillment costs for click-and-collect orders compared to home delivery, while simultaneously increasing store footfall and cross-selling opportunities. IKEA's expansion of click-and-collect points to 200+ locations across major markets demonstrates how furniture and home goods retailers are leveraging this model to serve customers without full-scale store investments. The technology infrastructure required, including inventory visibility systems and mobile payment integration, creates barriers to entry that favor established players with existing store networks and IT capabilities.

Under-Penetrated Tier-2/3 City Supermarkets in Asia & Africa

Modern trade penetration in smaller cities across Asia and Africa remains below 20% compared to 60-80% in major metropolitan areas, representing a USD 200-300 billion addressable market opportunity through 2030. Reliance Retail's expansion into 200+ tier-2 and tier-3 Indian cities since 2024 illustrates the scalable economics: lower real estate costs, reduced competition, and higher customer loyalty offset smaller initial basket sizes[2]Reliance Industries, “Annual Report 2023-24,” Ril.com. . The infrastructure development required cold chain logistics, payment system integration, and local supplier networks creates first-mover advantages that can sustain market leadership for decades. African markets show particularly strong potential, with supermarket penetration below 15% in most countries outside South Africa, while urbanization rates exceed 4% annually in key markets like Nigeria and Kenya.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying price wars compress margins | -0.7% | Global, most acute in mature North American and European markets | Short term (≤ 2 years) |

| Supply-chain disruptions from geopolitical risks | -0.5% | Global, with highest impact on import-dependent regions | Medium term (2-4 years) |

| Pure-play e-commerce competition reduces footfall | -0.6% | Developed markets primarily, spreading to urban emerging markets | Long term (≥ 4 years) |

| High CapEx for store automation & digitalisation | -0.3% | Global, constraining smaller regional players disproportionately | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intensifying Price Wars Compress Gross Margins

Retail price competition reached unprecedented intensity in 2024, with major chains reducing prices on thousands of items simultaneously, creating a deflationary spiral that compressed industry-wide gross margins by 50-100 basis points Wall Street Journal. Walmart's aggressive pricing on 7,000+ items, matched by Target's price cuts across grocery and household essentials, demonstrates how scale advantages in procurement and logistics become weapons in market share battles. The margin pressure is most acute in commodity categories where differentiation is limited, forcing retailers to accelerate private-label development and premium category expansion to maintain profitability. Smaller regional chains face existential pressure as they lack the procurement scale to match price reductions while maintaining viable operating margins.

Supply-Chain Disruptions from Geopolitical Risks

Global supply chain disruptions surged 38-40% in 2024, with geopolitical tensions, trade policy uncertainty, and regional conflicts creating persistent inventory and cost pressures across retail categories. The Red Sea shipping crisis alone added 10-15 days to delivery times and increased container costs by 200-300%, forcing retailers to maintain higher safety stock levels that tie up working capital and reduce inventory turnover efficiency. Retailers are responding through supply chain regionalization and near-shoring strategies, but these transitions require 2-3 years to implement fully and often involve 10-20% higher procurement costs during the transition period. The complexity is compounded by sustainability compliance requirements that limit supplier flexibility and increase due diligence costs across global supply networks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Essential Staples Sustain Scale While Discretionary Categories Drive Margin

Food, Beverage & Grocery retained the highest 2025 modern trade retail market share at 66.85%, reflecting daily consumption and cross-category basket anchoring. Toys, Hobby & Appliances, however, is forecast to deliver a 12.74% CAGR through 2031, buoyed by smart-home upgrades and gaming adoption. The mix shift supports gross-margin expansion, offsetting thin margins in staples. Retailers bundle loyalty rewards and financing options to encourage high-ticket upgrades, while category seasonality drives targeted promotions that stabilize quarterly revenue flows. In parallel, Personal & Household Care sees steady demand as consumers prioritize wellness and hygiene. Apparel, Footwear & Accessories face stiffer online rivalry, prompting in-store assortment curation and fast-replenishment cycles. Furniture & Home Décor benefits from hybrid work patterns that spur home improvement spending, yet remain sensitive to macro lending conditions. Balanced category portfolios give chains resilience, leveraging grocery foot traffic to upsell discretionary items and diversify the modern trade retail market revenue base.

By Ownership: Scale Consolidation Meets Independent Agility

Chains commanded 81.75% of the modern trade retail market size in 2025, capitalizing on centralized purchasing, data-rich loyalty ecosystems, and technology investments. Independents counter with localized assortments, community engagement, and rapid decision cycles, achieving a 9.96% CAGR that outpaces the broader market. Franchise partnerships and buying cooperatives allow smaller operators to tap shared logistics and marketing platforms without ceding local authenticity, preserving diversity across competitive landscapes. Cost escalation in sustainability reporting and digital infrastructure favors consolidation, yet regulatory scrutiny over market dominance restrains unchecked mergers. Successful operators balance scale and flexibility: regional chains deploy modular store formats that adapt to neighborhood demographics, while large groups create incubator programs for niche concepts, blending entrepreneurial speed with enterprise resources.

By Distribution Channel: Physical Stores Transform Into Fulfillment Engines

Supermarkets and hypermarkets accounted for 54.12% of 2025 sales, yet now act as omnichannel nodes, supporting online order pick-ups, same-day delivery dispatches, and returns processing. This hybrid model enhances asset utilization and customer convenience, sustaining the modern trade retail market relevance of large-format outlets. Online channels’ 13.88% CAGR, driven largely by traditional retailers’ digital extensions rather than stand-alone e-commerce entrants, underscores convergence rather than substitution. Specialty stores safeguard market share through curated assortments and expert service, doubling down on experiential merchandising to justify in-person visits. Convenience stores exploit immediate-need missions and extended hours, while warehouse clubs secure loyalty through bulk value offerings and membership ecosystems. Channel pluralism under a unified brand umbrella delivers seamless engagement, ensuring shoppers remain within the retailer’s ecosystem regardless of the journey start point.

Geography Analysis

Asia-Pacific held 37.10% of global revenue in 2025, underpinned by China’s broad store network and India’s rapid rollout of tier-2/3 supermarkets, where modern trade retail penetration is still under 25%. Investments in cold-chain logistics and digital payments unlock rural and peri-urban demand, cementing the region’s centrality to future volume growth. High smartphone penetration enables scan-and-go checkouts and hyper-localized promotions that elevate shopper engagement.

Africa offers the fastest trajectory at a 12.03% CAGR to 2031, driven by the continent’s young demographic, rising disposable income, and infrastructure upgrades that reduce distribution bottlenecks. Nigeria, Kenya, and Egypt record double-digit store rollouts, while mobile-money ecosystems simplify cash-flow management for both retailers and consumers. Supply chain volatility and regulatory heterogeneity remain operational hurdles, but first movers secure strategic sites and supplier relationships that underpin long-term scale. North America and Europe post mature yet profitable growth at 3.29% and 2.61% CAGR, respectively. Operators focus on AI-enabled demand forecasting, localized assortment, and sustainability compliance to protect margins in tight labor markets. Omni-fulfillment innovations, including curbside pickup and micro-fulfillment robotics, originate here and later diffuse to emerging regions. South America grows at a 4.96% CAGR, with performance tempered by macroeconomic swings and currency fluctuation risk.

Competitive Landscape

In 2024, the global modern trade retail market remains highly fragmented, with the top five players, Walmart, Carrefour, Schwarz Gruppe, Costco, and Tesco, holding a relatively modest share of total revenue. This fragmentation leaves room for regional challengers to scale and compete. Major global retailers are investing heavily in advanced technologies such as AI-powered demand forecasting, warehouse automation, and retail media networks that monetize loyalty data through targeted advertising. Walmart’s acquisition of a smart-TV brand broadens its connected-screen advertising capabilities, while Carrefour is experimenting with autonomous store pods to offer 24/7 service in dense urban areas. These innovations reflect a shift toward omnichannel integration and data monetization as key growth drivers. As global players pursue tech-enabled differentiation, they also reinforce their dominance through capital-intensive strategies that smaller competitors struggle to match.

Regional retailers are responding by consolidating to boost their competitiveness and improve operational efficiency. In the U.S., a notable merger between a major wholesaler and a mid-sized grocer in 2024 exemplified efforts to gain cross-channel advantages and supply chain synergies. Private equity activity has intensified, highlighted by the acquisition of a pharmacy-retail chain focused on integrating healthcare services more rapidly. Meanwhile, new entrants are testing asset-light models like dark stores in underserved regions such as Latin America and Africa. While innovative, these models face challenges related to high fulfillment costs and limited profitability without broader scale partnerships. As a result, sustainability for many start-ups depends on either rapid expansion or collaboration with larger platforms.

Technology adoption continues to define the competitive landscape across all tiers of retail. AI-powered pricing tools now allow dynamic adjustments in near real time, helping retailers lift gross margins by several percentage points in pilot locations. Back-of-house automation is also delivering results, reducing shrinkage and improving shelf availability, which in turn drives higher sales. The most successful retailers are those that unify physical locations, data systems, and fulfillment infrastructure under a single strategic framework. This alignment creates powerful advantages that are difficult for less integrated players to replicate. As technology and data become central to execution, firms with cohesive digital strategies build more defensible market positions. The modern trade landscape is increasingly shaped by those who can effectively merge innovation with scale.

Modern Trade Retail Industry Leaders

Walmart Inc.

Carrefour S.A.

Schwarz Gruppe (Lidl, Kaufland)

Costco Wholesale Corp.

Tesco PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Walmart announces expansion of 150+ stores over 5 years with 650 store remodels planned for 2025, representing the company's largest physical expansion since the 1990s and signaling renewed confidence in brick-and-mortar retail's omnichannel role. The investment includes technology upgrades and format optimization to support click-and-collect services and micro-fulfillment capabilities.

- December 2024: Walgreens Boots Alliance agrees to USD 23.7 billion take-private acquisition by Sycamore Partners, marking one of the largest retail sector buyouts and reflecting private equity confidence in pharmacy-retail format optimization potential. The transaction enables operational restructuring without public market quarterly earnings pressures.

- November 2024: Mars completes USD 36 billion acquisition of Kellanova, creating the world's largest snacking company and demonstrating food manufacturers' vertical integration strategies to capture retail margin and control distribution channels. The deal reshapes supplier-retailer power dynamics in packaged goods categories.

- October 2024: C&S Wholesale acquires SpartanNash for USD 1.77 billion, consolidating grocery distribution and wholesale operations across multiple regional markets. The merger creates operational synergies and enhanced negotiating power with national brand suppliers.

Global Modern Trade Retail Market Report Scope

The modern trade retail market refers to the segment of the retail industry that includes supermarkets, hypermarkets, department stores, and other organized retail formats. The modern trade retail market is segmented by product type, ownership, distribution channel, and geography. By product type, the market is segmented into food, beverage, and grocery, personal and household care, apparel, footwear, and accessories, furniture and home décor, toys, hobby, and household appliances, and pharmaceuticals. By ownership, the market is segmented into retail chains and independent retailers. By distribution channel, the market is segmented into supermarkets/hypermarkets, specialty stores, online, and others (convenience stores and department stores). By geography, the market is segmented into North America, Europe, Asia Pacific, South America, and the Middle East and Africa. The report offers market size and forecasts for the modern trade retail market in value (USD) for all the above segments.

| Food, Beverage, and Grocery |

| Personal and Household Care |

| Apparel, Footwear, and Accessories |

| Furniture and Home Decor |

| Toys, Hobby, & Household Appliances |

| Others |

| Retail Chains |

| Independent Retailers |

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online |

| Other Distribution Channels |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX | |

| NORDICS | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type | Food, Beverage, and Grocery | |

| Personal and Household Care | ||

| Apparel, Footwear, and Accessories | ||

| Furniture and Home Decor | ||

| Toys, Hobby, & Household Appliances | ||

| Others | ||

| By Ownership | Retail Chains | |

| Independent Retailers | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX | ||

| NORDICS | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the modern trade retail market in 2026?

The modern trade retail market size stands at USD 5.75 trillion in 2026 and is projected to reach USD 7.01 trillion by 2031 at a 4.05% CAGR.

Which region leads modern trade retail revenue?

Asia-Pacific commands 37.10% of global revenue because of large urban populations and rapid supply-chain modernization.

What category is growing fastest through 2031?

Toys, Hobby & Appliances is set to expand at a 12.74% CAGR due to rising discretionary spending on smart-home and gaming products.

Why are private-label products important?

Private-label penetration delivers margins 20–30 percentage points higher than national brands, helping retailers offset price-war pressures.

How are supermarkets adapting to e-commerce growth?

Supermarkets increasingly operate as omnichannel hubs, offering click-and-collect and micro-fulfillment services that cut last-mile costs by up to 40%.

Page last updated on: